Why Canadian Startups Often Relocate Headquarters

March 13, 2026 by Harshit Gupta

The migration of corporate headquarters from Canada to the United States represents a multifaceted strategic phenomenon driven by a complex interplay of capital scarcity, legal necessity, and market-scale imperatives. While the Canadian innovation landscape has matured significantly over the last two decades, particularly in the Toronto-Waterloo Corridor, Montreal, and Vancouver, it continues to grapple with structural imbalances that frequently necessitate a southward relocation for firms entering their hyper-growth phases. This shift is not merely a tactical maneuver for proximity to customers; it is an foundational realignment involving the navigation of disparate legal jurisdictions, tax regimes, and institutional investor preferences. As the venture capital environment in 2025 entered what industry analysts termed a "perfect storm" of contraction, the pressures on Canadian founders to secure American lifelines transitioned from a growth-oriented choice to an existential requirement.

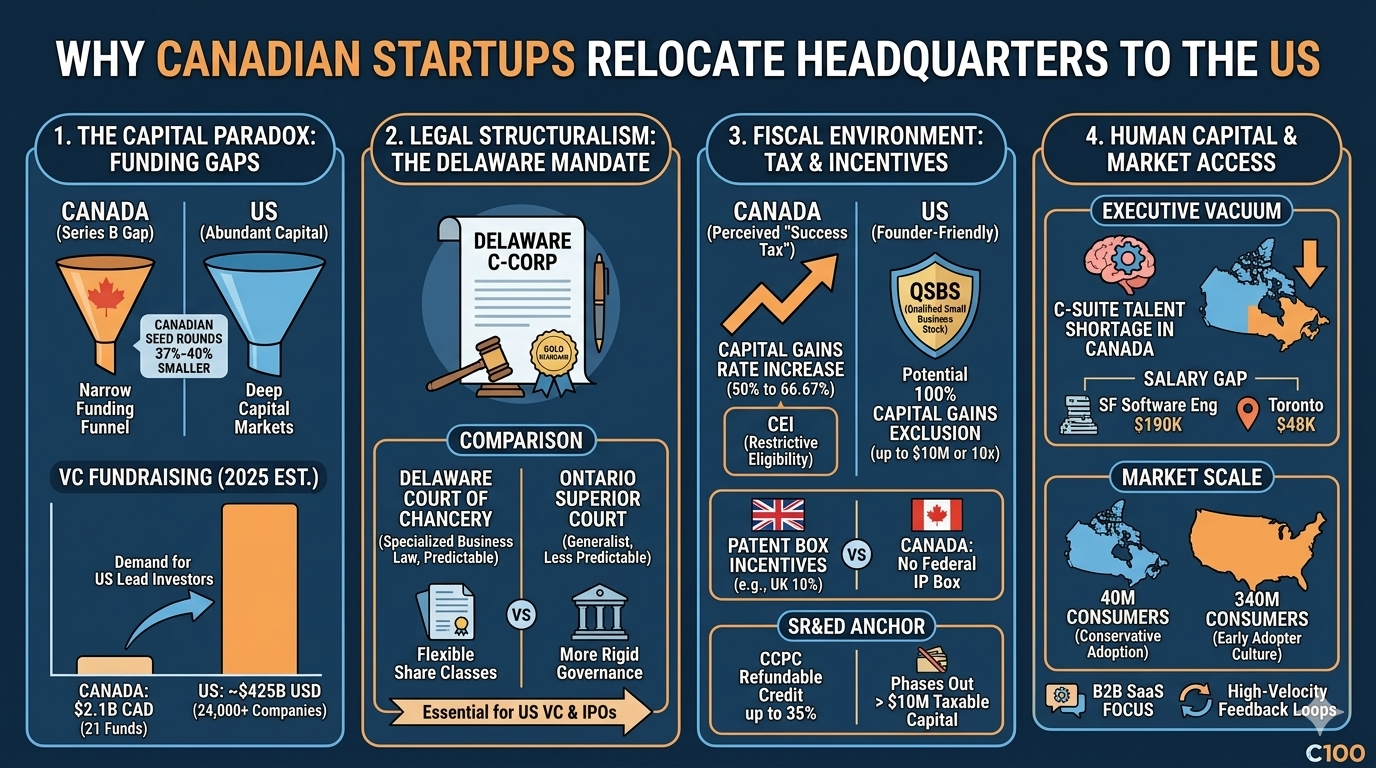

The current ecosystem is characterized by a "capital paradox" where world-class early-stage research and talent development are met with a narrowing funding funnel as companies attempt to navigate the "Series B gap." The implications of this paradox are profound, resulting in a systemic drain of high-potential ventures that incorporate in Delaware or relocate to Silicon Valley and New York to satisfy the requirements of global institutional investors. Understanding this relocation trend requires an exhaustive examination of the macroeconomic climate, the specialized legal protections afforded by U.S. jurisdictions, the nuances of cross-border fiscal policy, and the persistent executive talent vacuum that continues to hinder domestic scale-up efforts.

The Capital Paradox: Structural Gaps and the 2025 Market Contraction

The primary driver of headquarters relocation remains the profound disparity in the depth and velocity of capital markets between Canada and the United States. In 2025, the Canadian venture capital (VC) landscape experienced its most challenging fundraising year since 2016, with a mere 21 funds collectively raising approximately $2.1 billion CAD. This figure represents a 39% decline from the $3.4 billion raised in 2024, signaling that the modest post-pandemic recovery was short-lived. The contraction was driven by a scarcity of exits, as the drought in initial public offerings (IPOs) and mergers and acquisitions (M&A) left limited partners (LPs) with little liquidity to reinvest in the asset class.

