Why Every Silicon Valley Startup Is Now an AI Startup

February 24, 2026 by Harshit GuptaThe technological landscape of Silicon Valley is currently navigating a structural pivot of such magnitude that it has rendered the traditional distinctions between software sectors increasingly obsolete. The ubiquitous rebranding of startups as "AI companies" is not merely a promotional strategy designed to capture inflated venture capital premiums; it represents a fundamental realignment of the technical, economic, and cultural foundations of the digital economy. Since the public release of ChatGPT in November 2022, a historic turning point was reached where generative artificial intelligence transitioned from a research-intensive laboratory curiosity to the primary engine of global innovation. This shift is characterized by a "Great Migration" from the energy-hungry data centers of the cloud era to the palm of the user’s hand, enabled by specialized silicon that has effectively closed the performance gap between mobile devices and desktop workstations. As of early 2026, the industry has reached a consensus that the era of Software-as-a-Service (SaaS), as defined by human-centric interfaces and per-seat pricing models, is drawing to a close, replaced by an "Intelligence-Native" paradigm where value is derived from autonomous task execution and the orchestration of agentic workflows.

Historical Precedents and the End of the SaaS Era

The current metamorphosis in Silicon Valley mirrors previous shifts from on-premise software to cloud computing and from desktop to mobile interfaces. Historical patterns suggest that incumbents rarely emerge as the dominant winners in these new technological cycles. While established giants like Oracle successfully built applications-as-a-service, it was new entrants like Salesforce that led the enterprise SaaS revolution. Similarly, while Facebook attempted to port its desktop experience to mobile, the mobile-first social paradigm was defined by Instagram. The intelligence-native revolution is following a similar trajectory, where the winners are not those who simply "add-on" AI features to existing frameworks, but those who rethink the product management, development, and operational lifecycle from first principles.

The evolution of generative AI is punctuated by several critical breakthroughs that laid the groundwork for this systemic shift. The introduction of Recurrent Neural Networks (RNNs) in the late 1980s and Long Short-Term Memory (LSTM) networks in 1997 provided the initial ability to process sequential data, which was essential for speech recognition and machine translation. The creation of Generative Adversarial Networks (GANs) in 2014 by Ian Goodfellow revolutionized synthetic image generation by introducing a competitive mechanism between a generator and a discriminator network. However, the most significant catalyst was the 2017 "Attention Is All You Need" paper from Google researchers, which introduced the transformer architecture. Transformers replaced sequential RNNs with attention mechanisms, allowing for parallel processing of data and the modeling of long-range dependencies, which became the foundation for BERT in 2018 and the subsequent GPT series.

Milestone Year | Technological Breakthrough | Primary Innovation Impact | Key Model/Organization |

1997 | LSTM Networks | Order dependence in sequential data | Hochreiter/Schmidhuber |

2014 | GANs | Adversarial synthetic generation | Ian Goodfellow |

2017 | Transformer Architecture | Parallelization and attention mechanisms | Google Research |

2018 | GPT-1 / BERT | Bi-directional context understanding | OpenAI / Google |

2020 | GPT-3 | Massive parameter scale (175B) | OpenAI |

2022 | ChatGPT (GPT-3.5) | Public accessibility and interface | OpenAI |

2024 | Ironwood TPU / Gemini 3 | Hardware-model co-optimization | Alphabet (Google) |

2026 | 100-TOPS Mobile NPUs | On-device, offline agentic AI | Qualcomm / MediaTek |

By 2024, the impact of these milestones began to manifest as a "business model reset" rather than a mere feature wave. The traditional SaaS model, where buyers paid per seat because value scaled with the number of human users, began to fracture. When software starts completing work that previously required human time, the value is no longer tied to user counts but to the quality and volume of outcomes. This economic tension has forced startups to abandon the predictable recurring revenue of the per-user seat model in favor of consumption-based or hybrid models that align pricing with task-based business value.

The Economic Engine: Capital Concentration and Valuation Divergence

The financial landscape of Silicon Valley in 2025 and 2026 is defined by an unprecedented concentration of capital within the AI sector. Venture and growth investors poured approximately $425 billion into private companies in 2025, a 30% increase from the previous year. Crucially, roughly 50% of all global venture funding—reaching $211 billion—was allocated to AI-related fields. The dominance of AI is even more pronounced in the United States, which captured 64% of global startup funding in 2025. This surge is largely driven by "mega-rounds" for foundational model providers; five companies—OpenAI, Scale AI, Anthropic, Project Prometheus, and xAI—collectively raised $84 billion, or 20% of all venture capital in 2025.

