The Role of Corporate Venture Capital in Brazilian Startups

March 9, 2026 by Harshit Gupta

The Brazilian venture capital landscape has undergone a profound structural metamorphosis over the last decade, transitioning from an era of exuberant, liquidity-driven expansion into a disciplined, strategically aligned maturity. In the center of this evolution lies Corporate Venture Capital (CVC), which has shifted from a peripheral experimentation tool used by a handful of forward-thinking incumbents into a cornerstone of the national innovation strategy. As of the mid-2020s, CVC in Brazil represents not only a source of funding but a critical mechanism for industrial modernization, decarbonization, and digital inclusion within Latin America’s largest economy. The resilience of the Brazilian market, even during the global "Venture Capital Winter" of 2023, underscores a unique domestic dynamic where corporate balance sheets have stepped in to fill the void left by retreating international financial investors.

Macroeconomic Foundations and the 2021-2026 Cycle

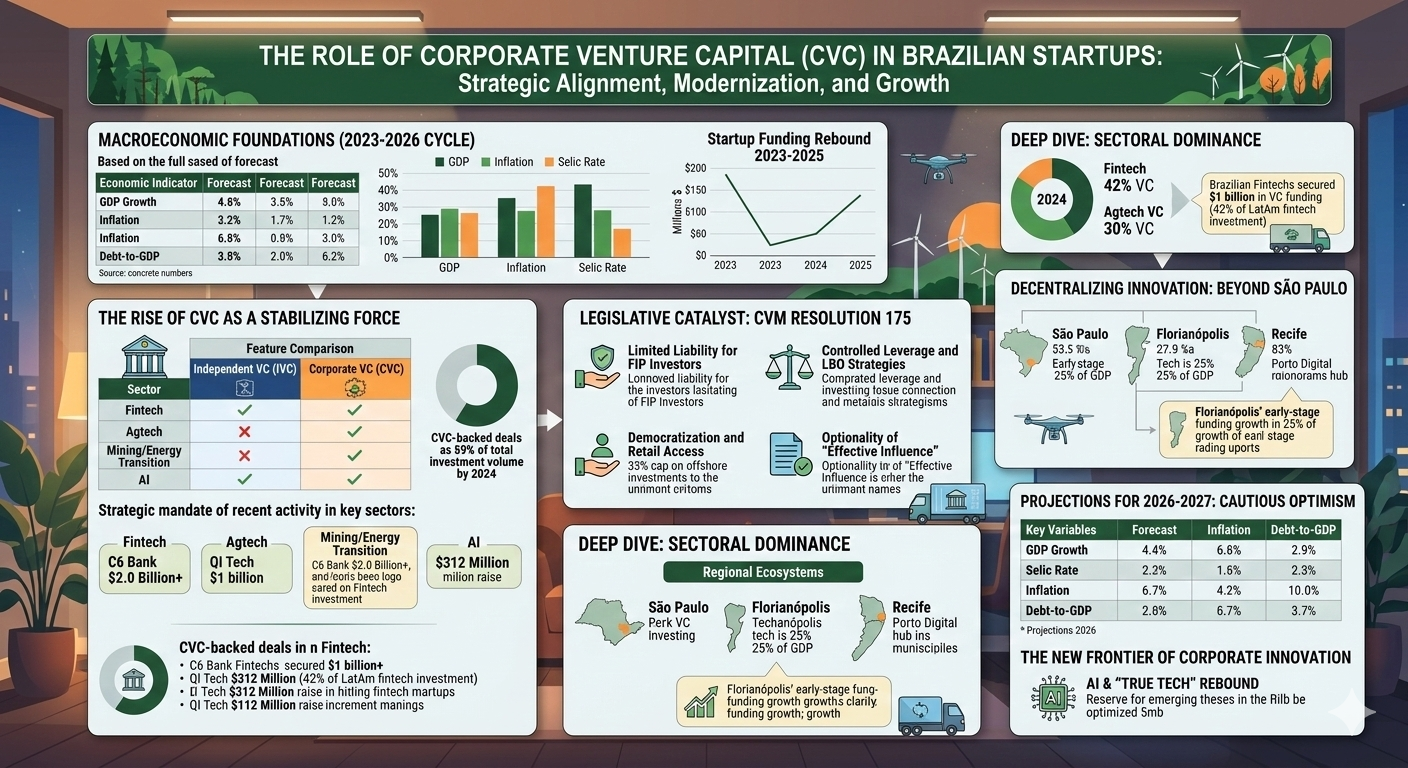

The trajectory of Brazilian startups cannot be untangled from the broader macroeconomic volatility that characterizes the region. Following a recovery in 2021 where Gross Domestic Product (GDP) grew by 4.6 percent, the economy faced a period of steady but slow performance, with growth rates of 2.9 percent in 2022 and accelerating slightly to 3.2 and 3.4 percent in 2023 and 2024. This acceleration was largely fueled by low unemployment, which hit a notable low of 6.2 percent by the end of 2024, and increased government expenditures under the Lula administration’s "New Industrial Policy". However, this growth came at the cost of significant fiscal pressure, with the nominal budget deficit standing at 8.45 percent of GDP in 2024 and the debt-to-GDP ratio climbing to 76.1 percent.

For venture capital, the most critical macroeconomic variable has been the interest rate environment. To combat inflation, the Central Bank of Brazil (BCB) maintained a restrictive monetary policy, with the Selic rate reaching as high as 15 percent by mid-2025. High interest rates naturally create a "crowding out" effect for venture capital, as investors find attractive, low-risk returns in government bonds, thereby increasing the hurdle rate for startup investments. Nevertheless, projections for 2026 and 2027 suggest a forthcoming easing cycle, with inflation expected to converge toward the 3 percent target and the Selic rate potentially falling to 11.50 percent by the end of 2026.

Economic Indicator | 2023 (Actual) | 2024 (Actual) | 2025 (Forecast) | 2026 (Forecast) |

