Why Some Canadian Founders Prefer Building in the US

March 13, 2026 by Harshit Gupta

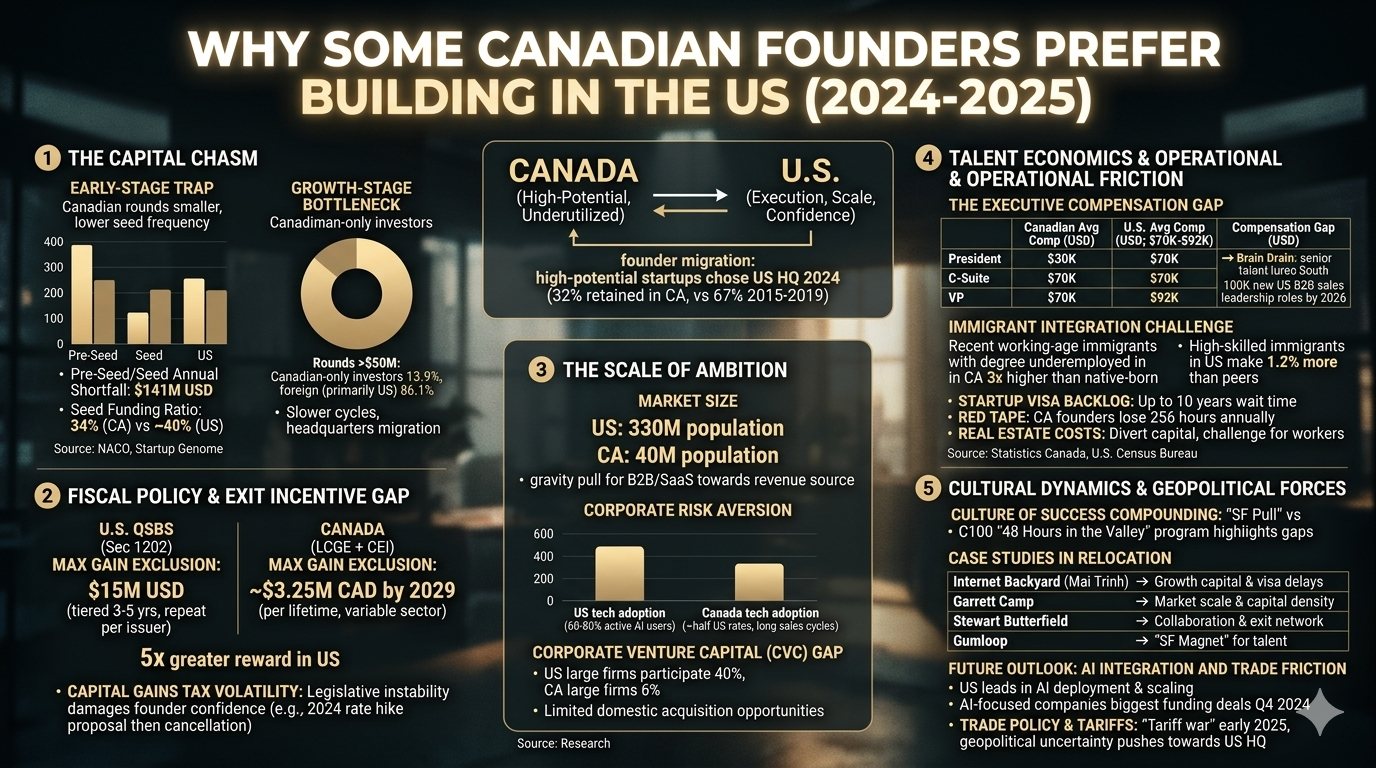

The Canadian technology landscape, long celebrated for its high-caliber talent and resilient economic foundations, has reached a critical juncture in the 2024-2025 period. While the nation boasts one of the most educated workforces globally and a high quality of life, the structural framework supporting the scaling of high-potential startups is under significant strain. A growing consensus among entrepreneurs, venture capitalists, and policy analysts indicates that the gap between Canada and the United States is no longer merely one of market size, but of execution and confidence. Data from late 2024 and early 2025 reveals a staggering decline in the domestic retention of high-potential ventures. Just 32% of Canadian-led high-potential startups launched in 2024 chose to remain headquartered in Canada, a precipitate drop from the 67% retention rate observed between 2015 and 2019. This shift represents a rational, operational response to systemic deficiencies in growth capital, fiscal policy, and regulatory efficiency.

