Why Venture Capital Is Expanding Rapidly in Brazil

July 2, 2026 by Harshit Gupta

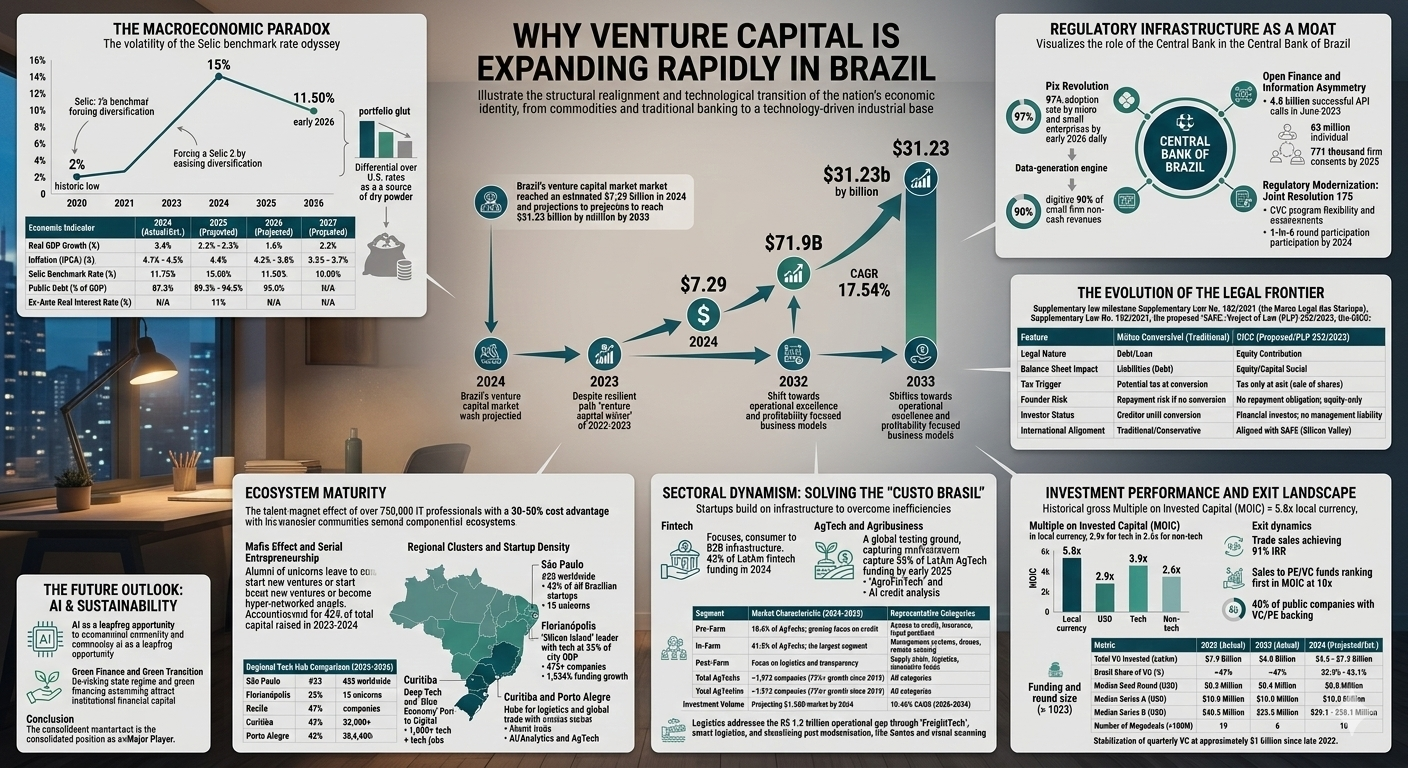

The rapid expansion of the venture capital ecosystem in Brazil represents a fundamental structural realignment of the nation’s economic identity, transitioning from a historical reliance on commodities and traditional banking toward a technology-driven, high-growth industrial base. This metamorphosis is not merely a cyclical trend but a convergence of aggressive regulatory modernization by the Central Bank of Brazil, the maturation of a resilient entrepreneurial class, and the strategic redirection of domestic and international capital into innovation-led assets. By 2024, the Brazilian venture capital investment market reached an estimated valuation of $7.29 billion, with projections indicating a compound annual growth rate of 17.54% through 2033, potentially reaching $31.23 billion. This trajectory persists despite the "venture capital winter" of 2022–2023, which catalyzed a shift toward operational excellence and profitability-focused business models.

