Why Indian Startups Must Think Global from Day One

July 1, 2026 by Harshit Gupta

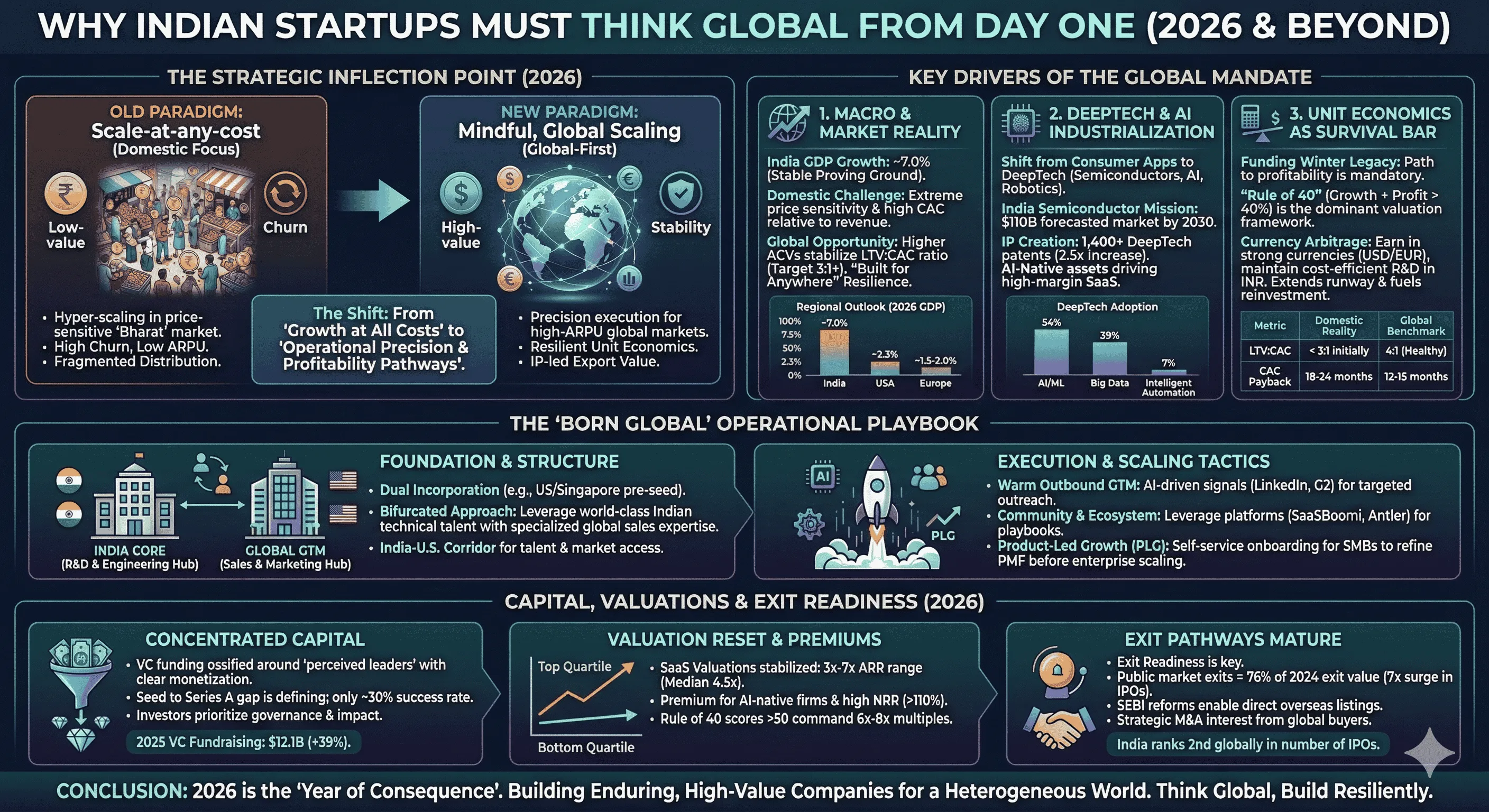

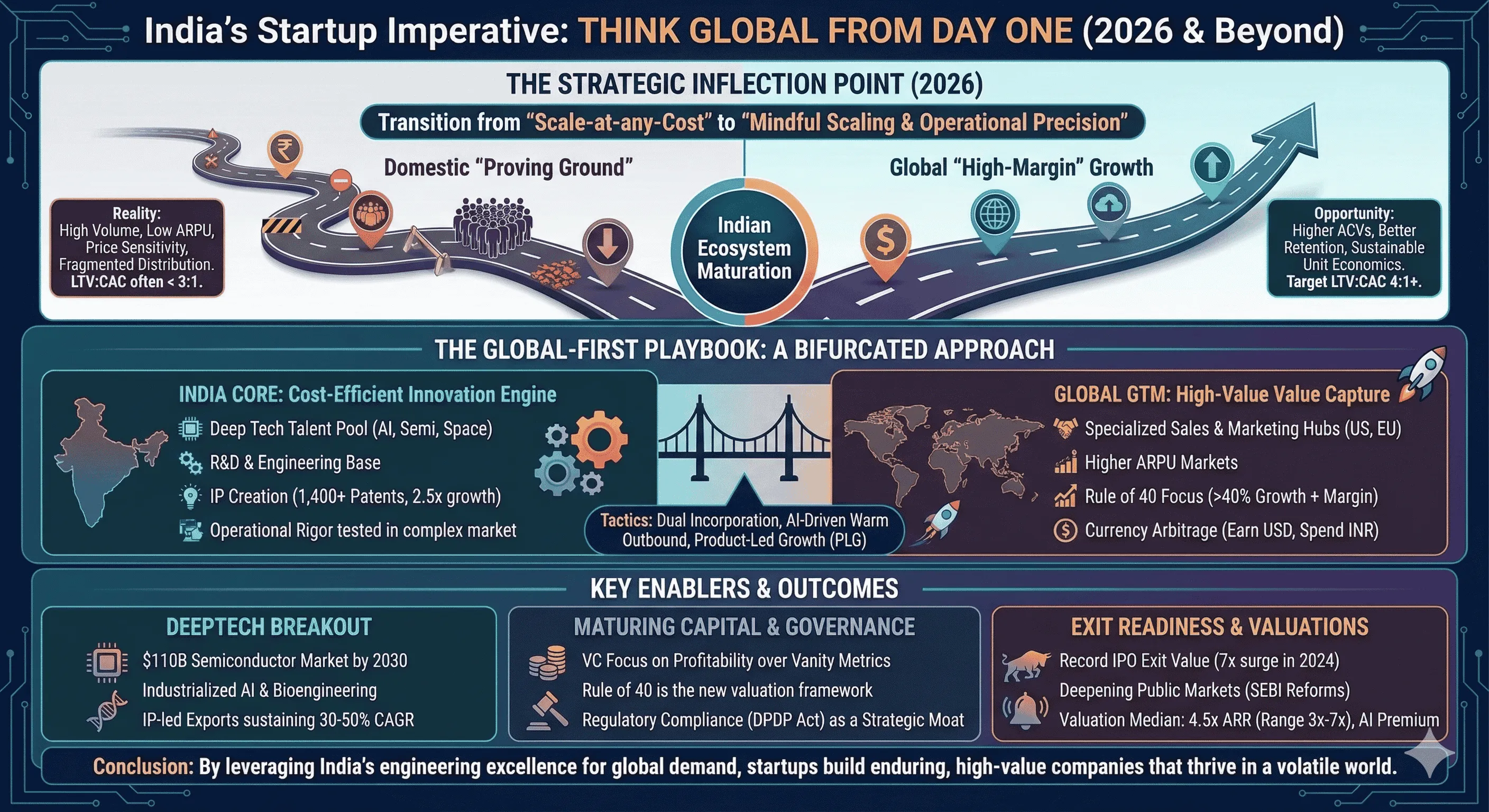

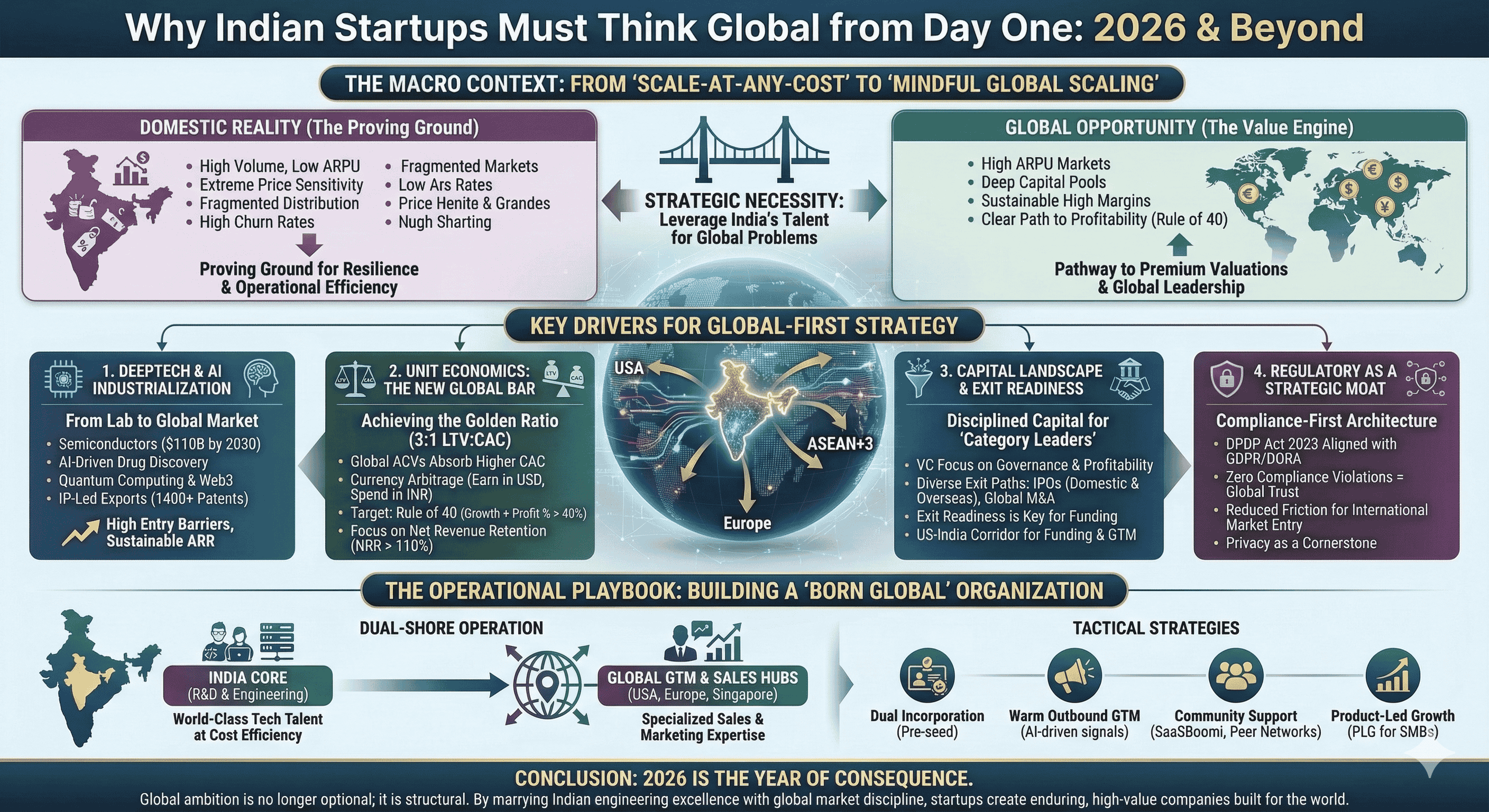

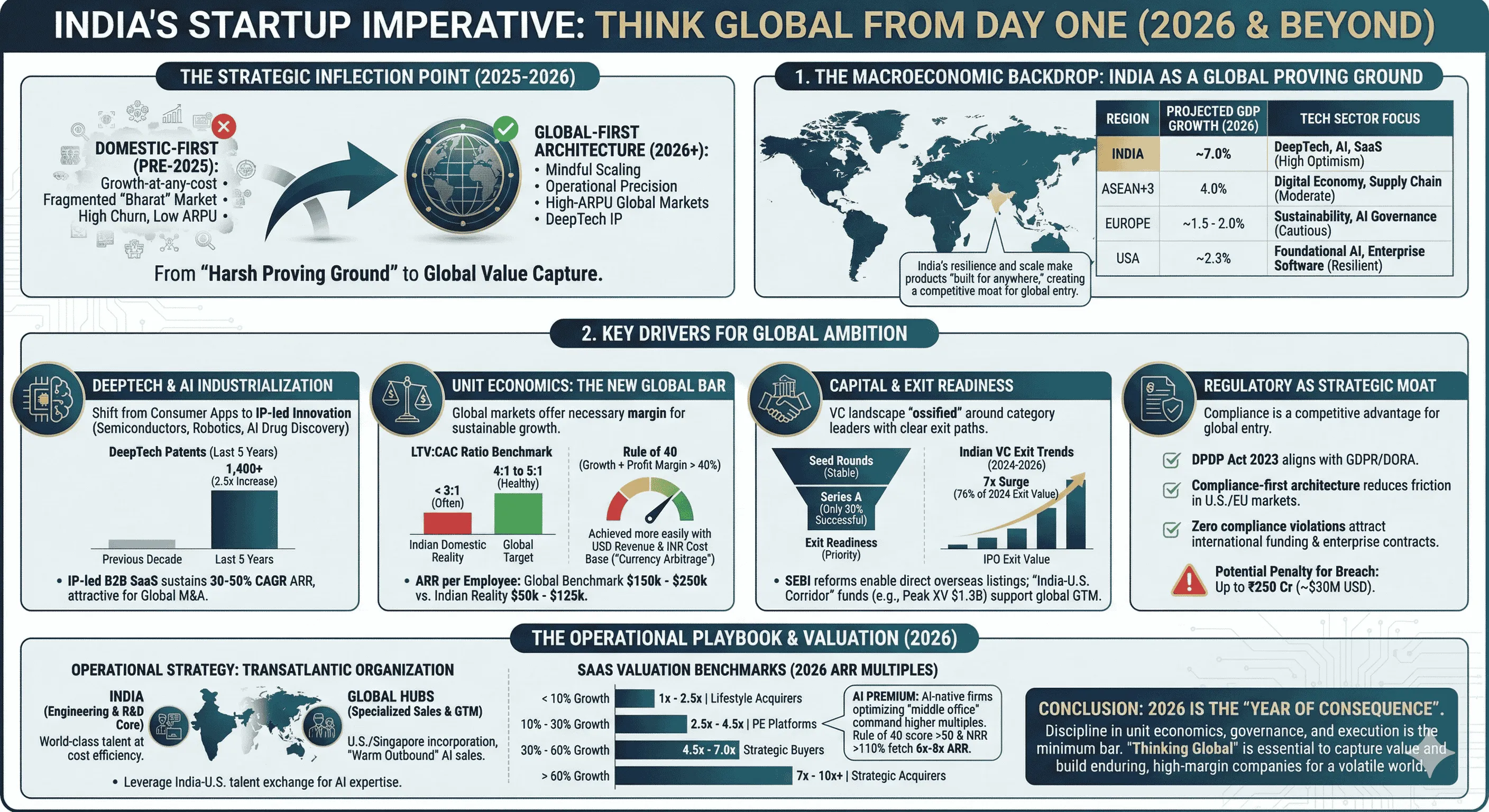

The Indian startup ecosystem, as it approaches the midpoint of the decade in 2026, has reached a critical strategic inflection point characterized by a transition from aggressive, scale-at-any-cost expansion to a philosophy of mindful scaling and operational precision. For the modern Indian founder, the decision to "think global from day one" is no longer a peripheral choice but a structural necessity dictated by the maturing nature of capital flows, the industrialization of artificial intelligence (AI), and the unique economic constraints of the domestic market. This shift is underscored by the realization that while India remains one of the world's most vibrant "proving grounds" for technology, the path to sustainable high-margin growth and premium valuations increasingly requires capturing value in high-Average Revenue Per User (ARPU) global markets.

