The Rise of Defense Tech Funding in 2024–2026

June 28, 2026 by Harshit Gupta

The global defense technology landscape has undergone a foundational metamorphosis between 2024 and 2026, transitioning from a niche venture category to a primary engine of industrial and technological growth. This era, frequently characterized by financial analysts as a "defense tech supercycle," is defined by a massive influx of capital, the rise of "neoprime" contractors, and a structural shift in military procurement priorities toward software-defined, autonomous, and attritable systems. Driven by sustained geopolitical volatility in Europe, the Middle East, and the Indo-Pacific, the sector has successfully shed previous ethical stigmas, attracting a diverse array of investors ranging from traditional venture capital and private equity titans to sovereign wealth funds and institutional pension managers.

The Macro-Geopolitical Engine of Capital Deployment

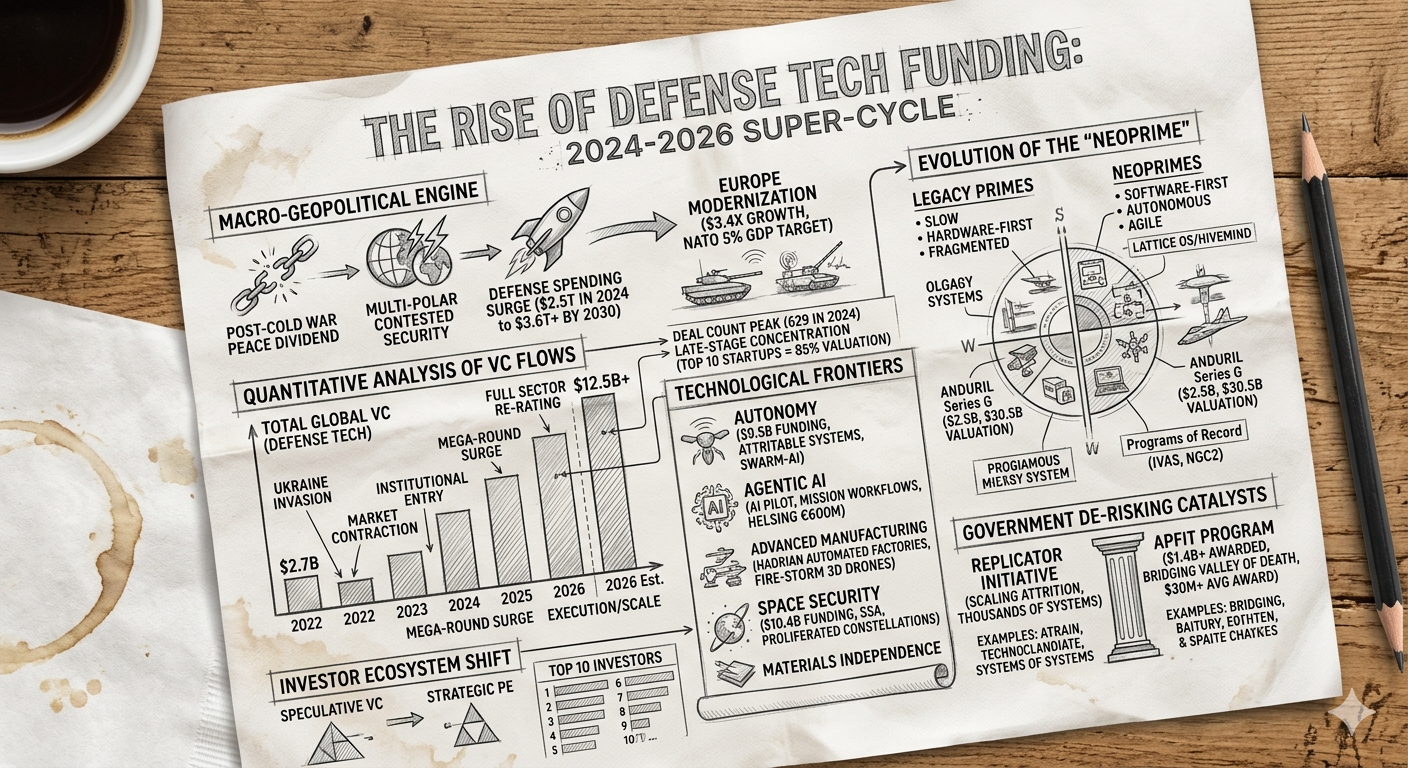

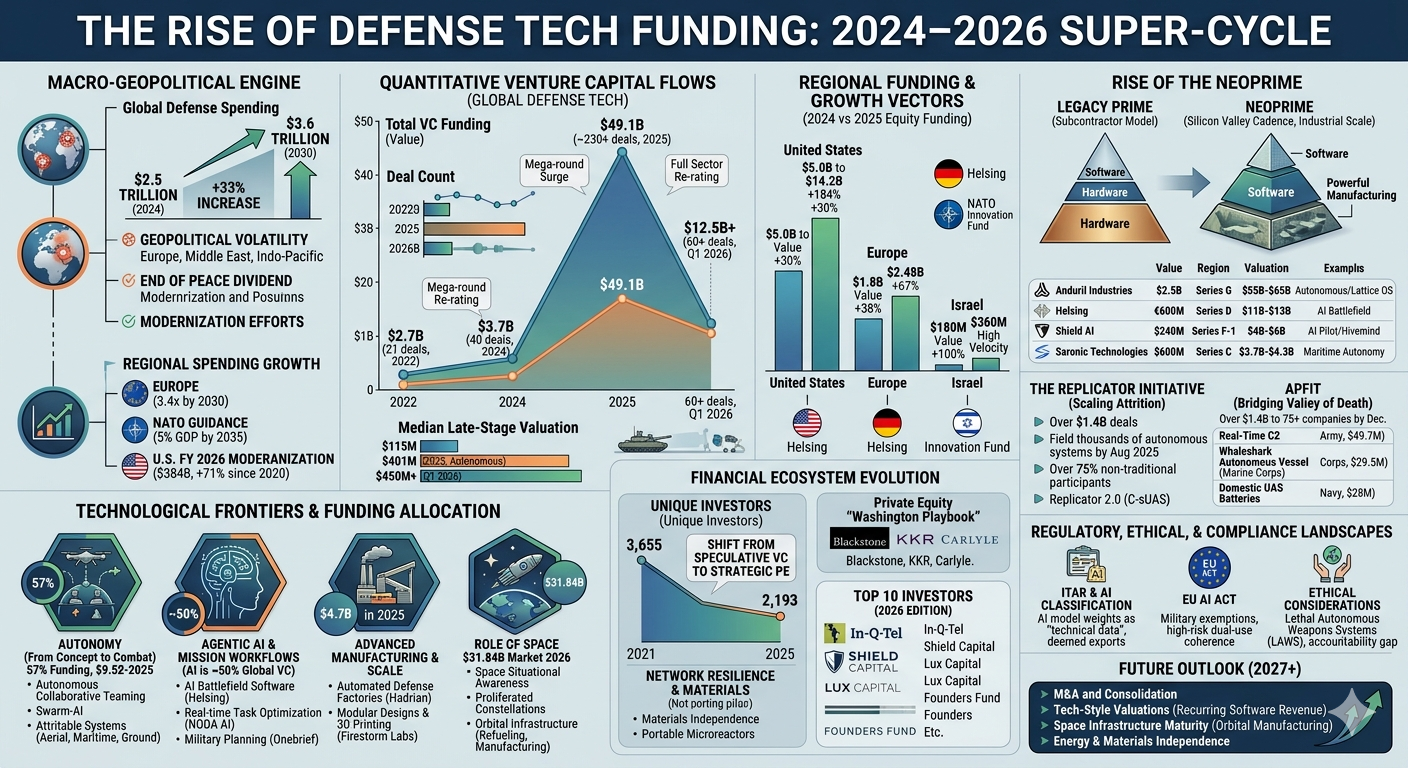

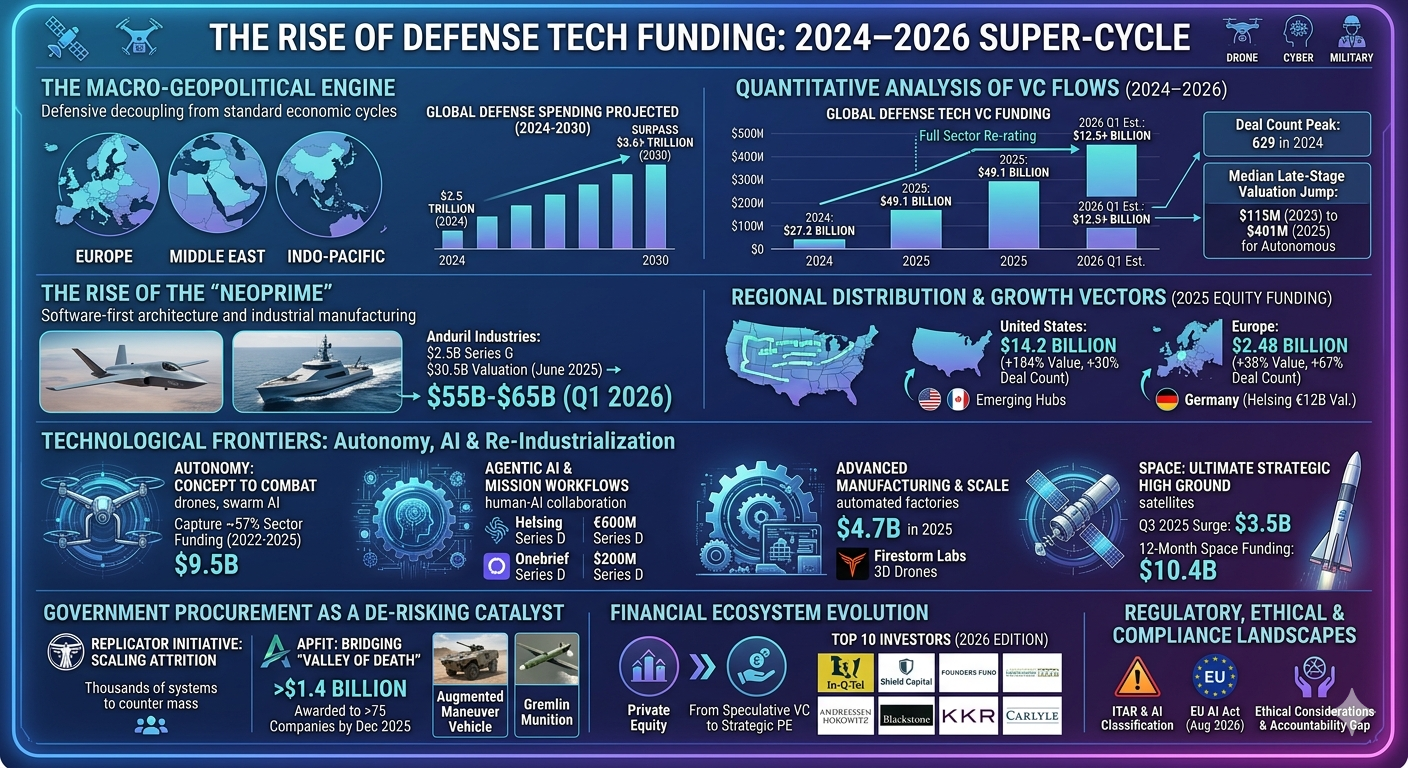

The fundamental driver behind the surge in defense technology funding is the definitive end of the post-Cold War "peace dividend" and the emergence of a multi-polar, technologically contested security environment. The period between 2024 and 2026 marks the point where defense spending decoupled from standard economic cycles, presenting investors with a unique diversification opportunity grounded in national security imperatives rather than consumer sentiment. Global defense spending reached $2.5 trillion in 2024 and is projected to surpass 3.6 trillion by 2030, representing a nearly 33% increase over 2024 levels.