The Macroeconomic Paradox: Volatility as a Catalyst for Maturity

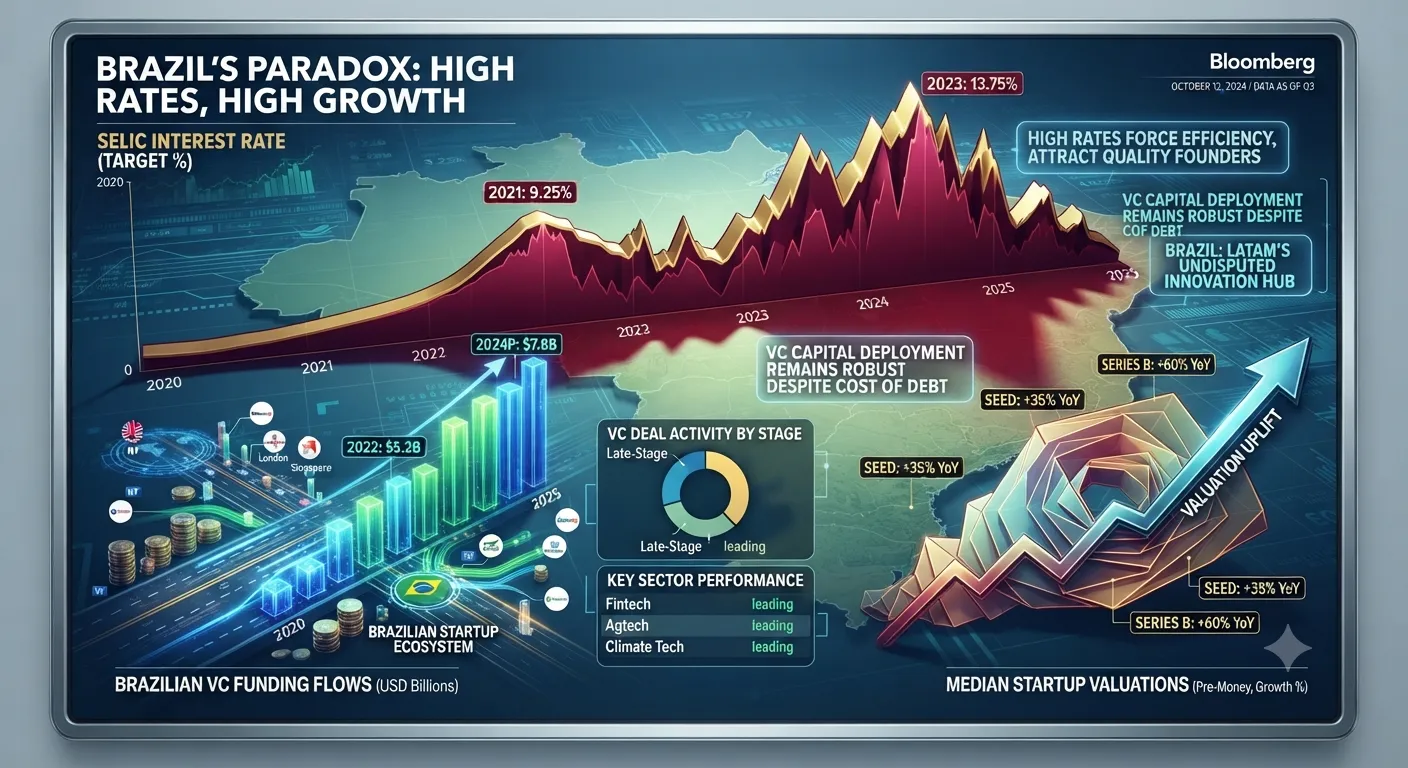

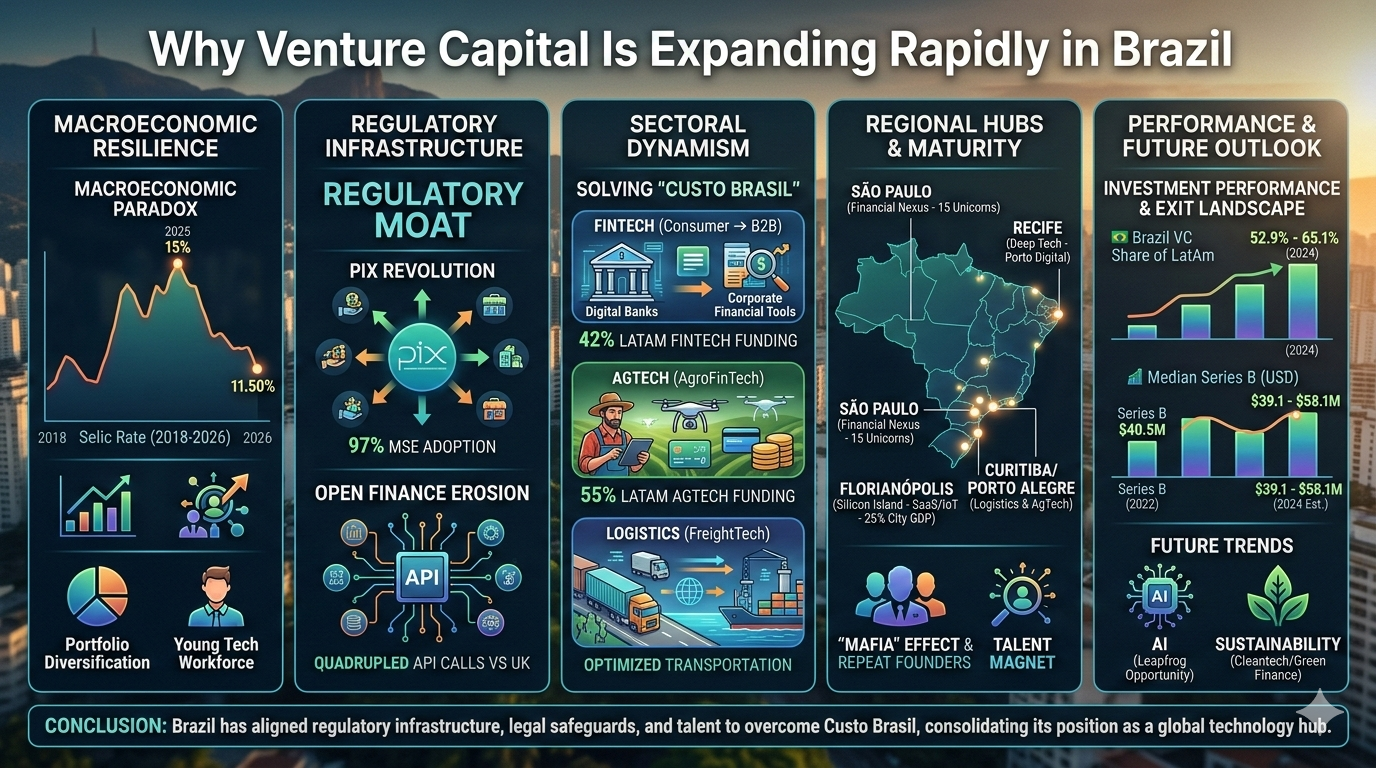

The expansion of venture capital in Brazil is inextricably linked to the nation’s macroeconomic cycles, particularly the fluctuations of the benchmark Selic interest rate. Between 2018 and 2026, the Brazilian economy experienced a dramatic interest rate odyssey that fundamentally altered investor behavior. In 2020, the Central Bank of Brazil (BCB) lowered the Selic rate to a historic low of 2% in response to the global pandemic, effectively ending the era of "easy" returns in low-risk fixed-income assets. This environment forced local institutional investors, pension funds, and family offices to diversify their portfolios into higher-risk asset classes, such as private equity and venture capital, to preserve yield.

The subsequent inflationary surge led the BCB to reverse this policy, raising the Selic rate to a restrictive 15% by mid-2025. While high interest rates typically throttle venture activity by increasing the cost of capital, the Brazilian ecosystem has demonstrated unique resilience. Market analysts describe the current environment as a "coiled spring," where the fundamentals for a massive surge in activity—including a young, tech-savvy workforce and a professionalized investment sector—are already in place, awaiting the anticipated easing cycle projected for early 2026.

