Why Brazil’s Startup Ecosystem Is Growing Faster Than Expected

June 29, 2026 by Harshit Gupta

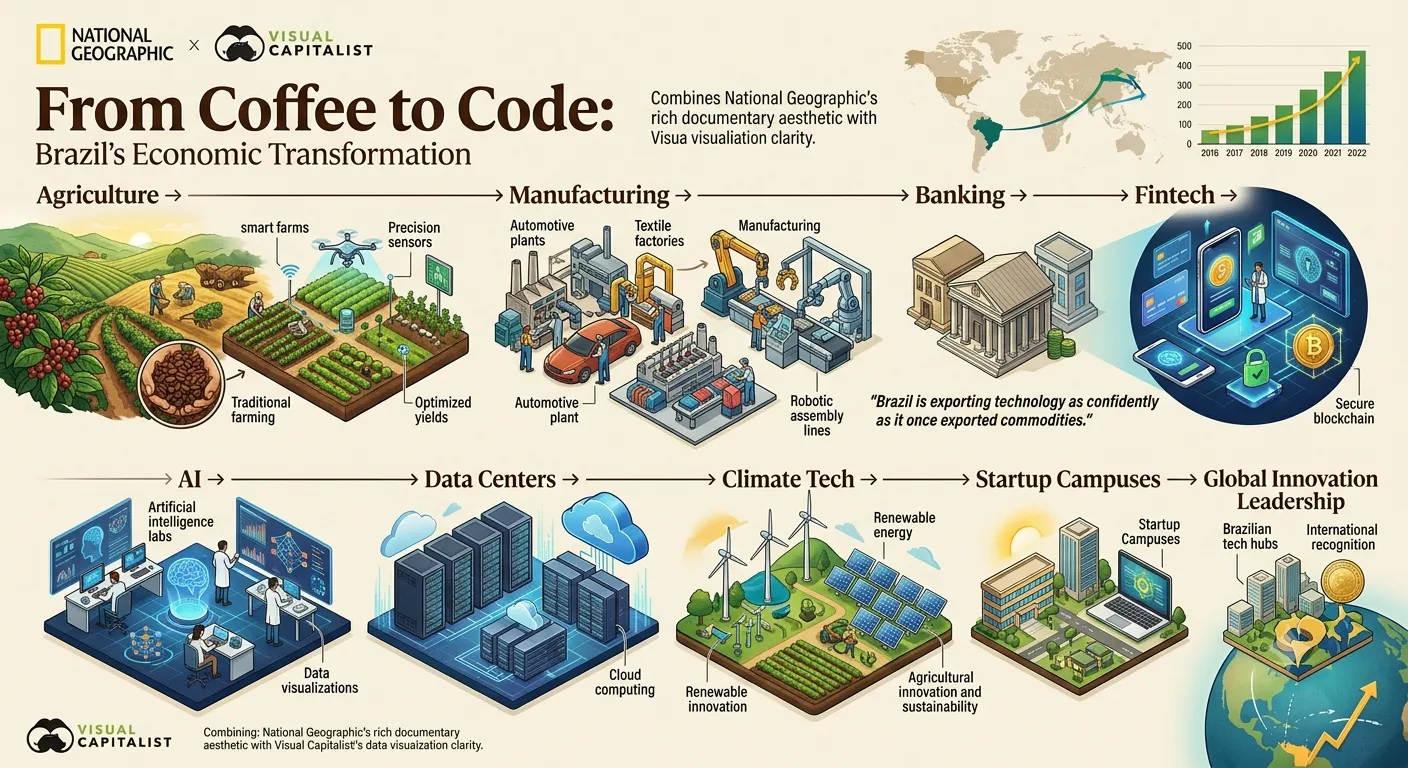

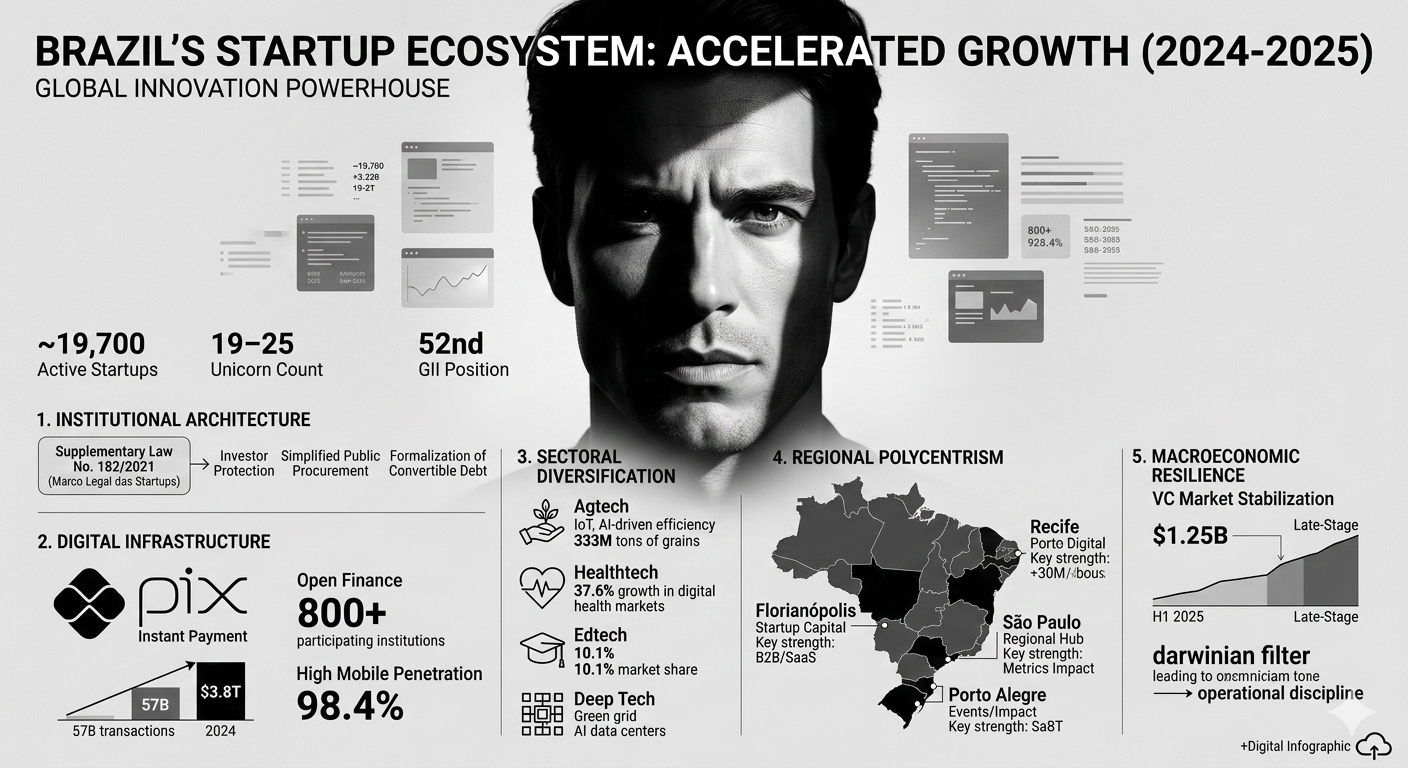

The evolution of the Brazilian startup ecosystem from a regional curiosity to a global innovation powerhouse represents one of the most significant structural shifts in emerging market economics over the last decade. In 2025, Brazil holds the 52nd position in the Global Innovation Index, ranking as the second-most innovative economy in Latin America and the Caribbean, and fifth among the 36 upper-middle-income group economies. While historical expectations often forecasted a slower trajectory due to chronic macroeconomic volatility and high interest rates, the reality has diverged sharply. The ecosystem is currently characterized by a "coiled spring" effect, where years of foundational digital infrastructure building, proactive regulatory reform, and a shift toward operational discipline have converged to create a period of accelerated growth that defies traditional cyclical downturns. With over 19,000 active innovative companies and 234 distinct innovation ecosystems, Brazil has moved beyond the "hype" phase into a state of structural maturity where technology is deeply embedded in the nation’s economic fabric.