The concentration of capital within the domestic market has further intensified these pressures. In 2025, the five largest Canadian venture funds captured a staggering 83% of all capital raised, creating a "top-heavy" ecosystem that fosters consensus-driven investing and leaves emerging managers—who typically back early-stage, high-risk innovation—critically underfunded. Emerging managers raised just $249 million in 2025, the lowest annual amount on record, which directly impacts the "roots" of the startup pipeline. When early-stage funds cannot raise successor capital, they are unable to provide the "follow-on" funding required for their portfolio companies to reach maturity, effectively forcing those companies to seek U.S. lead investors who often demand a headquarters relocation as a condition of investment.

Comparative Metrics of the Venture Capital Fundraising Environment (2024–2025)

Metric | 2024 Performance | 2025 Performance | Percentage Change |

Total Capital Raised (CAD) | $3.4 Billion | $2.1 Billion | -38.2% |

Number of Funds Closed | 22 | 21 | -4.5% |

Emerging Manager Capital (CAD) | >$400 Million | $249 Million | -37.8% (approx) |

Share of Capital (Top 5 Funds) | High | 83% | N/A (Increase) |

Median Fund Size (CAD) | ~$35 Million | $29 Million | -17.1% |

Top-Quartile Fund Size (CAD) | ~$140 Million | $43 Million | -69.3% |

This capital concentration is not an isolated event but part of a broader structural weakness at the top of the funding funnel. A landmark report from the National Angel Capital Organization (NACO) and Startup Genome revealed that Canada's top startup ecosystems—Toronto-Waterloo, Vancouver, and Montreal—have collectively lost an estimated $66 billion USD in ecosystem value since their respective peaks. This loss is measured by the country’s declining market share of global startup funding and exits. While the global startup economy grew at a compound annual growth rate (CAGR) of 9.5% between 2019 and 2024, Canada’s ecosystem expanded by only 2.2%, lagging significantly behind peers like the United Kingdom (13%) and France (17%).

The discrepancy in funding round sizes further highlights the competitive disadvantage faced by Canadian-based firms. Median seed rounds for Canadian startups are 37% to 40% smaller than comparable rounds in Tier-1 U.S. ecosystems, a gap that has widened since 2017. Smaller initial rounds restrict the ability of founders to compete for top-tier engineering talent and lengthen the timeline required to reach product-market fit. Consequently, Canadian startups take an average of five additional months to close a seed round and 13 months longer to reach Series A compared to their American counterparts. For many founders, the only way to escape this "sluggish growth" cycle is to move the headquarters to a jurisdiction where capital deployment is more aggressive and round sizes are sufficient to support global expansion.

