The New Playbook for Raising in Bangalore

March 10, 2026 by Harshit Gupta

The venture capital ecosystem in Bangalore has entered a definitive stage of structural maturity, transitioning from the erratic "growth-at-all-costs" era of the early 2020s to a disciplined, unit-economics-driven regime in 2025 and 2026. As the innovation capital of the Global South, Bangalore now ranks fourteenth globally in the Global Startup Ecosystem Report 2025, consolidating its position as the engine room of Indian capital deployment. Since 2010, the city’s startups have raised a staggering $79 billion in venture funding, with $70.5 billion deployed in the last decade alone, accounting for nearly 46% of all venture capital raised in India. This concentration of capital, talent, and policy support has created a "New Playbook" for founders and investors alike, characterized by a shift toward "commercial readiness" over mere technical innovation and a global-first approach to scaling.

The Macroeconomic Context: Multipolarity and the Wealth Pivot

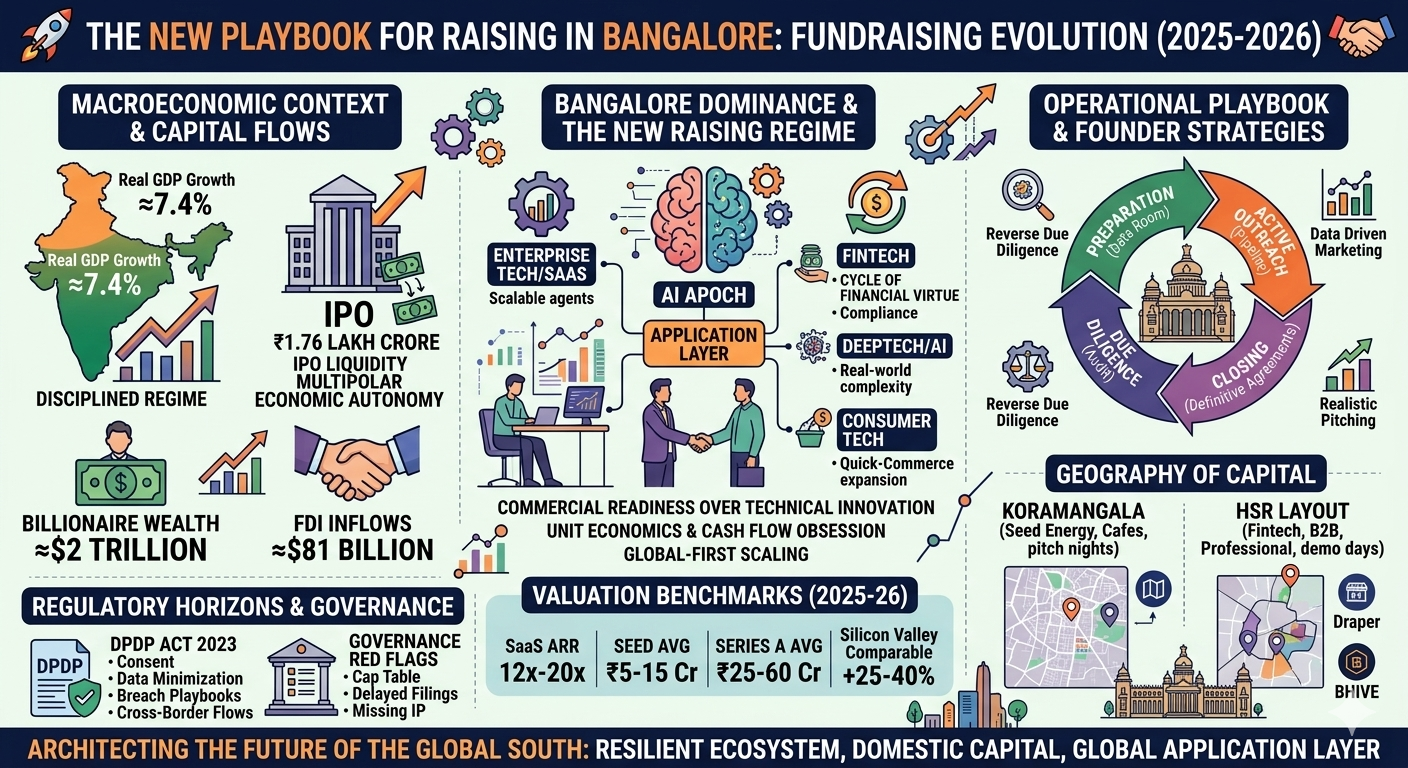

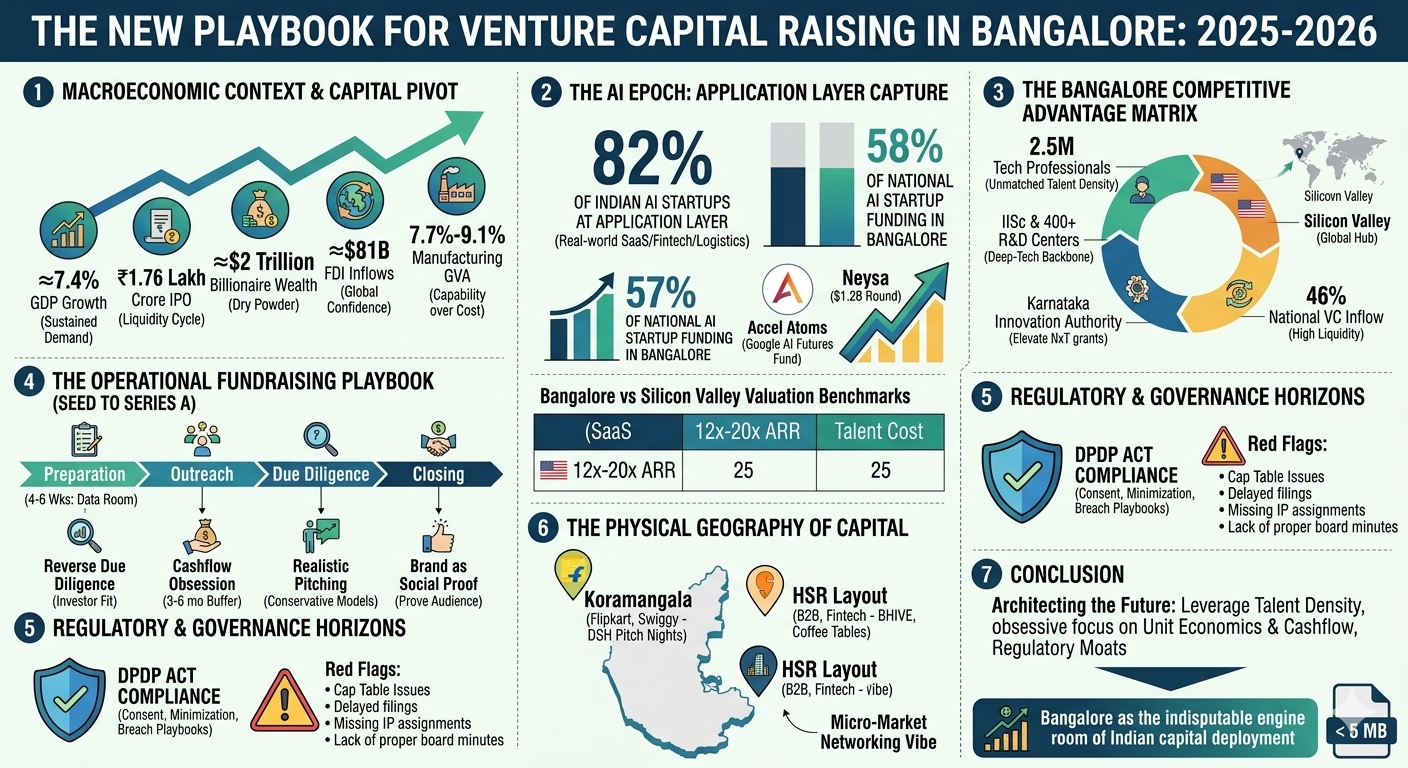

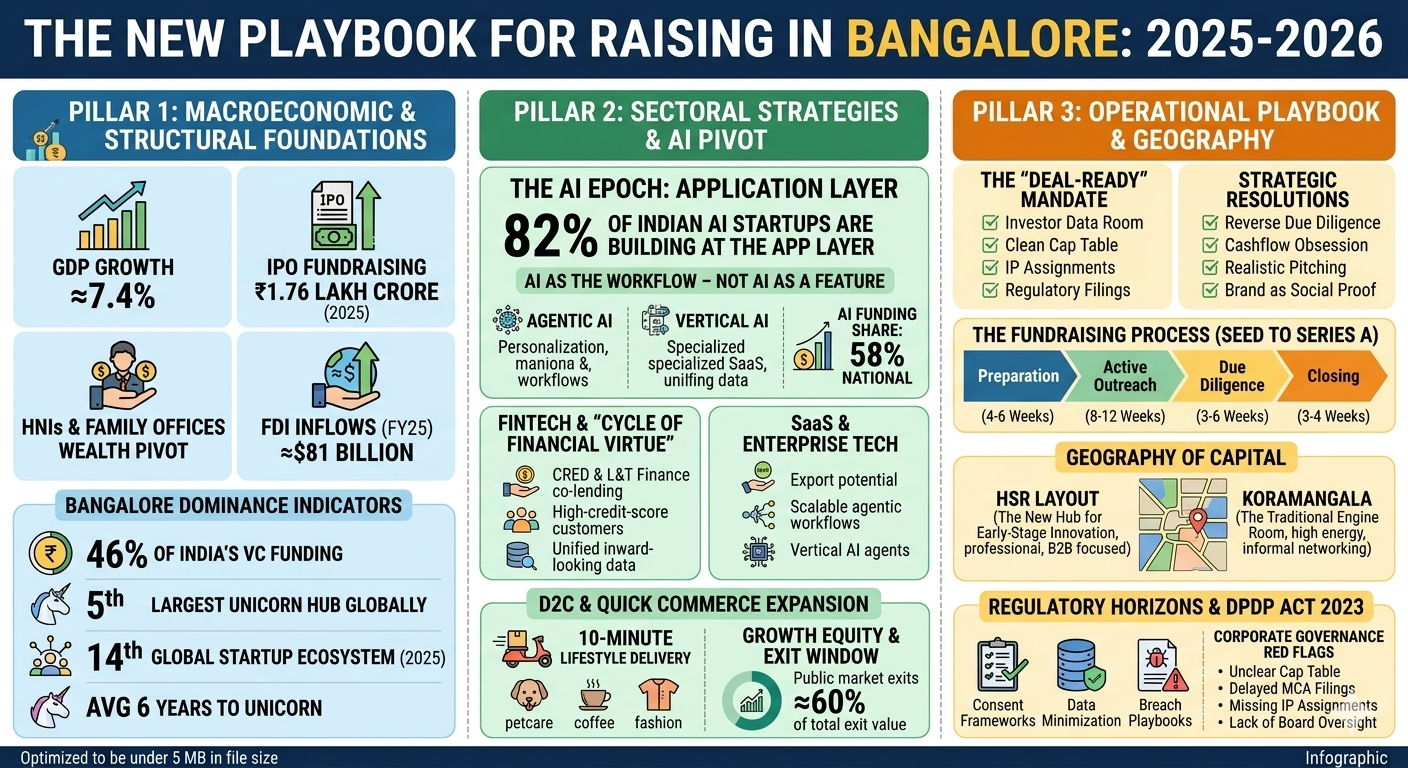

