Why Brazil Is Becoming Latin America’s Startup Powerhouse

June 30, 2026 by Harshit Gupta

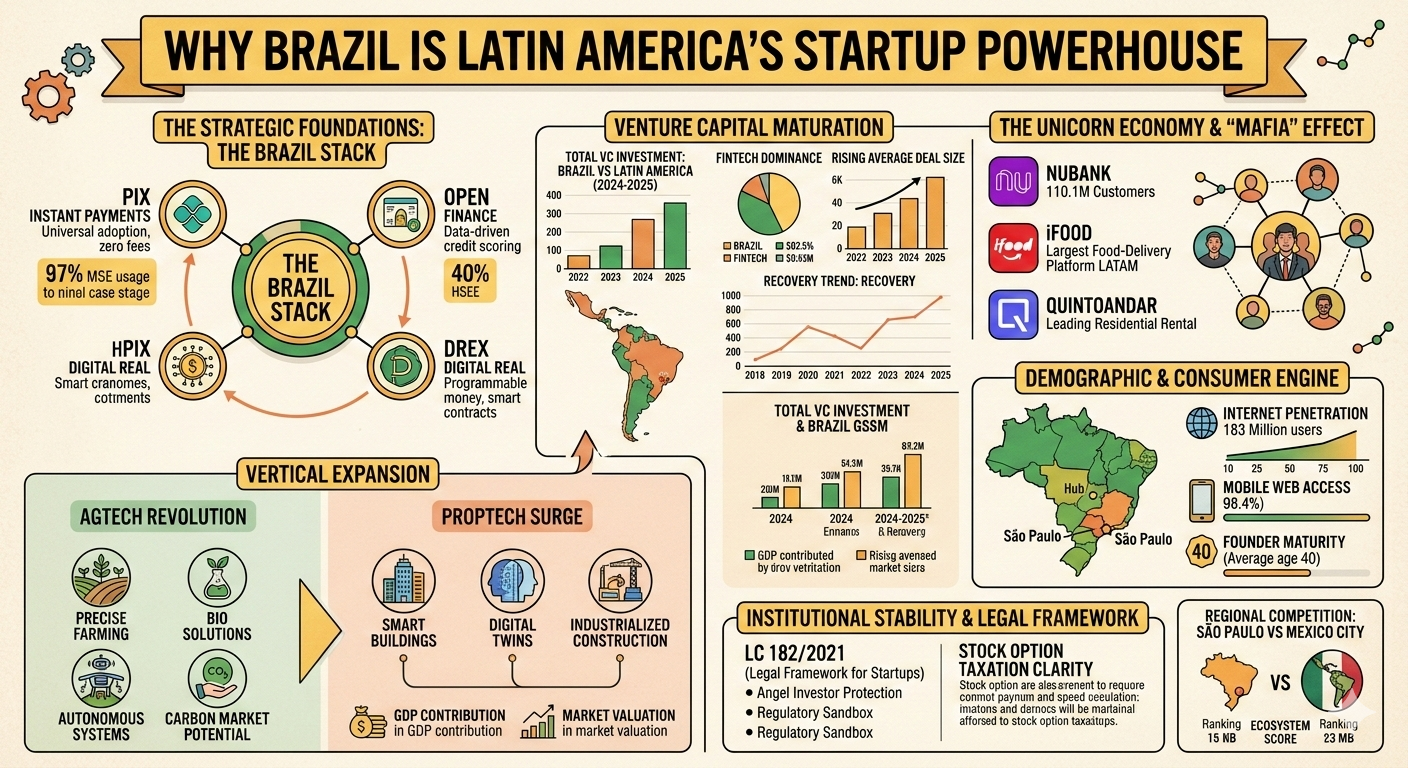

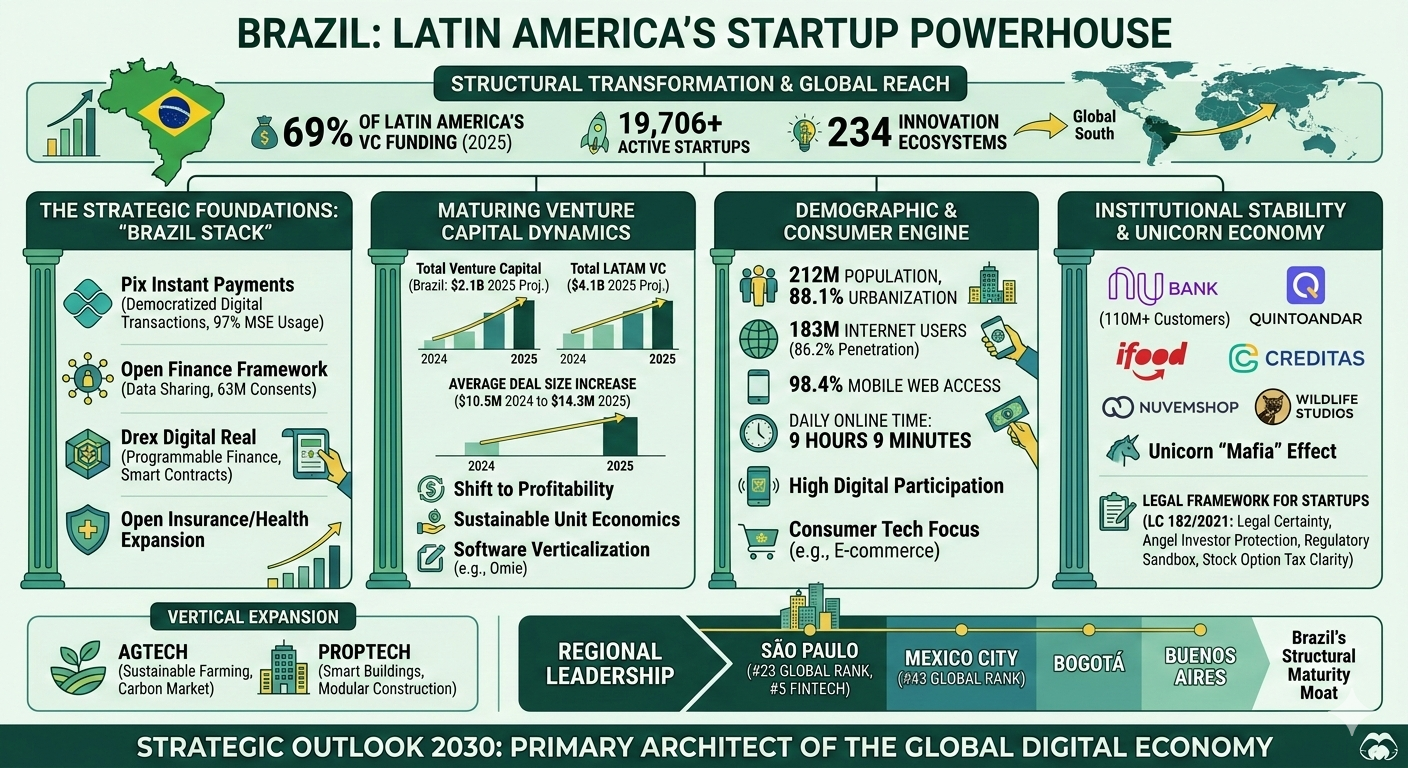

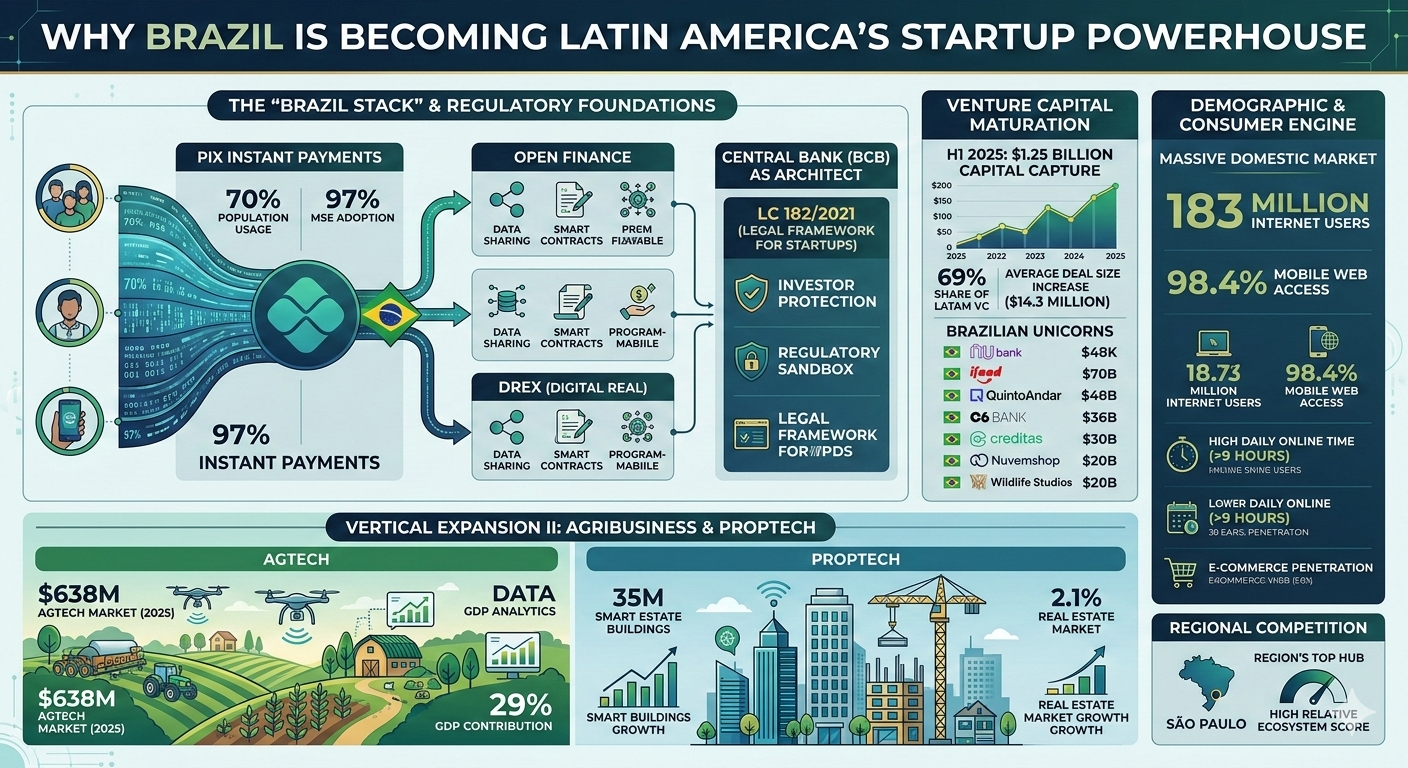

The structural transformation of Brazil into Latin America's preeminent startup ecosystem represents a definitive shift in the global geography of innovation. As of 2025, Brazil has transcended its historical reputation for macroeconomic volatility to establish a sophisticated, digital-first economy anchored by what global analysts increasingly refer to as the "Brazil Stack." This integrated technological and regulatory layer—comprising the Pix instant payment system, the Open Finance framework, and the nascent Drex digital currency—has provided the institutional stability and transaction efficiency necessary to catalyze a multi-billion dollar venture capital landscape. With over 19,706 active startups and a robust network of 234 innovation ecosystems, Brazil has effectively decoupled its technological growth from traditional industrial constraints, positioning itself as a central hub for the Global South's digital transition.

The maturation of this ecosystem is not merely a localized success story but a regional gravity shift. By mid-2025, Brazil captured approximately 69% of all venture capital investment in Latin America, raising over $1.25 billion in the first half of the year alone. This dominance is underpinned by the country's massive domestic market—the eighth largest consumer market in the world—and a population that is increasingly digital-native. The strategic focus has pivoted from "growth at all costs" to a paradigm of profitability and operational excellence, reflecting a more rigorous investment standard that has raised the average quality of the domestic pipeline.

