The Challenge of Scaling Startups in Belgium’s Smaller Market

March 14, 2026 by Harshit Gupta

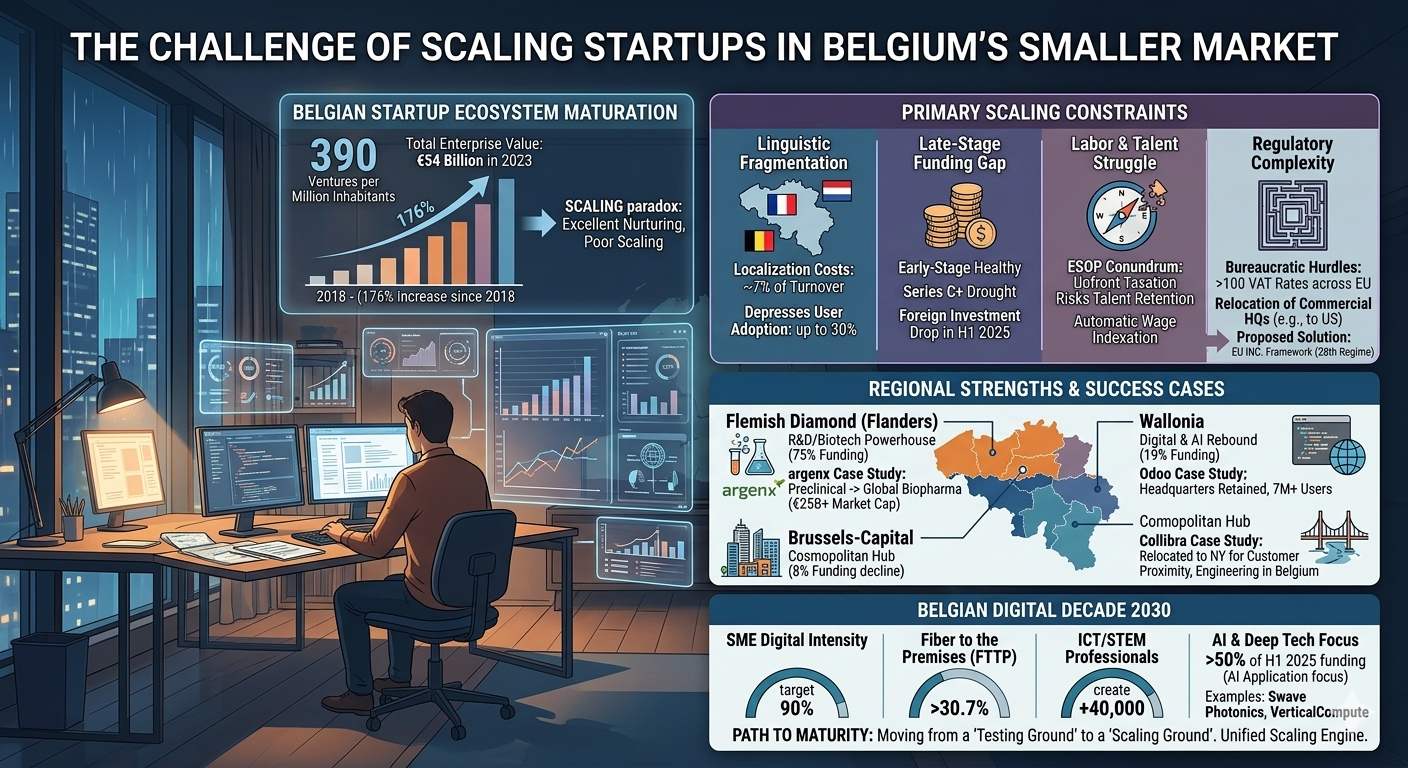

The Belgian technological landscape has entered a definitive phase of maturation, transitioning from a fragmented collection of early-stage ventures into a high-density hub of innovation that ranks among the most vibrant in the European Union. With a startup density of approximately 390 ventures per million inhabitants, the Belgian market serves as a sophisticated laboratory for technological advancement. However, this density is met by a profound structural paradox: while the nation excels at nurturing early-stage innovation through robust research and development (R&D) frameworks and world-class academic institutions, it faces persistent challenges in scaling these ventures within its own borders. The total enterprise value of the Belgian scale-up ecosystem reached €54 billion in 2023, representing a 176% increase since 2018, yet the path to international dominance remains complicated by linguistic fragmentation, late-stage funding gaps, and a regulatory environment that often necessitates the relocation of commercial activities to larger global markets.

