Why Toronto Is Becoming Canada’s Startup Capital

June 29, 2026 by Harshit Gupta

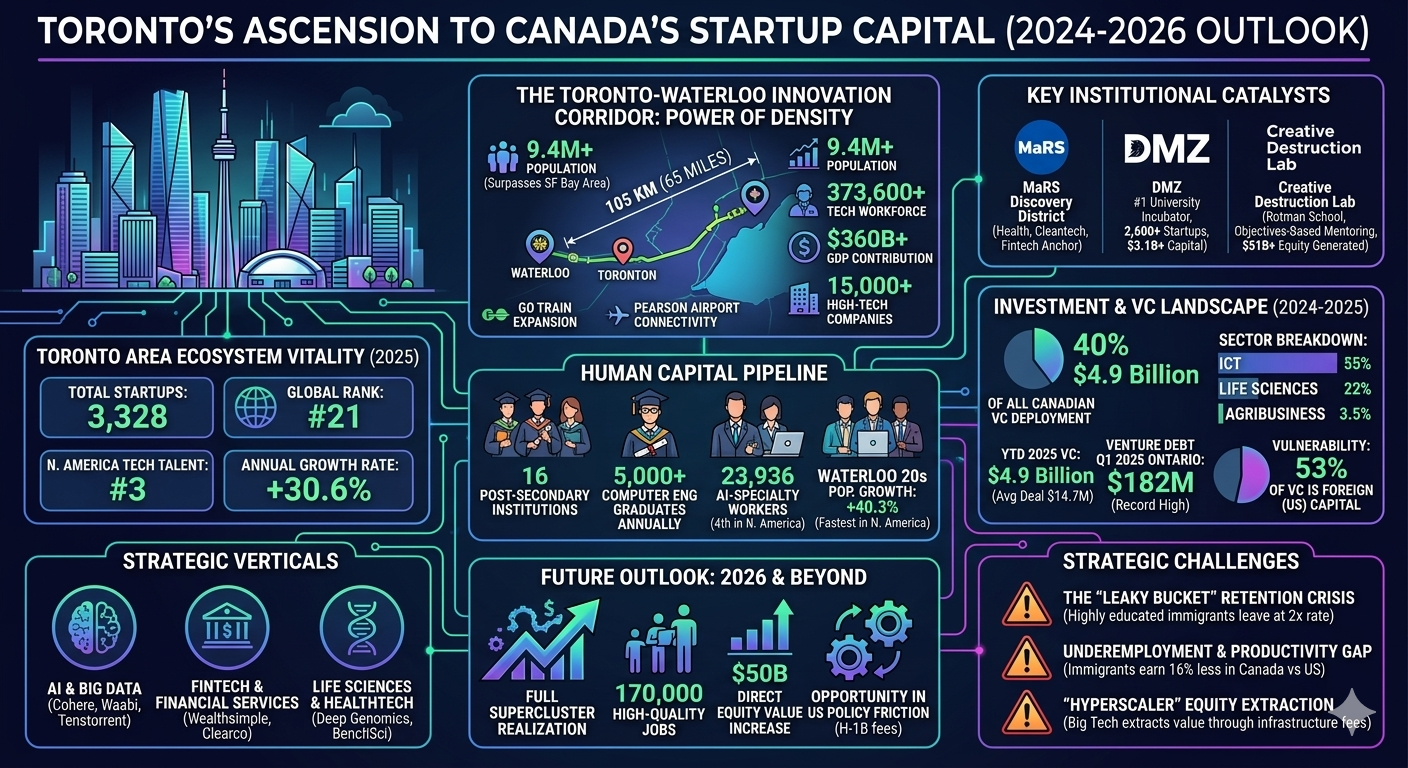

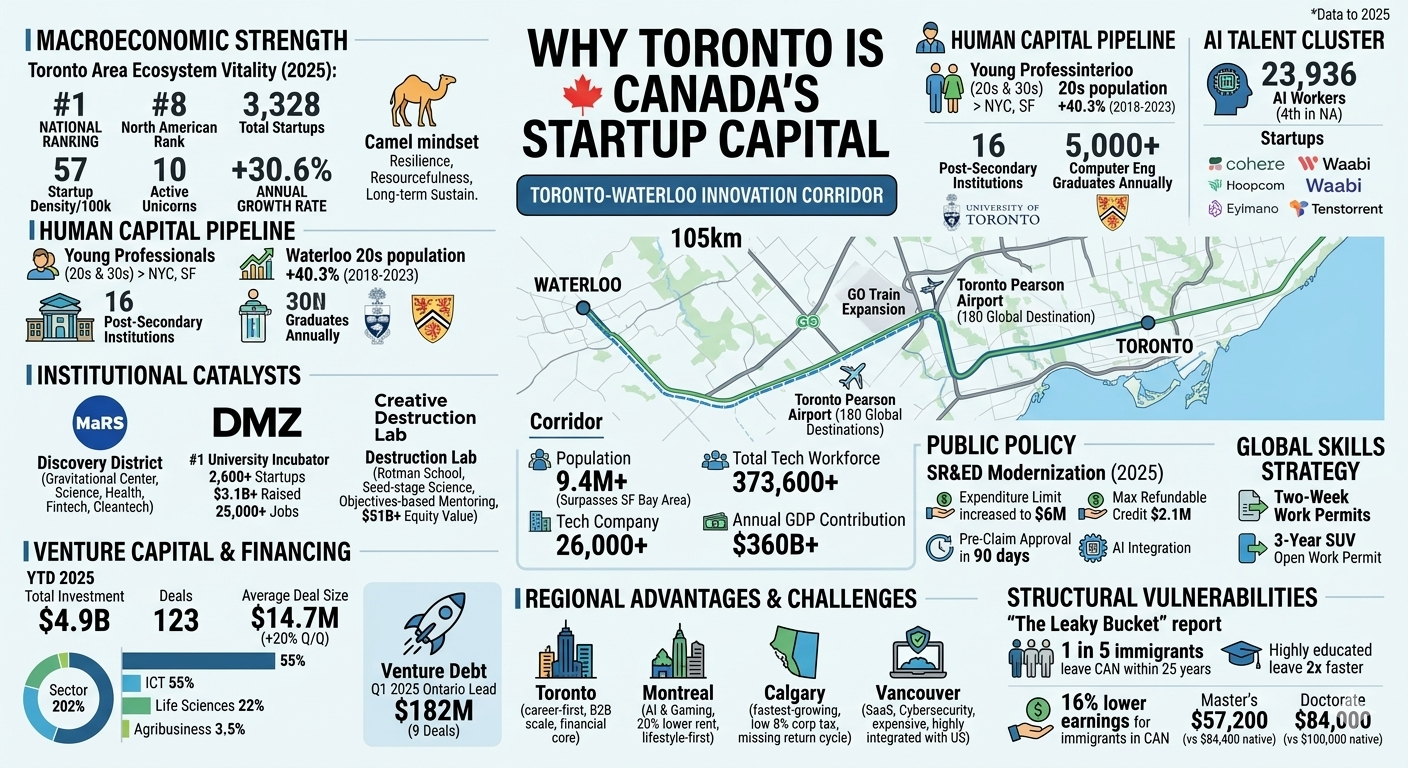

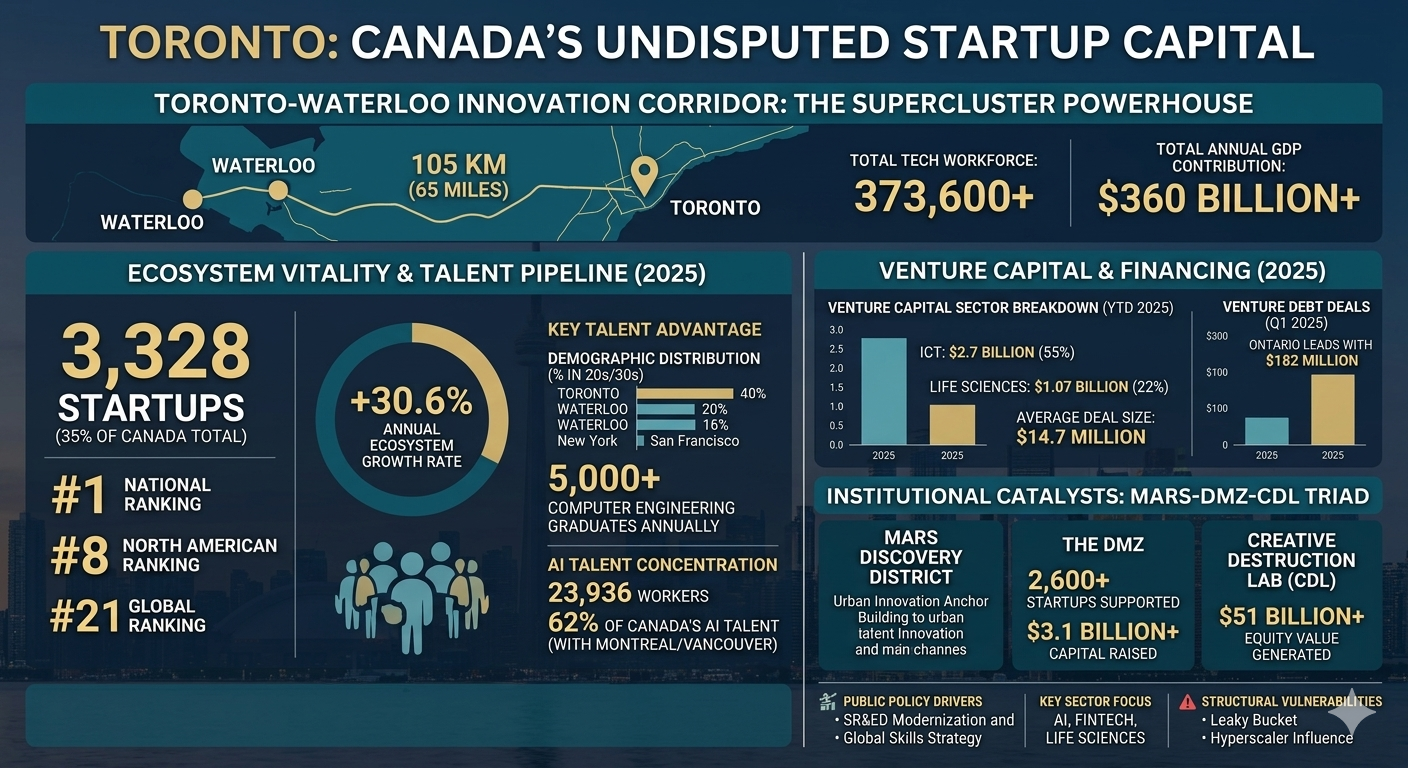

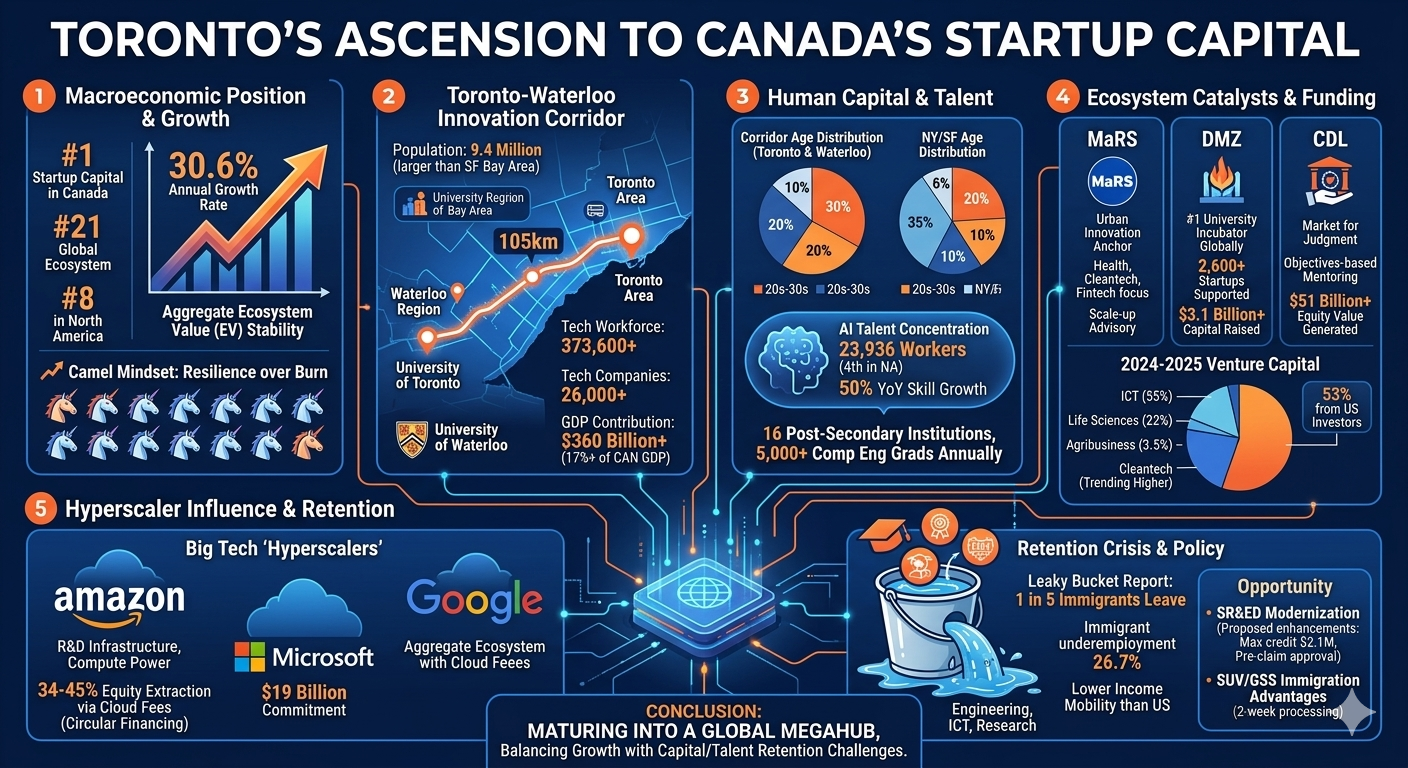

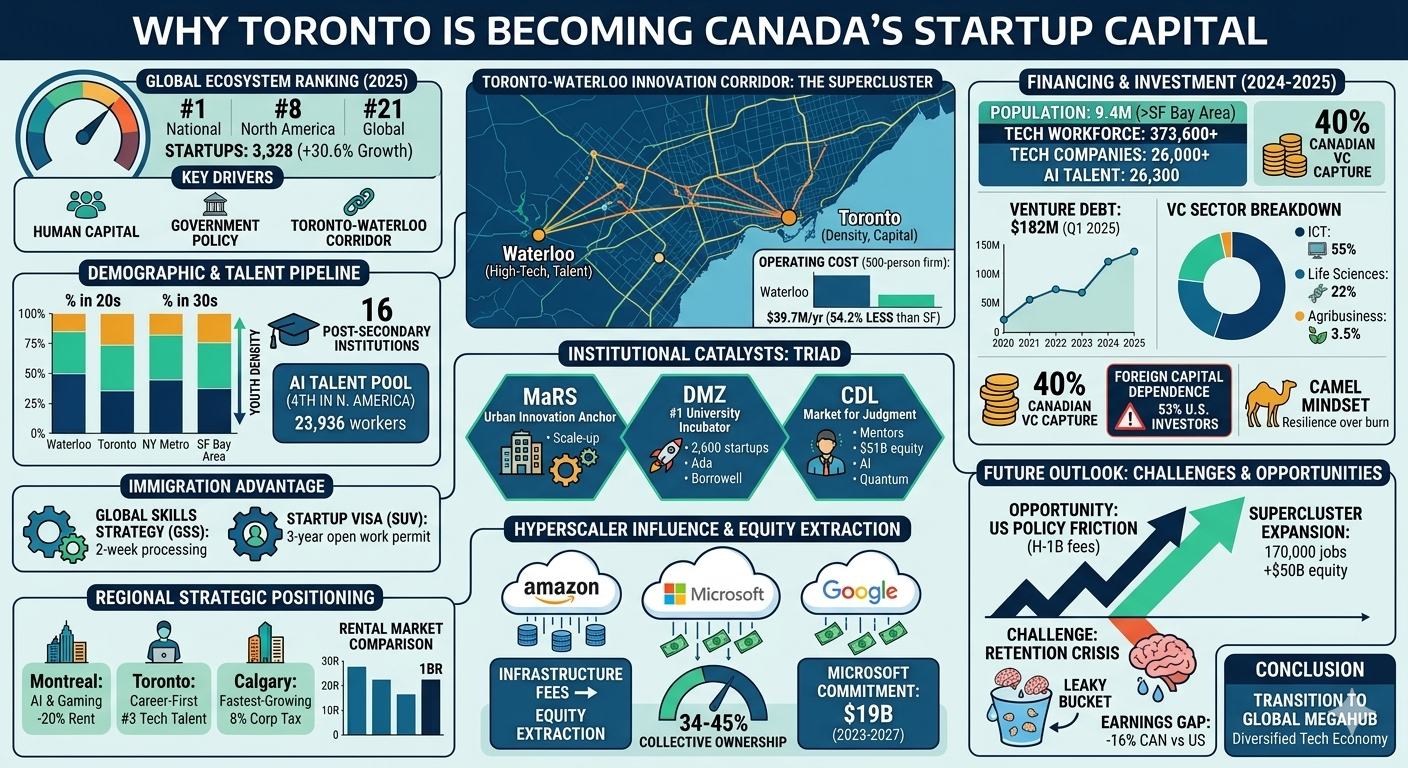

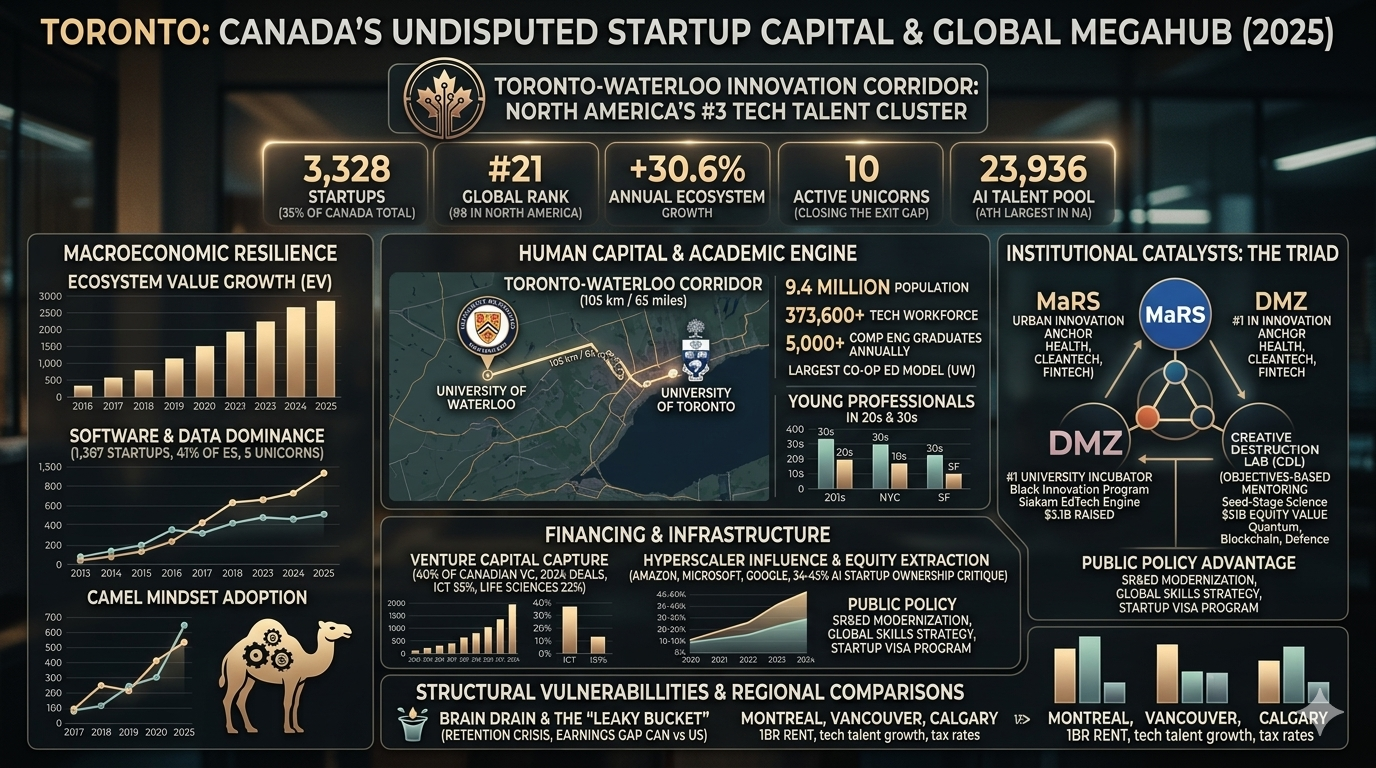

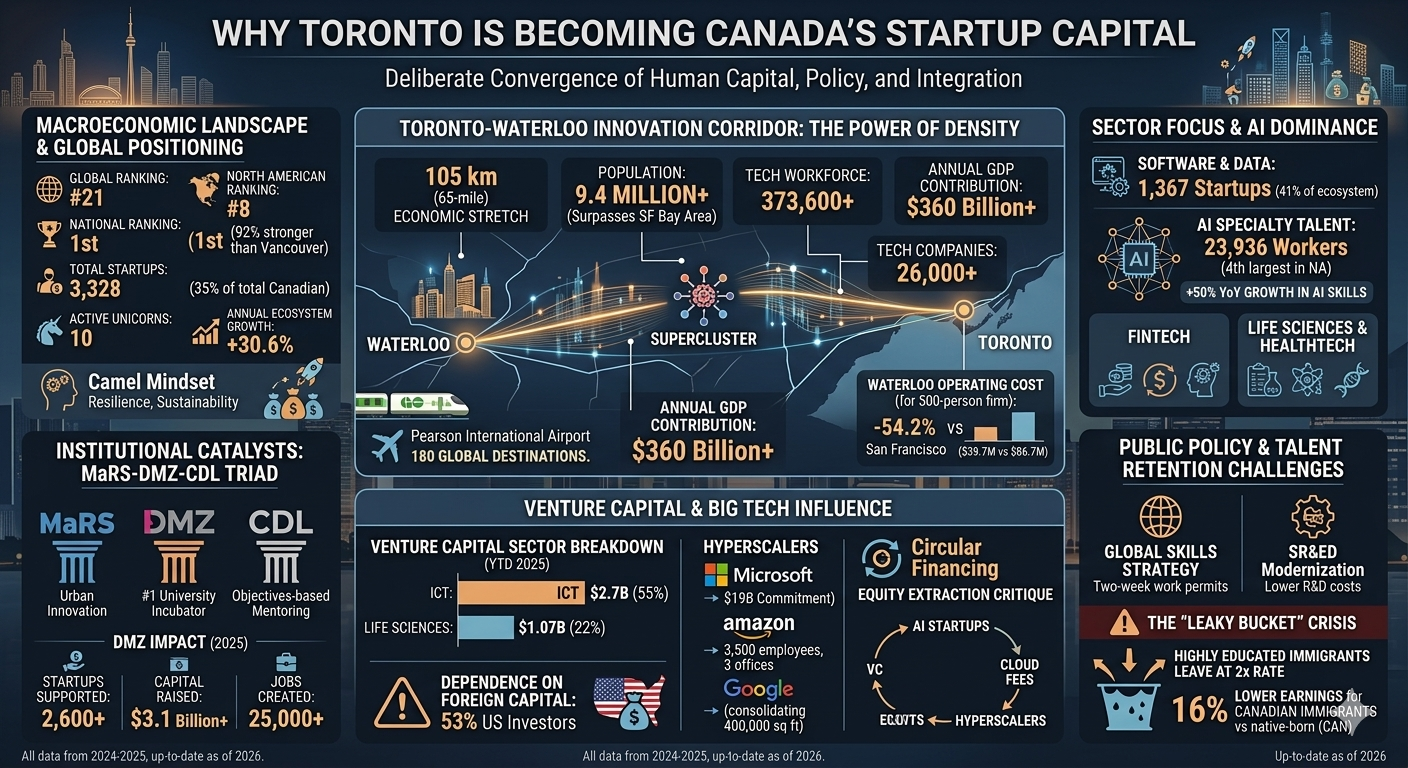

The transformation of the Toronto Area into Canada’s undisputed startup capital is the result of a deliberate convergence of human capital concentration, aggressive federal and provincial policy intervention, and a strategic geographic integration known as the Toronto-Waterloo Innovation Corridor. As of 2025, the Toronto Area is home to 3,328 startups, representing approximately 35% of the total Canadian startup population. This density is not merely a domestic achievement; the ecosystem has climbed to the #21 position globally and #8 in North America, recording an annual growth rate of 30.6%. By displacing traditional hubs such as New York Metro to claim the #3 spot in North American tech talent rankings—trailing only the San Francisco Bay Area and Seattle—Toronto has signaled a fundamental shift in the continental geography of innovation.