The Institutional Architecture of Innovation

The acceleration of the Brazilian ecosystem is fundamentally rooted in a series of legislative and regulatory shifts that have provided the legal certainty required for large-scale capital deployment. The most significant of these is Supplementary Law No. 182/2021, known as the Marco Legal das Startups. This framework addressed long-standing bottlenecks in the Brazilian business environment, particularly regarding the liability of investors and the complexity of public procurement. By defining startups as entities with up to ten years of registration and gross revenues of up to R16 million, the law created a targeted regulatory zone for high-growth firms.

One of the most transformative elements of the Marco Legal is the protection it affords to angel investors. Historically, the "piercing of the corporate veil" in Brazilian labor and tax courts posed a significant risk to passive investors, who could find their personal assets targeted for company debts. Article 8 of the Law explicitly limits this liability, provided there is no evidence of fraud or direct management participation, thereby unlocking a massive pool of local private wealth that was previously sidelined by risk aversion. Furthermore, the formalization of convertible debt instruments, such as the Mútuo Conversível, has standardized the investment process, bringing Brazilian practices in line with global standards like the SAFE notes used in Silicon Valley.

Comparative Regulatory and Performance Metrics

The following data summarizes the impact of these institutional changes on the broader innovation landscape:

Metric | 2020/2021 Status | 2024/2025 Status | Implication |

GII Position | 62nd | 52nd | Upward trajectory in innovation output. |

Active Startups | ~12,000 | 19,706 | Massive expansion of the entrepreneurial base. |

Unicorn Count | 10 | 19 - 25 | Maturation of late-stage ventures. |

Digital ID Usage | Developing | 95% Internet Daily Use | High addressable digital market. |

Business Sophistication | Moderate | 39th Globally (GII) | Strongest pillar in Brazil's innovation index. |

Beyond private investment, the Marco Legal introduced the "Public Contract for Innovative Solutions," which allows government bodies to bypass traditional, rigid bidding processes for pilot projects. This has turned the Brazilian state into a significant client for startups, particularly in Govtech and Smart City applications. In cities like Porto Alegre and Recife, these contracts have been instrumental in revitalizing urban infrastructure, with Porto Alegre alone seeing a 29.5% increase in local tax collection following the integration of startup-led events and solutions into its city planning.

Digital Infrastructure as a Force Multiplier

While legal frameworks provide the rules of engagement, Brazil’s digital infrastructure provides the high-performance rails upon which the ecosystem runs. The convergence of the Pix instant payment system, Open Finance, and high mobile penetration has created an environment where the cost of customer acquisition and financial intermediation has plummeted. Brazil’s internet penetration stood at 86.9% by the end of 2025, with 185 million individuals online, 98.4% of whom access the web via mobile devices.

The Pix system, launched by the Central Bank of Brazil, is perhaps the most successful fintech implementation globally. Within six years of its launch, 70% to 75% of Brazilians use the system, which handled 57 billion transactions totaling3.8 trillion in 2024. Pix has democratized payments, enabling real-time transactions 24/7 without fees, which has brought millions of previously unbanked citizens into the formal digital economy. For startups, this means an immediate, friction-free payment channel that covers nearly the entire adult population. The expansion into "Pix Parcelado" in late 2025, which integrates installment credit directly into the payment rail, further challenges the traditional credit card duopoly and provides a new growth engine for retail-tech and social commerce.