The Belgian Paradox: Innovation Excellence vs. Scaling Constraints

The fundamental challenge for Belgian startups is the inherent limitation of a domestic market encompassing approximately 11.7 million people. This small market size forces a "born global" mindset from the day of incorporation, as domestic demand is rarely sufficient to support the hypergrowth required to achieve unicorn status. The ecosystem's success is therefore not measured by domestic market share but by its ability to export high-value technology and IP. This dynamic has created a specialized economy where the quality threshold for startups is exceptionally high, ensuring that those that do survive are resilient and prepared for international competition.

Belgium’s strategic investment in R&D, which stands at approximately 3.2% of its GDP, provides the foundational engine for this innovation. Institutions such as KU Leuven and Ghent University are consistently ranked among the top global research centers, producing a steady stream of high-tech spin-offs. However, a historical disconnect exists where high levels of R&D funding—75% of which is provided by the corporate sector—do not always translate into disruptive, consumer-facing products. This "R&D paradox" suggests that while Belgium is a leader in knowledge creation, the commercialization and scaling of that knowledge require structural reforms to the venture capital and regulatory landscape.

Comparative Startup and Scale-up Density

To understand the Belgian position, it is necessary to compare its intensity against other mid-sized OECD economies. While the United Kingdom and France maintain larger absolute numbers of startups, Belgium excels in density measures, placing it in a high-intensity group alongside the Nordic countries, Estonia, and Israel.

Ecosystem Metric | Belgium | Netherlands | Israel | United Kingdom |

Startup Density (per million) | ~390 | High Intensity | Top Global | High Concentration |

Ecosystem Value (2023/24) | €54 billion | ~€240 billion | $12.2B (Invested) | 2nd Globally |

Late-Stage Capital Access | Early-stage heavy | Foreign-dependent | Robust | Deep Pools |

Primary Scaling Challenge | Fragmentation | Talent Scarcity | Geopolitical Risk | US Retention |

The data indicates that while Belgium’s density is high, its conversion into large-scale successes lags behind ecosystems like the UK or Israel, which have successfully established more mature late-stage financing pipelines. The UK, for instance, produces far more "growing startups" relative to its population, suggesting that the Belgian environment, while fertile for planting, lacks the irrigation of late-stage capital required for full maturity.

Regional Diversification and Specialized Clusters

The Belgian ecosystem is characterized by its regional diversity, with Flanders, Wallonia, and Brussels each contributing unique strengths that are often independent of one another. This regionalization allows for specialized clusters but also introduces another layer of fragmentation that startups must navigate as they scale.

Flanders: The R&D and Biotech Powerhouse

Flanders remains the dominant engine of the Belgian startup scene, capturing nearly 75% of total national funding in 2024 and 2025. With more than 2,100 startups, the region focuses heavily on life sciences, cleantech, and advanced manufacturing. The presence of imec, a world-leading R&D hub for nanoelectronics and digital technologies, has fostered a deep-tech ecosystem that is proportionally one of the most funded in Europe. Approximately 75% of Belgium's unicorns were born in Flanders, benefiting from the region's intense academic-industrial collaborations.

Wallonia: Rebounding Through Digital and AI

Wallonia has carved out a niche in digital technologies, e-commerce, and artificial intelligence. After a period of relative stagnation, funding in Wallonia rebounded to account for 19% of the national total in the first half of 2025. The region's entrepreneurial spirit is exemplified by Odoo, a global leader in open-source business software, which has maintained its headquarters in Wallonia while scaling to over 7 million users worldwide. The Regional Investment Company of Wallonia (SRIW) plays a critical role in this ecosystem, providing the patient capital necessary for digital scale-ups to mature.