Structural Shortfall in Early-Stage Financing Rounds

Funding Stage | Median Round Size Gap (Canada vs. US) | Estimated Annual Shortfall (USD) | Timeline to Close (Days Longer than US) |

Pre-Seed / Seed | 37%–40% Smaller | $141 Million | +150 Days |

Series A | Varies | $181 Million | +390 Days |

AI-Native Startups | 50% Smaller | N/A | Significantly Longer |

The impact is particularly acute for AI-native startups, which represent 20% of new Canadian firm formations but raise roughly half the seed funding of their U.S. peers. This funding gap at the "roots" of the ecosystem has a downstream effect: fewer seed-backed companies translate into fewer startups reaching Series A, fewer breakout success stories, and ultimately, a continued reliance on U.S. acquisition as the "gold standard" for an exit.

Legal Structuralism: The Delaware Mandate and Jurisdictional Allure

Beyond the availability of liquidity, the legal architecture of a startup is a primary consideration for institutional investors. The preference for incorporating as a Delaware C-Corporation is deeply embedded in the venture capital world, serving as a "global gold standard" that provides a predictable and efficient environment for resolving complex corporate disputes. For Canadian startups seeking U.S. venture capital or an eventual IPO on the NASDAQ or NYSE, incorporation in Delaware is often non-negotiable.

The primary legal pull factor is the Delaware Court of Chancery, a specialized non-jury court that focuses exclusively on business law cases. Decisions are made by judges who are experts in corporate law, rather than juries, which ensures that judicial outcomes are more predictable than in general jurisdiction courts. This predictability is a critical risk-mitigation factor for investors who want to ensure that their rights—such as preferred share protections and liquidation preferences—will be interpreted according to a well-established body of case law.

Comparative Legal and Governance Frameworks

Governance Feature | Delaware (C-Corp) | Ontario (OBCA) |

Legal System | US Common Law / DGCL | Canadian Common Law / OBCA |

Specialized Court | Court of Chancery (Corporate expertise) | Superior Court of Justice (Generalist) |

Fiduciary Duty | Primary duty to shareholders | Duty to the corporation (Stakeholder approach) |

Capital Flexibility | Seamless issuance of multiple share classes | More rigid; statutory minority rights |

Director Requirements | No residency or shareholding required | 25% Canadian residency requirement |

Privacy Protection | No disclosure of officer/director names | Public disclosure required |

Liability Veil | Strong limited liability; rare veil-piercing | Standard liability protections |

Delaware's General Corporation Law (DGCL) offers unmatched flexibility in structuring a company's internal governance. It allows for the easy issuance of multiple classes of stock with tailored rights, which is essential for managing the complex cap tables that result from multiple rounds of venture financing. In contrast, the Ontario Business Corporations Act (OBCA), while robust, is perceived as being more rigid and offering stronger statutory rights to minority shareholders, which can occasionally complicate the fast-paced pivots and restructuring often required by high-growth firms.

The "prestige" of being a Delaware corporation also serves as a market signal. It communicates to the investment community and potential acquirers that the startup is a "national" or "global" company that adheres to marketplace preferences. Many investment banks will not attempt to take a company public unless it is incorporated in Delaware, as the state's legal framework is optimized for IPOs and secondary market transactions. Furthermore, Delaware allows one individual to hold multiple corporate roles—officer, director, and shareholder—which simplifies the early-stage administrative burden.

For international student founders or immigrant entrepreneurs in Canada, the legal decision to relocate is also tied to immigration policy hurdles. The Canadian "Startup Visa" program, while innovative, currently suffers from a reported 10-year wait time. Founders who cannot secure permanent residency while building their companies are often forced to move to the U.S., where pathways like the TN visa or L-1A visa (for intercompany transfers) provide more immediate solutions for key personnel who need to be physically present to scale the business. The case of "Internet Backyard," a startup founded by international students in Canada who moved to Delaware in 2025 to close their seed round, illustrates how the combined pressure of capital requirements and visa wait times can drive even Gen Z entrepreneurs out of the domestic ecosystem.

