How Brazilian Startups Compete with Global Companies

March 9, 2026 by Harshit Gupta

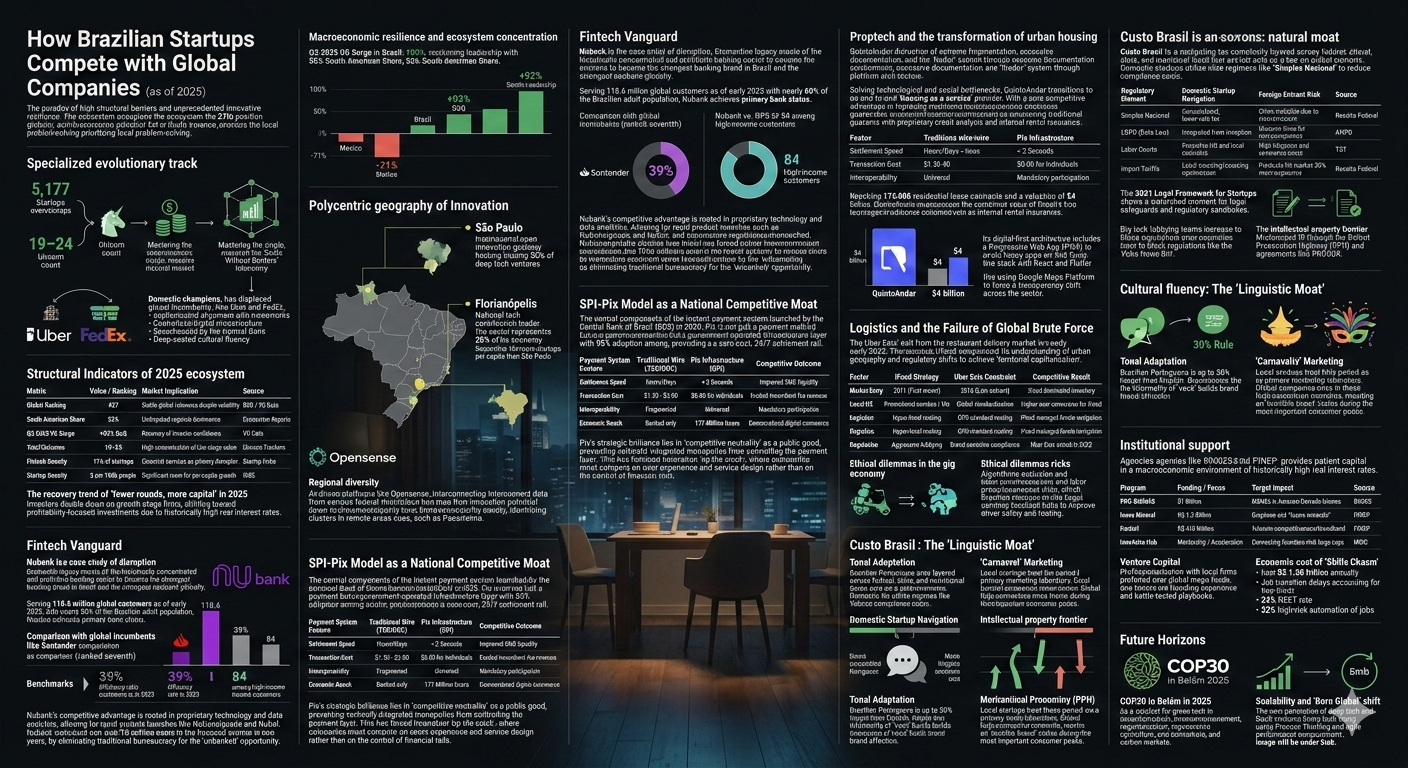

The Brazilian technological landscape, as of 2025, represents a paradox of high structural barriers and unprecedented innovative resilience. Occupying the 27th position globally and the 1st in South America, the Brazilian startup ecosystem has developed a specialized evolutionary track that prioritizes local problem-solving over global standardization. With over 5,177 startups and a unicorn count ranging from 19 to 24, Brazil has effectively become a laboratory for "Scale Without Borders," where firms achieve billion-dollar valuations by mastering the intricacies of a single, massive internal market. The ability of these domestic champions to compete with—and frequently displace—global incumbents such as Uber, FedEx, and traditional American banking institutions is not merely a byproduct of proximity. Rather, it is the result of a sophisticated alignment between proactive regulatory frameworks, a centralized digital infrastructure spearheaded by the Central Bank, and a deep-seated cultural fluency that global entrants find notoriously difficult to replicate.