Macroeconomic Landscape and Forecast (2024–2027)

Economic Indicator | 2024 (Actual/Est.) | 2025 (Projected) | 2026 (Projected) | 2027 (Projected) |

Real GDP Growth (%) | 3.4% | 2.2% - 2.3% | 1.6% | 2.2% |

Inflation (IPCA) (%) | 4.1% - 4.5% | 4.4% | 4.2% - 3.8% | 3.5% - 3.7% |

Selic Benchmark Rate (%) | 11.75% | 15.00% | 11.50% | 10.00% |

Public Debt (% of GDP) | 87.3% | 89.3% - 94.5% | 95.0% | N/A |

Ex-Ante Real Interest Rate (%) | N/A | 11% | N/A | N/A |

The significance of these indicators for venture capital expansion lies in the "portfolio glut" and the concentration of financial capital seeking diversification in a high-yield environment. Even with the Selic at 15%, Brazil continues to attract high portfolio flows due to the significant real interest rate differential—often exceeding 11 percentage points—over U.S. rates. This capital depth provides a buffer for the venture ecosystem, ensuring that "dry powder" remains available for high-quality startups that can demonstrate path-to-profitability in a high-cost environment.

Regulatory Infrastructure as a Competitive Moat

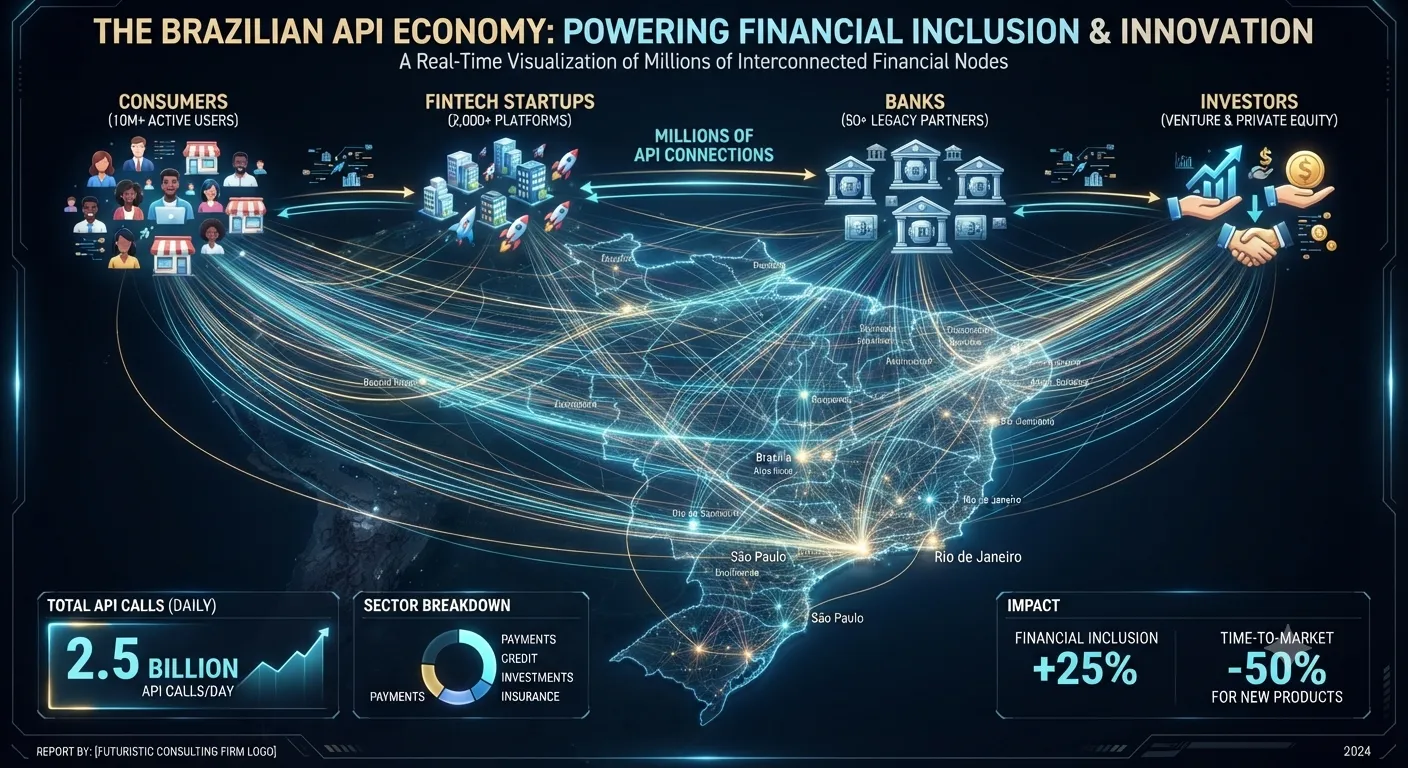

Perhaps the most potent "why" behind Brazil's venture capital expansion is the role of the Central Bank of Brazil as a proactive facilitator of innovation. Through a series of transformative initiatives, the BCB has created a digital public infrastructure that serves as a moat for the entire fintech and agtech sectors.

The Pix Revolution and Financial Digitization

Launched in late 2020, Pix has become the cornerstone of Brazil's digital economy. By early 2026, its adoption rate reached near-universal levels among micro and small enterprises (MSEs), with 97% of firms utilizing the platform daily. For venture capital investors, Pix represents more than a payment method; it is a data-generation engine. By digitizing 90% of non-cash business revenues for small firms, Pix has provided the raw data necessary for fintechs to build more accurate credit risk models.