The Fiscal Environment: Tax Reform and the "Success Tax" Perception

Taxation policy serves as a powerful "push" factor when founders compare the net proceeds of an exit in Canada versus the United States. The 2024 Canadian federal budget introduced a controversial increase in the capital gains inclusion rate, raising it from 50% to 66.67% for individuals on annual gains exceeding $250,000. While the government introduced the "Canadian Entrepreneurs' Incentive" (CEI) to mitigate this impact for founders, the psychological effect has been a perception of an increased "success tax" on elite entrepreneurs.

The CEI aims to reduce the inclusion rate to 33.3% on a lifetime maximum of $2 million in eligible capital gains, which, when combined with the increased Lifetime Capital Gains Exemption (LCGE) of $1.25 million, provides up to $3.25 million in total or partial tax-free gains. However, the eligibility criteria for the CEI are restrictive. It requires founders to be "founding investors" who have held at least 10% of the shares for five years and for whom the company has been their principal employment. Many high-growth founders find their ownership diluted below the 10% threshold after multiple venture rounds, rendering them ineligible for the incentive at the time of exit.

Comparison of Effective Capital Gains Taxation on High-Value Exits

Exit Value (Total Gain) | Pre-2024 Budget Policy | Post-2024 Budget Policy | US Policy (QSBS Eligible) |

$1 Million | $500K Taxable | $0 (Exempt via LCGE) | $0 (Exempt via QSBS) |

$5 Million | $2.5M Taxable | ~$1.8M Taxable (w/ CEI) | $0 (Exempt via QSBS) |

$10 Million | $5M Taxable | ~$4.8M Taxable (w/ CEI) | $0 (Exempt via QSBS) |

$100 Million | $50M Taxable | ~$65M Taxable | ~$0–$18M (depending on QSBS) |

In the United States, the Qualified Small Business Stock (QSBS) program allows founders and investors to potentially exclude up to 100% of capital gains from federal taxes on the first $10 million or 10 times the original investment, whichever is greater. This creates a massive disparity for successful "serial entrepreneurs" who may build multiple $100-million-dollar companies. Analysis shows that while Canada may have an edge for smaller exits (under $6.25 million), the tax burden for large-scale "unicorns" is significantly higher than in the U.S., driving the most successful entrepreneurs to relocate their personal and corporate headquarters to U.S. jurisdictions before reaching a liquidity event.

Furthermore, the Canadian tax system lacks the "Patent Box" incentives common in Europe and the United Kingdom, where income derived from patented intellectual property (IP) is taxed at a significantly reduced rate (e.g., 10% in the UK vs. the standard 25%). While provinces like Quebec and Saskatchewan have introduced versions of an "IP Box," there is no federal equivalent to match the global competitiveness of jurisdictions that prioritize the commercialization phase of the R&D cycle. Without these "back-end" incentives, the Canadian system remains heavily weighted toward the "front-end" of innovation through the Scientific Research and Experimental Development (SR&ED) tax credit.

The SR&ED Anchor and the "Straddle" Strategy

The SR&ED program is the single most effective "anchor" keeping technical operations within Canada. As Canada’s largest R&D incentive, it provides more than $3 billion annually in tax assistance to upwards of 20,000 businesses. For a Canadian-Controlled Private Corporation (CCPC), the SR&ED credit is often refundable, returning up to 35% of eligible expenditures on the first $3 million of R&D investment. When combined with provincial supplements, the total tax subsidy can reach up to 65% of eligible R&D costs.

This creates a significant cost advantage for startups in the development stage. Research indicates that the average cost of a software developer in Toronto is approximately 4x lower than in San Francisco when accounting for salaries, perks, turnover costs, and SR&ED credits.

Estimated Annual Cost Comparison per Software Engineer (2024/2025)

Expense Category | San Francisco (USD) | Toronto (USD equivalent) |

Base Salary | $120,000 | $50,000 |

Perks and Benefits | $30,000 | $15,000 |

Cost of Turnover | $40,000 | $10,000 |

SR&ED Credit | $0 | (-$27,000) |

Total Cost | $190,000 | $48,000 |

This cost disparity has given rise to the "Delaware-CanCo Straddle," a hybrid corporate structure where the startup maintains a Canadian operating company (CanCo) to conduct R&D and claim SR&ED credits, while the parent headquarters is incorporated in Delaware to facilitate U.S. fundraising and sales. In this model, the CanCo often retains ownership of the IP to satisfy Canadian grant requirements (like IRAP), licensing it to the Delaware entity for use in the U.S. market. This allows the startup to benefit from the lower operational "burn rate" in Canada while maintaining the legal and financial infrastructure preferred by American investors.