Macroeconomic Resilience and Ecosystem Concentration

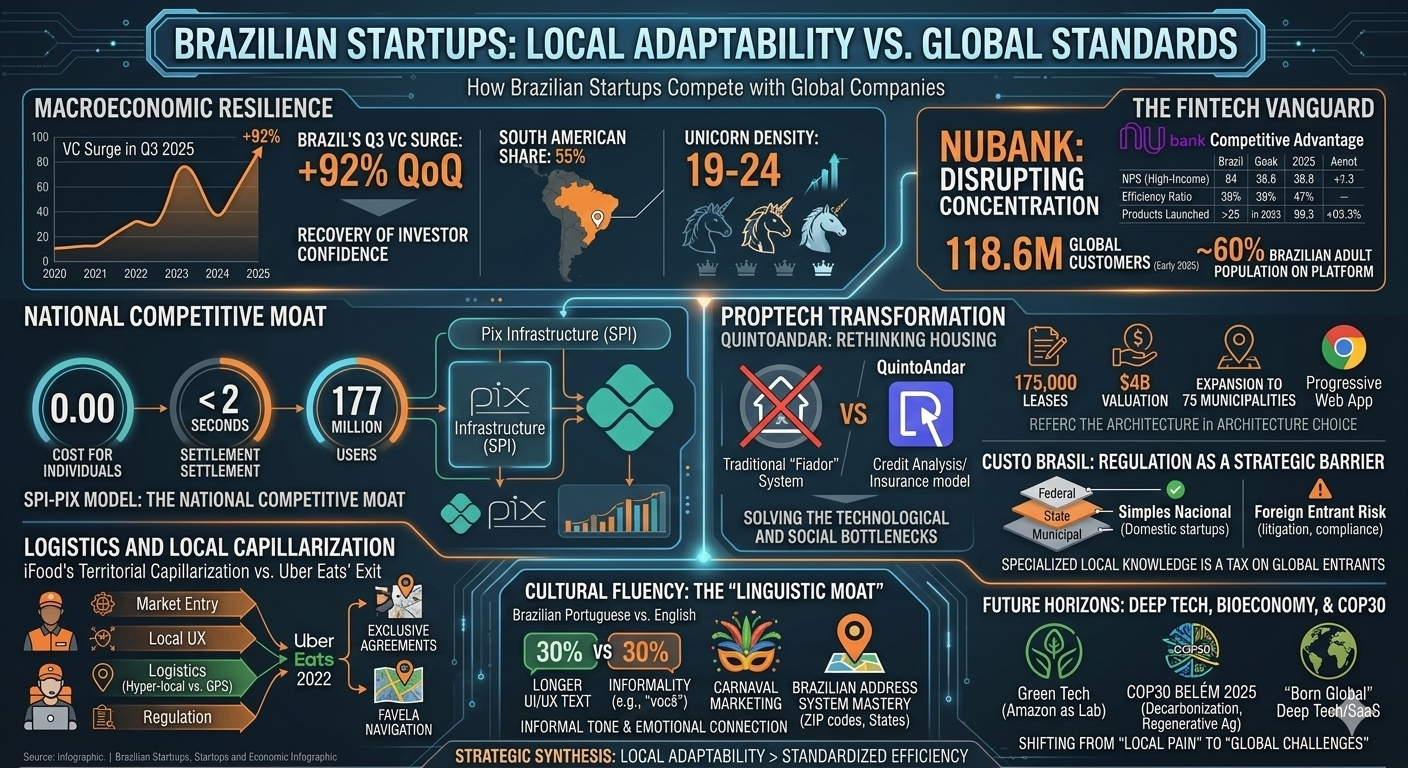

The resilience of the Brazilian startup sector is evidenced by its performance during global downturns. While other Latin American markets saw significant funding drops in 2025—Mexico, for instance, experienced a 71% quarter-over-quarter decline in Q3—Brazil reclaimed its leadership position with a 92% surge in venture capital commitments during the same period. This concentration of capital is a structural response to the maturity of the Brazilian ecosystem, which now accounts for 55% of all startups in South America.

