Why Most Campus Startup Ideas Fail

March 8, 2026 by Harshit Gupta

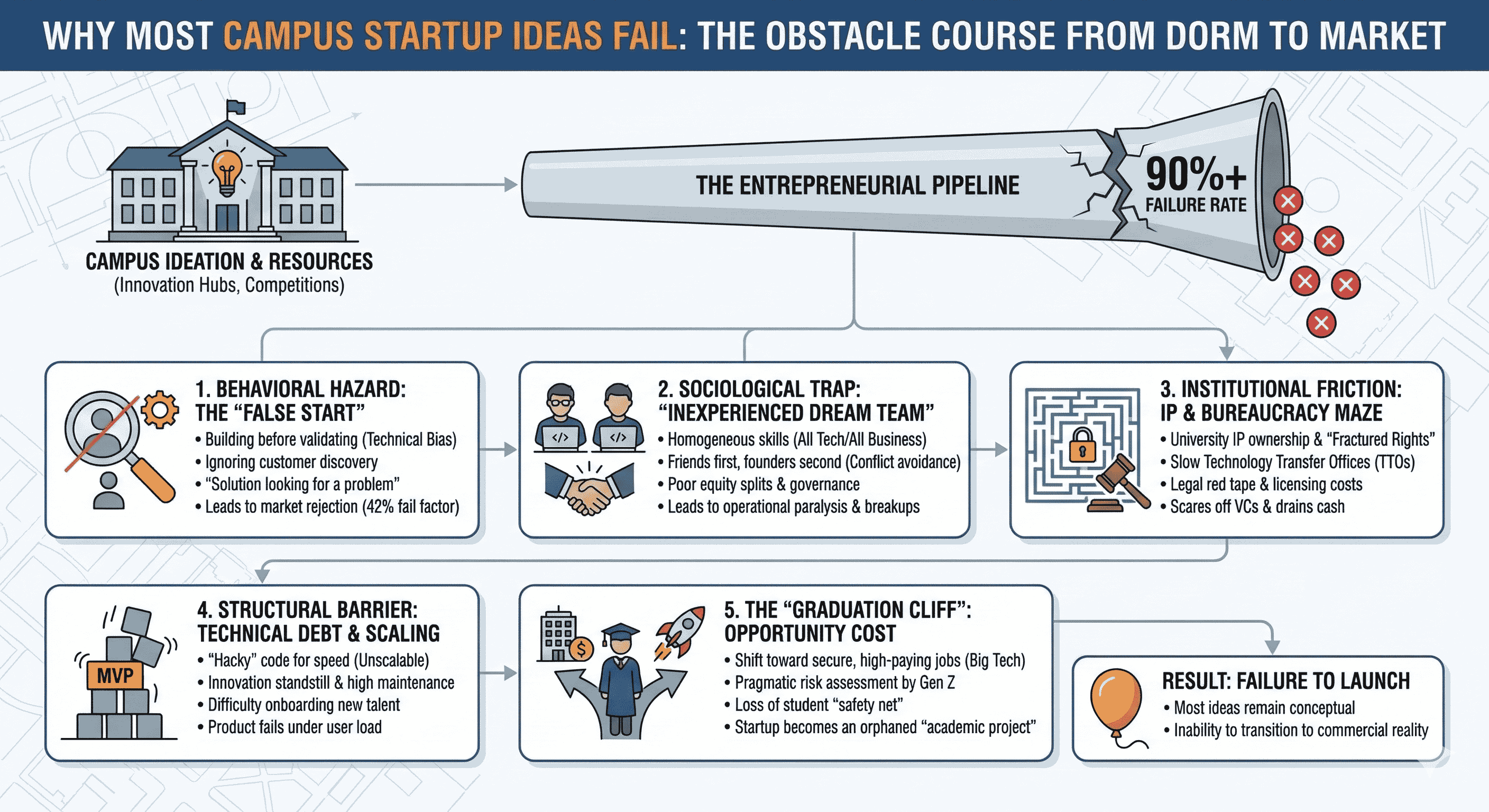

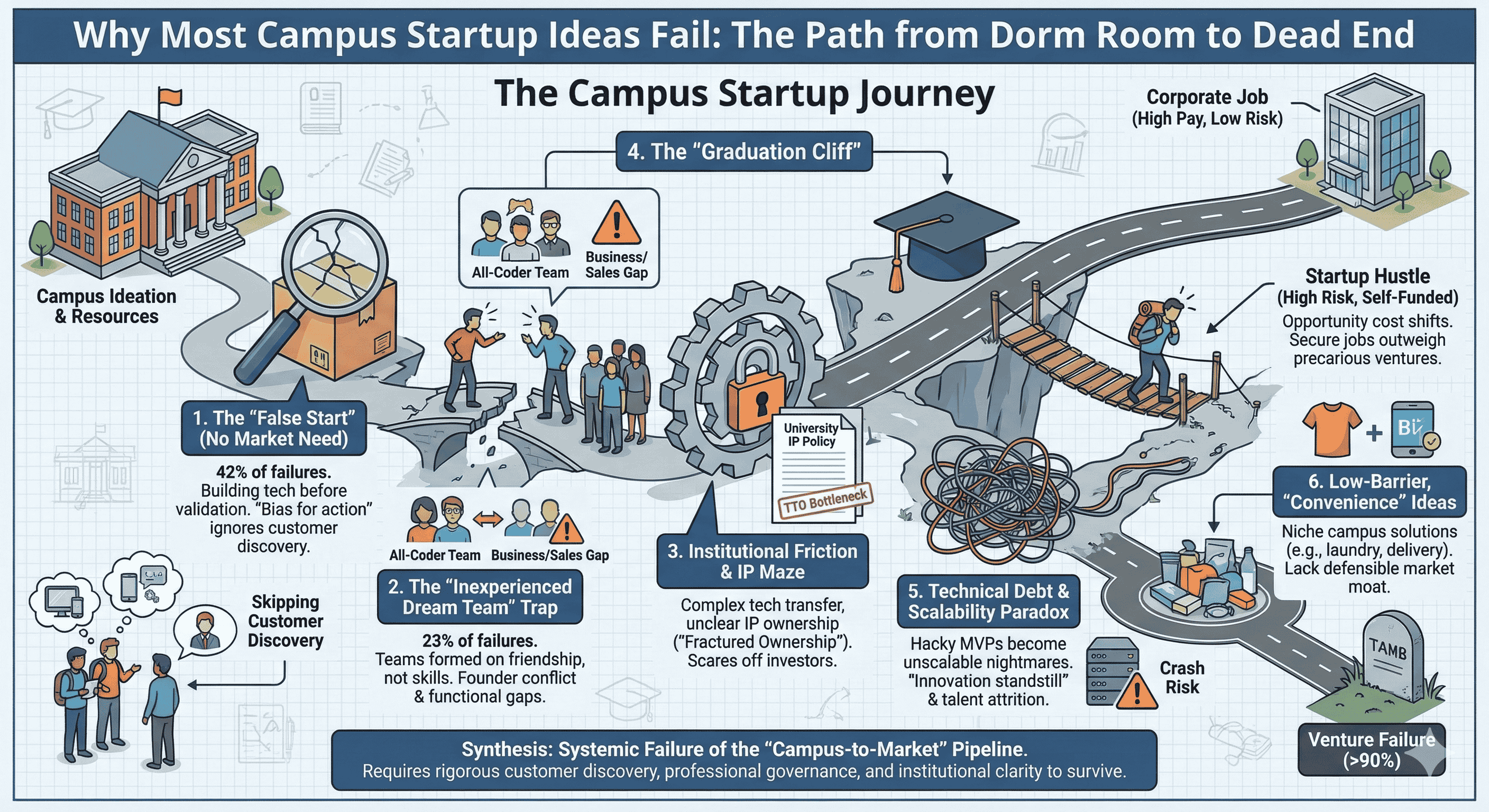

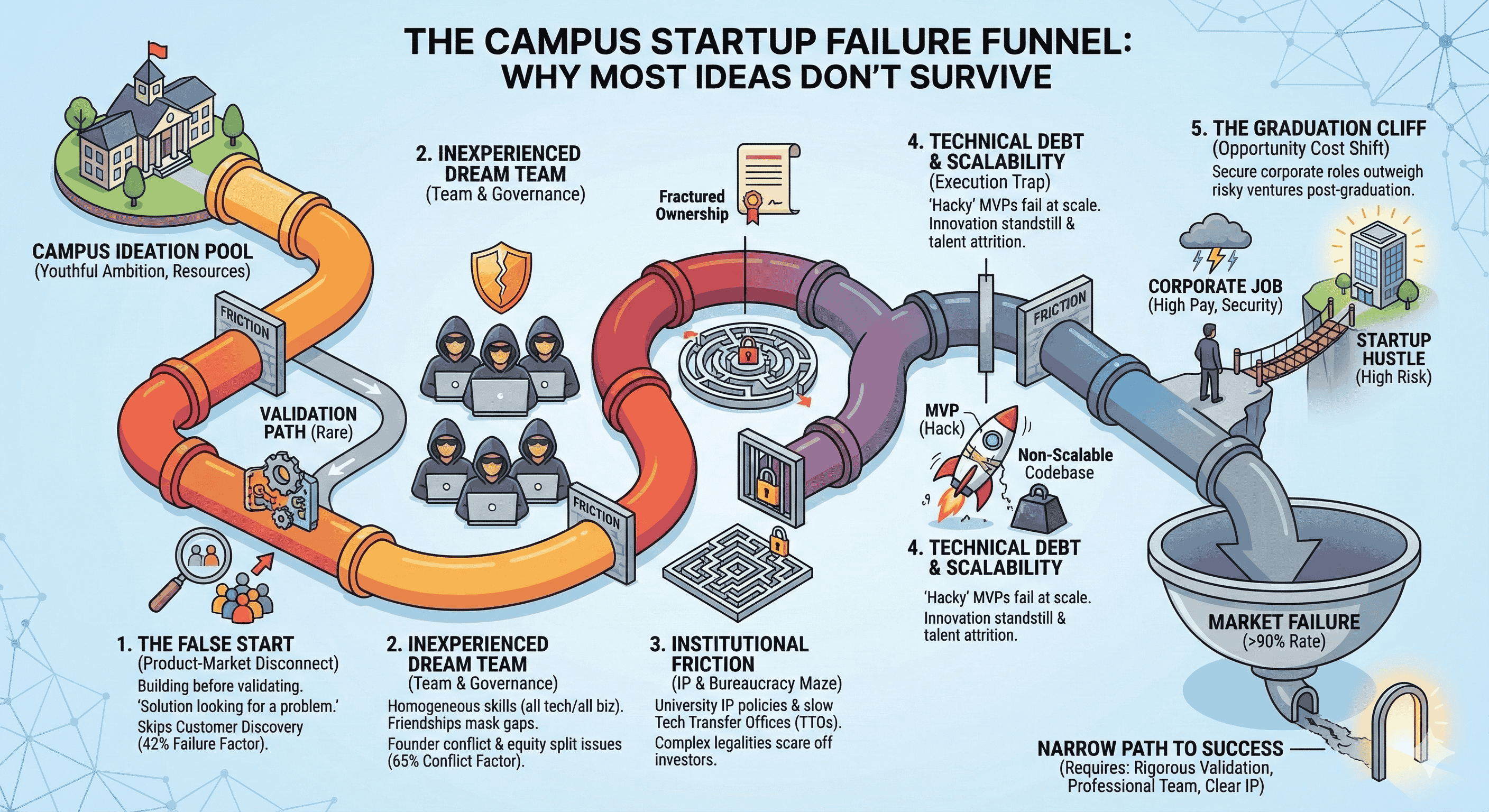

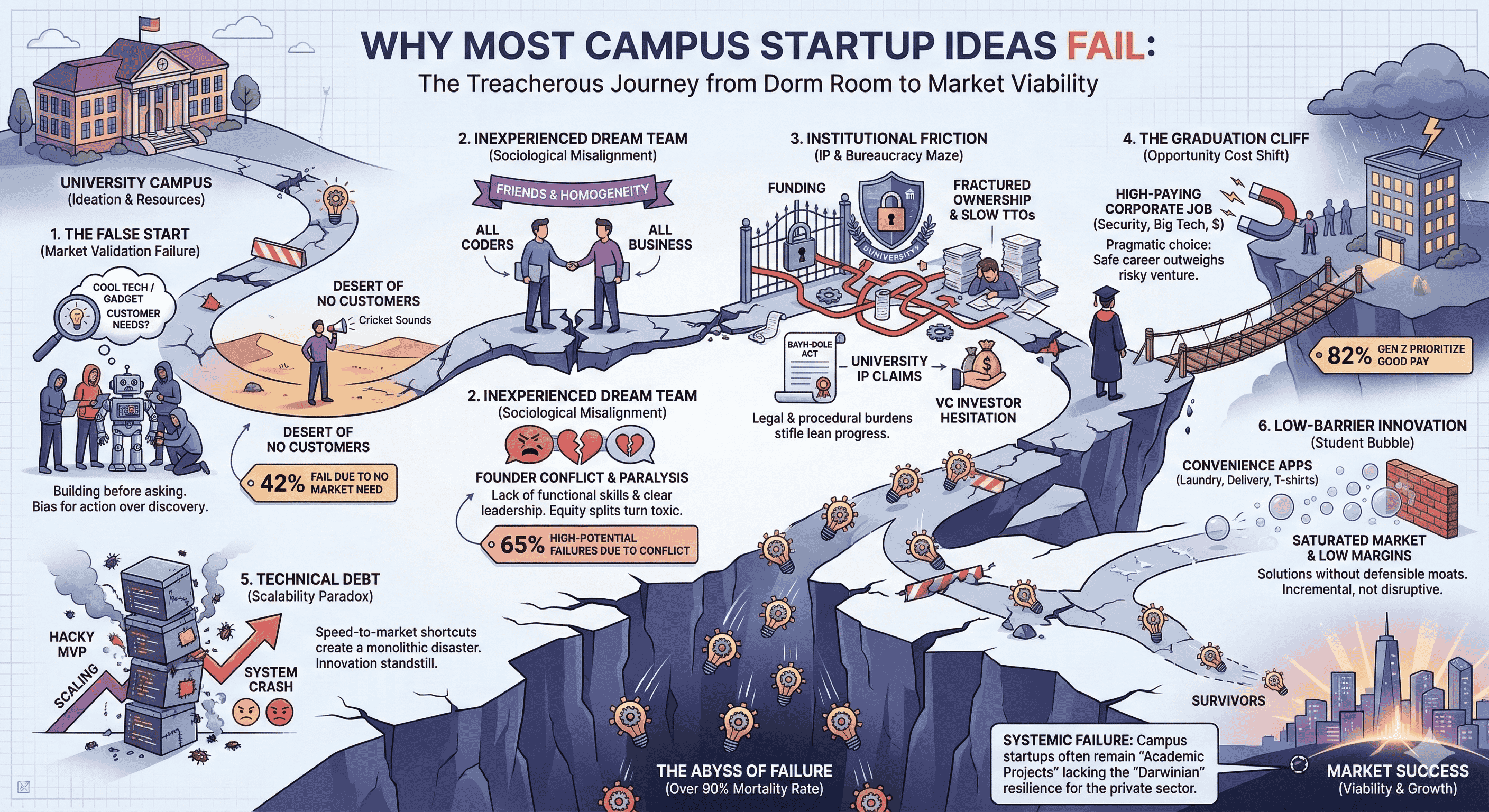

The university campus is frequently characterized in contemporary discourse as a primary engine of innovation and a fertile environment for the development of high-growth technology ventures. This narrative, popularized by the historical success of entities that emerged from institutional dormitories and research labs, posits that the confluence of youthful ambition, academic expertise, and subsidized resources creates a unique incubator for disruptive business models. However, empirical analysis of the entrepreneurial pipeline reveals a starkly divergent reality. The vast majority of campus-born startup ideas do not survive the transition from conceptualization to commercial viability, with failure rates for student-led ventures estimated to exceed 90 percent within the first few years of operation.

The failure of these ventures is rarely the result of a single catastrophic event. Instead, it is the product of an accumulation of structural, behavioral, and institutional frictions that undermine the venture’s foundation before