Why Most AI Startups Will Die in the Next 18 Months

March 11, 2026 by Harshit Gupta

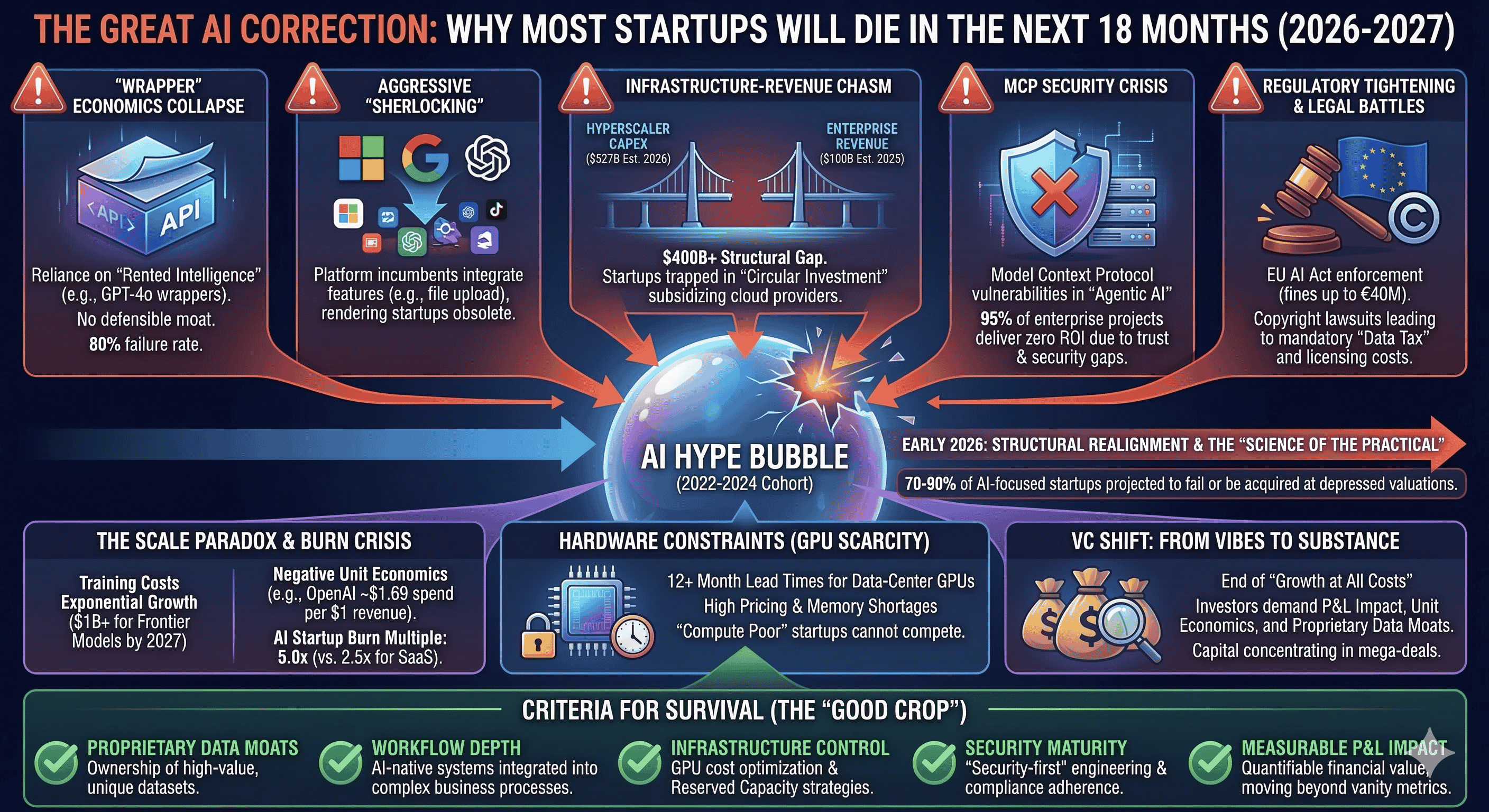

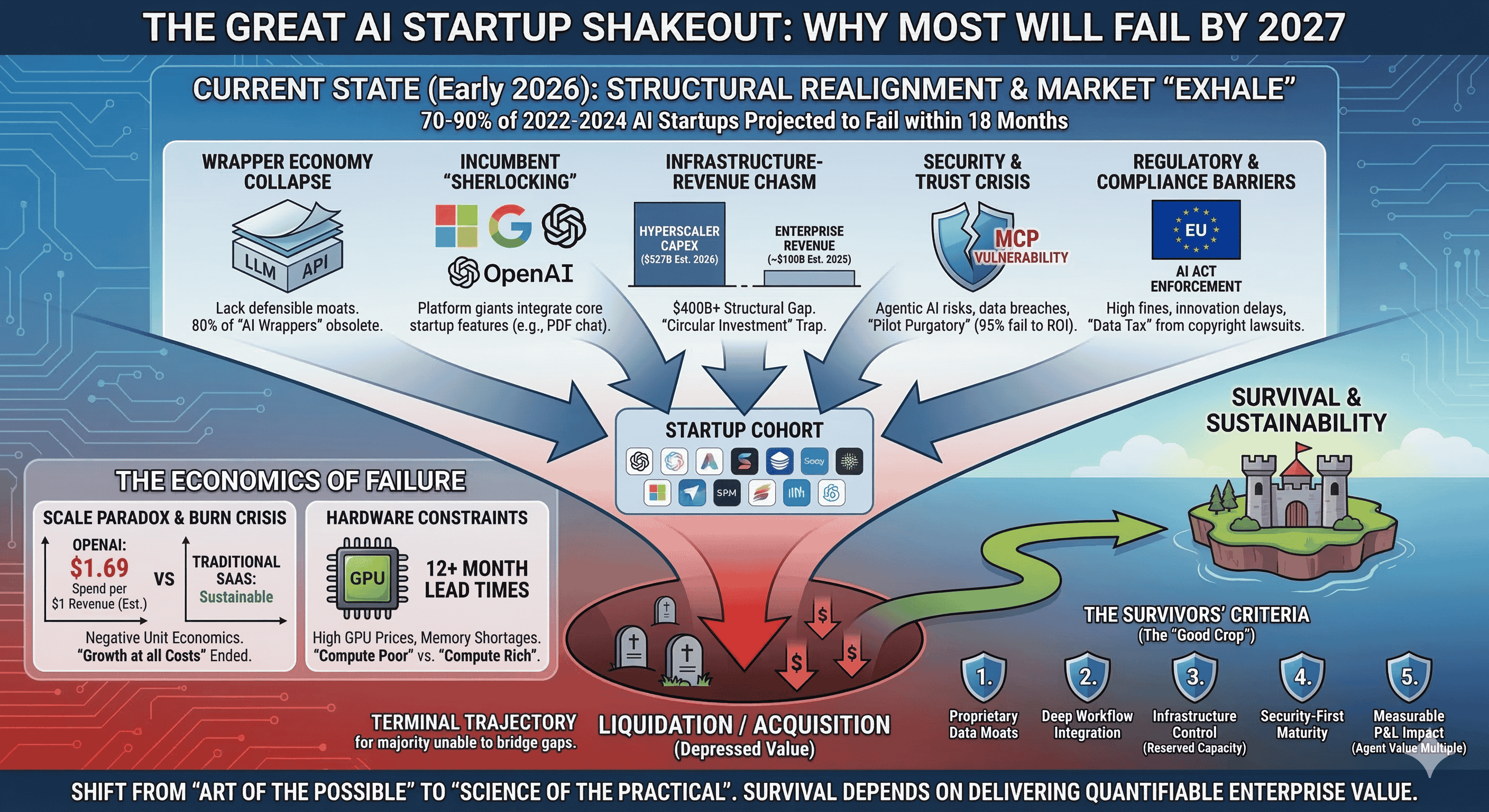

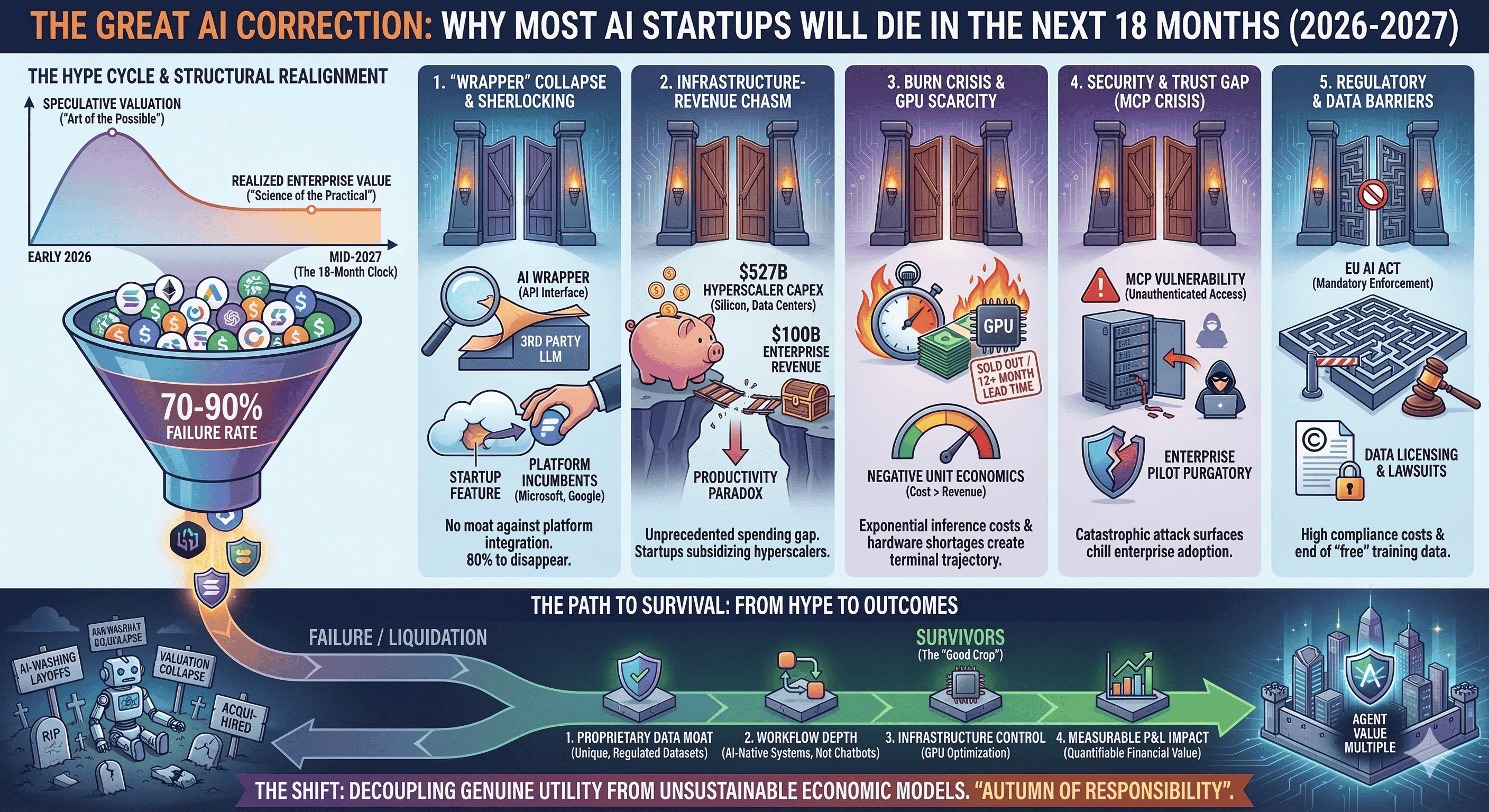

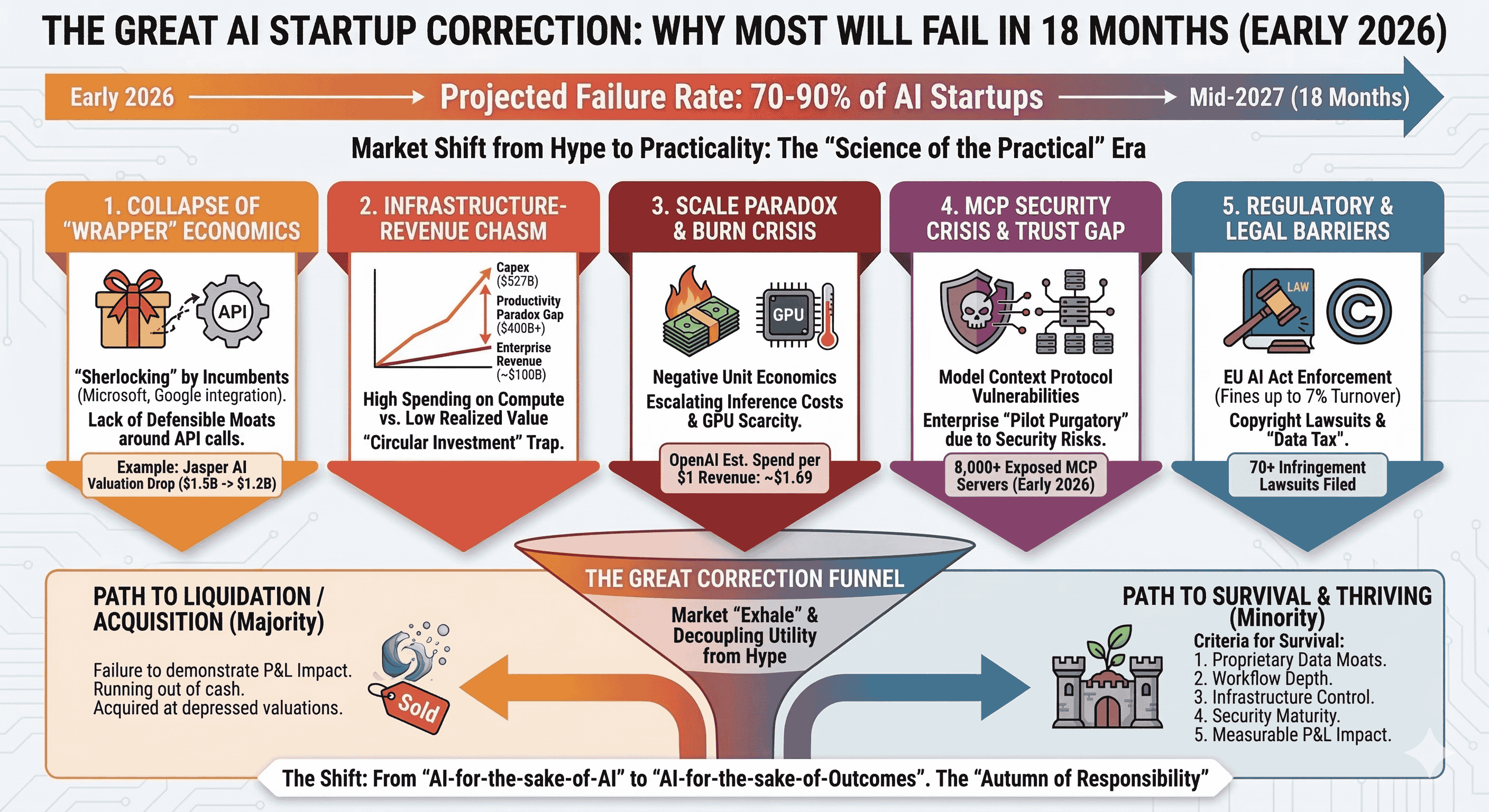

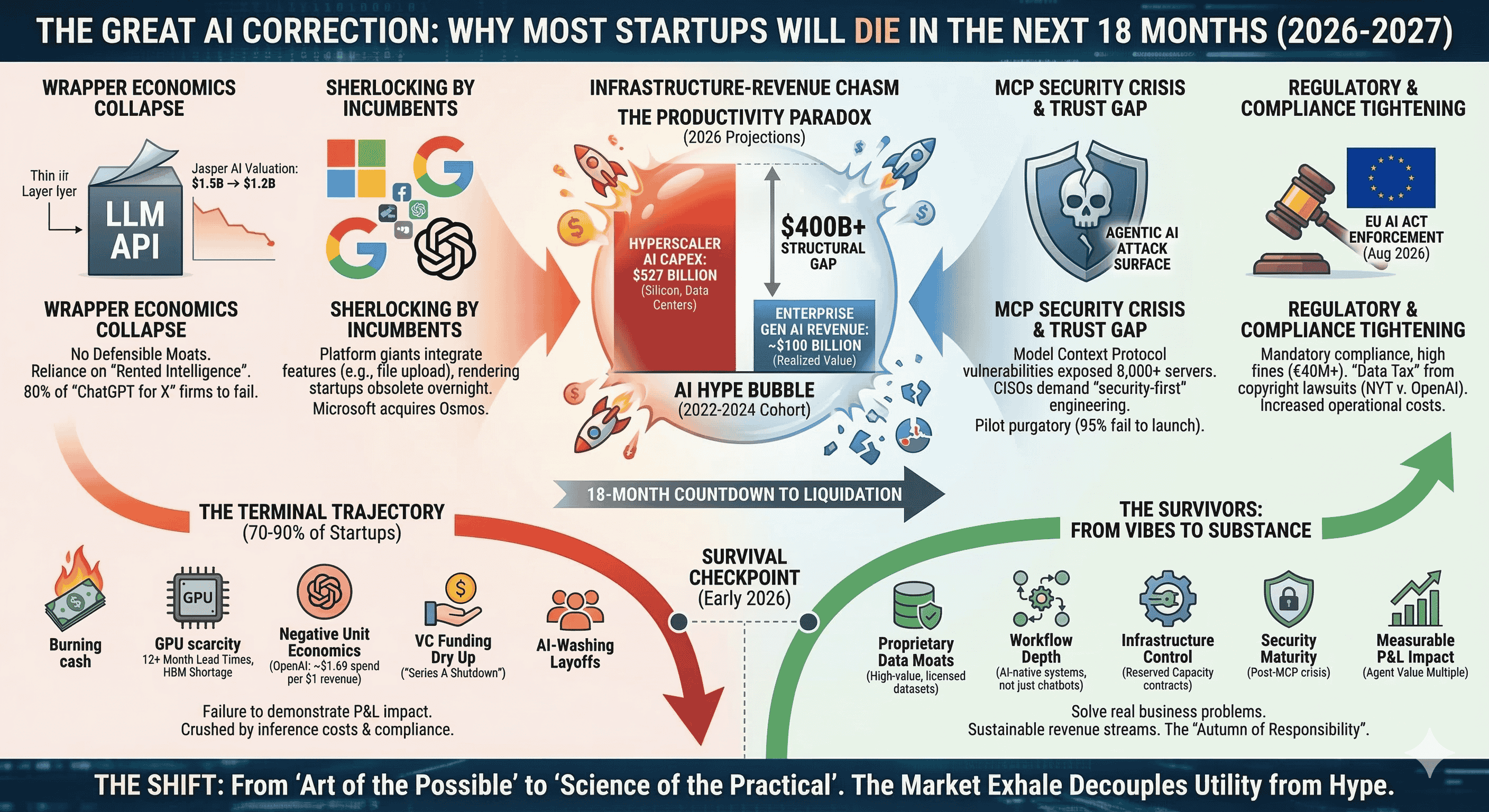

The artificial intelligence sector is currently navigating a period of profound structural realignment. As of early 2026, the market has transitioned from the "art of the possible" to the "science of the practical," a shift that necessitates the liquidation of a significant majority of the startup cohort founded between 2022 and 2024. While the infrastructure layer continues to see massive capital investment, the application layer is experiencing a terminal disconnect between speculative valuation and realized enterprise value. Current estimates suggest that between 70% and 90% of AI-focused startups will fail or be acquired at depressed valuations within the next 18 months, as the market corrects for over-investment, "AI-washing," and the lack of defensible moats. This correction is not a signal of the technology’s failure but rather a necessary market "exhale" that will decouple genuine utility from the unsustainable economic models that defined the initial hype cycle.

