How the US-China Tech Tensions Affect Global Startups

June 29, 2026 by Harshit Gupta

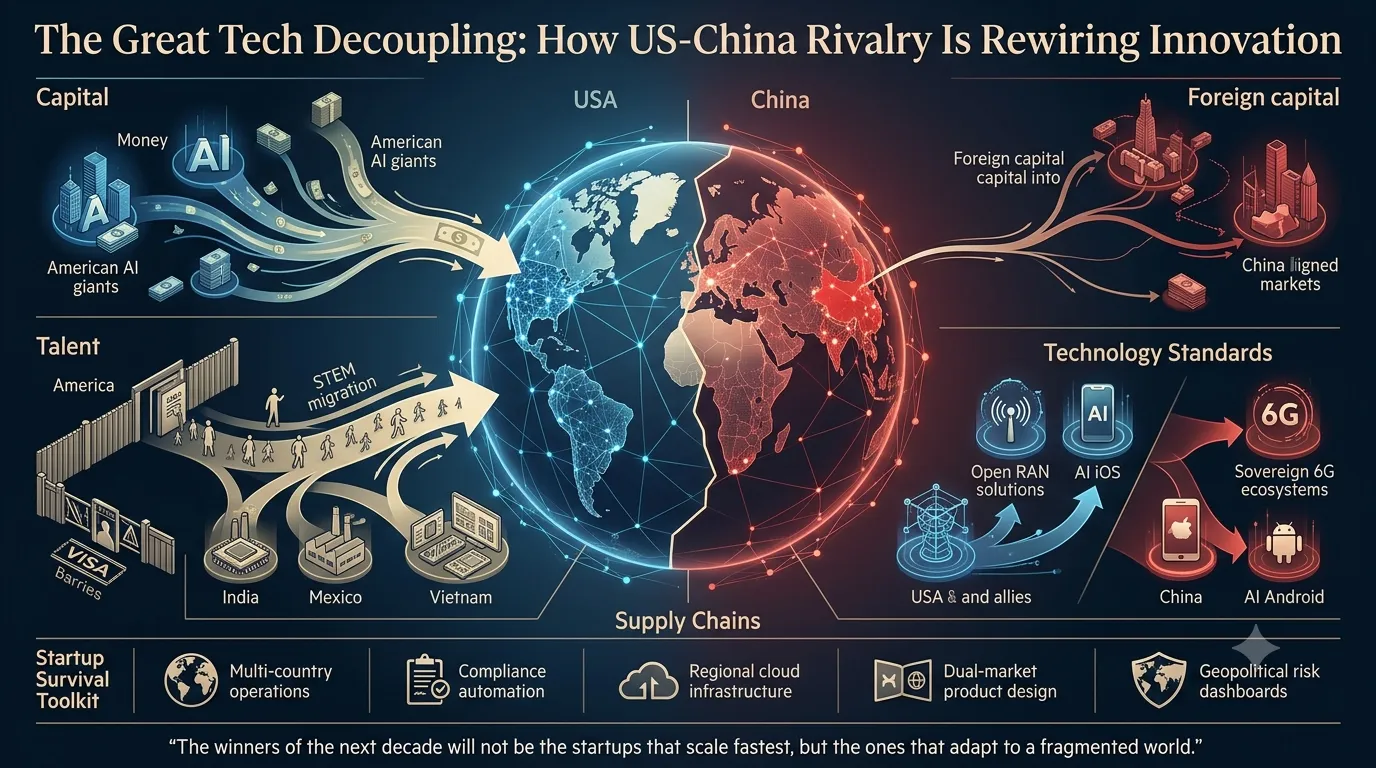

The global technology landscape is currently traversing a structural inflection point that marks the end of the post-Cold War era of laissez-faire digital integration and the dawn of a regime defined by geoeconomic statism. In 2025 and 2026, the intensifying rivalry between the United States and the People’s Republic of China has evolved from a series of tactical trade skirmishes into a comprehensive, strategic "tug of war" over the foundational pillars of the twenty-first-century economy: artificial intelligence, semiconductor fabrication, quantum computing, and high-speed telecommunications. For global startups, this shift represents a fundamental reconfiguration of the risk-reward calculus that has governed innovation for three decades. The emergence of parallel, often incompatible, technological ecosystems—frequently categorized as technological bifurcation—is forcing emerging enterprises to navigate a labyrinth of export controls, investment screenings, and diverging technical standards that threaten the very concept of the "born global" startup.