it can achieve product-market fit. While the broader startup ecosystem faces a general failure rate of approximately 90 percent, campus startups are subjected to a specific set of "dorm room hazards," including the "False Start" phenomenon, where technical development precedes customer discovery; the "Inexperienced Dream Team" trap, where homogeneous skill sets lead to operational paralysis; and a "Graduation Cliff," where the opportunity cost of entrepreneurship suddenly shifts in favor of corporate employment.

Statistical Landscapes of University Entrepreneurship and Survival

To understand why most campus startup ideas fail, it is first necessary to examine the survival trajectories and industry distributions within established university ecosystems. Data from the University of Illinois and University of Minnesota systems provide a quantitative baseline for institutional venture formation. In the Illinois university context, approximately 59.4 percent of startups founded over a recent five-year period remain active, while 39.3 percent are categorized as inactive. While a 60 percent survival rate over five years appears more favorable than the general 90 percent mortality figure, this statistic is heavily influenced by the nature of university-sponsored ventures, which are often in highly regulated sectors like biotechnology and healthcare.

Biotech and healthcare-related startups comprise more than one-third of the ventures spun out of Illinois universities, with 21 percent specifically in the biotech industry. These firms often exist in a state of pre-revenue "stasis," supported by university funding, SBIR/STTR grants, or the NSF I-Corps program, which temporarily buffers them from the Darwinian pressures of the private market. However, even within these supported cohorts, the "scaling ceiling" is evident: while two-thirds of active Illinois startups remain in-state, the majority of those that raise more than $5 million eventually relocate, suggesting that the campus environment, while effective for ideation, frequently lacks the infrastructure for long-term sustainment.

The University of Minnesota’s technology commercialization statistics further illustrate the friction between invention and survival. Between FY2020 and FY2025, the university consistently formed 19 to 26 startups annually, yet the number of invention disclosures—the raw material of innovation—fluctuated significantly, peaking at 450 in 2025. The conversion rate from a patented concept to a revenue-generating agreement remains low relative to the total output of research, highlighting the difficulty of translating "technical potential" into "market need".

Survival and Attrition Statistics by Timeframe | Failure Rate (%) | Source |

First Year of Operation | 20% | |

End of Second Year | 30% | |

End of Fifth Year | 50% - 70% | |

End of Tenth Year | 70% | |

Achievement of $1 Billion Valuation | 99% |

The discrepancy between the volume of university startups and their long-term survival is partly explained by the varying nature of the ventures themselves. University ecosystems produce three distinct categories of businesses: student startups, university research-based startups, and community startups. Student startups are typically owned and led by undergraduate or graduate students and are often developed in business school courses. These ventures are frequently based on "low-barrier" ideas—consumer products, apparel, or service-based companies—rather than deep technology. Because these businesses rarely involve university-owned intellectual property, the host institution rarely takes an ownership stake, but this lack of institutional "skin in the game" can also mean the ventures lack the rigorous oversight and capital infusion necessary to survive the post-graduation transition.