GDP Growth (%) | 3.2 | 3.4 | 2.2 | 1.6 - 1.7 |

Inflation (IPCA) (%) | 4.6 | 4.4 | 4.4 | 3.8 - 4.2 |

Selic Rate (End of Year) (%) | 11.75 | 12.25 | 15.0 | 11.50 |

Unemployment Rate (%) | 7.4 | 6.2 | 6.4 | 6.4 |

Debt-to-GDP Ratio (%) | 74.4 | 76.1 | 78.6 | 84.8 - 95.0 |

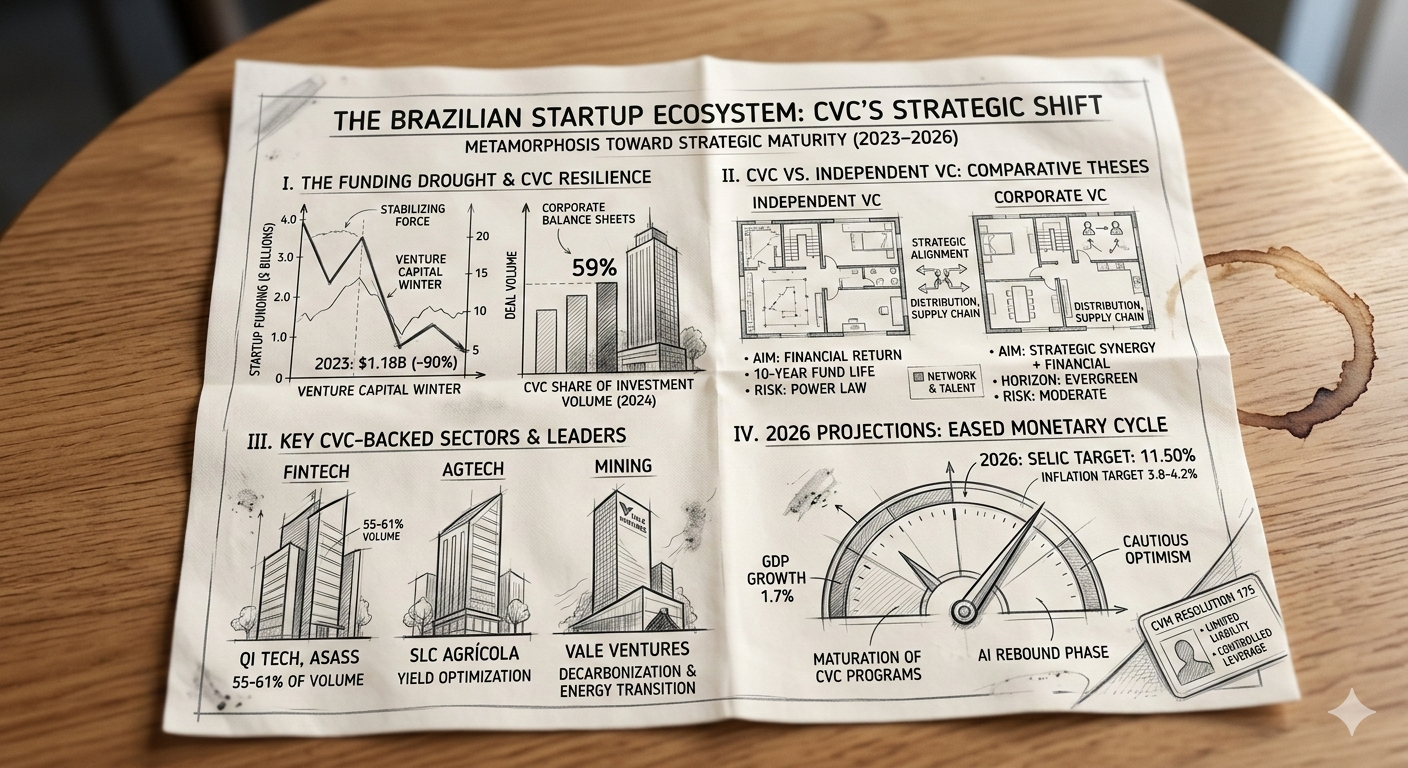

The impact of this macro environment on the startup ecosystem was a sharp correction in valuations and deal flow. In 2021, Brazilian startups raised a record $11.8 billion, a figure that plummeted to just $1.18 billion in 2023. This 90% contraction forced a pivot toward "survival mode" and operational efficiency. By late 2023 and through 2024, a "new normal" emerged where investors prioritized portfolio sustainability over rapid expansion. Interestingly, 2025 has seen a sharp rebound, with $1.25 billion raised in the first half of the year alone, signaling that the market bottomed out in 2023 and has entered a more sustainable growth phase.

The Rise of Corporate Venture Capital as a Stabilizing Force

During the funding drought of 2023, Corporate Venture Capital emerged as a remarkably resilient segment. While non-corporate venture rounds saw deep declines, corporate-backed deals maintained a stronger presence, eventually representing 59% of the total investment volume in Brazil by 2024. This marks the first time since 2018 that CVC-backed deals accounted for the majority of the dollar value in the market. This shift reflects a strategic realization among Brazilian incumbents: in a high-interest-rate environment where traditional M&A might be prohibitively expensive or risky, CVC offers a "call option" on innovation at more reasonable valuations.