The Capital Chasm: Funding Realities from Seed to Scale

The primary driver for the relocation of Canadian founders to the United States is the pervasive "funding gap" that plagues the domestic ecosystem at every developmental milestone. While early-stage activity remains relatively healthy in terms of startup formation, the ability to capitalize these ventures at a level competitive with U.S. peers is severely limited.

Early-Stage Undercapitalization

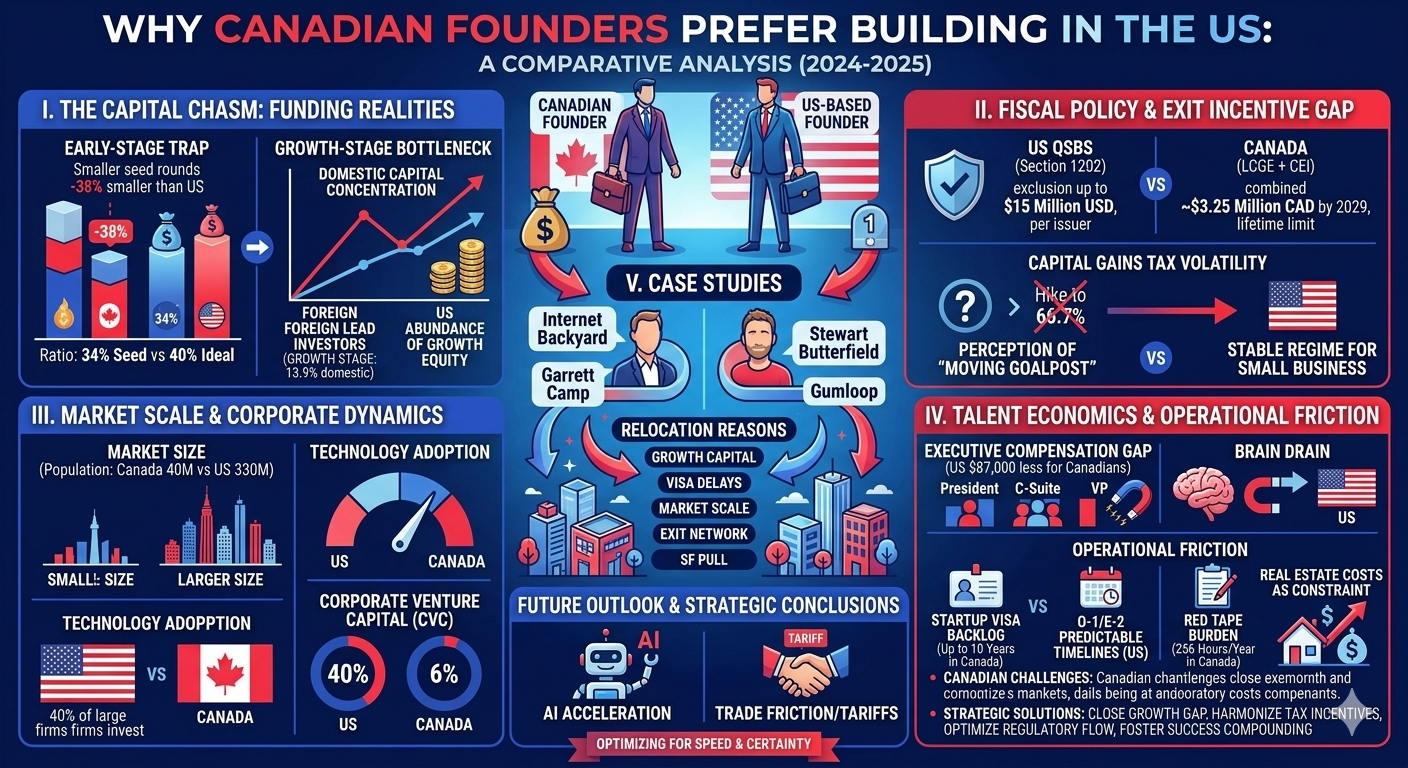

The financial disparity begins at the earliest stages of venture building. Research from the National Angel Capital Association (NACO) and Startup Genome indicates that Canadian startups are fundamentally undercapitalized relative to those in Tier-1 U.S. ecosystems such as New York, Boston, and Los Angeles. This "early-stage trap" is characterized by smaller round sizes and a lower frequency of seed-stage funding relative to the number of companies created. Canadian startups miss out on approximately $141 million USD annually at the pre-seed and seed stages compared to similar ventures in U.S. hubs.