The fundraising environment in Bangalore is inextricably linked to India’s broader macroeconomic resilience. As the country enters the 2025-2026 fiscal year, it maintains its position as the fastest-growing major economy, with real GDP growth projected at approximately 7.4%. This stability is supported by a sophisticated "New Playbook" for the nation’s 350+ billionaires and expanding millionaire base, who currently control wealth equivalent to nearly half of the country’s GDP. For these High-Net-Worth Individuals (HNIs) and family offices, the investment strategy has evolved into a barbell approach: anchoring portfolios with luxury real estate and gold while reinvesting the massive liquidity from a record-breaking IPO market into the technology ecosystem.

In 2025, Indian corporates raised ₹1.76 lakh crore through public offerings, the highest annual fundraising on record. This surge in public market activity has created a virtuous cycle of liquidity, allowing early investors and founders to exit through IPOs or secondary sales, which in turn fuels the next generation of pre-seed and seed-stage ventures. The global backdrop further reinforces this domestic strength; India’s new global playbook involves navigating a multipolar world with economic autonomy, reducing over-reliance on single markets like the United States while maintaining a measured tactical thaw with China to secure critical supply chains.

Indian Macroeconomic Indicators and Capital Context (2025-2026)

Metric | Value / Projection | Strategic Implication | Source |

Real GDP Growth | ≈7.4% | Sustained demand for tech-led services and products. | |

IPO Fundraising (2025) | ₹1.76 Lakh Crore | Massive liquidity injection for reinvestment in startups. | |

Billionaire Wealth | ≈$2 Trillion | Significant dry powder for angel and family office rounds. | |

Gold Import Duty | Reduced from 15% to 6% | Improved transparency in liquid hedges for HNIs. | |

FDI Inflows (FY25) | ≈$81 Billion | Continued global confidence in Indian tech infrastructure. | |

Manufacturing GVA | 7.7%−9.1% Growth | Shift from cost-based to capability-based manufacturing. |

This economic backdrop has fundamentally altered the risk appetite of domestic investors. While venture capital funding into Indian startups slipped 11.03% in 2025 to $12.1 billion, the quality of capital has improved. Investors are no longer chasing speculative growth but are instead prioritizing "financial virtue"—the intersection of high-quality institutions and affluent, high-credit-score customers.

