Why Hardware Startups Are More Vulnerable During Conflict

March 19, 2026 by Harshit Gupta

The axiom that "hardware is hard" has historically served as a shorthand for the multi-dimensional challenges of physical product development, encompassing rigorous engineering cycles, significant capital requirements, and the unforgiving nature of manufacturing physics. However, in the contemporary era of heightened global instability, this difficulty has transcended the technical and entered the geopolitical. While software startups possess an inherent fluidity—capable of iterating code in real-time, pivoting business models with minimal sunk costs, and deploying on cloud infrastructure that is largely abstracted from physical geography—hardware startups are fundamentally tethered to the "world of atoms". This physical anchoring creates a unique and profound set of vulnerabilities when regional or global conflicts erupt. These vulnerabilities are not merely incidental but are structural, stemming from the geographic concentration of specialized supply chains, the fragility of maritime logistics, and the extreme capital intensity of manufacturing processes that are highly sensitive to inflationary shocks and material scarcities.

The Structural Rigidity of Physical Development Cycles

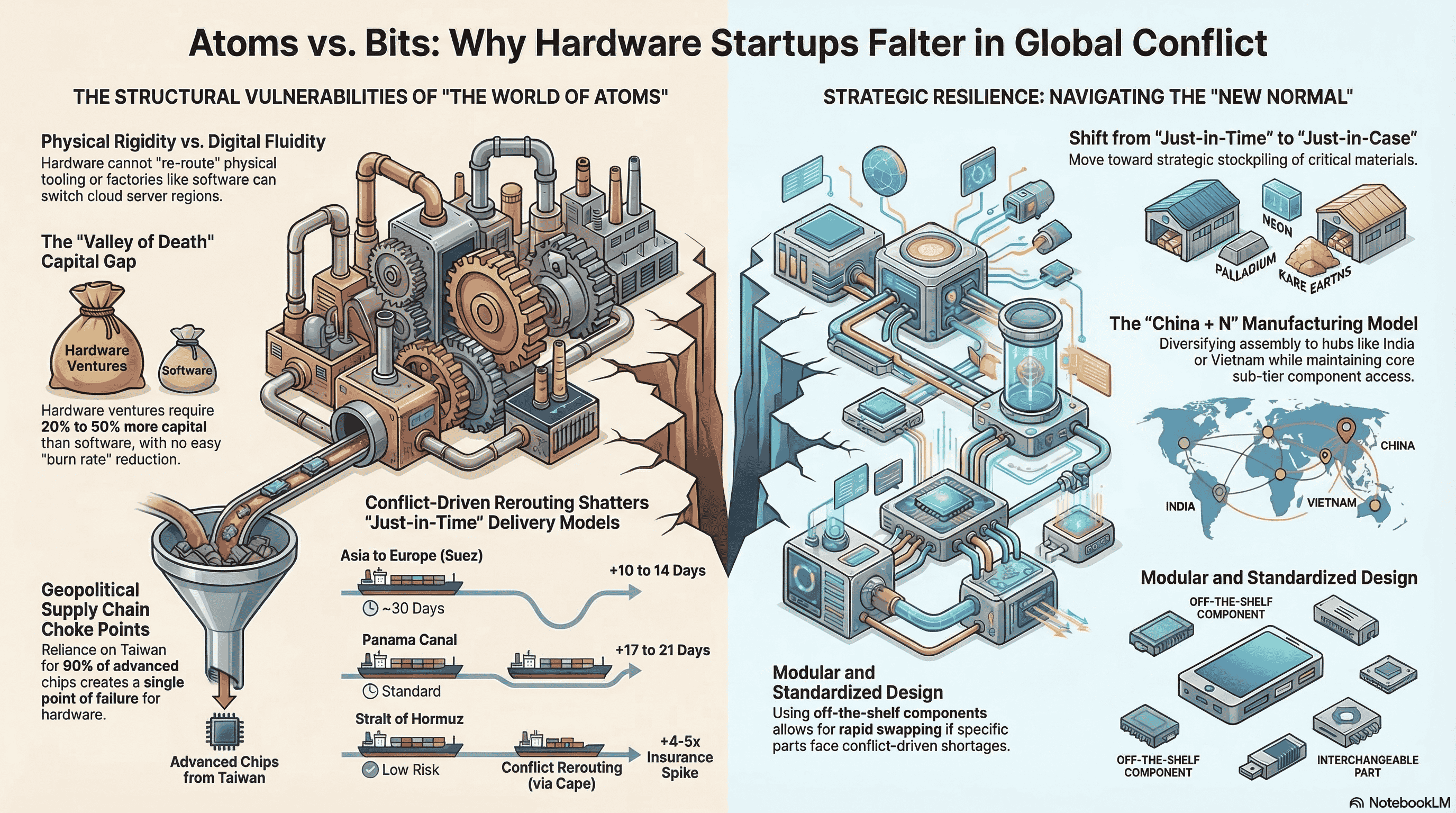

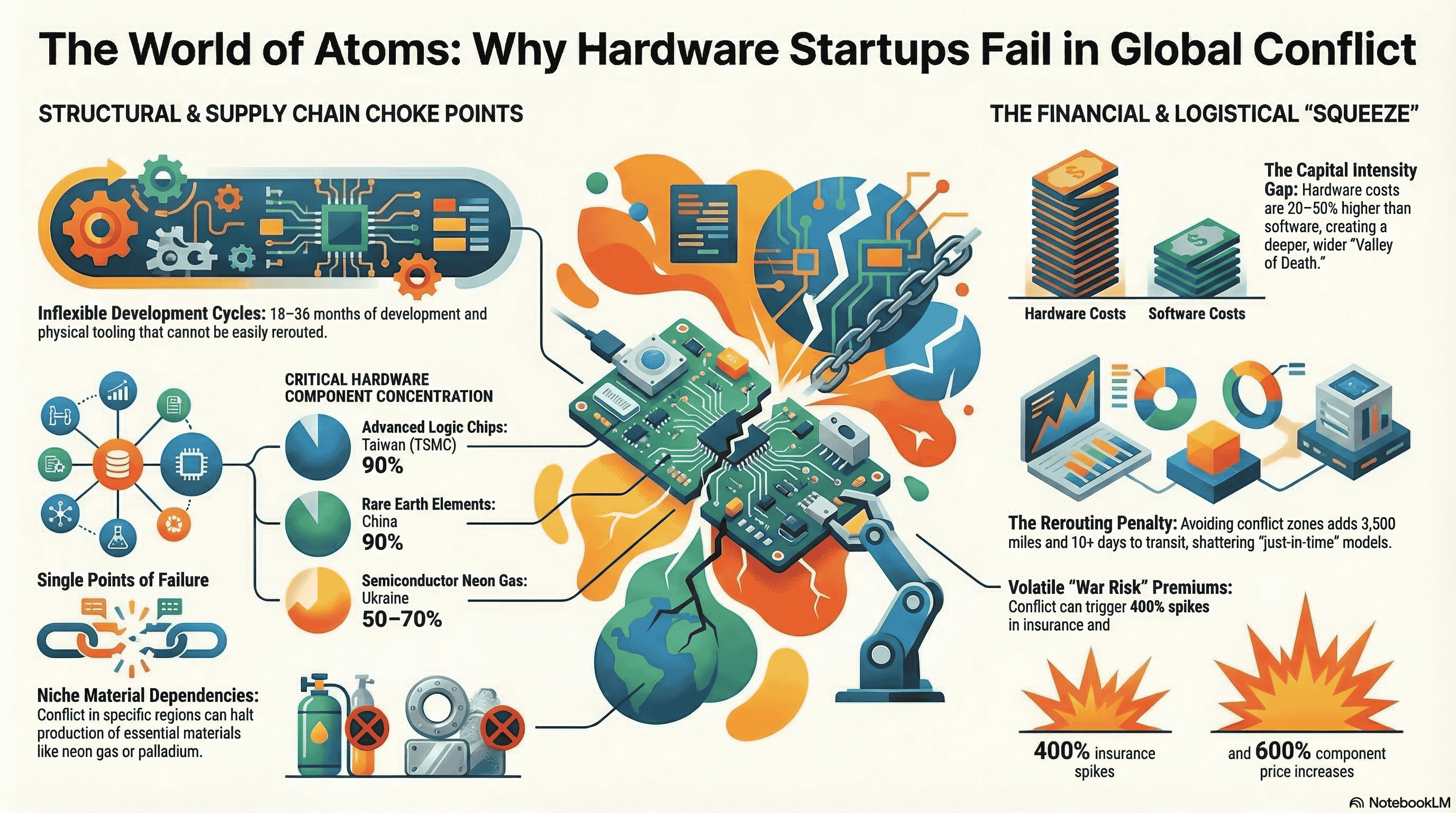

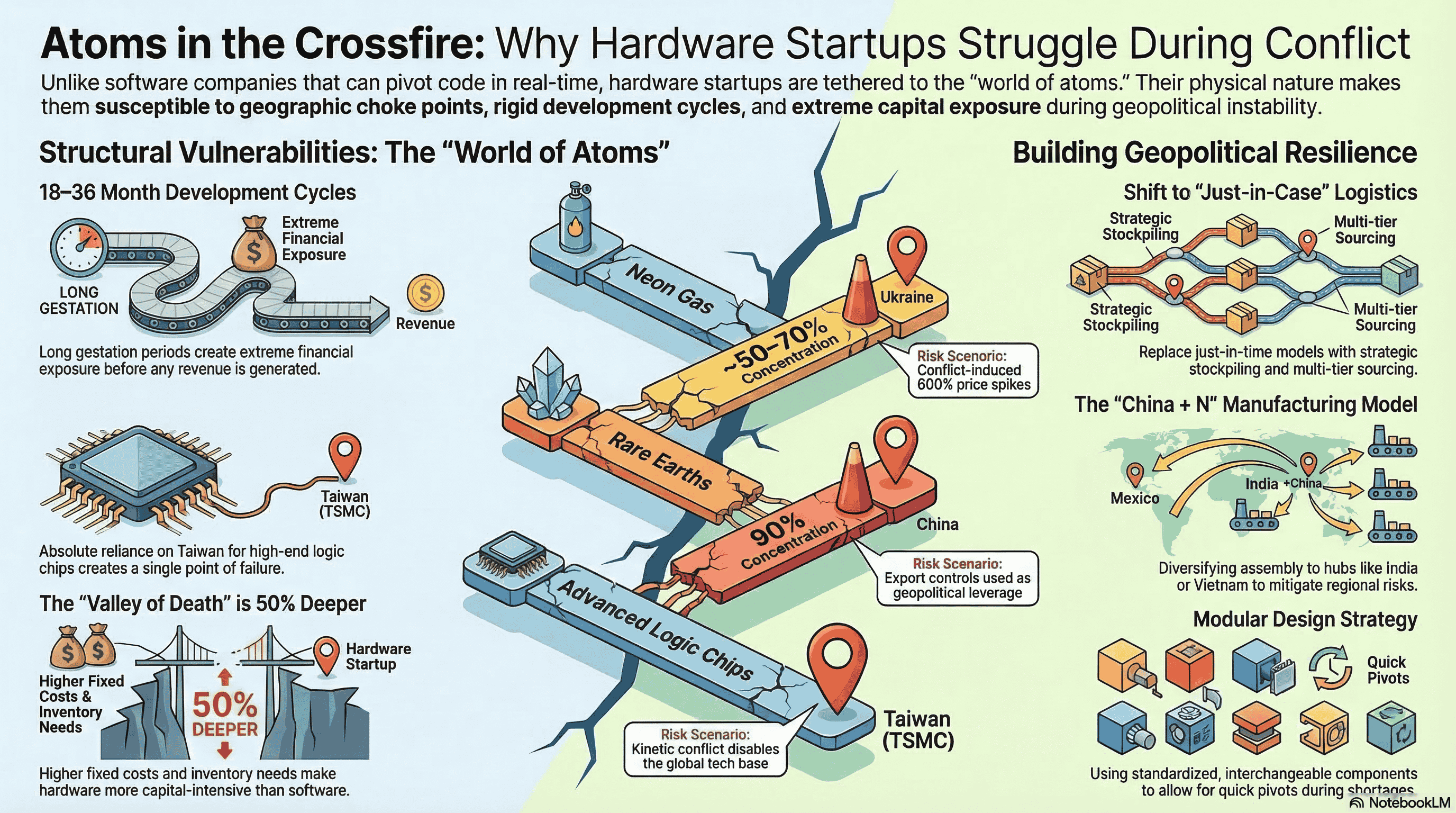

The primary vulnerability of hardware startups during conflict is rooted in the inherent rigidity of their development and manufacturing cycles. Unlike software Minimum Viable Products (MVPs), which can be deployed in weeks, hardware requires a long gestation period involving custom printed circuit board (PCB) design, prototyping, regulatory testing, and the creation of specialized tooling for mechanical enclosures. These phases are not only time-consuming but are also geographically dependent. When a conflict disrupts a specific region, a hardware startup cannot easily "re-route" its physical tooling or its specialized manufacturing partners in the same way a software firm might switch server regions.

