Why Distribution Is the Hardest Part of Building in India

March 9, 2026 by Harshit Gupta

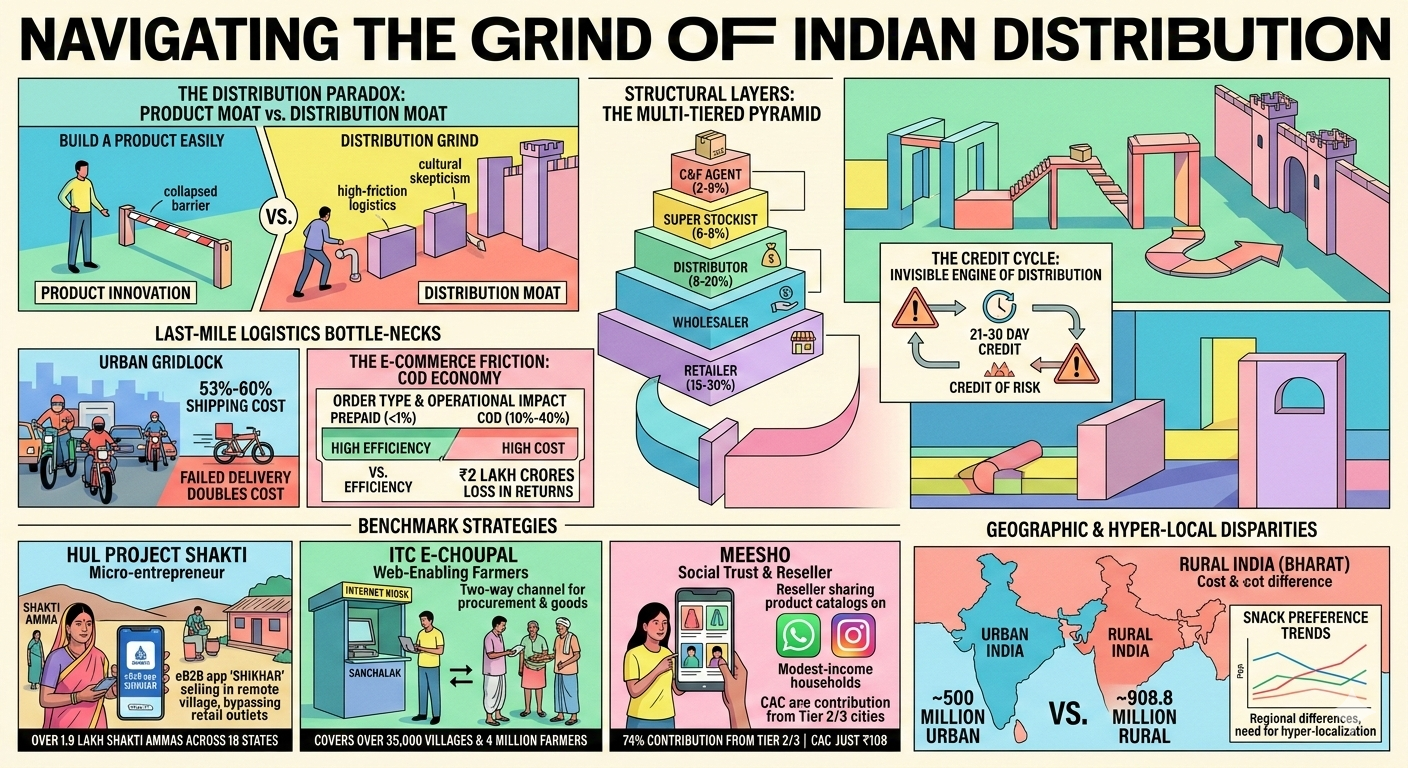

The contemporary landscape of Indian entrepreneurship is defined by a fundamental paradox: while the barriers to building products have collapsed due to the democratization of technology and capital, the barriers to reaching the consumer remain formidable and, in many sectors, have actually intensified. For the modern founder or venture capitalist, the "distribution problem" represents the most significant existential threat to scaling a business within the subcontinent. It is a challenge characterized by a unique confluence of fragmented retail networks, high-friction logistics, deep-seated cultural skepticism, and a regulatory environment that, while improving, still demands significant compliance bandwidth. The prevailing sentiment among industry veterans is that building is the "fun part," but distribution is the "soul crusher". This structural reality suggests that in India, a product moat is increasingly transient, whereas a distribution moat—the ability to reliably and cost-effectively deliver value to a highly price-sensitive and geographically dispersed population—remains the ultimate determinant of long-term commercial viability.