This shortfall is exacerbated by an "off-kilter" ratio between seed and Series A funding. In Canada, only 34% of total early-stage funding is allocated to seed rounds, whereas the ideal figure for a healthy ecosystem—and the average in top U.S. markets—is closer to 40%. Furthermore, Canadian seed rounds are consistently 37% to 40% smaller than those in comparable U.S. cities. The implication of smaller seed rounds is profound; companies are unable to achieve the aggressive milestones required to attract Series A investors, leading to a "sluggish" growth trajectory that is difficult to reverse in later stages.

Funding Metric | Canadian Ecosystem (2024/25) | U.S. Tier-1 Ecosystems | Gap Impact |

Pre-Seed/Seed Annual Shortfall | N/A | $141 Million USD | Slower initial growth |

Series A Annual Shortfall | N/A | $181 Million USD | Reduced scaling velocity |

Seed Funding Ratio | 34% | ~39-40% | Early-stage capital starvation |

Average Seed Round Size | ~38% Smaller | Baseline | Lower runway for validation |

The Growth-Stage Bottleneck

As ventures mature, the domestic capital constraints become even more acute. The venture capital market in Canada is characterized by a high concentration of capital in a small number of large funds, which limits the number of domestic lead investors capable of supporting Series B and later rounds. In 2025, Canadian venture capital firms raised just over $2 billion in new capital—a level well below historical averages—with emerging fund managers capturing a mere $249 million of that total.

This lack of domestic depth at the growth stage forces founders to rely heavily on foreign capital, primarily from the United States. In funding rounds over $50 million, the share of participation by Canadian-only investors falls to a negligible 13.9%, compared to 68% for rounds under $5 million. This structural dependence on foreign capital often results in slower fundraising cycles, less competitive term sheets, and, ultimately, pressure to relocate the corporate headquarters to the investor’s home market. Founders frequently optimize for "speed and certainty" rather than geography, and the U.S. market offers an abundance of growth equity that Canada cannot currently match.

Funding Stage | Domestic Participation Share | Primary Capital Source | Scaling Impact |

Seed & Pre-Seed (<$5M) | ~68% | Canadian Angel/Early VC | Strong early start |

Series A | Declining | Mixed Domestic/Foreign | The "Scaling Trap" |

Growth Stage (>$50M) | 13.9% | U.S. Venture/PE Funds | Headquarters migration |

Fiscal Policy and the Exit Incentive Gap

Beyond the immediate availability of capital, the fiscal environment in Canada serves as a powerful "push factor" for founders. The taxation of capital gains and the structure of incentives for business owners create a stark contrast between the potential net-of-tax proceeds in Canada versus the United States.

The Qualified Small Business Stock (QSBS) Advantage

A cornerstone of the U.S. startup ecosystem is Section 1202 of the Internal Revenue Code, which governs Qualified Small Business Stock (QSBS). This provision allows founders and early investors to exclude up to 100% of federal capital gains taxes on the sale of stock, provided certain criteria are met. Recent legislative changes via the "One Big Beautiful Bill Act" (OBBBA), signed on July 4, 2025, have further enhanced these benefits, raising the exclusion cap from $10 million to $15 million and introducing a tiered holding period starting at just three years.

In contrast, Canada’s primary incentive, the Lifetime Capital Gains Exemption (LCGE), is limited to a cap of approximately $1.25 million as of mid-2024. While the proposed Canadian Entrepreneurs' Incentive (CEI) aims to add another $2 million in partial exemptions by 2029, the combined total of $3.25 million remains nearly five times smaller than the U.S. equivalent. Furthermore, the U.S. QSBS limit applies "per issuer" (per company), allowing serial entrepreneurs to benefit multiple times, whereas the Canadian LCGE is a lifetime limit, effectively penalizing repeat builders.

