Comparison Culture in India’s Startup

March 8, 2026 by Harshit Gupta

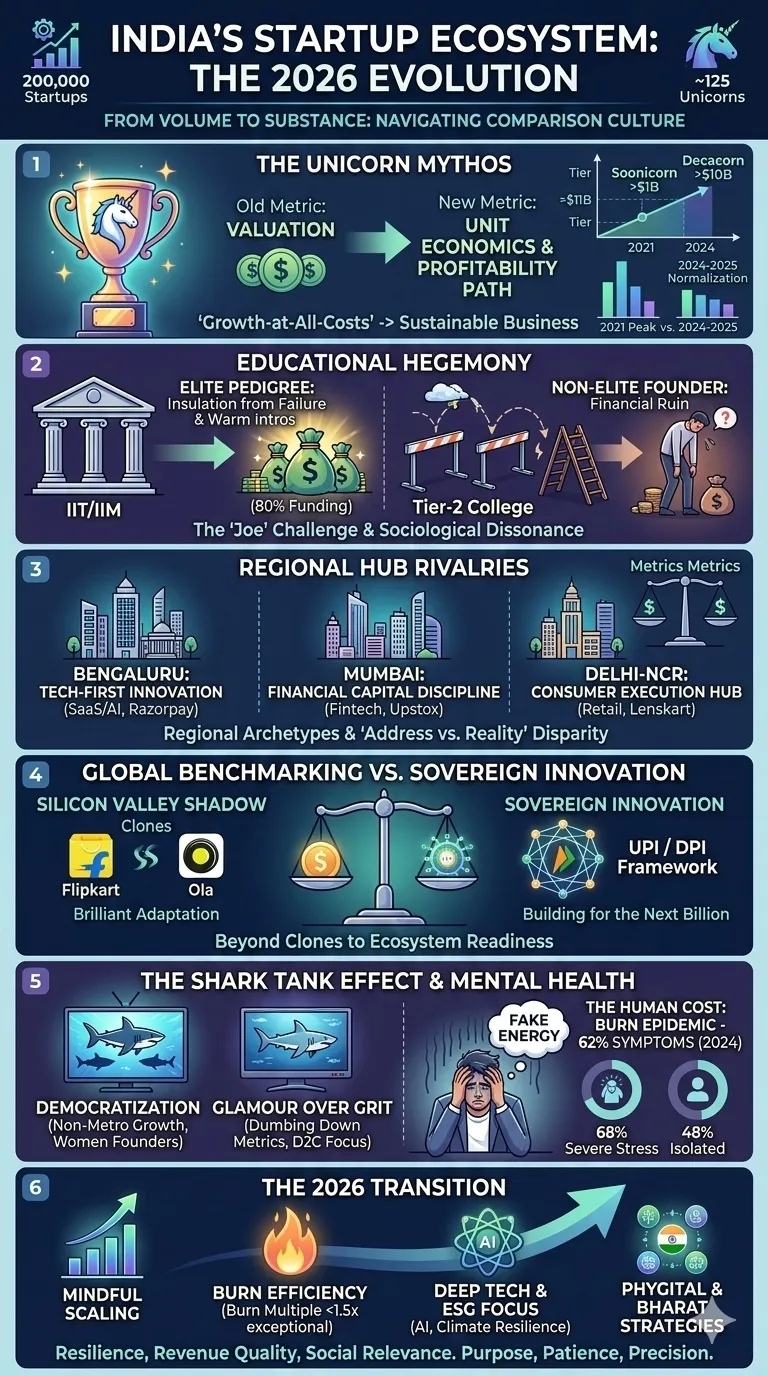

The Indian startup ecosystem, currently institutionalized as the third-largest entrepreneurial landscape globally, is defined by a complex "comparison culture" that dictates everything from capital allocation to founder mental health. As the ecosystem matures into 2026, it is no longer sufficient to view it through the lens of sheer volume—boasting over 200,000 recognized startups and approximately 125 unicorns—but rather through the structural frictions created by intense benchmarking. This report examines the multi-dimensional nature of comparison in India, encompassing the fixation on unicorn valuations, the sociological dominance of elite academic pedigrees, the regional rivalries between burgeoning hubs, and the psychological impact of a media-driven glamorization of the "hustle."