The Structural Engine: Why Bangalore Dominates the Raising Landscape

Bangalore's dominance is not merely a product of history but of a self-reinforcing cycle of human, financial, and institutional capital. The city is home to the largest tech workforce in the world and anchors India’s youngest urban workforce. This talent density is matched by a robust research backbone, with the Indian Institute of Science (IISc) providing a deep-tech R&D foundation that allows startups to build "infrastructure of the future" rather than just consumer-facing applications.

The Karnataka state government has played a pivotal role in this consolidation. The Karnataka Startup Policy 2022-27 provides a stable regulatory environment, while specific initiatives like the ₹5,000 crore Innovation Fund and deep-tech grants of up to ₹1 crore per startup (Elevate NxT) provide critical non-dilutive capital for early-stage ventures. Furthermore, the city’s status as the fifth largest unicorn hub globally—standing alongside the Bay Area, New York, London, and Beijing—ensures a deep pool of "second-time founders" and experienced operators who act as mentors and angel investors.

The Bangalore Competitive Advantage Matrix

Capital Type | Strategic Asset | Ecosystem Impact | Source |

Human Capital | 2.5 Million Tech Professionals | Unmatched talent density for AI and SaaS engineering. | |

Research Capital | IISc & 400+ Global R&D Centers | Deep-tech backbone for frontier innovation. | |

Policy Capital | Karnataka Innovation Authority | $48 Million fund-of-funds and tax incentives. | |

Financial Capital | 46% of National VC Inflow | High liquidity and presence of tier-1 global VC desks. | |

Digital Capital | 5G Rollout & Digital Public Rails | Accelerated scaling of population-scale solutions. |

The velocity of value creation is notably higher in Bangalore than in other Indian hubs. Startups in the city reach unicorn status in an average of six years, faster than the national average. This speed is facilitated by a localized "proximity premium"—the high concentration of VCs, mentors, and successful founders within micro-markets like Koramangala and HSR Layout allows for faster deal flow and more rigorous local due diligence.

The AI Epoch: Capturing the Global Application Layer

In 2025 and 2026, the fundraising playbook for Bangalore startups is dominated by the strategic pivot toward Artificial Intelligence. While Silicon Valley remains the battleground for foundational models, Bangalore has aggressively captured the "Application Layer" of AI. Approximately 82% of Indian AI startups are building at this layer, translating cutting-edge models into products that solve real-world complexity in SaaS, fintech, and logistics.

The city currently attracts 58% of all national AI startup funding, with global VCs like Accel and Peak XV Partners leading the charge. For example, Accel’s "Atoms" program now includes a dedicated AI cohort in partnership with the Google AI Futures Fund, providing up to $2 million per company for exceptional pre-seed teams. The focus in 2026 has shifted from "AI as a feature" to "AI as the workflow," where startups like Neysa raise massive rounds ($1.2 billion in February 2026) to build the infrastructure that will serve as the world's AI implementation backbone.

Sectoral Funding Distribution and Growth Signals (2025)

Sector | Funding Share / Amount | Primary Growth Driver | Source |

Enterprise Tech/SaaS | Dominant Volume | Export potential and scalable AI agentic workflows. | |

Fintech | $3.8 Billion (Total Karnataka) | B2B payment solutions and wealth management. | |

DeepTech/AI | $2.3 Billion | High-frequency application of LLMs to vertical SaaS. | |

Consumer Tech | High Ticket Size | Quick-commerce expansion and premium D2C brands. |

Founders in the AI space are finding that "technical readiness" is no longer enough to secure a term sheet. The 2026 market demands "commercial readiness," meaning startups must demonstrate structured pilot-to-revenue pathways and demand activation mechanisms early in their lifecycle. Investors are particularly bullish on "Agentic AI" that can personalize websites in real-time or streamline complex middle-office engineering workflows, as seen in the recent $5.7 million seed round for Fibr AI.

Fintech and the "Cycle of Financial Virtue"

The Bangalore fintech playbook has evolved from a focus on basic financial inclusion to the creation of sophisticated, data-driven "growth engines". The industry now operates in a high-stakes environment where margins are tight and acquisition costs are rising, making a data-driven marketing strategy a competitive necessity. For mid-sized NBFCs and fintechs, the "New Playbook" involves building a three-layer value pyramid: a foundation of unified inward-looking data, a second layer of deep personalization, and a final layer of predictive, AI-led decisioning.