The Strategic Shift from Product Innovation to Distribution Resilience

The evolution of the Indian startup ecosystem has reached a stage where product-market fit (PMF) is no longer a sufficient condition for success. Many entrepreneurs focus intensely on product development while neglecting the equally critical aspect of how that product will move through the market. This oversight often results in high-quality solutions that fail to achieve visibility or revenue because they cannot bridge the "last mile" to the paying customer. The distribution problem encompasses market reach, customer engagement, scalability, and cost efficiency. Without a robust delivery strategy, the best products in the Indian market succumb to substitution by cheaper, more accessible alternatives.

The challenge is further complicated by the "politeness trap" inherent in Indian consumer psychology. Founders often receive emotionally supportive feedback during the early stages of validation, which they mistake for genuine market demand. Cultural conditioning in India often prevents users from providing harsh, direct criticism. Consequently, a startup may see a high number of initial sign-ups only to witness those users "go silent" or never return after a single trial. This phenomenon suggests that the value was either not immediate or the friction of regular use was too high. True validation in this environment requires "early sacrifice"—measuring whether a user is willing to commit time, money, or reputation before the product is even fully built. The lack of such micro-commitments often signals a "good-to-have" rather than a "must-have" product, a distinction that is fatal in a market where consumers prioritize utility and essential needs over novelty.

Furthermore, the "attention economy" in India has become prohibitively expensive. In the era of ubiquitous social media and AI-driven content, acquiring a customer’s attention requires not just sharp positioning but significant capital. As organic reach declines and ad costs rise, distribution becomes the primary bottleneck. The ability to find paying customers in a crowded space, where users already have multiple alternatives, is the real grind that separates successful enterprises from those that stagnate at the minimum viable product stage.