The Unicorn Mythos: Valuation as the Primary Metric of Success

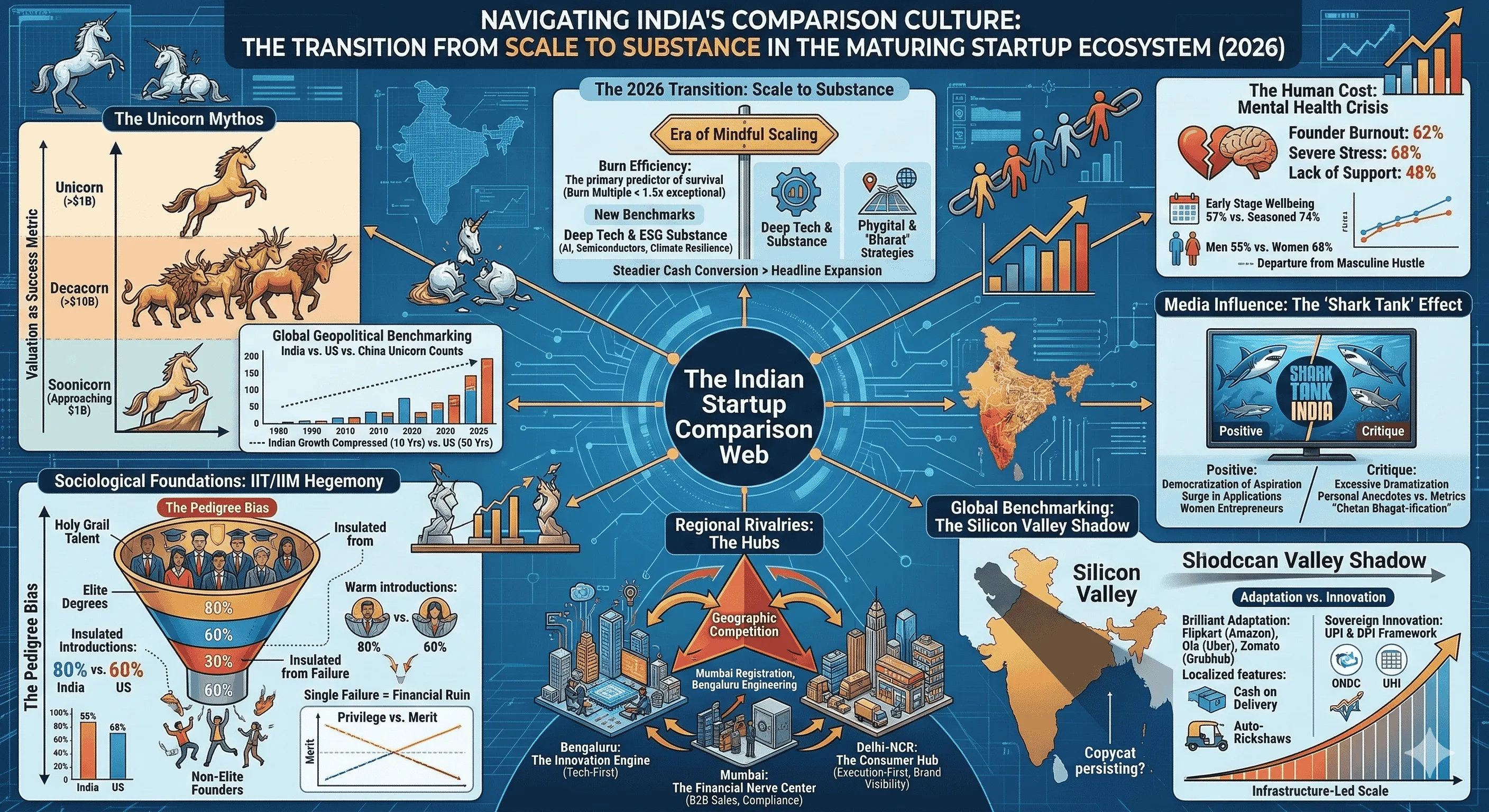

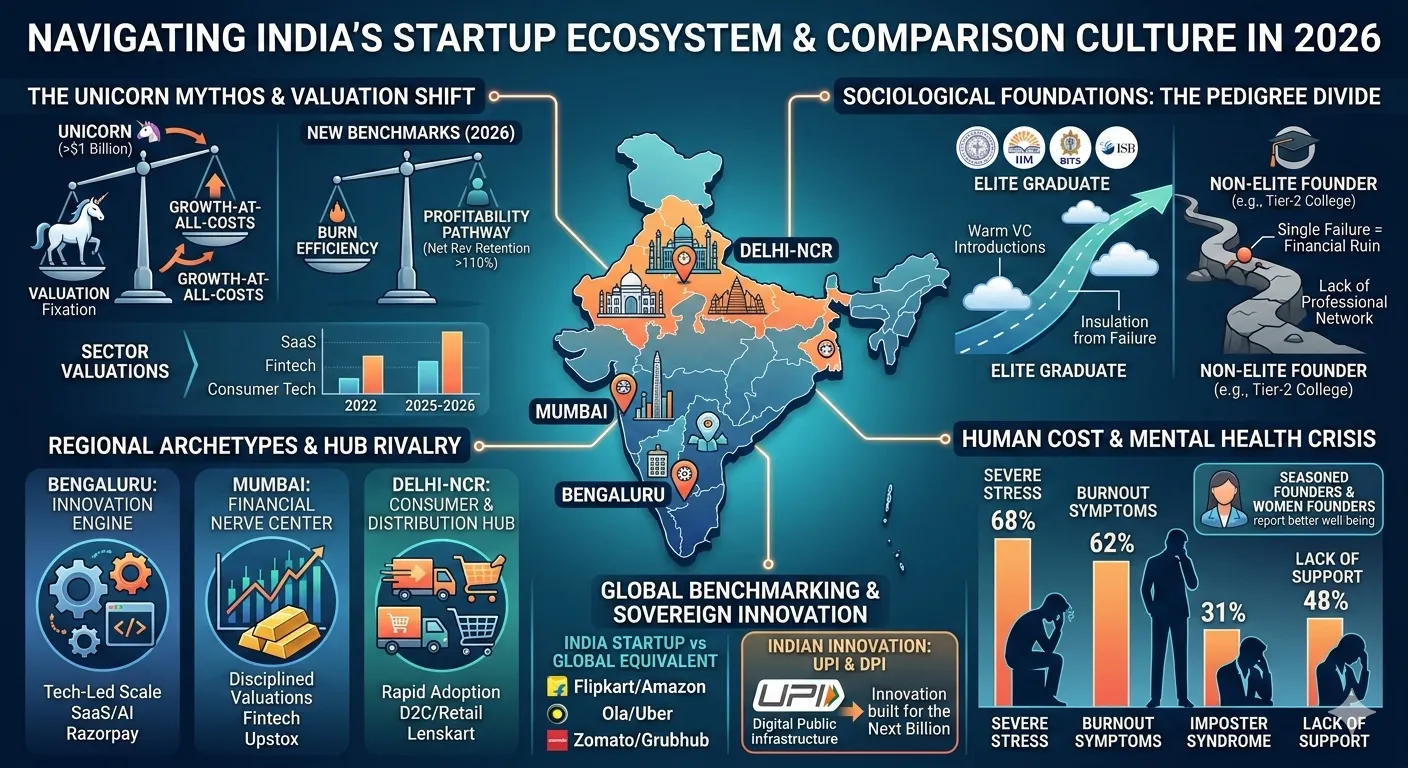

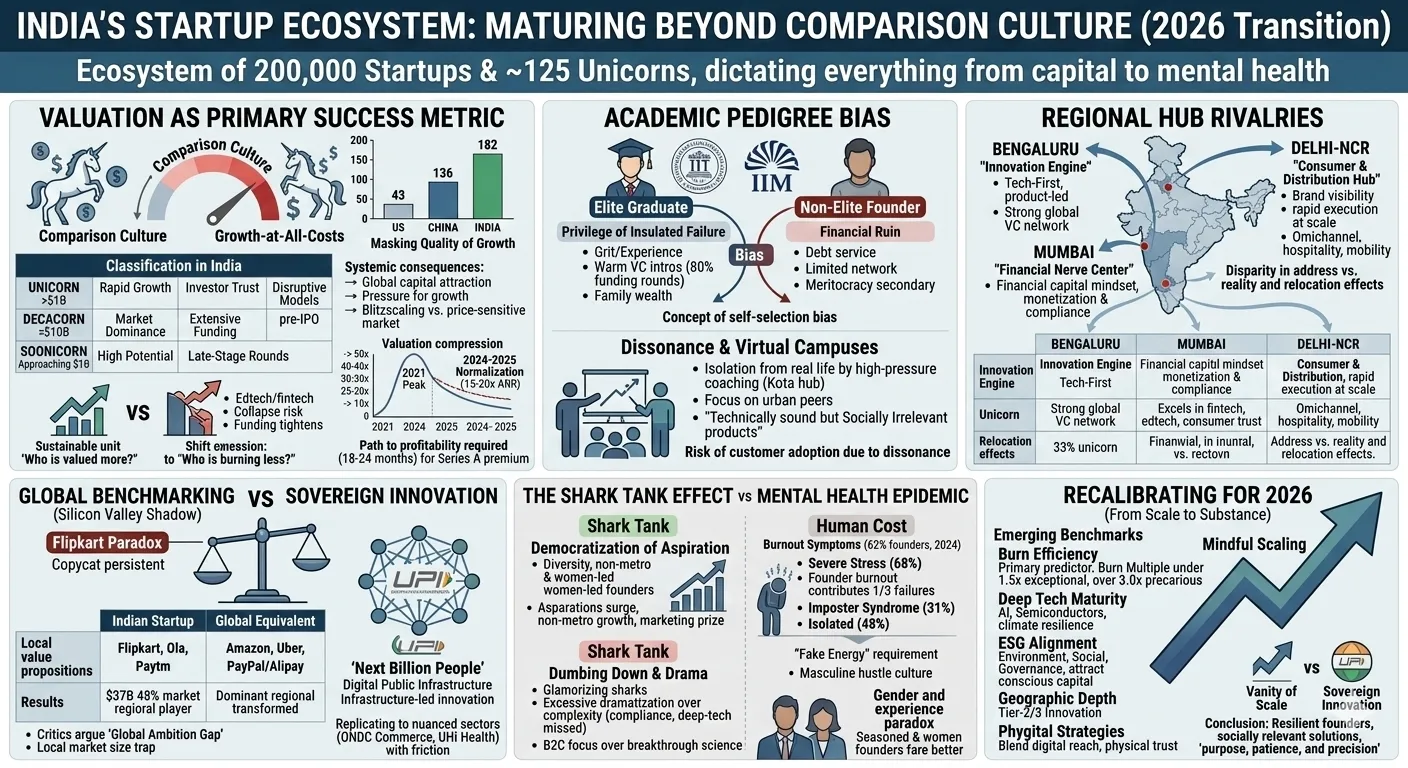

In the Indian context, the term “unicorn” has transitioned from a descriptor of rare success into a standardized benchmark that dictates the perceived legitimacy of a venture. Originally introduced by Aileen Lee to highlight the statistical improbability of a $1 billion valuation, the Indian narrative has embraced this figure as a prerequisite for national relevance. This fixation creates a performance culture where "growth-at-all-costs" is often prioritized over sustainable unit economics, a trend that became particularly pronounced during the hyper-funding cycle of 2021-2022.