The maturation of the CVC sector is evidenced by the increasing professionalization of fund managers. Many corporations are moving away from ad-hoc internal projects toward formal CVC structures, often utilizing "CVC-as-a-service" providers such as MSW Capital to manage compliance, deal sourcing, and due diligence. This has allowed homegrown giants to compete with international corporate investors like Microsoft, Qualcomm, and SoftBank, who have been active in the country for over a decade.

Key Feature | Independent VC (IVC) | Corporate VC (CVC) |

Primary Objective | Financial Return (IRR/MOIC) | Strategic Alignment + Financial Return |

Investment Horizon | 10-Year Fund Life | Often Open-Ended / Evergreen |

Value Proposition | Network, Talent, Fundraising | Distribution, Supply Chain, Industry Expertise |

Risk Appetite | High (Seeks Power Law) | Moderate (Seeks Strategic Synergies) |

Governance | Active (Board Seats) | Variable (Optional "Effective Influence") |

The strategic mandate of CVCs in Brazil is often tied to the "pain points" of the parent company. For instance, in the fintech sector, banks use CVC to acquire capabilities in open finance and blockchain. In the agribusiness sector, companies like SLC Agrícola and SP Ventures focus on precision agriculture and sustainable food systems to mitigate the risks of climate change and improve yield.