Structural Layers of Traditional Distribution: The Multi-Tiered Pyramid

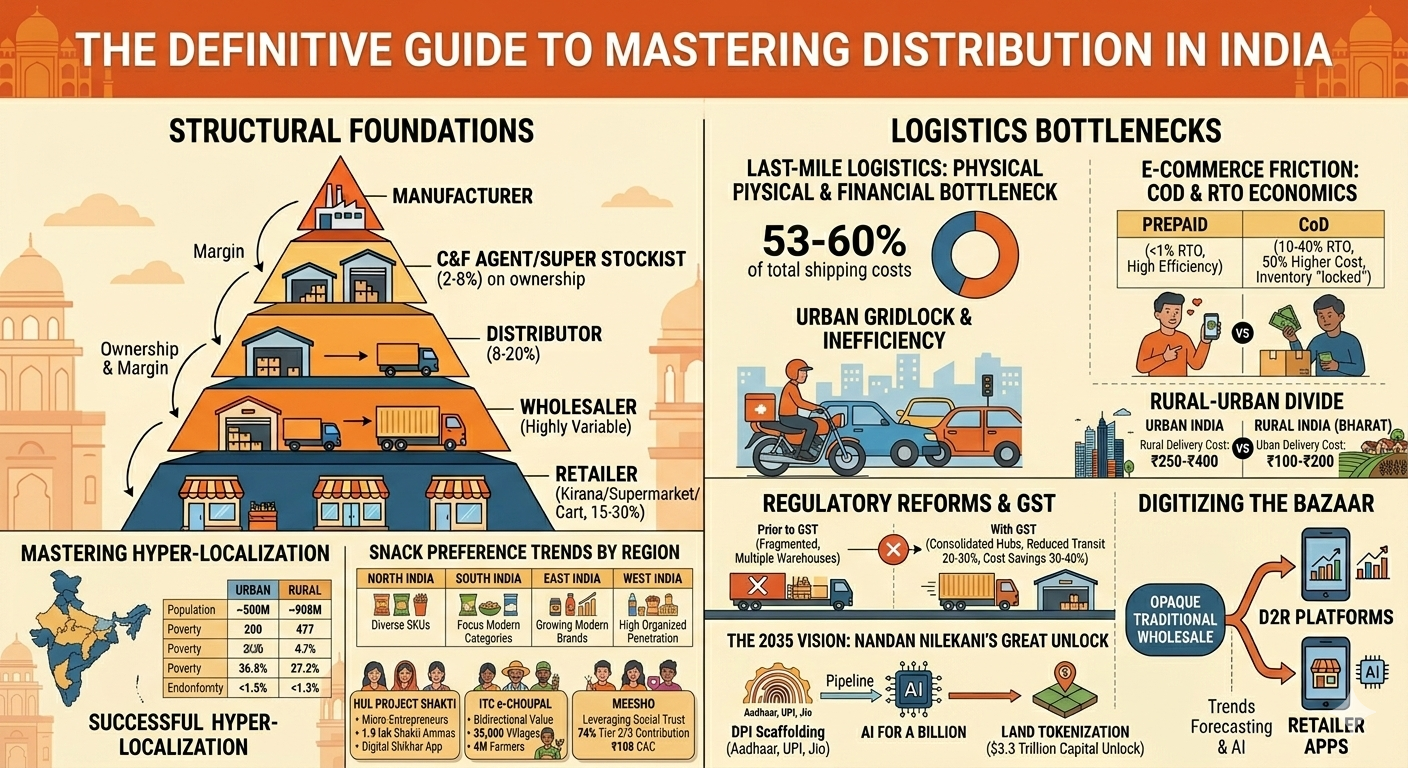

To understand why distribution is the hardest part of building in India, one must first deconstruct the traditional multi-layered system that has dominated the movement of goods for decades. This system is a sophisticated pyramid designed to overcome the fragmentation of the Indian retail landscape, which consists of millions of independent shops.

The Hierarchy of Intermediaries and Margin Economics

The standard movement of goods involves several distinct layers of intermediaries, each extracting a margin and providing a specific service related to warehousing, logistics, or credit.

Intermediary Role | Function and Ownership | Typical Commission/Margin |

C&F (Carrying and Forwarding) Agent | 3rd party logistics and warehousing provider; does not take ownership of goods. | 2%−8% |

Super Stockist | Small-scale C&F agent with focus on regional logistics and some sales activities. | 6%−8% |

Distributor | Direct partner of the brand; takes ownership, manages a territory, and provides credit. | 8%−20% |

Wholesaler | Bulk buyer without formal brand partnership; sells to retailers based on demand. | Highly variable; often higher than distributors. |

Retailer | The final point of sale (Kirana, supermarket, or mobile cart). | 15%−30% |

The distributor acts as an extension of the brand, taking ownership of the inventory once it leaves the C&F agent. This entity is responsible for "secondary sales"—moving products from the warehouse to the retailer. A single stockist or distributor might serve between 500 to 1,000 retailers in a specific proximity. The link between the manufacturer and this network is managed by a hierarchy of sales professionals, including Area Sales Managers (ASM) and Territory Sales Managers (TSM), who supervise the "beats" or "routes" taken by sales representatives. A typical representative visits approximately 40 stores per day, covering six beats per week to ensure consistent product availability.

The Credit Cycle: The Invisible Engine of Distribution

The Indian distribution system is fundamentally a credit-driven ecosystem. Manufacturers typically offer 21 to 30 days of credit to their distributors. To move the stock further, distributors must then extend credit to retailers, which carries immense risk. If a retailer defaults or is revealed as a fraudulent actor, the distributor's working capital can be wiped out, potentially ending the partnership and halting the brand's reach in that territory.

This reliance on informal credit is why distribution moats are so difficult to disrupt. A new entrant cannot simply offer a better product; they must often offer better credit terms or demonstrate "consumer pull" so strong that retailers are willing to pay cash for the stock. For established brands with high demand, retailers may accept thinner margins because the volume and velocity of sales provide sufficient absolute profit. For a new brand, however, the lack of "pull" means they must compensate the channel with higher margins, which can erode the unit economics of the business before it ever reaches scale.

The Kirana Ecosystem: Resilience and the Digitization Challenge

The bedrock of Indian retail is the Kirana store—the neighborhood grocery shop. There are approximately 13 to 15 million such stores in India, accounting for over 85% of the total retail market and generating over $800 billion in annual revenue. These stores thrive on proximity, personal relationships, and a deep understanding of their hyperlocal consumer base.

The Evolution from Paper to App

Historically, Kirana stores operated entirely on intuition and paper ledgers. Transactions were cash-based, and customer credit was managed in handwritten notebooks. The 2016 demonetization wave was a pivotal moment, forcing these retailers to adopt digital payments through UPI and QR codes. This was followed by the rise of eB2B platforms like Udaan, Jumbotail, and ElasticRun, which allowed Kiranas to order inventory online with doorstep delivery, thereby reducing their dependence on multiple local distributors.