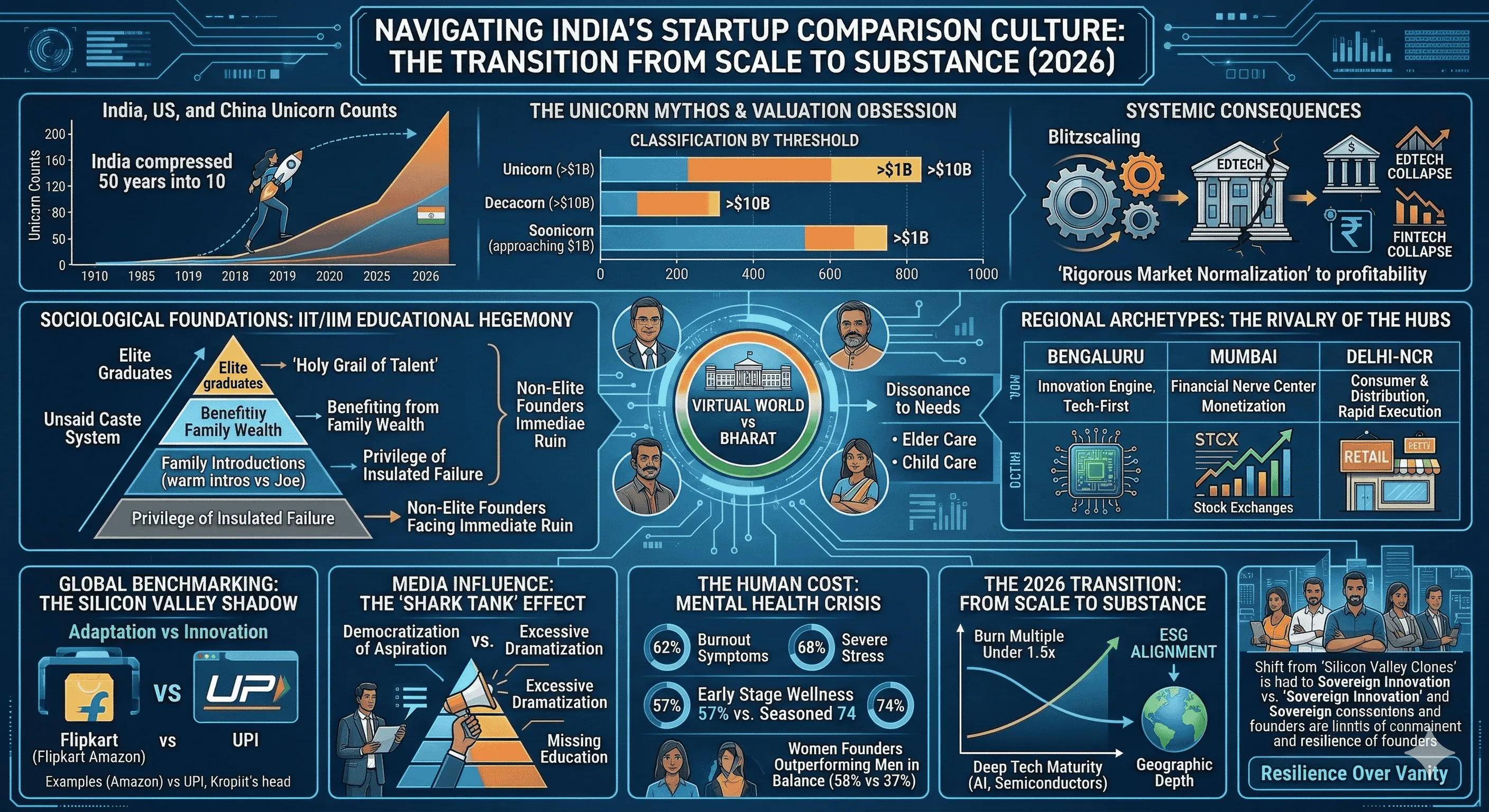

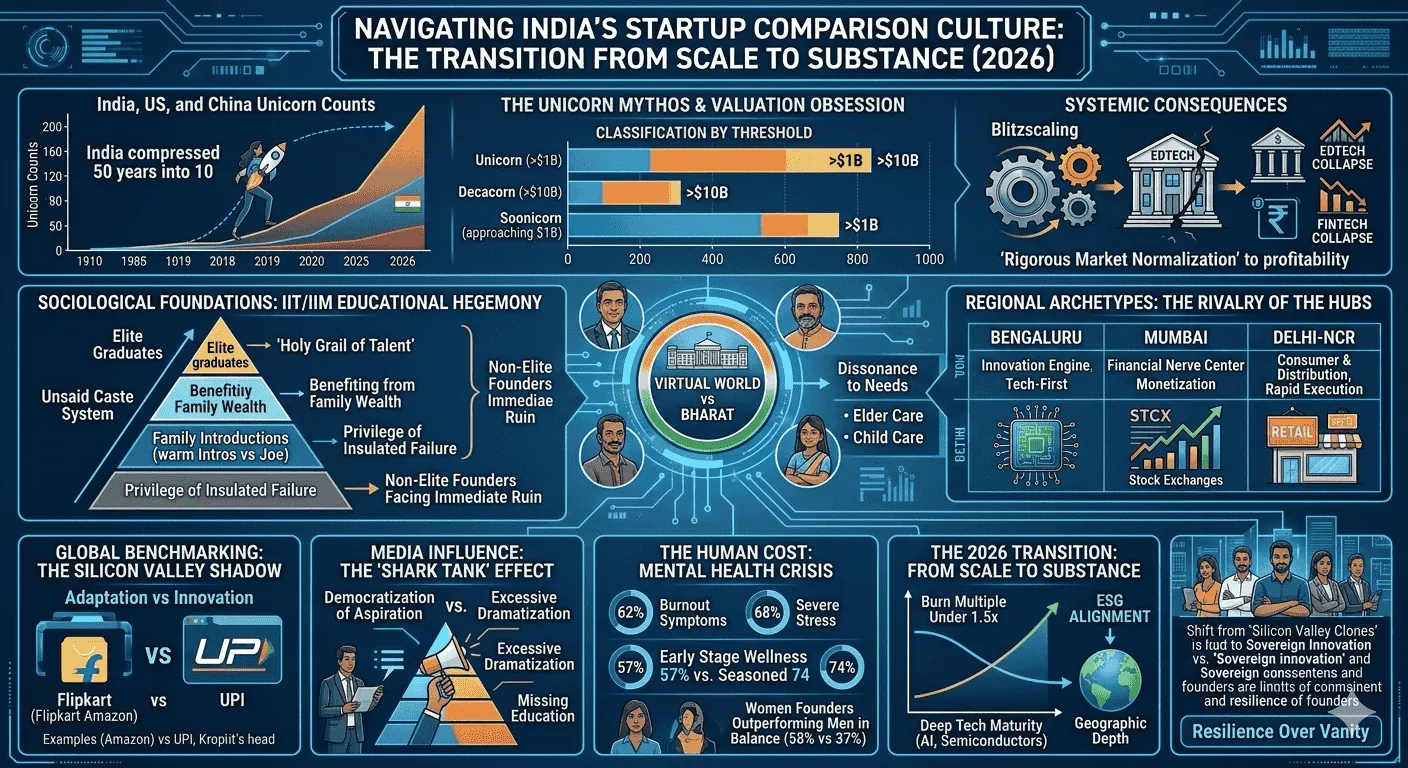

The comparison culture regarding unicorns is not merely domestic; it is a point of geopolitical pride. India consistently benchmarks its unicorn count against the United States and China to validate its status as a global technology power. However, this numerical comparison often masks the underlying quality of growth. While the US ecosystem evolved over five decades, India has compressed its growth into less than ten years, leading to a landscape where speed frequently replaces depth.

Classification | Valuation Threshold | Primary Characteristics in India |

Unicorn | >$1 Billion | Rapid revenue growth, strong investor trust, disruptive models. |

Decacorn | >$10 Billion | Market dominance, extensive funding history, often pre-IPO. |

Soonicorn | Approaching $1 Billion | High potential, often in late-stage growth rounds. |

The pursuit of these benchmarks has systemic consequences. The "unicorn" tag attracts significant global capital but also subjects founders to intense pressure to maintain high year-on-year revenue growth, often exceeding industry averages. This pressure frequently leads to the adoption of "blitzscaling" playbooks designed for the US market, which may not always align with the price-sensitive nature of the Indian consumer. When global funding liquidity tightened in 2023, many ventures that had optimized for unicorn-level valuations without underlying profitability faced severe corrections or collapses, as exemplified by the decline of major edtech and fintech players.

The 2021 Peak and the Reality Check of 2024-2025

The evolution of India's startup valuations reveals a pattern of "irrational exuberance" followed by rigorous market normalization. During the 2021 peak, valuations were often based on future potential rather than current profits, with SaaS companies commanding revenue multiples as high as 25-40x Annual Recurring Revenue (ARR). By 2024-2025, a significant correction occurred, with multiples normalizing to 15-20x ARR and seed-stage valuations compressing by nearly 50% across sectors.

Sector | 2022 Peak Valuation (Seed) | 2024-2025 Valuation (Seed) | Percentage Compression |

SaaS | $8 - $15 Million | $3 - $8 Million | 40-47% |

Fintech | $10 - $20 Million | $4 - $10 Million | 50-60% |

Consumer Tech | $7 - $15 Million | $3 - $7 Million | 53-57% |

This correction has birthed a healthier, albeit more selective, ecosystem. Investors in 2026 now demand a path to profitability within 18-24 months, offering a 30-50% valuation premium for startups that demonstrate contribution margin positive unit economics at the Series A stage. The comparison has shifted from "Who is valued more?" to "Who is burning less?".