This broad-based rearmament cycle is not merely a response to episodic conflicts but a long-cycle modernization effort. In Europe, the Russian invasion of Ukraine catalyzed a once-in-a-generation reset in air defense, artillery, and autonomous systems. European defense spending is projected to grow 3.4times over the next six years, making it the continent's fastest-growing sector. NATO guidance adopted in June 2025 now targets a spending threshold of 5% of GDP by 2035, a significant escalation from the previous $2\%$ benchmark. Similarly, in the Indo-Pacific, the U.S. National Security Strategy has prioritized the modernization of all military branches, with the Department of Defense (DoD) allocating a substantial $384$ billion for technology modernization in fiscal year 2026 alone—a 71% increase from 2020 levels.

Quantitative Analysis of Venture Capital Flows (2024–2026)

The quantitative data from 2024 through the first quarter of 2026 reveals a sector in high-velocity expansion. Venture capital funding for defense-focused startups reached an all-time peak in 2025, with total deal values hitting 49.1 billion. This represents a near doubling of the 27.2 billion recorded in 2024. The number of individual transactions also climbed to a peak of 629 in 2024, up from 414 in 2020, demonstrating a broader engagement of technology talent in the sector.

Year | Total Global VC Funding (Defense Tech) | Deal Count | Median Late-Stage Valuation | Key Market Driver |

2022 | $2.7B | 21 | $115M | Ukraine Invasion |

2023 | $1.65B | 33 | $110M | Market Contraction |

2024 | $3.7B | 40 | $95M | Institutional Entry |

2025 | $8.7B | 57 | $169.2M | Mega-round Surge |

2025 (Aggregate)* | $49.1B | ~230+ | $401M (Autonomous) | Full Sector Re-rating |

2026 (Q1 Est) | $12.5B+ | 60+ | $450M+ | Execution/Scale |

*Note: Differences in reporting figures between sources like PitchBook and S&P Global reflect varying classifications of "defense tech" versus "dual-use" aerospace and security.

The internal dynamics of these funding rounds indicate a shift toward "fewer, bigger, later-stage" deals. In 2025, capital deployment was heavily concentrated in venture-growth rounds, which totaled 20.4 billion through the third quarter alone. This concentration is exemplified by a small cohort of companies reaching multi-billion dollar valuations. The top 10 startups in the sector currently hold approximately 85% of the total defense tech valuation, with Anduril Industries alone capturing roughly one-third of all funding over the past four years.

Regional Funding Distributions and Growth Vectors

While the United States maintains its position as the dominant market, Europe has emerged as a high-growth corridor. In 2025, U.S.-based defense startups attracted 14.2 billion in equity funding, nearly tripling the 5 billion raised in 2024. In contrast, European defense tech funding rose to 2.48 billion in 2025. While smaller in absolute terms, the number of European equity deals grew by 67%, significantly outpacing the 30% deal count growth in the United States.

Geography | 2024 Equity Funding | 2025 Equity Funding | % Change (Value) | % Change (Deal Count) |

United States | $5.0B | $14.2B | +184% | +30% |

Europe | $1.8B | $2.48B | +38% | +67% |

Israel | $180M | $360M | +100% | High Velocity |

Germany has established itself as Europe's primary hub, largely due to the rise of Helsing, which reached a valuation of €12 billion (13.9 billion USD) in 2025. This European push for "technological sovereignty" is supported by initiatives like the NATO Innovation Fund, which has become one of the most active strategic investors in the region.

The Rise of the "Neoprime" and the Collapse of the Subcontractor Model

A definitive trend of the 2024–2026 cycle is the evolution of venture-backed firms from speculative projects into "neoprimes"—companies that own system-level architecture and manufacturing, moving beyond the historical role of subcontractor. These firms are characterized by a "Silicon Valley development cadence" paired with "industrial-scale manufacturing".

