India vs Global Market: Where Should You Focus First?

June 23, 2026 by Harshit Gupta

The global economic architecture of 2026 is defined by a profound divergence between traditional developed markets and the emerging resilience of the Indo-Pacific corridor. For organizations evaluating their next phase of expansion, the choice between focusing on the Indian domestic market or pursuing a "Global First" strategy involves a complex calculation of macroeconomic stability, regulatory shifts, and unit economics viability. While the global economy continues to weather the residual shocks of 2025 trade tensions, India has emerged as a distinct outlier, characterized by a return to pre-pandemic growth trends and a maturing digital infrastructure. This analysis evaluates the critical variables shaping this decision, from the implementation of landmark trade agreements to the structural challenges of customer acquisition in a high-competition environment.

The Macroeconomic Divergence: India’s Resilience vs. Global Subduction

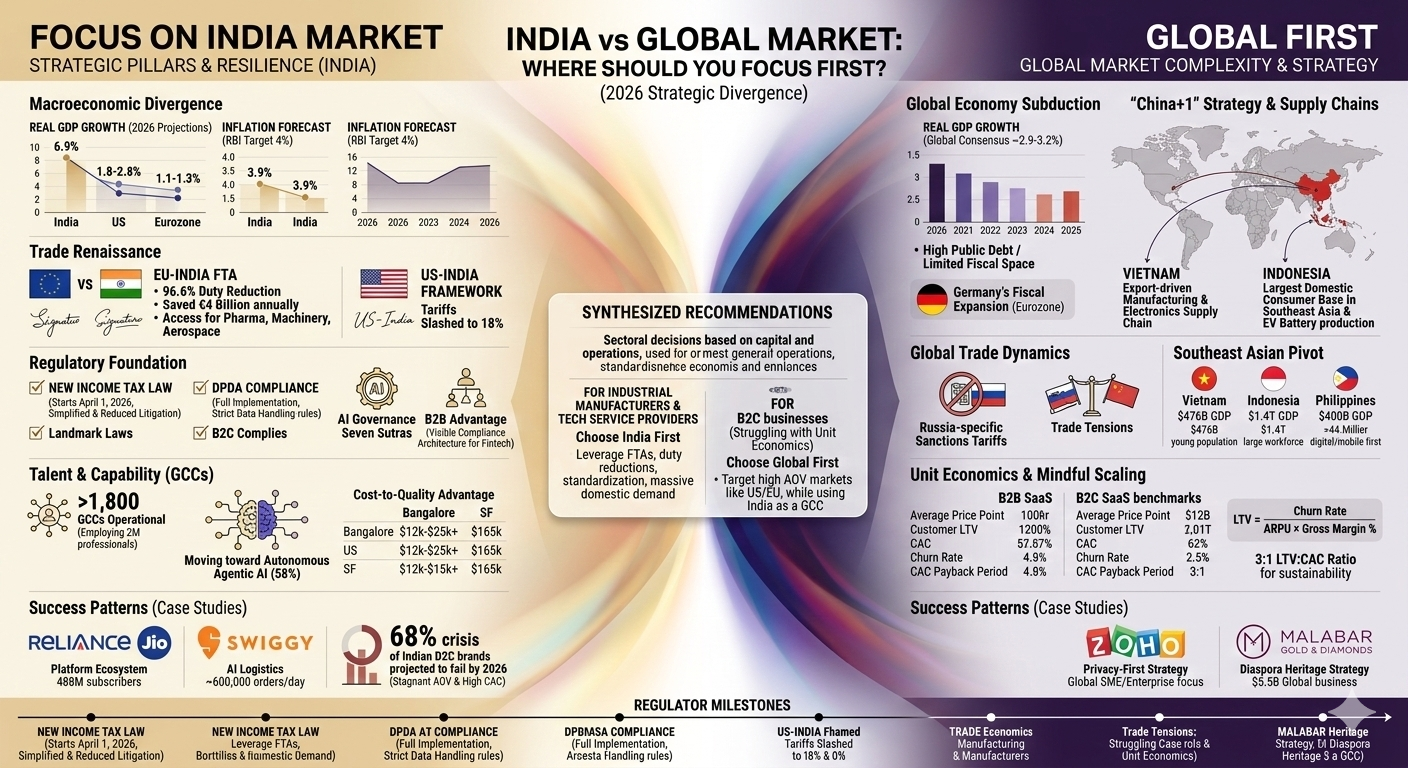

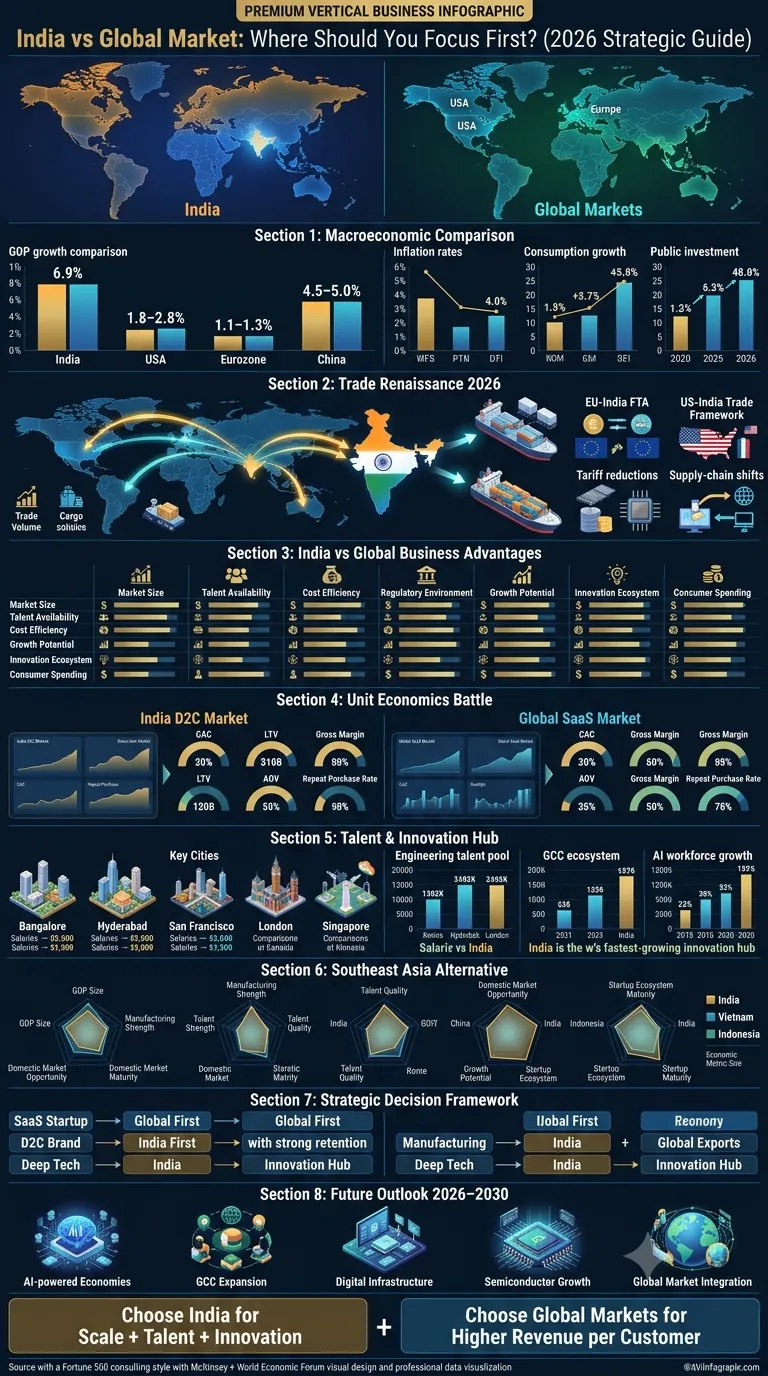

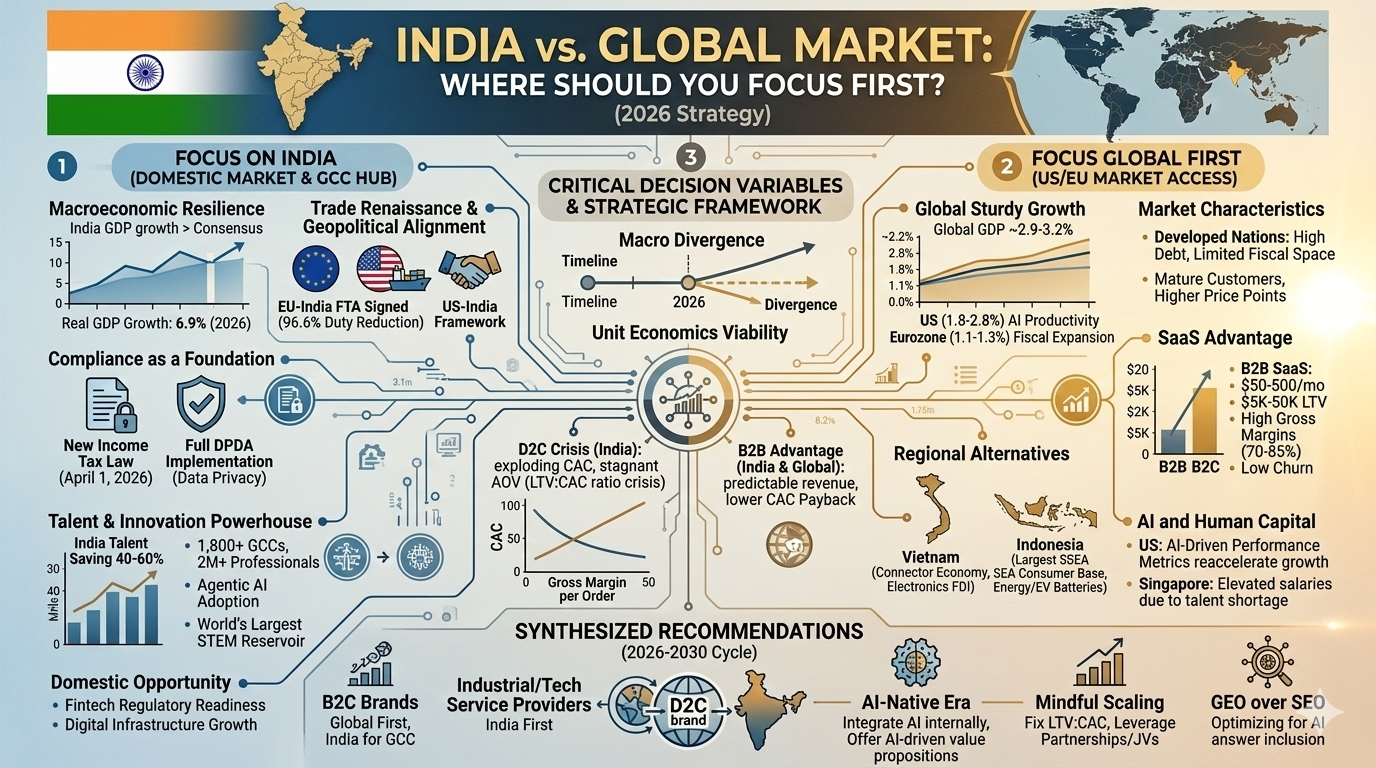

The global growth narrative in 2026 is characterized by "sturdy" but unspectacular performance, with real GDP projected to increase by approximately 2.9% to 3.2%. In contrast, the Indian economy exhibits a more aggressive trajectory, with real GDP expected to grow at 6.9% in 2026 and 6.8% in 2027, significantly outperforming the consensus estimates for major economies. This growth is anchored by a nascent recovery in urban consumption and a sustained resurgence in rural demand, supported by policy rate cuts and targeted fiscal relief.

The Indian landscape in 2026 is shaped by the successful management of headline inflation, which is forecast to settle at 3.9%, aligning closely with the Reserve Bank of India’s (RBI) 4% target. This stability has allowed for a series of policy rate cuts, injecting approximately 6.3 trillion rupees ($70 billion) of liquidity into the banking system, thereby fostering an environment conducive to credit growth and consumer spending. Conversely, the global outlook remains clouded by high public debt and limited fiscal space in developed nations, which constrains their ability to provide counter-cyclical support in the event of further external shocks.