Sociological Foundations: The IIT/IIM Educational Hegemony

Perhaps the most deeply entrenched aspect of India’s comparison culture is the "pedigree" bias. An unsaid caste system operates within the startup ecosystem, where graduates of the Indian Institutes of Technology (IITs) and the Indian Institutes of Management (IIMs) are treated as the "holy grail" of talent. This institutional favoritism creates a self-selection bias where nearly half of the nation's startups are founded by alumni from a handful of elite colleges, including the IITs, IIMs, BITS, and ISB.

The Privilege of Insulated Failure

The sociological advantage of an elite degree in the Indian startup scene is not merely about technical competency but about "insulation from failure". For an IIT/IIM graduate, a failed startup is often branded as "grit" or "entrepreneurial experience," allowing them multiple retries due to strong alumni networks, family wealth, and "warm" venture capital introductions. Data indicates that 80% of successful funding rounds in India originate from these warm introductions, compared to 60% in the United States.

In contrast, founders from non-elite backgrounds—often termed "Joe" from a tier-2 college—frequently lack the self-confidence and professional network to secure early-stage capital. For these founders, a single failure often results in immediate financial ruin, forcing them back into the workforce to service debts and fulfill family expectations. This creates a bifurcated market where meritocracy is often secondary to the starting line of the founder.

Dissonance and the "Virtual World" of Elite Campuses

A critical consequence of this academic focus is the "sociological dissonance" between founders and the broader Indian society. Most students destined for premier institutions lose touch with real life as early as 15 years old, entering high-pressure coaching hubs like Kota. Their subsequent years are spent in the "virtual worlds" of elite hostels and campuses, effectively cut off from the needs and aspirations of the typical Indian middle-class family.

This isolation leads to the creation of products that are "technically sound but socially irrelevant". Many founders focus on solving problems for their immediate peer group—convenience apps for high-earning urbanites—while ignoring the fundamental needs of people with young children or aged parents. This lack of a world view is cited as a primary reason for startup failure, as the dissonance between founder perceptions and actual market requirements leads to poor customer adoption.