Financial Fragmentation and the Shift in Global Venture Capital

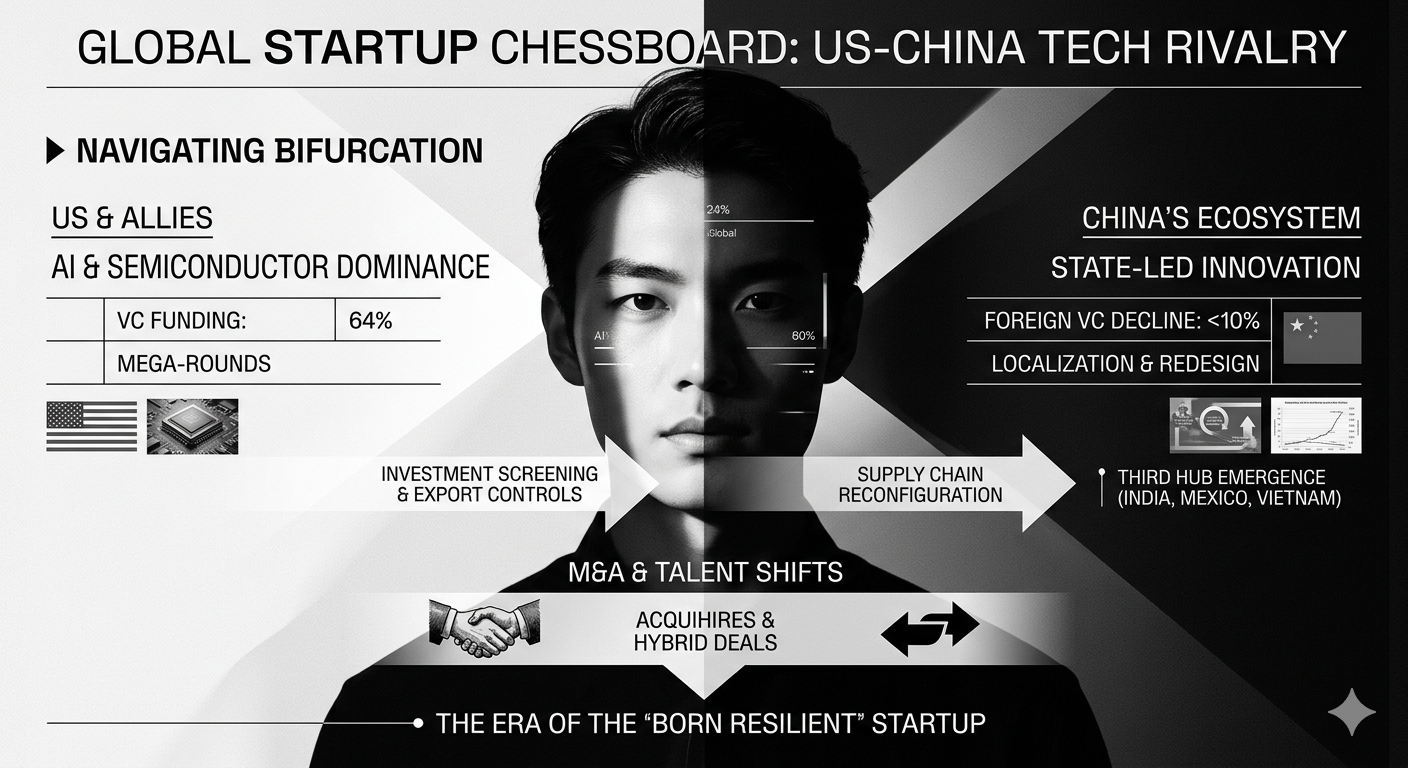

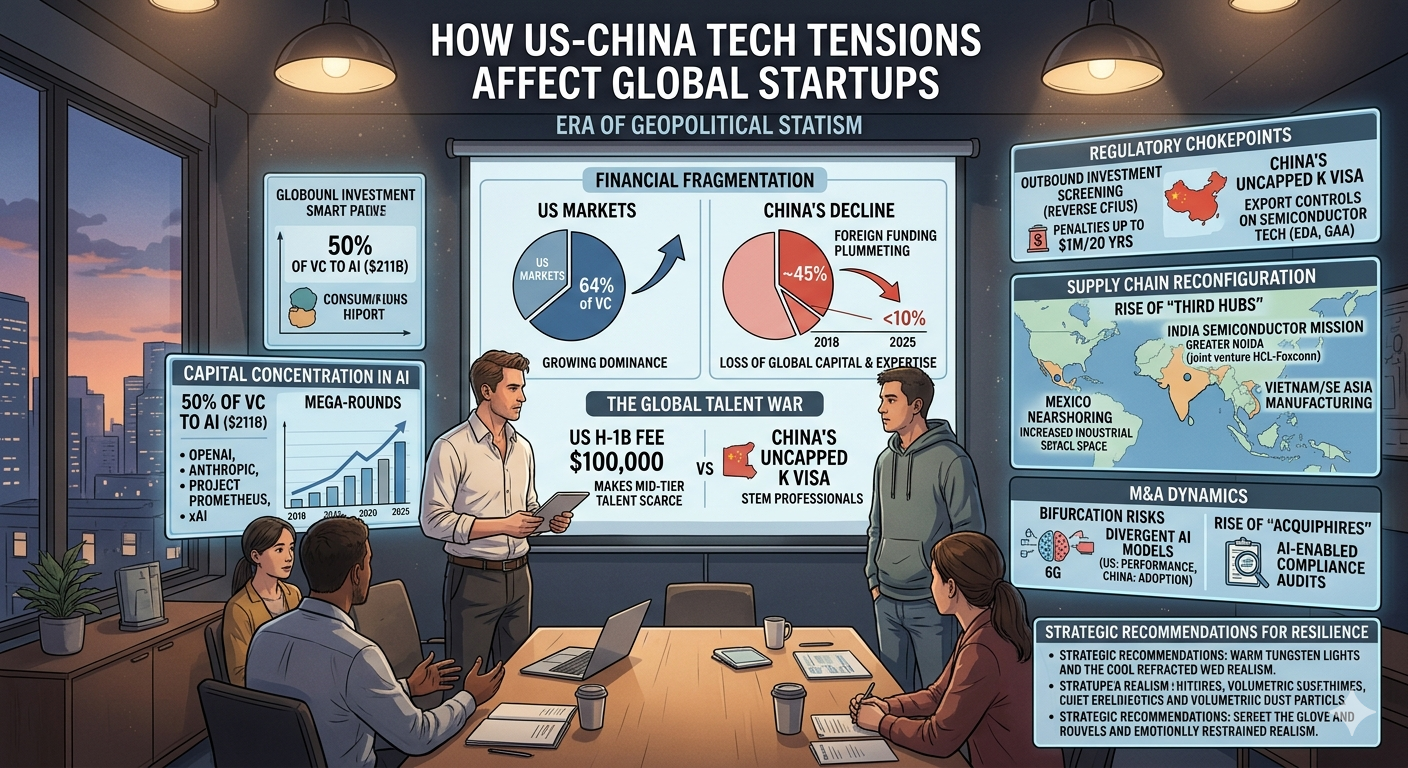

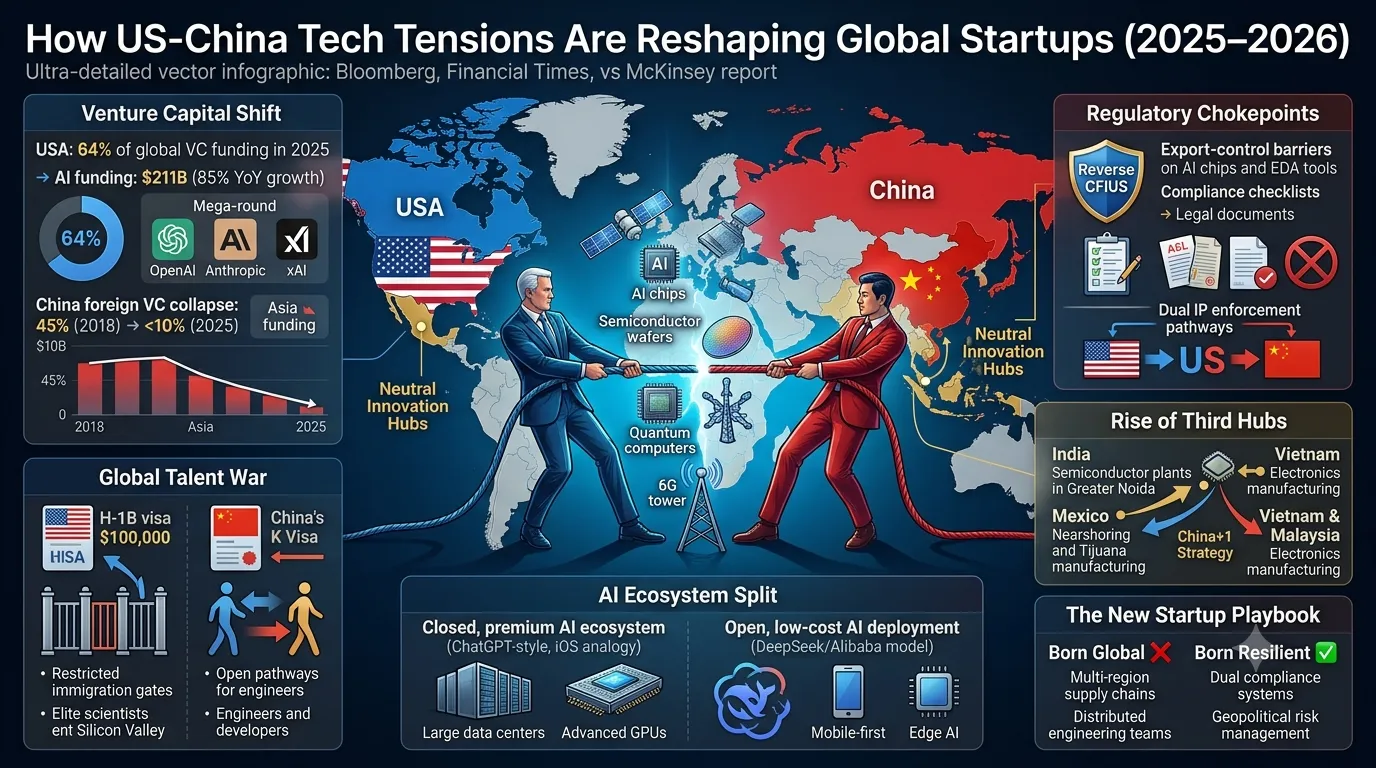

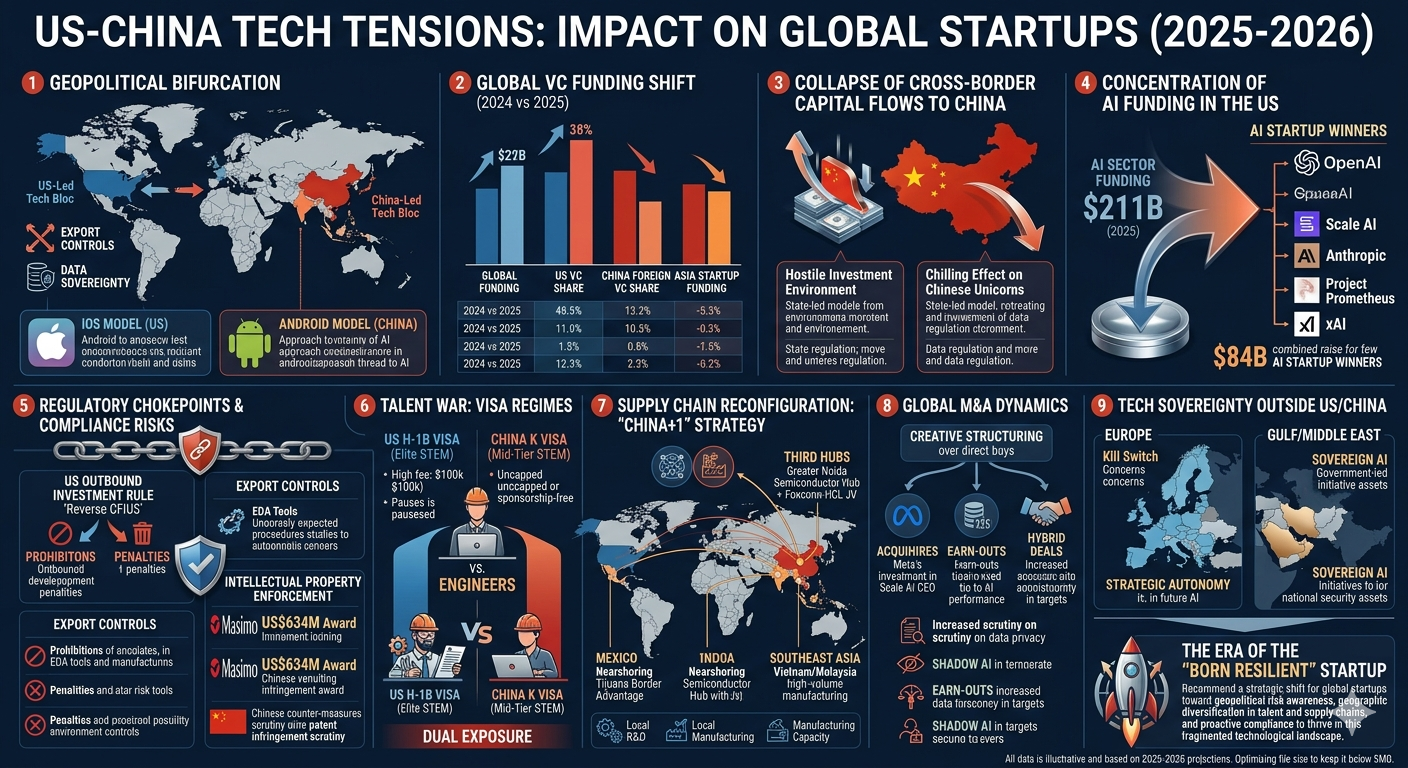

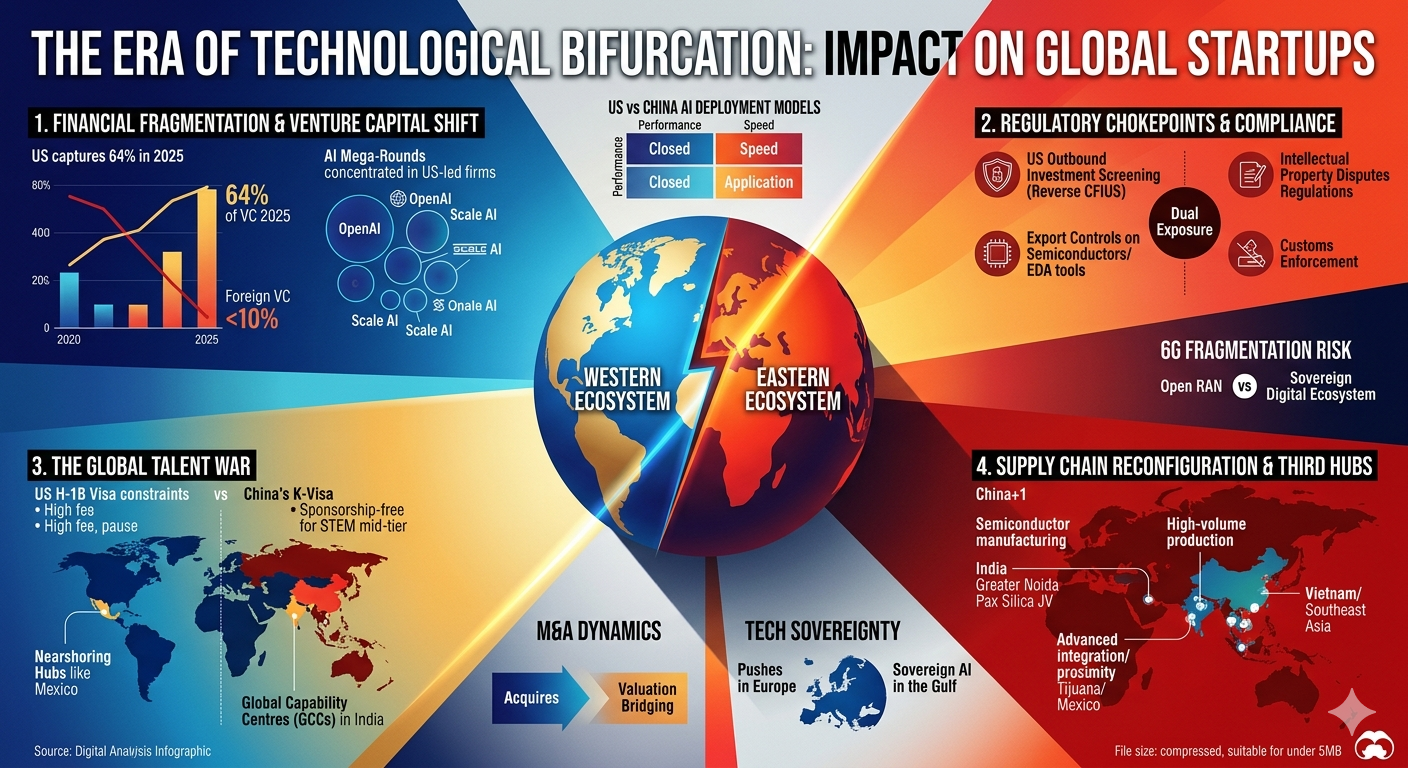

The venture capital environment in 2025 reflects a stark geographic and sectoral divergence, characterized by a flight to perceived safety in the United States and a precipitous withdrawal from the Chinese market. While global venture funding reached approximately $512.6 billion in 2025, a rebound following several years of malaise, this liquidity is concentrated in a "magnificent few" sectors and geographies. The United States has solidified its dominance, capturing 64% of global startup funding in 2025, a significant increase from 56% in 2024.