Brussels: The Cosmopolitan Connectivity Hub

As the heart of Europe, Brussels provides scale-ups with unparalleled access to international networks and regulatory talent. However, the Brussels region saw its share of national funding slip significantly from 38% in 2023 to just 8% in early 2025. This decline highlights a potential vulnerability in the capital's ability to retain high-growth firms as they move toward the Series B and C stages, where they may increasingly look toward more mature venture hubs like Paris or London.

The German-Speaking Community (Ostbelgien)

The German-speaking community, located in the east of the Liège province, represents the youngest federal entity in Belgium. Centered around hubs like Eupen and St. Vith, this community is an integral part of the Walloon economic framework but maintains its own autonomy in language and cultural matters. While its absolute population of 79,000 is small, its position at the intersection of the Netherlands, Germany, and Luxembourg makes it a strategic niche for cross-border collaboration and specialized manufacturing.

Funding Dynamics: Resilience in the Face of Correction

The Belgian venture capital market in 2024 and 2025 has been a tale of two realities. Following a record-breaking year in 2024, when the ecosystem attracted nearly €940 million in total investment, the first half of 2025 saw a 50% correction in funding volume, bringing levels back in line with 2023 stats. This decline mirrors a broader European trend of tightening capital markets but masks a high degree of resilience in the early-stage sector.

Early-Stage Resilience vs. Late-Stage Drought

In the first half of 2025, the number of recorded seed rounds in Belgium increased by nearly 50% compared to the same period in 2024. This surge suggests that local investors, particularly business angels and early-stage VC funds like Volta Ventures and Capricorn Partners, remain active and committed to the foundational layers of the ecosystem. Approximately 49% of funding rounds in Belgium involve participation from business angels, reflecting a healthy culture of non-institutional early support.

Conversely, late-stage funding (Series C and beyond) remains the "Achilles' heel" of the Belgian market. As companies mature, the average capital invested by stage has climbed—5.5x for Series B since 2018—but the frequency of these large rounds is insufficient to sustain a wide pipeline of unicorns. Furthermore, foreign investor participation dipped below 50% in early 2025, largely due to the absence of the mega-deals that typically attract US and UK-based firms.

Funding Stage | Average Growth in Invested Capital (since 2018) | Percentage of Total Belgian Capital (6-yr average) | European Average for Stage Capital |

Seed | 3.0x | High Concentration | 42% (Early Stage) |

Series A | 2.0x | 77% (incl. Seed) | - |

Series B | 5.5x | Minority Share | - |

The data confirms that Belgium is firmly in an "early maturation" phase, where it is excellent at generating a high volume of seed-funded companies but lacks the domestic firepower to transition them into global commercial leaders without significant external intervention.

The Role of AI and Deep Tech

Artificial Intelligence has emerged as the undisputed engine of growth within the Belgian tech scene. By H1 2025, funding for AI-related companies exceeded 50% of all investment in the sector. Unlike some other markets where AI is focused on foundational models, the Belgian AI scene is concentrated in the "application and implementation layer," which has attracted over 90% of AI-related funding since 2023. Large funding rounds by deep-tech companies such as Swave Photonics and VerticalCompute helped prevent the 2025 funding dip from being even more severe.

Structural Barriers: Fragmentation and the Costs of Localization

The "small market" challenge in Belgium is compounded by extreme linguistic and regulatory fragmentation. Europe as a whole is often marketed as a single market, but for a startup, it remains a mosaic of 27 different jurisdictions. For a Belgian firm, this fragmentation starts at home.

Linguistic Fragmentation as a Commercial Barrier

Belgium’s linguistic diversity—encompassing French, Dutch, and German—is a cultural asset but a commercial burden for nascent companies. Localization is not a luxury but a requirement for domestic survival. Marketing and localization costs for European startups average 7% of turnover, nearly double what US startups allocate. In Brussels, where 23 different languages are reported in the workplace, businesses must navigate a complex linguistic landscape where Dutch remains economically significant (used by 88.8% of companies for external contacts) despite its demographic minority status in the capital.