Tax Incentive Feature | U.S. QSBS (Sec 1202) | Canada (LCGE + CEI) | Implications |

Maximum Gain Exclusion | $15 Million USD | ~$3.25 Million CAD (by 2029) | 5x greater reward in U.S. |

Frequency of Claim | Per Issuer (Repeatable) | Per Lifetime | U.S. favors serial founders |

Exclusion Percentage | Up to 100% | 33.3% to 100% (tiered) | U.S. has higher tax shield |

Holding Requirement | 3 to 5 Years (Tiered) | Variable / Sector Restricted | U.S. is more flexible |

Capital Gains Tax Volatility and Uncertainty

The 2024 Canadian federal budget introduced significant uncertainty regarding the capital gains inclusion rate. Initially, the government proposed increasing the inclusion rate from 50% to 66.7% for gains over $250,000, effective June 25, 2024. Although this hike was eventually canceled or postponed until at least 2026 by a subsequent administration, the period of legislative instability severely damaged founder confidence. Founders noted that waiting an extra year to grow the business by 16% would only result in breaking even if the tax rate increased by the same amount, essentially nullifying a year of operational risk. This perception of a "moving goalpost" in tax policy encourages founders to move to the U.S., where the tax regime for small businesses is viewed as more stable and established.

The Scale of Ambition: Market Size and Corporate Dynamics

The decision to build in the U.S. is also driven by the fundamental reality of market scale. Canada’s population of roughly 40 million cannot compete with the U.S. market of 330 million, particularly for B2B and SaaS companies seeking to reach "unicorn" status.

Corporate Risk Aversion and Sales Cycles

Canadian enterprises are frequently characterized as risk-averse, with longer sales cycles and a slower adoption of new technologies compared to U.S. firms. Research indicates that technology adoption in Canada is roughly half that of the U.S., particularly in areas like AI integration, where 60-80% of U.S. companies are now active users compared to much lower rates in Canada. For a startup, having its first major customers located in the U.S. often leads to a natural "gravity pull" for the entire operation to move closer to its revenue source.

The Corporate Venture Capital (CVC) Gap

A critical component of a healthy ecosystem is the participation of established corporations in the venture asset class. In the U.S., 40% of large public companies (those with over $1 billion in revenue) participate in direct venture investments, compared to a mere 6% of similar Canadian firms. This lack of corporate engagement in Canada limits the availability of strategic partnerships, mentorship, and domestic acquisition opportunities. Consequently, Canadian startups often look to U.S. tech giants like Google or Meta for exits, which further reinforces the necessity of being physically present in the U.S. market.

Talent Economics: The Paradox of Education and Reward

Canada possesses one of the world's most educated workforces, yet it struggles to capitalize on this advantage due to a significant gap in compensation and senior leadership opportunity.

The Executive Compensation Gap

Canadian tech executives earn substantially less than their American peers. On average, total compensation for a Canadian tech executive is US$87,000 less than the comparable figure in the U.S.. This gap exists regardless of the startup’s funding stage, sector, or amount of capital raised. The disparity is most acute at the senior-most levels, where the average Canadian C-suite executive or Vice President is paid between $85,000 and $92,000 less than their American counterpart.

Executive Level | Canadian Avg Comp (USD) | U.S. Avg Comp (USD) | Compensation Gap (USD) |

President | $205,000 | $275,000 | $70,000 |

C-Suite Executive | $182,000 | $267,000 | $85,000 |

Vice President | $165,000 | $257,000 | $92,000 |

This compensation gap leads to a persistent "brain drain" of senior talent. Experienced leaders who have "scaled the mountain" before are essential for guiding young companies, yet they are often lured south by the "heavyweight" salaries and stock options available in the U.S.. By 2026, the U.S. is expected to open 100,000 new B2B sales leadership roles alone, with median total compensation for experienced leaders ranging from $95,000 to $130,000, and top performers clearing $180,000 plus.

The Immigrant Integration Challenge

Canada’s success in attracting global talent through its immigration-friendly policies is often undermined by labor market misalignment. Highly educated immigrants in Canada earn 16% less on average than native-born Canadians and face significantly higher rates of underemployment. In 2021, 26.7% of recent working-age immigrants with a bachelor’s degree or higher were working in jobs requiring only a high school diploma—a rate three times higher than that of native-born workers.