Digitization has also entered the internal operations of the Kirana. Ledger solutions like Khatabook and Vyapar have automated credit tracking and GST invoicing. Platforms like Badho further modernize the chain by connecting retailers directly with brands and authorized distributors, providing real-time visibility into product catalogs and promotions.

Competition and the Quick Commerce Threat

Despite their resilience, Kirana stores are facing significant pressure from the rise of quick commerce. Platforms that promise delivery in 10 to 20 minutes are eroding the Kirana's advantage of proximity. To survive, 80% of Kirana owners now feel the need to adopt online operations and digital storefronts. Partnerships with initiatives like the Open Network for Digital Commerce (ONDC) are seen as critical for these small retailers to reclaim lost business by offering home delivery and loyalty programs.

The comparative advantage of traditional retail over quick commerce remains rooted in perception and cost. Consumers still perceive traditional retail as offering higher product quality, better pricing, and easier return processes. However, as quick commerce scales and improves its quality control, the Kirana must evolve from a simple point of sale into a digitally integrated participant in a modern supply chain.

Last-Mile Logistics: The Financial and Physical Bottleneck

In India, the "last mile"—the final leg of the journey from a distribution center to the consumer's doorstep—is the most expensive part of the supply chain, accounting for up to 53% to 60% of total shipping costs. The challenges here are both infrastructural and behavioral.

Urban Gridlock and Navigational Inefficiency

Indian cities like Mumbai, Bengaluru, and Delhi are infamous for their traffic congestion, which is responsible for 60% of all delivery delays. Research indicates that delivery times in the central areas of Kolkata and Old Delhi are up to 35% longer than in newer urban zones. This congestion is not just a time problem; it is a financial one. Every minute spent in traffic increases fuel consumption and driver wages while reducing the daily delivery capacity per vehicle.

Furthermore, the lack of standardized addressing in India makes finding a specific house or shop "like searching for a needle in a haystack". Couriers often rely on landmark-based directions, leading to multiple failed attempts. In urban settings, where the working population is often away during standard delivery hours, and gated communities have strict security protocols, the rate of failed delivery attempts is high. Each failed attempt doubles the delivery cost, as the package must be returned to the hub and re-routed.

The E-commerce Friction: CoD and RTO Economics

The most unique and challenging aspect of the Indian e-commerce market is the continued dominance of Cash on Delivery (CoD). Despite the government's push for digital payments, 60% to 65% of online transactions still happen via CoD. CoD is a "lifeline" for consumers in Tier 2 and Tier 3 cities who cite trust and ease of return as their primary reasons for avoiding prepaid methods.

However, CoD transactions cost platforms up to 50% more than prepaid ones. They require multiple delivery attempts, involve the physical handling and reconciliation of cash, and—most importantly—have a significantly higher "Return to Origin" (RTO) rate.

Order Type | Typical RTO Rate | Operational Impact |

Prepaid | <1% | High efficiency; immediate cash flow. |

CoD | 10%−40% | High logistics cost; inventory "locked" in transit; cash handling risks. |

Social Commerce CoD | 20%−40% | Severe margin erosion for D2C brands. |

The economic impact of returns is staggering, with estimated annual losses of nearly ₹2 lakh crores in the Indian market due to reverse logistics, refund costs, and unsellable inventory. Brands are responding with "partial CoD" (requiring a small token payment upfront), AI-driven risk assessment of pin codes, and incentives for consumers to switch to prepaid modes.

Geographic Disparities: The Rural-Urban Divide in Reach

The distribution challenge in India is deeply bifurcated by geography. While urban centers represent modern consumption and advanced infrastructure, rural India—where 70% of the land area and 900 million people are located—remains a different "game" entirely.

The "Bharat" Accessibility Conundrum

Rural areas continue to grapple with underdeveloped infrastructure, limited power supply, and patchy telecom connectivity. Delivering to "deep corners" of the country is significantly more expensive, with average rural delivery costs ranging from ₹250 to ₹400, compared to ₹100 to ₹200 in urban areas.

