Why Capital Is Moving Toward “Safe” Startup Markets

March 18, 2026 by Harshit Gupta

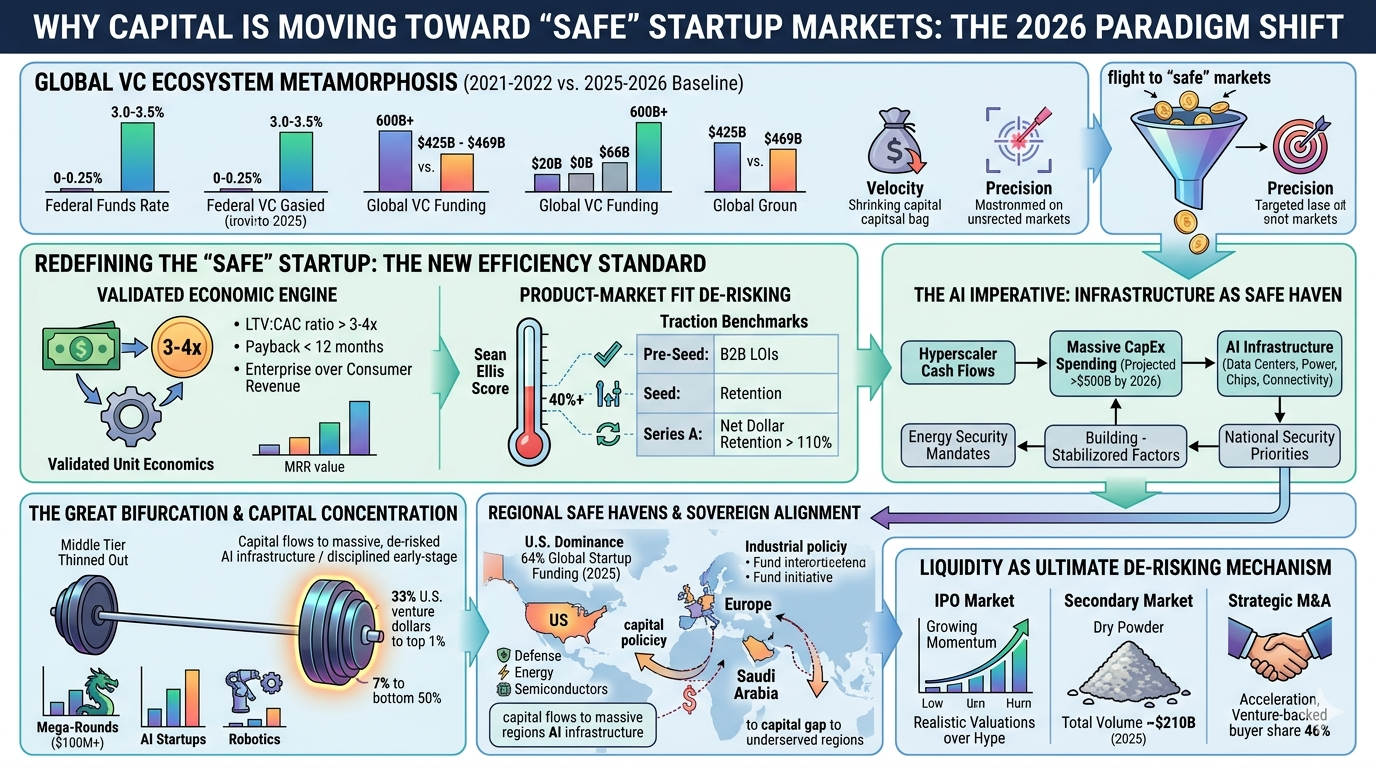

The global venture capital ecosystem has undergone a profound structural metamorphosis, transitioning from a decade defined by the velocity of capital to one dictated by surgical precision, systemic resilience, and a rigorous flight toward "safe" markets. As of the first half of 2026, the migration of capital is not merely a cyclical retreat from risk but a fundamental recalibration of the risk-reward calculus, driven by a convergence of high-interest-rate persistence, geopolitical fragmentation, and the emergence of artificial intelligence as a national security priority. In this environment, the definition of "safety" has been redefined. It no longer implies the absence of volatility but rather the presence of validated unit economics, institutional-grade governance, and alignment with the sovereign industrial policies of the world’s most stable economies.