The cost of this fragmentation is significant:

Product Iteration: Geographic dispersal of teams to access linguistic talent can add 15% to operating expenses and slow product cycles by months.

Market Adoption: Linguistic barriers are estimated to depress potential user adoption by up to 30% in certain southern and eastern European regions.

Staffing: The need for multilingual staff in Belgium increases labor costs and complicates the recruitment of international talent who may find the linguistic requirements daunting.

Regulatory Complexity and the "EU Inc." Solution

Bureaucratic hurdles and administrative procedures are consistently cited as the most pressing concerns for Belgian scale-ups. Over 50% of European scale-ups identify regulatory hurdles as a critical barrier to growth. The complexity of navigating different labor laws, social security systems, and over 100 different VAT rates across Europe slows the transition from national to continental scale.

In response, there is a growing momentum for the creation of an "EU Inc."—a unified legal framework that would allow startups to incorporate once and operate seamlessly across all EU member states. This "28th regime" would reduce legal and administrative fragmentation, making it easier for companies to attract investment and scale without the need to relocate their corporate structure to the United States. Currently, around 10% of EU scale-ups eventually relocate, with most choosing the US for its unified market and deep capital pools.

Labor and Talent: The Retentional Struggle

Talent acquisition is the lifeblood of any tech ecosystem, yet 62% of European startups cite it as their primary scaling challenge. In Belgium, the problem is not a lack of skills—the workforce is highly educated and multilingual—but rather a scarcity of "scaling experience" and a tax environment that makes it difficult to reward senior operators.

The ESOP Conundrum

Employee Stock Ownership Plans (ESOPs) are a critical tool for startups to attract top-tier talent without offering high initial salaries. However, the Belgian tax regime for ESOPs is often described as a major pain point for founders. Under the Law of 26 March 1999, employees are typically taxed upfront on the value of their stock options at the time of the grant. While this can be advantageous if the company value skyrockets, it presents a significant financial risk and cash flow burden for employees who must pay tax on a benefit they have not yet realized and may never realize if the company fails.

Tax Regime Element | Standard Belgian ESOP (1999 Law) | US/UK Standard Practice |

Timing of Taxation | At Grant (60-day acceptance) | At Exercise/Sale |

Valuation Basis | Flat % (18%) of FMV | Actual Realized Gain |

Risk Profile | High (Tax paid regardless of exit) | Low (Tax paid on gain) |

Founder/Employee Alignment | Can create friction due to upfront cost | Strong alignment for long-term growth |

This upfront taxation limits the "reinvestment power" of operators and makes it harder for Belgian founders to compete for international talent from hubs like London or Berlin, where ESOP rules are more flexible and growth-oriented.

Wage Indexation and Global Competitiveness

Belgium’s system of automatic wage indexation, which links salaries to inflation, presents another challenge for startups during periods of economic tightening. While this system protects the purchasing power of employees, it places immediate pressure on the margins of manufacturing and tech companies that must compete on a global scale. During the energy crisis and inflationary periods of 2022-2023, these rising labor costs put significant pressure on the added value and competitiveness of Belgian firms, forcing them to adopt a "doing more with less" mindset and accelerating the adoption of AI-driven automation.

Fiscal Incentives: anchoring Innovation in Belgium

To offset the challenges of a small market and high labor costs, Belgium has developed some of the most attractive tax incentives for R&D and innovation in the world. These incentives are the primary reason why many scale-ups choose to keep their "technical heart" and R&D activities in Belgium even if they move their commercial headquarters abroad.

The Innovation Income Deduction (IID)

The IID is a cornerstone of Belgian fiscal policy, allowing for a deduction of 85% of the qualifying net innovation income. This effectively reduces the maximum corporate tax rate on IP-related profits to just 3.75%.

Mechanism: The IID applies to income from patents, supplementary protection certificates, and qualifying copyrighted software.

Flexibility: Unused deductions can be carried forward indefinitely, a feature that is particularly attractive for startups and scale-ups that are not yet profitable.

Nexus Approach: Following OECD guidelines, the incentive rewards companies for the actual R&D activities they conduct themselves or outsource to unrelated parties.