Parameter | Urban India | Rural India (Bharat) |

Population (2022) | ~500 Million | ~908.8 Million |

Poverty Rate Decline | Notable progress | Larger absolute decline due to higher base. |

Health Indicators | Better access; lower mortality | Lagging; high need for investment. |

Primary Economy | Services and Industry | Agrarian; traditional values. |

Social Structure | Nuclear families; individualistic | Extended families; kinship-based. |

The spatial inequality is stark: only 13 out of 788 districts contribute to half of India's GDP. The top 10% of the population earns 60% of the national income, while the bottom 50% averages just ₹71,000 annually. This income disparity means that rural distribution must be highly cost-effective to be viable. Conventional business models often find rural markets unreachable because the cost of delivery exceeds the potential profit from low-value transactions.

Benchmark Strategies: Successful Distribution Models in India

Several organizations have successfully cracked the Indian distribution puzzle by innovating their delivery mechanisms rather than just their products. These cases serve as a blueprint for overcoming the structural barriers of the market.

HUL Project Shakti: Turning Consumers into Distributors

Launched in 2001, Hindustan Unilever’s Project Shakti addressed the unviability of rural markets by empowering underprivileged women as micro-entrepreneurs.

The Model: HUL recruits local women, known as "Shakti Ammas," and trains them to sell products door-to-door in their villages. These women become local brand endorsers and earn a commission on sales, often doubling their household income.

Infrastructure Bypass: This model moves the marketplace frontline away from local retail outlets—who might champion other products—directly into the homes of families in the remotest areas.

Digital Integration: Shaktis now use the eB2B app "Shikhar" to place orders with authorized distributors, bringing digital efficiency to the door-to-door model.

Scale: Project Shakti currently encompasses over 1.9 lakh "Shakti Ammas" across 18 states, reaching hundreds of millions of people in villages that were previously "media-dark" and inaccessible to traditional advertising.

ITC e-Choupal: Web-Enabling the First Mile

ITC’s e-Choupal initiative revolutionized rural procurement and distribution by addressing the information asymmetry that historically disadvantaged farmers.

The Model: ITC established internet kiosks in villages, run by a community member called a "Sanchalak." Farmers use the kiosks to check global closing prices for their crops, allowing them to bypass the arbitrary pricing of traditional "mandis" (government markets).

Bidirectional Value: While initially a procurement tool, the kiosks became a two-way channel. Farmers use the kiosks to order high-quality seeds, fertilizers, and consumer goods from ITC at lower prices than local traders.

Logistical Innovation: By aggregating village demand through the Sanchalak, ITC significantly lowered its logistics costs. The initiative now covers over 35,000 villages and serves over 4 million farmers.

Meesho: Leveraging Social Trust and Tier 2/3 Focus

Meesho disrupted the e-commerce landscape by recognizing that Tier 2 and Tier 3 consumers prefer a trust-based, social selling model rather than the "anonymous" interface of giants like Amazon or Flipkart.

The Reseller Model: Meesho empowers individuals (mostly housewives) to act as resellers. They share product catalogs with their social circles on WhatsApp and Instagram, adding a margin to the base price.

Affordability: By not owning warehouses and maintaining a reseller-centric model, Meesho kept its costs low. Most products are priced under ₹500 to appeal to modest-income households.

Vernacular Reach: Meesho implemented multi-channel advertising in nine languages and leveraged micro-influencers to build brand credibility quickly and cheaply.

Results: By 2024, Meesho achieved a 74% contribution from Tier 2/3 customers and a customer acquisition cost (CAC) of just ₹108, significantly lower than the industry average.

Hyper-Localization: Cultural Diversity as a Distribution Variable

India is not a single homogenous market but a "mosaic of micro-markets" influenced by geography, religion, and regional identity. For a national brand, success is impossible without "glocalization"—adapting to the local environment while maintaining global standards.

Linguistic and Cultural Immersion

With over 60% of Indian internet users preferring content in their native tongue, language is the primary bridge to the consumer. However, localization goes beyond translation; it requires "transcreation"—reimagining messages to fit the local emotional context and dialect.

Festivals as Amplifiers: Festivals like Diwali, Pongal, and Bihu are massive amplifiers for growth marketing. Brands that align their campaigns with local celebrations can foster a deep sense of belonging.

Rituals as Trust Portals: Hyperlocal campaigns that root themselves in community rituals and local customs show engagement rates up to 30% higher than standardized campaigns.

Product and Pricing Adaptation

Consumer purchasing power varies wildly from one pin code to the next. A discount that works in an affluent urban center like Bandra might be completely unappealing in a price-sensitive rural market.