Behavioral Archetypes: The Mechanics of the False Start

The primary reason campus startups fail is not a lack of effort or intelligence, but a fundamental misalignment between the development of a solution and the identification of a problem. Analysis conducted at Harvard Business School identified a recurring pattern known as the "False Start," which is disproportionately prevalent among student founders with technical backgrounds. Driven by a "bias for action," these founders often skip the crucial step of customer discovery, moving directly into engineering and product development.

The "False Start" occurs when a team launches a Minimum Viable Product (MVP) to "test the market" without first understanding the underlying customer needs. In the campus context, this often manifests as a group of engineers building a "cool app" or a "new gadget" in isolation. When they eventually launch, they are met with what is described as "the sound of crickets" because no actual market need was ever validated. Approximately 42 percent of all startup failures are attributed to this lack of market demand, making it the single most lethal factor in the venture lifecycle.

The psychological underpinnings of the False Start are rooted in the "lean startup" ideology, which encourages founders to "fail fast" and iterate. However, for a cash-strapped student venture, "failing fast" without a prior foundation of research often results in a "False Positive"—where the founders misinterpret early signals of interest from their peers as a sign of broad market demand. By the time the founders realize the product does not fit the wider market, they have often exhausted their initial capital and, more importantly, the psychological morale of the team.

A secondary behavioral pattern contributing to failure is the inability to transition from an academic problem-solving mindset to an entrepreneurial one. University Startup Entrepreneurs (USEs)—faculty and students—tend to be "communitarian" or "missionary" in their orientation, focusing on societal impact and intellectual stimulation. While these are noble goals, they often come at the expense of "Darwinian" commercial focus. USEs frequently prefer technical roles and shirk managerial, regulatory, and sales tasks, leading to an organizational power imbalance that makes the venture uncompetitive against Corporate Startup Entrepreneurs (CSEs) who possess tacit business knowledge and industry networks.

The Sociology of the "Inexperienced Dream Team"

The composition of the founding team is the second most common predictor of failure, accounting for approximately 23 percent of venture collapses. In the campus environment, founding teams are frequently formed through social convenience and geographic proximity rather than strategic necessity. These "Inexperienced Dream Teams" typically consist of friends from the same academic department, which leads to a critical homogeneity of skills.

When a team is composed entirely of coders or entirely of business students, they encounter a "functional gap" that prevents effective execution. A business requires a well-rounded team capable of navigating marketing, sales, finance, and product development simultaneously. On campus, however, the camaraderie of friendship often masks these deficiencies until the venture faces a crisis. Furthermore, the lack of hierarchy in these teams can lead to debilitating conflict over decision-making, particularly when the venture matures beyond the "project" stage and requires a clear CEO-style leadership.

Founder conflict is cited as the root cause for 65 percent of high-potential startup failures. On campus, this conflict is often delayed by the "academic rhythm"—the venture feels like a shared project for which the stakes are low as long as the founders are still in school. However, as graduation approaches, the "Broken Promise" occurs: co-founders who were equally committed in Year 1 find their interests diverging in Year 2 or 3 as financial pressures mount.

Founder and Team Success Factors vs. Failure Indicators | Impact Factor | Failure Mode |

Homogeneous Skill Sets (All Tech/All Business) | High | Functional Stagnation |

Prior Social Relationship (Friends/Family) | Mixed | Conflict Avoidance |

Solo Founder Status | Neutral/Positive | Slower Velocity (but higher survival) |

Equal Equity Split (50/50) | High | Resentment/Misalignment |

"Jack-of-all-trades" Employees | Medium | Inflexibility in scaling |

The issue of equity distribution further complicates team dynamics. In recent years, "even splits" have become more common; in 2024, 45.9 percent of two-person teams divided equity equally, compared to 31.5 percent in 2015. While an even split appears fair, it rarely reflects the actual long-term contributions of the founders. In a campus startup, one founder may provide $50,000 in seed capital or critical intellectual property in Year 1, while another provides "sweat equity". If the second founder leaves for a corporate job in Year 2, the "dead equity" they retain can prevent the company from raising further capital, effectively killing the venture.

Institutional Friction: The Intellectual Property and Technology Transfer Maze

For ventures that attempt to commercialize university research, the institution itself can become a primary obstacle to success. The transition from a university project to a formal business entity requires navigating a "maze" of institutional procedures, legal paperwork, and multi-layered approvals. This administrative burden is often incompatible with the pace and spirit of a lean startup.