Anduril Industries stands as the archetype of the neoprime. Following its 2.5 billion Series G round in June 2025, the company achieved a valuation of 30.5 billion. More importantly, Anduril has successfully secured foundational "Programs of Record," such as the U.S. Army's 22 billion Integrated Visual Augmentation System (IVAS) program and a 100 million contract for Next Generation Command and Control (NGC2). This ability to translate venture capital into major government contracts has shifted investor perception, making defense tech appear more like "long-duration industrial assets" rather than high-risk software plays.

Neoprime / Startup | Core Focus Area | Last Round / Value | Valuation (Q1 2026) |

Anduril Industries | Autonomous Systems / Lattice OS | $2.5B (Series G) | $55.0B – $65.0B |

Helsing | AI Battlefield Software | €600M (Series D) | $11.0B – $13.0B |

Chaos Industries | Radar / Threat Detection | $510M (Series D) | $4.2B – $4.8B |

Shield AI | AI Pilot / Hivemind | $240M (Series F-1) | $4.0B – $6.0B |

Saronic Technologies | Maritime Autonomy | $600M (Series C) | $3.7B – $4.3B |

BlueHalo | Multi-domain Defense | $1.4B Total Raised | $4.1B (Acquisition Value) |

The success of these firms is rooted in their software-first approach. Unlike legacy primes, who often treat software as an add-on to hardware platforms, neoprimes build "Lattice" or "Hivemind" architectures that allow for rapid iteration and the integration of diverse autonomous ecosystems. This structural shift toward software-driven models is reshaping industry economics, as digital platforms carry higher margins and longer-lived contracts than traditional hardware.

Technological Frontiers: Autonomy, AI, and Re-Industrialization

The allocation of capital in 2024–2026 has concentrated around five critical frontiers that are reshaping the modern battlefield: autonomy, agentic AI, advanced manufacturing, network resilience, and materials independence.

Autonomy: From Concept to Combat

Autonomous systems have transitioned from experimental prototypes to defining battlefield outcomes. This is the largest category in the defense tech market, capturing approximately 9.5 billion—roughly 57% of total sector funding—between 2022 and 2025. Innovation is moving beyond individual drones to "autonomous collaborative teaming" and "swarm-ai".

For late-stage deals, autonomous systems startups saw their median pre-money valuation jump from 115 million in 2023 to 401 million in 2025. This surge is driven by the urgent demand for "attritable" systems—low-cost, replaceable platforms designed to overwhelm adversary mass. In 2026, the focus is broadening from aerial systems to include autonomous maritime surface vessels (Saronic) and off-road ground vehicles (Forterra, Overland AI).