R&D Tax Credits and Withholding Tax Pass-Through

Belgium also offers a robust R&D tax credit, which is calculated based on the acquisition value of qualifying investments. A key advantage of this credit is that it is refundable if it remains unused for four or five consecutive tax years, providing a direct cash injection to innovation-heavy firms. Furthermore, a partial wage withholding tax (WHT) exemption allows employers to retain 80% of the WHT for employees engaged in R&D activities, significantly reducing the cost of high-level scientific and technical talent.

Case Studies: Scaling Beyond Borders

The success of the Belgian ecosystem is best understood through its "national champions"—companies that have navigated the small market constraints to achieve global leadership.

Collibra: The "Follow the Customer" Relocation

Collibra, a data governance powerhouse, moved from a slow-growth university spinoff in 2008 to a New York-based unicorn by 2019. Its strategy was rooted in proximity to its primary market: the financial services firms of New York.

Founder Relocation: CEO Felix Van de Maele stresses that for a scale-up to succeed internationally, a founder must move with the expansion to "transplant the company DNA". Hiring a local VP of Sales while staying in Europe is often a recipe for failure.

Dual Footprint: While the operational headquarters, management, and VPs are in New York, the engineering heart remains in Brussels and Poland.

Cultural Management: Scaling required Collibra to become highly "prescriptive" about its culture to manage the gap between European engineers and US sales personnel across time zones.

argenx: The "Holy Grail" of Biotech

Founded in 2008 in Ghent, argenx has transitioned from a preclinical startup into a global biopharmaceutical leader with a market cap exceeding $25 billion.

Commercial Juggernaut: In 2025, argenx achieved sustained operating profitability, with product net sales of $4.15 billion—a 90% increase from the previous year.

Capital Access: The company successfully leveraged both the Euronext Brussels and NASDAQ listings to raise the massive capital required for drug development and commercialization.

Regional Roots: Despite its global success, argenx remains deeply rooted in the Belgian R&D ecosystem, citing its relationship with European regulators and the Belgian antibody engineering talent pool as a strategic advantage.

Odoo: The Open Source Disruptor

Odoo’s strategy has been to simplify operations for millions of small and medium-sized enterprises (SMBs) through an affordable, all-in-one software suite.

Growth Model: Achieving a valuation of €3.2 billion, Odoo maintains its headquarters in Wallonia while opening half a dozen new offices worldwide and hiring 1,800 extra staff to support its 7 million users.

Ownership: Founder Fabien Pinckaers and his management team have retained 65% of the equity, resisting the pressure to sell out early—a common trend in the Belgian market.

Comparative Analysis: Belgium vs. The Netherlands and Israel

Comparing Belgium with its neighbors and other "small nation" success stories reveals distinct strategic differences.

Metric | Belgium | Netherlands | Israel |

Global Hub Ranking | #24 globally | Amsterdam #4 in EU | Global Leader |

Funding Growth (2024) | 41% increase | 25% drop (correction) | 31% increase |

Unicorns per Capita | Mid-range | High | Top Tier |

Scaling Mentality | Confident but Cautious | Largely Domestic Focus | Global Ambition |

The Netherlands faces many of the same challenges as Belgium, including talent scarcity and a low scale-up ratio—only 2 out of 10 VC-backed ventures reach the scale-up stage. However, the Netherlands has been more successful in establishing Amsterdam as a primary European hub, whereas the Belgian scene is more regionally distributed. Israel, meanwhile, serves as the benchmark for small nations, thriving on "grit" and global ambition despite geopolitical adversity, raising over $10 billion in 2024.

The Future Trajectory: Digital Decade 2030

Belgium’s digital roadmap consists of 166 measures with a budget of over €913 million, aimed at achieving the EU's Digital Decade targets. The country is already a leader in cybersecurity and online public services, with 72% of citizens reporting that digitalization is making their lives easier.

Key Strategic Objectives for 2025-2030

Infrastructure Acceleration: While gigabit coverage is strong, the primary focus is accelerating the rollout of Fiber to the Premises (FTTP), which remains below the EU average at 30.7%.