The Collapse of Cross-Border Capital Flows to China

The deteriorating relationship between Washington and Beijing has created an increasingly hostile environment for cross-border investment, fundamentally altering the innovation landscape in China. By 2025, foreign venture capital funding in China plummeted to less than 10% of total investment, a dramatic fall from 2018 when it accounted for nearly half of all capital inflows. In the first eight months of 2025 alone, foreign funding amounted to a mere $6.6 billion. This decline is not merely financial; it represents a fundamental shift in the risk appetite of global institutional investors who once viewed China as the ultimate growth frontier.

The implications for Chinese "unicorns" and high-growth startups are severe. Deprived of global capital and the operational expertise that typically accompanies it, these firms are increasingly forced into a state-led model that prioritizes political loyalty and strategic alignment over market efficiency. This transition has a chilling effect on entrepreneurial risk-taking, as startups are trapped in a bureaucratic maze of data regulations, censorship, and cross-border collaboration restrictions. The resulting inefficiency and reduced competitiveness threaten to slow China’s progress in industries critical to its future survival, such as advanced biotech and high-end semiconductors.

The Concentration of Capital in US-Led Artificial Intelligence

While the Chinese ecosystem becomes more self-contained and state-reliant, the US market has seen a surge in "mega-rounds," particularly in the artificial intelligence sector. In 2025, AI-related fields accounted for roughly 50% of all global venture funding, reaching $211 billion. This represents an 85% year-over-year increase from 2024. The concentration of value is unprecedented; five companies—OpenAI, Scale AI, Anthropic, Project Prometheus, and xAI—raised a combined $84 billion in 2025, representing 20% of all venture capital deployed globally that year.

The following table illustrates the dramatic shift in venture capital distribution between 2024 and 2025, highlighting the growing disparity between the US and Asian markets.

Metric | 2024 Data | 2025 Data | Trend/Analysis |

Global Venture Funding | $328 Billion | $512.6 Billion | 56% Increase |

US Market Share of VC | 56% | 64% | Increasing Dominance |

AI Sector Funding | $114 Billion | $211 Billion | 85% Sector Growth |

China Foreign VC Share | ~45% (2018) | <10% | Sharp Structural Decline |

China Total VC Investment | $63.5 Billion | $40.2 Billion | 36.7% Annual Decline |

Asia-wide Startup Funding | $71.8 Billion | $67.5 Billion | 6% Regional Decline |

This concentration of capital suggests a "winner-take-all" dynamic where a small group of perceived winners absorbs the majority of available capital, leaving the long tail of startups under significant pressure. For startups outside the AI gold rush, fundraising remains subdued, and the path to liquidity is increasingly defined by M&A rather than a robust IPO market. In 2025, only $1.6 billion was raised from nine biopharma IPOs, compared to $3.8 billion from 19 in 2024, marking the lowest IPO capital raise in five years.

Regulatory Chokepoints and Compliance as a Strategic Asset

The escalation of tech tensions has manifested in a series of regulatory measures that act as chokepoints for global startup operations. These measures are no longer purely defensive; they are increasingly designed to hamper the technological advancement of rivals, marking a departure from traditional "small yard, high fence" doctrines toward more expansive geoeconomic competition.

Outbound Investment Screening: The "Reverse CFIUS"

One of the most significant regulatory shifts is the implementation of the US Outbound Investment Rule, which became effective on January 2, 2025. Unlike the Committee on Foreign Investment in the United States (CFIUS), which screens inward investment for national security concerns, this "reverse CFIUS" prohibits or requires notification for US investments in "countries of concern"—currently China, Hong Kong, and Macau—related to three key capabilities: semiconductors and microelectronics, quantum information technologies, and artificial intelligence.

The rule operates more like a sanctions regime than a screening mechanism, prohibiting and criminalizing certain transactions rather than offering a pre-clearance process. It places the entire burden of due diligence on the investor, requiring them to conduct a "reasonable and diligent inquiry" to determine if a transaction involves a "covered foreign person". Failure to comply carries significant penalties, including civil fines of up to twice the value of the transaction or $360,000, whichever is greater, and criminal penalties of up to $1 million and 20 years in prison for willful violations. For US-based startups or venture funds with global ambitions, this creates a significant "chilling effect," discouraging even mundane international activities such as hiring sales teams in foreign markets for fear of triggering regulatory tripwires.

Export Controls and Intellectual Property Enforcement

The US has also broadened export controls to include the software, tools, and talent necessary to manufacture modern semiconductors. By 2026, semiconductor technologies such as etching, gate-all-around (GAA) transistors, and electronic design automation (EDA) tools have become critical supply chain chokepoints. These controls target the machines and the talent necessary for manufacturing modern chips, aiming to freeze China’s development at current levels. For instance, US restrictions on EDA tools—vital for compute-intensive generative AI workloads—have forced foundries in non-allied countries to either rely on older, less efficient nodes or attempt to develop domestic EDA capabilities, both of which stretch product cycles and dent competitiveness.

In response, China has strengthened its own enforcement mechanisms. On May 1, 2024, the State Council’s Regulations on the Handling of Foreign-Related Intellectual Property Disputes took effect, echoing the US International Trade Commission’s (ITC) approach to investigating IP violations in imported goods. This creates a "dual exposure" for global startups: a product redesign made to comply with US exclusion orders may still face scrutiny or exclusion under Chinese customs enforcement. Startups must now anticipate enforcement actions in both jurisdictions simultaneously, often requiring separate design modifications or licensing arrangements to maintain access to both markets. The Masimo US$634 million patent infringement award in late 2025 highlights how Section 337 actions, combined with related court proceedings, can significantly disrupt even the largest global corporations and the startups that supply them.

The Global Talent War: Visas and the STEM Migration

The competition for innovation is increasingly mirrored in the competition for human capital. As both the US and China implement more restrictive or strategically targeted immigration policies, the traditional patterns of tech talent migration are fracturing, with profound implications for startup scalability.

The Prohibitive Cost of US H-1B Visas

On September 19, 2025, the US administration introduced a $100,000 application fee for new H-1B skilled worker visas. For a startup, this fee makes hiring international talent nearly cost-prohibitive. For example, hiring a talented developer with a $90,000 salary would now incur a first-year cost exceeding $190,000 when the visa fee is included, before factoring in benefits or management overhead. This policy effectively reserves the H-1B pathway for a narrow slice of applicants: elite researchers, specialized architects, and senior technical leaders whose contributions clearly justify the investment.

The practical effect is a "hollowing out" of the mid-tier engineering talent pool in the US startup ecosystem. Startups are increasingly taking a "pause" or opting to cancel H-1B sponsorship programs altogether, even for in-demand roles like AI, DevOps, or Cybersecurity engineers. Adding to this pressure, the US State Department announced an indefinite pause to immigrant visa processing for nationals of 75 countries in January 2026, affecting major talent sources such as Brazil, Colombia, Nigeria, and the Philippines.

China's Counter-Move: The K Visa and Talent Luring

Capitalizing on the growing disillusionment with US visa restrictions, China launched its "K visa" in October 2025. This uncapped, sponsorship-free work visa targets STEM professionals, allowing them to reside in the country before securing a job offer. By targeting the "much larger pool of capable mid-tier engineers and developers," China aims to capture the talent that the US is increasingly excluding.