This concentration has led to a dramatic divergence in valuation multiples between AI-native startups and traditional SaaS companies. AI startups command revenue multiples that are often several times higher than their peers, reflecting a fundamental shift in investor expectations. While traditional SaaS is now priced as a proven, cash-generating business model with median multiples below 5x, AI is valued as a transformative technology with speculative growth potential, often trading in the 10x to 50x revenue range.

Investment Metric | AI Startup Segment (2025) | Non-AI Startup Segment (2025) |

Median Revenue Multiple | 25.8x | 2.5x - 7.0x |

Seed Stage Valuation Premium | 42% higher | Baseline |

Series A Valuation (Median) | $51.9 Million | $39.9 Million |

Series B Valuation (Median) | $143 Million | $95 Million |

Share of Total VC Dollars | 63.3% (US Peak) | 36.7% |

Investors justify these premiums through the concept of "defensible moats" built on proprietary data and data network effects. Unlike traditional SaaS, where features are easily copied, AI-native companies develop advantages that compound over time; every user interaction improves the underlying model, making the product more effective and creating high switching costs for customers. However, this environment also invites significant risks, as high upfront costs in research, development, and cloud computing often distort revenue-based valuations, requiring a shift toward discounted cash flow analysis and scenario-based modeling to understand long-term profitability.

The late-stage AI market has begun to show signs of maturity, with the "valuation curve" starting to plateau beyond Series A. While Seed-stage companies saw their valuations triple since 2019, Series C and D rounds in 2025 have experienced multiple compression as investors begin to prioritize performance and efficiency over pure momentum. Companies that can generate five to seven dollars of enterprise value for every dollar raised are now consistently rewarded with higher multiples, signaling that the era of narrative-driven funding is being replaced by a rigorous focus on measurable scalability and customer-led growth.

The Silicon Tipping Point: Hardware Drivers and Edge Intelligence

A critical technical breakthrough enabling the universal shift to AI is the arrival of the 100-TOPS (Trillions of Operations Per Second) milestone for mobile Neural Processing Units (NPUs). By early 2026, chips like Qualcomm's Snapdragon 8 Elite Gen 5 and MediaTek's Dimensity 9500S have effectively closed the "Inference Gap" between handheld devices and cloud-based workstations for 80% of common AI workflows. These processors utilize "Compute-in-Memory" (CIM) architectures to minimize data movement and support "BitNet 1.58-bit" models, allowing sophisticated 3-billion parameter models to run with 50% lower power draw.

This hardware evolution differs fundamentally from previous generations of "AI-enabled" hardware. Modern mobile silicon treats the NPU as the primary engine of the operating system, rather than a secondary co-processor for simple tasks like image enhancement. The transition marks the end of the "Cloud Trilemma"—the trade-off between latency, privacy, and cost—by moving inference to the edge. For startups, this means that the recurring subscription costs associated with cloud-based AI services can be mitigated, and data privacy can be guaranteed by processing information entirely offline.

Hardware Feature | Previous Generation (Cloud Era) | 2026 Generation (Intelligence Era) |

Primary Processor | CPU/GPU (Cloud) | On-Device NPU |

Latency Profile | 5G Network dependent | Real-time, offline |

Data Privacy | Cloud-transmitted | Local-only (Agentic AI) |

Efficiency Metric | High energy per inference | CIM / BitNet 1.58-bit optimization |

Context Window | Limited (4k - 8k) | 32k - 128k (Mobile native) |

The implication for the startup ecosystem is profound: every application developer is now empowered to integrate deep document analysis and real-time conversation into their products without the "round-trip delay" of 5G networks or the unpredictable compute bills of external LLM providers. This democratization of high-performance intelligence ensures that even small, capital-efficient teams can ship AI-native features that rival those of established tech giants.