Comparative Macroeconomic Projections for 2026

Region | Real GDP Growth (%) | Inflation Projection (%) | Primary Growth Driver |

India | 6.5% – 6.9% | 3.9% – 4.0% | Domestic Consumption & Public Capex |

United States | 1.8% – 2.8% | 2.2% | Productivity Gains from AI Adoption |

Eurozone | 1.1% – 1.3% | 1.7% | German Fiscal Expansion |

China | 4.5% – 5.0% | < 0% (Deflator) | Government Policy Support |

United Kingdom | 1.0% | 2.0% | Sluggish Potential Supply |

Southeast Asia | 3.5% | 3.0% – 4.0% | AI Value Chain & Connector Economics |

The resilience of India's economy is further underscored by the recovery of private final consumption expenditure, which grew by 7.9% in the second quarter of the fiscal year. This was primarily supported by the lowest inflation level seen in a decade—1.7%—and rising disposable incomes resulting from tax and GST relief. Furthermore, the Indian government maintained high public capital expenditure, at 3.4% of GDP, particularly in infrastructure and green-transition projects, ensuring domestic demand remained the central growth pillar.

Geopolitical Re-alignment and the Trade Renaissance

A pivotal factor in the 2026 strategic decision is the sudden acceleration of bilateral trade integration. The signing of the EU-India Free Trade Agreement (FTA) on January 27, 2026, represents a seismic shift in global trade dynamics. Termed the "mother of all deals," this agreement covers 25% of global GDP and one-third of global trade, aiming to eliminate or reduce duties on approximately 96.6% of European exports to India. This creates an estimated annual saving of 4 billion euros for EU companies while liberalizing tariff lines for Indian goods over a multi-year horizon.