The impending shakeout is driven by a convergence of five critical pressures: the collapse of "wrapper" economics, the aggressive "Sherlocking" of features by platform incumbents, a widening chasm between infrastructure capital expenditure and enterprise revenue, the emergence of the Model Context Protocol (MCP) security crisis, and a tightening global regulatory environment. In this environment, the primary metric of success has shifted from user acquisition and model parameters to the "Agent Value Multiple" and measurable impact on the corporate profit and loss statement. For the majority of startups, the inability to demonstrate this impact, coupled with escalating inference costs and GPU scarcity, creates a terminal trajectory.

The Infrastructure-Revenue Chasm: A Productivity Paradox

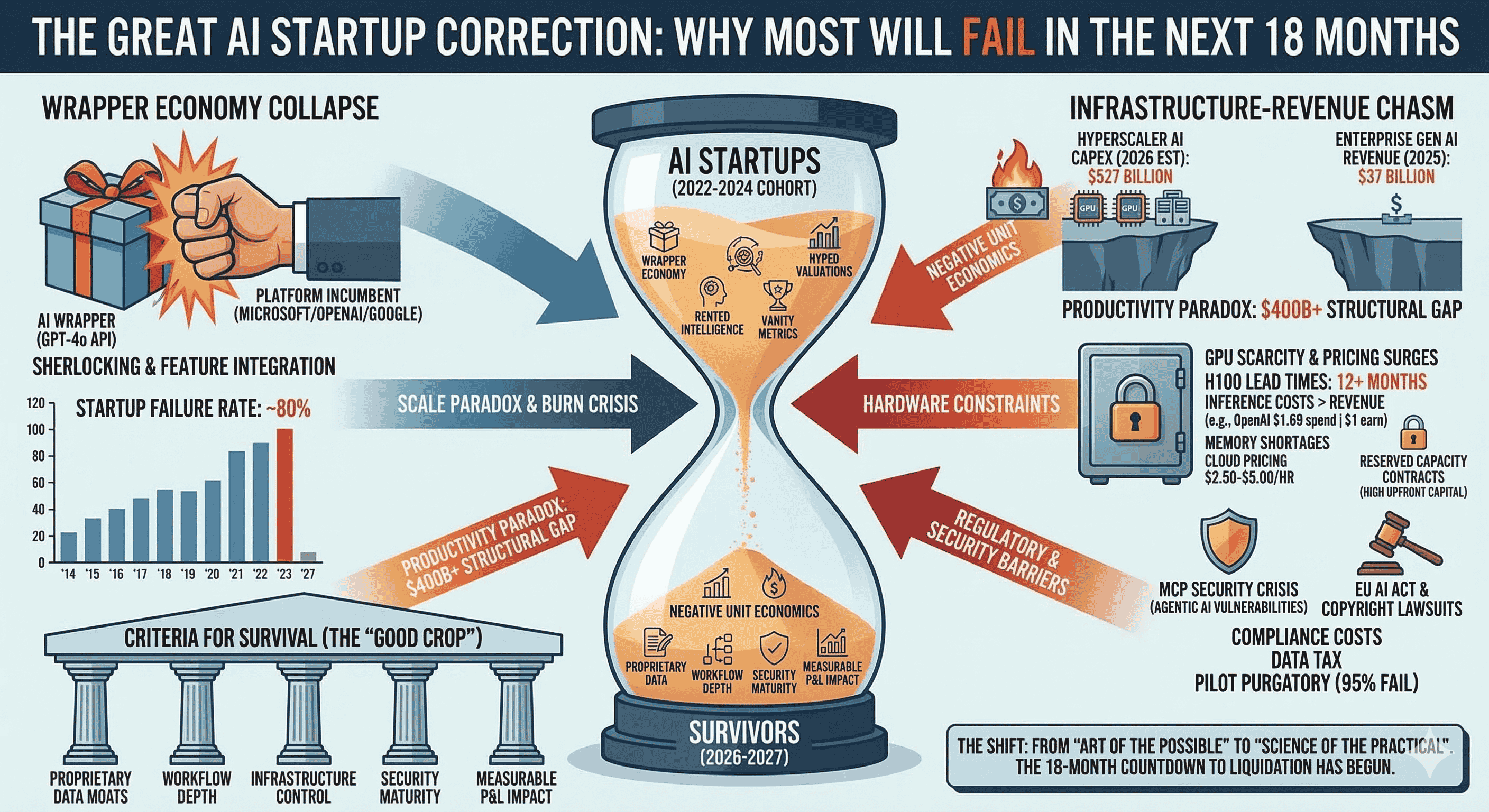

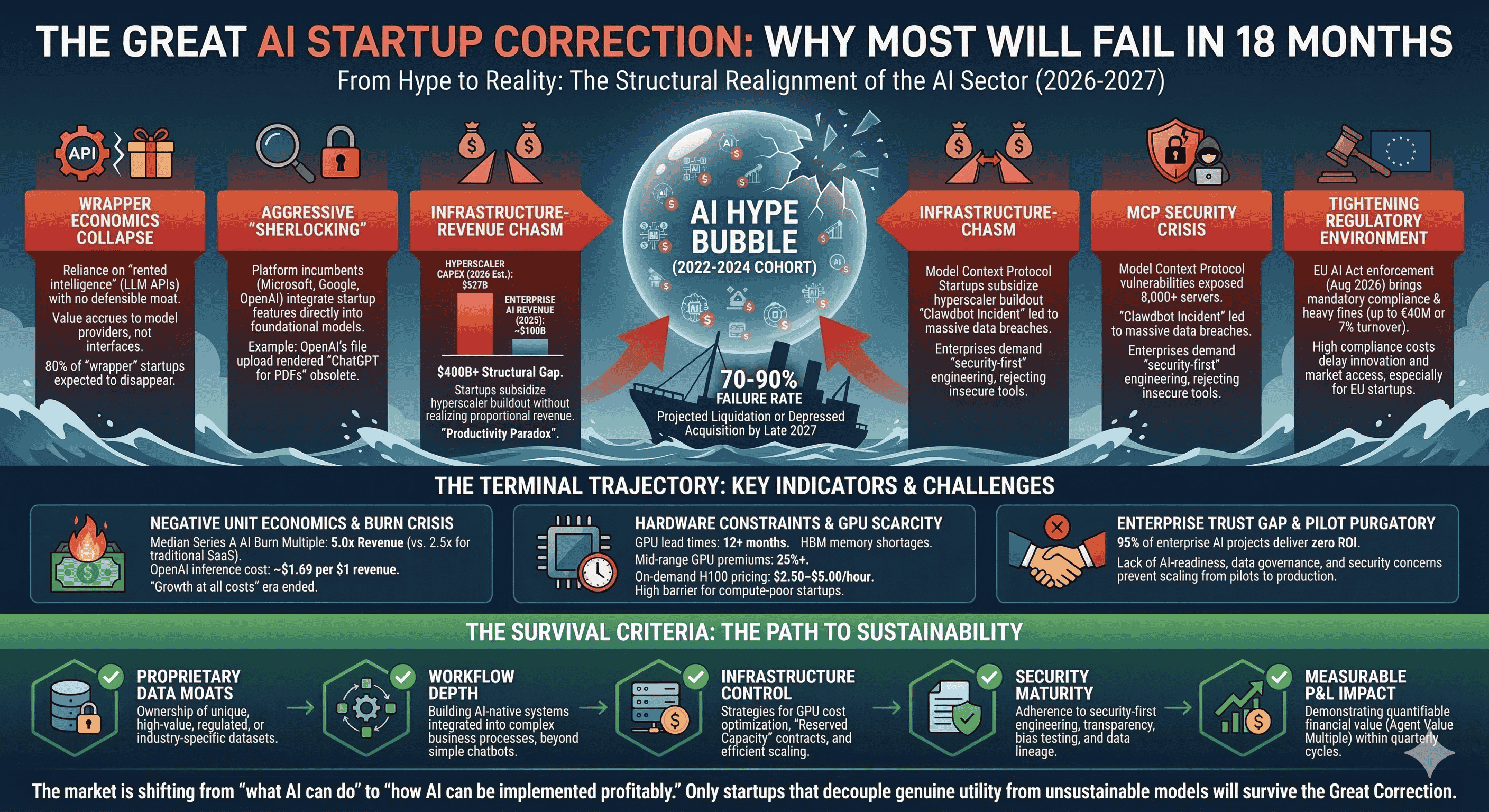

The most immediate threat to the survival of AI startups is the unprecedented gap between the cost of building intelligence and the revenue generated from its application. By February 2026, the consensus among Wall Street analysts for hyperscaler capital expenditure (capex) reached $527 billion. This investment, primarily directed toward silicon, data centers, and cooling systems, represents a calculated long-term bet on AI as the new "electricity" of the global economy. However, the enterprise revenue realized from these investments remains disproportionately low, estimated at approximately $100 billion for the 2025 fiscal year.

2026 AI Economic Indicators and Projections

Financial Metric | Estimated Value | Context / Data Source |

Hyperscaler AI Capex (2026 Consensus) | 527 billion | Goldman Sachs Research |

Worldwide AI Spending (2026 Projection) | 2+ trillion | Gartner Estimates |

Enterprise Generative AI Revenue (2025) | 37 billion | Menlo Ventures Analysis |

Total VC Funding Captured by AI (2025) | 238 billion | 47% of all venture capital |

OpenAI Projected Net Loss (2026) | 14−17 billion | Internal Financial Projections |

Alphabet Target Capex (2026) | 175−185 billion | Public Disclosures |

This $400 billion structural gap between spending and revenue realization is described as the single biggest risk to the AI investment thesis. Unlike the overbuilt fiber optic networks of the dot-com era, which remained unused for years, current GPU assets are heavily utilized. However, the economic value they produce is largely being captured by model providers and hardware manufacturers, leaving startups in a "circular investment" trap. In this cycle, venture capital flows into startups, which then immediately transfer that capital to cloud providers for compute access, effectively subsidizing the hyperscalers' own capex cycles.