The Strategic Foundations of Digital Hegemony: The Brazil Stack

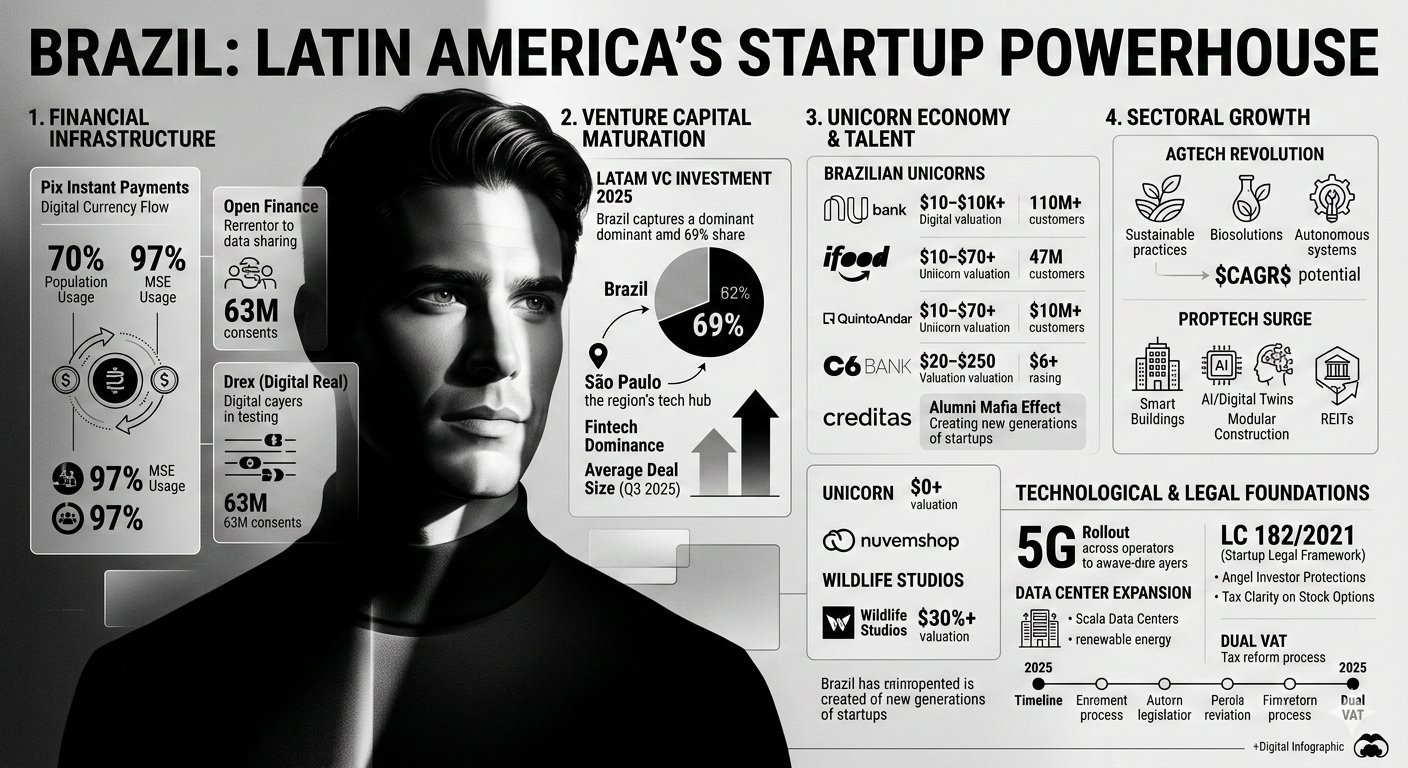

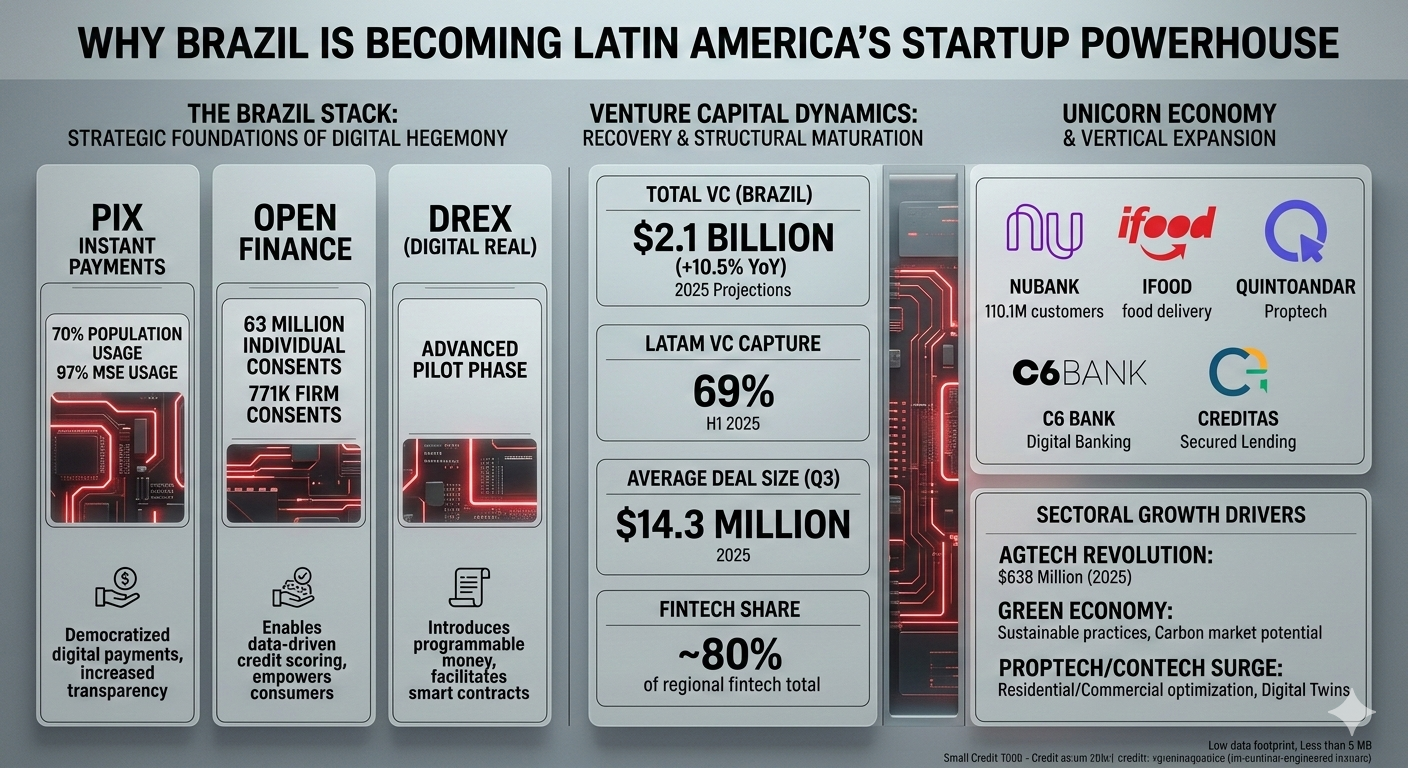

The primary driver of Brazil's acceleration is the proactive and architectural role played by the Central Bank of Brazil (BCB). In a departure from typical regulatory models, the BCB has functioned as a primary platform founder, creating a unified financial operating system for the nation. The introduction of Pix in 2020 served as the fundamental catalyst, transforming digital transactions into a universal utility. By late 2025, Pix had achieved nearly universal adoption among small businesses, with 97% of micro and small enterprises (MSEs) utilizing the platform for daily operations.

The success of Pix is deeply intertwined with the development of the Open Finance framework, which allows for the secure sharing of financial data across institutions. Although firm-level adoption of Open Finance lagged at 3.2% in early 2025, the correlation between frequent Pix usage and Open Finance adoption suggests that the former acts as a "gateway drug" for deeper digital financial participation. This ecosystem is set to evolve further with the full implementation of Drex, the digital real, which will enable programmable finance and smart contracts on a national scale, further reducing the costs of financial intermediation.

Financial Infrastructure Component | Implementation Status (2025) | Core Strategic Impact |

Pix Instant Payments | 70% population usage; 97% MSE usage. | Democratized digital payments; eliminated transaction fees; increased transparency. |

Open Finance | 63 million individual consents; 771k firm consents. | Enables data-driven credit scoring; increases banking competition; empowers consumers. |

Drex (Digital Real) | Advanced pilot and testing phases. | Introduces programmable money; facilitates smart contracts; modernizes the settlement layer. |

Open Insurance/Health | Sectoral expansion of data-sharing models. | Extends data portability to non-financial sectors, fueling insurtech and healthtech. |

The regulatory environment has been further solidified by Resolution No. 493 and Resolution No. 498, which enhanced the governance of the Pix system and established stricter security and capital requirements for payment institutions. These measures ensure that the digital infrastructure remains resilient against fraud while maintaining the high liquidity levels that attract international venture capital. For instance, payment institutions are now required to maintain a minimum capital of BRL 15 million and adhere to internationally recognized information security standards to participate in the payment system. This high bar for entry has ironically acted as an attractor for sophisticated investors, as it provides a level of institutional security rarely found in other emerging markets.