The announcement of a joint framework for a US-India trade agreement in February 2026 has further stabilized the investment climate. By slashing reciprocal tariffs to 18%, the deal removes a "hanging sword" over equity and rates markets, effectively positioning India as a more attractive alternative to rivals like Vietnam, Malaysia, and China. This re-alignment is particularly critical as US businesses seek to insulate themselves from geostrategic supply chain disruptions and "Russia-specific" sanction tariffs that had previously complicated India-US relations.

Strategic Impact of the 2026 Trade Agreements

Agreement | Status (Feb 2026) | Key Provisions | Strategic Opportunity |

EU-India FTA | Signed/Legal Scrubbing | 96.6% Duty Reduction; Security/Defense Partnership | Market access for machinery, pharma, and aerospace. |

US-India Framework | Framework Announced | Reciprocal Tariffs slashed to 18% | Revitalization of the "China+1" manufacturing strategy. |

DPDA Compliance | Full Implementation | Comprehensive Data Privacy Rules | Standardized trust framework for global SaaS/Tech. |

The geopolitical landscape remains volatile, with the Indian Rupee (INR) facing significant pressure due to a "strategic power gap" and foreign outflows. The Rupee settled near an all-time low of 91.96 against the US Dollar in early 2026, depreciating by approximately 6.5% since April 2025. While this depreciation aids in offsetting the impact of US tariffs on Indian exports, it complicates the calculus for foreign investors and creates inflationary pressure on essential imports like crude oil.

The Regulatory Horizon: Compliance as a Strategic Foundation

For companies targeting India in 2026, regulatory compliance has evolved from a legal obligation into a core competitive advantage. The country's policy environment is becoming more structured, transparent, and investor-friendly, providing greater certainty for multinational corporations and high-growth startups alike.

A major milestone is the introduction of India's new Income Tax framework, scheduled to take effect on April 1, 2026. Designed to simplify tax provisions, reduce litigation, and improve clarity for businesses, the reform is expected to strengthen investor confidence and lower administrative friction for foreign enterprises operating in India.