The geography of innovation in Brazil is increasingly polycentric. While São Paulo remains the primary gateway for international open innovation, hosting 55% of the country’s deep tech ventures, other hubs have achieved higher levels of specialization. Florianópolis, for example, has emerged as the national leader in tech contribution to GDP, with the sector representing 25% of its economy and supporting ten times more startups per capita than São Paulo. This regional diversity is supported by AI-driven platforms like Opensense, which interconnects data from various federal ministries to map innovation potential down to the municipality level, identifying clusters even in remote areas such as Pacaraima in Roraima.

Structural Indicators of the 2025 Ecosystem

Metric | Value / Ranking | Market Implication | Source |

Global Ranking | #27 | Stable global relevance despite volatility | |

South American Share | 55% | Undisputed regional dominance | |

Q3 2025 VC Surge | +92% QoQ | Recovery of investor confidence | |

Total Unicorns | 19–24 | High concentration of late-stage value | |

Fintech Density | 11% of startups | Financial services as primary disruptor | |

Startup Density | 3 per 100k people | Significant room for per-capita growth |

The recovery in 2025 was marked by a "fewer rounds, more capital" trend, where investors showed a selective approach to early-stage bets while doubling down on growth-stage firms. This shift toward profitability-focused investments is a second-order effect of historically high real interest rates, which forced Brazilian founders to optimize unit economics long before their peers in lower-rate environments like the United States or Europe.