The Macro-Economic Architecture of Risk Aversion and the Non-Zero Cost of Capital

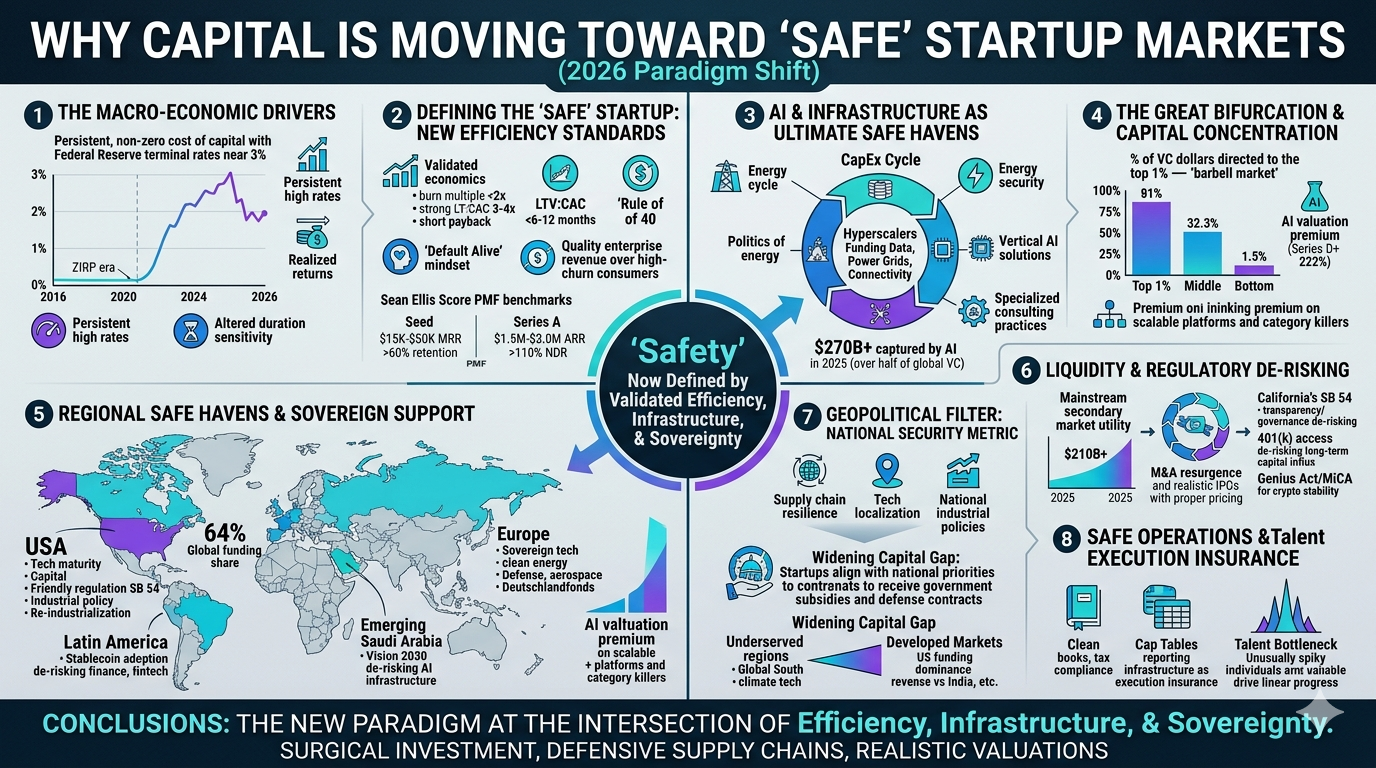

The most significant driver behind the movement of capital toward safe startup markets is the definitive end of the Zero Interest Rate Policy (ZIRP) era. Although the Federal Reserve initiated a shallow easing path in 2025, delivering 75 basis points of rate cuts, the expectations for 2026 suggest only an additional 50 basis points of reduction, leaving terminal rates near 3%. This persistent, non-zero cost of capital has institutionalized a fundamental shift in what defines a fundable startup. Investors and Limited Partners (LPs) now demand real, realized returns rather than paper markups, leading to a "flight to quality" that favors durable, cash-generative businesses.