Macroeconomic Landscape and Global Ecosystem Positioning

The maturation of the Toronto startup scene is evidenced by its increasing resilience in the face of a complex global macroeconomic environment. While much of the global startup landscape faced a dramatic shake-up in 2024 and early 2025, with aggregate ecosystem values (EV) declining by nearly 31% in some regions, Toronto maintained its upward trajectory through a disciplined focus on high-value sectors such as software, data, and artificial intelligence. The ecosystem’s strength is particularly concentrated in Software & Data, which hosts 1,367 startups—representing 41% of the local ecosystem—and five of the city’s ten unicorns.

Toronto Area Ecosystem Vitality Index (2025) | Data Point |

National Ranking | 1st |

North American Ranking | 8th |

Global Ranking | 21st |

Total Startups | 3,328 |

Active Unicorns | 10 |

Startup Density (per 100k people) | 57 |

Annual Ecosystem Growth Rate | +30.6% |

The narrative of Toronto’s growth has historically been overshadowed by the "brain drain" and the early acquisition of its most promising ventures by American interests. However, current data suggests that the ecosystem has reached a critical mass where local founders are choosing to scale rather than exit prematurely. This shift is supported by a robust network of 3,000 investors and mentors and the creation of over 25,000 jobs within specialized hubs like the DMZ. The emergence of 10 unicorns indicates that the "exit gap" is narrowing, as the city now possesses the mentorship and late-stage capital required to sustain billion-dollar valuations within Canadian borders.

The Role of Ecosystem Value and Discipline

In the 2025 Global Startup Ecosystem Ranking, the focus has shifted toward Ecosystem Value (EV), a measure of economic impact calculated through total exit valuations and startup valuations over a two-and-a-half-year period. Although large exits (defined as those over $50 million) decreased by 31% across the top 40 global ecosystems, Toronto’s stability in the #1 national spot—ranking 92% stronger than Vancouver—highlights its role as the primary engine of Canadian equity creation. This dominance is underpinned by a "Camel mindset," a philosophy increasingly adopted by Toronto-based founders who prioritize resilience, resourcefulness, and long-term sustainability over the "burn-at-all-costs" mentality often seen in Silicon Valley.