Vertical AI Specialization: Constructing Moats in Niche Domains

As foundational models from OpenAI, Anthropic, and Google become increasingly commoditized, Silicon Valley startups are pivoting toward "Vertical AI"—industry-specific solutions designed for targeted sectors like healthcare, legal, construction, and finance. The consensus among venture capitalists, including those at Y Combinator, is that "thin wrapper" companies—those that merely apply a user interface to an existing LLM—are highly vulnerable to being subsumed by foundational leaders. To survive, startups must develop deep domain expertise and integrate AI so tightly into specialized workflows that it becomes indispensable.

Vertical AI agents excel by leveraging niche data that horizontal models struggle to access. This focus allows for the creation of proprietary datasets and the fine-tuning of models on regulated or siloed information. Over time, these companies build a "data flywheel" where specialized usage data continuously improves the model's accuracy, creating a defensive moat that horizontal players cannot replicate.

Case Studies in Industry Transformation

In the Architecture, Engineering, and Construction (AEC) industry, AI is being deployed to eliminate "administrative waste" that has historically accounted for 30% of non-billable hours. Automated takeoff systems can now interpret plans with 97% accuracy, saving estimators roughly 90 minutes per sheet and allowing firms to bid on two to three times more projects with the same headcount. Companies like Joist have transformed proposal creation from an erratic, knowledge-dependent process into a structured, AI-powered workflow that connects directly to a firm's systems of record.

Similarly, in the legal and medical sectors, vertical AI is moving beyond simple assistance to the automation of entire high-friction processes. Harvey AI has embedded legal practitioner expertise into multi-layered verification systems that detect hallucinations and align with regulatory frameworks like HIPAA and SOC 2. These systems deliver a faster ROI than horizontal tools because they solve specific, high-cost bottlenecks such as prior authorization or legal clause extraction.

Industry Vertical | Specific AI Agent Application | Economic Impact/Metric |

Construction/AEC | Automated takeoff and bidding | 80% manual process automation |

Legal Services | Clause extraction and verification | 28% Am Law 100 penetration |

Sales Operations | Account workspace orchestration | 30% shorter deal cycles |

Healthcare | Clinical documentation/Medical scribe | HIPAA-compliant workflow reduction |

Banking/Credit | Decisioning and decision auditing | $15M Series A for credit analysis |

The market for vertical AI is predicted to reach ten times the size of the traditional SaaS market, potentially creating multiple companies valued at over $300 billion. The "Good, Better, Best" framework for founders suggests that the most successful vertical AI products do not just boost productivity; they tackle end-to-end workflows with "LLM magic" that was previously impossible, essentially replacing expensive human labor with high-utility digital agents.

Technical Maturity: The Shift from AI-Powered to AI-Native

The transition of Silicon Valley startups is also a story of architectural evolution. "AI-powered" systems, which were common during the 2023-2024 hype cycle, typically extended existing architectures with supplementary AI capabilities. These systems often relied on batch data movement and predefined pipelines, which struggled with real-time intelligence and autonomous operation. In contrast, "AI-native" startups are building systems where intelligence is the core design principle from the start.

AI-native architecture prioritizes real-time data streaming, event sourcing, and continuous learning. These systems are built around agents and orchestration layers that can act on insights directly within defined governance boundaries, rather than simply generating recommendations for human validation. Furthermore, AI-native products assume that the "first user" of the product is an AI system—an agent deciding whether a human will ever see the interface. This requires products to have "machine-consumable surfaces" and workflows optimized for AI decisions, featuring predictable timings, stable response shapes, and observable states.

Becoming AI-native also necessitates a cultural shift within the startup. Hiring priorities move away from pixel-obsessed frontend developers toward engineers who think in contracts, schemas, and event-driven architectures. Product managers must understand how LLMs read, rank, and chain calls, and transparency becomes a fundamental technical requirement to make the product "legible" to both machines and humans. This architectural edge allows startups to pivot and test more quickly than incumbents, who are often slowed by committee-driven decision-making and legacy technical debt.

The Talent Super-Cycle: Global Competition and Executive Migration

The rapid pivot to AI has intensified the region's "talent wars," creating a demand curve that has gone vertical since 2022. There is a critical scarcity of individuals capable of doing "frontier AI research," with only a few hundred PhDs graduating each year judged to meet the standards of the leading labs. This has driven total compensation packages for senior AI engineers to commonly exceed $1.5 million, with signing bonuses for experienced researchers routinely topping $1 million.