The persistence of these rates has altered the duration sensitivity of venture portfolios. In the previous decade, capital could wait ten to fifteen years for a liquidity event; however, the current cost of capital necessitates a faster path to profitability or an earlier exit through secondary markets and strategic acquisitions. This structural change is evident in the "Default Alive" mindset that has become a prerequisite for late-stage funding. Investors are no longer willing to bridge "Default Dead" companies—those that require continuous external funding to survive—unless their growth metrics are in the top 1% globally.

Economic Indicator | 2021-2022 Average | 2025-2026 Baseline |

Federal Funds Rate (Terminal) | 0.00%−0.25% | 3.00%−3.50% |

Global VC Funding Volume | 600B+ | $425\text{B} - $469\text{B} |

Average Seed Revenue at Raise | 156K | 363K |

Median EBITDA Multiples (Buyout) | 10.0x | 11.8x |

AI Valuation Premium (Series D+) | Negligible | 222% |

The data indicates that while global venture funding grew 30% year-over-year in 2025 to reach approximately $425 billion, this growth is highly concentrated in specific safe havens and sectors. The "Great Bifurcation" has created a barbell market where capital is either flowing to massive, de-risked AI infrastructure plays or to extremely disciplined early-stage companies with validated unit economics.

Defining the "Safe" Startup: The New Efficiency Standard

In 2026, a "safe" startup is defined by its ability to function as a predictable economic engine. The era of "growth at any cost" has been replaced by the "Rule of 40" and stringent unit economic benchmarks. Investors are prioritizing the "Burn Multiple"—the ratio of net burn to net new ARR—requiring it to be below 2x for a company to be considered resilient. This shift toward efficiency is not just a preference but a survival mechanism in a market where graduation rates are sobering; only 13% of Series A companies successfully raised a Series B within 24 months in 2025.

The Validated Economic Engine

The movement of capital toward safe markets is essentially a movement toward validated economics. Startups are now expected to prove that for every dollar invested in customer acquisition, at least three to four dollars are generated in lifetime value (LTV:CAC ratio). Furthermore, the payback period on marketing spend must typically be less than twelve months, with the most "safe" and sought-after companies achieving payback in under six months. This focus on short-term capital recovery reflects the broader market's aversion to long-duration risk and its preference for liquidity.

The quality of revenue has also become a critical metric for "safety." Investors increasingly value enterprise contracts with multi-year lock-ins over high-churn consumer subscriptions. In the 2026 landscape, $50,000 in Monthly Recurring Revenue (MRR) from five stable enterprise contracts is often valued at 10x the multiple of the same MRR derived from thousands of high-churn consumers. This preference is driving capital away from the "frothy" consumer apps of the previous era and toward vertical SaaS and B2B infrastructure that provides mission-critical services.

Product-Market Fit and the "Sean Ellis" De-risking

The qualitative assessment of product-market fit (PMF) has been quantified to provide a "safety" filter for early-stage investors. The use of the "Sean Ellis Score"—where more than 40% of users must state they would be "very disappointed" if the product were discontinued—has become a standard requirement for Seed and Series A rounds. This ensures that capital is only moving toward companies with a "hair on fire" problem to solve, such as automating privacy compliance for new federal fines or securing post-quantum digital infrastructure.

Funding Stage | 2026 "Safe" Traction Benchmark | Key Risk Mitigation Factor |

Pre-Seed | 0−$5K MRR / 5 B2B LOIs | Proof of Concept and Intent |

Seed | $15K−$50K MRR | >60% Month 1 Retention |

Series A | $1.5M−$3.0M ARR | Net Dollar Retention >110% |

Series B+ | Cash Flow Positive / High NDR | Operational Scalability |

The focus on these metrics allows investors to treat venture capital as a risk-assessment equation rather than a speculative bet. By the time a company reaches Series A in 2026, it is expected to exhibit the characteristics that were previously reserved for Series B or C companies, such as high net dollar retention and clear paths to profitability.

The AI Imperative: Infrastructure as a Safe Haven

Artificial Intelligence has emerged as the ultimate "safe" sector, not because it is low-risk, but because it is perceived as the fundamental utility of the 2026 economy. In 2025, AI-related companies captured approximately $270 billion, accounting for more than half of all global venture capital investment. This concentration is driven by the belief that AI is rewiring the entire investment landscape, creating a multi-year CapEx cycle in data centers, power, chips, and connectivity.

