Why Many Canadian Startups Expand to the US Early

July 2, 2026 by Harshit Gupta

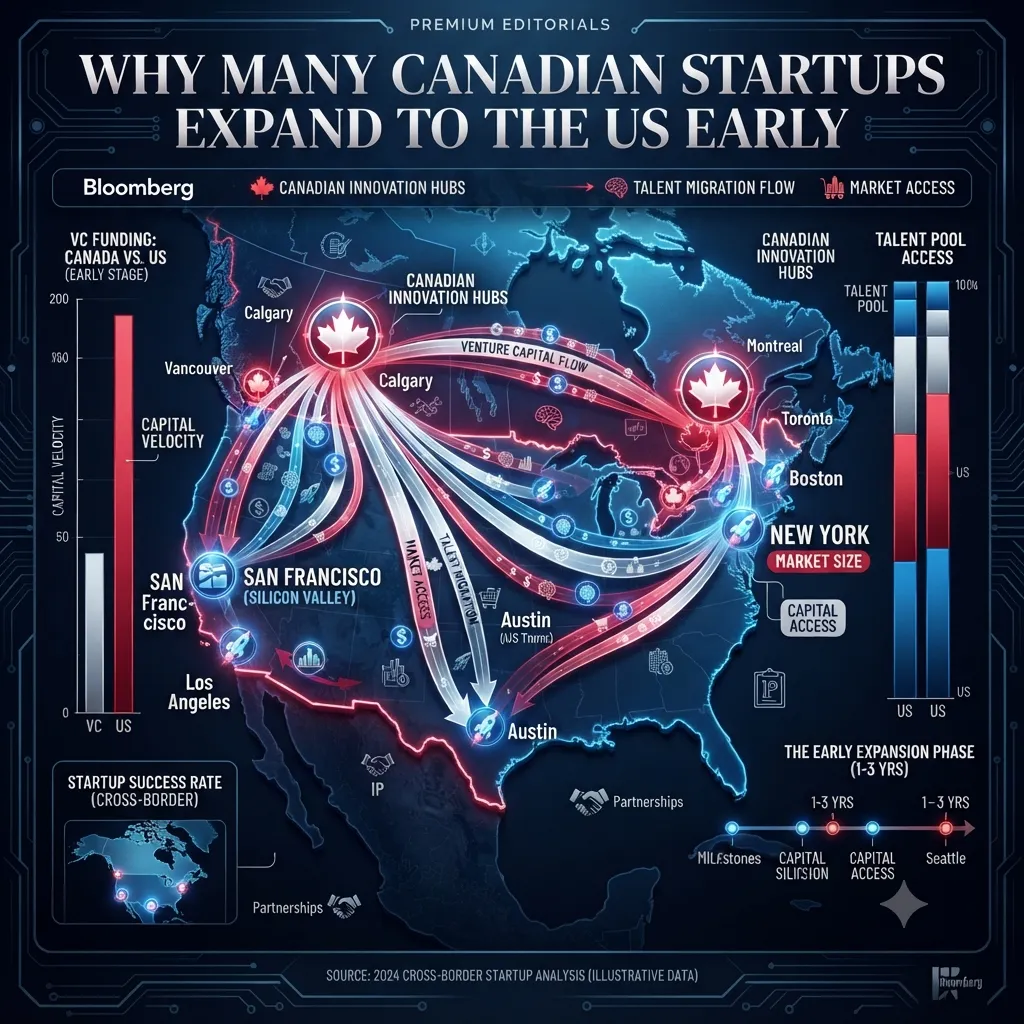

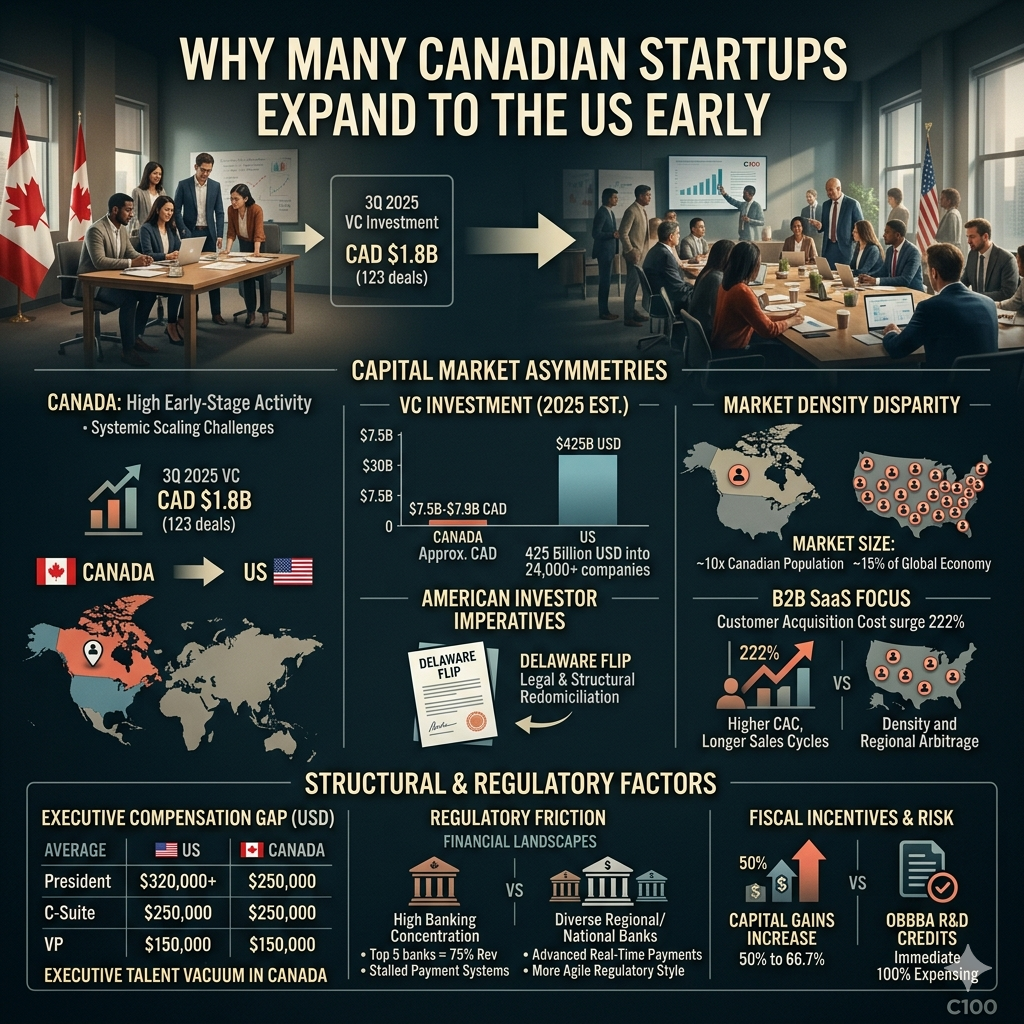

The trajectory of the Canadian technology ecosystem is increasingly defined by a dualistic reality: while Canada possesses the highest level of early-stage entrepreneurial activity among G7 nations, it simultaneously faces a systemic challenge in retaining its high-potential ventures as they transition toward global scale. This phenomenon, colloquially termed the "southward migration," is not merely a choice of geographic preference but a complex, multi-dimensional imperative driven by capital market asymmetries, structural legal requirements, and profound disparities in market density. As of 2025, the motivation for early expansion into the United States has evolved from a simple pursuit of larger customer bases into a comprehensive strategic necessity involving the redomiciliation of corporate entities, the relocation of executive leadership, and the navigation of increasingly divergent fiscal and regulatory landscapes.