Silicon Valley's demographic and leadership structures are being reshaped by this competition. Because domestic talent pools are insufficient, labs and startups have become heavily reliant on international talent, particularly from China and India. In 2024, an analysis showed that 42% of AI research staff at U.S. companies with more than $1 billion in funding were born in one of these two countries. This has elevated the O-1 "extraordinary ability" visa to a critical workhorse for the region, as researchers with top-tier conference publications or contributions to foundational models like Llama 3 or GPT-4o can qualify for fast-tracked processing.

Talent Category | Typical Compensation (2025) | Key Recruitment Barrier |

Frontier AI Researcher | $1.5M - $3.0M total comp | Extreme global scarcity (<900/yr) |

Senior AI Engineer | $800k - $1.2M | Competition from Hyperscalers |

Fresh CS PhD | $500k - $750k signing bonus | Visa/H-1B lottery mess |

ML/Data Scientist | $175k - $213k base salary | Retention in high-churn environment |

The talent migration extends to the executive level, where proactive succession planning and internal career progression have become central to startup success. Despite the focus on AI, startups face challenges in retention, with 72% of executive roles still being filled externally. To combat this, companies are rethinking compensation strategies, though most plan to keep equity grants steady in 2025 as a signal of focus on stability amid economic uncertainty. The widespread integration of AI in HR processes has also emerged, though adoption is tempered by concerns over data security and the need for seamless integration into existing workforce strategies.

Risks and Regulatory Scrutiny: AI-Washing and Market Reckoning

The frantic race toward AI has inevitably led to "AI-washing"—the misrepresentation or overstatement of AI capabilities in products and services to gain a competitive advantage. This practice has become a significant reputational and financial risk, as stakeholders demand authenticity and regulators accelerate their oversight. In March 2024, the SEC coined the term and announced penalties against investment firms like Delphia and Global Predictions for falsely claiming their strategies were driven by proprietary machine learning.

AI-washing creates multiple levels of damage. Beyond regulatory fines—which appeared in 25% of AI-washing media coverage in 2025—misleading claims can trigger extensive due diligence that slows investment and increases costs for startups. Furthermore, the "cyclical nature of AI mistrust" forms when exaggerated claims lead to "AI booing"—public backlash against technologies that fail to meet inflated expectations. Research has found that as many as 20% of AI responses in some domains contain inaccuracies, and Google’s AI Overviews showed error rates as high as 26%, further fueling skepticism.

The socio-economic impact of the AI pivot is also evident in the labor market. In 2025, AI was cited as a reason for more than 54,000 layoffs, with Amazon alone reducing its headcount by 16,000 in January 2026 after making 14,000 reductions in late 2025. While some CEOs, like Marc Benioff, have attributed these cuts to the efficiency of AI agents, researchers have cautioned that many companies use AI as a financial justification for layoffs before they have a "mature, deployed AI application" ready to backfill the lost labor. This gap between the narrative of AI transformation and the reality of technical implementation represents a major risk for the Silicon Valley ecosystem’s long-term credibility.

Philosophical Underpinnings: Accelerationism and the Bias for Action

The rapid pivot of Silicon Valley is not just a technological or economic trend; it is deeply rooted in a cultural philosophy known as "Effective Accelerationism," or "e/acc". This movement advocates for unrestricted technological progress, specifically in AI, as the primary solution to human problems like poverty, war, and climate change. Proponents of e/acc, including influential figures like Marc Andreessen and OpenAI’s Will DePue, believe that technology's acceleration is inevitable and should be embraced to preserve the "light of consciousness".

The e/acc movement acts as a powerful counterweight to "doomers" or "decelerationists" who advocate for AI safety and regulation. It draws inspiration from transhumanism and extropianism, favoring "technocapital"—the combined effect of innovation and market forces—over government intervention. The movement was unmasked in 2023 to have been founded by Guillaume Verdon, a former Google engineer who promoted the ideology through memes and viral social media engagement to ensure its spread throughout the Silicon Valley consciousness.

This philosophy translates into a "bias for action" as a defining cultural value. In the Valley’s high-stakes environment, speed is a critical asset; waiting for perfect information can lead to missed opportunities and allow competitors to gain an advantage. This cultural value encourages founders to take calculated risks, experiment early, and iterate fast—even if it means failing frequently. Leadership at companies like Alphabet maintains this startup-like agility by prioritizing swift decision-making and rapid prototyping, frequently releasing early AI models to gather feedback and improve based on real-world user data.