The Toronto-Waterloo Innovation Corridor: The Power of Density

The most significant driver of Toronto’s status as a startup capital is its integration into the Toronto-Waterloo Innovation Corridor. This 105-kilometer (65-mile) economic stretch functions as a "supercluster," connecting the massive urban density and financial resources of Toronto with the high-tech research and talent production of the Waterloo Region. This corridor represents one of the largest tech clusters in North America, with a population of 9.4 million people—surpassing the population of the San Francisco Bay Area.

Corridor Talent and Infrastructure Metrics (2025) | Statistics |

Total Tech Workforce | 373,600+ |

Tech Company Population | 26,000+ |

AI-Specialty Talent Cluster | 26,300 |

Software Engineering Concentration (Waterloo) | 58% |

Post-Secondary Student Population | 662,000+ |

Total Annual GDP Contribution | $360 Billion+ |

The corridor added the most tech jobs in North America in 2025, driven by the widespread adoption of AI and the presence of world-class engineering schools like the University of Waterloo and the University of Toronto. The symbiotic relationship within the corridor allows companies to leverage Toronto’s deep capital pools and B2B markets while tapping into Waterloo’s research ecosystem, where operating costs for a 500-person firm are approximately $39.7 million annually—54.2% less than in San Francisco.

Connectivity and the "Supercluster" Hypothesis

The economic theory of agglomeration is clearly visible within the corridor, where the concentration of over 15,000 high-tech companies facilitates knowledge spillover and specialized labor markets. The corridor contributes more than 17% of Canada's total GDP, acting as a "hub-and-spoke" model that breeds secondary clusters across the country. Infrastructure improvements, such as the GO Train expansion and the proximity to Toronto Pearson International Airport—which serves 180 global destinations—have effectively reduced the "friction of distance" between these two hubs. This connectivity ensures that investors and capital can flow seamlessly between the mature Toronto market and the nascent, high-growth startups in Waterloo.