The development timeline for a hardware product often stretches across 18 to 36 months before reaching market readiness. During this period, the startup is in a state of extreme financial exposure, having invested heavily in research and development (R&D) and pre-production without generating significant revenue. A conflict-induced delay of even a few months can be fatal. For instance, the regulatory landscape—including CE, FCC, or RoHS certifications—acts as a mandatory gate for global market entry. Conflicts can shut down testing laboratories or delay the delivery of pre-compliance modules, effectively blocking a startup's path to market.

Development Phase | Hardware Requirement | Vulnerability During Conflict | Impact on Startup |

Prototyping | Custom PCBs and specialized components | Supply chain interruptions for niche parts | Delays in functional validation |

Tooling/Mold Making | Precision machining for injection molding | Closure of specialized factories in conflict zones | High sunk costs and inability to pivot |

Certification | Testing for CE, FCC, RoHS compliance | Shutdown of labs or disruption of global standards | Blocked market entry and legal risk |

Pilot Production | Manufacturing coordination and assembly | Logistics bottlenecks and labor shortages | Missed launch windows and cash depletion |

The "Valley of Death" and Capital Intensity

The capital intensity of hardware ventures is approximately 20% to 50% higher than that of software startups, a figure that nearly doubles when accounting for non-dilutive funding and the lack of traditional venture capital (VC) support for early-stage manufacturing. Hardware startups must maintain high liquidity to manage the bill of materials (BOM), inventory, and shipping costs. In a conflict environment, macroeconomic pressures such as rising interest rates and inflation exacerbate this strain.

The "Valley of Death"—the period between initial funding and sustainable revenue—is both wider and deeper for hardware firms. While a software startup might survive a temporary funding slowdown by reducing its "burn rate" (primarily headcount), a hardware startup is often locked into fixed costs related to manufacturing agreements and inventory procurement. If a conflict causes a spike in component prices, such as the 600% increase in Random Access Memory (RAM) witnessed in early 2026, a startup's unit economics can be destroyed overnight. Small manufacturers are particularly vulnerable to being "priced out" of the market as larger entities with greater negotiating power secure the remaining supply.

Supply Chain Fragility and Geographic Choke Points

Hardware startups are uniquely susceptible to "choke points"—systemically significant bottlenecks along the technology stack that can be exploited for geopolitical leverage. The global technology ecosystem is a geographically distributed web of materials, manufacturing, and design expertise. However, certain nodes in this web have become so concentrated that they represent single points of failure for the entire industry.

The Semiconductor Dependence: Taiwan as a Single Point of Failure

The concentration of semiconductor manufacturing in Taiwan is perhaps the most acute vulnerability for the global hardware sector. Taiwan produces over 60% of the world's semiconductors and a staggering 90% of the most advanced logic chips (7nm, 5nm, 3nm). For a hardware startup building products in the Artificial Intelligence (AI), autonomous systems, or high-performance computing sectors, reliance on the Taiwan Semiconductor Manufacturing Company (TSMC) is "absolute and non-negotiable".

Any kinetic conflict in the Taiwan Strait would have catastrophic consequences. Analysts suggest that a major disruption to the Taiwanese semiconductor base could set the global economy back "at least 20 years". For a startup, the loss of access to advanced chips does not just mean higher prices; it means the total inability to manufacture their product. While giants like Apple or Samsung have begun to decrease their overall Taiwanese supplier exposure, their reliance on TSMC for cutting-edge silicon remains a structural vulnerability that cannot be mitigated in the short term.

Category | Component/Material | Leading Global Source | Market Concentration | Risk Scenario |

Raw Material | Neon Gas (Semiconductor grade) | Ukraine (Ingas, Cryoin) | ~50–70% | Conflict halts production; 600% price spike |

Rare Earths | Rare Earth Elements (REM) | China | >90% | Export controls used as geopolitical leverage |

Manufacturing | Advanced Logic Chips (<7nm) | Taiwan (TSMC) | >90% | Kinetic conflict disables global tech base |

Processing | Back-end ATP (Assembly/Test) | Malaysia | 13% | Regional instability affects helium/energy |

Raw Material Scarcity: The Neon and Palladium Case Studies

The Russia-Ukraine war has provided a vivid demonstration of how niche material dependencies can derail the hardware industry. Ukraine produces approximately 54% to 70% of the world’s semiconductor-grade neon gas, which is essential for the deep-ultraviolet (DUV) lithography used in chip manufacturing. Neon is a byproduct of older types of steel plants that have been phased out elsewhere, making the supply highly concentrated in the region. When the 2022 invasion forced companies like Ingas and Cryoin to halt operations, the global chip shortage was immediately exacerbated, causing production delays across the automotive and medical device sectors.