Incumbent Response and Infrastructure Support

While the revolution is led by startups, Silicon Valley’s incumbents are not idle. Companies like Salesforce have launched "Agentforce," a platform for creating and managing agentic AI infrastructure. By October 2025, Salesforce reported explosive growth in the "Agentic Enterprise," with agent creation among early adopters increasing by 119% in the first six months of deployment. These agents are increasingly performing core business actions such as querying records, drafting emails, and summarizing customer interactions, demonstrating a compound annual growth rate (CAGR) of over 2,000% in customer service conversations.

Cloud infrastructure providers—AWS, Google, and Microsoft—have also become the backbone of the startup pivot by offering massive credit programs. AWS committed $230 million to accelerate generative AI startups, offering up to $1 million in credits to select cohorts. Google for Startups provides up to $350,000 in credits to AI-first companies, alongside access to its seventh-generation Tensor Processing Units (TPUs) like Ironwood.

Cloud Program | Maximum Credit Allotment | Key AI/ML Resources Provided |

AWS Activate / Accelerator | $1,000,000 | Amazon Bedrock, FM stacks, ML engineers |

Google for Startups Cloud | $350,000 | Vertex AI, Gemini 3, Ironwood TPUs |

Microsoft for Startups | $150,000 (Azure Credits) | Azure OpenAI, Llama/Phi models, Pegasus GTM |

NVIDIA Inception | 10,000 Inference Credits | GPU-optimized models, Clara healthcare platform |

These incumbents are leveraging their control over the technology ecosystem to benefit from the data center boom, even as they compete with the very startups they fund. The relationship between Big Tech firms and startups is symbiotic: startups provide the innovation and high-risk experimentation, while hyperscalers provide the compute power and infrastructure, essentially ensuring they "win" regardless of which individual AI startup achieves dominance.

Conclusion: The Finality of the Pivot

The total reorganization of Silicon Valley around artificial intelligence represents a permanent shift in the technological order. As the "Inference Gap" closes and on-device agentic AI becomes the default, the barriers between software and active task performance will continue to dissolve. Every startup is now an AI startup because the underlying economics of software have changed: the per-user subscription is a relic of the manual era, replaced by consumption-based models that reflect the vast range of activities digital agents can now conduct independently.

The path forward for the ecosystem will be defined by the tension between "unfettered innovation" and the need for "responsible implementation". While the e/acc philosophy drives the speed of development, the threat of AI-washing and the collapse of "thin wrappers" will eventually filter the market, favoring startups that build deep, vertical moats and intelligence-native architectures. In 2026, the question is no longer whether a startup uses AI, but whether an AI agent—interacting with that startup's product—knows exactly how to derive value from it. Those that achieve this machine-readability and agentic orchestration will define the next twenty years of Silicon Valley history.