The following table compares the two primary visa regimes currently shaping the global talent market for startups.

Feature | US H-1B Visa (2025/26) | China K Visa (2025) |

Application Fee | $100,000 | Standard/Low-cost |

Cap/Quota | Capped annually | Uncapped |

Sponsorship Requirement | Employer-driven | Sponsorship-free |

Target Demographic | Elite Researchers/Architects | Mid-tier STEM Professionals |

Key Hurdle | Financial cost/Processing pause | Language/Work culture (996) |

The result of these divergent policies is a bifurcated talent map. While the US remains the destination for the top 1% of researchers and architects, China is positioning itself as a hub for the engineers who drive the practical deployment of AI and other emerging technologies. Startups are responding by exploring offshoring or nearshoring markets to access high-quality developers without the prohibitive costs of US sponsorship.

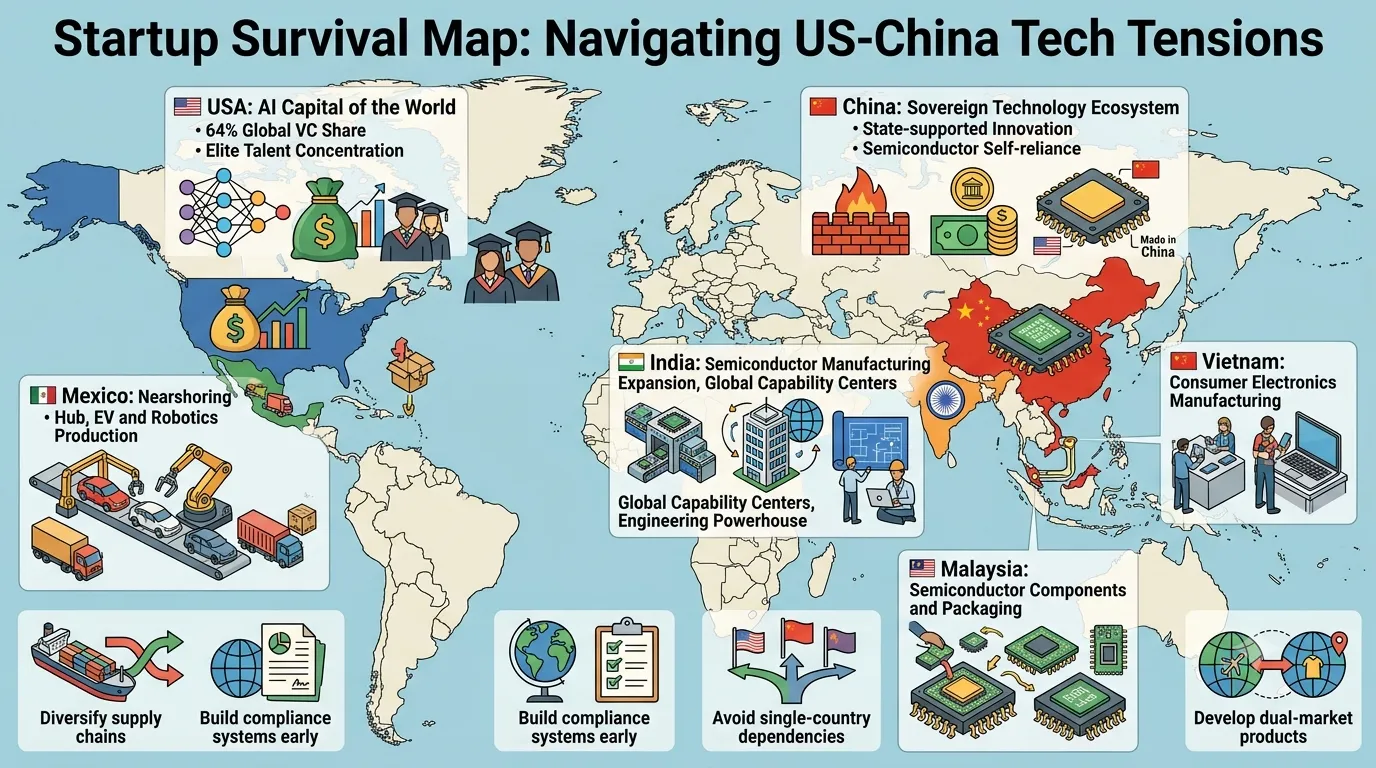

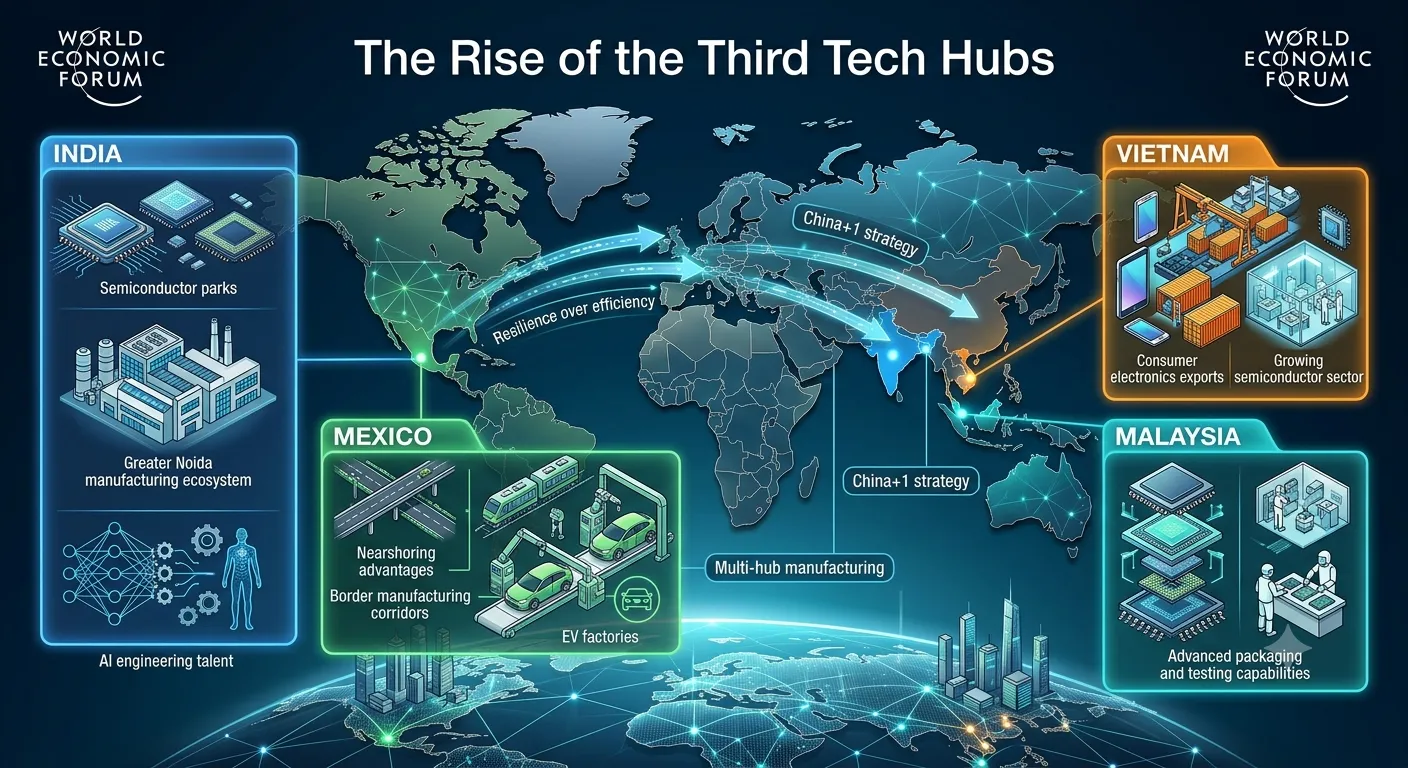

Supply Chain Reconfiguration and the Rise of "Third Hubs"

The pursuit of "China-free" or "blue" supply chains is driving a massive structural shift in global manufacturing and network design. The traditional model of a single, centralized supply base in Asia feeding Western markets is rapidly being replaced by a multi-regional, multi-hub architecture. This reconfiguration offers both challenges and opportunities for hardware and electronics startups, particularly in regions like India, Mexico, and Southeast Asia.