Regional Archetypes: The Rivalry of the Hubs

The internal comparison culture is further manifest in the geographic competition between India’s primary startup centers. Bengaluru, Mumbai, and the Delhi National Capital Region (NCR) dominate the landscape, accounting for over 75% of growth-stage ventures. Each hub has developed a distinct cultural and economic archetype that influences valuation and operational strategy.

Bengaluru: The Innovation Engine

Known as the "Silicon Valley of India," Bengaluru thrives on a culture of product-led innovation and a dense concentration of technical talent. The city provides 33% of India's total unicorn contributions, supported by a mature network of global venture capital firms. The cultural archetype here is "tech-first," where startups often focus on building robust technology foundations for scale before aggressive monetization.

Mumbai: The Financial Nerve Center

Mumbai’s ecosystem is shaped by its proximity to major banks, stock exchanges, and regulators. The "financial capital" mindset ensures that startups are built with monetization and regulatory compliance in mind from day one. This leads to more stable, disciplined valuations compared to the experimentation-heavy models of Bengaluru. Mumbai excels in fintech, edtech, and consumer platforms that require long-term trust and institutional relationships.

Delhi-NCR: The Consumer and Distribution Hub

Delhi-NCR has evolved into a powerhouse for brand visibility and rapid execution at scale. Leveraging its proximity to large consumer markets and robust logistics networks, the region has produced high-valuation startups in omnichannel retail, hospitality, and mobility. The cultural archetype in Delhi is "execution-first," focusing on understanding mass-market behavior and achieving rapid distribution.

Metric (2025-2026) | Mumbai | Bengaluru | Delhi NCR |

Primary Strength | Financial Depth | Tech Talent | Consumer Reach |

Valuation Trend | Disciplined/Stable | Tech-Led Scale | Rapid Adoption |

Top Sector | Fintech | SaaS/AI | D2C/Retail |

Key Player Example | Upstox ($3.5B) | Razorpay ($9.2B) | Lenskart ($5.0B) |

The competition between these cities extends beyond valuations. There is a notable "address versus reality" disparity, where many startups register in Maharashtra (Mumbai/Pune) for policy benefits while conducting their core engineering and product work in Bengaluru. Furthermore, high real estate costs in Mumbai have historically pushed many tech startups to relocate to Bengaluru, although Mumbai remains the undisputed leader for business-to-business (B2B) sales conversions in the financial sector.

Global Benchmarking: The Silicon Valley Shadow and the "Flipkart Paradox"

A central tension in the Indian startup scene is the comparison with Silicon Valley. While the US hub remains the "North Star" for global innovation, India has transitioned from being a mere reflection to a distinct creator of value. However, a "copycat" label persists, often referred to as the "Flipkart-Amazon Paradox".

Adaptation versus Innovation

The Indian startup playbook has historically been one of "brilliant adaptation" rather than breakthrough innovation. Ventures like Flipkart (Amazon for India), Ola (Uber for India), and Zomato (Grubhub for India) have seen massive success by localizing Western models to suit Indian infrastructure, regulatory, and cultural constraints.

Indian Startup | Global Equivalent | Value Proposition | Result |

Flipkart | Amazon | Cash on delivery, local supply chain | $37B valuation, 48% market share |

Ola | Uber | Integration with auto-rickshaws, cash payments | Dominant regional player |

Paytm | PayPal/Alipay | Utility bill payments, QR-code ubiquity | Transformed digital payments |

Critics argue that this strategy has led to a "global ambition gap". While Chinese adaptations like TikTok or Alibaba evolved into global giants, Indian adaptations have largely remained domestic. This is attributed to the "market size trap"—the belief that with 1.4 billion potential customers, a startup does not need to look elsewhere. However, this local focus often results in different architectural decisions that make global scaling difficult later in the company’s lifecycle.

Sovereign Innovation: UPI and the DPI Framework

Where India has truly innovated is in the realm of "Digital Public Infrastructure" (DPI). The success of the Unified Payments Interface (UPI) represents a form of innovation that builds for the "next billion" people entering the formal economy. Unlike the US, where innovation is often private-sector-led and focused on incremental convenience, India’s innovation is frequently infrastructure-led, making services economically viable at scale.

Despite this, the "comparison culture" has driven the government to attempt to replicate the UPI success in more nuanced sectors like commerce (ONDC) and health (UHI). These newer DPIs face friction because they require deeper ecosystem readiness and behavioral changes, illustrating that "scale" is not synonymous with "mass adoption".

Media Influence: The "Shark Tank" Effect and Glamorization

The arrival of Shark Tank India has significantly altered the public perception of entrepreneurship, democratizing funding awareness across middle-class households. Living room conversations have shifted from "fixed deposits" to "equity and SIPs," and entrepreneurship has become a mainstream career aspiration for the youth.

The Democratization of Aspiration

The show has been instrumental in promoting diversity, providing a national platform for founders from non-metro cities and women-led startups. This has shattered the myth that innovation is restricted to Bengaluru or Mumbai, with significant interest surfacing in cities like Surat, Coimbatore, and Ranchi.

Impact Category | Observation |

Aspirations | Surge in startup applications and inquiries to incubators. |

Gender Diversity | Increased visibility and funding for women entrepreneurs. |

Regional Growth | Decentralization of startup activity to Tier-2 and Tier-3 cities. |

Marketing Prize | 85% of featured startups see a surge in website traffic and brand recognition. |

The Critique of "Dumbing Down" and Drama

Conversely, professional peers have criticized the show for glamorizing the lifestyle of "Sharks" over the grit of business operations. The critique highlights an "excessive dramatization," where discussions often hinge on personal anecdotes—such as where someone's grandmother lived—rather than rigorous financial metrics. This "Chetan Bhagat-ification" of content is viewed as a missed opportunity to educate the youth on the actual complexities of running a business in India, such as regulatory compliance, legal must-knows, and deep-tech innovation.