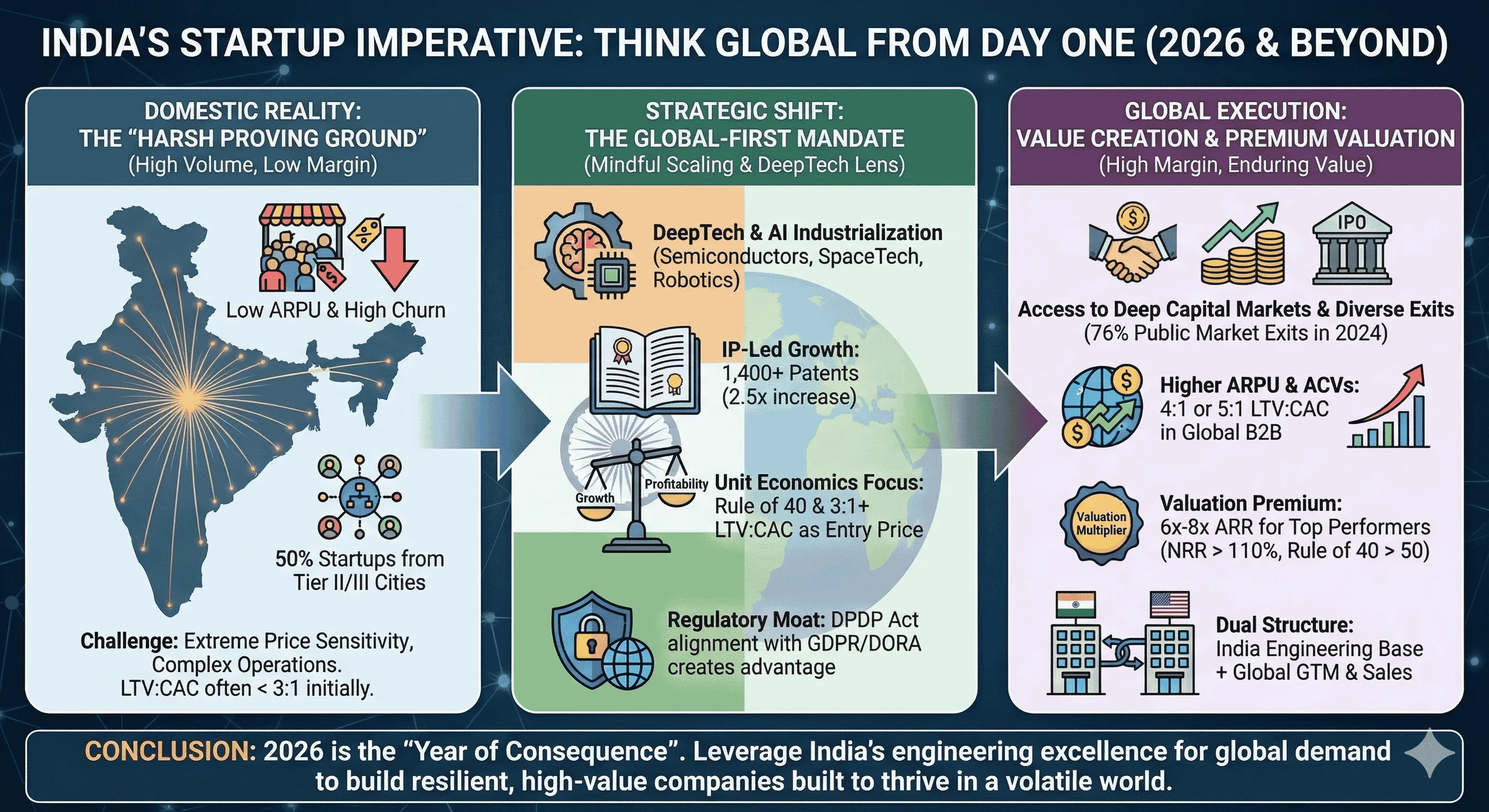

A decade of the "Startup India" initiative has successfully democratized entrepreneurship, pushing innovation into Tier II and Tier III cities like Kochi, Jaipur, and Indore, where nearly 50% of the country’s 200,000 recognized startups now originate. However, the economic reality of 2026 reveals a bifurcation in the ecosystem. Founders who design products exclusively for the domestic "Bharat" market often face the "harsh proving ground" of extreme price sensitivity and fragmented distribution. Conversely, those who build with a "global-first" architecture leverage India’s deep technical talent to solve problems for international enterprises, thereby accessing the deep-pocketed capital markets of the West while maintaining a cost-efficient R&D base in India.

The Macroeconomic Backdrop: Growth, Stability, and the Global Proving Ground

In 2025 and 2026, the Indian economy has maintained a robust growth trajectory, with real GDP expanding at approximately 7 per cent. This growth is broad-based, fueled by rural consumption, government infrastructure spending, and a resilient export sector. For startups, this stability provides a fertile environment for experimentation, but it also highlights a significant challenge: the domestic market's low ARPU and high churn rates relative to Western counterparts.

The concept of India as a "proving ground" has emerged as a central thesis for global-first startups. Products that can survive the operational complexity, price sensitivity, and scale demands of the Indian market are considered inherently resilient and "built for anywhere". This resilience becomes a competitive moat when these companies enter global markets, where they can often provide superior value at a more efficient price point than incumbents.

Comparative Regional Economic Outlook (2025-2026)

Region | Projected GDP Growth (2026) | Primary Market Sentiment | Tech Sector Focus |

India | ~7.0% | High Optimism; Mindful Scaling | DeepTech, AI, SaaS |

ASEAN+3 | 4.0% | Moderate Growth; Elevated Uncertainty | Digital Economy; Supply Chain |

Europe | ~1.5 - 2.0% | Cautious Recovery; Regulatory Focus | Sustainability; AI Governance |

USA | ~2.3% | Resilient; High Capital Concentration | Foundational AI; Enterprise Software |

The structural confidence in Indian founders is reflected in the venture capital (VC) landscape, where India remains a top-five global VC market, accounting for 8% of global deal volume. However, the nature of these investments has changed. Venture capitalists are prioritizing governance, measurable impact, and pathways to profitability over "vanity metrics". This creates a "global-first" mandate: if a startup’s unit economics do not work at the domestic level, the global market offers the necessary margin to achieve the 3:1 LTV:CAC (Lifetime Value to Customer Acquisition Cost) ratio that investors now demand as the "price of entry" for capital.