The India Opportunity: Pax Silica and Greater Noida

India has emerged as a critical player in this reshaping global ecosystem, leveraging its unmatched scale of tech talent and strategic geopolitical positioning. In February 2026, India formally joined "Pax Silica," a US-led initiative focused on securing supply chains for semiconductors, AI infrastructure, and critical minerals. This alliance, which includes nations like Japan, Singapore, and the UK, targets the development, funding, and deployment of advanced technologies while reducing dependence on China.

The state of Uttar Pradesh, particularly the Yamuna Expressway region in Greater Noida, is rapidly transforming into a semiconductor hub. A center-piece of this effort is a ₹3700-crore ($440 million) project by India Chip Private Limited, a 60:40 joint venture between India's HCL Group and Foxconn. This facility, an Outsourced Semiconductor Assembly and Test (OSAT) plant, is expected to be operational by 2028 and has a planned capacity to process 20,000 wafers per month. The presence of such anchor projects is already attracting ten other companies—including Vivo, Sify, and Dixon Technologies—to purchase land in the region, fostering a nascent startup ecosystem in chip design and R&D.

Mexico and the Nearshoring Advantage

Mexico has also seen significant gains as US manufacturers seek to localize production to build long-term resilience. In 2023, Mexico overtook China as the top exporter of manufactured goods to the US. Tijuana, in particular, is emerging as a strategic complement to traditional chip fabrication hubs. Its "border advantage" and time zone alignment allow for real-time collaboration between US-based engineering teams and Mexico-based production facilities, significantly reducing the operational friction associated with distant offshore models.

By 2026, industrial building availability in Tijuana and Monterrey has tripled, facilitating the expansion of electric vehicle (EV), robotics, and medical device manufacturing. For hardware startups, Mexico offers a rare combination of technical capability, proximity to the US market, and workforce stability, allowing them to scale specialized processes from concept through testing more efficiently than in traditional Asian hubs.

Vietnam and the Southeast Asian Manufacturing Shift

While India and Mexico focus on advanced integration and proximity, Southeast Asia—led by Vietnam and Malaysia—is emerging as a high-volume manufacturing cluster. Vietnam’s semiconductor market is projected to reach USD 3.14 billion in size by 2026, driven by sustainable growth and increasing foreign investment in consumer electronics. Malaysia is simultaneously growing as a semiconductor and high-tech component hub, while Thailand gains traction in automotive and EV production.

For startups, the shift to these regions requires a more sophisticated supply chain strategy. Companies are reducing single-country dependence and spreading operations across several APAC markets to improve resilience. This "China+1" strategy is no longer a luxury but a requirement for demonstrating resilience in financial reporting and audits.

Technological Standards and AI Sovereignty: A New Frontier

As the focus of US-China competition shifts from hardware to the software, data, and standards that govern it, the risk of global fragmentation increases. This is particularly evident in the development of 6G telecommunications and the contrasting deployment models for artificial intelligence.