A significant trend in 2026 is the convergence of high-quality institutions with affluent customers, a concept championed by CRED founder Kunal Shah. Partnerships such as the co-lending agreement between L&T Finance and CRED to offer unsecured personal loans illustrate this shift. By focusing on members with high credit scores and impeccable repayment histories, these startups are fostering a "cycle of financial virtue" that reduces risk and improves unit economics.

The Fintech Valuation and Metric Playbook

Metric / Factor | Benchmark / Value | Strategic Significance | Source |

Revenue Multiple | 8x−15x for payments | Lower than SaaS but reflects higher volume potential. | |

Regulatory Premium | +40% | Valuation uplift for full compliance with RBI and DPDP. | |

GMV Multiple | 2x−5x for marketplaces | Focus on high-frequency engagement. | |

Network Effects | +50% | Platform-based models command higher premiums. |

For fintech founders, the emphasis is now on "Personalized Finance" and "AI-first Financial Distribution". As fraud becomes a "hair-on-fire" problem for the industry, security and trust infrastructure are also attracting significant investment, with companies like IDfy raising $53 million to strengthen digital identity frameworks.

Valuation Benchmarks: The Quantitative Reality of 2026

Valuations in Bangalore have undergone a significant recalibration, moving away from the inflated multiples of 2021 toward benchmarks that reflect global competitiveness and local cost efficiency. The average startup valuation in Bangalore currently sits at approximately ₹285 crore for a Series A median, representing a blend of high talent quality and a 75% lower operational cost structure compared to Silicon Valley.

Comparative Valuation Metrics: Bangalore vs. Global Hubs

Metric | Bangalore (2025-26) | Silicon Valley | Source |

SaaS Revenue Multiple | 12x−20x ARR | 15x−25x ARR | |

Talent Cost Index | 25 | 100 | |

Seed Raise (Avg) | ₹5 - 15 Crore | $1.5M - $4M | |

Series A Raise (Avg) | ₹25 - 60 Crore | $5M - $50M | |

Unicorn Threshold | ₹830+ Crore | $1 Billion |

Startups that can demonstrate proven US market penetration or a global customer base often command a "Silicon Valley Comparable" premium of +25−40%. In the current landscape, investors are prioritizing ARR growth rate, international revenue percentage, and unit economics over raw user acquisition. For SaaS startups, a gross margin of 40%+ and a CAC payback period of under 12 months are considered essential "readiness" signals for a Series A round.

The Operational Fundraising Playbook: Strategies for Founders

Raising capital in Bangalore in 2026 requires a fundamental departure from the "spray and pray" pitching methods of the past. The market has shifted toward a more disciplined, data-driven approach where "fundraise hacking"—raising funds way above the current stage of the startup without business progress—is increasingly viewed with skepticism.

The "Deal-Ready" Mandate

Success in the 2026 fundraising environment depends on being "deal-ready" from day one. This involves building a comprehensive "Investor Data Room" even before the first pitch meeting. Founders who can share a clean cap table, intellectual property assignments, and regulatory filings immediately gain a competitive advantage in speed.

Strategic Resolutions for 2026 Fundraising

Reverse Due Diligence: Founders must research potential investors for industry fit and relevant experience before meetings. Checking references with an investor's existing portfolio companies is now standard practice for the top 30% of founders.

Cashflow Obsession: With 84% of startups identifying cashflow as their biggest risk, business plans must demonstrate resilience. Investors expect to see a 3–6 month cash buffer and a clear path to being "recession-proofed".

Realistic Pitching: Over-optimistic "hockey stick" projections hurt credibility. Modeling conservative, realistic, and optimistic scenarios is essential, as 70% of successful commitments are driven by a clear, grounded value proposition.

Brand as Social Proof: Founders often neglect marketing during the "fundraising grind," yet investors look for social proof and market traction. A targeted campaign that proves a "hungry audience" is often more valuable than unproven code.

The Fundraising Timeline and Process (Seed to Series A)

Phase | Activity | Duration | Goal |

Preparation | Target list (50-75 names), Deck, Data Room | 4 - 6 Weeks | Pipeline establishment. |

Active Outreach | 10-15 warm intros per week, first meetings | 8 - 12 Weeks | Selection of 2-3 lead candidates. |

Due Diligence | Technical audit, customer calls, legal review | 3 - 6 Weeks | Term sheet negotiation. |

Closing | Definitive agreements, regulatory filings | 3 - 4 Weeks | Allocation of shares and fund transfer. |

Source:

The transition from Seed to Pre-Series A is currently the most fragile stage in the ecosystem. Many startups "lose momentum" here, often because they reach technical readiness before commercial readiness. To bridge this gap, founders are increasingly seeking "transition-stage capital" or blended funding instruments like SAFEs (Simple Agreements for Future Equity), which are faster to close and involve less paperwork.