At the same time, the full implementation of the Digital Personal Data Protection Act (DPDP Act) marks a significant shift in India's digital governance landscape. The law imposes stringent obligations on organizations handling the personal data of Indian residents, regardless of where those organizations are located. Businesses must now establish robust consent-management systems, audit trails, data-retention policies, and governance frameworks to remain compliant.

The government's broader vision for responsible innovation is reflected in its "Seven Sutras" of AI Governance, which emphasize trust, transparency, accountability, and human-centric development. Rather than restricting technological advancement, these principles seek to create a balanced framework that enables innovation while safeguarding public interests.

This maturation of India's regulatory architecture is further reinforced by efforts to eliminate outdated compliance burdens, including the removal of certain certification requirements such as Scheme X under the BIS framework. Together, these reforms reduce operational uncertainty and create a more predictable environment for global businesses seeking long-term growth in India.

Regulatory Milestone Checklist for 2026

Timeline | Key Development | Strategic Impact |

|---|---|---|

April 1, 2026 | New Income Tax Law comes into force | Simplified tax administration, reduced disputes, and improved planning certainty for multinational corporations |

Q1 2026 | Full implementation of DPDP compliance requirements | Mandatory data governance frameworks, auditability, and privacy controls for technology-driven businesses |

March 2026 | Expected timeline for foundational US–India trade agreement | Potential improvements in digital trade, market access, and investment flows |

July 2026 | Expansion of centralized electronic labor contract systems across parts of Asia | Signals a broader regional shift toward digital compliance and workforce transparency |

Compliance as an Investment Signal

Regulatory readiness is increasingly becoming a decisive factor in capital allocation, particularly within fintech, SaaS, and data-driven industries. Venture capital firms are no longer evaluating startups solely on growth metrics; they are also scrutinizing governance structures, compliance frameworks, and operational resilience.

In sectors such as digital lending, payments infrastructure, and financial data services, investors now expect companies to demonstrate strong controls around risk management, model governance, cybersecurity, and regulatory reporting. The prevailing expectation is clear: successful startups must increasingly operate with the discipline and reliability of financial institutions rather than merely functioning as technology platforms.

As global capital becomes more selective, compliance is no longer viewed as a cost center—it is emerging as a prerequisite for investment, scalability, and long-term market credibility.

Unit Economics: The Battle for Sustainable Profitability

The contrast between "India First" and "Global First" business strategies becomes most apparent when examining unit economics.

Between 2023 and 2025, startups worldwide experienced a significant Unit Economics Correction, as rising interest rates and tighter funding conditions forced companies to shift their focus from growth-at-all-costs toward sustainable profitability. By 2026, this transition has become particularly challenging for India's Direct-to-Consumer (D2C) ecosystem.

Customer acquisition costs (CAC) have surged dramatically, driven by increased competition across digital advertising platforms, influencer marketing saturation, and declining efficiency of performance marketing channels. Meanwhile, average order values (AOV) have remained relatively stagnant, placing significant pressure on margins.

The Indian D2C Unit Economics Challenge (2026 Benchmarks)

Metric | Benchmark (INR) | Context |

|---|---|---|

Customer Acquisition Cost (CAC) | ₹1,850 | Up from approximately ₹650 in 2021 |

Average Order Value (AOV) | ₹1,450 | Nearly 5× lower than the U.S. average (~₹7,100) |

Gross Margin per Order | ₹607 | After product costs, logistics, and returns |

Net Gain/Loss on First Order | –₹1,243 | Most brands lose money on initial customer acquisition |

Average Repeat Purchase Rate | 22% | Breakeven typically requires four or more repeat purchases |

Why Many D2C Brands Struggle

The projected failure of a large share of Indian D2C brands by 2026 stems from a fundamental mismatch between acquisition costs and customer lifetime value.

Several structural challenges contribute to this pressure:

Escalating digital advertising costs across Meta, Google, and influencer channels.

High return rates, particularly in fashion and lifestyle categories, where returns can reach 25–35%.

Continued reliance on Cash on Delivery (COD), which increases logistics expenses, working-capital requirements, and return-to-origin costs.

Limited pricing power in a highly competitive and value-sensitive consumer market.

As a result, many companies generate negative contribution margins on first purchases and depend heavily on repeat orders to recover acquisition costs.

The Critical Metric: LTV:CAC Ratio

In this environment, the Lifetime Value to Customer Acquisition Cost (LTV:CAC) ratio has become the most important indicator of scalability.

LTV:CAC > 3:1 → Sustainable growth and efficient capital deployment.

LTV:CAC between 1:1 and 3:1 → Growth is possible but operational efficiency must improve.

LTV:CAC < 1:1 → Every additional customer acquired destroys value.

For businesses operating in India, maintaining a minimum 3:1 LTV:CAC ratio requires disciplined spending, strong retention strategies, supply-chain efficiency, and rigorous control of returns and payment costs. When the ratio falls below this threshold, expansion efforts should be paused until unit economics improve, as continued aggressive spending can rapidly lead to a liquidity crisis.