SME Digital Intensity: Reaching the 90% target for basic digital intensity among SMEs requires broader national coordination and more concrete support for cloud adoption.

Talent Development: Addressing the shortage of ICT and STEM professionals is critical. The technology industry aims to create a net 40,000 additional jobs by 2030, but success depends on reskilling initiatives and closing the gender gap in digital leadership.

Scaling Global Champions: 84% of Belgian citizens consider it important that European companies grow into "European Champions" capable of competing globally. This requires moving beyond product excellence—where Belgian scale-ups already score highly (69-73%)—toward "organizational maturity".

Conclusion: The Path Toward Sustained Maturity

The Belgian startup and scale-up ecosystem has proven its resilience and adaptability in a challenging macroeconomic climate. The transition toward a "fewer but larger" deal philosophy and the explosion of AI-related investment indicate an ecosystem that is increasingly sophisticated and globally relevant. However, the transition from a "testing ground" to a "scaling ground" remains incomplete. To fully unlock its potential, Belgium must address the structural frictions that currently drive its most promising companies to relocate.

The implementation of the "EU Inc." framework, reform of ESOP taxation, and the continued professionalization of sales and operational workflows are the necessary next steps. By leveraging its world-class R&D foundations and attractive fiscal incentives, Belgium can move beyond being a nursery for startups to becoming a permanent home for global technology leaders. The confidence remains high—67% of startup leaders are confident in their growth trajectory—but the realization of that growth will depend on transforming the Belgian paradox into a unified scaling engine for the next decade of digital innovation.

The Real Startup Playbook: Ideas, Growth, Funding, and Founder Psychology

Building a startup is exciting, chaotic, and often misunderstood. If you’ve ever wondered how founders actually validate ideas, find co-founders, raise funding, and survive the emotional rollercoaster, these articles explore the realities behind the startup world.

Start with How to Validate Your Startup Idea in 48 Hours for $0 to understand how founders test ideas quickly before wasting months building the wrong product. Once you have an idea, the next challenge is building it—From Idea to MVP: A Step-by-Step Guide for Solo Founder walks through the journey from concept to a real product.

Many founders struggle with partnerships and team decisions. Should your co-founder live in the same city? Explore Remote vs. Local: Does Your Co-Founder Need to Live in the Same City? and learn the risks hidden in partnerships in 5 Red Flags to Look for When Choosing a Startup Partner. If you’re searching for technical help, How to Find a Technical Co-Founder (Without a Six-Figure Salary) explains how founders actually do it.

The startup journey isn’t just about building products—it’s also about mindset and decision-making. Articles like Decision Fatigue: The Silent Startup Killer, Fear vs Logic: How Founders Actually Make Decisions, and How Overthinking Destroys Early Momentum reveal the psychological battles founders face behind the scenes.

Growth is another misunderstood part of startups. Learn why strategy matters more than hype in Ideas Don’t Scale. Systems Do. and why discipline matters in Why Your Startup Doesn’t Need Growth — It Needs Focus. Discover the importance of early traction in How the First 100 Users Decide Your Startup’s Fate and understand team building through The First Hire That Actually Matters.

Funding is often romanticized, but reality is more complex. Why First-Time Founders Should Avoid Big Funding challenges common assumptions about venture capital, while Revenue Solves More Problems Than Funding explains why sustainable businesses matter more than investor money.

The startup ecosystem also varies by geography. If you're curious about India’s startup scene, explore The New Playbook for Raising in Bangalore, Why Raising Pre-Seed in Bangalore Is Harder Than Ever, and Why B2B SaaS from Bangalore Scales Faster.

But startups are not just about strategy and growth—they’re also about people and emotions. Articles like The Hidden Burnout of Bangalore Founders, Comparison Culture in India’s Startup, and The Loneliness of First-Time Founders in Bangalore reveal the personal struggles founders rarely talk about publicly.

And finally, if you want a deeper perspective on the startup journey itself, explore Lessons Learned Too Late by First-Time Founders and The Myth of the “Overnight Success” Startup—because the truth behind startup success is far more complex than it appears.