Region | Snack Preference Trends | Implications for Distribution |

North India | Balanced (52% Western, 48% Ethnic) | Diverse SKUs needed; focus on variety. |

South India | High Western Preference (67%) | Focus on modern snack categories and brands. |

East India | High Western Preference (61%) | Growing market for organized Western brands. |

West India | Lean toward Western (56%) | Competitive space with high organized penetration. |

Successful brands like Parle-G maintain deep-rooted distribution networks that ensure their product is available in the remotest village at a consistent price point—a feat that many modern startups struggle to emulate.

The Regulatory and Compliance Landscape: GST and Beyond

One of the historical reasons distribution was so difficult in India was the fragmented tax system. Before the Goods and Services Tax (GST), each state was its own market with its own tax rates and regulations.

The GST Structural Shift: From Tax Optimization to Operational Efficiency

Prior to GST, logistics strategies were driven by tax avoidance. Companies opened warehouses in every state to avoid the Central Sales Tax (CST) on interstate stock transfers. This led to a highly fragmented and inefficient warehouse network.

With the introduction of GST, the need for state-specific warehouses was eliminated. This led to:

Warehouse Consolidation: Companies have closed smaller units and moved to large, centralized hubs equipped with automation and modern inventory management.

Reduced Transit Times: The removal of interstate checkpoints has reduced transportation times by up to 20%−30%.

Cost Savings: Operational logistics costs have been reduced by 30% to 40% for many sectors, making Indian products more competitive.

Ongoing Regulatory Pain Points

Despite the success of GST, regulatory complexities remain a deterrent to investment. Lengthy approval processes for land acquisition, frequent changes in tax filings, and liquidity blockage due to delayed input tax credits continue to plague small and medium enterprises. Furthermore, petroleum products and alcohol remain outside the GST framework, meaning they are still subject to varied state-level excise duties and VAT.

The introduction of the E-Way Bill system was intended to track the movement of goods and prevent tax evasion, but it adds another layer of compliance for businesses. Failure to comply with E-Way Bill rules can lead to the seizure of vehicles and goods, adding significant operational risk to the distribution process.

Digitizing the Bazaar: B2B Integration and Wholesale Opacity

While the retail segment has digitized rapidly, the traditional wholesale "bazaars" remain a major hurdle for modern distribution. These markets, like Sadar Bazaar in Delhi or Johari Bazaar in Jaipur, operate on relationship-based pricing and "gut-driven" decisions.

The Problem of Opacity and Asymmetry

In traditional wholesale, there is no standardization of pricing. A retailer in Mumbai might pay 30% more for the same product than a retailer in Delhi simply due to broker markups and information asymmetry. Finding new suppliers historically required physical travel to these hubs, and transactions were hampered by a chronic "working capital crunch" caused by 90-day credit cycles.

Disruptive D2R Platforms

New B2B startups are bypassing the traditional marketplace model by building their own direct-to-retailer (D2R) platforms. By aggregating demand from thousands of small retailers, these platforms use their volume to negotiate directly with manufacturers, passing the savings to the shopkeepers. These startups also use AI for trend forecasting, helping manufacturers produce what will actually sell rather than relying on guesswork—a major shift in categories like home decor and textiles where styles change seasonally.

However, the "trust deficit" remains high. Wholesale buyers are often skeptical of ordering high-value items without seeing them in person. Onboarding older-generation wholesalers requires significant training and a "hand-holding" process that can take 18 to 24 months.

Consumer Psychology: Trust, Status, and the Soul of Consumption

A nuanced understanding of the Indian consumer is critical for anyone building a distribution moat. Kunal Shah, founder of CRED, argues that Indian consumer psychology is fundamentally different from Western models, favoring "soulfulness" over standardization.

Trust as a Collective Aggregate

In India, trust is often aggregated in large, established entities. Consumers are inherently skeptical of startups or new brands that have not yet proven their "staying power". This is why brand building in India is synonymous with distribution—if a product is not visible on the shelf of the trusted neighborhood Kirana or in the hands of a trusted social reseller, it effectively does not exist.

Status and Spending Patterns

Spending patterns in India are heavily influenced by status-based values. While the "consumption class" is often cited as being 400 to 500 million people, the truly profitable core is much smaller—approximately 20 to 30 million people who drive 80% of the business for platforms like Zomato or Swiggy. These users prioritize "soul" and "desire" over pure utility, and they often invest in shared spaces and luxury goods as markers of social progression.