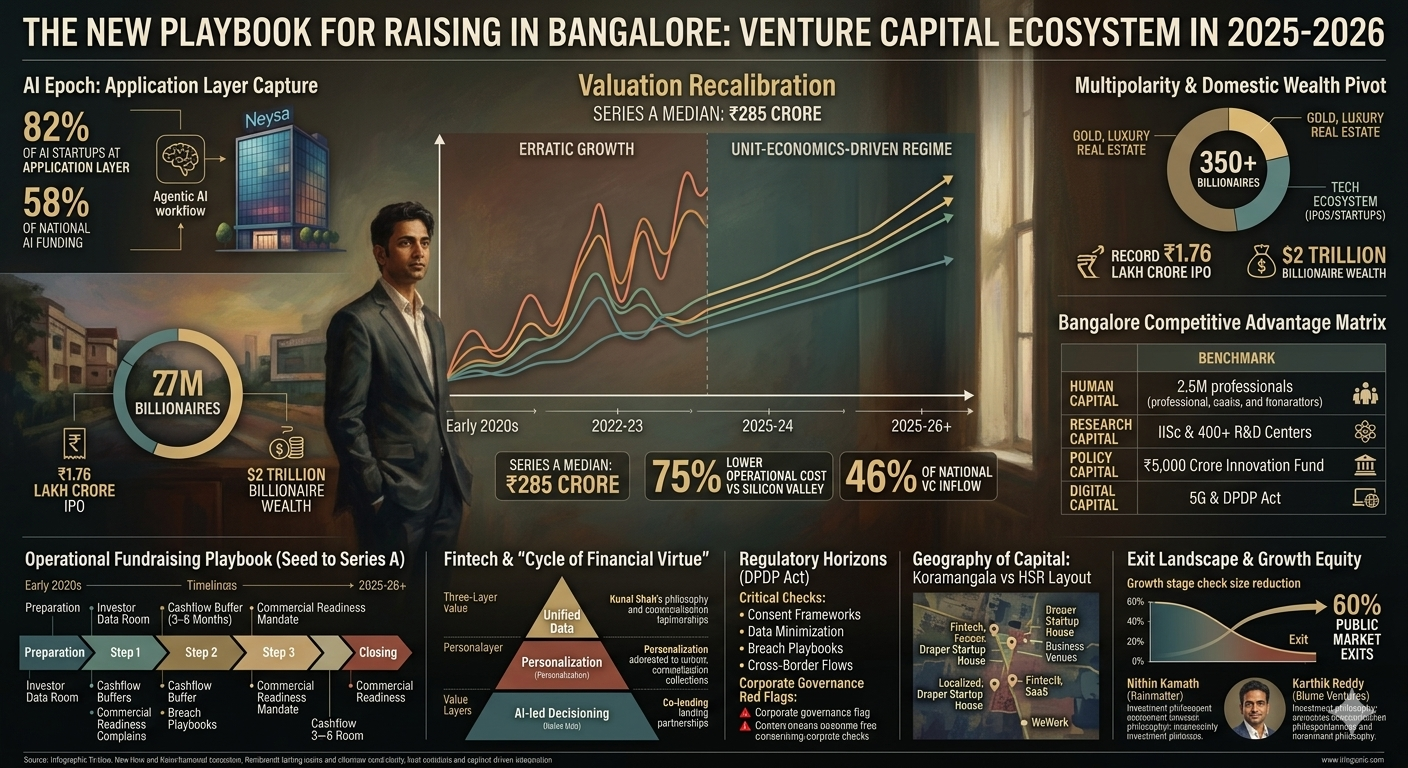

Talent and Capability: India's Rise as the Global Innovation Hub

The case for an India-focused strategy in 2026 extends far beyond market size and cost advantages. India has emerged as the world's most significant destination for Global Capability Centers (GCCs), transforming from a traditional outsourcing hub into a center for innovation, product development, and advanced technology operations.

More than 1,800 GCCs now operate across India, employing over two million professionals and supporting critical business functions for multinational corporations including Microsoft, Google, Goldman Sachs, and hundreds of Fortune 500 companies. These centers are no longer confined to back-office operations; they increasingly lead global initiatives in artificial intelligence, cybersecurity, cloud computing, data engineering, and product innovation.

The evolution is particularly visible in enterprise AI adoption. A growing share of GCCs are investing in Agentic AI systems capable of automating complex workflows, enabling Indian operations to move up the value chain from execution to decision-making and innovation. As a result, India is increasingly viewed as a global innovation powerhouse rather than merely a low-cost service destination.

The Cost-to-Quality Advantage in Technology Talent

India's technology workforce continues to offer one of the strongest value propositions in the global economy. Companies can typically achieve operational cost savings of 40–60% compared with major Western technology hubs while maintaining access to highly skilled engineering talent.

Comparative Talent Economics

Location | Median Tech Salary (USD) | Effective Tax Rate | Approximate Monthly Disposable Income |

|---|---|---|---|

San Francisco | $165,000 | ~35% | ~$5,500 |

Seattle | $152,000 | ~28% | ~$6,900 |

London | $95,000 (£75K) | ~30% | ~$3,100 |

Singapore | $80,000 (SGD 108K) | ~10% | ~$3,500 |

Bangalore / Hyderabad | $12,000–$25,000+ | Varies | High relative to local cost of living |

Although compensation levels remain substantially higher in Silicon Valley and other developed markets, elevated housing, transportation, and living costs often reduce the practical advantage for employees. In contrast, skilled professionals in India's leading technology hubs frequently enjoy stronger purchasing power relative to their local cost of living.

Beyond economics, India offers an unmatched scale advantage. The country's higher education system produces more than two million engineering graduates annually, creating one of the world's deepest technical talent pools. This enables organizations to scale teams rapidly—from five engineers to fifty or more within weeks—a capability that is increasingly difficult to replicate in talent-constrained Western markets.