Market Scale and the Economics of Proximity

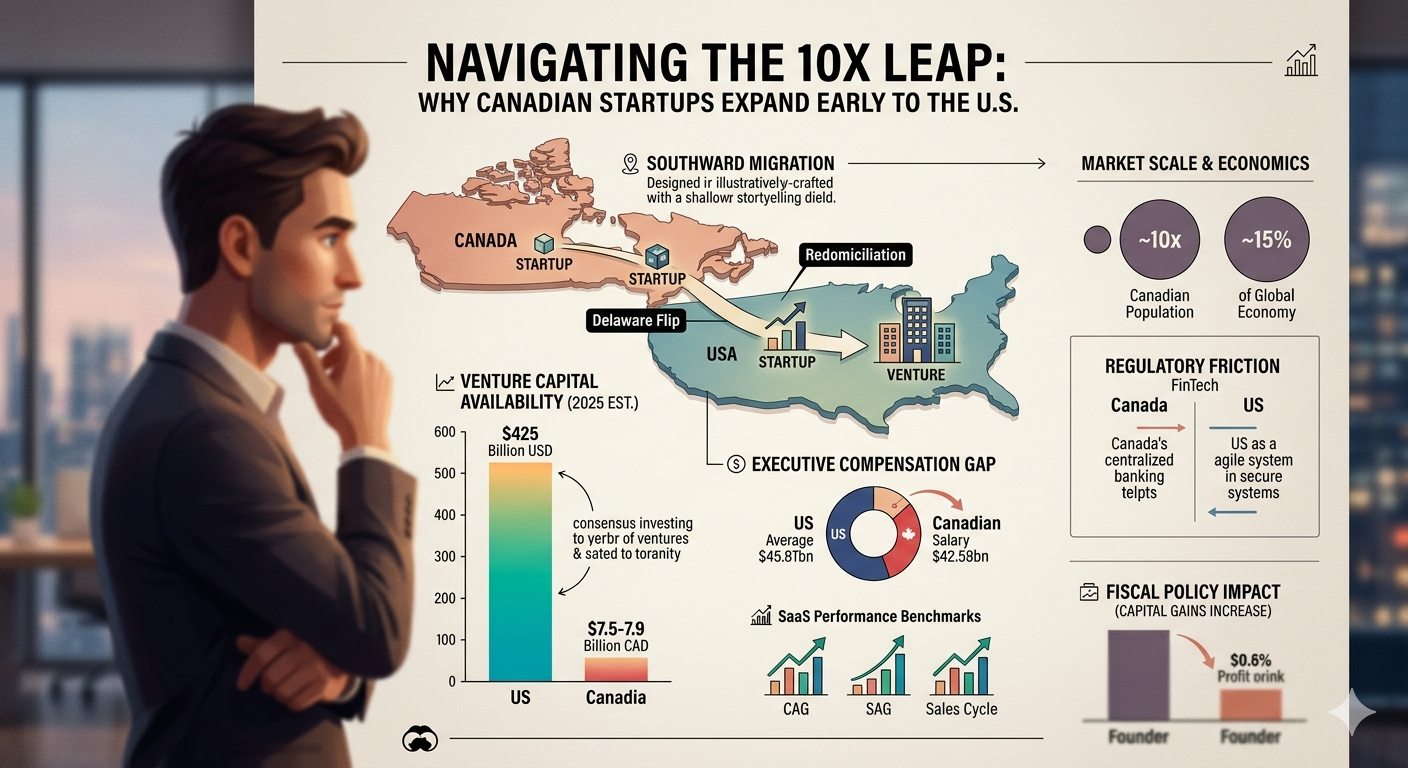

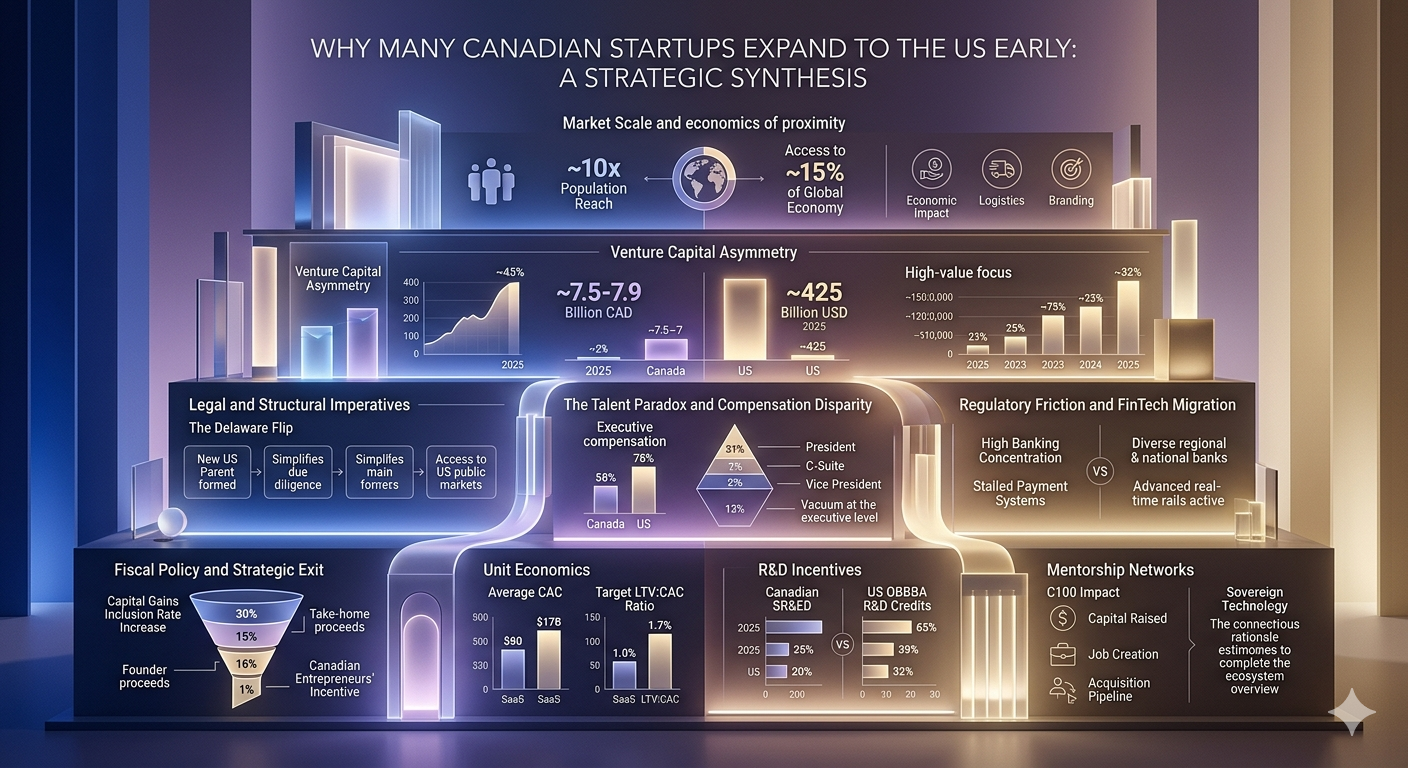

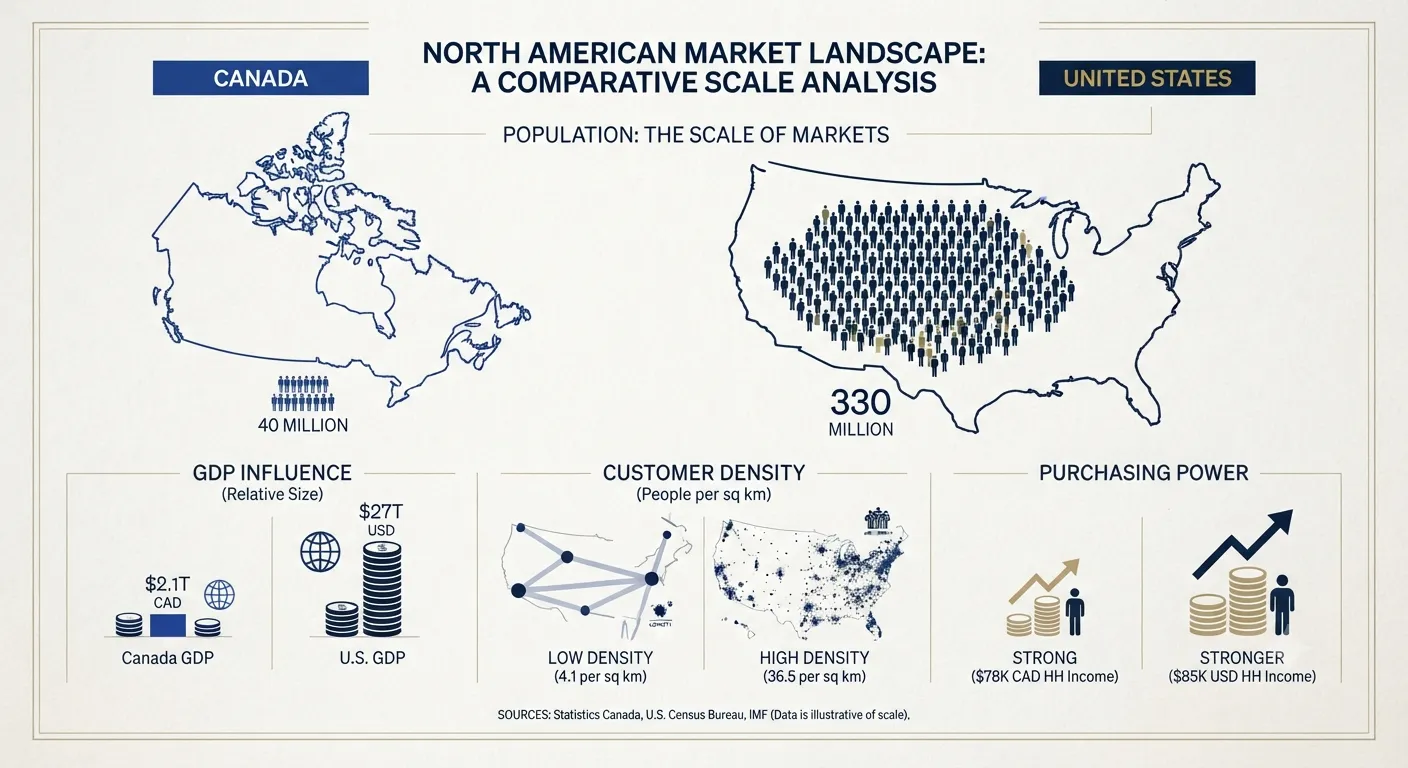

The fundamental driver for Canadian startups expanding into the United States is the pursuit of a market that is ten times larger than the domestic Canadian landscape. With nearly 330 million people and representing approximately 15% of the global economy, the United States remains the wealthiest and most influential consumer and enterprise market in the world. For Canadian business owners, the domestic scale often proves insufficient to support the high-growth requirements of venture-backed models, particularly in sectors such as software-as-a-service (SaaS) and artificial intelligence (AI), where market penetration and volume are the primary determinants of survival.

Strategic Market Dimensions and Cross-Border Advantages

Expansion Driver | Economic Impact/Metric | Strategic Benefit |

Population Reach | ~10x Canadian Population | Access to a market of 330 million people. |

Global GDP Share | ~15% of Global Economy | Engagement with the world's richest consumer base. |

Branding | "Made in the U.S." Label | Mitigates skepticism regarding foreign companies. |

Logistics | Bridge & Duty Reduction | Lowers costs associated with international crossings. |

Procurement | US Government Contracts | Ability to compete for military and federal deals. |

The proximity to the border allows for unique logistical advantages that reduce the friction of expansion. For instance, regions such as Buffalo Niagara have emerged as critical "landing spots" for Canadian firms. By establishing a presence in these border regions, Canadian startups can manage dual-country operations while hiring a similar workforce and benefiting from lower hydropower and real estate costs. This geographic strategy also addresses the significant "bridge costs"—duties, taxes, and delays associated with international shipping—that often hamper the competitiveness of Canadian products in the American market.

Beyond logistics, the expansion is often a response to American buyer psychology. U.S. customers frequently demonstrate skepticism toward doing business with foreign entities, even those from a neighboring ally like Canada. Establishing a physical U.S. office or manufacturing site allows a company to brand itself as "American," which is often a prerequisite for winning lucrative government and military contracts. Furthermore, the lack of technological adoption in some traditional Canadian firms forces more innovative startups to seek the U.S. market, where operational efficiency and robust online presence are standard expectations for doing business.