In contrast, high-skilled immigrants in the U.S. make 1.2% more than their American-born peers and enjoy an 8% higher employment rate. This makes the U.S. a more attractive destination for "top-tier" immigrants from the higher end of the global skill distribution. For foreign-born founders, the U.S. represents a market that more effectively rewards the "superpower" of immigrant grit and entrepreneurship.

Operational Friction: Visas, Red Tape, and Real Estate

Founders are increasingly prioritizing "operational certainty," and in many respects, Canada’s regulatory and physical environment has become a source of significant friction.

The Startup Visa and Immigration Backlog

While Canada’s Start-up Visa program was designed to attract global builders, the reality of its implementation has been plagued by delays. Some founders report wait times for the program reaching up to 10 years, making it functionally unusable for rapid-growth companies. In comparison, the U.S. offers established pathways such as the O-1 and E-2 visas, which, while subject to intense scrutiny, offer more predictable timelines for founders who can prove their business’s viability and capitalization.

The Burden of Red Tape

Administrative friction remains a significant drain on productivity. Canadian founders lose over 256 hours annually—more than six full work weeks—to "red tape" and regulatory compliance. This is particularly damaging for early-stage companies where the founder's time is the most valuable resource. When compared to the relatively streamlined "founder-first" infrastructure in hubs like Silicon Valley, Canada’s regulatory environment is viewed as a hurdle rather than a support system.

Real Estate Costs as a Growth Constraint

An under-discussed risk to the Canadian startup ecosystem is the rising cost of residential and commercial real estate. Housing affordability has become a primary challenge for tech workers in Toronto and Vancouver, effectively increasing the "cost of living" salary floor that startups must pay to attract talent. In 2024, studies suggested that "Canada's real estate addiction" acts as a major hurdle, diverting capital away from productive innovation and making it harder for domestic startups to recover post-pandemic. Founders find that they can build savings and achieve financial security faster in the U.S., even in high-cost cities, due to the significantly higher earning potential.

Cultural Dynamics: Compounding Success vs. Isolated Islands

A critical factor in the dominance of the U.S. tech ecosystem, particularly Silicon Valley, is the culture of "success compounding." In the U.S., alumni of successful startups are significantly more likely to fund or found their own companies, creating a perpetual engine of growth.

The "Pay It Forward" Mentality

Silicon Valley is characterized by a "forgiving attitude" toward failure and a deep network of mentors who have successfully scaled companies into global category leaders. Canada, despite its talent, struggles to replicate this model. Success stories in Canada often feel like "islands" rather than ecosystem champions. For instance, while matrox and BlackBerry were pioneers, they did not spawn the same level of secondary ecosystem development seen after the success of companies like Google or Meta.

Programs like the C100 have attempted to bridge this gap by providing high-potential Canadian founders with "48 hours in the Valley," offering exposure to the risk-embracing mindset and mentorship of top global innovators. However, the very existence of such programs highlights the "SF Pull"—the sense that true global scaling can only be learned or achieved by tapping into the American market's dense networks of capital and expertise.

Case Studies in Relocation

The case of "Internet Backyard," a fintech startup valued at $35 million, serves as a prominent example of the trend. Despite reaching product-market fit and achieving a significant valuation in Canada, the founders chose to move to the U.S. in early 2026, citing access to growth capital and visa limitations as the primary drivers. The founders noted that the infrastructure for quickly launching and scaling a fintech company was simply more robust south of the border. Similarly, legendary Canadian-born founders like Garrett Camp (Uber) and Stewart Butterfield (Slack, Flickr) found that the "gravity" of the U.S. market and its "Ingenuity" culture were essential for transforming their ideas into global platforms.

Founder/Company | Origins | Industry | Relocation Reason |

Internet Backyard (Mai Trinh) | Vancouver/Simon Fraser | Fintech | Growth capital & visa delays |

Garrett Camp | Calgary | Tech/Transpo | Market scale & capital density |

Stewart Butterfield | British Columbia | Tech/Comm | Collaboration & exit network |

Gumloop | Vancouver | Workflow/AI | "SF Magnet" for talent |

Future Outlook: AI Integration and Trade Friction

As the tech sector moves into 2026, two primary forces are shaping the future of the Canada-U.S. divide: the acceleration of AI and the emergence of trade protectionism.