Similarly, Russia produces 35% to 45% of the world's palladium supply, a metal used in semiconductor packaging and sensor production. Hardware startups, lacking the deep inventory buffers and diverse sourcing networks of multinational corporations, are the first to suffer when these materials are hit by sanctions or regional blockades. While larger firms can invest in neon recycling technologies or secure multi-tier sourcing agreements, startups often lack the capital and technical expertise to implement such mitigation strategies.

Maritime Logistics and the Rerouting Penalty

Hardware startups must move physical goods across vast distances, making them highly sensitive to disruptions in maritime trade routes. Conflict in key maritime corridors, such as the Red Sea, the Strait of Hormuz, or the Bashi Channel, can sever the arteries of a hardware company's operations.

Rerouting and Transit Delays

The Red Sea is a critical link in global trade, accounting for 12% of global trade volume and 30% of global container shipping. Since late 2023, attacks on commercial vessels have forced shipping lines to abandon the Suez Canal in favor of the Cape of Good Hope. This rerouting adds approximately 3,000 to 3,500 nautical miles to a journey between Asia and Europe, resulting in at least 10 extra days of transit time.

For a hardware startup, these delays have ripple effects throughout the business. Just-in-time (JIT) delivery models, which startups use to conserve cash, are shattered by unpredictable transit times. Longer routes also require more fuel and resources, leading to higher shipping costs and increased carbon footprints. It is estimated that these disruptions can reduce corporate profits by as much as 40% and contribute significantly to global inflation.

Shipping Route | Normal Transit (Asia to Europe) | Conflict Rerouting (via Cape) | Impact on Costs/Time |

Suez Canal / Red Sea | ~30 Days | Rerouted around Africa | +10 to 14 Days |

Panama Canal | Standard transit | Drought + Rerouting | +17 to 21 Days |

Strait of Hormuz | 20% of seaborne oil | Risk of total closure | 4-5x Insurance spike |

The "Perfect Storm" of Freight Costs

By mid-2024, the Shanghai Containerized Freight Index (SCFI) had more than doubled compared to late 2023 levels. These skyrocketing rates represent a "perfect storm" for hardware startups. Unlike software companies, which have negligible distribution costs, hardware firms must absorb the rising costs of fuel, insurance, and labor associated with shipping. Furthermore, when shipments finally reach ports, they often face "demurrage and storage" costs due to congestion caused by disrupted schedules.

The sharp rise in freight rates is projected to increase global consumer prices by 0.6% by 2025 as shipping costs filter through supply chains. For a startup competing on price, these additional costs can be the difference between a viable product and a market failure.

The Insurance Crisis and the Geopolitical Barometer

Insurance premiums serve as a real-time geopolitical barometer, reflecting the risk level of different geographic regions. For hardware startups, the cost of insuring physical assets—both in transit and in storage—can become prohibitively expensive during times of conflict.

War Risk Premiums and Capacity Shrinkage

Following hostilities in the Persian Gulf in early 2026, war risk premiums for transiting the Strait of Hormuz surged four to five times within days. For vessels with a perceived American, British, or Israeli nexus, premiums increased even more dramatically. In some cases, maritime insurers have withdrawn war risk coverage entirely for certain conflict zones, forcing startups to "self-insure" or absorb catastrophic risk onto their balance sheets.

Global insured losses from political violence and war risks soared to an estimated $6 billion recently. This has led insurers to rewrite policy language, aggressively expanding war exclusion clauses to cover state-backed cyberattacks and supply chain contagion. A hardware startup relying on a critical component from a factory in a volatile region may find that its "all-risk" policy no longer covers losses arising from regional hostilities or cyber-physical attacks on infrastructure.

The Impact on Unit Economics

The increase in insurance premiums directly impacts a startup's unit economics. For a transit through a high-risk zone, rates have reached between 1.5% and 3% of the hull value—levels not seen since the 1980s. When applied to cargo, these premiums can increase by more than 1,000%. For a hardware startup operating on thin margins, these costs cannot be easily passed on to consumers without losing market share.

Insurance Type | Pre-Conflict Baseline | Conflict Impact (2024–2026) | Corporate Response |

War Risk (Marine) | Nominal | 200–400% Spike | Search for specialized covers |

Marine Cargo | ~$22.6B Global Market | +1.6% (Standard) / +1000% (High Risk) | Revaluation of CIF models |

Political Violence | Standard Inclusion | Widespread Exclusions | Investment in "resilience" assets |

Cyber (State-backed) | Emerging | Carve-outs for state actors | Hardening of operational tech |

Venture Capital Redirection and the "Geopolitical Discount"

Geopolitical conflict fundamentally alters the behavior of investors, creating a challenging environment for hardware startups that do not have direct strategic relevance to national security.