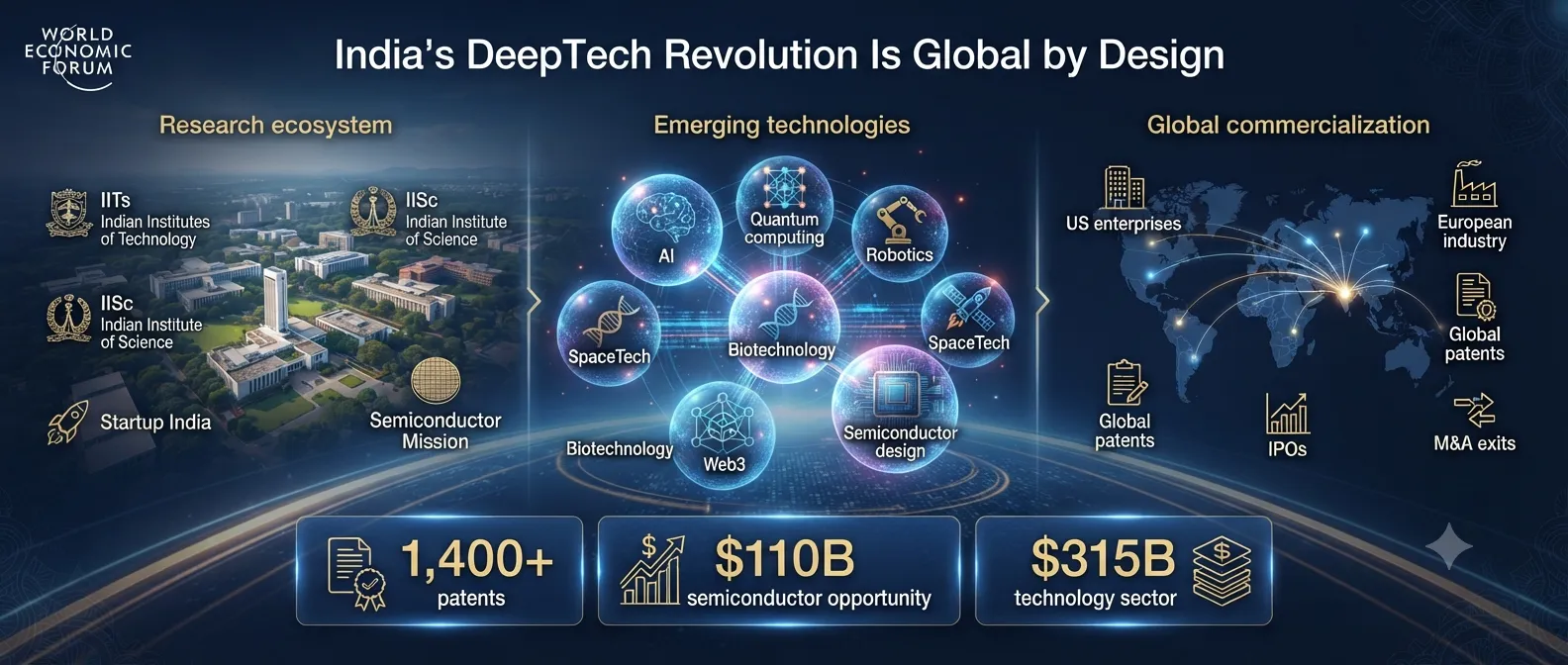

The Rise of DeepTech: From Academia to Global Commercialization

The year 2026 marks the "breakout moment" for DeepTech-led innovation in India. For the previous decade, the tech landscape was dominated by consumer applications in e-commerce, fintech, and mobility. Today, semiconductors, high-end robotics, space technology, and AI-driven drug discovery have moved from academic laboratories to the center stage of the commercial market. The India Semiconductor Mission alone has catalyzed a market forecast to reach 110 billion by 2030, offering massive opportunities for chip-design and AI-hardware startups.

This DeepTech shift is inherently global. Technologies like quantum computing, Web3, and bioengineering address global challenges, and the intellectual property (IP) created in these sectors gives India a new export category. For instance, inventive DeepTech focused B2B SaaS firms in India have filed over 1,400 patents in the last five years, a 2.5x increase over the previous decade. This focus on IP is critical because it allows Indian firms to sustain Annual Recurring Revenue (ARR) growth at Compound Annual Growth Rates (CAGRs) of 30% to 50%, a benchmark that makes them highly attractive for global M&A.

DeepTech Adoption and Intellectual Property Trends

Technology Segment | Adoption Rate (SaaS) | Common Use Cases | Strategic Relevance |

AI / Machine Learning | 54% | Predictive Analytics; Conversational AI | Core Business Engine |

Big Data / Analytics | 39% | Customer Insights; Talent Analysis | Operational Efficiency |

Intelligent Automation | 7% | Middle-Office Workflows | Margin Optimization |

DeepTech Patents | 1,400+ | Proprietary Algorithms; Hardware Design | IP-Led Global Export |

The industrialization of AI is a primary driver of this trend. India has transitioned from AI experimentation to full-scale industrialization, consolidating AI-native assets through strategic mergers and acquisitions. By FY26, the technology sector is expected to cross the315 billion mark, shifting from scale-led growth to value and innovation-led growth. This maturation is particularly visible in B2B SaaS, where "Subscription-AI-and-Software" models are replacing traditional software delivery.

Unit Economics: The New Bar for Global Competitiveness

In 2026, unit economics are the primary survival predictor for startups. The funding "winter" that followed the 2021-2022 peak forced a rationalization of growth assumptions. Investors now look for a clear path to profitability, and for many Indian startups, that path leads through international markets. The Indian domestic market, while large, suffers from a lower ARPU and a higher cost of acquisition relative to the revenue generated.