Geography of Capital: HSR Layout vs. Koramangala

The physical geography of Bangalore continues to play a critical role in how capital is raised and distributed. While Indiranagar and Whitefield remain important for enterprise SaaS and late-stage tech, the core "raising" energy is concentrated in Koramangala and HSR Layout.

Koramangala: The Traditional Engine Room

Koramangala remains the undisputed heart of the Bangalore startup ecosystem. It hosts some of the most successful startups like Flipkart, Swiggy, and Practo, providing a historical environment of success that inspires new founders. Networking in Koramangala is centered around high-density spots like Draper Startup House, which hosts frequent "Pitch Nights" and "Founder-Operator Meetups". The café culture, particularly Third Wave Coffee on 80 Feet Road, serves as a de facto office and meeting ground for pre-seed founders and angel investors.

HSR Layout: The New Hub for Early-Stage Innovation

HSR Layout has emerged as the premier destination for B2B and fintech startups, characterized by a more focused, professional networking vibe. Venues like BHIVE Premium HSR Campus and UrbanVault are primary locations for demo days and panel conversations with VCs. The "Coffee Tables" platform in HSR's 7th Sector has become a flagship networking event for business investment and peer-to-peer mentoring.

Networking Venues and Resident Ecosystems

Micro-Market | Key Venues | Vibe / Audience | Source |

Koramangala | Draper Startup House, Third Wave Coffee | High energy, informal, pre-seed to seed focused. | |

HSR Layout | BHIVE HSR, The Dome Café | Professional, B2B focused, Series A+ networking. | |

Indiranagar | WeWork, Global Incubation Services | Enterprise-grade, late-stage, global desks. | |

ORR / Bellandur | Radisson Blu, Happy Llama AI | Large-scale AI summits and institutional networking. |

This geographic concentration allows for what investors call "local due diligence"—the ability to vet a founder by simply walking through the neighborhood and talking to former colleagues or co-investors. Proximity to portfolio companies in these hubs significantly strengthens investor engagement and enables a faster feedback loop during the "build" phase of a startup.

Regulatory Horizons: The DPDP Act and Governance in 2026

A critical component of the "New Playbook" is the integration of high-level governance and regulatory compliance into the early stages of a startup. In 2026, corporate hygiene is no longer an afterthought; it is a fundamental driver of valuation and a prerequisite for Series A funding.

The Impact of the DPDP Act 2023

The enforcement of the Digital Personal Data Protection (DPDP) Act has become a central focus for due diligence. Investors now check for:

Consent Frameworks: Transparent and granular consent options for Indian users.

Data Minimization: Proof that startups are only collecting data essential for the product.

Breach Playbooks: Documented procedures for managing data leaks.

Cross-Border Flows: Compliance with evolving rules on where data can be stored and processed.

Corporate Governance Red Flags in 2026 Due Diligence

Governance Area | Red Flag | Investor Reaction | Source |

Cap Table | Unclear or disputed ownership | Immediate halt to the deal. | |

Regulatory | Delayed MCA filings (AOC-4/MGT-7) | Penalty assessments and deal slowdown. | |

Legal | Missing IP assignments from contractors | Valuation markdown or escrow requirements. | |

Board Structure | Lack of proper minutes or independent oversight | Requirement for board reorganization post-round. |

Founders who fail to maintain "corporate hygiene"—such as regular board minutes, updated ROC filings, and clear employment contracts—are finding their rounds taking months longer to close, or falling through entirely during the final stages of diligence. Conversely, startups that proactively address "technical debt" and regulatory moats are being rewarded with faster closing cycles and higher premiums.

Sectoral Deep Dives: Consumer, SaaS, and the Growth Equity Pivot

The 2025-2026 landscape is marked by a clear rotation toward sectors that can demonstrate "recession-proof" resilience and "Quicker Everything" default systems.

The SaaS and Enterprise Strategy

Bangalore’s SaaS startups are increasingly pivoting to agentic AI and autonomous workflows to streamline traditional agency and engineering processes. The focus is on "Vertical AI"—specialized tools for healthcare, manufacturing, or legal services—that can integrate deeply into existing enterprise workflows. Investors are particularly interested in "Bharat-first" products that solve local complexities but have the architecture to scale globally, such as AI-powered analytics for Indian retail logistics.

D2C and Lifestyle: The Expansion of Quick Commerce

The Direct-to-Consumer (D2C) space has been revitalized by the expansion of "Quick Commerce" beyond groceries into lifestyle categories. Partnerships like The House of Rare with Zepto demonstrate a new playbook where premium fashion is delivered in ten minutes, creating a high-frequency engagement model that appeals to urban millennials and Gen Z. D2C startups like Supertails (petcare) and Drickle (coffee) have raised significant rounds in 2025-2026 by leveraging this rapid delivery infrastructure to reach consumers during "impulse and occasion-driven" moments.