Furthermore, the "Shark Tank effect" often provides a short-term marketing boost but lacks the substance to create a lasting competitive moat. Many featured businesses are direct-to-consumer (D2C) brands in crowded sectors like clothing or cosmetics, leading to concerns that the show prioritizes "boring and repetitive" innovations over breakthrough scientific products.

The Human Cost: Mental Health and the Burnout Epidemic

The dark side of India’s comparison culture is the staggering psychological toll on founders. In a system where the "unicorn" is the only accepted benchmark of success, mental health frequently takes a backseat.

Statistics of a Hidden Crisis

Data from 2024 and 2025 paints a grim picture of founder well-being. Approximately 62% of Indian founders reported burnout symptoms in 2024. The "Emotional Wellbeing of Entrepreneurs 2024" report revealed that 68% of entrepreneurs experience severe stress, and founder burnout contributes to nearly one-third of all startup failures.

Psychological Metric | Status in Indian Founders |

Severe Stress | 68% (ASSOCHAM 2023). |

Burnout Symptoms | 62% (2024 Survey). |

Imposter Syndrome | 31% (Particularly early-stage founders). |

Lack of Community Support | 48% (Feel isolated in their journey). |

The "fake energy" requirement is a significant driver of this crisis. Founders feel they cannot show vulnerability because their "name is on the cap table," and admitting to burnout is equated with admitting failure. This isolation is compounded by a lack of community support, with only 31% of founders feeling strong support from entrepreneurial networks.

The Gender and Experience Paradox

Interestingly, the data suggests that experienced founders (6+ years) and women founders fare better. Seasoned entrepreneurs report higher wellness (74%) compared to early-stage ones (57%), suggesting that the initial "comparison phase" is the most psychologically hazardous. Women founders were found to outperform men in work-life balance (58% vs 37%) and emotional well-being (68% vs 55%), hinting that a departure from the "masculine hustle culture" might lead to more sustainable business models.

The 2026 Transition: From Scale to Substance

As India enters 2026, the metrics of comparison are undergoing a fundamental recalibration. The era of "growth-at-all-costs" has been replaced by an era of "mindful scaling".

The Rise of "Burn Efficiency"

Investors are now emphasizing "burn efficiency" as the primary predictor of survival. The "burn multiple"—calculated as the amount of cash burned to generate one rupee of new ARR—has become a standard metric. A burn multiple under 1.5x is considered exceptional, while anything above 3.0x is viewed as a precarious runway dynamic.

Deep Tech and ESG as New Benchmarks

The comparison is also shifting toward "Deep Tech" and ESG (Environmental, Social, and Governance) impact. India is no longer just chasing the "vanity of scale" but is pioneering the "reality of substance" in areas like semiconductors, AI-driven drug discovery, and climate resilience. By 2026, deep tech ventures that once showed only prototypes are moving toward real-world deployment in healthcare and defense.

Emerging Benchmark (2026) | Focus Area | Goal |

Profitability Pathway | Unit Economics | Net revenue retention >110%. |

Deep Tech Maturity | AI/Semiconductors | Building long-term national capability. |

ESG Alignment | Sustainability/Impact | Attracting global "conscious" capital. |

Geographic Depth | Tier-2/3 Innovation | Economic inclusivity. |

The "Phygital" and "Bharat" Strategies

Successful Indian startups in 2026 are those that have mastered the "phygital" approach—blending digital reach with physical trust. This is particularly relevant for the "Bharat" cohort (non-metro ventures), which often posts lower average revenue but achieves near-breakeven net outcomes and positive EBITDA compared to their loss-making national counterparts. This suggests that "choosing steadier cash conversion over headline expansion" is becoming a winning strategy in the current landscape.

Conclusion: Navigating the Comparative Future

The Indian startup ecosystem’s comparison culture has served as a powerful, if flawed, engine for rapid growth. The fixation on unicorn status and elite pedigrees provided the necessary benchmarks to attract global capital and establish India as a major player on the tech stage. However, the human and economic costs of this culture—evidenced by widespread burnout, systemic inequality, and the collapse of unsustainable business models—demand a structural shift.

The transition observed in 2026 toward "burn efficiency," deep tech substance, and ESG responsibility indicates a maturation of the ecosystem. To sustain this momentum, the comparison must move away from Silicon Valley clones and toward "sovereign innovation" that leverages India’s unique Digital Public Infrastructure. Founders and investors alike must reject the "vanity of scale" in favor of "revenue quality" and "operational discipline". Ultimately, the success of India’s entrepreneurial journey will be defined not by the number of unicorns it produces, but by the resilience of its founders and the social relevance of its innovations. The goal is no longer just to create world-class startups, but to create solutions that shape the world with "purpose, patience, and precision".