In India, Customer Acquisition Cost (CAC) varies dramatically between digital-heavy acquisition in metros and community-led acquisition in Tier II and III towns. The "golden ratio" for investors—an LTV:CAC of 3:1—often takes longer for Indian B2C startups to achieve than founders expect. In contrast, global B2B markets offer higher ACVs (Annual Contract Values), allowing startups to absorb higher acquisition costs while maintaining a 4:1 or 5:1 LTV:CAC ratio.

2026 SaaS Unit Economics Benchmarks

Metric | 2026 Target / Benchmark | Indian Domestic Reality | Implications for Global-First |

LTV : CAC Ratio | 4:1 (Healthy) | Often < 3:1 initially | Global ACVs stabilize the ratio. |

CAC Payback Period | 12 - 15 months (Excellent) | Often 18 - 24 months | High ARPU in US/EU shortens payback. |

Net Revenue Retention | 106% (Median) | Lower in price-sensitive segments | Focus on expansion ARR in global accounts. |

ARR per Employee | 150k -250k | 50k -125k | Automation/AI required for efficiency. |

The Rule of 40—the principle that a software company's combined growth rate and profit margin should exceed 40%—has become the dominant framework for SaaS valuations in 2026. Only 17% of publicly traded SaaS companies met this threshold by late 2025, down from 30% a decade ago. For Indian founders, achieving the Rule of 40 is significantly easier when revenue is denominated in USD while R&D and engineering costs are maintained in INR. This "currency arbitrage" not only extends the startup's runway but also allows for a higher reinvestment rate into R&D, fueling a cycle of innovation that domestic-only peers cannot match.

The Capital Landscape: Discipline, Concentration, and Exit Readiness

The venture capital ecosystem in India has "ossified" into rigid patterns by 2026. Capital is not necessarily scarce, but it is highly concentrated around "perceived category leaders" and ventures with clear monetization strategies. In 2025, VC and PE fundraising surged by 39% to 12.1 billion, but investors are increasingly selective. Seed rounds have remained stable, but the gap between Seed and Series A has become the defining characteristic of the environment; only 30% of companies attempting a Series A in 2025 were successful.

A major factor in this selectivity is "exit readiness." Investors are prioritizing startups that have a clear path to an IPO or a high-value M&A exit. In 2024, exit activity edged up to6.8 billion, with public market exits accounting for a staggering 76% of that value. This represents a 7x surge in IPO exit value compared to previous years. For global-first startups, the exit options are even more diverse. SEBI (Securities and Exchange Board of India) has reformed listing requirements, allowing growth-oriented technology companies to list on domestic exchanges without a prior record of profitability, and crucially, opening doors for direct overseas listings.

Indian VC Funding and Exit Trends (2024-2026)

Funding Milestone | 2024 Statistics | 2025/2026 Outlook | Key Driver |

Total VC Funding | 13.7B | 12.1B - 13.5B | Recalibration to Unit Economics |

Number of Unicorns | 120 | 125 | Stability in High-Value Assets |

IPO Exit Value | Surge (7x growth) | Continued Record Levels | Maturing Public Markets |

Inbound M&A Deals | ~25% of total value | Rising (e.g., Emirates NBD) | Strategic Global Interest |

Venture capital firms like Peak XV Partners have secured massive fresh commitments—1.3 billion across India and APAC funds—specifically to support early-stage company formation through to public listings. The firm is leaning heavily into the "U.S.-India corridor," backing founders where engineering moats sit in India while GTM (Go-to-Market) strategies target global enterprises. This corridor is further supported by global heavyweights like General Catalyst, which plans to invest 5 billion in India over five years.

Regulatory Compliance: From Burden to Strategic Advantage

Navigating India's regulatory landscape has historically been a challenge for startups, but in 2026, compliance is becoming a strategic moat. The introduction of the Digital Personal Data Protection (DPDP) Act in 2023, along with updated IT Rules and tighter RBI oversight, has significantly increased the operational burden. For startups targeting only the Indian market, these regulations impose heavy costs that can divert funds from innovation.

However, for global-first startups, the DPDP Act’s alignment with international standards like GDPR (General Data Protection Regulation) and DORA (Digital Operational Resilience Act) is an advantage. By building a compliance-first architecture from day one, Indian startups can enter the U.S. and European markets with minimal friction. Firms that achieve "zero compliance violations" are finding it easier to secure international funding and enterprise contracts.

Regulatory Landscape and Compliance Fines (2026)

Regulation | Scope | Potential Penalty for Breach | Compliance Goal |

DPDP Act 2023 | Personal Data Processing | Up to ₹250 Cr (~30M USD) | Data Privacy & Trust |

SEBI / MCA | ESG & Corporate Governance | Regulatory Scrutiny; Exit Delay | Transparency & Accountability |

CCI (Antitrust) | M&A Combinations | Compounding Penalties; Unwinding | Market Competition |

GST / Tax | Financial Reporting | Penalties; Input Credit Loss | Digital Governance |

The cost of non-compliance is high, and investors are watching regulatory timelines closely. For early-stage companies, the inability to plan for "Significant Data Fidelity" (SDF) obligations can dampen investor appetite and shorten runways. Nevertheless, the Ministry of Electronics and Information Technology projects that India's digital economy will reach $1 trillion by 2026, and privacy compliance is viewed as the "cornerstone" of this market entry.