The Multi-Year CapEx Cycle

The movement of capital toward AI is largely a movement toward infrastructure. Large U.S. technology companies have tripled their annual capital investment spending from $150 billion in 2023 to what is projected to be over $500 billion in 2026. This massive deployment of capital is creating a "scaffolding" for the next generation of industry. Investors see these infrastructure plays as "safe" because they are funded largely by cash flows from hyperscalers rather than debt, and they are underpinned by a near-limitless demand for compute capacity.

The "politics of energy" has become a central theme within this AI infrastructure build-out. Data centers are driving a rapid surge in global energy demand, with U.S. consumption expected to rise by 10% per year over the next decade. This has redirected venture capital toward "safe" energy bets, such as nuclear power, energy storage, and carbon capture technologies. These sectors are viewed as stable because they are essential for the AI-driven economy to function and are supported by long-term government policies and energy security mandates.

From Experimental Pilots to Production-Scale Implementation

In 2026, the AI market has reached an inflection point, shifting from experimental deployments to production-scale implementations. This maturation makes the sector "safer" for late-stage investors. Enterprises are no longer merely running proofs of concept; they are rolling out enterprise-wide solutions, which drives a step change in spending levels and performance expectations. This transition is reflected in the growing sophistication of procurement processes and the emergence of specialized consulting practices focused on AI deployment, creating a more predictable and transparent market for investors.

Furthermore, capital is moving away from "generic AI models" and toward highly specialized, "vertical" solutions for specific industries like healthcare, finance, and logistics. These specialized startups are considered safer because they combine proprietary data and domain expertise to deliver measurable productivity gains and cost reductions, making them more defensible against larger, general-purpose models.

The Great Bifurcation and the Concentration of Capital

One of the most defining trends of 2026 is the "Great Bifurcation" or "Barbell Market," where capital is moving aggressively toward the top 1% of companies while the middle section is thinned out. This trend is a clear signal that capital is seeking "winners" who have already established a dominant market position or have the potential to become "index-moving" public companies.

The Barbell Effect in Capital Allocation

In 2025, 33% of all U.S. venture dollars were directed to the top 1% of companies by valuation, a significant increase from 12% in 2022. Conversely, only 7% of capital reached the bottom 50% of companies. This concentration suggests that investors are increasingly averse to "mid-market" risk, preferring to over-capitalize a few "category killers" rather than spreading capital across a broad portfolio. This strategy is driven by the belief that in the AI era, the "winner takes most" dynamic is amplified.

The bifurcation is also visible in the funding stages. While Seed funding has remained relatively stable, focused on "pre-consensus" bets where being right matters more than broad market coverage, the "Series A/B bridge" has become a "valley of death" where most startups fail to raise follow-on capital. The capital that does move through this bridge is concentrated in the most promising companies that can demonstrate traction and unit economics early, often raising larger rounds than in previous eras because the competition has been effectively neutralized.

The Premium on Scalable Platforms

The market's flight to quality is most evident in the valuation premiums commanded by AI-focused firms. In 2025, AI valuation premiums versus non-AI business models reached 222% at the Series D+ stage. This premium reflects the market's conviction that AI is not just a feature but a new foundational platform. Investors are willing to pay a premium for "durability and downside protection" in an uncertain macro-environment, leading to a situation where quality is scarce and deployment pressures among GPs are fueling higher multiples for resilient assets.

Investment Class | 2025 Volume | YoY Change | Primary Driver |

Global VC Total | $469\text{B} | +47% | AI and Mega-rounds |

AI Startups | $226\text{B} | +98% | Infrastructure and Models |

Robotics | $40.7\text{B} | +74% | Supply Chain Automation |

Mega-Rounds ($100\text{M}+) | $312\text{B} | +40% | Concentration in Winners |

This data shows that the "safe" path for large-scale capital is to double down on the infrastructure and platforms that will support the next decade of digital transformation.

Regional Safe Havens and the Resurgence of Domesticity

The geography of venture capital has shifted as investors prioritize regions with stable rule of law, energy security, and supportive industrial policies. The United States has reinforced its position as the world’s primary "safe" market, but other regions are emerging as strategic alternatives based on sovereign initiatives.

U.S. Dominance and the "American Firm" Advantage

In 2025, U.S.-based companies captured 64% of global startup funding, a significant increase from 56% in 2024. In high-growth sectors like AI, American firms have captured an even larger share, with some reports suggesting they captured 92% of global venture capital in specific sub-sectors in 2026. The U.S. is perceived as "safe" due to its convergence of technological maturity, massive domestic capital availability, and a regulatory environment that has become increasingly friendly to strategic sectors like semiconductors, defense, and energy.