As global demand for digital skills accelerates, the technology talent shortage is becoming a structural challenge. Industry forecasts suggest that as many as 85 million technology-related positions could remain unfilled worldwide by 2030. Against this backdrop, India's GCC ecosystem serves not only as a cost-optimization strategy but as a critical solution to the global talent gap.

Regional Alternatives: The Southeast Asian Pivot

While India remains the preferred destination for technology, R&D, and knowledge-intensive operations, Southeast Asia has emerged as an increasingly important component of global diversification strategies.

Countries such as Vietnam and Indonesia are benefiting from the ongoing reconfiguration of global supply chains, as businesses seek to reduce concentration risk and diversify production beyond China.

Vietnam has positioned itself as a highly competitive manufacturing and export platform, leveraging strong trade relationships, improving infrastructure, and an expanding role in the global semiconductor and electronics ecosystem. The country continues to attract significant foreign investment as companies pursue "China+1" strategies.

Indonesia, meanwhile, offers a different value proposition. With a population exceeding 275 million, it represents Southeast Asia's largest consumer market while also controlling strategic resources essential to the energy transition, particularly nickel and other materials used in electric vehicle batteries.

Choosing Between India, Vietnam, and Indonesia

The optimal destination depends largely on a company's strategic priorities.

India

India is the preferred choice for organizations seeking a combination of a massive domestic market, world-class technical talent, and advanced innovation capabilities. The opportunity extends beyond cost arbitrage toward value creation through engineering, AI, digital transformation, and product development.

Vietnam

Vietnam is particularly attractive for export-oriented manufacturers and companies seeking alternatives to China-based production. Its strengths lie in electronics manufacturing, logistics efficiency, and integration into global supply chains.

Indonesia

Indonesia offers access to Southeast Asia's largest consumer economy and significant natural resource advantages. It is especially attractive for businesses operating in energy, mining, electric vehicles, battery technology, and consumer sectors.

Supply Chain Realignment and Regional Resilience

The reintroduction of U.S. tariffs in 2025 accelerated global supply-chain diversification efforts, reinforcing Southeast Asia's role as a strategic manufacturing base. Vietnam emerged as one of the primary beneficiaries of this trend, attracting increased foreign direct investment and expanding its position within global electronics and semiconductor value chains.

However, by early 2026, regional economies demonstrated greater resilience than many analysts anticipated. Strong electronics exports, continued foreign investment inflows, and domestic consumption helped sustain economic momentum despite heightened geopolitical and trade-related uncertainty.

Comparative Economic Metrics (2024–2026 Outlook)

Metric | Vietnam | Indonesia | Philippines |

|---|---|---|---|

GDP Size (Approx.) | $476 Billion | $1.4 Trillion | $400+ Billion |

Primary FDI Driver | Electronics & High-Tech Manufacturing | Energy, Mining & EV Supply Chain | Services & Digital Economy |

Workforce Profile | Young Demographic Dividend | Large Resource-Oriented Workforce | Digital-First, English-Proficient Workforce |

Strategic Strength | Export Manufacturing Hub | Domestic Market & Natural Resources | BPO, Services & Digital Innovation |

Strategic Takeaway

The choice is no longer between India and Southeast Asia—it is increasingly about how organizations combine them. India is becoming the preferred destination for innovation, engineering, and knowledge-intensive operations, while Vietnam and Indonesia serve complementary roles in manufacturing, supply-chain diversification, and regional market expansion. Companies that successfully integrate these ecosystems into a unified regional strategy will be best positioned to capture growth across Asia's next decade of economic transformation.

Strategic Framework for Market Entry in 2026

The evidence suggests that a "Focus First" decision is not binary but sectoral. The success of companies like Zoho and Freshworks highlights a hybrid pattern: leveraging Indian cost and talent efficiencies to build products that serve a global SME and enterprise customer base.

Case Study Insights: Success Patterns

The "Global-First" SaaS Model (Freshworks, Zoho): These companies utilized Indian engineering talent to build world-class products, then listed on global exchanges (NASDAQ) or scaled through bootstrapping. Their success lies in combining Indian cost efficiencies with customer-centric global operations. Zoho specifically addressed the global "Trust Paradox" by adopting a "Privacy-First" strategy, which resonated in markets like the GCC where 80% of consumers express anxiety over data use.

The "India-First" Digital Ecosystem (Reliance Jio): Reliance transformed India's digital infrastructure by investing heavily in 4G and 5G before monetization, creating a platform ecosystem that locks in 488 million subscribers across connectivity, commerce, and content.

The Hyperlocal Playbook (Lulu Group, Swiggy): Understanding the "long tail" of consumer demand in a diverse population. Swiggy’s use of AI-driven logistics to optimize delivery times in dense urban environments allowed it to reach nearly 600,000 orders per day.

The Diaspora Heritage Strategy (Malabar Gold & Diamonds): Leveraging deep cultural roots to build a $5.5 billion global business. By understanding the emotional needs of the diaspora and implementing features like "Gold Rate Lock," the brand successfully combined physical retail expansion with digital insight.

Strategic Takeaways for 2026

Shift from SEO to GEO: Traditional search engine optimization is being superseded by Generative Engine Optimization. For B2B SaaS, optimizing for AI answer inclusion and citation authority in LLM-driven search (ChatGPT, Perplexity) offers a 6–15x ROI in significantly less time than traditional methods.