The AI Advantage

While Canada outpaced the U.S. in tech talent growth in 2024 (5.9% Gain vs 1.1%), much of this was driven by a strong pool of AI researchers in Toronto, Montreal, and Waterloo. However, the U.S. leads in the actual deployment and scaling of AI technologies. AI-focused companies accounted for the five largest funding deals in Q4 2024, led by Databricks’ $10 billion raise and OpenAI’s $6.6 billion round. Canadian leaders expect that 30% of their full-time equivalent capacity will come from the "digital workforce" (AI agents, bots) by 2027, but the capital required to build these "AI-native" challengers is currently concentrating in the U.S..

Trade Policy and Tariffs

The emergence of a "tariff war" between the U.S. and Canada in early 2025 has introduced a new layer of complexity. With 75% of Canadian exports going to the U.S., the downstream consequences of tariffs extend beyond physical goods to the digital services and supply chains that support them. Shopify CEO Tobi Lütke has emphasized that Canada "thrives when it works with America together" and criticized retaliatory measures that could lead to economic decline. For founders, this geopolitical uncertainty adds another reason to consider a U.S. headquarters: it provides a hedge against potential protectionist policies that might target cross-border digital services.

Strategic Conclusions

The preference among Canadian founders for building in the United States is a rational response to a cumulative set of structural disadvantages in the domestic market. The "Brain Drain" is not a failure of Canadian ingenuity but a failure of the Canadian "railway system" to support the transition from early-stage success to long-term scale.

To address these challenges, the analysis suggests that Canada must:

Close the Growth Capital Gap: Incentivize domestic pension funds and corporations to participate in Series B and growth-stage rounds to reduce the 13.9% domestic participation rate in mega-deals.

Harmonize Tax Incentives: Implement a "per-business" capital gains incentive competitive with the U.S. QSBS $15 million cap to encourage repeat founders and senior talent retention.

Optimize Immigration and Regulatory Flow: Reduce the Startup Visa wait times from 10 years to a matter of months and decrease the 256 hours of annual red tape that stifles founder productivity.

Foster Success Compounding: Encourage a shift in corporate culture toward active CVC investment and acquisition of domestic startups to ensure capital and talent are recycled within the Canadian ecosystem.

Ultimately, the choice to move to the U.S. remains an optimization for speed and certainty. Until the Canadian ecosystem can offer a similar level of "scaling velocity" and "fiscal reward" for the highest-potential ventures, the pull of the U.S. market will remain an insurmountable competitive force for Canada's most ambitious builders.

Read More -

1. From Idea to MVP: A Step-by-Step Guide for Solo Founder

🔗 https://findnstart.com/blogs/from-idea-to-mvp-a-step-by-step-guide-for-solo-founder

2. How to Validate Your Startup Idea in 48 Hours for $0

🔗 https://findnstart.com/blogs/how-to-validate-your-startup-idea-in-48-hours-for-0

3. Remote vs. Local: Does Your Co-Founder Need to Live in the Same City?

🔗 https://findnstart.com/blogs/remote-vs-local-does-your-co-founder-need-to-live-in-the-same-city

4. The 2026 Startup Landscape: What Has Fundamentally Changed (and Why Founder Skills Matter More Than Ever)

5. The Most In-Demand Skills for Startup Founders in 2026

🔗 https://findnstart.com/blogs/the-most-in-demand-skills-for-startup-founders-in-2026

6. How to Find a Technical Co-Founder (Without a Six-Figure Salary)

🔗 https://findnstart.com/blogs/how-to-find-a-technical-co-founder-without-a-six-figure-salary

7. 5 Red Flags to Look for When Choosing a Startup Partner

🔗 https://findnstart.com/blogs/5-red-flags-to-look-for-when-choosing-a-startup-partner

8. How to Pitch Your Idea to Potential Co-Founders

🔗 https://findnstart.com/blogs/how-to-pitch-your-idea-to-potential-co-founders

9. How to Build a Portfolio that Attracts High-Growth Startup Founders

🔗 https://findnstart.com/blogs/how-to-build-a-portfolio-that-attracts-high-growth-startup-founders