The U.S. market’s resilience to geopolitical shocks—such as military tensions in the Middle East—further solidifies its status as a safe haven. Investors believe that even if global trade is fragmented, the U.S. has the domestic capacity to sustain a robust innovation ecosystem. This "re-industrialization" of the American economy, supported by policies that promote skilled immigration and state capacity, is a powerful magnet for both domestic and international capital.

Emerging Strategic Hubs: Saudi Arabia and Latin America

Beyond the U.S., capital is moving toward regions with clear sovereign "roadmaps." Saudi Arabia's Vision 2030 is a primary example, where massive state-led investment in data centers and AI infrastructure is creating a "safe" environment for international VCs and corporates. By positioning itself as a host for large computing clusters with guaranteed energy supply, the Kingdom is de-risking the infrastructure challenges that plague European and American markets.

Latin America is also being viewed as a "safe" region for liquidity preparation. With nearly triple the number of unicorns since 2020 and over 60 tech companies having raised $150M+, the region is gearing up for a significant exit cycle in 2026. Stablecoin adoption in Latin America, which grew 40% year-over-year, has provided a "safe" financial foundation in volatile currency environments, enabling a thriving fintech and remittance ecosystem that attracts risk-averse capital looking for real-world utility.

The European "Flight to Quality" and Sovereign Support

In Europe, venture capital is characterized by a "flight to quality" and a focus on "Class A" assets. While Europe's share of global funding decreased to 14% in 2025, the region has seen a surge in investment into "sovereign" technologies like clean energy, aerospace, and defense. The launch of the "Deutschlandfonds" in Germany in late 2025 to mobilize private investment through cheap loans and scale-up financing is an example of how European governments are trying to create "safe" corridors for private capital to flow into critical infrastructure.

Liquidity as the Ultimate De-risking Mechanism

In 2026, a market is only as "safe" as its ability to provide an exit. The "liquidity dam" is full, and pressure is building in productive ways through the mainstreaming of secondary markets and the resurgence of strategic M&A.

Secondaries as a Core Liquidity Tool

Secondary transactions have transitioned from a niche tactical consideration to a "core portfolio strategy". Total secondary volume reached approximately $210 billion in 2025, as LPs, GPs, and founders turned to the secondary market as an established avenue for liquidity. Secondary funds, now sitting on record levels of dry powder, are accepting narrower discounts and executing deals with greater speed. This de-risks the entire venture asset class by allowing investors to realize returns without waiting for the still-volatile IPO market.

Liquidity Channel | 2024 Volume | 2025 Volume | 2026 Outlook |

IPO Market | Moderate | +20% Volume / +84% Proceeds | Growing Momentum |

Secondary Market | $160 | $210 | Mainstream Utility |

Global M&A | Subdued | +40% (Surpassing 2021) | Acceleration |

GP-Led Secondaries | Growing | 35% of Exit Proceeds | Strategic Pillar |

The rise of GP-led continuation vehicles has also allowed managers to hold high-performing assets longer while providing liquidity to existing investors, further stabilizing the private equity and venture capital ecosystem.

The Resurgence of M&A and "Realistic" Valuations

Global M&A activity is poised to accelerate in 2026, driven by an ongoing Fed rate-cutting cycle and robust demand for strategic high-value transactions, particularly in the tech sector. In 2025, the share of M&A deals with a venture-backed buyer reached 46%, signaling that the ecosystem is becoming more self-sustaining. Large-scale acquisitions, such as Wiz's $32 billion acquisition by Alphabet, have set a precedent for "safe" exits at significant scale.

Furthermore, the IPO market has reopened with a "new playbook" that prioritizes realistic valuations over hype. Down-round IPOs became common in 2025, but many of these companies traded up substantially post-listing, indicating that the public market is hungry for high-quality companies priced at realistic levels. This convergence of public and private market valuations makes the path to exit more predictable and, therefore, "safer" for late-stage investors.

Regulatory Frontiers and the "Safe" Governance Model

The movement of capital is increasingly influenced by regulatory frameworks that mandate transparency and de-risk the investment process. In 2026, institutional investors are prioritizing funds and startups that adhere to high standards of governance and compliance.