Localization is not Translation: Entering markets like the GCC or different Indian regions requires "transcreation"—adapting content to Khaleeji dialects or vernacular Indian languages to avoid brand ridicule and ensure trust.

Unit Economics over Growth: For India-focused B2C brands, the immediate priority must be fixing the LTV:CAC ratio through smart bundling, dynamic upsells, and increasing repeat rates via personalized retention strategies (e.g., WhatsApp commerce).

The Partnership Model: Given the regulatory complexity in both India and Indonesia, joint ventures (JVs) with local partners remain the most effective way to navigate FDI norms and local governance requirements (e.g., Emaar's JV with Adani).

Conclusion: Synthesized Recommendations

The determination of where to focus first in 2026 depends upon the alignment of a firm's capital structure with its operational strengths. The Indian market offers a unique combination of high GDP growth, a maturing digital regulatory environment, and a massive, pre-qualified talent pool. However, the "India First" strategy for B2C businesses is currently fraught with unit economics challenges, necessitated by exploding customer acquisition costs and low average order values. For these firms, the "Global First" approach—particularly targeting US or EU markets while using India as a Global Capability Center—provides the most sustainable path to profitability.

Conversely, for industrial manufacturers and technology service providers, the recent signing of the EU-India and US-India trade agreements has opened a historic window for direct market entry into India. The reduction of tariffs and the standardization of data privacy and tax laws have lowered the barriers to entry to their lowest levels in a decade. For these sectors, focusing on the Indian domestic market while leveraging its talent for global innovation represents the optimal strategic posture for the 2026–2030 cycle. Organizations must balance the "innovation density" of Western markets with the "unmatched scale and execution" of the Indian ecosystem to survive in an increasingly fragmented global economy.

The shift toward a "mindful scaling" era implies that companies launched in 2026 will be more accountable, stronger, and more globally competitive. As geographic expansion continues into Tier II and III Indian cities, and as digital platforms become the de facto "operating systems" for commerce in the GCC and Southeast Asia, the traditional boundaries between "domestic" and "global" are dissolving. The winners of 2026 will be those who can navigate this strategic bifurcation with "purpose, patience, and precision".

The Convergence of AI and Human Capital

By mid-2026, the integration of Artificial Intelligence into business operations is no longer a peripheral experiment but a core driver of efficiency and productivity. In the United States, real growth is expected to reaccelerate to 1.8% as AI adoption drives meaningful productivity gains. In India, GCCs have moved toward "innovation ownership," where AI talent demand now accounts for 22.5% of total hiring, highlighting their central role in global enterprise strategy.

The transition to an "AI-Native" era is fundamentally changing the way organizations view human capital. In the Singaporean market, junior developer salaries have stayed elevated, ranging from SGD 50,000 to 72,000, due to a persistent talent shortage in AI and cloud computing. Meanwhile, in India, the rise of "deep tech" startups in semiconductors and high-end robotics is building long-term capability rather than just new companies. The domestic semiconductor market in India is forecast to hit $100–110 billion by 2030, pointing to the immense scale of opportunity for startups specializing in chip design and hardware.

AI-Driven Performance Metrics (2026 Projections)

Segment | Efficiency Gain (%) | Primary Mechanism | Strategic Implication |

SaaS Management | 64% | Automation of routine tasks | Reduction in IT team overhead. |

D2C Marketing | 45% – 60% | Smart Bundling & AI Personalization | Direct improvement in AOV and Gross Margin. |

GCC Operations | 30% | Agentic AI (Autonomous Agents) | Faster scaling without human intervention. |

Global Logistics | 25% | AI-driven optimization | Reduction in delivery costs and time. |

The adoption of SaaS-management platforms (SMPs) is expected to grow from less than 10% in 2024 to over 50% by 2027, as organizations centralize the management of their sprawling digital stacks. For startups, this creates a dual pressure: the need to integrate AI to maintain internal efficiency, and the need to offer AI-driven value propositions to a customer base that is increasingly "AI-First."

Final Assessment: The Cost of Delay

As we enter the latter half of the 2020s, the "wait and watch" approach to the Indian market has become a significant competitive disadvantage. Enterprises that delay building their global capability centers in India are losing ground to competitors who are already achieving 30-60% operational optimization while maintaining global standards in engineering excellence.

The structural demand for premium technologies and goods in the Indian market, combined with the significant duty reductions of the EU-India FTA, has created a "perfect example" of a partnership between major global economies. For global SMEs, the choice is clear: choose India if the goal is to build a durable, innovation-led center that drives long-term digital transformation; choose Southeast Asia if the primary focus is on export-driven manufacturing or specific resource-driven sectors. Regardless of the choice, the "math of survival" in 2026 demands a ruthless focus on unit economics, regulatory readiness, and the strategic integration of AI across all layers of the business model.