Growth Equity and the Exit Window

The growth stage (Series B and beyond) has seen a decline in absolute dollar volume but an increase in the number of deals, as average check sizes reduced from $60 million to $30 million in 2024-2025. Investors in this segment are exercising more control over the usage of funds, focusing heavily on sustainability in cash flows and management quality. The exit landscape remains robust, with 263 exits recorded in 2024-2025, worth approximately $28 billion. Public market exits now account for nearly 60% of total exit value, providing a clear path for growth-stage investors to realize value.

The Role of Key Ecosystem Personalities and Philosophies

The "New Playbook" is also shaped by the philosophies of influential leaders in the Bangalore ecosystem.

Rainmatter and the "Participatory" Model

Nithin Kamath's Rainmatter has become a pivotal force in backing startups that solve systemic barriers in health, fitness, and climate action. The Rainmatter philosophy emphasizes "alignment in purpose" over rapid scaling, often supporting startups like Machaxi or The Kenko Life that focus on product quality and trust before chasing massive user numbers. This "grounded growth" advice—living the problem before solving it—has become a mantra for founders building in deeply cultural sectors like nutrition and sports.

Blume Ventures and the "Quick-Commerce" Skepticism

Karthik Reddy and Blume Ventures have provided a counter-narrative to the quick-commerce hype, warning that the sector may struggle to maintain growth beyond major cities due to stiff competition and high operational costs. This cautious outlook has encouraged a segment of the ecosystem to focus on more sustainable, high-margin enterprise models rather than participating in capital-intensive consumer "burn" wars.

The "Micro-VC" and "Micro-Grant" Explosion

The rise of specialized seed funds like 3one4 Capital, Speciale Invest, and Ankur Capital has created a more nuanced funding stack. These funds are comfortable with high technical risk and often act as "co-founders," helping early-stage startups navigate the fragile transition to Series A. Additionally, the student-founder ecosystem is being supported by funds like Campus Fund, which has raised $100 million specifically for academic-led AI and SaaS startups.

Conclusion: Architecting the Future of the Global South

The Bangalore fundraising landscape in 2026 is no longer a mimicry of Silicon Valley but a distinct, resilient ecosystem that has architected its own frontier. The "New Playbook" is defined by a rare combination of growth visibility, financial stability, and execution capacity. While global venture capital remains essential, the ascendancy of domestic capital and the maturation of the public markets have insulated Bangalore from the "winter" cycles that previously paralyzed the market.

For founders, the mandate for the remainder of the decade is clear: leverage Bangalore’s talent density to solve global application-layer problems, maintain obsessive focus on unit economics and cash flow resilience, and treat regulatory compliance as a strategic moat. As India marches toward becoming the world’s third-largest economy by 2030, Bangalore’s role as the undisputed capital of innovation ensures that the startups raised here today are the ones that will architect the global technology landscape of tomorrow. The current environment offers a sophisticated canvas for deploying long-term capital, supported by a new generation of wealth creators who prioritize impact, durability, and commercial excellence.

Read More -

1. From Idea to MVP: A Step-by-Step Guide for Solo Founder

🔗 https://findnstart.com/blogs/from-idea-to-mvp-a-step-by-step-guide-for-solo-founder

2. How to Validate Your Startup Idea in 48 Hours for $0

🔗 https://findnstart.com/blogs/how-to-validate-your-startup-idea-in-48-hours-for-0

3. Remote vs. Local: Does Your Co-Founder Need to Live in the Same City?

🔗 https://findnstart.com/blogs/remote-vs-local-does-your-co-founder-need-to-live-in-the-same-city

4. The 2026 Startup Landscape: What Has Fundamentally Changed (and Why Founder Skills Matter More Than Ever)

5. The Most In-Demand Skills for Startup Founders in 2026

🔗 https://findnstart.com/blogs/the-most-in-demand-skills-for-startup-founders-in-2026

6. How to Find a Technical Co-Founder (Without a Six-Figure Salary)

🔗 https://findnstart.com/blogs/how-to-find-a-technical-co-founder-without-a-six-figure-salary

7. 5 Red Flags to Look for When Choosing a Startup Partner

🔗 https://findnstart.com/blogs/5-red-flags-to-look-for-when-choosing-a-startup-partner