California’s SB 54 and Reputational De-risking

The implementation of California’s Fair Investment Practices by Venture Capital Companies law (FIPVCC), also known as SB 54, represents a major shift in regulatory oversight. Beginning in March 2026, covered venture capital firms must register with the state and report demographic data on their founding teams. While this creates a compliance burden, it is also a "de-risking" mechanism for LPs who are under increasing pressure to demonstrate diversity and ethical investment practices. Firms that successfully navigate these transparency requirements are viewed as "safer" institutional-grade partners.

401(k) Access and the Democratization of Private Markets

A pivotal regulatory shift in 2025—the Trump administration's executive order "Democratizing Access to Alternative Assets for 401(k) Investors"—has begun to open a massive new channel of capital into venture and private equity. By 2026, potential changes to ERISA and securities regulations could allow millions of Americans to invest in "safe" private market assets through their retirement plans. This structural change is expected to provide a "perpetual" source of capital for the asset class, further stabilizing valuations and reducing the volatility associated with traditional VC cycles.

Regulatory Change | Region | Target Implementation | Impact on "Safety" |

SB 54 / FIPVCC | California (US) | March 1, 2026 | Enhanced Transparency / LP Alignment |

GENIUS Act | US | 2025/2026 | Crypto / Stablecoin Legitimacy |

MiCA Regulation | EU | 2025/2026 | Digital Asset Market Stability |

401(k) Alt Access | US | 2026/2027 | Stable, Long-term Capital Influx |

These regulatory developments are essentially "paving the roads" for institutional capital to move more freely and safely into the startup ecosystem.

The Geopolitical Filter: National Security as a Primary Risk Metric

In 2026, venture capital has become an instrument of industrial policy. Geopolitical fragmentation has forced investors to look at startups through the lens of "national security" and "resilience" rather than just "growth."

The Multipolar World and Supply Chain Control

Geopolitical risks, ranging from U.S.-China competition to conflicts in the Middle East and Ukraine, have made "The Multipolar World" a top-performing thematic investment category. Capital is moving toward startups that help sovereigns and multinationals secure their supply chains, energy access, and defense capabilities. "Tech localization" is a major trend, where governments prioritize domestic control over key technologies like semiconductors, critical minerals, and biotech.

This geopolitical filter acts as a "safety" screen. Startups that align with these national priorities are more likely to receive government subsidies, defense contracts, and strategic investment from corporate VCs. Conversely, startups that are overly dependent on volatile international supply chains or markets are increasingly viewed as high-risk "non-consensus" bets.

The Impact on Underserved Regions and the "Capital Gap"

The flight to "safe" markets has created a widening "capital gap" in the Global South and other underserved regions. In India, despite a thriving AI ecosystem, venture investment in 2025 was only $2.5 billion—roughly 1% of the total in the United States. This disparity is driven by a lower early-stage risk appetite among domestic investors and a tendency to fund "safe" clones of Silicon Valley models rather than tackling hard, structural problems.

Similarly, the "30:1 Finance Gap" in nature and climate tech highlights the difficulty underserved regions face in attracting capital for long-term ecological resilience. While the Global South hosts the majority of the planet's biodiversity, global finance continues to move toward "nature-negative" activities in developed markets. For these regions, the flight to safety in the West means a drought of the patient, catalytic capital needed to build their own "foundational moments".

The "Safe" Operations: Clean Books and Talent as Execution Insurance

Finally, capital is moving toward "operationally ready" startups. In 2026, "clean books, taxes, and cap tables" are considered "must-haves," and startups that lack institutional-quality reporting are filtered out faster and more aggressively than ever.

Operational Readiness as a Fundraising Prerequisite

Investors now view a startup's operational infrastructure as "execution insurance." If a company is scrambling to set up its fund administration or compliance frameworks during due diligence, it is already behind. The managers and founders closing rounds successfully are those who invested in reporting infrastructure before going to market. This focus on operational excellence is a direct response to the "triage" years of 2022-2023, as investors seek to avoid the governance failures that plagued the previous cycle.

The Talent Bottleneck and Scalability

A key risk metric in 2026 is a startup's ability to attract and retain top-tier talent. In the AI era, every startup can only move as quickly as its engineering and product teams allow. Investors are moving capital toward founders who have a demonstrated ability to hire "unusually spiky" individuals—people with deep domain expertise and the ability to drive non-linear progress. This "talent as a safety metric" approach ensures that capital is only deployed into companies with the human capital necessary to execute at scale in a hyper-competitive market.