The Human Capital Pipeline: Academic and Demographic Advantages

Toronto’s ascendance is fundamentally a talent story. The region possesses a unique demographic profile, with young professionals in their 20s and 30s making up a larger percentage of the population than in New York or San Francisco. In Waterloo specifically, the population of residents in their 20s grew by 40.3% between 2018 and 2023, a rate 50% faster than any other market on the continent.

Demographic Distribution of Tech Markets (2025) | % in 20s | % in 30s |

Waterloo Region | 19.1% | 15.9% |

Toronto Area | 16.3% | 15.7% |

New York Metro | Lower than TOR/WAT | Lower than TOR/WAT |

San Francisco Bay Area | Lower than TOR/WAT | Lower than TOR/WAT |

The corridor is home to 16 post-secondary institutions producing over 5,000 computer engineering graduates annually. The University of Waterloo, which hosts the largest computer science program in North America, provides a continuous stream of talent through its co-operative education model, the largest of its kind globally. This pipeline is supplemented by Toronto’s ability to attract international students and professionals, many of whom are incentivized by Canada’s favorable immigration pathways.

The AI Talent Concentration

Toronto has positioned itself as the premier Canadian market for Artificial Intelligence talent. Along with Montreal and Vancouver, Toronto accounts for 62% of Canada’s total AI-specialty talent. In 2025, Toronto’s AI talent pool reached 23,936 workers, the fourth largest in North America. This specialization is a key reason why Toronto has been able to maintain high job creation rates even as other tech hubs slowed hiring; organizations in Toronto have aggressively realigned their workforces to pursue AI initiatives, leading to a 50% year-over-year growth in workers with AI skills as of mid-2025.

Institutional Catalysts: The MaRS-DMZ-CDL Triad

A defining feature of the Toronto ecosystem is its sophisticated network of incubators and accelerators, which have evolved beyond providing office space to becoming critical engines of commercialization and mentorship.

The MaRS Discovery District: The Urban Innovation Anchor

MaRS is one of the world's largest urban innovation hubs, serving as the "gravitational center" of the tech scene. It operates as a bridge between science, technology, and entrepreneurship, focusing on high-impact sectors like health, cleantech, and fintech. Unlike traditional accelerators that use fixed cohorts, MaRS provides ongoing advisory services and connections to capital for scale-ups. Its impact is measurable through success stories such as RetiSpec, which utilized MaRS to raise awareness for its medical devices, and Effenco, which secured contracts with the City of Toronto through MaRS’s network.

The DMZ: World-Class University Incubation

Ranked as the #1 university-based tech incubator in the world, the DMZ (affiliated with Toronto Metropolitan University) has become the "crown jewel" of the ecosystem. It focuses on startups that have already achieved a Minimum Viable Product (MVP) and early traction.

DMZ Success and Impact Metrics (2025) | Cumulative Total |

Startups Supported | 2,600+ |

Capital Raised by DMZ Startups | $3.1 Billion+ |

Jobs Created | 25,000+ |

Global Program Presence | 15+ Countries |

Notable Alumni | Ada, Borrowell, Chexy |

The DMZ offers specialized programming such as the Black Innovation Program, which provides $10,000 grants and dedicated mentorship, and the Siakam EdTech Engine, a 12-week accelerator designed to transform educational technology. Its "Camel mindset" curriculum emphasizes that resilience is more valuable than rapid, unsustainable growth in the current macroeconomic climate.

Creative Destruction Lab (CDL): The Market for Judgment

Located at the Rotman School of Management at the University of Toronto, CDL is unique for its "objectives-based mentoring" process. It targets seed-stage, science-based companies, aiming to address the failure in the "market for judgment" that often prevents academic inventions from reaching commercial success. CDL takes no equity and provides no direct funding; instead, it provides access to elite mentors and angel investors. Since its founding, CDL ventures have generated over $51 billion in equity value. In 2025, CDL expanded its specialized streams to include AI, quantum, blockchain, and a new "Defence" stream for dual-use technologies.

Venture Capital and the Financing of Growth

Toronto captures approximately 40% of all Canadian venture capital deployment, making it the primary theater for financial activity in the country. In 2024, the Canadian venture capital industry secured $8.89 billion across 739 deals. While this represented a healthy historical figure, 2025 has seen a shift toward "disciplined" investment cycles, characterized by fewer but higher-value deals.

Investment Trends and Sector Distribution (2024-2025)

By Q3 2025, venture investment reached $1.8 billion across 123 deals, with the year-to-date total hitting $4.9 billion. The average deal size climbed to $14.7 million, a 20% increase quarter-over-quarter, reflecting investor selectivity for companies with strong fundamentals.

Venture Capital Sector Breakdown (YTD 2025) | Investment Amount | % of Total |

ICT (Information & Communication Tech) | $2.7 Billion | 55% |

Life Sciences | $1.07 Billion | 22% |

Agribusiness | $175 Million | 3.5% |

Cleantech | Trending higher | N/A |

Ontario led all provinces by total investment value at approximately $2.6 billion year-to-date in 2025. However, a concerning trend persists: the dependence on foreign capital. United States investors alone contributed 53% of all Canadian VC funding in 2024, totaling $4.69 billion. While Asian investment from South Korea, China, and Japan is growing—reaching $842 million—the lack of domestic capital recycling remains a vulnerability for Toronto’s long-term independence.

The Rise of Venture Debt

As equity markets have tightened and valuations have adjusted from 2021 peaks, Toronto founders have increasingly turned to venture debt to extend their runway without diluting ownership. In Q1 2025, Ontario led the country with nine venture debt deals worth $182 million, the highest Q1 dollar value recorded since tracking began. This indicates a maturing founder class that is sophisticated in its use of non-dilutive financing to navigate complex market conditions.