8. How to Pitch Your Idea to Potential Co-Founders

🔗 https://findnstart.com/blogs/how-to-pitch-your-idea-to-potential-co-founders

9. How to Build a Portfolio that Attracts High-Growth Startup Founders

🔗 https://findnstart.com/blogs/how-to-build-a-portfolio-that-attracts-high-growth-startup-founders

10. Equity vs. Salary: How to Split Ownership with Your First Teammate

🔗 https://findnstart.com/blogs/equity-vs-salary-how-to-split-ownership-with-your-first-teammate

11. Why Joining an Early-Stage Startup is Better Than a Corporate Job

🔗 https://findnstart.com/blogs/why-joining-an-early-stage-startup-is-better-than-a-corporate-job

12. The Future of EdTech: Why Developers and Educators Need to Team Up Now

🔗 https://findnstart.com/blogs/the-future-of-edtech-why-developers-and-educators-need-to-team-up-now

13. The Architecture of Symbiosis: Analytical Perspectives on the Five Habits of Successful Startup Duos

14. Finding a Co-Founder in the AI Space: What Skills Should You Look For?

🔗 https://findnstart.com/blogs/finding-a-co-founder-in-the-ai-space-what-skills-should-you-look-for

15. Overcoming Analysis Paralysis and the Strategic Path to Execution

🔗 https://findnstart.com/blogs/overcoming-analysis-paralysis-and-the-strategic-path-to-execution

16. From College Project to Company: How to Find Your Student Co-Founder

🔗 https://findnstart.com/blogs/from-college-project-to-company-how-to-find-your-student-co-founder

17. How to Start a Startup While Working a Full-Time Job

🔗 https://findnstart.com/blogs/how-to-start-a-startup-while-working-a-full-time-job

18. How to Build a HealthTech Startup Without a Medical Degree

🔗 https://findnstart.com/blogs/how-to-build-a-healthtech-startup-without-a-medical-degree

19. The Solitary Architect: Executive Isolation in Entrepreneurship

20. The 2026 Guide to Launching a SaaS as a Solo Developer

21. What Sustainable Growth Actually Looks Like

🔗 https://findnstart.com/blogs/what-sustainable-growth-actually-looks-like

22. The Early Warning Signs Your Startup Is in Trouble

🔗 https://findnstart.com/blogs/the-early-warning-signs-your-startup-is-in-trouble

23. How to Grow Without Burning Out

🔗 https://findnstart.com/blogs/how-to-grow-without-burning-out

24. The Truth About “Runway” Most Founders Ignore

🔗 https://findnstart.com/blogs/the-truth-about-runway-most-founders-ignore

25. Revenue Solves More Problems Than Funding

🔗 https://findnstart.com/blogs/revenue-solves-more-problems-than-funding

26. What No One Tells You About Being a Solo Founder

🔗 https://findnstart.com/blogs/what-no-one-tells-you-about-being-a-solo-founder

27. Why Smart People Quit High-Paying Jobs to Build Startups (And Why Most Regret It)

28. Why Most Startup Advice on Twitter Is Dangerous

🔗 https://findnstart.com/blogs/why-most-startup-advice-on-twitter-is-dangerous

29. Decision Fatigue: The Silent Startup Killer

🔗 https://findnstart.com/blogs/decision-fatigue-the-silent-startup-killer

30. Fear vs Logic: How Founders Actually Make Decisions

🔗 https://findnstart.com/blogs/fear-vs-logic-how-founders-actually-make-decisions

31. How Overthinking Destroys Early Momentum

🔗 https://findnstart.com/blogs/how-overthinking-destroys-early-momentum

32. Ideas Don’t Scale. Systems Do.

🔗 https://findnstart.com/blogs/ideas-dont-scale-systems-do

33. The First Hire That Actually Matters

🔗 https://findnstart.com/blogs/the-first-hire-that-actually-matters

34. How the First 100 Users Decide Your Startup’s Fate

🔗 https://findnstart.com/blogs/how-the-first-100-users-decide-your-startups-fate

35. Why Your Startup Doesn’t Need Growth — It Needs Focus

🔗 https://findnstart.com/blogs/why-your-startup-doesnt-need-growthit-needs-focus

36. Why Most Startups Die Quietly

🔗 https://findnstart.com/blogs/why-most-startups-die-quietly

37. Lessons Learned Too Late by First-Time Founders

🔗 https://findnstart.com/blogs/lessons-learned-too-late-by-first-time-founders

38. The Myth of the “Overnight Success” Startup

🔗 https://findnstart.com/blogs/the-myth-of-the-overnight-success-startup

Protect Your Future: The Precision Vesting Calculator

Don't let a "handshake deal" complicate your exit. Map out your ownership journey with our Vesting Calculator

Calculate Your Vesting Schedule →