Legislative Catalyst: CVM Resolution 175 and the Modernized FIP

Perhaps the most significant tailwind for Brazilian venture capital in recent years is the regulatory overhaul spearheaded by the Brazilian Securities Commission (CVM). Resolution No. 175, which took effect in October 2023, serves as a "Unified Rulebook" that modernizes the entire fund industry. For CVCs, which typically operate through Fundos de Investimento em Participações (FIPs), this resolution addressed several long-standing structural frictions that made Brazil an outlier in the global market.

Introduction of Limited Liability

Before the implementation of Resolution 175, investors in Brazilian investment funds were subject to an unlimited liability regime. In the event of a fund's insolvency or negative net equity, the personal assets of the quota holders could be targeted to satisfy the fund's debts. This was a significant deterrent for risk-averse corporate boards. The new framework allows for the introduction of Limited Liability, where an investor's exposure is strictly capped at the amount of their subscribed capital. While this is optional and must be specified in the fund's bylaws, it aligns Brazil with international standards in Delaware and the Cayman Islands, making the FIP a much more attractive vehicle for both domestic and foreign corporate investors.

Controlled Leverage and LBO Strategies

Historically, Brazilian FIPs were strictly prohibited from using leverage. Resolution 175, and the subsequent modernization of Annex IV, now permit FIPs to contract debt or structure transactions that expose the fund's net asset value to capital risk. This reform opens the door for Brazilian PE/VC funds to employ Leveraged Buyout (LBO) strategies and utilize NAV-based credit facilities. For CVCs, this provides a powerful tool to execute larger, more impactful acquisitions or to support portfolio companies through credit-heavy growth phases without immediate equity dilution.

Democratization and Retail Access

In an effort to broaden the investor base and deepen secondary market liquidity, the new rules allow for the creation of FIP classes accessible to retail investors. To protect these less sophisticated investors, retail-accessible FIPs are prohibited from making capital calls (ensuring the total commitment is paid upfront) and are subject to a 33% cap on offshore investments. For professional and qualified investors, however, the rules have been relaxed to allow up to 100% offshore allocation, simplifying the process for Brazilian CVCs to invest in international startups that can solve domestic innovation challenges.

The Optionality of "Effective Influence"

One of the most rigid requirements of the previous FIP regime was the mandate for the fund to maintain "effective influence" over the management of its portfolio companies, typically through board seats or veto rights. While this was standard in Private Equity, it was often at odds with the minority investment structures common in early-stage Venture Capital. The modernized rules make "effective influence" optional for most FIP classes, facilitating a broader range of investment structures and making it easier for funds to participate in "club deals" where they do not lead the round.

Deep Dive: Sectoral Dominance and Emerging Theses

The distribution of venture capital in Brazil remains heavily concentrated in sectors where the country possesses either a massive underserved consumer base or a dominant global competitive advantage.

Fintech: Rebuilding the Rails of Finance

Fintech continues to anchor the Brazilian startup ecosystem, consistently accounting for 55% to 61% of total investment volume. This dominance is not merely a result of the success of Nubank, but a broader structural shift toward digital banking, open finance, and embedded finance. In 2024, Brazilian fintechs secured $1 billion in VC funding, representing 42% of all fintech investment in the Latin American region.

The current wave of fintech innovation is focused on infrastructure and "Banking-as-a-Service" (BaaS). Companies like QI Tech, Kanastra, and Pagaleve are rebuilding the "rails" of finance, utilizing the Central Bank's Pix instant payment system as a foundation. QI Tech’s $312 million total equity raise and its expansion into insurance and FX infrastructure illustrate the move from simple consumer interfaces to deep backend systems.