The Sovereign Pivot in Private Markets

The escalation of hostilities in early 2026 triggered a "Sovereign Pivot" in the venture capital landscape. Capital is no longer flowing mainly toward consumer demand or discretionary software. Instead, it is being redirected toward technologies tied to sovereign security and industrial resilience. Defense technology, once a niche category, has become a central investment thesis, with median pre-money valuations for defense-tech startups reaching approximately $115 million in 2025.

This shift is driven by the pull of "guaranteed demand." Procurement signals from governments—such as the U.S. proposal for $1.5 trillion in defense spending—act as a powerful catalyst for private investment. For investors, multi-year replenishment cycles for missiles, drones, and autonomous systems reduce the uncertainty that typically plagues hardware ventures.

The Funding Gap for Non-Strategic Hardware

Outside of the defense and strategic sectors, hardware startups face a much grimmer reality. Early-stage startups without strategic relevance are experiencing stretched deal timelines, stricter due diligence, and declining valuations. In regions like the Middle East (MENA), international investors—who historically provide 44% of late-stage capital—have become more selective and cautious.

This "geopolitical discount" means that even mature startups looking for liquidity or exit opportunities may find their valuations depressed by the perceived risk of regional instability. For a hardware startup that requires significant capital to scale its manufacturing, this funding gap can be an existential threat.

Manufacturing Recalibration: The "China+N" Model and Its Risks

For decades, China served as the undisputed hub for hardware manufacturing. However, persistent geopolitical tensions, rising labor costs, and the vulnerabilities exposed by the pandemic have forced a "great recalibration" of the global manufacturing network.

The Complexity of Diversification

Hardware startups are increasingly adopting a "China+N" manufacturing model, where they maintain some operations in China while diversifying assembly to other Asian hubs like India, Vietnam, Thailand, or Malaysia. While this strategy aims to improve resilience, it introduces new complexities and costs.

The move away from the efficiency of the Chinese ecosystem results in a "resilience premium"—higher corporate operational costs due to fragmented supply chains and strained infrastructure in emerging hubs. Furthermore, even when final assembly moves to "N" locations, many crucial sub-tier components (e.g., printed circuit boards and specialized materials) still overwhelmingly originate in China. This creates a "dilemma of continued interdependence" where a conflict involving China would still paralyze a company that has ostensibly moved its manufacturing elsewhere.

Hub Specialization and New Vulnerabilities

Each of the emerging manufacturing hubs has developed its own set of specializations and, consequently, its own set of vulnerabilities.

India: Has become a central production hub for high-volume smartphone assembly (e.g., Apple and Samsung). However, it remains dependent on the import of mundane discrete components and specialized materials.

Vietnam: A key production center for complex products like laptops and smartphones. It is central to the diversification strategies of Dell and Samsung but faces challenges related to infrastructure and regional tensions in the South China Sea.

Malaysia: Solidifying its position in back-end processes like assembly, testing, and packaging (ATP), accounting for 13% of global operations. However, the industry is vulnerable to disruptions in helium and energy supplies caused by conflict in the Middle East.

Hub Region | Primary Specialization | Growth Rate (Suppliers) | Geopolitical Risk Profile |

India | Smartphone Assembly | +85% (2019–2024) | Border tensions; reliance on sub-tier China parts |

Vietnam | Laptops/Complex Electronics | +96% (2019–2024) | South China Sea volatility; infrastructure strain |

Malaysia | Back-end ATP / Semiconductors | +50% (2019–2024) | Vulnerable to Middle East energy/helium shocks |

Taiwan | Leading-edge Fabrication | Indispensable | "Single point of failure" for the entire world |

The Legal and Contractual Battlefield

Conflict doesn't just disrupt the flow of atoms; it also tests the integrity of the legal agreements that hold the hardware supply chain together. Hardware startups often find themselves in disadvantageous positions when facing sudden cost spikes or delivery failures.

Inadequate Price Adjustment Mechanisms

Many hardware supply agreements are based on fixed-price models that do not account for the extreme volatility of a conflict environment. When the price of a critical component like RAM increases by 600% in a single year, manufacturers face a "solvency and fulfillment risk". Smaller manufacturers, in particular, may be priced out of their own contracts, leading to defaults that ripple through the supply chain.