However, the SR&ED program is not without its limitations. As a company grows and its taxable capital exceeds $10 million, the enhanced 35% refundable credit begins to phase out, disappearing entirely at $50 million. For a scaling firm, this creates a "cliff" where the financial incentive to remain a CCPC diminishes, often aligning with the same moment the company needs to raise a Series B or C round from U.S. investors. At this juncture, the administrative burden of maintaining the "straddle" may no longer be justified by the shrinking tax credits, prompting a full relocation of the headquarters and senior leadership to the U.S..

Human Capital: The Executive Vacuum and the Salary Gap

A critical but often overlooked driver of relocation is the "executive talent vacuum" in Canada. While the country excels at producing high-quality engineering talent—producing some of the most sought-after STEM graduates globally—it lacks a deep pool of leaders with experience scaling companies from $100 million to $10 billion in revenue. Roles such as Chief Revenue Officer (CRO), Chief Marketing Officer (CMO), and Chief Digital Officer (CDO) with "global giant" experience are in critically short supply.

When a Canadian startup reaches the scale where it needs these leaders, it almost invariably must recruit them from the United States. Once an executive team is predominantly U.S.-based, the gravity of the company's "center of mass" shifts. Boards often pressure founders to move the headquarters to follow the leadership, ensuring that the CEO and C-suite are co-located with their key peers and investors in hubs like San Francisco or New York. This is compounded by the fact that 70% of Canadian businesses report that a shortage of skilled workers is holding them back, despite Canada's high levels of skilled immigration.

The salary gap also drives a persistent "brain drain." Software developers in U.S. hubs can earn 2x to 3x the salary of their Canadian counterparts, a difference that far exceeds the higher cost of living in cities like San Francisco or Seattle. A survey by ComIT found that 64% of Canadian IT workers would consider moving to the U.S. for a similar job, citing better pay, more advanced tech infrastructure, and a lack of concern for employee well-being in domestic firms as primary motivations.

Talent Comparison: Toronto-Waterloo vs. Silicon Valley

Talent Metric | Toronto-Waterloo Corridor | Silicon Valley (Bay Area) |

Total Tech Workforce | ~373,600 | ~405,330 |

Tech Talent Density | 11.6% (Ottawa) / 11.7% (Waterloo) | 10.9% - 11.4% |

Avg. Tech Salary (USD) | $68,000 | $144,000 |

Avg. Rent (2-Bedroom) | ~US$1,800 - $2,200 | ~US$4,500 - $5,500 |

Quality of Living Rank | #19 (Ottawa) / #31 (Toronto) | #34 |

Executive Experience | Emerging (Fewer "Unicorn" leaders) | High (Concentration of "Scale-up" vets) |

The loss of graduates is particularly pronounced among elite institutions. A 2018 study of LinkedIn profiles found that 66% of software engineering and 30% of computer science graduates from the Universities of Toronto, British Columbia, and Waterloo left Canada within a year of graduation. Only two of the top 10 employers for these graduates were Canadian-owned (Scotiabank and Shopify), while the rest were U.S.-headquartered firms like Google, Amazon, and Microsoft. When the "builders" of the future tech ecosystem leave, the startups they create often start—or quickly move—their headquarters to the U.S. to stay connected to that talent network.

Market Access and the Proximity to "Early Adopters"

The scale and behavior of the customer base provide an irresistible pull for startups that have outgrown the 40-million-person Canadian market. The U.S. market offers direct access to 340 million consumers with higher average purchasing power. For a B2B SaaS company, the geographic distribution of enterprise customers is a critical variable. While Toronto is the second-largest financial center in North America, many fintech founders report that Canadian financial institutions are often slower to engage as customers compared to their U.S. counterparts.