The Federal Reserve has begun to monitor this "productivity paradox" closely, debating whether the structural boost to productivity will materialize within the next 2-5 years or if the current buildout is a speculative excess. A National Bureau of Economic Research study published in February 2026 found that despite 90% of firms reporting no current impact of AI on workplace productivity, executives still project a 1.4% increase in the near future. For startups, the 18-month clock is ticking; they must bridge the gap between these executive projections and actual balance sheet impact before investor patience is exhausted.

The Obsolescence of the "Wrapper" Economy and the Integration War

The most vulnerable segment of the market consists of "AI wrappers"—startups that provide a functional layer or user interface on top of third-party Large Language Model (LLM) APIs such as GPT-4o or Claude 3.5. In the 18-month window following early 2026, approximately 80% of these firms are expected to disappear as their lack of defensible moats is exposed by platform incumbents.

The primary catalyst for this failure is "Sherlocking," where platform giants like Microsoft, OpenAI, and Google integrate features into their foundational models that were previously the primary offering of third-party startups. A definitive example occurred in November 2023 when OpenAI introduced a file upload feature, effectively rendering dozens of "ChatGPT for PDFs" startups obsolete overnight.

Strategic Devaluations and Startup Failures (2022-2026)

Startup | Event / Outcome | Financial Impact |

Jasper AI | Competitive expansion by LLM providers | Valuation fell from 1.5B to 1.2B; revenue collapsed from 120M to 55M |

Revealed as "offshore human developers" faking AI | Filed for bankruptcy in May 2025 after burning 445M | |

Adept AI | Talent drain / "Acqui-hire" | Founders joined Amazon; technology licensed |

Acquired for IP/Talent | Acquired by Google in 2024 for 2.7B despite only 30M ARR | |

Rain AI | Sustainability crisis | Shut down as enterprise wrapper model failed |

Kite | Monetization failure | Shut down in 2022 after raising 30M |

The fundamental flaw in the wrapper business model is the reliance on "rented intelligence". When a startup’s value proposition is merely the orchestration of an API call, it possesses no defensible advantage against the API provider or a well-resourced incumbent with deeper distribution. In 2026, the market has realized that the value is not in the model itself, which is becoming a commodity, but in the proprietary data, the context, and the deep integration into specific industry workflows. Startups that failed to move beyond the "chat layer" are finding their margins collapsing as inference costs remain high while customer willingness to pay for "extra packaging" evaporates.