Fintech Leader | Total Funding (Estimated) | Core Focus | Recent Activity |

C6 Bank | $2.0 Billion+ | Digital Banking (B2B/B2C) | Backed by JP Morgan Chase |

Creditas | $829 Million | Secured Lending | Last round Series F @ $4.8B |

Neon | $754 Million | Digital Account / Credit | Focus on profitability for 30M users |

Ebanx | $460 Million | Cross-border Payments | Partnerships with Stripe for Pix |

QI Tech | $312 Million | BaaS / Infrastructure | $63M extension in July 2025 |

Asaas | $174 Million | SME Financial Services | $148M Series C in Oct 2024 |

Agtech: Sustainability and Yield Optimization

Agribusiness contributes over 25% of Brazil’s GDP, and the sector’s digital transformation is a primary target for CVCs. The focus has shifted from simple farm management software to complex platforms for rural credit, carbon sequestration, and precision agriculture. CVCs like SP Ventures and the venture arms of giants like SLC Agrícola are at the forefront of this trend.

Success stories include Agrosmart, which provides agricultural production automation, and Nagro, an app that facilitates access to rural credit for small and medium farmers. The integration of Agtech and Fintech (Agfintech) is particularly potent in Brazil, where traditional bank credit for farmers can be scarce or expensive.

Mining and the Energy Transition: The Vale Ventures Mandate

In the industrial sector, Vale Ventures serves as a benchmark for how a global incumbent can use CVC to lead an industry-wide transition toward sustainability. With a $100 million initial commitment, Vale Ventures focuses on "Green Steel" pathways, circular mining, and metals for the energy transition. This is not merely an ESG initiative but a core strategic necessity; as global steelmakers seek to decarbonize, they require high-quality, lower-emission iron ore and "green briquettes" that can reduce CO2 emissions by 10% to 15%.

Vale’s CVC arm actively invests in technologies for autonomous haulage and drilling, aiming to have dozens of autonomous trucks operational by 2025 to cut fuel consumption and improve safety. This exemplifies the "strategic returns" of CVC: the technologies developed by startups like Allonnia are directly integrated into Vale’s global operations to enhance productivity and safety.

AI and the 2025 Rebound

After the pandemic-era bubble burst, AI startups in Brazil have entered a "rebound" phase characterized by stricter due diligence and a focus on "True Tech". In 2025, venture capital has returned to AI with force, but with a different mandate: investors are rewarding startups that combine AI-driven innovation with strong revenue traction and financial discipline.

SaaS leaders like Omie, which raised R$855 million (~160million)inlate2025,areusingAItoautomateaccountingandtaxreconciliationfor180,000clients.[3]TelecommunicationsgiantVivohasalsopivoteditsCVCstrategytoreserveasignificantportionofitsR470 million fund for "emerging AI theses," recognizing that AI will be the guiding principle for future investments in finance, health, and energy.

The "Brazil Cost" and Operational Friction

Despite the promising growth and regulatory advancements, the Brazilian market remains one of the most difficult environments in the world to operate efficiently. The "Custo Brasil" (Brazil Cost) encompasses the high direct and indirect expenses resulting from regulatory complexity, tax inefficiency, and bureaucratic paralysis.

Tax and Labor Rigidity

Brazil’s tax system is a "labyrinth of complexities," ranking 124th out of 190 countries in the World Bank’s Ease of Doing Business Index. Companies spend approximately 1,500 hours annually just to meet fiscal obligations. Furthermore, labor charges can nearly double the cost of formal employment, with the total cost of a worker under the CLT (Consolidation of Labor Laws) expected to approach 190% of the nominal salary in 2026. These high "authoritarian labor shackles" often lead to high business mortality, with less than 40% of companies surviving after five years.

The Cultural Gap in CVC

A significant internal friction point for Brazilian CVCs is the "culture gap" between fast-moving startups and stable, process-oriented large corporations. Solo industry teams often fail because they lack alignment with the parent company's strategic objectives or struggle to integrate the startup's agile methodology into the corporate bureaucracy. The most successful Brazilian CVCs, such as Vivo and Inovabra, utilize diverse teams that combine professionals from both the corporation and the innovation market to establish "buy-in" from leadership and ensure operational autonomy.

Infrastructure and Logistics

Brazil’s vast geography and diverse terrain create logistical challenges that can significantly increase the cost of doing business. While the government has worked to improve customs processes and infrastructure, product clearance times and logistical costs remain higher than in more developed markets. Startups expanding into Brazil must often re-test and re-certify products to meet local technical requirements, even if they have already met international standards.