To mitigate these risks, firms are increasingly incorporating "extraordinary cost-sharing" provisions and "market-based pricing triggers". For example, a contract might specify that if component costs increase by more than 20%, the supplier and customer will split the additional expense. However, implementing such changes requires negotiating power that many early-stage startups simply do not have.

Force Majeure and Hardship Challenges

Under English law, which governs many international trade contracts, "Force Majeure" is typically construed narrowly. Making performance "merely more expensive" is usually insufficient to trigger relief. This places a heavy burden on startups to prove that a conflict event rendered performance "impossible" rather than just "less profitable".

"Hardship" clauses, which require good-faith renegotiation when performance becomes "materially more burdensome," offer some protection, but courts are often reluctant to imply a duty to renegotiate if it is not explicitly stated in the contract. This legal rigidity makes hardware startups more vulnerable to the financial shocks of conflict than their more flexible software counterparts.

The Human Element: Talent Migration and Labor Vulnerability

Hardware startups require a diverse team of specialized engineers, including those in electrical, mechanical, and industrial design. Conflict can suddenly displace this talent or make it impossible for teams to collaborate.

Brain Drain and Mobilization

In regions experiencing kinetic conflict, such as Israel or Ukraine, the mobilization of military reserves can decimate a startup's engineering team overnight. Hardware development, which often requires physical presence in labs or factories for testing and prototyping, is more severely affected by these disruptions than software development, which can more easily shift to a remote-work model.

Furthermore, the "brain drain" associated with regional instability can lead to a long-term loss of technical expertise. For countries like Malaysia, which already faces a shortage of engineering graduates (5,000 annually against an industry demand of 50,000), any further loss of talent due to regional tensions can impede the growth of the entire sector.

The Impact of "Zero-COVID" and Regional Lockdowns

The pandemic-era lockdowns in China served as a dry run for the kind of labor disruptions that occur during conflict. "Zero-COVID" policies led to sudden factory closures and logistical chaos, exposing the dangers of over-concentration in a single geographic region. For hardware startups, these closures meant missed production cycles and the loss of critical momentum in competitive markets.

Cybersecurity and the Modern Conflict Landscape

In the modern era, conflict is not limited to physical battlefields; it extends into digital and infrastructure networks. Hardware startups are increasingly vulnerable to "non-kinetic" state activity.

Infrastructure and Supply Chain Cyberattacks

Cloud infrastructure, which supports the design and logistics of hardware products, is now a direct target for state-level adversaries. Jurisdictional risk—where cloud providers are subject to conflicting legal obligations due to geopolitical pressure—can jeopardize a startup's data and operations.

Moreover, cyberattacks on critical infrastructure (e.g., power grids, fiber-optic cables, and port systems) can halt the physical production and shipping of hardware products. A factory may remain physically untouched, but a "hostile cyber act" that halts its operational technology can be just as devastating as a missile strike. Hardware startups, often lacking the robust cybersecurity budgets of larger firms, are particularly vulnerable to these "contagion" effects.

The Role of AI in Conflict and Resilience

As conflict accelerates the adoption of AI, hardware startups in the AI-infrastructure space face both opportunities and risks. Defense demand for autonomous systems and AI-driven logistics can provide a "strategic turning point" for hardware companies, offering new revenue streams and accelerating adoption cycles.

However, this intersection also raises ethical and regulatory questions about the boundaries between commercial innovation and military use. Hardware developers may find themselves subject to new "supply chain risk designations" that can harm their competitiveness or restrict their ability to work with international partners.

Strategic Resilience: Navigating the "New Normal"

In a world where geopolitical conflict is a persistent threat, hardware startups must move beyond traditional risk management toward a posture of "resilience as a balance-sheet asset".

Moving Toward "Just-in-Case" Models

The lessons of the 2024–2026 conflict period have forced a shift from the efficient "just-in-time" model to a "just-in-case" model. This includes:

Strategic Stockpiling: Maintaining inventory buffers of critical components and materials (e.g., neon, palladium, and rare earths) to weather short-term disruptions.

Multi-Tier Sourcing: Establishing relationships with multiple suppliers at different geographic levels to reduce the risk of a single point of failure.

Modular Design: Using standardized, off-the-shelf components that can be easily interchanged if a specific part faces a conflict-driven shortage.

Financial Preparedness and the Role of the Virtual CFO

Founders and startup leaders must understand "wartime economics". This involves strategic modeling and cash management that accounts for extreme volatility in costs and supply chains. Virtual CFOs (VCFOs) are becoming crucial for hardware startups, helping them interpret macroeconomic signals, redesign financial models, and strengthen liquidity to transform geopolitical uncertainty into strategic advantage.