The "Hyperscaler" Influence: Big Tech’s Strategic Entrenchment

The presence of Amazon, Microsoft, and Google in Toronto has moved beyond simple regional offices to become a fundamental part of the ecosystem’s R&D infrastructure. These "hyperscalers" provide the compute power and AI platforms that local startups require to scale, but they also extract significant value from the ecosystem.

Microsoft’s $19 Billion Commitment

Microsoft’s commitment to Canada includes a total of $19 billion CAD between 2023 and 2027. In Toronto, this has manifested in a 132,000 square foot headquarters at 81 Bay Street, featuring a Data Innovation Centre of Excellence (DICE). Microsoft’s partner ecosystem in Canada generates between $33 billion and $41 billion in annual revenue and supports nearly 426,000 jobs. This massive footprint acts as a "stabilizer" for the tech economy, providing a secondary market for startup talent and services.

Amazon’s Urban Tech Hubs and Applied AI

Amazon occupies approximately 500,000 square feet of space across three Toronto offices, employing 3,500 people. By late 2024, Amazon expanded its YYZ18 office at 18 York Street by an additional 79,000 square feet. These hubs focus on deep learning, machine learning, and natural language processing. Notably, Amazon has used its Toronto offices to pilot its "Just Walk Out" technology, which leverages computer vision and sensor fusion—technologies that are also being developed by local startups in the retail-tech space.

Google’s Consolidation at 65 King East

Google is in the process of tripling its Canadian workforce, with a major consolidation occurring at its new Toronto headquarters at 65 King East. The 400,000 square foot building is 100% leased to Google, representing a significant long-term commitment to the downtown core. Google’s research teams in Toronto focus on novel neural network architectures and learning algorithms with applications in computer vision and medical image analysis.

The Extraction of Equity through Infrastructure

An emerging critique of the hyperscaler model suggests that Big Tech companies are systematically extracting equity from the startup ecosystem. By "investing" capital into AI startups, which is then immediately paid back to the giant for cloud infrastructure fees (AWS, Azure, or GCP), these companies gain significant equity stakes while recovering their initial capital. Estimates suggest that Amazon, Microsoft, and Google collectively own 34-45% of many major AI companies through this "circular financing" model. For Toronto, which has the densest cluster of AI startups in the world, this means a significant portion of future "Canadian" innovation value may already be owned by American tech giants.

Public Policy: Tax Incentives and Immigration Pathways

Canada’s competitive advantage over the United States is often cited as its proactive government support for the innovation economy, particularly through the Scientific Research and Experimental Development (SR&ED) program and aggressive immigration policies.

SR&ED Modernization (2025)

The SR&ED program is the primary mechanism for lowering the cost of R&D in Canada. Under the 2025 Federal Budget, several major enhancements were proposed to increase the liquidity of startups.

Proposed SR&ED Enhancements (2025) | Detail |

Expenditure Limit (35% Credit) | Increased to $6 Million |

Max Refundable Credit (CCPCs) | $2.1 Million (up from $1.575M) |

Capital Expenditure Eligibility | Reinstated for machinery and equipment |

Pre-Claim Approval Process | Technical approval within 90 days |

AI Integration | AI-driven risk assessment for faster processing |

These changes are particularly beneficial for capital-intensive startups in deep tech, hardware, and clean technology, as they can now claim credits on specialized testing and prototyping equipment that was previously excluded.

The Global Skills Strategy (GSS) and Startup Visa (SUV)

Toronto’s ability to attract global talent is facilitated by the Global Skills Strategy, which offers two-week work permit processing for high-skilled professionals. This is a critical differentiator for Toronto companies competing with U.S. firms that face lengthy H-1B processing times.

The Start-up Visa Program has also been modified to address lengthy wait times. In 2024-2025, the government introduced a three-year "open work permit" for SUV applicants, allowing founders to work for other employers while their startups are in early-stage development. This reduces the financial pressure on international entrepreneurs and makes Toronto a more appealing destination for immigrant founders who may not be able to draw a full salary immediately.

Regional Competition: The Strategic Positioning of Toronto

Toronto’s growth must be understood in the context of other Canadian hubs like Montreal, Vancouver, and Calgary, each of which has developed a distinct value proposition.

Montreal: The AI and Gaming Specialist

Montreal is Toronto’s primary domestic competitor, particularly in the AI and gaming sectors. Montreal captured 24% of Canadian AI/ML funding in 2024 and is home to Mila, the world-renowned AI research lab. Montreal’s primary advantage is cost; mid-2025 data shows that rent for a one-bedroom apartment in Montreal (~$1,688) is nearly 20% lower than in Toronto (~$2,078). For digital nomads and early-stage founders, Montreal offers a "lifestyle-first" strategic choice, whereas Toronto is viewed as "career-first" due to its higher salaries and density of corporate clients.

Calgary: The Fastest-Growing Challenger

Calgary has emerged as North America’s fastest-growing tech hub, with a 78% increase in tech talent over five years. It offers the lowest corporate tax rate in Canada (8%) and a significantly lower cost of living than Toronto or Vancouver. However, Calgary faces a "missing returns cycle" due to a lack of major exits compared to the Toronto-Waterloo corridor, which boasts over 10 unicorns to Calgary’s two.

Vancouver: The West Coast Gateway

Vancouver remains a top-tier North American ecosystem (#15 globally) with strengths in SaaS and cybersecurity. However, it is the most expensive city in Canada for housing, with average rents for 1BR apartments reaching $2,223. Vancouver’s ecosystem is highly integrated with the U.S. West Coast, but it lacks the B2B scale and financial core that defines Toronto.

2025 Rental Market Comparison | Montreal | Toronto | Vancouver |

Avg 1BR Rent | $1,688 | $2,078 | $2,223 |

Monthly Transit Pass | $97 | $156 | $105-$140 |

Cost of Living Index | 45.8 | 54.7 | 57.3 |

Reference: New York City = 100

Structural Vulnerabilities: The Retention Crisis and Brain Drain

Despite its momentum, Toronto’s status as a startup capital is threatened by a persistent retention crisis. A major 2025 study, The Leaky Bucket, reveals that highly skilled immigrants are leaving Canada at the fastest rates in decades.