The "early adopter" culture of the San Francisco Bay Area allows startups to iterate on their products with high-velocity feedback loops. In Canada, consumers and businesses are often perceived as more conservative, waiting for a technology to be proven in the U.S. before adopting it domestically. For many founders, this "market lethargy" is a primary reason to move the headquarters to a region where people are "eager to try new products and services," such as house sharing (Airbnb) or on-demand delivery (Instacart).

Customer Acquisition and Sales Dynamics

Metric | Canadian Ecosystem | Silicon Valley / US |

Total Population | ~40 Million | ~340 Million |

Customer Adoption Style | Conservative / Late-Adopter | Aggressive / Early-Adopter |

Networking Density | Hubs are geographically dispersed | Extreme density in Valley/SF |

B2B SaaS Sales Cycle | Often longer due to risk-aversion | Shorter for "Scale-up" solutions |

Market Fragmentation | National market | 50 distinct state markets |

Customer Acquisition Cost (CAC) | Varies by sector | Higher, but with higher LTV potential |

Furthermore, the reintroduction of trade uncertainty and tariffs has turned what was once a growth-oriented move into a defensive necessity. Small to medium-sized manufacturers and logistics firms, which make up 97% of Canadian exporters to the U.S., face disrupted supply chains and shrinking margins due to tariffs. Operating from within the U.S. eliminates duties, streamlines fulfillment, and avoids the bottlenecks associated with border delays. Commercial movers in Calgary reported a sharp rise in inquiries in 2025 from firms looking to relocate headquarters to Michigan or Texas specifically to "storm-proof" their operations against unpredictable trade policies.

Cross-Border Legal Risks: IP Protection and Litigation Costs

A final, subtle driver of relocation is the differing approach to intellectual property (IP) and litigation between the two countries. While Canada is often seen as a "less litigious" environment, this can be a double-edged sword for startups. The U.S. legal system, characterized by "forum shopping" and the constitutional right to jury trials for civil matters, creates a high-stakes environment for IP disputes.

Median damages in U.S. patent cases between 2018 and 2023 were $5.9 million USD, whereas Canadian awards tend to be smaller and punitive damages are a rarity. For a startup whose primary asset is its IP, having a U.S. presence and U.S. legal counsel is critical for defending those rights in the "most active" patent litigation arena in the world.

Comparison of IP Litigation Environments

Litigation Feature | Canada (Federal Court) | United States (District Courts) |

Cost System | "Loser Pays" (Award of ~20-30% of costs) | "American Rule" (Each party pays own) |

Jury Trials | No (Judges only in IP cases) | Yes (Constitutional right) |

Discovery Scope | Narrow (One rep per party) | Broad (Voluminous third-party discovery) |

Speed to Trial | Slower (Significant backlogs in Toronto) | Faster (Some trials within 1-2 years) |

Remedies | Accounting of profits; Injunctions common | Damages (Treble for willful); Injunctions rare |

Forum Shopping | Limited (Single nationwide court) | Prevalent (Strategic selection of district) |

The "loser pays" system in Canada acts as a deterrent for speculative or frivolous claims, providing a measure of comfort for foreign companies operating in the country. However, the U.S. system’s "American Rule," where each party bears its own costs regardless of the outcome, lowers the bar for commencing litigation, which can be a significant risk for undercapitalized startups. Consequently, startups that are scaling often relocate to the U.S. to be better positioned to manage the aggressive litigation and enforcement strategies that are standard in the American market.

Policy Responses and the Future Outlook

The Canadian government and domestic institutional investors have not been idle in the face of this "brain drain." A major policy debate centers on the role of the "Maple Eight"—Canada’s largest public pension funds—which hold more than $2.4 trillion in assets. Critics argue that these funds invest too much capital abroad and should be incentivized to back the domestic innovation economy.

In 2025, the federal government advanced reforms to encourage more pension fund investment in Canada, focusing on "incentives rather than mandates". These include:

Repealing the "30% Rule": Removing the restriction that prevents pension funds from owning more than 30% of the voting shares of a single Canadian entity, allowing them to take more active, controlling roles in domestic scale-ups.