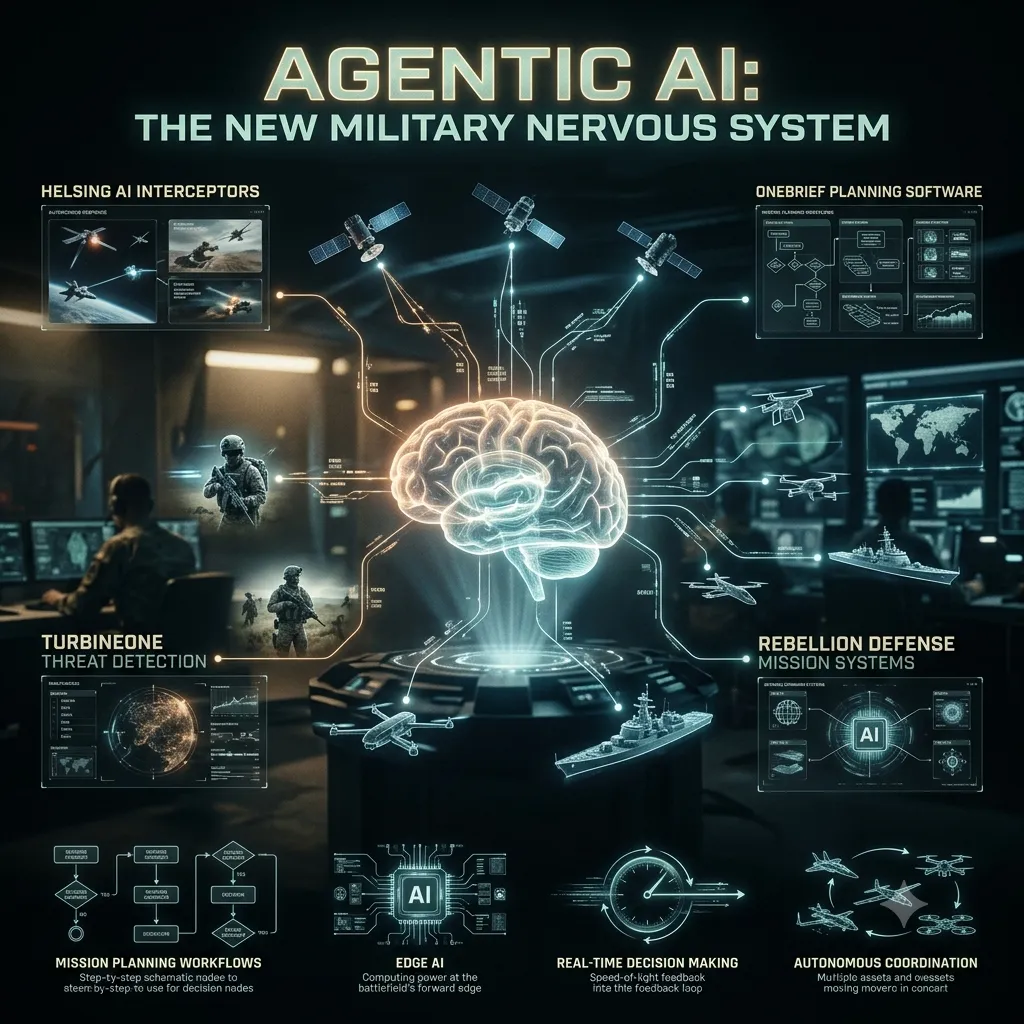

Agentic AI and Mission Workflows

Artificial Intelligence has moved into a deployment phase, acting as the "central nervous system" for military operations. In 2025, approximately $50\%$ of all global venture funding went to AI-related fields, with defense-specific AI funding reaching record levels. "Agentic AI" is now being used to autonomously plan and execute decisions across complex workflows, such as coordinating test plans or managing iterative development cycles.

AI Defense Startup | Specific Application | Recent Funding |

Helsing | AI-guided air defense interceptors | €600M (Series D) |

Onebrief | Military planning workflow software | $200M (Series D) |

TurbineOne | Edge-first threat detection | $36M (Series B) |

NODA AI | Real-time task optimization | N/A (Emerging) |

Rebellion Defense | Mission software and AI | $150M (Series B) |

The software infrastructure has matured to the point where modern Large Language Models (LLMs) can ingest "messy" inputs—notes, chats, PDFs—and reliably output the artifacts that drive military workflows, such as mission plans or logistics schedules.

Advanced Manufacturing and Scale

The primary challenge identified for 2026 is "manufacturing scale". While 2025 was defined by invention, 2026 is defined by execution. Investment in manufacturing-focused defense rose to 4.7 billion in 2025, up from 2.6 billion in 2024. This shift is essential because the Western industrial base has struggled to rapidly scale production for munitions and energetics.

Startups like Hadrian are building "automated defense manufacturing factories" to solve this capacity gap, while Firestorm Labs uses modular designs and 3D printing to build drones in hours rather than weeks. This "factory as a product" approach is a prerequisite for sovereign resilience in a contested supply chain environment.

The Role of Space: The Ultimate Strategic High Ground

Space has been codified as a critical warfighting domain, attracting significant capital for both infrastructure and situational awareness. The space launch services market expanded to 31.84 billion in 2026, reflecting a massive rotation of capital into reusable infrastructure. In the third quarter of 2025 alone, a 3.5 billion surge in capital investment pushed the trailing 12-month space funding total to 10.4 billion.