The "Leaky Bucket" Report Findings

Approximately one in five immigrants leave Canada within 25 years, with departure rates peaking in the first five years. Highly educated immigrants leave at twice the rate of lower-skilled workers, and critical high-growth sectors—engineering, ICT, and research—show the weakest retention.

Immigrant Retention and Salary Gaps (2025) | Metric |

Departure Rate (Highly Educated) | 2x lower-skilled rate |

Earnings Gap (Canada vs. US) | 16% lower for immigrants in CAN |

Underemployment Rate (Immigrants) | 26.7% in low-skill jobs |

Master's Degree Pay (Immigrant) | $57,200 (vs. $84,400 native) |

Doctorate Pay (Immigrant) | $84,000 (vs. $100,000 native) |

The primary driver of this brain drain is the lack of income mobility and career growth. In the U.S., high-skilled immigrants earn 1.2% more than their native-born peers, whereas in Canada, they earn 16% less on average. This pay gap, combined with the rising cost of living in Toronto, makes the city a "stepping stone" rather than a final destination for global talent.

Underemployment and Productivity

A secondary issue is the "productivity gap" between the U.S. and Canada. The top 10 percent of income earners in the U.S. account for three-quarters of the GDP-per-adult gap and two-thirds of the productivity gap. This is largely because the U.S. is more successful at growing startups into medium and large-sized companies, whereas Canada has historically struggled to scale its ventures to a global level. While the Toronto-Waterloo Corridor is an exception, the national trend of a "lack of world-class tech companies" limits the ceiling for high-level talent in Toronto.

Sector Focus: High-Potential Verticals in Toronto

Toronto's startup identity is increasingly defined by several specialized high-tech industries that are attracting outsized portions of venture capital.

Artificial Intelligence and Big Data

Toronto’s AI cluster is not just about foundational research; it is increasingly focused on applied industrial solutions. Startups like Cohere (AI), Waabi (Self-driving), and Tenstorrent (AI hardware) are at the forefront of this movement. The Vector Institute acts as a central hub for academic-industry collaboration, ensuring that the results of U of T’s research are channeled into commercial ventures. The city hosts more AI startups per capita than any other global hub, with 273 firms in the GTA alone.

Fintech and Financial Services

Fintech remains a core pillar of Toronto, leveraging the city's status as North America’s #3 financial hub. Startups in this space focus on payments infrastructure, lending, and blockchain. Major success stories like Wealthsimple (Series E, $393M) and Clearco (Series C, $215M) have paved the way for a second generation of fintechs like chexy and Borderless AI.

Life Sciences and Healthtech

The health and life sciences sector in Toronto is growing rapidly, with over $1.07 billion invested year-to-date in 2025. This sector benefits from proximity to the "Discovery District," a concentrated area of research hospitals and universities. High-profile startups such as Deep Genomics ($180M Series C) and BenchSci ($83M) are utilizing machine learning to accelerate drug discovery and genetic therapies.

Future Outlook: Challenges and Opportunities for 2026 and Beyond

As Toronto looks toward 2026, the ecosystem faces a series of strategic pivot points. The 30.6% growth rate recorded in 2025 is a strong indicator of vitality, but the long-term sustainability of the ecosystem will depend on its ability to recycle capital and retain talent.

The "Hyperscaler" influence remains a double-edged sword. While Amazon, Microsoft, and Google provide the necessary infrastructure for AI growth, their extraction of equity from local startups could lead to a future where Toronto’s most successful companies are effectively subsidiaries of Silicon Valley giants. Furthermore, the reliance on U.S. venture capital (53% of all funding) leaves Toronto vulnerable to changes in U.S. tax and trade policy.

The Opportunity in US Policy Friction

Conversely, Toronto may benefit from rising costs and policy friction in the United States. For example, recent U.S. government proposals to add a $100,000 USD fee to H-1B visas could push more high-skilled talent toward Canada’s Global Skills Strategy and Startup Visa pathways. This "backdoor opportunity" could allow Toronto to secure the elite talent it needs to close the productivity gap with its southern neighbor.

The planned expansion of the Toronto-Waterloo Corridor into a fully realized "supercluster" by late 2025 is expected to create 170,000 high-quality jobs and deliver a $50 billion increase in direct equity value. If this potential is realized, Toronto will have successfully transitioned from a regional leader to a permanent fixture in the global top 10 of startup ecosystems.

Conclusion: Toronto’s Maturation as a Global Megahub

The evidence presented through the 2024-2025 data suggests that Toronto is not merely becoming Canada’s startup capital; it has already secured that title and is now competing for global relevance. The unique combination of the Toronto-Waterloo Innovation Corridor, a world-class academic engine, and a favorable regulatory environment for immigration and R&D has created a density of innovation that is unmatched in Canada. However, the "Leaky Bucket" retention crisis and the "Hyperscaler" equity extraction are significant second-order challenges that will define the next phase of the ecosystem’s evolution. Toronto’s ability to foster "Camel" resilience while pursuing "Unicorn" scale will be the deciding factor in its journey toward becoming a world-leading innovation megahub.

By focusing on high-value sectors like AI, fintech, and healthtech, and by leveraging its proximity to the Waterloo research engine, Toronto has built a diversified tech economy that is more resilient to commodity cycles and macroeconomic downturns than other Canadian cities. The 30.6% growth rate and the #3 ranking in tech talent markets confirm that the city is on the right trajectory. For professional observers and investors, Toronto now represents a mature, sophisticated, and high-growth alternative to traditional American hubs, provided the structural challenges of talent retention and domestic capital supply are addressed in the coming years.

Want to calculate the equity for your cofounder?

Nail your cap table before you sign. Whether you're splitting equity with a co-founder or planning your next funding round, our Equity Calculator gives you precision in seconds

Equity calculator →