Venture Capital Catalyst Initiative (VCCI): A fourth round of funding with $1 billion to "crowd-in" private capital alongside pension funds.

Mid-Cap Growth Fund: A $1 billion fund aimed at providing capital to companies that have outgrown the early-stage VC rounds but are not yet ready for the public markets.

These reforms aim to address the "Series B/C gap" that is currently the primary reason startups move their headquarters south. If domestic institutional capital can provide the same level of support as U.S. venture firms, the pressure to relocate for funding may diminish.

Summary of Major Canadian Tech Ecosystem Milestones (2020–2025)

Company / Event | Year | Strategic Outcome |

Salesforce Acquires Slack | 2020 | $27.7B USD deal for Vancouver-founded firm. |

Cohere AI Sovereign Funding | 2023 | $240M from Ottawa to keep AI compute domestic. |

2024 Federal Budget | 2024 | Capital gains inclusion rate increased to 66.7%. |

"Perfect Storm" for VCs | 2025 | Fundraising hits decade-low of $2.1B. |

Internet Backyard Relocation | 2025 | Gen Z founders move to Delaware for $4.5M seed round. |

30% Rule Repeal Proposal | 2025 | Fall Economic Statement moves to unlock pension capital. |

Conclusion: The Equilibrium of Necessity

The relocation of Canadian startup headquarters to the United States is the result of a rational calculation by founders and investors seeking to maximize growth and minimize jurisdictional risk. The "pull" of the U.S. capital markets, legal predictability in Delaware, and the sheer scale of the customer base remain the dominant forces in North American innovation. For many ventures, the "Delaware-CanCo Straddle" provides a temporary equilibrium, allowing them to leverage the cost advantages of Canadian R&D while participating in the global financial stage of the United States.

However, the continued loss of "unicorn" headquarters and the outflow of STEM graduates suggest that Canada’s role in the global tech economy is currently that of a "nursery" rather than a "home." While SR&ED and open immigration provide a strong foundation for launching companies, the structural weaknesses in late-stage funding, the executive talent vacuum, and the perceived "success tax" on large exits continue to drive high-potential firms south. The future of the Canadian startup ecosystem will depend on whether policy reforms—such as the repeal of the 30% pension rule and the expansion of "Patent Box" incentives—can create a domestic environment that supports not just the birth of an idea, but its maturation into a global leader. Until that balance is achieved, the "continental divide" will continue to be a defining feature of the Canadian innovation narrative.

Read More -

1. From Idea to MVP: A Step-by-Step Guide for Solo Founder

🔗 https://findnstart.com/blogs/from-idea-to-mvp-a-step-by-step-guide-for-solo-founder

2. How to Validate Your Startup Idea in 48 Hours for $0

🔗 https://findnstart.com/blogs/how-to-validate-your-startup-idea-in-48-hours-for-0

3. Remote vs. Local: Does Your Co-Founder Need to Live in the Same City?

🔗 https://findnstart.com/blogs/remote-vs-local-does-your-co-founder-need-to-live-in-the-same-city

4. The 2026 Startup Landscape: What Has Fundamentally Changed (and Why Founder Skills Matter More Than Ever)

5. The Most In-Demand Skills for Startup Founders in 2026

🔗 https://findnstart.com/blogs/the-most-in-demand-skills-for-startup-founders-in-2026

6. How to Find a Technical Co-Founder (Without a Six-Figure Salary)

🔗 https://findnstart.com/blogs/how-to-find-a-technical-co-founder-without-a-six-figure-salary

7. 5 Red Flags to Look for When Choosing a Startup Partner

🔗 https://findnstart.com/blogs/5-red-flags-to-look-for-when-choosing-a-startup-partner

8. How to Pitch Your Idea to Potential Co-Founders

🔗 https://findnstart.com/blogs/how-to-pitch-your-idea-to-potential-co-founders

9. How to Build a Portfolio that Attracts High-Growth Startup Founders

🔗 https://findnstart.com/blogs/how-to-build-a-portfolio-that-attracts-high-growth-startup-founders

10. Equity vs. Salary: How to Split Ownership with Your First Teammate

🔗 https://findnstart.com/blogs/equity-vs-salary-how-to-split-ownership-with-your-first-teammate