The legal framework governing university inventions was fundamentally altered by the Bayh-Dole Act of 1980, which encourages universities to claim ownership of intellectual property (IP) generated through federal funding. While intended to accelerate commercialization, the Act has led many universities to assert broad ownership rights over all patentable inventions created by faculty, staff, and even students.

Student entrepreneurs are often unaware that their work in a campus lab or as part of a "Senior Design Course" may be legally owned by the university or a corporate sponsor. This "fractured ownership" of IP rights can be a lethal blow to a startup's funding prospects. Venture capitalists are notoriously hesitant to invest in companies that do not have clear, unencumbered title to their core technology. When a university demands an equity stake or high royalty payments in exchange for licensing back a student’s own invention, it can deplete the startup's cash reserves before it has reached maturity.

Furthermore, the Technology Transfer Office (TTO) process is frequently described as a bottleneck. TTOs are tasked with maximizing the university's revenue and minimizing its liability, which can lead to adversarial negotiations with the very founders they are meant to support. In some cases, as seen in Stanford v. Roche, the complexity of these ownership assignments leads to protracted litigation that small startups cannot survive.

Technical Debt and the Scalability Paradox

The "speed-to-market" imperative of the startup world often forces campus ventures to accrue significant "technical debt"—the trade-off between the short-term benefit of rapid delivery and the long-term value of stable engineering. In the campus context, where students are often learning to code while simultaneously building a business, technical debt is not merely a strategic choice but an inevitable consequence of limited experience.

Technical debt acts as a "silent assassin" for campus ventures. A codebase that was "stitched together" to win a business plan competition or to serve a few hundred students on campus often becomes a "monolithic disaster" when scaled to 100,000 users. This is particularly prevalent in the EdTech sector, where the stakes for failure are high—an app that crashes during final exams will lose its entire user base overnight.

The "interest payments" on technical debt manifest in several ways that kill scaling:

Innovation Standstill: As the codebase becomes tangled, even minor updates take weeks rather than days, causing the startup’s feature speed to grind to a halt.

Top Talent Attrition: Skilled developers, often the lifeblood of a startup, grow frustrated with "firefighting" messy code and "abandon ship" for stable corporate roles.

Onboarding Nightmares: The codebase becomes a convoluted mess that only the original founders understand, making it impossible to add new personnel to solve scaling problems.

Technical Debt Management for Startups | Impact Category | Long-term Risk |

Reckless Debt (Ugly Hacks) | Velocity | Product Atrophy |

Strategic Debt (Calculated Shortcuts) | Flexibility | High Refactoring Costs |

Outdated Frameworks | Security | Infrastructure Collapse |

Insufficient Documentation | Onboarding | Knowledge Silos |

The "Graduation Cliff" and the Reality of Earning Potential

The most insurmountable barrier to the success of a campus startup is often the graduation of its founders. The "Graduation Cliff" represents a dramatic shift in the opportunity cost of entrepreneurship. While in school, a student’s downside risk is limited—failure is a "data point" rather than a financial catastrophe. However, upon graduation, the founder must choose between a precarious, self-funded startup and a high-paying corporate role.

Statistics reveal a significant gap between entrepreneurial "intent" and "action" post-graduation. A survey of 2022 college graduates found that while 60 percent intended to launch or continue operating a business, only 17 percent were actually running a business they started during college. Conversely, 27 percent had no intentions of starting a business at all, preferring the security of a large company.

Gen Z founders are characterized by a pragmatic approach to risk. Deciding whether to accept a job is often based on whether the position offers good pay, which is a priority for 82 percent of Gen Zers, compared to 76 percent of millennials. The lure of "Big Tech" employers like Google, Microsoft, and Apple—which have adopted "lean startup" cultural elements like R&D innovation and rapid deployment—further reduces the incentive to take the personal and financial risk of launching a solo venture.

The "Human Capital Theory" suggests that university education acts as a double-edged sword for entrepreneurship. While it imparts necessary skills, it also professionalizes students, signaling their value to corporate recruiters and increasing their potential income from employment. Systematic analyses often find no positive association between graduating from university and becoming an entrepreneur, precisely because the alternative pathways (employment) are too attractive. For a campus startup to survive, it must generate enough revenue or secure enough venture capital within the "protected years" of school to offset the immediate earning potential of a corporate job—a feat few student ventures achieve.

The Failure of "Low-Barrier" Innovation

The "Student Bubble" frequently leads to a proliferation of what might be termed "convenience-based" startups—ideas that solve the very specific, low-stakes problems of campus life but have no defensible moat in the broader market. These include "Niche Tutoring," "Campus Laundry," "Dorm Delivery," and "T-Shirt Design".

While these ventures provide excellent "experiential learning," they rarely possess the unit economics to scale. For instance, a "Campus Laundry/Delivery Service" has a startup cost of only $50–$100, but its margins are thin and its operational model is difficult to sustain without a subsidized student labor pool. These businesses are "orphaned" upon graduation because the founders realize that the time-to-revenue realization is too slow to support a professional lifestyle.