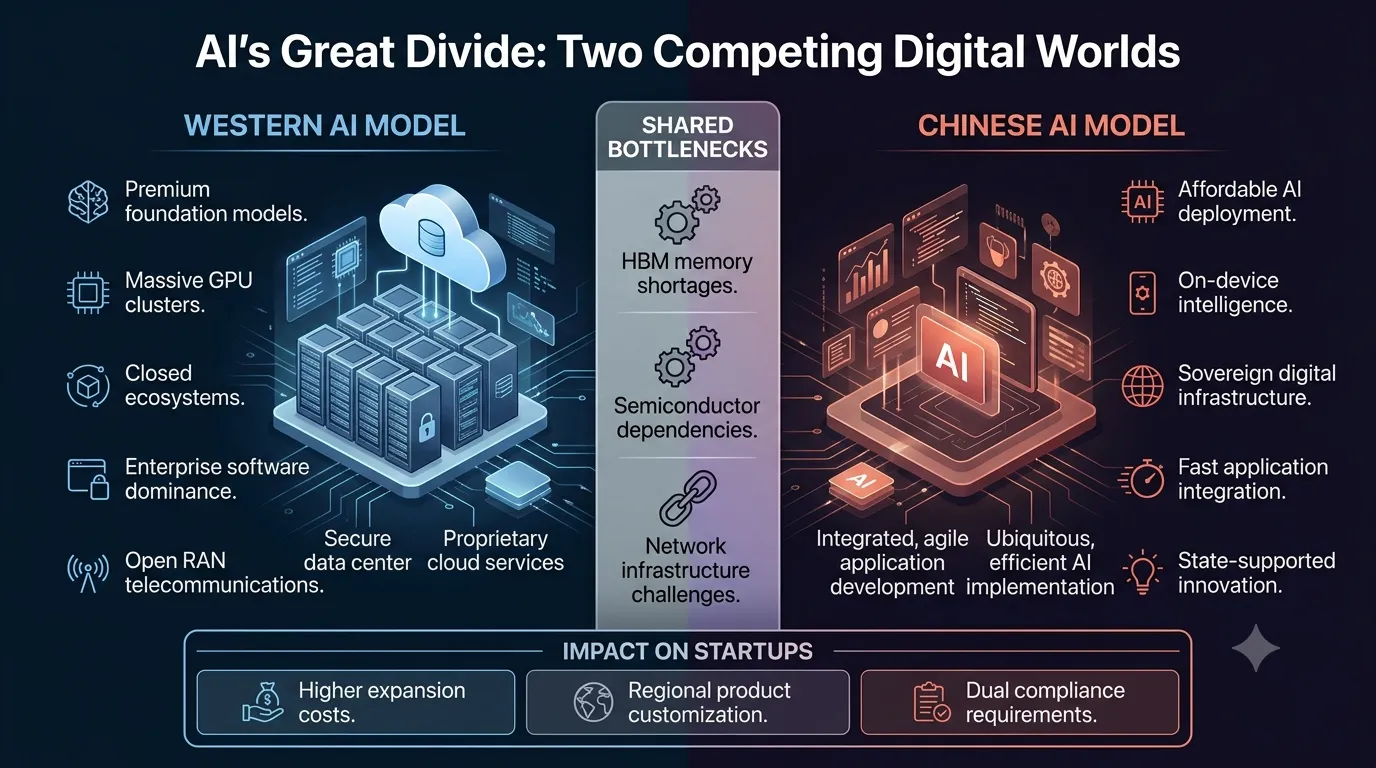

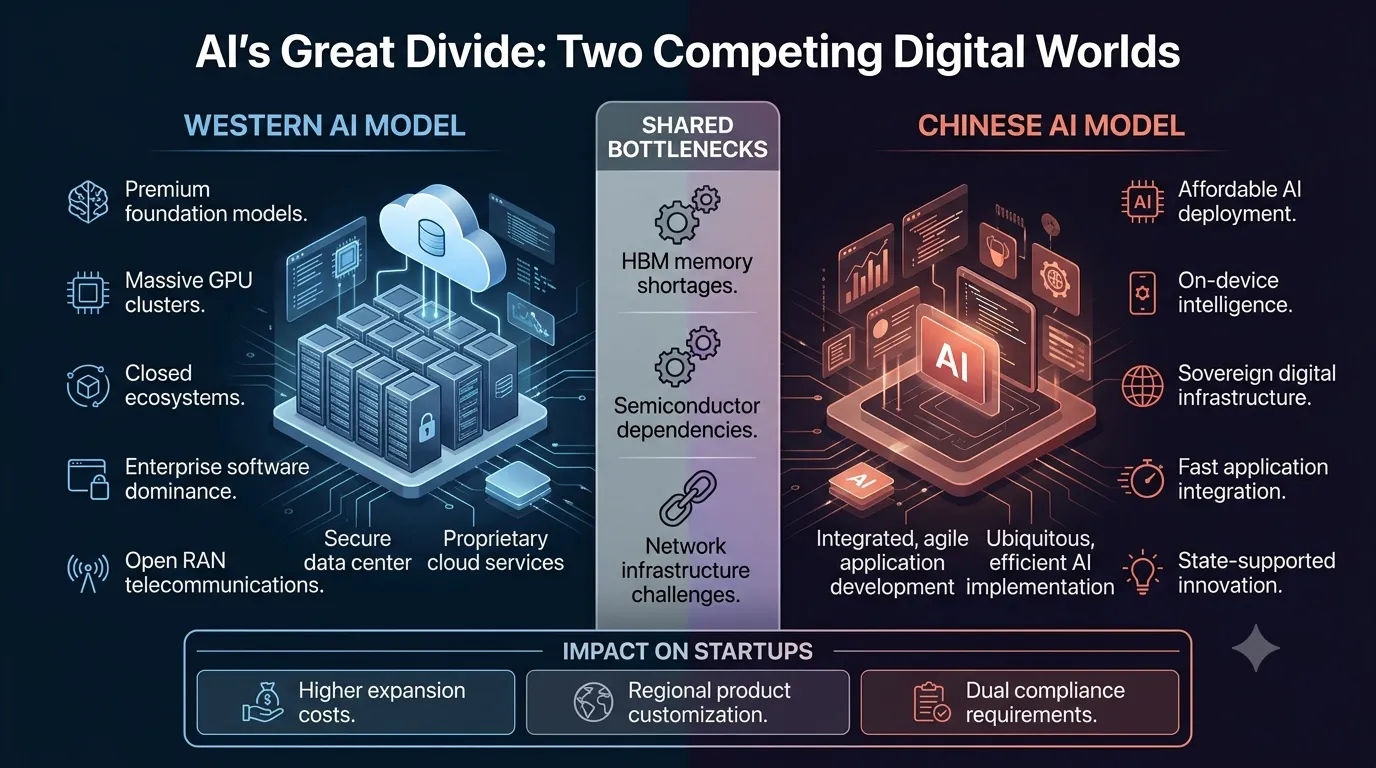

Divergent AI Deployment Models: iOS vs. Android

The US and China are pursuing fundamentally different approaches to AI development, which some analysts compare to the "iOS vs. Android" models. The US AI industry seeks optimal model performance and end-to-end control, with generative models like Gemini and ChatGPT commanding premium pricing to compensate for superior computational horsepower and security. This "closed" ecosystem approach aims to accrue value as competitive moats deepen over time.

In contrast, the Chinese industry focuses on spreading technology quickly at a lower cost, threading it into myriad applications. Models from companies like DeepSeek and Alibaba aim for "good enough" performance and fast customization, focusing on on-device or hybrid deployment to monetize more quickly through rapid adoption. However, both ecosystems face common "choke points," specifically in memory chips and network connectivity. Prices for legacy DRAM and flash memory chips may rise as much as 20% to 50% in early 2026 as manufacturers shift production to high-bandwidth memory (HBM) to meet the AI boom.

The 6G Fragmentation Risk

The rollout of 6G, anticipated in the early 2030s, represents the next major "game changer," with the potential to generate well over $50 billion in the first five years. However, the development of these standards is bifurcating along geopolitical lines.

The Western Vision: The US, EU, Japan, and South Korea are promoting "Open RAN" models—open and interoperable systems based on shared interfaces that encourage competition and lower costs.

The Chinese Vision: China is developing a "sovereign digital ecosystem," focusing on an integrated system that allows for consistent performance and greater sovereign control.

If these two visions cannot be reconciled through global bodies like 3GPP, the result could be a "costly purchase of new devices or tricky modifications" as smartphones and IoT devices designed for one standard become incompatible with networks following the other. For startups in the communications and IoT space, this fragmentation increases the cost of global expansion and creates significant uncertainty regarding which standard will dominate in specific regional blocks. China already holds among the world's highest number of patents for 6G-related technology, such as channel coding and intelligent surfaces, and conducted the world's first 6G test satellite launches between 2020 and 2024.