For a startup, focusing on the right set of customers is more important than achieving mass scale early on. A resilient business in India is built by starting with a core cohort and then "chipping away" to expand to other cohorts.

The 2035 Vision: Nandan Nilekani’s Great Unlock

Looking toward the future, Nandan Nilekani, co-founder of Infosys, predicts that India will host one million startups by 2035. This growth will be powered by a "virtuous cycle" where successful founders reinvest their capital and knowledge into the next generation of ventures.

Digital Public Infrastructure (DPI) as Scaffolding

The "invisible scaffolding" of India's distribution future is its Digital Public Infrastructure—Aadhaar, UPI, and the rollout of Reliance Jio. These systems have already formalised significant portions of the economy. The next phase will involve:

AI for a Billion: Scaling Artificial Intelligence to make it accessible through regional languages and intuitive, voice-based interfaces.

Land Tokenization: Nilekani believes that tokenizing land assets can unlock $3.3 trillion in capital, providing the collateral needed for MSMEs and farmers to invest in better distribution and productivity.

Tier 2/3 Entrepreneurship: Nearly half of all Indian startups are now based in smaller cities, solving region-specific problems—such as Apnamart, a retail chain focused on smaller towns.

The ONDC Experiment

The Open Network for Digital Commerce (ONDC) is a government-backed initiative aimed at breaking the duopoly of major e-commerce platforms. By unbundling the components of a transaction—search, order, payment, and delivery—ONDC allows small retailers and logistics providers to participate in a unified digital network. This could potentially democratize distribution, allowing a local Kirana store to compete on price and speed with national giants.

Conclusion: Mastering the Grind of Indian Distribution

Distribution is the hardest part of building in India because it requires solving a multi-dimensional puzzle involving physical geography, ingrained consumer behavior, and structural economic hurdles. A superior product is merely the "table stakes" for entering the market. The real battle is won through:

Navigational Resilience: Building systems that can overcome the high costs of last-mile gridlock and non-standardized addressing.

Trust Intermediation: Leveraging existing social networks (as Meesho did) or community leaders (as ITC and HUL did) to bridge the trust deficit.

Financial Ingenuity: Managing the precarious credit cycle of the traditional distributor-retailer network while encouraging a shift to prepaid digital transactions.

Regulatory Agility: Exploiting the efficiencies of the GST regime while navigating the lingering complexities of state-level regulations.

As the Indian economy grows toward its $8 trillion target, the companies that thrive will not be those with the most innovative algorithms, but those with the most robust and adaptive distribution moats. Distribution is not just a logistics function; it is the essence of the Indian market—a vibrant, chaotic, and ultimately rewarding challenge for those willing to endure the "soul-crushing" grind of the last mile.

Read More -

1. From Idea to MVP: A Step-by-Step Guide for Solo Founder

🔗 https://findnstart.com/blogs/from-idea-to-mvp-a-step-by-step-guide-for-solo-founder

2. How to Validate Your Startup Idea in 48 Hours for $0

🔗 https://findnstart.com/blogs/how-to-validate-your-startup-idea-in-48-hours-for-0

3. Remote vs. Local: Does Your Co-Founder Need to Live in the Same City?

🔗 https://findnstart.com/blogs/remote-vs-local-does-your-co-founder-need-to-live-in-the-same-city

4. The 2026 Startup Landscape: What Has Fundamentally Changed (and Why Founder Skills Matter More Than Ever)

5. The Most In-Demand Skills for Startup Founders in 2026

🔗 https://findnstart.com/blogs/the-most-in-demand-skills-for-startup-founders-in-2026

6. How to Find a Technical Co-Founder (Without a Six-Figure Salary)

🔗 https://findnstart.com/blogs/how-to-find-a-technical-co-founder-without-a-six-figure-salary

7. 5 Red Flags to Look for When Choosing a Startup Partner

🔗 https://findnstart.com/blogs/5-red-flags-to-look-for-when-choosing-a-startup-partner

8. How to Pitch Your Idea to Potential Co-Founders

🔗 https://findnstart.com/blogs/how-to-pitch-your-idea-to-potential-co-founders

9. How to Build a Portfolio that Attracts High-Growth Startup Founders

🔗 https://findnstart.com/blogs/how-to-build-a-portfolio-that-attracts-high-growth-startup-founders