Furthermore, the lack of "originality or world exposure" prevents many students from identifying genuinely innovative business ideas. They often build "solutions without problems," such as "social discovery" apps for students who already have well-established social networks, or "roommate bill-splitters" that compete with free, entrenched digital payment platforms. These ventures fail because they are "incremental" rather than "disruptive," and they often lack the "ecosystem moat" that allows winners like Facebook or Apple Watch to survive.

Common Campus Startup Ideas | Industry Category | Barrier to Entry | Reason for Failure |

T-shirt Design | Retail/E-commerce | Low | Saturated Market / Low Margins |

Dorm Room Cleaning | Service | Low | Non-scalable Labor Model |

Bill-Splitting Apps | Fintech | Medium | Competition with Incumbents (Venmo) |

Local Review Hubs | Media | Low | Lack of Monetization Strategy |

Campus Delivery | Logistics | Medium | Poor Unit Economics / High Burn |

The Disconnect in Entrepreneurial Education

A final contributor to the failure of campus startups is the "theory-reality gap" in entrepreneurial pedagogy. Many university programs focus on "polished lecture slides" and "thorough exams" that test memory rather than application. Statistics indicate that 2 out of 3 graduates cannot apply classroom knowledge at work, and 3 out of 4 employers believe new hires panic during real-world crises.

Student founders who "nail every exam" often "bomb their first real business meeting" because they have not practiced the emotional resilience required for entrepreneurship. Traditional assessments fail to teach "how to stay calm when everything is falling apart" or "how to negotiate when you have no leverage". When students are taught negotiation theory in October but don't receive feedback until November, the "feedback loop" is too slow to influence their actual business decisions. Programs that emphasize "active learning" through simulations show a 78 percent faster problem-analysis speed, yet many institutions remain wedded to a linear, lecture-based model that does not tolerate the messy, iterative reality of startup failure.

Synthesis: Why the Majority of Ideas Fail

The high mortality rate of campus startup ideas is not the result of a single flaw, but a systemic failure of the "campus-to-market" pipeline.

Market Validation Failure: The "False Start" pattern, driven by a technical "bias for action," ensures that 42 percent of ventures build products for which there is no customer.

Sociological Misalignment: Founding teams formed on friendship rather than strategic fit face a 65 percent risk of "death by conflict," particularly when equity splits are not managed with long-term vesting schedules.

Institutional Burden: University IP policies and the "maze" of technology transfer procedures create a "friction tax" that many young companies cannot pay, leading to "fractured ownership" that scares off venture capital.

The Opportunity Cost of Graduation: The "Graduation Cliff" forces a pragmatic choice where the security and high earning potential of corporate roles (e.g., at Google or Apple) outweigh the high-risk, self-funded "hustle" of a campus project.

Technical Debt and Scaling: The inability of student founders to manage the transition from a "hacky" MVP to a scalable, architecturally sound product leads to "innovation standstills" and the death of user experience.

Ultimately, most campus startup ideas fail because they are treated as "academic projects" rather than "industrial entities." The university environment provides a "protective bubble" that encourages experimentation but often fails to prepare the venture for the Darwinian realities of the private sector. For a campus idea to succeed, it must navigate the "Three Pillars of Survival": rigorous customer discovery to avoid the False Start, professionalized team governance to avoid the Co-Founder Split, and institutional IP clarity to ensure investor readiness. Without these, even the most innovative research will likely remain an "orphan" of the academic ecosystem.

Read More -

1. From Idea to MVP: A Step-by-Step Guide for Solo Founder

🔗 https://findnstart.com/blogs/from-idea-to-mvp-a-step-by-step-guide-for-solo-founder

2. How to Validate Your Startup Idea in 48 Hours for $0

🔗 https://findnstart.com/blogs/how-to-validate-your-startup-idea-in-48-hours-for-0

3. Remote vs. Local: Does Your Co-Founder Need to Live in the Same City?

🔗 https://findnstart.com/blogs/remote-vs-local-does-your-co-founder-need-to-live-in-the-same-city

4. The 2026 Startup Landscape: What Has Fundamentally Changed (and Why Founder Skills Matter More Than Ever)

5. The Most In-Demand Skills for Startup Founders in 2026

🔗 https://findnstart.com/blogs/the-most-in-demand-skills-for-startup-founders-in-2026

6. How to Find a Technical Co-Founder (Without a Six-Figure Salary)

🔗 https://findnstart.com/blogs/how-to-find-a-technical-co-founder-without-a-six-figure-salary

7. 5 Red Flags to Look for When Choosing a Startup Partner

🔗 https://findnstart.com/blogs/5-red-flags-to-look-for-when-choosing-a-startup-partner