This trend is exemplified by Microsoft’s 2026 acquisition of Osmos, an AI-driven data engineering platform. By folding Osmos’ autonomous agents directly into Microsoft Fabric and the OneLake data repository, Microsoft eliminated the need for third-party orchestration tools in that vertical. This "platform absorption" strategy ensures that value accrues to the companies that own the data and the distribution, rather than the startups providing the interface.

The Scale Paradox: Negative Unit Economics and the Burn Crisis

The survival of AI startups is increasingly dictated by the brutal mathematics of model inference and energy consumption. While the cost of older or smaller models has plummeted—for instance, the powerful THUDM/GLM-4 model now costs $0.086 per million tokens compared to previous generational costs of $60—the cost to train and run "frontier" models is growing exponentially. Training top-tier systems is projected to hit $1 billion or more by 2027, creating a capital barrier that excludes all but the most well-funded entities.

For startups, this creates a "Scale Paradox" where popularity can become a liability. In early 2026, leaked financial data revealed that OpenAI’s inference costs were exceeding its subscription revenue. Simply put, for every dollar earned, the company was spending roughly $1.69 to generate that intelligence. This negative unit economic model is even more severe for startups that lack the favorable cloud contracts enjoyed by foundational model providers.

Median Unit Economics and Burn Rates in 2026

Company Stage / Type | Burn Multiple (Spend per $1 Revenue) | Efficiency Relative to Non-AI SaaS |

Median Series A AI Startup | 5.00 | 1.40 higher than traditional SaaS |

Median Series C AI Startup | 3.10 | 0.60 higher than traditional SaaS |

OpenAI (Internal Projection) | 1.69 | Negative marginal utility per query |

Traditional SaaS Median | 2.50 | Benchmark for sustainable growth |

This disparity in spending matters because the "growth at all costs" era has definitively ended. Investors now demand visibility into customer acquisition costs, lifetime value, and specifically the economics of AI operations, including infrastructure scaling and model training expenses. Startups that continue to burn through cash to maintain "vanity metrics" like task completion rates are being replaced by those measuring "Agent Value Multiple"—the financial value generated per agent cost.

Furthermore, the physical requirements for these operations are reaching an environmental and financial limit. By 2026, global AI data centers are expected to consume 90 terawatt-hours of electricity annually, a tenfold increase from 2022 levels. Securing this power requires grid approvals and infrastructure that take years to build, creating a physical bottleneck that startups cannot bypass with software innovation alone.

Hardware Constraints and the GPU Supply-Market Disconnect

The physical infrastructure of AI is facing a structural shift where artificial intelligence has become the dominant consumer of global computing hardware. In 2026, the compute crunch has moved from anecdotal complaints to a global economic issue, with lead times for data-center GPUs climbing to over a year. While hyperscalers like Amazon, Meta, and Google have the capital to secure long-term training capacity, startups lack the negotiating power to secure hardware directly from vendors.

GPU Pricing and Supply Realities in 2026

Lead Times: Global hardware distributors report that lead times for premium AI accelerators are sustained at 12+ months through late 2026.

Memory Shortages: DRAM and HBM memory shortages are "strangling" GPU production, with data centers consuming 70% of the global memory supply.

Pricing Surges: NVIDIA and AMD implemented significant price hikes in early 2026. Mid-range GPUs are commanding 25% premiums above MSRP, while on-demand cloud pricing for H100s fluctuates between $2.50 and $5.00 per hour.

Memory Costs: HBM shortages are reported at 30-70% globally, with DRAM costs surging 15%, a bottleneck expected to persist until 2028.

For a mid-stage startup, GPU costs can easily exceed $150,000 per month on an on-demand basis, a figure that is often higher than the company’s entire payroll. To survive, startups must pivot to "Reserved Capacity" contracts, committing to 3-12 month terms to unlock 40-72% discounts. However, this requires significant upfront capital—a resource that is becoming increasingly scarce as VCs tighten their belts. The result is a hardware-driven stratification where the "compute poor" startups are unable to iterate fast enough to compete with "compute rich" incumbents.

The Enterprise Trust Gap: Pilot Purgatory and Security Vulnerabilities

A critical barrier to startup survival is the failure of AI projects to move from pilot programs to enterprise-wide production. A blunt MIT study found that 95% of enterprise AI projects are currently delivering zero financial return on investment. This failure is often rooted in the "AI-Readiness Gap"—the lack of trustworthy, governed, and contextualized data within the enterprise.

Enterprises are discovering that layering modern AI over fragile legacy infrastructure creates massive security gaps and inconsistent performance, leading to "hallucinations" that are rooted in poor data plumbing rather than the AI itself. For startups, this means that success is no longer measured by implementation, but by systemic resilience and the ability to integrate with decades-old data architectures.

The 2026 Model Context Protocol (MCP) Security Crisis

The emergence of "Agentic AI"—systems capable of executing complex, multi-step tasks autonomously—has introduced a new and catastrophic attack surface. In early 2026, security researchers identified a massive vulnerability in the Model Context Protocol (MCP) ecosystem, which had been rapidly adopted to enable agents to access enterprise tools.

Exposed Servers: Scanners found over 8,000 MCP servers visible on the public internet, many with unauthenticated admin panels.

Clawdbot Incident: The popular Clawdbot ecosystem experienced a catastrophic breach where 1,000+ admin panels were publicly accessible, leading to the extraction of API keys and internal database credentials.

Default Vulnerabilities: The root cause was identified as default configurations binding admin panels to public-facing ports without authentication.

Prompt Injection: Attackers exploited unauthenticated access to modify agent behavior and inject malicious system prompts, leading to unauthorized API charges and data exfiltration.

This security crisis has led to a "chill" in enterprise adoption. CISOs (Chief Information Security Officers) are now demanding documented proof of model transparency, bias testing, and data lineage before any tool is granted "execution authority" within the network. Startups that built their products without "security-first engineering" are being systematically rejected by the very Fortune 500 customers they need to achieve sustainability.

Regulatory Barriers and the Cost of Global Compliance

The regulatory landscape in 2026 has transitioned from voluntary governance to mandatory enforcement, particularly with the full implementation of the European Union AI Act on August 2, 2026. This shift represents a "landmark year for enforcement," where compliance has become a strategic imperative for market access.