Case Studies in Strategic Synergy

The primary value proposition of CVC in Brazil is the ability to offer startups access to a "distribution moat" or a "supply chain bridge" that financial VCs cannot provide.

The MaisMu and BAT Distribution Flywheel

MaisMu, a healthy food startup, achieved a transformational scaling event through a distribution agreement with BAT Brazil (via its CVC arm, Btomorrow Ventures). Through the agreement, MaisMu expanded its sales network from 10,000 to 40,000 points of sale in just six months. For a startup, replicating the logistical reach of a global conglomerate like BAT would have taken decades of capital-intensive effort; the CVC partnership allowed it to occur in a single fiscal cycle.

Vivo and the "Hospital Púrpura" Initiative

Vivo Ventures’ investment in the healthtech company Conexa illustrates a deep "ecosystem play." Conexa provides telemedicine services through Vivo’s "Vale Saúde" platform. Recently, Conexa became the backbone of "Hospital Púrpura," an internal healthcare platform available to Vivo’s 33,000 employees and their 50,000 dependents. This provides Conexa with a massive, stable contract while giving Vivo a high-tech solution to manage its human resource costs.

Ambev: Z-Tech and the Smart Drinking Lab

Ambev’s innovation model is unique in that it combines a B2B platform (BEES) with an incubator (Smart Drinking Lab) to disrupt its own business model. The BEES platform has digitized the relationship with millions of retailers, connect-and-enhancing every step of the route to the consumer. Meanwhile, the Smart Drinking Lab collaborates with biotech startups and neuroscientists to develop products that discourage harmful drinking, such as AI apps that evaluate vocal changes due to alcohol consumption. This "disruptive self-innovation" ensures that Ambev remains relevant as consumer behaviors shift toward moderation and digital-first purchasing.

Regional Ecosystems: Beyond São Paulo

While São Paulo remains the gravitational center of the Brazilian innovation economy, hosting about 55% of deep-tech ventures in 2025, a significant decentralization is underway.

Florianópolis: The Silicon Island of the South

Florianópolis was officially recognized as the "Startup Capital of Brazil" by federal law in 2024. The city’s tech sector represents a staggering 25% of its GDP, the highest concentration in the country. Florianópolis boasts up to ten times more startups per capita than São Paulo and is home to over 6,000 tech companies. The city has become a hub for SaaS and fintech, attracting $298 million in VC funding between 2020 and 2024.

Recife: The "Porto Digital" Success

Recife has leveraged its rich cultural history to build a thriving innovation ecosystem, particularly through the "Porto Digital" technology park. The ecosystem is designed to reduce friction for early entrants while providing structured pathways toward scale, making it a model for mid-sized cities seeking innovation-led growth.

Hub | Key Strength | Notable Characteristic |

São Paulo | Deep Tech / Finance | 55% of all deep tech ventures; financial nexus |

Florianópolis | SaaS / Tech Jobs | Tech is 25% of local GDP; highest job concentration |

Recife | Software / BPO | Porto Digital hub; successful ecosystem design |

Florianópolis | Fintech | 19% growth in early-stage funding (2020-2024) |

Exit Dynamics and Market Timing in Brazil

The exit landscape in Brazil remains one of the most challenging aspects for venture investors. The number of VC-backed startup exits fell to 79 in 2024, the lowest level in recent history. However, 2025 showed a strong rebound, with exit value reaching $4.9 billion.

Exit rates in Brazil are highly sensitive to "market timing." Research indicates that exit rates increase by approximately two times during moments of high market price-earnings ratios and currency appreciation. Conversely, the high Selic rates of 2024-2025 have acted as a brake on IPOs, forcing many startups to seek liquidity through M&A or secondary market sales.

CVCs play a unique role here. Unlike financial VCs who must exit to return capital to LPs, CVCs often act as the "ultimate exit" themselves, acquiring their portfolio companies once they reach strategic maturity. This provides a "liquidity backstop" for the ecosystem during periods when the public markets are closed.