The efficiency of Pix—characterized by low acceptance costs and the removal of multiple intermediaries—has fundamentally changed the unit economics of startups. This has allowed a new generation of fintechs to reach segments of the population previously excluded from the formal financial system. The institutional trust built through Pix has further catalyzed the adoption of Open Finance, which reached 63 million consents from individuals and 771 thousand from firms by 2025.

Open Finance and the Erosion of Information Asymmetry

The synchronization of a popular real-time payment system with a comprehensive Open Finance framework makes Brazil a global benchmark for financial innovation. In June 2023, Brazil recorded 4.8 billion successful API calls, quadrupling the volume of the United Kingdom, despite the UK having a head start in open banking implementation. This ecosystem reduces the traditional "information asymmetry" that once favored incumbent banks, allowing venture-backed startups to compete based on service quality and data-driven personalization rather than historical incumbency.

Regulatory Modernization: Joint Resolution 175

Further strengthening the investment environment, the 2024 implementation of Joint Resolution BCB/CVM No. 175 has modernized the regulation of Investment Funds. This framework provides greater flexibility for fund managers, including the ability to structure corporate venture capital (CVC) programs with a focus on both financial returns and strategic operational support. CVCs have become integral to the ecosystem, participating in one in every six startup funding rounds in 2024, providing a crucial bridge between established industrial players and innovative startups.