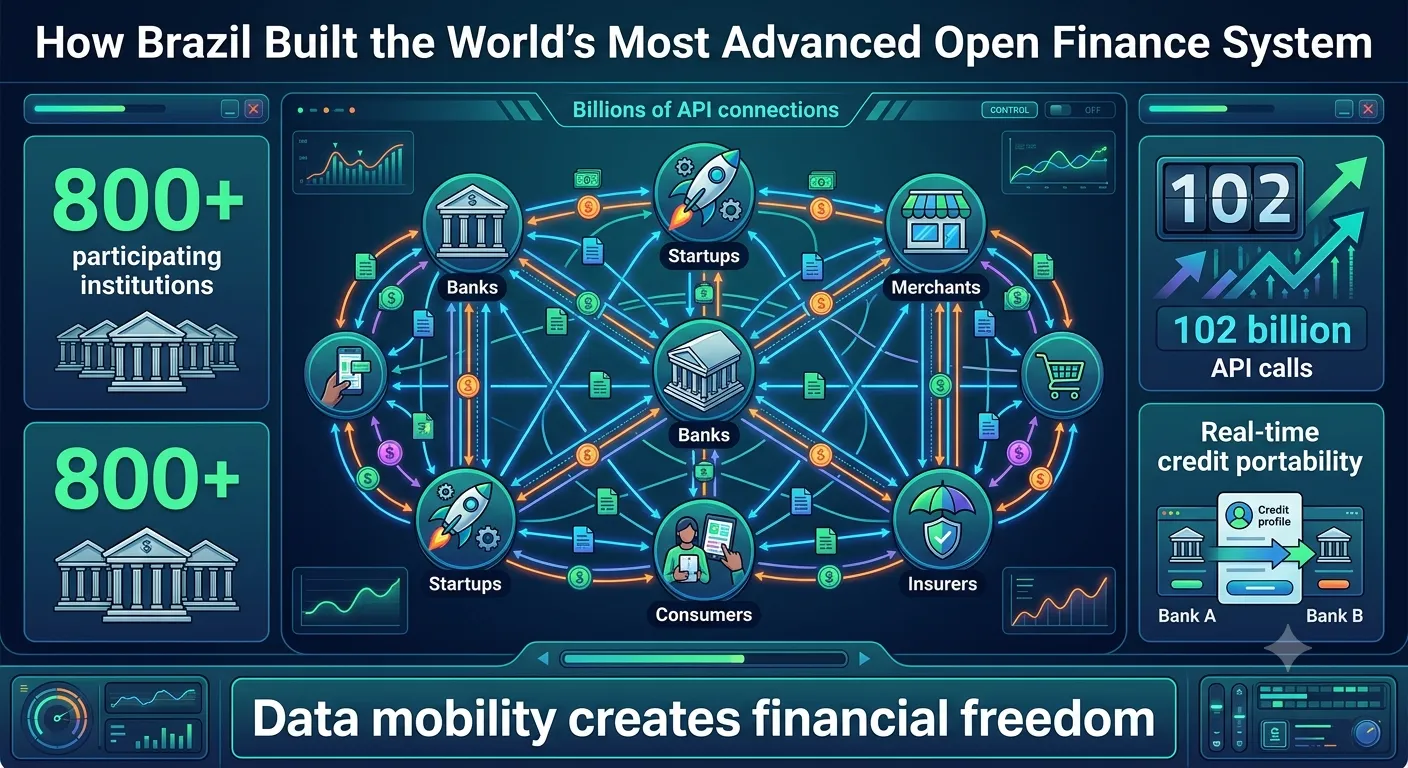

The second pillar of this infrastructure is Open Finance, which reached its fourth phase of implementation by 2024. Brazil now boasts one of the most advanced financial data-sharing frameworks in the world, with over 800 participating institutions and 102 billion API calls recorded in 2024 alone. This system allows for hyper-personalized financial products and seamless credit portability, where a consumer can transfer their entire credit history and loan profile to a competing institution with a single click. The synergy between Pix and Open Finance has turned financial services into an "operating model" rather than just a sector, allowing non-financial companies to embed lending and insurance directly into their customer journeys.