The Venture Capital Asymmetry: A Structural Funding Gap

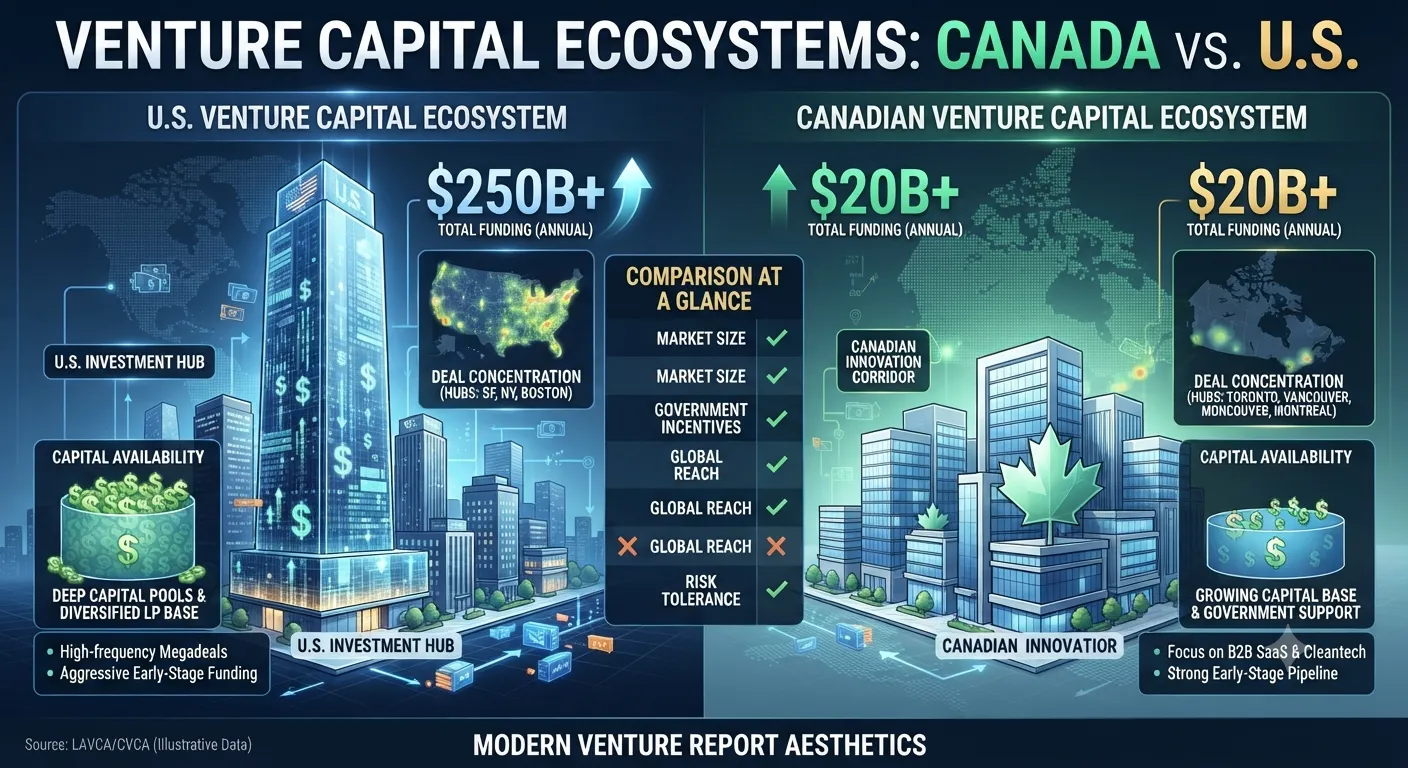

The migration of Canadian startups is fundamentally accelerated by a severe imbalance in the availability of venture capital. While the Canadian venture market has shown resilience, with investment reaching CAD $1.8 billion across 123 deals in the third quarter of 2025, it remains dwarfed by the massive scale of the American investment ecosystem. In 2025, U.S. venture and growth investors deployed $425 billion into over 24,000 private companies, marking the third-highest financing year on record.

Comparative Venture Capital Activity (2025 Estimates)

Region | Total Capital Invested | Deal Count (Approx.) | Trend Analysis |

Canada | ~$7.5 - $7.9 Billion CAD | ~500 - 600 | Worst fundraising year since 2016. |

United States | ~$425 Billion USD | ~24,000+ | 30% increase year-over-year. |

High-Value Focus | ~60% in Large Deals | 629 Deals > $100M | High capital concentration in U.S.. |

The year 2025 was characterized as a "perfect storm" for Canadian venture capital fundraising, which nosedived to its lowest level since 2016. Only 21 Canadian VC funds collectively raised nearly $2.1 billion CAD from limited partners (LPs), a figure that signals a significant dearth of available capital for domestic tech startups. This decline is attributed to a lack of exits (M&A and IPOs), macroeconomic uncertainty, and a shift in LP sentiment toward more established firms with longer track records. In Canada, capital concentration has reached a critical point, with the five largest VC funds capturing 83% of all capital raised in 2025, leading to "consensus investing" and a reduction in support for emerging managers.

For high-potential Canadian startups, the necessity of moving to the U.S. is often a direct result of this capital vacuum. American investors contributed to a third of all Canadian deals by volume in 2024 and accounted for an estimated 40% of the total VC investment value in the country. However, as geopolitical tensions and trade uncertainties rise, there is a persistent risk that this foreign capital will pull back, forcing late-stage Canadian companies to either relocate or face acquisition by foreign buyers to survive. The data indicates that in 2024, nearly half of Canadian founders who raised $1 million or more chose to build their companies abroad, primarily in the U.S., where the ratio of high-potential startups produced is now 45 times higher than in Canada.

Legal and Structural Imperatives: The Delaware Flip

For many startups, expansion into the U.S. is not a voluntary strategic move but a mandatory legal requirement imposed by American investors. The "Delaware Flip" is a corporate reorganization where a new U.S. parent company—typically a Delaware C-Corporation—is formed to hold 100% of the shares of the original Canadian company. This structure is designed to align the startup with the governance, tax, and intellectual property (IP) preferences of U.S. venture capitalists.

The Rationale for Redomiciliation

American investors generally demand a Delaware structure for several reasons:

Legal Familiarity: Delaware has a highly sophisticated and respected corporate legal regime, which simplifies due diligence and long-term governance.

IP Protection: Establishing a clear IP ownership structure under U.S. law is often a prerequisite for large-scale investment.

Exit Opportunities: A U.S. holding company provides easier access to U.S. public markets and a larger pool of potential buyers who may only be interested in acquiring domestic entities.

The flip is most common at the Seed or Series A stages, as the process becomes prohibitively expensive and complex as a company matures. Accelerators such as Y Combinator have recently formalized this trend, moving to no longer invest in Canadian-domiciled businesses, thereby requiring startups to redomicile in the U.S. as a condition of participation. While some industry leaders argue that this change simply "formalizes the inevitable," it exerts significant economic force on the Canadian tech sector, fueling a "Valley or bust" mindset among young entrepreneurs.

However, the Delaware Flip carries significant risks and costs. Legal fees can exceed $25,000 USD, and the transaction is often irreversible from a tax perspective. It exposes the startup to U.S. litigation risks and a dual compliance burden, as the company must adhere to both Canadian and U.S. regulations. Furthermore, it may result in a higher effective tax rate and complex transfer-pricing implications. Despite these drawbacks, the "flip" remains the primary foundation for Canadian startups looking to access the vast U.S. venture market.