Read More -

1. From Idea to MVP: A Step-by-Step Guide for Solo Founder

🔗 https://findnstart.com/blogs/from-idea-to-mvp-a-step-by-step-guide-for-solo-founder

2. How to Validate Your Startup Idea in 48 Hours for $0

🔗 https://findnstart.com/blogs/how-to-validate-your-startup-idea-in-48-hours-for-0

3. Remote vs. Local: Does Your Co-Founder Need to Live in the Same City?

🔗 https://findnstart.com/blogs/remote-vs-local-does-your-co-founder-need-to-live-in-the-same-city

4. The 2026 Startup Landscape: What Has Fundamentally Changed (and Why Founder Skills Matter More Than Ever)

5. The Most In-Demand Skills for Startup Founders in 2026

🔗 https://findnstart.com/blogs/the-most-in-demand-skills-for-startup-founders-in-2026

6. How to Find a Technical Co-Founder (Without a Six-Figure Salary)

🔗 https://findnstart.com/blogs/how-to-find-a-technical-co-founder-without-a-six-figure-salary

7. 5 Red Flags to Look for When Choosing a Startup Partner

🔗 https://findnstart.com/blogs/5-red-flags-to-look-for-when-choosing-a-startup-partner

8. How to Pitch Your Idea to Potential Co-Founders

🔗 https://findnstart.com/blogs/how-to-pitch-your-idea-to-potential-co-founders

9. How to Build a Portfolio that Attracts High-Growth Startup Founders

🔗 https://findnstart.com/blogs/how-to-build-a-portfolio-that-attracts-high-growth-startup-founders

10. Equity vs. Salary: How to Split Ownership with Your First Teammate

🔗 https://findnstart.com/blogs/equity-vs-salary-how-to-split-ownership-with-your-first-teammate

11. Why Joining an Early-Stage Startup is Better Than a Corporate Job

🔗 https://findnstart.com/blogs/why-joining-an-early-stage-startup-is-better-than-a-corporate-job

12. The Future of EdTech: Why Developers and Educators Need to Team Up Now

🔗 https://findnstart.com/blogs/the-future-of-edtech-why-developers-and-educators-need-to-team-up-now

13. The Architecture of Symbiosis: Analytical Perspectives on the Five Habits of Successful Startup Duos

14. Finding a Co-Founder in the AI Space: What Skills Should You Look For?

🔗 https://findnstart.com/blogs/finding-a-co-founder-in-the-ai-space-what-skills-should-you-look-for

15. Overcoming Analysis Paralysis and the Strategic Path to Execution

🔗 https://findnstart.com/blogs/overcoming-analysis-paralysis-and-the-strategic-path-to-execution

16. From College Project to Company: How to Find Your Student Co-Founder

🔗 https://findnstart.com/blogs/from-college-project-to-company-how-to-find-your-student-co-founder

17. How to Start a Startup While Working a Full-Time Job

🔗 https://findnstart.com/blogs/how-to-start-a-startup-while-working-a-full-time-job

18. How to Build a HealthTech Startup Without a Medical Degree

🔗 https://findnstart.com/blogs/how-to-build-a-healthtech-startup-without-a-medical-degree

19. The Solitary Architect: Executive Isolation in Entrepreneurship

20. The 2026 Guide to Launching a SaaS as a Solo Developer

21. What Sustainable Growth Actually Looks Like

🔗 https://findnstart.com/blogs/what-sustainable-growth-actually-looks-like

22. The Early Warning Signs Your Startup Is in Trouble

🔗 https://findnstart.com/blogs/the-early-warning-signs-your-startup-is-in-trouble

23. How to Grow Without Burning Out

🔗 https://findnstart.com/blogs/how-to-grow-without-burning-out

24. The Truth About “Runway” Most Founders Ignore

🔗 https://findnstart.com/blogs/the-truth-about-runway-most-founders-ignore

25. Revenue Solves More Problems Than Funding

🔗 https://findnstart.com/blogs/revenue-solves-more-problems-than-funding

26. What No One Tells You About Being a Solo Founder

🔗 https://findnstart.com/blogs/what-no-one-tells-you-about-being-a-solo-founder

27. Why Smart People Quit High-Paying Jobs to Build Startups (And Why Most Regret It)

28. Why Most Startup Advice on Twitter Is Dangerous

🔗 https://findnstart.com/blogs/why-most-startup-advice-on-twitter-is-dangerous

29. Decision Fatigue: The Silent Startup Killer

🔗 https://findnstart.com/blogs/decision-fatigue-the-silent-startup-killer

30. Fear vs Logic: How Founders Actually Make Decisions

🔗 https://findnstart.com/blogs/fear-vs-logic-how-founders-actually-make-decisions

31. How Overthinking Destroys Early Momentum

🔗 https://findnstart.com/blogs/how-overthinking-destroys-early-momentum

32. Ideas Don’t Scale. Systems Do.

🔗 https://findnstart.com/blogs/ideas-dont-scale-systems-do

33. The First Hire That Actually Matters

🔗 https://findnstart.com/blogs/the-first-hire-that-actually-matters

34. How the First 100 Users Decide Your Startup’s Fate

🔗 https://findnstart.com/blogs/how-the-first-100-users-decide-your-startups-fate

35. Why Your Startup Doesn’t Need Growth — It Needs Focus

🔗 https://findnstart.com/blogs/why-your-startup-doesnt-need-growthit-needs-focus

36. Why Most Startups Die Quietly

🔗 https://findnstart.com/blogs/why-most-startups-die-quietly

37. Lessons Learned Too Late by First-Time Founders

🔗 https://findnstart.com/blogs/lessons-learned-too-late-by-first-time-founders

38. The Myth of the “Overnight Success” Startup

🔗 https://findnstart.com/blogs/the-myth-of-the-overnight-success-startup

Protect Your Future: The Precision Vesting Calculator

Don't let a "handshake deal" complicate your exit. Map out your ownership journey with our Vesting Calculator

Calculate Your Vesting Schedule →