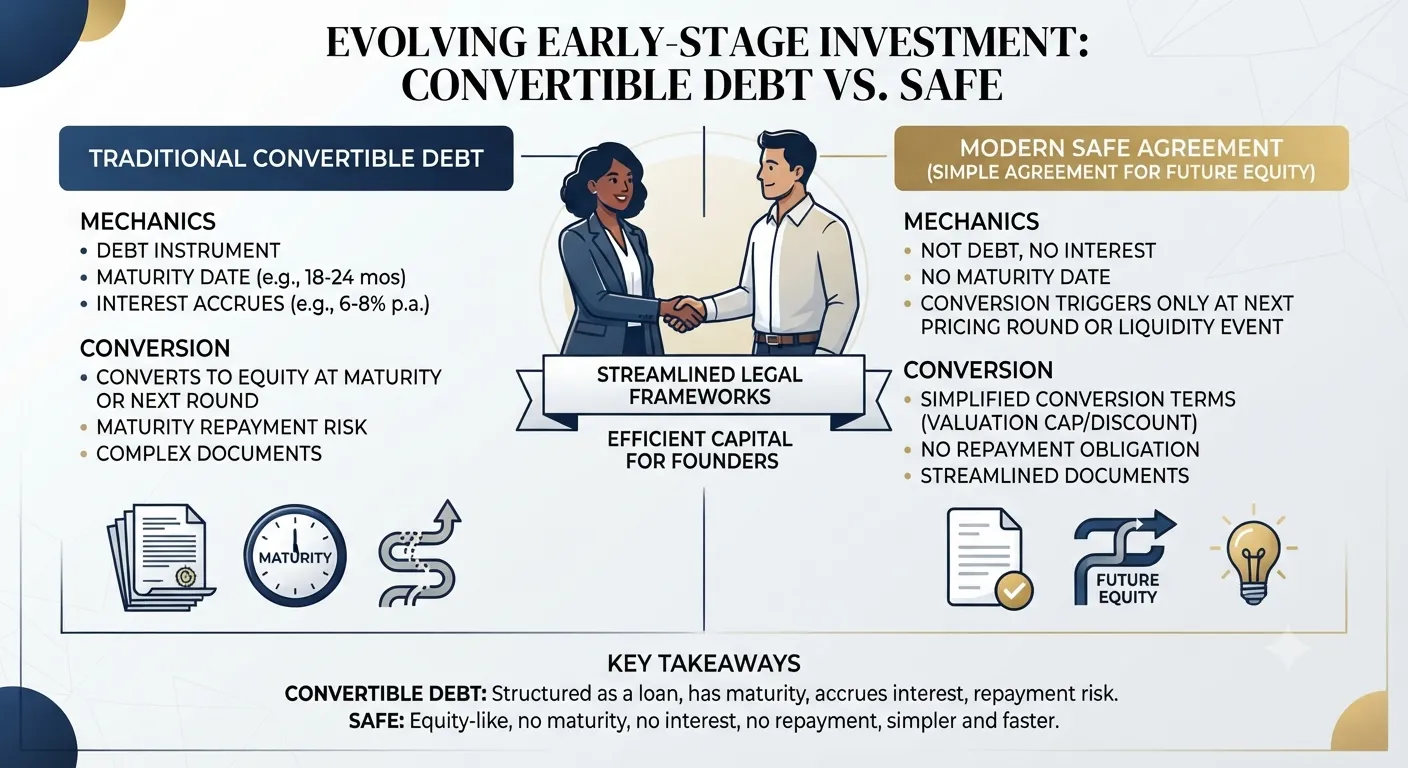

The Evolution of the Legal Frontier: Security and Standardization

Historically, the complexity of the Brazilian legal and tax system—the "Custo Brasil"—was a significant hurdle for international venture capital. However, recent legislative milestones have dramatically improved the legal security for investors.

The Marco Legal das Startups (2021)

Supplementary Law No. 182/2021, known as the Marco Legal das Startups, provided the first official legal definition of a startup in Brazil (companies with up to R$ 16 million in annual revenue and up to 10 years of registration). Crucially, it introduced the "regulatory sandbox," allowing government agencies like ANVISA and the BCB to suspend certain regulations for innovative companies to test new products.

The law also addressed investor liability, explicitly stating that "angel investors" and those using convertible instruments are not considered partners and, therefore, are not liable for the company’s labor or tax debts except in cases of fraud. This protection was vital in attracting risk-averse domestic capital into the pre-seed and seed stages.

The SAFE Transition: PLP 252/2023 and the CICC

While the 2021 law validated the mútuo conversível (convertible loan), this instrument remained technically a debt on the startup’s balance sheet, which was not "founder-friendly". As of 2025–2026, the legislative focus has shifted to Project of Law (PLP) 252/2023, which proposes the Contrato de Investimento Conversível em Capital Social (CICC).

The CICC is designed to mirror the Silicon Valley "Simple Agreement for Future Equity" (SAFE). It treats the investment as equity from the beginning, removing the debt burden and providing clearer tax rules. Under the CICC, taxes are not triggered at the moment of conversion into shares but only when those shares are eventually sold. This move toward international standards is expected to further simplify early-stage fundraising, making it faster and cheaper for both founders and investors.

Comparison of Primary Investment Instruments in Brazil

Feature | Mútuo Conversível (Traditional) | CICC (Proposed/PLP 252/2023) |

Legal Nature | Debt/Loan | Equity Contribution |

Balance Sheet Impact | Liabilities (Debt) | Equity/Capital Social |

Tax Trigger | Potential tax at conversion | Tax only at exit (sale of shares) |

Founder Risk | Repayment risk if no conversion | No repayment obligation; equity-only |

Investor Status | Creditor until conversion | Financial Investor; no management liability |

International Alignment | Traditional/Conservative | Aligned with SAFE (Silicon Valley) |

Sectoral Dynamism: Solving the "Custo Brasil"

Venture capital in Brazil is primarily expanding in sectors that address the fundamental inefficiencies of the economy. Startups are not just creating new "nice-to-have" services; they are building the infrastructure required for the nation to compete globally.