Projections for 2026-2027: The Imminent Easing Cycle

As Brazil enters 2026, the consensus among analysts is one of "cautious optimism". The economy is expected to grow between 1.7% and 2.2% in 2026, with inflation likely ending the year at 3.8%. The most critical projection is the onset of a monetary easing cycle in early 2026, which could bring the Selic rate to around 11.5% - 12.0% by the end of that year.

Projections 2026 | Value / Target | Implications for CVC |

GDP Growth | 1.7% - 2.2% | Moderate expansion; sustainable pace |

Selic Rate (Target) | 11.5% | Lower cost of capital; improved VC risk appetite |

Inflation (IPCA) | 3.8% - 4.0% | Within target range; price stability |

Debt-to-GDP | 84.8% - 95.0% | Continued fiscal concern; currency pressure |

FX (BRL/USD) | R$ 5.50 | Pressure on imports; attractive for foreign VC |

The "AI boom" is expected to further boost aggregate demand and productivity in 2026-2027, potentially offsetting some of the negative effects of high public debt and global protectionism. For CVCs, this period will be defined by the "maturation of programs," where corporations move from the "hangover" of the pandemic era into a new phase of disciplined, strategic investment focused on long-term industrial transformation.

Conclusion: The New Frontier of Brazilian Corporate Innovation

The role of Corporate Venture Capital in Brazilian startups has evolved from a speculative trend into a structural necessity. The "Venture Capital Winter" served as a filter, removing "tourist" investors and leaving behind a more disciplined ecosystem where corporate balance sheets provide a critical source of stable, strategic capital. With the regulatory modernization provided by CVM Resolution 175—particularly the introduction of limited liability and leverage—the legal barriers to CVC participation have been significantly lowered.

As the economy enters a more favorable monetary cycle in 2026, the focus will shift toward "True Tech" and the integration of AI across traditional sectors like mining, agriculture, and finance. The Brazilian ecosystem is no longer merely an "emerging market"; it is a sophisticated innovation hub that sets the tone for the rest of Latin America. For startups, the path to scale in Brazil now undeniably leads through the CVC arms of the country's most powerful incumbents, who offer the distribution, supply chain access, and industry expertise necessary to navigate the "Brazil Cost" and achieve sustainable growth in a complex global environment.

Read More -

1. From Idea to MVP: A Step-by-Step Guide for Solo Founder

🔗 https://findnstart.com/blogs/from-idea-to-mvp-a-step-by-step-guide-for-solo-founder

2. How to Validate Your Startup Idea in 48 Hours for $0

🔗 https://findnstart.com/blogs/how-to-validate-your-startup-idea-in-48-hours-for-0

3. Remote vs. Local: Does Your Co-Founder Need to Live in the Same City?

🔗 https://findnstart.com/blogs/remote-vs-local-does-your-co-founder-need-to-live-in-the-same-city

4. The 2026 Startup Landscape: What Has Fundamentally Changed (and Why Founder Skills Matter More Than Ever)

5. The Most In-Demand Skills for Startup Founders in 2026

🔗 https://findnstart.com/blogs/the-most-in-demand-skills-for-startup-founders-in-2026

6. How to Find a Technical Co-Founder (Without a Six-Figure Salary)

🔗 https://findnstart.com/blogs/how-to-find-a-technical-co-founder-without-a-six-figure-salary

7. 5 Red Flags to Look for When Choosing a Startup Partner

🔗 https://findnstart.com/blogs/5-red-flags-to-look-for-when-choosing-a-startup-partner

8. How to Pitch Your Idea to Potential Co-Founders

🔗 https://findnstart.com/blogs/how-to-pitch-your-idea-to-potential-co-founders

9. How to Build a Portfolio that Attracts High-Growth Startup Founders

🔗 https://findnstart.com/blogs/how-to-build-a-portfolio-that-attracts-high-growth-startup-founders

10. Equity vs. Salary: How to Split Ownership with Your First Teammate

🔗 https://findnstart.com/blogs/equity-vs-salary-how-to-split-ownership-with-your-first-teammate

11. Why Joining an Early-Stage Startup is Better Than a Corporate Job

🔗 https://findnstart.com/blogs/why-joining-an-early-stage-startup-is-better-than-a-corporate-job