Key trends in the space domain for 2026 include:

Space Situational Awareness (SSA): Integration of ground- and space-based sensors with AI to detect and characterize threats in contested orbits.

Proliferated Constellations: A shift toward resilient, low-latency satellite networks designed to maintain communications even in degraded conditions.

Orbital Infrastructure: Graduation of technologies like refueling stations and in-space manufacturing from demonstrations to operational assets.

Companies like ICEYE (SAR satellites), HawkEye 360 (RF intelligence), and True Anomaly (space security) have secured significant rounds in 2025 and 2026, validating space as a mainstream asset class for institutional investors.

Government Procurement as a De-Risking Catalyst

The surge in private funding has been met with a corresponding evolution in government procurement pathways. Programs like the Department of Defense’s Replicator and APFIT have been instrumental in signaling "demand pull" to the venture community.

The Replicator Initiative: Scaling Attrition

The Replicator initiative, launched in 2023, aimed to field thousands of autonomous systems by August 2025 to counter China's "mass" in the Indo-Pacific. While the initiative faced technical glitches and transparency concerns, it successfully moved "hundreds" of drones to warfighters by summer 2025, with "thousands more on contract". Replicator 2.0, announced in late 2024, has expanded this focus to "counter-small unmanned aerial systems" (C-sUAS) for the defense of fixed sites. Approximately 75% of Replicator participants are non-traditional defense companies, highlighting its role in diversifying the industrial base.

APFIT: Bridging the "Valley of Death"

The Accelerate the Procurement and Fielding of Innovative Technologies (APFIT) program has become a cornerstone of the U.S. strategy to transition technologies from development to production. As of December 2025, APFIT has awarded over 1.4 billion to more than 75 companies.

FY 2026 APFIT Project Example | Service | Funding | Focus |

Real-Time Command and Control | Army | $49.7M | Tactical Edge Computing |

Augmented Maneuver Vehicle | Space Force | $48.5M | Satellite Mobility |

Gremlin Low-Cost Munition | Marine Corps | $35M | Attritable Strike |

Whaleshark Autonomous Vessel | Marine Corps | $29.5M | Low-Profile Logistics |

Domestic UAS Batteries | Navy | $28M | High-Performance Power |

The increase in the average APFIT award to over $30$ million in 2026 demonstrates the program's ability to scale mature technologies effectively.

Financial Ecosystem Evolution: From Speculative VC to Strategic PE

The investor profile in defense tech has matured significantly. Between 2021 and 2025, the number of unique investors dropped from a peak of 3,655 to 2,193, reflecting a shift from "speculative inflows" to a "persistent base of strategics, defense-focused funds, and large asset managers".

Private Equity and the "Washington Playbook"

Large private equity firms like Blackstone, KKR, and Carlyle have significantly increased their defense allocations in 2025 and 2026. This "Great Re-Entry" was facilitated by interest rate stabilization and a regulatory thaw in early 2026. Carlyle, in particular, has leveraged its 40-year history in Washington, D.C., to tap into global defense spending, viewing it as a core "power alley". These firms are pursuing "add-on" and "roll-up" strategies, acquiring smaller defense tech platforms to build scaled, vertically integrated entities.

Top 10 Investors in Aerospace, Defense, and Dual-Use (2026 Edition)

Rank | Firm | Primary Focus | Notable Characteristic |

1 | In-Q-Tel (IQT) | National Security Venture | Bridge between frontier tech and Intel community |

2 | Shield Capital | Early-stage Dual-use | Advisory board includes former SECDEFs and Generals |

3 | Lux Capital | Frontier Science / Hard Tech | Backs PhD-led "hard tech" for defense |

4 | Founders Fund | Category-defining Deep Tech | Early backer of Palantir, SpaceX, and Anduril |

5 | AE Industrial Partners | National Security / Aerospace | Specialist with deep operational depth |