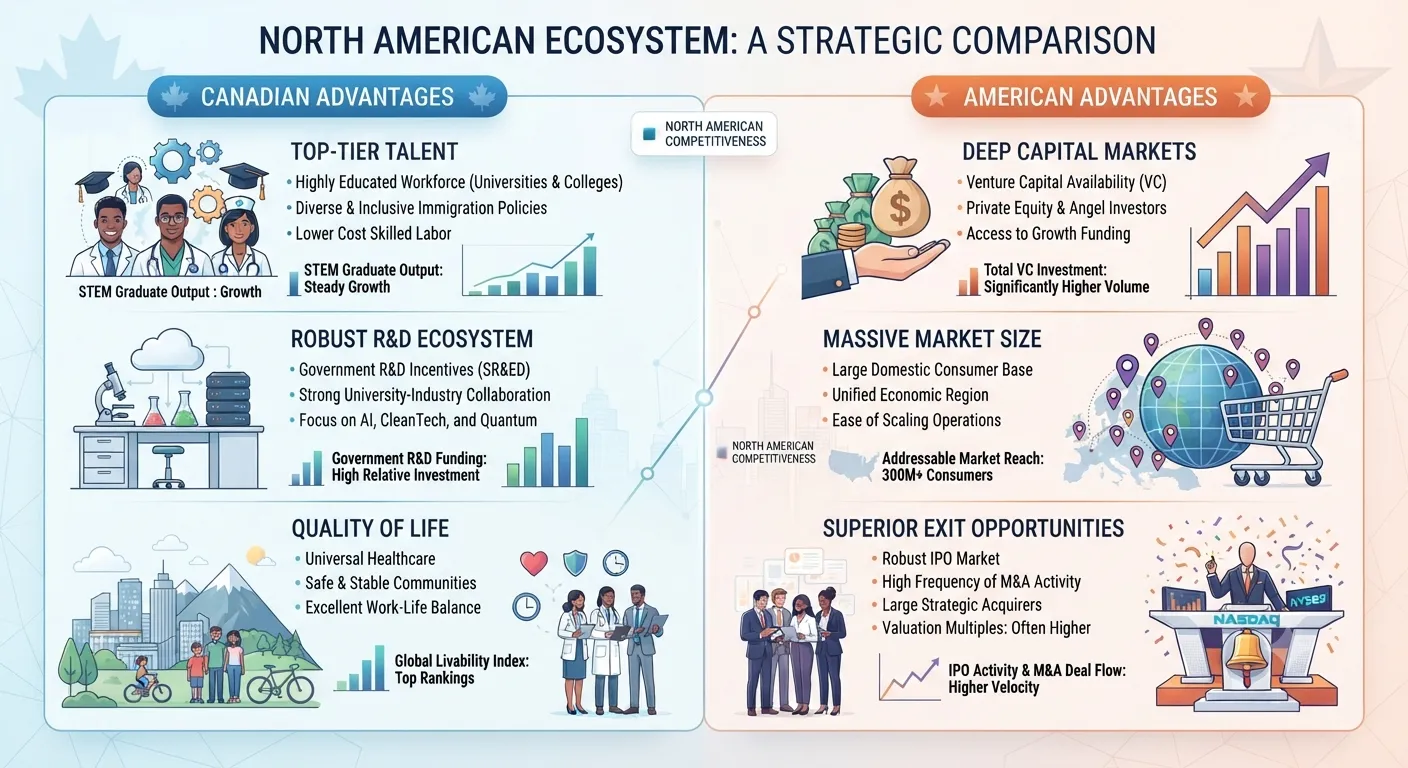

The Talent Paradox and Compensation Disparity

A critical, often overlooked factor in early U.S. expansion is the disparity in executive leadership talent and compensation between Canada and the United States. While Canada has an abundance of skilled tech workers and a growing pool of STEM graduates, it faces a significant "vacuum" at the executive level. There is a noted shortage of leaders with experience in scaling companies from mid-sized startups to multi-billion dollar global giants, particularly those who have navigated public listings or major international mergers.

The Executive Compensation Gap (USD)

Role | U.S. Average Compensation | Canada Average Compensation | Disparity |

President | US$ 320,000+ | US$ 250,000 | US$ 70,000. |

C-Suite Executive | US$ 285,000+ | US$ 200,000 | US$ 85,000. |

Vice President | US$ 260,000+ | US$ 168,000 | US$ 92,000. |

Total Average | US$ 277,000 | US$ 190,000 | US$ 87,000. |

The average Canadian tech executive earns US$87,000 less than their American counterpart, a gap that persists regardless of funding stage, sector, or the amount of capital raised. This compensation chasm makes it increasingly difficult for Canadian firms to compete for world-class talent, as U.S. firms not only raise more capital in total but also raise significantly more capital per employee, allowing for more aggressive resource allocation toward talent.

Furthermore, Canada's immigration system, while robust in quantity, is criticized for relying on "proxies" like formal degrees rather than assessing practical ability, creating a disconnect between the labor pool and employer needs. This has led to a scenario where 70% of Canadian businesses report a shortage of skilled workers in high-demand fields like AI and cybersecurity, despite a cooled overall job market. As a result, many Canadian startups expand to the U.S. to access "ready" talent—executives who have already gone through the cycles of growth and exit that are less common in the Canadian ecosystem. Conversely, the presence of foreign tech multinationals in Canada (such as FAANG companies) serves as a training ground for future Canadian entrepreneurs, equipping them with the best practices in software development and operations necessary to launch their own ventures.

Regulatory Friction and the FinTech Migration

Regulatory environments also play a decisive role in the decision to expand early. Canada's financial sector is highly concentrated, with the top five banks controlling three-quarters of the market revenue. While this structure provided stability during global crises, it has also "stifled growth and innovation," making Canada a laggard in real-time payments and open banking.

Regulatory and Banking Landscape Comparison

Feature | Canada | United States |

Banking Concentration | High (Top 5 banks = 75% Rev) | Low (Diverse regional & national banks). |

Regulatory Style | Principle-based/Ambiguous | More agile/Responsive to FinTech. |

Payment Systems | Stalled (Real-time payments pending) | Advanced (Real-time rails active). |

FinTech Hurdles | Slow onboarding, limited core access | Banks eager to innovate & partner. |

Canadian FinTechs like Zum Rails have cited the "larger, more competitive FinTech landscape and banks eager to innovate" as primary reasons for expanding into the U.S.. The Canadian regulatory framework is often perceived as ambiguous, offering "guardrails" but no "detailed map," which creates high hurdles for emerging startups. Consequently, Canadian founders often view the U.S. as a more favorable environment for validating their products and achieving rapid adoption, as American institutions are more accustomed to the balance between innovation and compliance.