11. Why Joining an Early-Stage Startup is Better Than a Corporate Job

🔗 https://findnstart.com/blogs/why-joining-an-early-stage-startup-is-better-than-a-corporate-job

12. The Future of EdTech: Why Developers and Educators Need to Team Up Now

🔗 https://findnstart.com/blogs/the-future-of-edtech-why-developers-and-educators-need-to-team-up-now

13. The Architecture of Symbiosis: Analytical Perspectives on the Five Habits of Successful Startup Duos

14. Finding a Co-Founder in the AI Space: What Skills Should You Look For?

🔗 https://findnstart.com/blogs/finding-a-co-founder-in-the-ai-space-what-skills-should-you-look-for

15. Overcoming Analysis Paralysis and the Strategic Path to Execution

🔗 https://findnstart.com/blogs/overcoming-analysis-paralysis-and-the-strategic-path-to-execution

16. From College Project to Company: How to Find Your Student Co-Founder

🔗 https://findnstart.com/blogs/from-college-project-to-company-how-to-find-your-student-co-founder

17. How to Start a Startup While Working a Full-Time Job

🔗 https://findnstart.com/blogs/how-to-start-a-startup-while-working-a-full-time-job

18. How to Build a HealthTech Startup Without a Medical Degree

🔗 https://findnstart.com/blogs/how-to-build-a-healthtech-startup-without-a-medical-degree

19. The Solitary Architect: Executive Isolation in Entrepreneurship

20. The 2026 Guide to Launching a SaaS as a Solo Developer

21. What Sustainable Growth Actually Looks Like

🔗 https://findnstart.com/blogs/what-sustainable-growth-actually-looks-like

22. The Early Warning Signs Your Startup Is in Trouble

🔗 https://findnstart.com/blogs/the-early-warning-signs-your-startup-is-in-trouble

23. How to Grow Without Burning Out

🔗 https://findnstart.com/blogs/how-to-grow-without-burning-out

24. The Truth About “Runway” Most Founders Ignore

🔗 https://findnstart.com/blogs/the-truth-about-runway-most-founders-ignore

25. Revenue Solves More Problems Than Funding

🔗 https://findnstart.com/blogs/revenue-solves-more-problems-than-funding

26. What No One Tells You About Being a Solo Founder

🔗 https://findnstart.com/blogs/what-no-one-tells-you-about-being-a-solo-founder

27. Why Smart People Quit High-Paying Jobs to Build Startups (And Why Most Regret It)

28. Why Most Startup Advice on Twitter Is Dangerous

🔗 https://findnstart.com/blogs/why-most-startup-advice-on-twitter-is-dangerous

29. Decision Fatigue: The Silent Startup Killer

🔗 https://findnstart.com/blogs/decision-fatigue-the-silent-startup-killer

30. Fear vs Logic: How Founders Actually Make Decisions

🔗 https://findnstart.com/blogs/fear-vs-logic-how-founders-actually-make-decisions

31. How Overthinking Destroys Early Momentum

🔗 https://findnstart.com/blogs/how-overthinking-destroys-early-momentum

32. Ideas Don’t Scale. Systems Do.

🔗 https://findnstart.com/blogs/ideas-dont-scale-systems-do

33. The First Hire That Actually Matters

🔗 https://findnstart.com/blogs/the-first-hire-that-actually-matters

34. How the First 100 Users Decide Your Startup’s Fate

🔗 https://findnstart.com/blogs/how-the-first-100-users-decide-your-startups-fate

35. Why Your Startup Doesn’t Need Growth — It Needs Focus

🔗 https://findnstart.com/blogs/why-your-startup-doesnt-need-growthit-needs-focus

36. Why Most Startups Die Quietly

🔗 https://findnstart.com/blogs/why-most-startups-die-quietly

37. Lessons Learned Too Late by First-Time Founders

🔗 https://findnstart.com/blogs/lessons-learned-too-late-by-first-time-founders

38. The Myth of the “Overnight Success” Startup

🔗 https://findnstart.com/blogs/the-myth-of-the-overnight-success-startup