12. The Future of EdTech: Why Developers and Educators Need to Team Up Now

🔗 https://findnstart.com/blogs/the-future-of-edtech-why-developers-and-educators-need-to-team-up-now

13. The Architecture of Symbiosis: Analytical Perspectives on the Five Habits of Successful Startup Duos

14. Finding a Co-Founder in the AI Space: What Skills Should You Look For?

🔗 https://findnstart.com/blogs/finding-a-co-founder-in-the-ai-space-what-skills-should-you-look-for

15. Overcoming Analysis Paralysis and the Strategic Path to Execution

🔗 https://findnstart.com/blogs/overcoming-analysis-paralysis-and-the-strategic-path-to-execution

16. From College Project to Company: How to Find Your Student Co-Founder

🔗 https://findnstart.com/blogs/from-college-project-to-company-how-to-find-your-student-co-founder

17. How to Start a Startup While Working a Full-Time Job

🔗 https://findnstart.com/blogs/how-to-start-a-startup-while-working-a-full-time-job

18. How to Build a HealthTech Startup Without a Medical Degree

🔗 https://findnstart.com/blogs/how-to-build-a-healthtech-startup-without-a-medical-degree

19. The Solitary Architect: Executive Isolation in Entrepreneurship

20. The 2026 Guide to Launching a SaaS as a Solo Developer

21. What Sustainable Growth Actually Looks Like

🔗 https://findnstart.com/blogs/what-sustainable-growth-actually-looks-like

22. The Early Warning Signs Your Startup Is in Trouble

🔗 https://findnstart.com/blogs/the-early-warning-signs-your-startup-is-in-trouble

23. How to Grow Without Burning Out

🔗 https://findnstart.com/blogs/how-to-grow-without-burning-out

24. The Truth About “Runway” Most Founders Ignore

🔗 https://findnstart.com/blogs/the-truth-about-runway-most-founders-ignore

25. Revenue Solves More Problems Than Funding

🔗 https://findnstart.com/blogs/revenue-solves-more-problems-than-funding

26. What No One Tells You About Being a Solo Founder

🔗 https://findnstart.com/blogs/what-no-one-tells-you-about-being-a-solo-founder

27. Why Smart People Quit High-Paying Jobs to Build Startups (And Why Most Regret It)

28. Why Most Startup Advice on Twitter Is Dangerous

🔗 https://findnstart.com/blogs/why-most-startup-advice-on-twitter-is-dangerous

29. Decision Fatigue: The Silent Startup Killer

🔗 https://findnstart.com/blogs/decision-fatigue-the-silent-startup-killer

30. Fear vs Logic: How Founders Actually Make Decisions

🔗 https://findnstart.com/blogs/fear-vs-logic-how-founders-actually-make-decisions

31. How Overthinking Destroys Early Momentum

🔗 https://findnstart.com/blogs/how-overthinking-destroys-early-momentum

32. Ideas Don’t Scale. Systems Do.

🔗 https://findnstart.com/blogs/ideas-dont-scale-systems-do

33. The First Hire That Actually Matters

🔗 https://findnstart.com/blogs/the-first-hire-that-actually-matters

34. How the First 100 Users Decide Your Startup’s Fate

🔗 https://findnstart.com/blogs/how-the-first-100-users-decide-your-startups-fate

35. Why Your Startup Doesn’t Need Growth — It Needs Focus

🔗 https://findnstart.com/blogs/why-your-startup-doesnt-need-growthit-needs-focus

36. Why Most Startups Die Quietly

🔗 https://findnstart.com/blogs/why-most-startups-die-quietly

37. Lessons Learned Too Late by First-Time Founders

🔗 https://findnstart.com/blogs/lessons-learned-too-late-by-first-time-founders

38. The Myth of the “Overnight Success” Startup

🔗 https://findnstart.com/blogs/the-myth-of-the-overnight-success-startup

Want to calculate the equity for your cofounder?

Nail your cap table before you sign. Whether you're splitting equity with a co-founder or planning your next funding round, our Equity Calculator gives you precision in seconds

Equity calculator →