The Fintech Vanguard: Nubank and the Disruption of Concentration

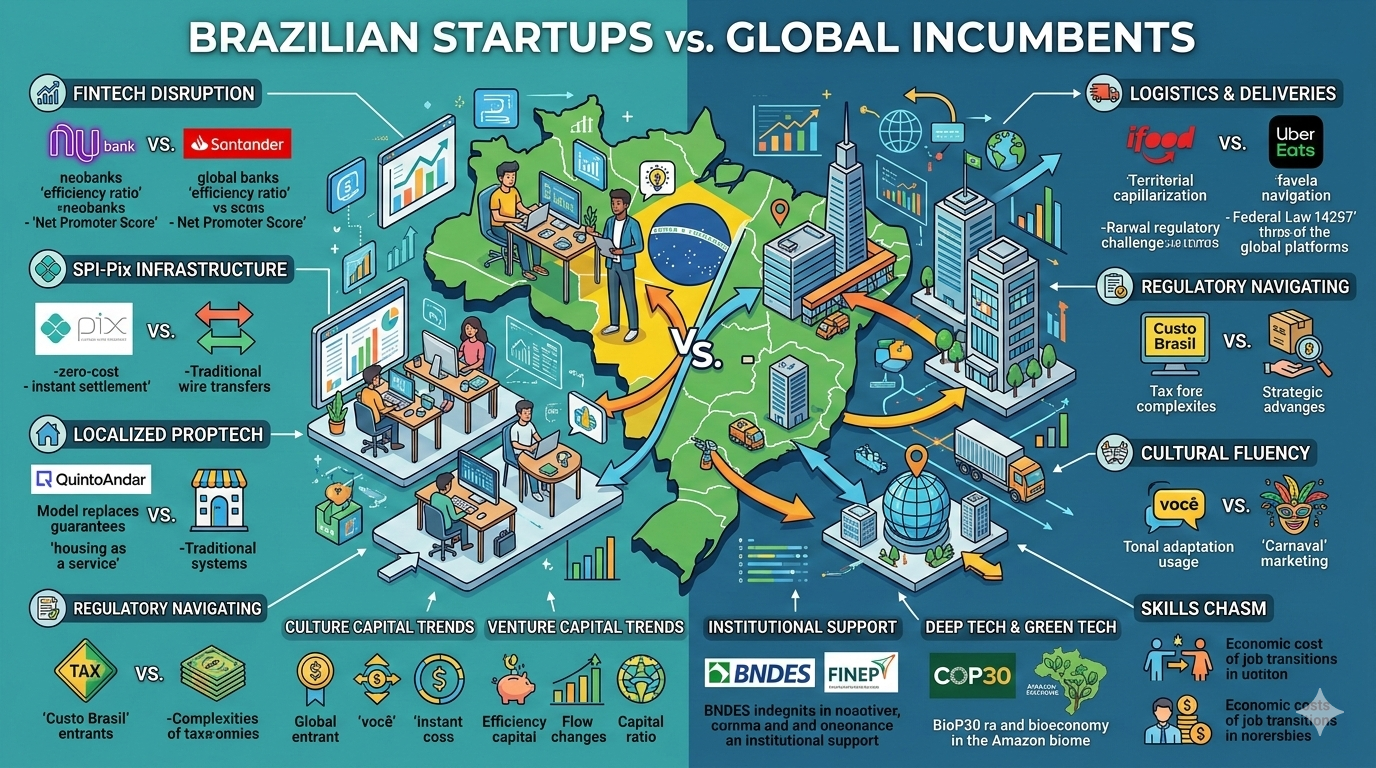

The Brazilian banking sector was historically one of the most concentrated and profitable in the world, a factor that ironically served as the perfect fertilizer for fintech disruption. Nubank’s rise to become the strongest banking brand in Brazil—and the strongest neobank globally—is a case study in using digital-native architecture to dismantle legacy moats. Serving 118.6 million global customers as of early 2025, with nearly 60% of the Brazilian adult population on its platform, Nubank has achieved a primary bank status that few global digital banks have replicated elsewhere.

Competitive Advantage over Global Incumbents

Global banks like Santander, which ranks as the seventh strongest banking brand in Brazil, find themselves in a defensive posture against Nubank’s efficiency. Nubank’s efficiency ratio of 39% in 2023 and a Net Promoter Score (NPS) of 84 among high-income customers are benchmarks that traditional institutions struggle to match while maintaining their physical branch networks and legacy IT systems. The competitive advantage here is rooted in proprietary technology and data analytics, allowing Nubank to launch over 25 products in 2023 alone, from payroll loans (NuConsignado) to mobile virtual network services (NuCel).

The "unbanked" opportunity was another primary driver. By eliminating the traditional bureaucracy that required physical signatures and extensive documentation, fintechs included over 70 million users in the financial system in just two years. This massive expansion of the addressable market created a "maturing cohort" of consumers who are now being up-sold more complex products like insurance and investment solutions, categories where traditional banks like Itaú—still the most valuable banking brand at $9.9 billion—continue to hold a lead but face rapidly eroding margins.

The SPI-Pix Model as a National Competitive Moat

A fundamental component of the Brazilian fintech success story is Pix, the instant payment system launched by the Central Bank of Brazil (BCB) in 2020. Pix is not merely a payment method; it is a government-operated infrastructure layer that has achieved 95% adoption among adults. By providing a zero-cost, 24/7 settlement rail, the BCB effectively "leveled the playing field" between startups and incumbent banks.

Payment System Feature | Traditional Wire (TED/DOC) | Pix Infrastructure (SPI) | Competitive Outcome |

Settlement Speed | Hours/Days | < 2 Seconds | Improved SME liquidity |

Transaction Cost | $1.50 - $3.00 | $0.00 for individuals | Eroded incumbent fee revenue |

Interoperability | Fragmented | Universal | Mandatory participation |

Economic Reach | Banked only | 177 Million Users | Democratized digital commerce |

The strategic brilliance of Pix lies in its "competitive neutrality." By building the infrastructure as a public good, the BCB prevented vertically integrated monopolies or global big tech firms (like Facebook’s attempted WhatsApp Pay launch) from controlling the payment layer. This has forced innovation "up the stack," where companies must compete on user experience and service design rather than on the control of financial rails. For international e-commerce merchants, the lesson is clear: failing to integrate Pix or insisting on dollar-denominated pricing is a barrier to 50% of the Brazilian consumer base.

Proptech and the Transformation of Urban Housing

The Brazilian real estate market was traditionally defined by extreme fragmentation, excessive documentation, and the "fiador" (guarantor) system, which required a tenant to find a property owner in the same city to co-sign their lease. QuintoAndar’s disruption of this sector is perhaps the most significant example of a startup using platform architecture to solve a purely local sociological bottleneck.

Solving the Technological and Social Bottlenecks

QuintoAndar transitioned from a listing marketplace to an end-to-end "housing as a service" provider. Its core competitive advantage lies in replacing traditional guarantees with a proprietary credit analysis model and internal rental insurance. This innovation allowed the platform to capture 175,000 residential lease contracts and reach a valuation of $4 billion, surpassing the combined value of Brazil's two largest traditional real estate developers.