Read More -

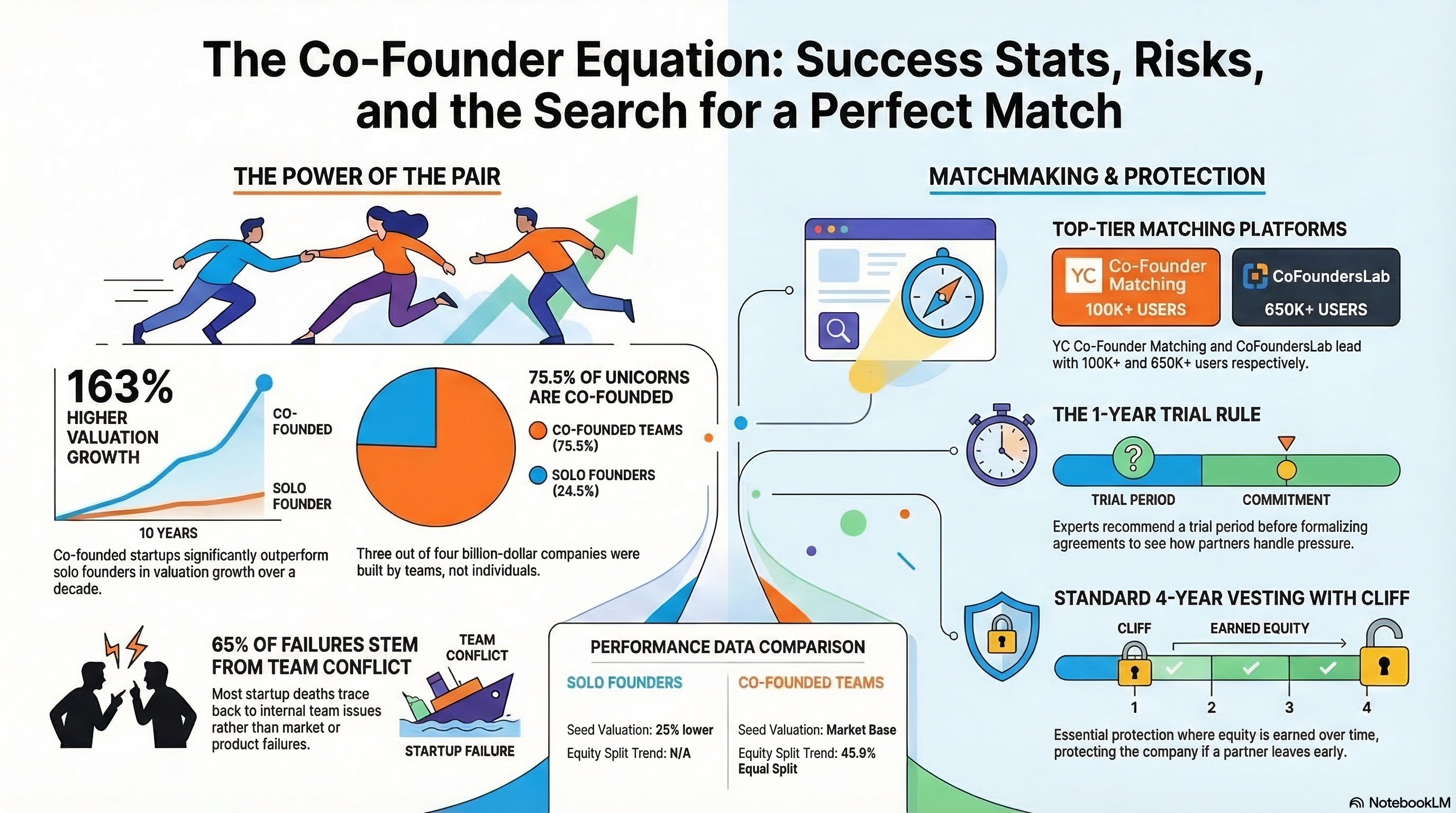

1. From Idea to MVP: A Step-by-Step Guide for Solo Founder

🔗 https://findnstart.com/blogs/from-idea-to-mvp-a-step-by-step-guide-for-solo-founder

2. How to Validate Your Startup Idea in 48 Hours for $0

🔗 https://findnstart.com/blogs/how-to-validate-your-startup-idea-in-48-hours-for-0

3. Remote vs. Local: Does Your Co-Founder Need to Live in the Same City?

🔗 https://findnstart.com/blogs/remote-vs-local-does-your-co-founder-need-to-live-in-the-same-city

4. The 2026 Startup Landscape: What Has Fundamentally Changed (and Why Founder Skills Matter More Than Ever)

5. The Most In-Demand Skills for Startup Founders in 2026

🔗 https://findnstart.com/blogs/the-most-in-demand-skills-for-startup-founders-in-2026

6. How to Find a Technical Co-Founder (Without a Six-Figure Salary)

🔗 https://findnstart.com/blogs/how-to-find-a-technical-co-founder-without-a-six-figure-salary

7. 5 Red Flags to Look for When Choosing a Startup Partner

🔗 https://findnstart.com/blogs/5-red-flags-to-look-for-when-choosing-a-startup-partner

8. How to Pitch Your Idea to Potential Co-Founders

🔗 https://findnstart.com/blogs/how-to-pitch-your-idea-to-potential-co-founders

9. How to Build a Portfolio that Attracts High-Growth Startup Founders

🔗 https://findnstart.com/blogs/how-to-build-a-portfolio-that-attracts-high-growth-startup-founders

10. Equity vs. Salary: How to Split Ownership with Your First Teammate

🔗 https://findnstart.com/blogs/equity-vs-salary-how-to-split-ownership-with-your-first-teammate