Macroeconomic Resilience and the Profitability Pivot

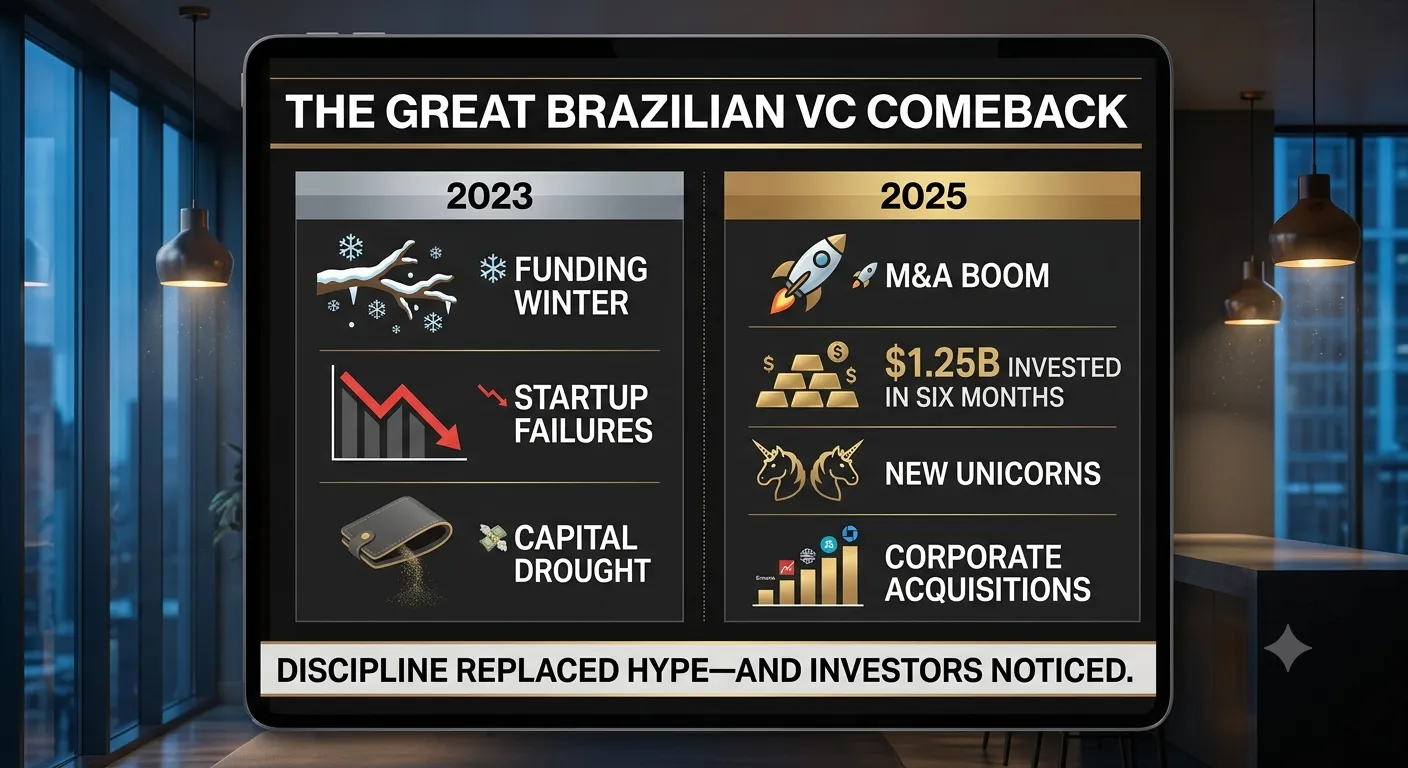

A common critique of Brazil’s growth potential has been its historically high interest rates. However, the period between 2023 and 2025 has demonstrated that the startup ecosystem can grow even when the SELIC rate hovers between 12% and 15%. This is due to a fundamental shift in the "founder mindset." The funding drought of 2023, where investment plummeted by 86% in the first quarter, served as a "Darwinian filter". Startups that survived this period did so by pivoting away from "growth at any cost" toward unit economics and sustainable cash flow.

By 2025, the venture capital market has entered a recovery phase, but with a different character than the 2021 boom. Investments reached $1.25 billion in the first half of 2025, more than half of 2024’s total of $2.25 billion. Investors are now concentrated on "targeted bets" in companies with high revenue traction and AI-driven efficiency. This new discipline has made the ecosystem more resilient to interest rate fluctuations. Analysts now view Brazil as a market where technology is used to solve deep-seated structural inefficiencies—such as the massive gap in corporate credit, which represents only 32% of GDP in Brazil compared to 73% in the United States—meaning the potential for value creation remains enormous regardless of the cost of capital.

Investment Trends and Market Stabilization

The stabilization of the VC market is evident in the deal sizes and the profiles of the companies receiving funding:

Funding Indicator | 2023 Status | 2024/2025 Status | Growth/Change |

Total VC Dollars (LATAM) | 4.2 Billion | 4.5 Billion | +8% YoY Stability |

Late-Stage (Series C+) | Slowdown | 1.6 Billion | +55% YoY Growth |

Brazil Share of VC | Dominant | 34.7% of Regional Total | Reclaimed top spot in Q3 2025 |

Early-Stage Focus | Selective | 80% of All Transactions | Strong local investor support |

Median Series C Size | 40 Million | 50 Million | Rebound in international interest |

The "reawakening" of the M&A market in 2025 further underscores this resilience. Corporate buyers, rather than private equity firms, have led the charge, using acquisitions to capture innovation and digital capabilities in ERP, cloud SaaS, and verticalized enterprise software. In the first ten months of 2025, over 40 software M&A deals were announced, outpacing previous years and signaling a consolidation phase that often precedes a new cycle of public offerings.