The company's expansion into 75 municipalities was supported by a hybrid marketplace model. Rather than acting as a broker itself, QuintoAndar monetizes by enabling a network of partner agents who use its technology stack for pricing (QPreço) and AI-led property matching. This strategy has been so effective that global incumbents like Grupo OLX have engaged in "unfair competition" litigation against QuintoAndar to slow its momentum.

Digital-First Architecture for Emerging Connectivity

QuintoAndar's success is also a lesson in adapting to the hardware constraints of the Brazilian population. Recognizing that many users were hesitant to install heavy apps on mid-range devices, the company participated in the Google for Startups Accelerator to build a Progressive Web App (PWA). This architectural choice allowed them to unify their stack using React and Flutter, driving traffic growth of 30 times. By using Google Maps Platform to show exact property locations—a feature previously avoided by the market to prevent "drive-by" deals that bypassed agents—QuintoAndar forced a transparency shift across the entire sector.

Logistics and the Failure of Global Brute Force: The Case of Uber Eats

The delivery and logistics sector in Brazil serves as a cautionary tale for global companies that underestimate the power of local capillarization. The exit of Uber Eats from the restaurant delivery market in early 2022 highlights how a deeply localized incumbent like iFood can weaponize its understanding of urban geography and regulatory shifts.

Territorial Capillarization and Exclusivity

iFood, founded in 2011, achieved what researchers call "territorial capillarization"—a dense, algorithmic monitoring of demand zones, service availability, and delivery driver patterns across varied socio-spatial formations. While Uber Eats attempted to apply its global ride-hailing playbook, iFood secured exclusivity agreements with key restaurant chains, a move that was investigated by CADE but nonetheless solidified its dominance.

Factor | iFood Strategy | Uber Eats Constraint | Competitive Result |

Market Entry | 2011 (First mover) | 2016 (Late entrant) | iFood dominated inventory |

Local UX | Promotional combos / Pix | Global standardization | Higher user conversion for iFood |

Logistics | Hyper-local routing | GPS-standard routing | iFood managed favela navigation |

Regulation | Aggressive lobbying | Brand-sensitive compliance | Uber Eats exited in 2022 |

The introduction of Federal Law 14297 in 2022 further altered the competitive landscape. This legislation, a response to the "Breque dos Apps" (strike of the apps) movement, mandated that delivery platforms provide insurance and financial assistance to workers, significantly increasing operational costs. For Uber Eats, facing a 37% growth that was still insufficient to challenge iFood's lead, these rising regulatory costs made the restaurant delivery segment unviable, forcing a pivot to grocery delivery via Cornershop.

Ethical Dilemmas in the Gig Economy

The logistics sector also faces significant headwinds regarding social responsibility. Both iFood and Rappi have been criticized for failing to combat child labor among drivers, often relying on AI-based facial recognition that is easily circumvented. This "algorithmic exclusion" and the precariousness of labor in a country with high unemployment and low minimum wages have created a "digital colonialism" narrative that local regulators are increasingly monitoring. Brazilian startups that can solve these social issues while maintaining efficiency—such as Loggi’s use of localized hubs to improve driver safety and routing—are likely to gain long-term regulatory favor.

Custo Brasil: Regulation as a Strategic Barrier

The "Custo Brasil" is often viewed as a deterrent for foreign business, but for domestic startups, it functions as a natural moat. Navigating the tax complexity—layered across federal, state, and municipal levels—requires a level of specialized local knowledge that acts as a tax on global entrants.

Tax Regimes and Compliance Levers

Global companies often fail in Brazil because they "copy-paste" their international pricing models without accounting for ICMS (state tax) variations or the "substitution tax" system. In contrast, Brazilian startups utilize regimes like "Simples Nacional" to consolidate taxes and reduce compliance costs during their early years.

Regulatory Element | Domestic Startup Navigation | Foreign Entrant Risk | Source |

Simples Nacional | Consolidated, lower-rate tax | Often ineligible due to size/structure | |

LGPD (Data Law) | Integrated from inception | Massive fines for non-compliance | |

Labor Courts | Proactive HR and local contracts | High litigation and severance costs | |

Import Tariffs | Local sourcing/sourcing optimization | Products hit market 30% more expensive |

The 2021 Legal Framework for Startups was a watershed moment, providing legal safeguards for angel investors and introducing "regulatory sandboxes" for testing emerging technologies. However, the landscape remains combative; big tech companies have built robust lobbying teams in Brazil—half of which were hired between 2021 and 2023—to block regulations like the "Fake News Bill" (PL 2630), which they fear could set a precedent for the entire Global South.