Conclusions: The New Paradigm of "Safe" Venture Capital

The research indicates that the movement of capital toward "safe" startup markets is a permanent, structural shift rather than a temporary retreat. In 2026, "safety" is found at the intersection of three core forces: Efficiency, Infrastructure, and Sovereignty.

Efficiency is the New Alpha: The end of ZIRP has made unit economics the primary filter for fundability. A "safe" startup is one that can prove it is a capital-efficient economic engine with a "Default Alive" trajectory.

Infrastructure is the New Safety Net: Massive CapEx spending by hyperscalers has made AI infrastructure the most de-risked and sought-after sector. Capital is flowing to the "scaffolding" of the digital economy—chips, data centers, and power.

Sovereignty is the New Geopolitical Filter: National security and supply chain resilience have become primary investment themes. Capital is moving toward startups that align with sovereign industrial policies in stable hubs like the U.S., Saudi Arabia, and Europe.

The "Great Bifurcation" has created a market where the top 1% of companies are over-capitalized safe havens, while the middle and underserved regions face a "measured scarcity" of capital. For professional investors and founders, success in this environment requires a radical commitment to operational excellence, realistic valuations, and a strategic alignment with the long-term structural shifts in energy, technology, and global policy.

The "safe" market of 2026 is not an easy market; it is a "surgical" one where the bar for entry has been permanently raised. However, for those companies and funds that can meet these high standards of efficiency and utility, the rewards have never been greater, as they are positioned to capture the value creation of the next generational platform shift.

From Idea to Startup: The Real Journey of Modern Founders

Building a startup is exciting, chaotic, and often misunderstood. If you’ve ever wondered how founders actually validate ideas, find co-founders, raise funding, and survive the emotional rollercoaster, these articles explore the realities behind the startup world.

Start with How to Validate Your Startup Idea in 48 Hours for $0 to understand how founders test ideas quickly before wasting months building the wrong product. Once you have an idea, the next challenge is building it—From Idea to MVP: A Step-by-Step Guide for Solo Founder walks through the journey from concept to a real product.

Many founders struggle with partnerships and team decisions. Should your co-founder live in the same city? Explore Remote vs. Local: Does Your Co-Founder Need to Live in the Same City? and learn the risks hidden in partnerships in 5 Red Flags to Look for When Choosing a Startup Partner. If you’re searching for technical help, How to Find a Technical Co-Founder (Without a Six-Figure Salary) explains how founders actually do it.

The startup journey isn’t just about building products—it’s also about mindset and decision-making. Articles like Decision Fatigue: The Silent Startup Killer, Fear vs Logic: How Founders Actually Make Decisions, and How Overthinking Destroys Early Momentum reveal the psychological battles founders face behind the scenes.

Growth is another misunderstood part of startups. Learn why strategy matters more than hype in Ideas Don’t Scale. Systems Do. and why discipline matters in Why Your Startup Doesn’t Need Growth — It Needs Focus. Discover the importance of early traction in How the First 100 Users Decide Your Startup’s Fate and understand team building through The First Hire That Actually Matters.

Funding is often romanticized, but reality is more complex. Why First-Time Founders Should Avoid Big Funding challenges common assumptions about venture capital, while Revenue Solves More Problems Than Funding explains why sustainable businesses matter more than investor money.

The startup ecosystem also varies by geography. If you're curious about India’s startup scene, explore The New Playbook for Raising in Bangalore, Why Raising Pre-Seed in Bangalore Is Harder Than Ever, and Why B2B SaaS from Bangalore Scales Faster.

But startups are not just about strategy and growth—they’re also about people and emotions. Articles like The Hidden Burnout of Bangalore Founders, Comparison Culture in India’s Startup, and The Loneliness of First-Time Founders in Bangalore reveal the personal struggles founders rarely talk about publicly.

And finally, if you want a deeper perspective on the startup journey itself, explore Lessons Learned Too Late by First-Time Founders and The Myth of the “Overnight Success” Startup—because the truth behind startup success is far more complex than it appears.

Want to calculate the equity for your cofounder?

Nail your cap table before you sign. Whether you're splitting equity with a co-founder or planning your next funding round, our Equity Calculator gives you precision in seconds

Equity calculator →