Sectoral Diversification and the Rise of Agtech

Brazil’s startup success is no longer confined to fintech. The country is leveraging its natural competitive advantages to lead in Agtech and deep tech. As an agricultural powerhouse producing a significant portion of the world’s soy, corn, and beef, Brazil has become a global laboratory for sustainable digital agriculture. The sector has shifted from land expansion to tech-driven efficiency, with a growing network of startups offering solutions across the entire production chain—from bio-inputs produced on-farm to blockchain-based logistics.

Startups like Solinftec and Agrosmart are at the forefront of this movement, integrating IoT and AI to optimize crop management. The impact of rural connectivity is a critical driver here; 5G and broadband rollout in rural areas are transforming landscapes into "hubs of innovation," with connected farms achieving 20% to 30% higher productivity. The government’s "New Industrial Policy" and "Radar AgTech Brasil" programs have funneled significant capital into these areas, recognizing that Brazil’s role in global food security is inextricably linked to its technological capabilities.

Diversity in the Startup Landscape

The distribution of startups across sectors reveals a maturing and diversified economy:

Sector | Market Share | Growth Driver |

Edtech | 10.1% | Demand for digital skills and remote learning. |

Fintech | 9.7% | Open Finance and Pix-led inclusion. |

Software Dev | 9.2% | Digitization of traditional MSMEs. |

Healthtech | 8.5% | 37.6% growth in digital health markets. |

Agtech | Emerging | Sustainable productivity and carbon credits. |

In addition to Agtech, Healthtech has seen a surge, growing at an annual rate of 37.6% in 2024, far outpacing the global average of 5.5%. This growth is driven by telemedicine and diagnostic solutions that address the geographical challenges of the Brazilian territory. Companies like Isa Saúde are attracting institutional capital by combining financial scalability with measurable social impact, reflecting a broader trend of ESG (Environmental, Social, and Governance) considerations becoming central to the Brazilian VC ecosystem.

The AI Frontier and the New Industrial Policy

Artificial Intelligence has emerged as the most significant technological catalyst in the 2024-2025 period. The Brazilian Artificial Intelligence Plan (PBIA 2024-2028), titled "AI for the Good of All," represents a R 23 billion (approximately 4 billion) commitment to technological modernization. The plan is exhaustive, covering everything from AI infrastructure—including the upgrade of the Santos Dumont supercomputer—to training programs for a new generation of workers.

The PBIA allocates nearly R 14 billion specifically for business innovation projects, with a strong focus on startups and MSMEs. This is a strategic move to ensure that Brazilian firms do not merely consume foreign AI but build local solutions that reflect the country’s unique social and economic context. For instance, AI is being used in the financial sector to improve credit scoring for the unbanked and to detect fraud in real-time within the Pix network. Large enterprises are driving this adoption, with 90% of major Brazilian firms already implementing AI applications in 2024.

However, the rapid adoption of AI has also triggered a complex regulatory debate. The Brazilian AI Bill (PL 2338/2023), which passed the Senate in late 2024, adopts a risk-based classification system similar to the EU AI Act. While it aims to protect fundamental rights, the startup community has raised concerns about the potential for high compliance costs to stifle innovation. The industry is advocating for a more "proportional" approach that focuses on high-risk applications while leaving the "frontier" of innovation relatively unencumbered. Despite these debates, the presence of a clear regulatory roadmap is viewed as a sign of institutional maturity that attracts long-term international investment.

Regional Polycentrism: Beyond São Paulo

A defining feature of the "faster than expected" growth is the emergence of robust innovation hubs outside the traditional center of São Paulo. While São Paulo State still hosts 55% of deep tech ventures and remains the primary gateway for international capital, other regions are carving out distinct specializations.