The Intellectual Property Frontier

Brazil has also moved to modernize its IP regime through the Patent Prosecution Highway (PPH) and agreements like PROSUR, which allow for faster patent recognition across Latin American partner countries. For "deep tech" startups, particularly those emerging from universities like USP or UNICAMP, these improvements are critical for protecting technological breakthroughs in healthcare and green energy before they scale globally.

Cultural Fluency: The "Linguistic Moat"

A primary driver of customer loyalty for Brazilian startups is an innate understanding of the "Brazilian tone." Global brands often sound "cold" or "boardroom-teleprompter rigid" to a population that values informality and emotional connection.

Tonal Adaptation and the 30% Rule

Brazilian Portuguese is up to 30% longer than English, which fundamentally changes UI/UX design requirements. Beyond length, the use of "você" for "you" reflects a national informality that local startups like Nubank and iFood weaponize to build brand affection.

Furthermore, the Brazilian address system—with its 27 states and mandatory ZIP code formatting—is a common point of friction for global e-commerce sites that lack the "required number and size of boxes" to accommodate local addresses. Startups that prioritize these details, such as the fashion-tech firm AMARO or the retail platform Olist, gain an immediate trust advantage over global sites where prices are displayed in dollars and international shipping costs are opaque.

Seasonality and "Carnaval" Marketing

Local mastery extends to the "Carnaval" season, which local startups treat as a primary marketing laboratory. During this period, travel and gaming apps are hyper-localized to capture a population on the move. Global companies that rely on a "standardized global calendar" miss these high-conversion cultural moments, resulting in an "invisible brand" status during the most important consumer peaks of the year.

Institutional Support: BNDES, FINEP, and the "New Industry Brazil"

The Brazilian state is not a passive bystander but an active "market maker." State agencies like BNDES and FINEP provide non-reimbursable grants and long-term credit lines that are essential in a macroeconomic environment of historically high real interest rates.

Strategic Investment Missions

The "New Industry Brazil" strategy defines six priority missions, including digital transformation and bioeconomy, backed by a R$ 3 billion budget to attract R&D centers.

Program | Funding / Focus | Target Impact | Source |

PRÓ-BIOMAS | $1 Billion | MSMEs in Amazon/Cerrado biomes | |

Inova Mineral | R$ 1.2 Billion | Graphene and "future minerals" | |

Funttel | R$ 410 Million | Telecom competitiveness/Broadband | |

InovAtiva Hub | Mentorship / Acceleration | Connecting founders with large caps |

These programs focus on "capillarizing" innovation, moving beyond the São Paulo-Rio axis to support hubs in the North and Northeast. This institutional support provides a "patient capital" alternative to the 2025 VC trend, where private investors have become increasingly risk-averse regarding early-stage "blue sky" projects.

Venture Capital: The Dominance of Local Wisdom

The venture capital landscape in Brazil is increasingly professionalized, with local firms like Kaszek and Monashees being preferred by founders over global mega-funds. This preference stems from the VCs' "founding experience" and their ability to provide "constructive feedback" that accounts for local operational hurdles.

The Role of Serial Entrepreneurs

The Brazilian ecosystem is entering its second and third generations, characterized by a "network of serial entrepreneurs" who are alumni of early exits like MercadoLibre and Rappi. These individuals bring not only capital but also a "battle-tested" playbook for scaling in emerging markets. This talent flow has shifted the national mindset; leaving a multinational to join a startup is now a socially accepted—and often preferred—career path for top Brazilian graduates.

While global VCs like Softbank have historically made "mega-investments" in regional leaders, the 2025-2026 cycle shows a rise in local corporate venture capital (CVC). Major domestic players like Bradesco, Ambev, and Natura have launched accelerators to integrate startup innovations into their supply chains, creating a "matchmaking nexus" that many investors say was previously the missing link in the LatAm innovation cycle.

The Economic Cost of the "Skills Chasm"

Despite the ecosystem's success, Brazil faces a significant "Lost in Transition" crisis. Inefficiencies in job transitions and a "skills chasm" cost the economy an estimated R$ 1.08 trillion annually—equivalent to 9% of GDP.

Job Transition Delays: Prolonged gaps in moving between roles account for two-thirds of these losses, as 20% of unemployed Brazilians remain jobless for over two years.