The sensitivity of a hardware startup's unit economics to energy price shocks, often a byproduct of Middle East conflict, can be modeled using LaTeX notation:

If Cunit represents the unit cost and Penergy represents the energy price index, the impact of a conflict-induced energy spike on production costs can be estimated as:

ΔCunit=i=1∑n(∂Li∂Cunit⋅ΔLi)+β⋅ΔPenergy

Where Li represents logistical costs and β is a coefficient representing the energy-intensity of the manufacturing process. This mathematical reality underscores why hardware firms are more vulnerable to the macro-financial squeeze of conflict than software-as-a-service (SaaS) companies.

Conclusion: The New Paradigm for the Hardware Sector

The analysis of the global landscape from 2024 to 2026 demonstrates that hardware startups are fundamentally more vulnerable during conflict due to their inescapable ties to physical geography and material resources. The "world of atoms" is subject to blockades, price shocks, and physical destruction in a way that the "world of bits" is not.

The most successful hardware companies of the next decade will be those that embrace "geopolitical necessity" as a central design principle. This requires a proactive approach to risk, moving away from a reliance on single-hub efficiency toward a fragmented but resilient global network. For the hardware startup, survival in an era of conflict depends on its ability to build "geopolitical moats"—technologies and supply chains that are not only indispensable but also diversified and strategically aligned with the requirements of a volatile global order.

While "hardware is hard," the geopolitical reality of the 2020s has made it a matter of strategic endurance. Those who can navigate the complexities of manufacturing in a fractured world—balancing the "China+N" reality with the necessity of advanced silicon from Taiwan and raw materials from Eastern Europe—will be the architects of the next industrial age. The fragility of atoms, once understood, becomes the foundation upon which a more resilient, adaptive, and strategically robust hardware ecosystem can be built.

Startup Guides, Founder Lessons, and Real Insights from the Startup World

Building a startup is exciting, chaotic, and often misunderstood. If you’ve ever wondered how founders actually validate ideas, find co-founders, raise funding, and survive the emotional rollercoaster, these articles explore the realities behind the startup world.

Start with How to Validate Your Startup Idea in 48 Hours for $0 to understand how founders test ideas quickly before wasting months building the wrong product. Once you have an idea, the next challenge is building it—From Idea to MVP: A Step-by-Step Guide for Solo Founder walks through the journey from concept to a real product.

Many founders struggle with partnerships and team decisions. Should your co-founder live in the same city? Explore Remote vs. Local: Does Your Co-Founder Need to Live in the Same City? and learn the risks hidden in partnerships in 5 Red Flags to Look for When Choosing a Startup Partner. If you’re searching for technical help, How to Find a Technical Co-Founder (Without a Six-Figure Salary) explains how founders actually do it.

The startup journey isn’t just about building products—it’s also about mindset and decision-making. Articles like Decision Fatigue: The Silent Startup Killer, Fear vs Logic: How Founders Actually Make Decisions, and How Overthinking Destroys Early Momentum reveal the psychological battles founders face behind the scenes.

Growth is another misunderstood part of startups. Learn why strategy matters more than hype in Ideas Don’t Scale. Systems Do. and why discipline matters in Why Your Startup Doesn’t Need Growth — It Needs Focus. Discover the importance of early traction in How the First 100 Users Decide Your Startup’s Fate and understand team building through The First Hire That Actually Matters.

Funding is often romanticized, but reality is more complex. Why First-Time Founders Should Avoid Big Funding challenges common assumptions about venture capital, while Revenue Solves More Problems Than Funding explains why sustainable businesses matter more than investor money.

The startup ecosystem also varies by geography. If you're curious about India’s startup scene, explore The New Playbook for Raising in Bangalore, Why Raising Pre-Seed in Bangalore Is Harder Than Ever, and Why B2B SaaS from Bangalore Scales Faster.

But startups are not just about strategy and growth—they’re also about people and emotions. Articles like The Hidden Burnout of Bangalore Founders, Comparison Culture in India’s Startup, and The Loneliness of First-Time Founders in Bangalore reveal the personal struggles founders rarely talk about publicly.

And finally, if you want a deeper perspective on the startup journey itself, explore Lessons Learned Too Late by First-Time Founders and The Myth of the “Overnight Success” Startup—because the truth behind startup success is far more complex than it appears.

Want to calculate the equity for your cofounder?

Nail your cap table before you sign. Whether you're splitting equity with a co-founder or planning your next funding round, our Equity Calculator gives you precision in seconds

Equity calculator →