Financial Penalties and Compliance Tiers under the EU AI Act

Infraction Category | Maximum Penalty | Risk Classification Examples |

Prohibited AI Use | €40M or 7% of annual turnover | Social scoring, manipulative AI |

Data or Transparency Violations | €20M or 4% of annual turnover | Generative AI without disclosure |

High-Risk System Obligations | €15M or 3% of annual turnover | Recruitment, credit scoring, healthcare |

Incorrect Information to Regulators | €7.5M or 1% of annual turnover | Deceptive audit documentation |

For startups, the cost of compliance is not just the threat of fines but the "hidden cost" of lost innovation and market access. In the EU and UK, technology SMEs are losing between $109,000 and $375,000 annually due to delays in AI model launches driven by regulatory friction. Six in ten EU/UK startups report delayed access to frontier AI models, a structural barrier that does not exist in the United States, where regulation is treated as a "speed bump" rather than a "brake".

The result is a widening "Adoption Gap": 62% of U.S. startups are actively using AI compared to only 50% in the EU. Furthermore, U.S. firms are realizing median cost savings of 10.7% from AI, compared to 8.9% for their European counterparts. For European startups, the 18-month survival window is even tighter, as they must compete against better-funded and less-regulated U.S. peers while navigating the "compliance maze".

The Legal Battlefield: Copyright, Licensing, and the "Data Tax"

The foundation of the AI startup economy—unrestricted access to training data—is currently being dismantled in the courts. As of early 2026, over 70 infringement lawsuits have been filed by copyright owners against AI companies. These cases are moving toward a mandatory licensing model that will impose a significant "data tax" on all AI development.

Major AI Copyright Lawsuits Status (February 2026)

New York Times v. OpenAI/Microsoft: The Times alleges millions of copyrighted articles were used without permission. A settlement is expected in 2026, likely involving a multi-million dollar licensing agreement similar to the $20-25 million deal between the NYT and Amazon.

Getty Images v. Stability AI: Getty claims Stability AI unlawfully processed millions of images. The case marks three years of litigation in London with no definite conclusion, though it has forced Stability to seek authorized licensing options.

Concord v. Anthropic: Music publishers allege Anthropic used pirate library websites (Library Genesis) to train its models. In January 2026, the court denied a request to include specific BitTorrent claims, but the case remains a landmark for the music industry.

Authors Guild v. OpenAI: This multidistrict litigation involves dozens of authors (including Sarah Silverman) alleging their books were used as a "training ground" without permission. Settlement negotiations are reported as the "big trend" for 2026.

The implication of these cases is clear: the era of "free" data is over. Future AI models will be trained on "fully authorized and licensed" data, with new subscription services for licensed music and text already planned for 2026. For startups, this creates an insurmountable cost barrier. Only the largest tech firms can afford to pay for high-quality, authorized datasets, while startups relying on "scraped" data face mounting litigation risk and the potential for "unlearning" orders that could wipe out their primary intellectual property.

The 2026 Tech Layoffs: AI-Washing and the "Efficiency" Narrative

As the financial realities of AI set in, a troubling trend of "AI-washing" in corporate layoffs has emerged. In early 2026, several major technology companies announced significant workforce reductions, attributing them to AI-driven efficiencies when, in reality, they were restructuring to compensate for the higher interest rate environment and cautious investor sentiment.

Notable Tech Layoffs Attributed to AI (Jan-Feb 2026)

Company | Headcount Reduction | AI Rationale / Context |

Block (Square/Cash App) | 4,000 employees (40%) | CEO Jack Dorsey cited "intelligence tools" as the catalyst for leaner operations |

Amazon | 16,000 corporate staff | CEO Andy Jassy vocal about AI rollout reducing the need for human roles |

700 employees (15%) | Redirecting resources to "AI-forward strategy" | |

Livspace | 1,000 employees | Frame as "AI-driven cost rationalization" rather than replacement |

xAI | "Co-founders and engineers" | Reorganization under Elon Musk to hire "aggressively" elsewhere |

eBay | 800 employees (6%) | Effort to align resources with "strategic priorities" |

Economists urge caution, pointing out that realizing workforce reductions from AI productivity gains requires "significant managerial adjustment" that may not be happening as swiftly as the layoff announcements imply. In many cases, AI provides a "future-oriented scapegoat" for trimming fat accumulated during the pandemic-era tech boom. For AI startups, this trend is a double-edged sword: while it validates the demand for automation tools, it also increases regulatory scrutiny on how AI is used to replace humans, potentially leading to new labor mandates that could increase the cost of doing business.

The VC Shift: From "Vibes" to Substance

The venture capital landscape in 2026 has matured from "irrational exuberance" to "nuanced frameworks" for evaluating AI startups. Investors are no longer impressed by technical complexity alone; they are seeking startups with unique data assets, proprietary training methodologies, and exclusive access to specific market segments.

The era of "growth at all costs" has definitively ended. VCs now demand clear visibility into unit economics from the earliest stages, including model training expenses and infrastructure scaling requirements. Startups that survived the initial 2024-2025 reset are those that demonstrated "real resilience" and the ability to generate "sustainable revenue streams".

Comparison of AI Startup Funding: 2024 vs. 2025

Funding Metric | 2024 Final | 2025 Final | YoY Growth |

Total AI VC Investment | 114.4 billion | 238 billion | +194% |

AI Share of Global VC | 34% | 47% | +13% |

Median Burn per $1 Revenue | 3.60 (Est.) | 5.00 | +38% |

Unicorn Count (AI) | 120 (Est.) | Over 250 | +108% |

However, this concentration of capital in a few "mega-deals" (OpenAI, xAI, Anthropic) raises significant bubble concerns. While AI captured nearly half of all VC funding in 2025, five companies raised 20% of that total, leaving the thousands of smaller "wrapper" startups to fight over a diminishing pool of capital. For the 2024-2025 cohort of startups, the "Series A shutdown" has become a documented reality, with a 2.5x year-over-year increase in failures for startups that simply resell existing APIs.

Synthesis and Strategic Outlook for 2026-2027

The analysis of current market data suggests that the AI startup ecosystem is entering a "Great Correction." The sound of the "bubble popping" is not a catastrophic crash but the deflation of the hype bubble, clearing the way for a "good crop" of startups that solve real business problems.

The Criteria for Startup Survival

To survive the next 18 months, an AI startup must possess:

Proprietary Data Moats: Ownership of high-value, regulated, or industry-specific datasets that cannot be easily replicated by model providers.

Workflow Depth: Moving beyond chatbots to build AI-native systems that weave intelligence directly into complex, multi-step business processes.

Infrastructure Control: Strategies for GPU cost optimization and the ability to operate within the "Reserved Capacity" model.

Security Maturity: Adherence to "security-first" engineering, particularly in the wake of the MCP security crisis, to bridge the enterprise "trust gap".

Measurable P&L Impact: The ability to move beyond "vanity metrics" and deliver quantifiable financial value within quarterly reporting cycles.