8. How to Pitch Your Idea to Potential Co-Founders

🔗 https://findnstart.com/blogs/how-to-pitch-your-idea-to-potential-co-founders

9. How to Build a Portfolio that Attracts High-Growth Startup Founders

🔗 https://findnstart.com/blogs/how-to-build-a-portfolio-that-attracts-high-growth-startup-founders

10. Equity vs. Salary: How to Split Ownership with Your First Teammate

🔗 https://findnstart.com/blogs/equity-vs-salary-how-to-split-ownership-with-your-first-teammate

11. Why Joining an Early-Stage Startup is Better Than a Corporate Job

🔗 https://findnstart.com/blogs/why-joining-an-early-stage-startup-is-better-than-a-corporate-job

12. The Future of EdTech: Why Developers and Educators Need to Team Up Now

🔗 https://findnstart.com/blogs/the-future-of-edtech-why-developers-and-educators-need-to-team-up-now

13. The Architecture of Symbiosis: Analytical Perspectives on the Five Habits of Successful Startup Duos

14. Finding a Co-Founder in the AI Space: What Skills Should You Look For?

🔗 https://findnstart.com/blogs/finding-a-co-founder-in-the-ai-space-what-skills-should-you-look-for

15. Overcoming Analysis Paralysis and the Strategic Path to Execution

🔗 https://findnstart.com/blogs/overcoming-analysis-paralysis-and-the-strategic-path-to-execution

16. From College Project to Company: How to Find Your Student Co-Founder

🔗 https://findnstart.com/blogs/from-college-project-to-company-how-to-find-your-student-co-founder

17. How to Start a Startup While Working a Full-Time Job

🔗 https://findnstart.com/blogs/how-to-start-a-startup-while-working-a-full-time-job

18. How to Build a HealthTech Startup Without a Medical Degree

🔗 https://findnstart.com/blogs/how-to-build-a-healthtech-startup-without-a-medical-degree

19. The Solitary Architect: Executive Isolation in Entrepreneurship

20. The 2026 Guide to Launching a SaaS as a Solo Developer

21. What Sustainable Growth Actually Looks Like

🔗 https://findnstart.com/blogs/what-sustainable-growth-actually-looks-like

22. The Early Warning Signs Your Startup Is in Trouble

🔗 https://findnstart.com/blogs/the-early-warning-signs-your-startup-is-in-trouble

23. How to Grow Without Burning Out

🔗 https://findnstart.com/blogs/how-to-grow-without-burning-out

24. The Truth About “Runway” Most Founders Ignore

🔗 https://findnstart.com/blogs/the-truth-about-runway-most-founders-ignore

25. Revenue Solves More Problems Than Funding

🔗 https://findnstart.com/blogs/revenue-solves-more-problems-than-funding

26. What No One Tells You About Being a Solo Founder

🔗 https://findnstart.com/blogs/what-no-one-tells-you-about-being-a-solo-founder

27. Why Smart People Quit High-Paying Jobs to Build Startups (And Why Most Regret It)

28. Why Most Startup Advice on Twitter Is Dangerous

🔗 https://findnstart.com/blogs/why-most-startup-advice-on-twitter-is-dangerous

29. Decision Fatigue: The Silent Startup Killer

🔗 https://findnstart.com/blogs/decision-fatigue-the-silent-startup-killer

30. Fear vs Logic: How Founders Actually Make Decisions

🔗 https://findnstart.com/blogs/fear-vs-logic-how-founders-actually-make-decisions

31. How Overthinking Destroys Early Momentum

🔗 https://findnstart.com/blogs/how-overthinking-destroys-early-momentum

32. Ideas Don’t Scale. Systems Do.

🔗 https://findnstart.com/blogs/ideas-dont-scale-systems-do

33. The First Hire That Actually Matters

🔗 https://findnstart.com/blogs/the-first-hire-that-actually-matters

34. How the First 100 Users Decide Your Startup’s Fate

🔗 https://findnstart.com/blogs/how-the-first-100-users-decide-your-startups-fate

35. Why Your Startup Doesn’t Need Growth — It Needs Focus

🔗 https://findnstart.com/blogs/why-your-startup-doesnt-need-growthit-needs-focus

36. Why Most Startups Die Quietly

🔗 https://findnstart.com/blogs/why-most-startups-die-quietly

37. Lessons Learned Too Late by First-Time Founders

🔗 https://findnstart.com/blogs/lessons-learned-too-late-by-first-time-founders

38. The Myth of the “Overnight Success” Startup

🔗 https://findnstart.com/blogs/the-myth-of-the-overnight-success-startup

Protect Your Future: The Precision Vesting Calculator

Don't let a "handshake deal" complicate your exit. Map out your ownership journey with our Vesting Calculator

Calculate Your Vesting Schedule →