10. Equity vs. Salary: How to Split Ownership with Your First Teammate

🔗 https://findnstart.com/blogs/equity-vs-salary-how-to-split-ownership-with-your-first-teammate

11. Why Joining an Early-Stage Startup is Better Than a Corporate Job

🔗 https://findnstart.com/blogs/why-joining-an-early-stage-startup-is-better-than-a-corporate-job

12. The Future of EdTech: Why Developers and Educators Need to Team Up Now

🔗 https://findnstart.com/blogs/the-future-of-edtech-why-developers-and-educators-need-to-team-up-now

13. The Architecture of Symbiosis: Analytical Perspectives on the Five Habits of Successful Startup Duos

14. Finding a Co-Founder in the AI Space: What Skills Should You Look For?

🔗 https://findnstart.com/blogs/finding-a-co-founder-in-the-ai-space-what-skills-should-you-look-for

15. Overcoming Analysis Paralysis and the Strategic Path to Execution

🔗 https://findnstart.com/blogs/overcoming-analysis-paralysis-and-the-strategic-path-to-execution

16. From College Project to Company: How to Find Your Student Co-Founder

🔗 https://findnstart.com/blogs/from-college-project-to-company-how-to-find-your-student-co-founder

17. How to Start a Startup While Working a Full-Time Job

🔗 https://findnstart.com/blogs/how-to-start-a-startup-while-working-a-full-time-job

18. How to Build a HealthTech Startup Without a Medical Degree

🔗 https://findnstart.com/blogs/how-to-build-a-healthtech-startup-without-a-medical-degree

19. The Solitary Architect: Executive Isolation in Entrepreneurship

20. The 2026 Guide to Launching a SaaS as a Solo Developer

21. What Sustainable Growth Actually Looks Like

🔗 https://findnstart.com/blogs/what-sustainable-growth-actually-looks-like

22. The Early Warning Signs Your Startup Is in Trouble

🔗 https://findnstart.com/blogs/the-early-warning-signs-your-startup-is-in-trouble

23. How to Grow Without Burning Out

🔗 https://findnstart.com/blogs/how-to-grow-without-burning-out

24. The Truth About “Runway” Most Founders Ignore

🔗 https://findnstart.com/blogs/the-truth-about-runway-most-founders-ignore

25. Revenue Solves More Problems Than Funding

🔗 https://findnstart.com/blogs/revenue-solves-more-problems-than-funding

26. What No One Tells You About Being a Solo Founder

🔗 https://findnstart.com/blogs/what-no-one-tells-you-about-being-a-solo-founder

27. Why Smart People Quit High-Paying Jobs to Build Startups (And Why Most Regret It)

28. Why Most Startup Advice on Twitter Is Dangerous

🔗 https://findnstart.com/blogs/why-most-startup-advice-on-twitter-is-dangerous

29. Decision Fatigue: The Silent Startup Killer

🔗 https://findnstart.com/blogs/decision-fatigue-the-silent-startup-killer

30. Fear vs Logic: How Founders Actually Make Decisions

🔗 https://findnstart.com/blogs/fear-vs-logic-how-founders-actually-make-decisions

31. How Overthinking Destroys Early Momentum

🔗 https://findnstart.com/blogs/how-overthinking-destroys-early-momentum

32. Ideas Don’t Scale. Systems Do.

🔗 https://findnstart.com/blogs/ideas-dont-scale-systems-do

33. The First Hire That Actually Matters

🔗 https://findnstart.com/blogs/the-first-hire-that-actually-matters

34. How the First 100 Users Decide Your Startup’s Fate

🔗 https://findnstart.com/blogs/how-the-first-100-users-decide-your-startups-fate

35. Why Your Startup Doesn’t Need Growth — It Needs Focus

🔗 https://findnstart.com/blogs/why-your-startup-doesnt-need-growthit-needs-focus

36. Why Most Startups Die Quietly

🔗 https://findnstart.com/blogs/why-most-startups-die-quietly

37. Lessons Learned Too Late by First-Time Founders

🔗 https://findnstart.com/blogs/lessons-learned-too-late-by-first-time-founders

38. The Myth of the “Overnight Success” Startup

🔗 https://findnstart.com/blogs/the-myth-of-the-overnight-success-startup

Want to calculate the equity for your cofounder?

Nail your cap table before you sign. Whether you're splitting equity with a co-founder or planning your next funding round, our Equity Calculator gives you precision in seconds

Equity calculator →