Florianópolis has emerged as the "Startup Capital of Brazil," leading the nation in tech’s contribution to GDP (25%). The city’s ecosystem is characterized by a high density of startups per capita—ten times higher than São Paulo—and a core strength in B2B software and data analytics. Similarly, Recife’s Porto Digital has transformed the city’s historic center into a vibrant tech hub with over 475 companies, focusing on the creative economy and Govtech. In the South, Porto Alegre has used the South Summit Brazil event as a catalyst for economic regeneration, with the 2025 edition injecting 166 million BRL into the economy and revitalizing urban spaces like the Cais Mauá.

Innovation Hub | Key Strength | Impact/Metric |

São Paulo | Regional Hub | 113 Billion Ecosystem Value |

Florianópolis | B2B / SaaS | 38,400+ Direct Tech Jobs |

Recife | Creative Economy | Porto Digital (475 Companies) |

Porto Alegre | Events / Impact | 3rd Strongest Hub in S. America |

Santa Catarina | Remote Work | 100,000 New Tech Jobs by 2027 |

This regional diversification is supported by organizations like Sebrae and ACATE, which provide the training and go-to-market strategies necessary for local entrepreneurs to scale. The decentralization of innovation makes the national ecosystem more resilient, as it taps into a broader range of talent and industry-specific needs across the country’s diverse geography.

Human Capital and Founder Maturity

The acceleration of Brazil’s startup scene is also a demographic story. The average age of a Brazilian startup founder is 40, with 40% of founders falling between the ages of 35 and 44. These are not "college dropouts" but mature professionals with significant industry experience and business networks. This maturity has been a key factor in the shift toward profitability and operational excellence, as these founders are better equipped to navigate complex regulatory environments and high-interest-rate cycles.

Brazil also hosts the largest tech workforce in Latin America, with over 500,000 software developers. While there is a recognized need to "professionalize" the deep tech founder pool—moving away from "solutions in search of a problem"—the existing talent base is significant. Programs like "Brasil Mais Produtivo" and partnerships with European universities are working to bridge the skills gap, preparing a new generation of workers for the AI-driven 4.0 industrial era.

The ESG Catalyst and COP30

Sustainability has moved from a compliance check to a core business driver in the Brazilian ecosystem. Brazil enjoys one of the cleanest energy matrices in the world, with 88% of its electricity coming from renewable sources. This "green grid" is attracting energy-intensive industries, such as AI data centers, which are seeking low-carbon alternatives to meet global climate goals. Mega-investors like Goldman Sachs and Patria Investimentos are expanding their bets on Brazilian data centers, projecting an absorption of20 billion in investment by 2030.

The upcoming COP30 summit in Belém in 2025 is acting as a "north star" for the ecosystem. The government has launched platforms like "Empreender Clima" to provide green credit with reduced interest rates for small businesses and startups focusing on climate change mitigation. These loans offer long-term repayment periods of up to 25 years, providing the "patient capital" necessary for hard-tech and sustainability ventures. Success stories like Trashin, a sustainability startup awarded at South Summit, demonstrate that circular economy models are now becoming commercially viable at scale in Brazil.

Conclusion: A Structural Inflection Point

The evidence from the 2024-2025 period suggests that Brazil’s startup ecosystem has reached a structural inflection point. The combination of a world-class digital payment and data infrastructure, a proactive and protective legal framework, and a resilient, disciplined founder class has created an environment where technology acts as the primary driver of economic modernization.

The growth is "faster than expected" because it is no longer reliant on the "easy money" of the low-interest-rate era. Instead, it is fueled by the resolution of deep-seated inefficiencies in the Brazilian economy. As the country prepares to host major global forums like COP30 and continues to lead in areas like Open Finance and Agtech, its position as the regional reference point for technology growth is being reaffirmed. For international investors, the message is clear: Brazil has built the foundational "rails" for the next cycle of disciplined, innovation-led growth, making it one of the most compelling destinations for capital in the emerging world. The transition from a local innovation hub to a global benchmark is well underway, and the momentum appears to be structural rather than merely cyclical.

Want to calculate the equity for your cofounder?

Nail your cap table before you sign. Whether you're splitting equity with a co-founder or planning your next funding round, our Equity Calculator gives you precision in seconds

Equity calculator →