The technology itself is over-delivering, sprinting ahead of the ability to regulate, integrate, and ethically manage it. The "chill" currently felt in the market is not a "winter of disillusionment" but the "autumn of responsibility". For the startups that can navigate this transition—those that move from "AI-for-the-sake-of-AI" to "AI-for-the-sake-of-outcomes"—the rewards will be immense. However, for the majority of the current cohort, the 18-month clock represents the final countdown to liquidation. The conversation has shifted from "what AI can do" to "how AI can be implemented profitably," and in that shift, the weak, the over-leveraged, and the "Sherlocked" will inevitably fall by the wayside.

Read More -

1. From Idea to MVP: A Step-by-Step Guide for Solo Founder

🔗 https://findnstart.com/blogs/from-idea-to-mvp-a-step-by-step-guide-for-solo-founder

2. How to Validate Your Startup Idea in 48 Hours for $0

🔗 https://findnstart.com/blogs/how-to-validate-your-startup-idea-in-48-hours-for-0

3. Remote vs. Local: Does Your Co-Founder Need to Live in the Same City?

🔗 https://findnstart.com/blogs/remote-vs-local-does-your-co-founder-need-to-live-in-the-same-city

4. The 2026 Startup Landscape: What Has Fundamentally Changed (and Why Founder Skills Matter More Than Ever)

5. The Most In-Demand Skills for Startup Founders in 2026

🔗 https://findnstart.com/blogs/the-most-in-demand-skills-for-startup-founders-in-2026

6. How to Find a Technical Co-Founder (Without a Six-Figure Salary)

🔗 https://findnstart.com/blogs/how-to-find-a-technical-co-founder-without-a-six-figure-salary

7. 5 Red Flags to Look for When Choosing a Startup Partner

🔗 https://findnstart.com/blogs/5-red-flags-to-look-for-when-choosing-a-startup-partner

8. How to Pitch Your Idea to Potential Co-Founders

🔗 https://findnstart.com/blogs/how-to-pitch-your-idea-to-potential-co-founders

9. How to Build a Portfolio that Attracts High-Growth Startup Founders

🔗 https://findnstart.com/blogs/how-to-build-a-portfolio-that-attracts-high-growth-startup-founders

10. Equity vs. Salary: How to Split Ownership with Your First Teammate

🔗 https://findnstart.com/blogs/equity-vs-salary-how-to-split-ownership-with-your-first-teammate

11. Why Joining an Early-Stage Startup is Better Than a Corporate Job

🔗 https://findnstart.com/blogs/why-joining-an-early-stage-startup-is-better-than-a-corporate-job

12. The Future of EdTech: Why Developers and Educators Need to Team Up Now

🔗 https://findnstart.com/blogs/the-future-of-edtech-why-developers-and-educators-need-to-team-up-now

13. The Architecture of Symbiosis: Analytical Perspectives on the Five Habits of Successful Startup Duos

14. Finding a Co-Founder in the AI Space: What Skills Should You Look For?

🔗 https://findnstart.com/blogs/finding-a-co-founder-in-the-ai-space-what-skills-should-you-look-for

15. Overcoming Analysis Paralysis and the Strategic Path to Execution

🔗 https://findnstart.com/blogs/overcoming-analysis-paralysis-and-the-strategic-path-to-execution

16. From College Project to Company: How to Find Your Student Co-Founder

🔗 https://findnstart.com/blogs/from-college-project-to-company-how-to-find-your-student-co-founder

17. How to Start a Startup While Working a Full-Time Job

🔗 https://findnstart.com/blogs/how-to-start-a-startup-while-working-a-full-time-job

18. How to Build a HealthTech Startup Without a Medical Degree

🔗 https://findnstart.com/blogs/how-to-build-a-healthtech-startup-without-a-medical-degree

19. The Solitary Architect: Executive Isolation in Entrepreneurship

20. The 2026 Guide to Launching a SaaS as a Solo Developer

21. What Sustainable Growth Actually Looks Like

🔗 https://findnstart.com/blogs/what-sustainable-growth-actually-looks-like

22. The Early Warning Signs Your Startup Is in Trouble

🔗 https://findnstart.com/blogs/the-early-warning-signs-your-startup-is-in-trouble

23. How to Grow Without Burning Out

🔗 https://findnstart.com/blogs/how-to-grow-without-burning-out

24. The Truth About “Runway” Most Founders Ignore

🔗 https://findnstart.com/blogs/the-truth-about-runway-most-founders-ignore

25. Revenue Solves More Problems Than Funding

🔗 https://findnstart.com/blogs/revenue-solves-more-problems-than-funding

26. What No One Tells You About Being a Solo Founder

🔗 https://findnstart.com/blogs/what-no-one-tells-you-about-being-a-solo-founder

27. Why Smart People Quit High-Paying Jobs to Build Startups (And Why Most Regret It)

28. Why Most Startup Advice on Twitter Is Dangerous

🔗 https://findnstart.com/blogs/why-most-startup-advice-on-twitter-is-dangerous

29. Decision Fatigue: The Silent Startup Killer

🔗 https://findnstart.com/blogs/decision-fatigue-the-silent-startup-killer

30. Fear vs Logic: How Founders Actually Make Decisions

🔗 https://findnstart.com/blogs/fear-vs-logic-how-founders-actually-make-decisions

31. How Overthinking Destroys Early Momentum

🔗 https://findnstart.com/blogs/how-overthinking-destroys-early-momentum

32. Ideas Don’t Scale. Systems Do.

🔗 https://findnstart.com/blogs/ideas-dont-scale-systems-do

33. The First Hire That Actually Matters

🔗 https://findnstart.com/blogs/the-first-hire-that-actually-matters

34. How the First 100 Users Decide Your Startup’s Fate

🔗 https://findnstart.com/blogs/how-the-first-100-users-decide-your-startups-fate

35. Why Your Startup Doesn’t Need Growth — It Needs Focus

🔗 https://findnstart.com/blogs/why-your-startup-doesnt-need-growthit-needs-focus

36. Why Most Startups Die Quietly

🔗 https://findnstart.com/blogs/why-most-startups-die-quietly

37. Lessons Learned Too Late by First-Time Founders

🔗 https://findnstart.com/blogs/lessons-learned-too-late-by-first-time-founders

38. The Myth of the “Overnight Success” Startup

🔗 https://findnstart.com/blogs/the-myth-of-the-overnight-success-startup

Protect Your Future: The Precision Vesting Calculator

Don't let a "handshake deal" complicate your exit. Map out your ownership journey with our Vesting Calculator

Calculate Your Vesting Schedule →