The NEET Population: A 24% "neither studying nor working" (NEET) rate among youth threatens future workforce productivity.

Automation Risks: While not the current dominant driver of loss, 32% of jobs in agriculture and industry are at high risk of automation, necessitating proactive reskilling programs.

Brazilian startups are increasingly positioning themselves to solve these structural gaps. Edtech firms like Descomplica and infrastructure startups like BotCity are leveraging AI to bridge the vocational divide and automate the "bureaucratic friction" that slows down the national labor cycle.

Future Horizons: COP30, Deep Tech, and Global Ambition

As Brazil moves toward 2030, its startup strategy is shifting from "solving local pain" to "addressing global challenges." The hosting of COP30 in the Amazon region (Belém) in 2025 serves as a catalyst for startups focused on decarbonization, regenerative agriculture, and carbon markets.

The Green Tech Lab

The Amazon biome is emerging as a global innovation hub for the bioeconomy. Startups like Navegam and Proesc are leveraging "remote orientation" policies to integrate forest-based research into scalable business models. This "knowledge-intensive entrepreneurship" generates systemic-level impacts, converting technological maturity into superior business performance in sectors where Brazil has a natural comparative advantage.

Scalability and the "Born Global" Shift

While 86% of startups currently focus on the domestic market, the new generation of "deep tech" and SaaS ventures is being built as "born global". Using frameworks like "Process Thinking" and agile performance measurement, these firms are overcoming the "managerial difficulties" that previously hindered internationalization. Success stories like Wildlife Studios (gaming) and Magnamed (healthcare) demonstrate that when Brazilian creativity is paired with disciplined execution, local startups can dominate global creative and entertainment industries.

Strategic Synthesis and Conclusions

The competitive dynamic between Brazilian startups and global companies is fundamentally a contest between "standardized efficiency" and "localized adaptability." Global firms that treat Brazil as a "copy-paste" market frequently fail due to the pincer maneuver of Custo Brasil and the cultural fluency of domestic champions. Conversely, Brazilian startups that weaponize local regulatory complexity—using Pix as a rail, navigating the guarantor system with AI, and adopting the informality of the national tone—have created an ecosystem that is virtually immune to external disruption in its core verticals.

The ultimate competitive moat for the Brazilian startup is its ability to turn structural friction into a proprietary insight. As the ecosystem matures into its deep tech and green tech phases, the "Brazilian case" will likely become the global benchmark for how emerging economies can leverage public-private synergy to achieve technological sovereignty in an increasingly fragmented global economy. For global observers and participants, the directive is clear: in Brazil, success is not won through the imposition of global standards, but through the patient, strategic adoption of the national complexity.

Read More -

1. From Idea to MVP: A Step-by-Step Guide for Solo Founder

🔗 https://findnstart.com/blogs/from-idea-to-mvp-a-step-by-step-guide-for-solo-founder

2. How to Validate Your Startup Idea in 48 Hours for $0

🔗 https://findnstart.com/blogs/how-to-validate-your-startup-idea-in-48-hours-for-0

3. Remote vs. Local: Does Your Co-Founder Need to Live in the Same City?

🔗 https://findnstart.com/blogs/remote-vs-local-does-your-co-founder-need-to-live-in-the-same-city

4. The 2026 Startup Landscape: What Has Fundamentally Changed (and Why Founder Skills Matter More Than Ever)

5. The Most In-Demand Skills for Startup Founders in 2026

🔗 https://findnstart.com/blogs/the-most-in-demand-skills-for-startup-founders-in-2026

6. How to Find a Technical Co-Founder (Without a Six-Figure Salary)

🔗 https://findnstart.com/blogs/how-to-find-a-technical-co-founder-without-a-six-figure-salary

7. 5 Red Flags to Look for When Choosing a Startup Partner

🔗 https://findnstart.com/blogs/5-red-flags-to-look-for-when-choosing-a-startup-partner

8. How to Pitch Your Idea to Potential Co-Founders

🔗 https://findnstart.com/blogs/how-to-pitch-your-idea-to-potential-co-founders

9. How to Build a Portfolio that Attracts High-Growth Startup Founders

🔗 https://findnstart.com/blogs/how-to-build-a-portfolio-that-attracts-high-growth-startup-founders