6 | Veritas Capital | Mission-critical Software | Influential owner of gov-tech platforms |

7 | Sequoia Capital | Early to Growth Stage | Backs foundational infrastructure and autonomy |

8 | Andreessen Horowitz | American Dynamism | Largest operator network for recruitment/scaling |

9 | Arlington Capital | Gov Contracting / Services | Strong track record in DoD/Intel services platforms |

10 | The Veteran Fund | Seed-stage Veteran-led | Thesis driven around veteran domain expertise |

Regulatory, Ethical, and Compliance Landscapes in 2026

The rapid advancement of technology has created a friction point with existing regulatory frameworks. Defense tech companies in 2026 must navigate a complex landscape of export controls, AI safety rules, and ethical considerations.

ITAR and the Classification of AI

In 2026, AI-driven defense innovation is colliding with a regulatory structure (ITAR) originally designed for physical components. AI model weights, source code, and training data are increasingly classified as "technical data" or "defense services". For venture-backed startups, even an informal inquiry regarding export violations can materially affect funding and M&A eligibility.

Key compliance risks in 2026 include:

Deemed Exports: Disclosing code to foreign-national software developers, even within the U.S., can trigger violations.

Defense Services: Consulting on the optimization of AI-driven targeting systems for foreign persons qualifies as a "defense service".

Training Data Blind Spots: Datasets derived from controlled defense systems are now a major compliance exposure.

The EU AI Act: Dual-Use and Military Exemptions

The EU AI Act, fully applicable as of August 2, 2026, imposes strict obligations on "high-risk" AI systems. While the regulation contains a sweeping exemption for AI systems used exclusively for military or national security purposes, the "blurring" of dual-use technology creates a legal gap. A system developed for military use that is then briefly used for civilian law enforcement must comply with the full transparency and risk management requirements of the Act. This "regulatory incoherence" poses a significant challenge for European startups developing versatile AI platforms.

Ethical Considerations and the "Accountability Gap"

The development of Lethal Autonomous Weapons Systems (LAWS) has raised profound ethical questions. Experts warn of an "accountability gap," where existing legal frameworks fail to attribute responsibility for harm caused by independent machine decisions. Machine learning's "black box" nature makes it difficult to prove negligence among developers or military leaders. International discussions under the United Nations Group of Governmental Experts (UN GGE) remain fractured, leaving national legislation fragmented and unsystematic.

The Future Outlook: Consolidation and the Re-Industrialization Phase

The defense technology sector enters the second half of 2026 with strengthening fundamentals. Global defense transformation is no longer driven by any single conflict but by a broad rearmament cycle aimed at meeting future threats through modern, tech-focused solutions.

Anticipated Trends for 2027 and Beyond

M&A and Consolidation: As competition for government contracts heats up, significant consolidation is expected. Strategic acquirers will move to buy up startups that have successfully navigated the manufacturing scale-up phase.

Tech-Style Valuations: The shift toward recurring software revenue will likely move defense valuations closer to those of software businesses, away from traditional industrial multiples.

Space Infrastructure Maturity: Technologies like in-space refueling and orbital manufacturing will transition from experimental to operational status, becoming essential components of global security.

Energy and Materials Independence: Securing critical minerals and deploying portable microreactors for energy resilience will become a prerequisite for defense technology sovereignty.

In conclusion, the rise of defense tech funding in 2024–2026 represents a structural re-ordering of the industrial landscape. The influx of nearly 50 billion in venture capital, paired with the entry of private equity titans and the implementation of rapid procurement initiatives like Replicator and APFIT, has created a robust ecosystem for national security innovation. While regulatory and ethical hurdles remain, the momentum is undeniably toward a software-defined, autonomous, and industrial-scale future for global defense. The "execution phase" has officially begun.

Protect Your Future: The Precision Vesting Calculator

Don't let a "handshake deal" complicate your exit. Map out your ownership journey with our Vesting Calculator

Calculate Your Vesting Schedule →