11. Why Joining an Early-Stage Startup is Better Than a Corporate Job

🔗 https://findnstart.com/blogs/why-joining-an-early-stage-startup-is-better-than-a-corporate-job

12. The Future of EdTech: Why Developers and Educators Need to Team Up Now

🔗 https://findnstart.com/blogs/the-future-of-edtech-why-developers-and-educators-need-to-team-up-now

13. The Architecture of Symbiosis: Analytical Perspectives on the Five Habits of Successful Startup Duos

14. Finding a Co-Founder in the AI Space: What Skills Should You Look For?

🔗 https://findnstart.com/blogs/finding-a-co-founder-in-the-ai-space-what-skills-should-you-look-for

15. Overcoming Analysis Paralysis and the Strategic Path to Execution

🔗 https://findnstart.com/blogs/overcoming-analysis-paralysis-and-the-strategic-path-to-execution

16. From College Project to Company: How to Find Your Student Co-Founder

🔗 https://findnstart.com/blogs/from-college-project-to-company-how-to-find-your-student-co-founder

17. How to Start a Startup While Working a Full-Time Job

🔗 https://findnstart.com/blogs/how-to-start-a-startup-while-working-a-full-time-job

18. How to Build a HealthTech Startup Without a Medical Degree

🔗 https://findnstart.com/blogs/how-to-build-a-healthtech-startup-without-a-medical-degree

19. The Solitary Architect: Executive Isolation in Entrepreneurship

20. The 2026 Guide to Launching a SaaS as a Solo Developer

21. What Sustainable Growth Actually Looks Like

🔗 https://findnstart.com/blogs/what-sustainable-growth-actually-looks-like

22. The Early Warning Signs Your Startup Is in Trouble

🔗 https://findnstart.com/blogs/the-early-warning-signs-your-startup-is-in-trouble

23. How to Grow Without Burning Out

🔗 https://findnstart.com/blogs/how-to-grow-without-burning-out

24. The Truth About “Runway” Most Founders Ignore

🔗 https://findnstart.com/blogs/the-truth-about-runway-most-founders-ignore

25. Revenue Solves More Problems Than Funding

🔗 https://findnstart.com/blogs/revenue-solves-more-problems-than-funding

🆕 Newly Added Articles

26. What No One Tells You About Being a Solo Founder

🔗 https://findnstart.com/blogs/what-no-one-tells-you-about-being-a-solo-founder

27. Why Smart People Quit High-Paying Jobs to Build Startups (And Why Most Regret It)

28. Why Most Startup Advice on Twitter Is Dangerous

🔗 https://findnstart.com/blogs/why-most-startup-advice-on-twitter-is-dangerous

29. Decision Fatigue: The Silent Startup Killer

🔗 https://findnstart.com/blogs/decision-fatigue-the-silent-startup-killer

30. Fear vs Logic: How Founders Actually Make Decisions

🔗 https://findnstart.com/blogs/fear-vs-logic-how-founders-actually-make-decisions

31. How Overthinking Destroys Early Momentum

🔗 https://findnstart.com/blogs/how-overthinking-destroys-early-momentum

32. Ideas Don’t Scale. Systems Do.

🔗 https://findnstart.com/blogs/ideas-dont-scale-systems-do

33. The First Hire That Actually Matters

🔗 https://findnstart.com/blogs/the-first-hire-that-actually-matters

34. How the First 100 Users Decide Your Startup’s Fate

🔗 https://findnstart.com/blogs/how-the-first-100-users-decide-your-startups-fate

35. Why Your Startup Doesn’t Need Growth — It Needs Focus

🔗 https://findnstart.com/blogs/why-your-startup-doesnt-need-growthit-needs-focus

36. Why Most Startups Die Quietly

🔗 https://findnstart.com/blogs/why-most-startups-die-quietly

37. Lessons Learned Too Late by First-Time Founders

🔗 https://findnstart.com/blogs/lessons-learned-too-late-by-first-time-founders

38. The Myth of the “Overnight Success” Startup

🔗 https://findnstart.com/blogs/the-myth-of-the-overnight-success-startup

Want to calculate the equity for your cofounder?

Nail your cap table before you sign. Whether you're splitting equity with a co-founder or planning your next funding round, our Equity Calculator gives you precision in seconds

Equity calculator →