10. Equity vs. Salary: How to Split Ownership with Your First Teammate

🔗 https://findnstart.com/blogs/equity-vs-salary-how-to-split-ownership-with-your-first-teammate

11. Why Joining an Early-Stage Startup is Better Than a Corporate Job

🔗 https://findnstart.com/blogs/why-joining-an-early-stage-startup-is-better-than-a-corporate-job

12. The Future of EdTech: Why Developers and Educators Need to Team Up Now

🔗 https://findnstart.com/blogs/the-future-of-edtech-why-developers-and-educators-need-to-team-up-now

13. The Architecture of Symbiosis: Analytical Perspectives on the Five Habits of Successful Startup Duos

14. Finding a Co-Founder in the AI Space: What Skills Should You Look For?

🔗 https://findnstart.com/blogs/finding-a-co-founder-in-the-ai-space-what-skills-should-you-look-for

15. Overcoming Analysis Paralysis and the Strategic Path to Execution

🔗 https://findnstart.com/blogs/overcoming-analysis-paralysis-and-the-strategic-path-to-execution

16. From College Project to Company: How to Find Your Student Co-Founder

🔗 https://findnstart.com/blogs/from-college-project-to-company-how-to-find-your-student-co-founder

17. How to Start a Startup While Working a Full-Time Job

🔗 https://findnstart.com/blogs/how-to-start-a-startup-while-working-a-full-time-job

18. How to Build a HealthTech Startup Without a Medical Degree

🔗 https://findnstart.com/blogs/how-to-build-a-healthtech-startup-without-a-medical-degree

19. The Solitary Architect: Executive Isolation in Entrepreneurship

20. The 2026 Guide to Launching a SaaS as a Solo Developer

21. What Sustainable Growth Actually Looks Like

🔗 https://findnstart.com/blogs/what-sustainable-growth-actually-looks-like

22. The Early Warning Signs Your Startup Is in Trouble

🔗 https://findnstart.com/blogs/the-early-warning-signs-your-startup-is-in-trouble

23. How to Grow Without Burning Out

🔗 https://findnstart.com/blogs/how-to-grow-without-burning-out

24. The Truth About “Runway” Most Founders Ignore

🔗 https://findnstart.com/blogs/the-truth-about-runway-most-founders-ignore

25. Revenue Solves More Problems Than Funding

🔗 https://findnstart.com/blogs/revenue-solves-more-problems-than-funding

26. What No One Tells You About Being a Solo Founder

🔗 https://findnstart.com/blogs/what-no-one-tells-you-about-being-a-solo-founder

27. Why Smart People Quit High-Paying Jobs to Build Startups (And Why Most Regret It)

28. Why Most Startup Advice on Twitter Is Dangerous

🔗 https://findnstart.com/blogs/why-most-startup-advice-on-twitter-is-dangerous

29. Decision Fatigue: The Silent Startup Killer

🔗 https://findnstart.com/blogs/decision-fatigue-the-silent-startup-killer

30. Fear vs Logic: How Founders Actually Make Decisions

🔗 https://findnstart.com/blogs/fear-vs-logic-how-founders-actually-make-decisions

31. How Overthinking Destroys Early Momentum

🔗 https://findnstart.com/blogs/how-overthinking-destroys-early-momentum

32. Ideas Don’t Scale. Systems Do.

🔗 https://findnstart.com/blogs/ideas-dont-scale-systems-do

33. The First Hire That Actually Matters

🔗 https://findnstart.com/blogs/the-first-hire-that-actually-matters

34. How the First 100 Users Decide Your Startup’s Fate

🔗 https://findnstart.com/blogs/how-the-first-100-users-decide-your-startups-fate

35. Why Your Startup Doesn’t Need Growth — It Needs Focus

🔗 https://findnstart.com/blogs/why-your-startup-doesnt-need-growthit-needs-focus

36. Why Most Startups Die Quietly

🔗 https://findnstart.com/blogs/why-most-startups-die-quietly

37. Lessons Learned Too Late by First-Time Founders

🔗 https://findnstart.com/blogs/lessons-learned-too-late-by-first-time-founders

38. The Myth of the “Overnight Success” Startup

🔗 https://findnstart.com/blogs/the-myth-of-the-overnight-success-startup

Want to calculate the equity for your cofounder?

Nail your cap table before you sign. Whether you're splitting equity with a co-founder or planning your next funding round, our Equity Calculator gives you precision in seconds

Equity calculator →