The Operational Playbook for "Born Global" Success

For the "born global" Indian startup, the operational strategy in 2026 focuses on building a transatlantic organization that thrives on both sides of the ocean. This involves a "bifurcated approach": maintaining a core technical innovation and engineering team in India—where world-class talent is available at half the cost of New York or San Francisco—while strategically adding specialized sales and marketing expertise in global hubs.

One of the key tactical advantages is the India-U.S. talent exchange. Indian founders are increasingly using the U.S. market to access specialized AI and machine learning talent, while simultaneously leveraging India's deep developer pool to build products for global giants. Experience gained by working with large Indian entities like the Government of India or L&T has enabled firms like Zetwerk to mirror these complex operations when working with U.S. companies like Airbus and GE.

Tactical Strategies for Global Expansion

Dual Incorporation: Many startups incorporate in the U.S. or Singapore at the pre-seed stage to facilitate global investment and GTM, while keeping operations in India.

Warm Outbound GTM: Utilizing AI-driven signals from LinkedIn, G2, and CRM data to move from cold calling to "warm outbound" sales sequences, often managed by Indian BDR (Business Development Representative) teams working across time zones.

Community Support: Platforms like SaaSBoomi and the Antler India AI Residency provide playbooks and peer networks that help early-stage founders increase their odds of success overseas.

Product-Led Growth (PLG): Targeting global SMBs through self-service onboarding allows startups to achieve lower acquisition costs while refining product-market fit (PMF) before moving up-market to larger enterprise deals.

Founders are warned that "market size" in a pitch deck is no longer a valuable signal. Instead, investors look for extreme ownership of outcomes and the ability to iterate based on actual customer behavior. Achieving a sustainable Rule of 40 score—where growth is balanced by profitability—is the ultimate goal for startups seeking premium valuations.

Valuation Benchmarks and the Premium for Global Scale

Valuations in 2026 have stabilized in a range of 3x to 7x ARR for private SaaS companies, with a median of 4.5x. The double-digit revenue multiples seen in 2021 are not returning, as the market has undergone a "reset to fundamentals". However, the gap between the bottom and top quartiles has widened significantly. Companies that demonstrate NRR (Net Revenue Retention) above 110% and Rule of 40 scores above 50 can still command multiples of 6x to 8x ARR.

A significant trend is the premium paid for AI-native companies. As the market sorts "winners from losers" in the AI integration wave, startups that have embedded AI into their "middle office" to optimize underwriting, claims, and compliance are seeing higher efficiency gains and higher valuations.

SaaS Valuation Drivers and Multiple Brackets (2026)

Growth Rate (YoY) | Typical ARR Multiple | Buyer Profile |

< 10% | 1x - 2.5x | Search funds; Lifestyle acquirers |

10% - 30% | 2.5x - 4.5x | PE platforms; Bolt-on acquirers |

30% - 60% | 4.5x - 7.0x | Growth PE; Strategic Buyers |

> 60% | 7x - 10x+ | Strategic Acquirers; Growth Equity |

Strategic buyers are increasingly looking at Indian firms that have "cracked the code" on ROI for AI. For instance, early-stage VC valuations in India have historically hovered at 20-50% of the levels in the U.S., making Indian startups attractive targets for "multiple arbitrage" at exit. As Indian public markets deepen—ranking second globally by number of IPOs—the liquidity for these high-quality assets has improved significantly.

Conclusion: 2026 as the "Year of Consequence" for Global Ambition

The transition from 2025 to 2026 signals a more mature, globally competitive chapter for Indian entrepreneurship. If previous years were about experimentation and testing adoption, 2026 is the year those experiments harden into systems. The discipline adopted by founders around unit economics, governance, and execution has become the "minimum bar," and the predictability of outcomes is now more important than the pace of growth.

For the Indian startup, the domestic market will continue to be a vital "proving ground" that stress-tests products against complexity and sensitivity. However, the mandate to "think global from day one" is essential for capturing the value created by this rigor. By leveraging India’s engineering excellence to serve global demand, and by aligning with international regulatory and valuation standards, Indian startups are no longer just solving local problems—they are creating the solutions that will shape the world economy in the coming decade. The "global-first" strategy is not just about expansion; it is about building enduring, high-value companies that are built to thrive in a volatile and heterogeneous world.

Want to calculate the equity for your cofounder?

Nail your cap table before you sign. Whether you're splitting equity with a co-founder or planning your next funding round, our Equity Calculator gives you precision in seconds

Equity calculator →