10. Equity vs. Salary: How to Split Ownership with Your First Teammate

🔗 https://findnstart.com/blogs/equity-vs-salary-how-to-split-ownership-with-your-first-teammate

11. Why Joining an Early-Stage Startup is Better Than a Corporate Job

🔗 https://findnstart.com/blogs/why-joining-an-early-stage-startup-is-better-than-a-corporate-job

12. The Future of EdTech: Why Developers and Educators Need to Team Up Now

🔗 https://findnstart.com/blogs/the-future-of-edtech-why-developers-and-educators-need-to-team-up-now

13. The Architecture of Symbiosis: Analytical Perspectives on the Five Habits of Successful Startup Duos

14. Finding a Co-Founder in the AI Space: What Skills Should You Look For?

🔗 https://findnstart.com/blogs/finding-a-co-founder-in-the-ai-space-what-skills-should-you-look-for

15. Overcoming Analysis Paralysis and the Strategic Path to Execution

🔗 https://findnstart.com/blogs/overcoming-analysis-paralysis-and-the-strategic-path-to-execution

16. From College Project to Company: How to Find Your Student Co-Founder

🔗 https://findnstart.com/blogs/from-college-project-to-company-how-to-find-your-student-co-founder

17. How to Start a Startup While Working a Full-Time Job

🔗 https://findnstart.com/blogs/how-to-start-a-startup-while-working-a-full-time-job

18. How to Build a HealthTech Startup Without a Medical Degree

🔗 https://findnstart.com/blogs/how-to-build-a-healthtech-startup-without-a-medical-degree

19. The Solitary Architect: Executive Isolation in Entrepreneurship

20. The 2026 Guide to Launching a SaaS as a Solo Developer

21. What Sustainable Growth Actually Looks Like

🔗 https://findnstart.com/blogs/what-sustainable-growth-actually-looks-like

22. The Early Warning Signs Your Startup Is in Trouble

🔗 https://findnstart.com/blogs/the-early-warning-signs-your-startup-is-in-trouble

23. How to Grow Without Burning Out

🔗 https://findnstart.com/blogs/how-to-grow-without-burning-out

24. The Truth About “Runway” Most Founders Ignore

🔗 https://findnstart.com/blogs/the-truth-about-runway-most-founders-ignore

25. Revenue Solves More Problems Than Funding

🔗 https://findnstart.com/blogs/revenue-solves-more-problems-than-funding

26. What No One Tells You About Being a Solo Founder

🔗 https://findnstart.com/blogs/what-no-one-tells-you-about-being-a-solo-founder

27. Why Smart People Quit High-Paying Jobs to Build Startups (And Why Most Regret It)

28. Why Most Startup Advice on Twitter Is Dangerous

🔗 https://findnstart.com/blogs/why-most-startup-advice-on-twitter-is-dangerous

29. Decision Fatigue: The Silent Startup Killer

🔗 https://findnstart.com/blogs/decision-fatigue-the-silent-startup-killer

30. Fear vs Logic: How Founders Actually Make Decisions

🔗 https://findnstart.com/blogs/fear-vs-logic-how-founders-actually-make-decisions

31. How Overthinking Destroys Early Momentum

🔗 https://findnstart.com/blogs/how-overthinking-destroys-early-momentum

32. Ideas Don’t Scale. Systems Do.

🔗 https://findnstart.com/blogs/ideas-dont-scale-systems-do

33. The First Hire That Actually Matters

🔗 https://findnstart.com/blogs/the-first-hire-that-actually-matters

34. How the First 100 Users Decide Your Startup’s Fate

🔗 https://findnstart.com/blogs/how-the-first-100-users-decide-your-startups-fate

35. Why Your Startup Doesn’t Need Growth — It Needs Focus

🔗 https://findnstart.com/blogs/why-your-startup-doesnt-need-growthit-needs-focus

36. Why Most Startups Die Quietly

🔗 https://findnstart.com/blogs/why-most-startups-die-quietly

37. Lessons Learned Too Late by First-Time Founders

🔗 https://findnstart.com/blogs/lessons-learned-too-late-by-first-time-founders

38. The Myth of the “Overnight Success” Startup

🔗 https://findnstart.com/blogs/the-myth-of-the-overnight-success-startup