Fintech: From Consumer Banking to B2B Infrastructure

Fintech remains the dominant vertical, capturing 42% of total fintech funding in Latin America by 2024. The current wave of fintech expansion is characterized by a shift from consumer-facing digital banks (like Nubank) toward specialized B2B financial services, insurtech, and tax-as-a-service platforms. Companies like Velotax, Kanastra, and Pagaleve are attracting large "Series B" rounds to solve specific pain points in tax compliance, credit securitization, and "Buy Now Pay Later" for the B2B sector.

Agribusiness and AgTech: The Global Testing Ground

Brazil’s role as the world’s leading exporter of soybeans, sugar, and coffee makes it a natural hub for AgTech. The sector is responsible for nearly half of all Brazilian exports and a fifth of its GDP. AgTech investments reached a surge in early 2025, with Brazil capturing 55% of all Latin American AgTech funding.

The evolution of AgTech is increasingly tied to "AgroFinTech" solutions. Because Brazilian farmers often face restricted access to traditional bank credit, startups like Agrolend have developed AI-driven credit analysis that waives the need for physical guarantees like mortgages or grain pledges. These platforms integrate behavioral and agronomic data—often through mobile devices—to approve and disburse credit in minutes.

Growth and Segmentation of Brazil AgTech Market

Segment | Market Characteristic (2024-2025) | Representative Categories |

Pre-Farm | 18.6% of AgTechs; growing focus on credit | Access to credit, insurance, input purchase |

In-Farm | 41.5% of AgTechs; the largest segment | Management systems, drones, remote sensing |

Post-Farm | Focus on logistics and transparency | Supply chain, logistics, innovative foods |

Total AgTechs | ~1,972 companies (75%+ growth since 2019) | All categories |

Investment Volume | Projecting $1.56B market by 2034 | 10.46% CAGR (2026-2034) |

Logistics and Supply Chain: Overcoming Infrastructure Gaps

The "Custo Brasil" is most visible in the logistics sector, where operational costs average R1.2 trillion annually, driven by fuel prices and aging infrastructure. Venture capital is flowing into "FreightTech" and smart logistics to address these bottlenecks. Startups like Loggi and CargoX are using technology to address the "last-mile" challenge and optimize transportation through digital freight matching.

The modernization of ports, such as the Port of Santos, has become a focus for "maritime tech" and IoT. Collaborative programs like the Port of Ashdod's "innovation embassy" in Santos aim to implement AI-driven visual scanning and advanced maintenance systems to reduce container turnaround times and enhance operational excellence.

The Ecosystem Maturity: Talent, "Mafias," and Regional Clusters

A critical internal factor for the expansion of venture capital is the presence of a "talent magnet" effect. Brazil has over 750,000 IT professionals, including over 550,000 core software developers, offering a 30–50% cost advantage compared to U.S.-based talent.

The "Mafia" Effect and Serial Entrepreneurship

The ecosystem is now experiencing the "alumni effect," common in established hubs like Silicon Valley. Former employees and founders of early unicorns—referred to as the "99 mafia" or "Nubank mafia"—are leaving to start new ventures or become "hyper-networked angels". These repeat founders are highly attractive to VCs; they accounted for 42% of total capital raised in 2023–2024. Their experience in scaling runaway successes allows them to challenge the status quo and improve people's lives through more sophisticated technology solutions.

Regional Clusters and Startup Density

While São Paulo remains the regional ranking leader (#23 worldwide), hosting 50% of the nation's startups and most of its unicorns, other cities are emerging with specialized focuses.

Florianópolis: Known as "Silicon Island," it is the national leader in tech contribution to GDP (25%). The city boasts ten times more startups per capita than São Paulo and focuses on B2B SaaS and digital infrastructure.

Recife: A hub for Deep Tech and "Blue Economy" innovation, with a high concentration of IT students and IT-tailored educational programs like the CESAR School.

Curitiba and Porto Alegre: Strong ecosystems for logistics-tech (e.g., Logcomex) and AgTech.