Read More -

1. From Idea to MVP: A Step-by-Step Guide for Solo Founder

🔗 https://findnstart.com/blogs/from-idea-to-mvp-a-step-by-step-guide-for-solo-founder

2. How to Validate Your Startup Idea in 48 Hours for $0

🔗 https://findnstart.com/blogs/how-to-validate-your-startup-idea-in-48-hours-for-0

3. Remote vs. Local: Does Your Co-Founder Need to Live in the Same City?

🔗 https://findnstart.com/blogs/remote-vs-local-does-your-co-founder-need-to-live-in-the-same-city

4. The 2026 Startup Landscape: What Has Fundamentally Changed (and Why Founder Skills Matter More Than Ever)

5. The Most In-Demand Skills for Startup Founders in 2026

🔗 https://findnstart.com/blogs/the-most-in-demand-skills-for-startup-founders-in-2026

6. How to Find a Technical Co-Founder (Without a Six-Figure Salary)

🔗 https://findnstart.com/blogs/how-to-find-a-technical-co-founder-without-a-six-figure-salary

7. 5 Red Flags to Look for When Choosing a Startup Partner

🔗 https://findnstart.com/blogs/5-red-flags-to-look-for-when-choosing-a-startup-partner

8. How to Pitch Your Idea to Potential Co-Founders

🔗 https://findnstart.com/blogs/how-to-pitch-your-idea-to-potential-co-founders

9. How to Build a Portfolio that Attracts High-Growth Startup Founders

🔗 https://findnstart.com/blogs/how-to-build-a-portfolio-that-attracts-high-growth-startup-founders

10. Equity vs. Salary: How to Split Ownership with Your First Teammate

🔗 https://findnstart.com/blogs/equity-vs-salary-how-to-split-ownership-with-your-first-teammate

11. Why Joining an Early-Stage Startup is Better Than a Corporate Job

🔗 https://findnstart.com/blogs/why-joining-an-early-stage-startup-is-better-than-a-corporate-job

12. The Future of EdTech: Why Developers and Educators Need to Team Up Now

🔗 https://findnstart.com/blogs/the-future-of-edtech-why-developers-and-educators-need-to-team-up-now

13. The Architecture of Symbiosis: Analytical Perspectives on the Five Habits of Successful Startup Duos

14. Finding a Co-Founder in the AI Space: What Skills Should You Look For?

🔗 https://findnstart.com/blogs/finding-a-co-founder-in-the-ai-space-what-skills-should-you-look-for

15. Overcoming Analysis Paralysis and the Strategic Path to Execution

🔗 https://findnstart.com/blogs/overcoming-analysis-paralysis-and-the-strategic-path-to-execution

16. From College Project to Company: How to Find Your Student Co-Founder

🔗 https://findnstart.com/blogs/from-college-project-to-company-how-to-find-your-student-co-founder

17. How to Start a Startup While Working a Full-Time Job

🔗 https://findnstart.com/blogs/how-to-start-a-startup-while-working-a-full-time-job

18. How to Build a HealthTech Startup Without a Medical Degree

🔗 https://findnstart.com/blogs/how-to-build-a-healthtech-startup-without-a-medical-degree

19. The Solitary Architect: Executive Isolation in Entrepreneurship

20. The 2026 Guide to Launching a SaaS as a Solo Developer

21. What Sustainable Growth Actually Looks Like

🔗 https://findnstart.com/blogs/what-sustainable-growth-actually-looks-like

22. The Early Warning Signs Your Startup Is in Trouble

🔗 https://findnstart.com/blogs/the-early-warning-signs-your-startup-is-in-trouble

23. How to Grow Without Burning Out

🔗 https://findnstart.com/blogs/how-to-grow-without-burning-out

24. The Truth About “Runway” Most Founders Ignore

🔗 https://findnstart.com/blogs/the-truth-about-runway-most-founders-ignore

25. Revenue Solves More Problems Than Funding

🔗 https://findnstart.com/blogs/revenue-solves-more-problems-than-funding

26. What No One Tells You About Being a Solo Founder

🔗 https://findnstart.com/blogs/what-no-one-tells-you-about-being-a-solo-founder

27. Why Smart People Quit High-Paying Jobs to Build Startups (And Why Most Regret It)

28. Why Most Startup Advice on Twitter Is Dangerous

🔗 https://findnstart.com/blogs/why-most-startup-advice-on-twitter-is-dangerous

29. Decision Fatigue: The Silent Startup Killer

🔗 https://findnstart.com/blogs/decision-fatigue-the-silent-startup-killer

30. Fear vs Logic: How Founders Actually Make Decisions

🔗 https://findnstart.com/blogs/fear-vs-logic-how-founders-actually-make-decisions

31. How Overthinking Destroys Early Momentum

🔗 https://findnstart.com/blogs/how-overthinking-destroys-early-momentum

32. Ideas Don’t Scale. Systems Do.

🔗 https://findnstart.com/blogs/ideas-dont-scale-systems-do

33. The First Hire That Actually Matters

🔗 https://findnstart.com/blogs/the-first-hire-that-actually-matters

34. How the First 100 Users Decide Your Startup’s Fate

🔗 https://findnstart.com/blogs/how-the-first-100-users-decide-your-startups-fate

35. Why Your Startup Doesn’t Need Growth — It Needs Focus

🔗 https://findnstart.com/blogs/why-your-startup-doesnt-need-growthit-needs-focus

36. Why Most Startups Die Quietly

🔗 https://findnstart.com/blogs/why-most-startups-die-quietly

37. Lessons Learned Too Late by First-Time Founders

🔗 https://findnstart.com/blogs/lessons-learned-too-late-by-first-time-founders

38. The Myth of the “Overnight Success” Startup

🔗 https://findnstart.com/blogs/the-myth-of-the-overnight-success-startup

Want to calculate the equity for your cofounder?

Nail your cap table before you sign. Whether you're splitting equity with a co-founder or planning your next funding round, our Equity Calculator gives you precision in seconds

Equity calculator →