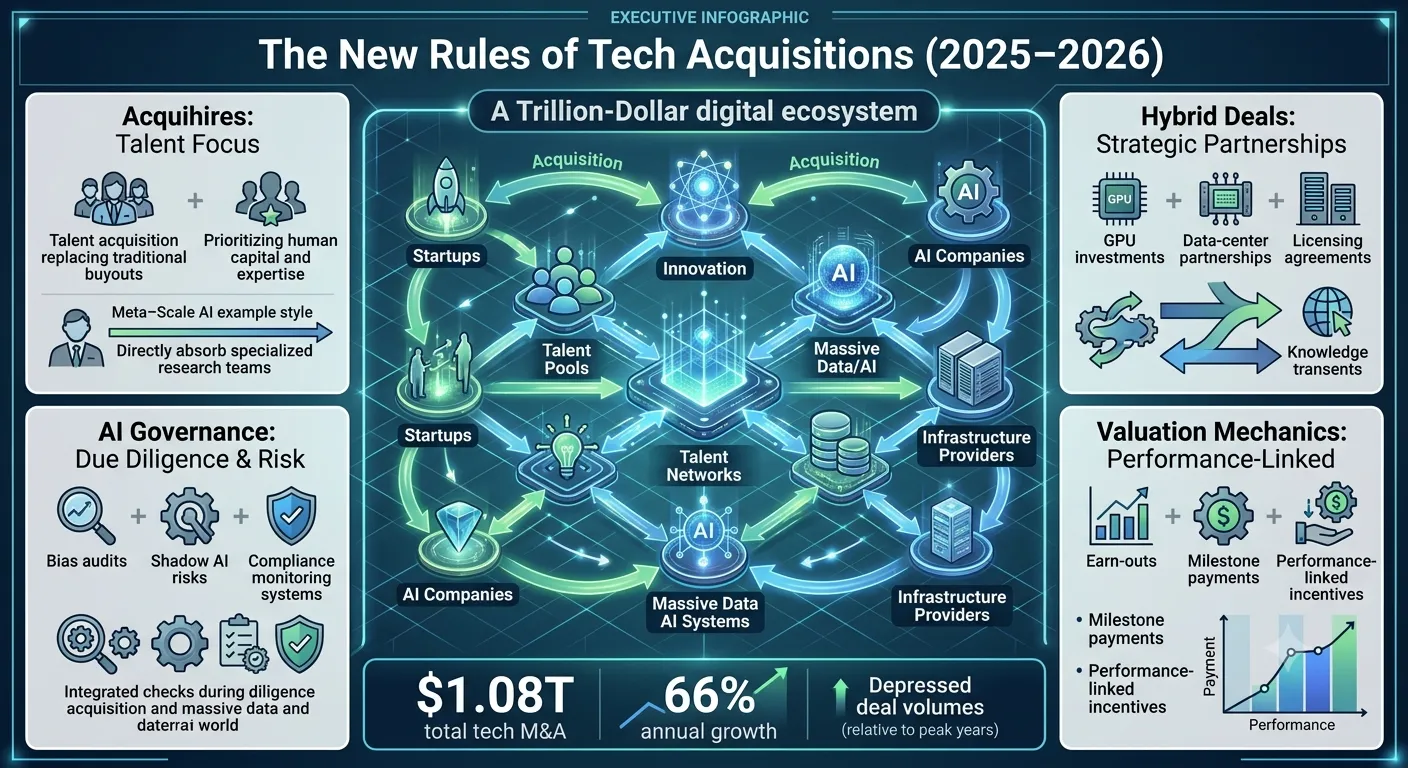

M&A Dynamics and the "Acquihire" Strategy

In a market defined by high valuations, intense talent competition, and regulatory scrutiny, the nature of technology M&A is evolving. Total technology M&A value rose 66% in 2025 to $1.08 trillion, yet deal volume remained depressed as investors exercised continued discipline.

The Rise of "Acquihires" and Creative Structuring

Regulators in both the US and Europe have intensified their scrutiny of large platform acquisitions of elite researchers and engineers to prevent anti-competitive talent hoarding. To circumvent these hurdles, many companies have turned to "acquihires"—hiring key talent and making significant investments or licensing arrangements without acquiring the entire company. A notable example is Meta’s $14.3 billion investment in and "hiring" of the CEO of Scale AI in 2025.

2026 is expected to see an increase in "hybrid deals" that involve talent, infrastructure financing (such as data centers and GPUs), and strategic partnerships rather than traditional corporate control transactions. For startups, this means the exit strategy may no longer be a straightforward buyout but a complex series of licensing deals and talent transfers that preserve some level of independent capitalization. Furthermore, the use of earn-outs and performance-linked covenants—centered on model quality, safety, or uptime—has become essential to bridge the gap between AI "hype" and actual cash flows.

AI-Enabled Compliance and "Shadow AI" Risks

M&A targets are also facing heightened scrutiny over their internal use of AI. In 2025, tools for automated hiring began to draw significant regulatory attention due to concerns about algorithmic discrimination. New York City's automated hiring law, for example, requires annual bias audits, and buyers are now pressure-testing whether targets have adequate governance structures to manage "Shadow AI"—the use of unapproved AI tools by employees that can lead to data leakage and privacy violations.

The following table summarizes the key M&A trends affecting startups in the 2025-2026 period.

Trend | Description | Impact on Startups |

Acquihire at Scale | Large platforms buying talent, not the entity | Complex exits; talent-only valuations |

Valuation Bridging | Use of earn-outs and milestone payments | Extended payout periods for founders |

AI Governance Audits | Scrutiny of internal AI use and bias | Increased pre-deal due diligence costs |

Infrastructure JVs | Strategic investments in GPU/Data centers | New funding models for compute-heavy firms |

Cross-Border Licensing | R&D partnerships with China-based firms | Landmark deals like GSK-Hengrui ($12.5B) |

The Challenge of Tech Sovereignty in Europe and the Middle East

The US-China rift is forcing other major economic blocs to pursue their own versions of "tech sovereignty," which in turn creates a more fragmented market for startups to navigate.

Europe's "Kill Switch" Concerns and Strategic Autonomy

European companies have expressed significant concern that President Trump’s foreign policy could lead to a "tech decoupling" between the US and Europe. This has sparked discussions about a "kill switch" scenario in which the US government could require American technology companies to suspend services to European customers through sanctions or export controls. While many executives consider this unlikely, it has driven a push for "tech sovereignty" in the region.

However, European industries—including banking and manufacturing—face a difficult trade-off. Shifting away from US-based cloud infrastructure, office software, and AI services is not only expensive but could cause massive operational disruption. Replacing these systems would involve retraining employees, rewriting software, and renegotiating thousands of contracts. Consequently, many European carmakers and German government officials suggest focusing "tech sovereignty" primarily on future initiatives, such as AI, rather than attempting to replace existing foundational business operations.

Sovereign AI in the Gulf and Middle East

In the Middle East, particularly the Gulf, governments are intensifying efforts to build nationally controlled cloud platforms and AI infrastructure. These sovereign AI initiatives are seen as a lever for productivity and a defense against the volatility of global tech trade. For startups in this region, the priority is shifting toward defense analytics, cybersecurity applications, and nationally aligned digital platforms. Unlike traditional IT spending, AI investment in the Gulf is likely to prove more resilient to economic shocks, as it is viewed as a national security asset rather than a discretionary expense.

Conclusion: Strategic Recommendations for Global Startups

The US-China tech tensions have created a world where resilience has overtaken efficiency as the primary driver of corporate strategy. For global startups, navigating this landscape requires a fundamental shift in how they manage capital, talent, and technology.

Navigating the Dual-Standard Reality

Startups can no longer assume a single global standard for their products. The emergence of parallel enforcement systems in the US and China requires a "dual-track" approach to intellectual property and compliance. Companies must anticipate enforcement actions in both jurisdictions simultaneously, which may require separate design modifications or licensing arrangements to maintain access to both markets.

Building Geographic Risk-Awareness into Talent

The prohibitive cost of US H-1B visas and the lures of the Chinese K-visa suggest that the talent market is becoming geographically stratified. Startups should explore offshoring or nearshoring to markets like Mexico, India, or Eastern Europe early in their lifecycle to avoid the "visa trap". Furthermore, the rise of Global Capability Centres (GCCs) in India offers a model for scaling R&D and engineering talent without the strategic risks of a Chinese footprint.

Supply Chain Resilience through Hub-and-Spoke Models

The shift toward multi-hub supply chain architectures—as seen in the India Semiconductor Mission and Tijuana’s nearshoring cluster—allows startups to move beyond distant, high-risk offshore models. By co-locating suppliers, manufacturers, and logistics providers in regional hubs, startups can gain the speed and flexibility necessary to respond to geopolitical disruptions and tariff volatility.

Preparing for "Sanctions-Style" Investment Screening

The implementation of the US Outbound Investment Rule marks a permanent change in the relationship between government and business. Founders and venture capital funds must incorporate sophisticated outbound investment screening into their due diligence processes and develop new contractual language to reflect the representations required by these regulations. The cost of doing business is no longer just about market entry; it is about the compliance burden of maintaining a "China-free" or "US-aligned" technology stack.

In summary, the startups that will thrive in the era of US-China tech tensions are those that treat geopolitical risk as a core component of their product and business architecture. The era of the "born global" startup is being replaced by the era of the "born resilient" startup, where strategic autonomy and the ability to operate across bifurcated ecosystems are the new markers of success.

Want to calculate the equity for your cofounder?

Nail your cap table before you sign. Whether you're splitting equity with a co-founder or planning your next funding round, our Equity Calculator gives you precision in seconds

Equity calculator →