Regional Tech Hub Comparison (2025-2026)

Hub | Regional Focus | Key Economic Driver | Startup Ecosystem Characteristic |

São Paulo | Finance & Services | National Financial Hub | 43% of all Brazilian startups; 15 unicorns |

Florianópolis | B2B SaaS & IoT | 25% of City GDP | 6,000+ tech companies; 38,400+ tech jobs |

Recife | Deep Tech & Blue Econ | Porto Digital | 475+ companies; 1,534% funding growth |

Curitiba | Logistics & Global Trade | Industrial & Logistics | High density of AI/Analytics platforms |

Investment Performance and the Exit Landscape

The final "why" for venture capital expansion is the historical performance and the emerging market for exits. Brazilian PE and VC delivered an average gross Multiple on Invested Capital (MOIC) of 5.8x in local currency and 2.9x in USD terms. Despite currency volatility, tech deals have demonstrated a higher average return than non-tech deals, with an average gross MOIC in USD of 3.9 compared to 2.6 for the non-tech segment.

Exit Dynamics and Liquidity Events

The path to liquidity in Brazil is traditionally dominated by "trade sales" (M&A) to strategic acquirers or larger private equity funds. Trade sales achieve an impressive IRR of 91% for tech companies, while Sales to PE/VC funds rank first in MOIC at 10x. While IPOs remain a goal for mature companies like Creditas and Agibank, the Brazilian capital markets have been slower to reopen for new listings since the 2021 peak. However, approximately 40% of companies that went public in the last decade had venture capital or private equity backing, reinforcing the sector's role in strengthening the public markets.

Brazil Venture Capital Funding and Round Sizes (2022–2024)

Metric | 2022 (Actual) | 2023 (Actual) | 2024 (Projected/Est.) |

Total VC Invested (LatAm) | $7.9 Billion | $4.0 Billion | $4.5 - $7.3 Billion |

Brazil Share of VC (%) | ~47% | ~47% | 52.9% - 65.1% |

Median Seed Round (USD) | $0.5 Million | $0.4 Million | $0.5 Million |

Median Series A (USD) | $10.0 Million | $10.0 Million | $10.0 Million |

Median Series B (USD) | $40.5 Million | $25.5 Million | $39.1 - $58.1 Million |

Number of Megadeals (>100M) | 19 | 6 | 10 |

The stabilization of quarterly VC investment at approximately $1 billion since late 2022 suggests that the market has reached a healthy floor. Investors are no longer in a frenzy but are writing larger checks for fewer companies with stronger traction and mature business fundamentals.

The Future Outlook: AI, Sustainability, and Beyond

As Brazil moves into 2026 and 2027, the venture capital landscape is expected to be defined by two massive trends: Artificial Intelligence and the Green Transition.

AI and the Leapfrog Opportunity

Brazil is positioned to "leapfrog" traditional technology cycles using AI, much like Africa bypassed the desktop computing era by moving straight to mobile. Startups are already integrating generative AI into culture and operations to drive up revenue and reduce the high labor costs associated with the "Custo Brasil". The Central Bank is expected to play a role here as well, potentially developing proactive regulatory policies for AI development similar to those used for fintech.

Green Finance and the "Wall Street Consensus"

Brazil’s wealth of biological resources and critical minerals (such as niobium and rare earths) provides a historic opportunity to lead the global energy transition. Venture capital is increasingly focused on "cleantech" and "blue economy" projects, including regenerative agriculture, carbon sequestration, and next-generation biofuels. This shift aligns with the "Wall Street Consensus," where Brazil’s de-risking state regime and green financing strategies are attracting institutional financial capital into sustainable development.

Conclusion

Venture Capital is expanding rapidly in Brazil because the nation has successfully aligned its regulatory infrastructure, legal safeguards, and talent pool with the demands of a high-tech global economy. The "Custo Brasil," while still a challenge, has become the primary source of opportunity for entrepreneurs solving structural inefficiencies in finance, agriculture, and logistics. The resilience of the ecosystem through the high-interest-rate environment of 2025 demonstrates that Brazil's tech hub status is no longer a fragile experiment but a foundational pillar of its long-term economic strategy. As the interest rate easing cycle begins in 2026 and instruments like the CICC are formalized, Brazil is poised to consolidate its position not just as the leader of Latin American innovation, but as a major player in the global technology landscape.

Protect Your Future: The Precision Vesting Calculator

Don't let a "handshake deal" complicate your exit. Map out your ownership journey with our Vesting Calculator

Calculate Your Vesting Schedule →