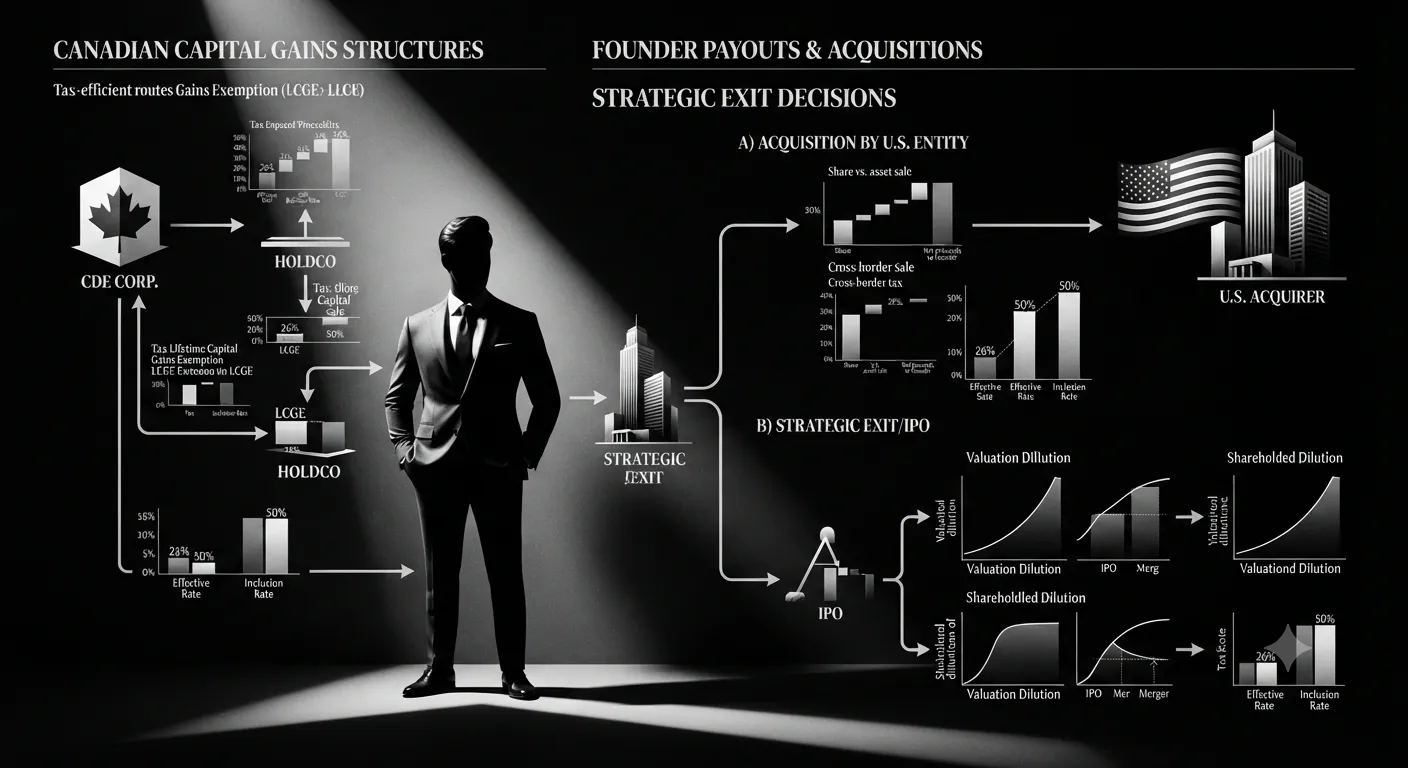

Fiscal Policy and the Strategic Exit

The 2024 and 2025 Canadian federal budgets introduced significant changes to the fiscal landscape that have further incentivized early expansion and influenced exit timelines. The most notable change was the increase in the capital gains inclusion rate from one-half (50%) to two-thirds (66.7%) for gains exceeding CA$250,000 realized by individuals, and for all gains realized by corporations and trusts.

The Fiscal Math of a Startup Exit

For a SaaS founder, the increase in the capital gains rate represents a substantial reduction in the take-home proceeds from a sale or acquisition. Analysis suggests that selling a business in 2025 rather than 2026—when the new rate is fully implemented—could result in a founder taking home 16% more in net proceeds. If a company is growing at a moderate pace, the founder may find that another year of risk only serves to "break even" after the higher taxes are applied.

Policy Component | Threshold/Rate | Strategic Impact for Founders |

Inclusion Rate Increase | 50% to 66.7% | Increases tax burden on exits > $250k. |

Lifetime Cap. Gains Exempt. | $1.25 Million | Benefit for qualifying small business shares. |

Cdn Entrepreneurs' Incentive | $2 Million (at 33.3% Rate) | Phased-in relief for eligible sectors. |

Employee Stock Options | Better treatment in CCPCs | Critical for retaining Canadian talent. |

While the government introduced the Canadian Entrepreneurs' Incentive (CEI) to reduce the inclusion rate to 33.3% on a lifetime maximum of $2 million in capital gains, the exclusion of many sectors—including finance and insurance—limits its effectiveness for the broader tech ecosystem. These fiscal pressures, combined with a functionally paused IPO market in Canada, make the "allure of U.S. acquisition" almost impossible to resist for many founders who are looking to realize the value of their ventures.

Unit Economics: CAC, Density, and the SaaS Scaling Metric

The economics of customer acquisition also dictate early U.S. expansion. In the B2B SaaS sector, the average customer acquisition cost (CAC) has surged by 222% over the past eight years, reaching a baseline of approximately $1,200 per customer in 2025. In Canada, the geographic dispersion of customers often leads to higher CAC ratios and longer sales cycles compared to the denser tech hubs in the U.S..

SaaS Performance Benchmarks (2025-2026 Estimates)

Segment | Average CAC | Sales Cycle | Target LTV:CAC Ratio |

Small Business SaaS | $100 - $400 | 1 - 3 Months | 4:1 to 6:1. |

Mid-Market SaaS | $400 - $800 | 3 - 6 Months | 4:1 to 7:1. |

Enterprise SaaS | $800+ | 6+ Months | 4:1 to 10:1. |

Fintech SaaS | $1,450 - $14,700 | 6+ Months | High LTV requirements. |

Canadian startups frequently struggle with "decreasing revenue growth efficiency," spending upwards of $2.00 in sales and marketing to acquire $1.00 of new annual recurring revenue (ARR). Expanding to U.S. markets provides access to higher customer density and "regional arbitrage" opportunities. For instance, while West Coast markets run 15-25% above average costs, Midwest and Southern hubs like Austin and Miami offer similar quality talent and market access at 10-20% discounts. These hubs have become "magnets" for Canadian founders due to their no-state-income-tax policies, business-friendly regulations, and supportive entrepreneurial ecosystems.

R&D Incentives: SR&ED vs. the US OBBBA

A significant portion of Canadian startup strategy is built around the Scientific Research and Experimental Development (SR&ED) tax credit, which is often the difference between extending a runway and "scrambling for capital". In 2025, the Canadian federal budget implemented the most significant changes to SR&ED in a decade, doubling the expenditure limit from $3 million to $6 million and restoring eligibility for capital expenditures (such as hardware and AI infrastructure).

SR&ED 2025 Update vs. US R&D Credits

Feature | New Canadian SR&ED (2025) | US R&D Credit (OBBBA 2025) |

Expenditure Limit | $6 Million (at 35% Refundable) | No cap; 100% immediate expensing. |

Refundability | Cash payout even if no tax owed | Payroll tax offsets for startups. |

Capital Assets | Eligible (Servers, GPUs, Lab gear) | Included in domestic R&D expensing. |

Structural Impact | Includes public companies | Amortization removed for domestic R&D. |

While these Canadian enhancements are "founder-friendly," the U.S. countered with the "One Big Beautiful Bill Act" (OBBBA) in July 2025. OBBBA restored immediate 100% expensing for domestic R&D, reversing the 2017 requirement to amortize costs over five years. This change removes a critical cash flow barrier for U.S.-based startups, slashing effective R&D costs by 15-25% when combined with other tax credits. For a Canadian startup, the choice often comes down to the refundable cash of SR&ED (which favors lean technical teams) versus the massive scaling capacity and immediate tax relief offered by the U.S. regime for capital-intensive R&D.

Mentorship Networks and the Diaspora Influence

The decision to expand to the U.S. early is also heavily influenced by structured mentorship networks such as C100. C100, which includes over 400 Canadian CEOs and executives based in major tech hubs like Silicon Valley, acts as an "indispensable resource" for founders looking to scale globally. Programs like "48Hrs in the Valley" provide high-potential Canadian founders with unparalleled access to a "risk-embracing community" and Silicon Valley's best practices.

The impact of these networks is significant:

Capital Raised: C100 fellowship companies have collectively raised over $13.2 billion in venture funding.

Job Creation: These companies have created more than 23,000 jobs, primarily in Canada and the U.S..

Acquisition Pipeline: Alumni ventures have a high rate of successful exits, with 26% of Fellows companies being acquired by major players like Apple, Autodesk, and Instacart.

These networks effectively act as a bridge, lowering the "fear of failure"—which 53% of Canadians cite as a barrier to entrepreneurship—by providing direct connections to a "mastermind" of seasoned operators who have successfully navigated the U.S. market. For founders, being part of these communities ensures they are "never alone" on an entrepreneurial journey that almost inevitably leads through the United States.

Sovereign Technology and the Resilience Movement

Despite the powerful allure of the U.S., a growing movement in Canadian policy circles emphasizes "sovereign tech" as a counter-strategy. The realization that Canada's critical infrastructure—from energy grids to cloud services—is heavily dependent on American entities has prompted a shift toward building and buying Canadian. In 2025, reports highlighted that the top three cloud providers for the Canadian government and business (Microsoft, AWS, Google) are subject to the U.S. CLOUD Act and Patriot Act, meaning Canada does not have full sovereignty over its data.

Sovereign Capability Rationale

Challenge | Impact on Tech Ecosystem | Proposed Solution |

Talent Retention | Talent recruited by U.S./China | Tie fellowships to Canadian employment. |

IP Ownership | IP leaves Canada via foreign VCs | National Sovereignty Fund (NSF). |

Data Residency | Subject to foreign law (CLOUD Act) | Sovereign Canadian Cloud initiative. |

Deep Tech | Steps change in security/dual-use | Patient capital for "Dual-Use" firms. |

This movement advocates for a "National Sovereignty Fund" (NSF) that would provide "patient capital" to scale companies at home before they are bought abroad. Success stories like Shopify, Clio, and Cohere serve as case studies for this resilience. Shopify's leadership famously resisted pressure to move to the U.S. during their Series A, instead finding partners content to let them build in Canada. Cohere's co-founder Aidan Gomez recently noted that "acquisition is failure," arguing that moving companies outside the country is unsavory and that entrepreneurs should "fight to appease VCs to keep their Canadian headquarters".

The Integrated Future: A Strategic Synthesis

The early expansion of Canadian startups to the United States is the result of a multifaceted "gravitational pull" that combines economic necessity with structural and legal requirements. While the "10x factor" of market size remains the primary motivator, the systemic issues of capital concentration, compensation disparities, and regulatory friction ensure that the U.S. market will remain the "gold standard" for Canadian scaling.

However, the 2025-2026 period marks a potential inflection point. The combination of enhanced domestic R&D incentives (SR&ED), the rise of "sovereign tech" initiatives, and a new generation of founders who view domestic headquarters as a point of pride may begin to stem the tide. For professional peers in the investment and startup communities, the path forward requires a nuanced understanding of these cross-border mechanics—leveraging the capital and market depth of the United States while maintaining the technical talent and operational efficiency that have made Canada a global leader in early-stage innovation. The successful startup of the future will not necessarily "leave" Canada or "stay" in Canada, but will instead operate as a truly North American entity, strategically allocating its resources across both borders to maximize growth, resilience, and sovereign value.

Want to calculate the equity for your cofounder?

Nail your cap table before you sign. Whether you're splitting equity with a co-founder or planning your next funding round, our Equity Calculator gives you precision in seconds

Equity calculator →