Venture Capital Dynamics: From Recovery to Structural Maturation

The Brazilian venture capital market in 2025 represents the culmination of a "purification" process that followed the global funding correction of 2022-2023. The "VC Winter" of the previous years effectively filtered out capital-inefficient business models, leaving a cohort of startups that prioritize sustainable unit economics and defensible market positions. While total funding levels remain below the 2021 peak, the quality of current deals is significantly higher, characterized by larger round sizes even as the total deal count remains selective.

Investment Metric | 2024 Performance | 2025 Projections/H1 Data |

Total Venture Capital (Brazil) | $2.0 Billion | $2.1 Billion (+10.5% YoY) |

Total Venture Capital (LATAM) | $4.5 Billion | $4.1 Billion (+14.3% YoY) |

Fintech Share of VC | ~80% of regional fintech total | Dominant vertical, with rising B2B and AI focus. |

Average Deal Size (Q3) | $10.5 Million (2024) | $14.3 Million (2025) |

The investment recovery is notably structural. In the first half of 2025, Brazil's $1.25 billion in funding already exceeded half of the 2024 total, indicating a steady climb in investor confidence. This resurgence is driven by two parallel trends: the continued dominance of fintech and the "Software Verticalization" of other sectors. Successful startups are increasingly specialized, addressing the specific legal, medical, or agricultural pain points of the Brazilian economy rather than offering generic horizontal solutions. For example, the Series D round of $160 million for Omie, a SaaS platform for SMEs, represents the largest Brazilian deal of 2025 and highlights the massive opportunity in digitizing traditional back-office functions.

Furthermore, the regional geography of investment is recalibrating. While Mexico briefly surpassed Brazil in quarterly funding during the second quarter of 2025—driven by significant rounds for digital banks like Klar and Plata—Brazil reclaimed the top spot by the third quarter, accounting for 69% of the region's venture funding. This "see-saw" effect between the two largest economies highlights a maturing regional market where capital flows to high-impact opportunities regardless of local borders, though São Paulo remains the undisputed "tech capital" with a startup ecosystem score nearly eight times higher than its closest domestic rival, Rio de Janeiro.

The Demographic and Consumer Engine

The sheer scale and density of the Brazilian consumer market provide a "natural moat" that facilitates rapid scaling for digital-first enterprises. With a population of 212 million and an urbanization rate of 88.1%, Brazil offers a concentrated audience for mobile-delivered services. The depth of digital engagement is particularly profound: 183 million Brazilians use the internet daily, with 98.4% of users connecting via mobile devices. This creates a high-velocity feedback loop for product development, where startups can iterate based on real-time data from millions of active users.

The behavior of the Brazilian consumer is characterized by a high degree of digital participation. On average, Brazilians spend over 5 hours a day online via their smartphones, primarily for utilitarian purposes such as researching products, managing financial services, and communicating with family and friends. This digital fluency has allowed for the rapid expansion of e-commerce, which consistently remains the second-largest vertical by deal count in the venture capital landscape.

Consumer Market Indicator | Value (2025 Estimates) |

Total Internet Users | 183 Million (86.2% penetration) |

Mobile Web Access | 98.4% of internet users |

Daily Online Time | 9 Hours 9 Minutes |

Digital Ad Market Revenue | $34.3 Billion |

Programmatic Ad Spend | 80% of total digital ad spend |

The demographic profile also supports long-term entrepreneurial stability. The average age of Brazilian startup founders is 40, with a significant concentration in the 35–44 age bracket. These founders typically enter the ecosystem with significant professional experience and mature business networks, which mitigates the execution risks common in younger, less experienced cohorts. This maturity is reflected in the fact that over 86% of Brazilian startups focus initially on the domestic market, leveraging its scale to reach viability before attempting international expansion.

The Unicorn Economy and the "Mafia" Effect

Brazil’s position as a global startup leader is further evidenced by its status as one of the top ten countries globally for "unicorns" (startups valued at $1 billion or more). As of late 2025, the country hosts between 21 and 24 unicorns, primarily concentrated in fintech, proptech, and logistics. These organizations are no longer merely high-growth companies; they have become systemic pillars of the Brazilian economy, providing essential services to millions.

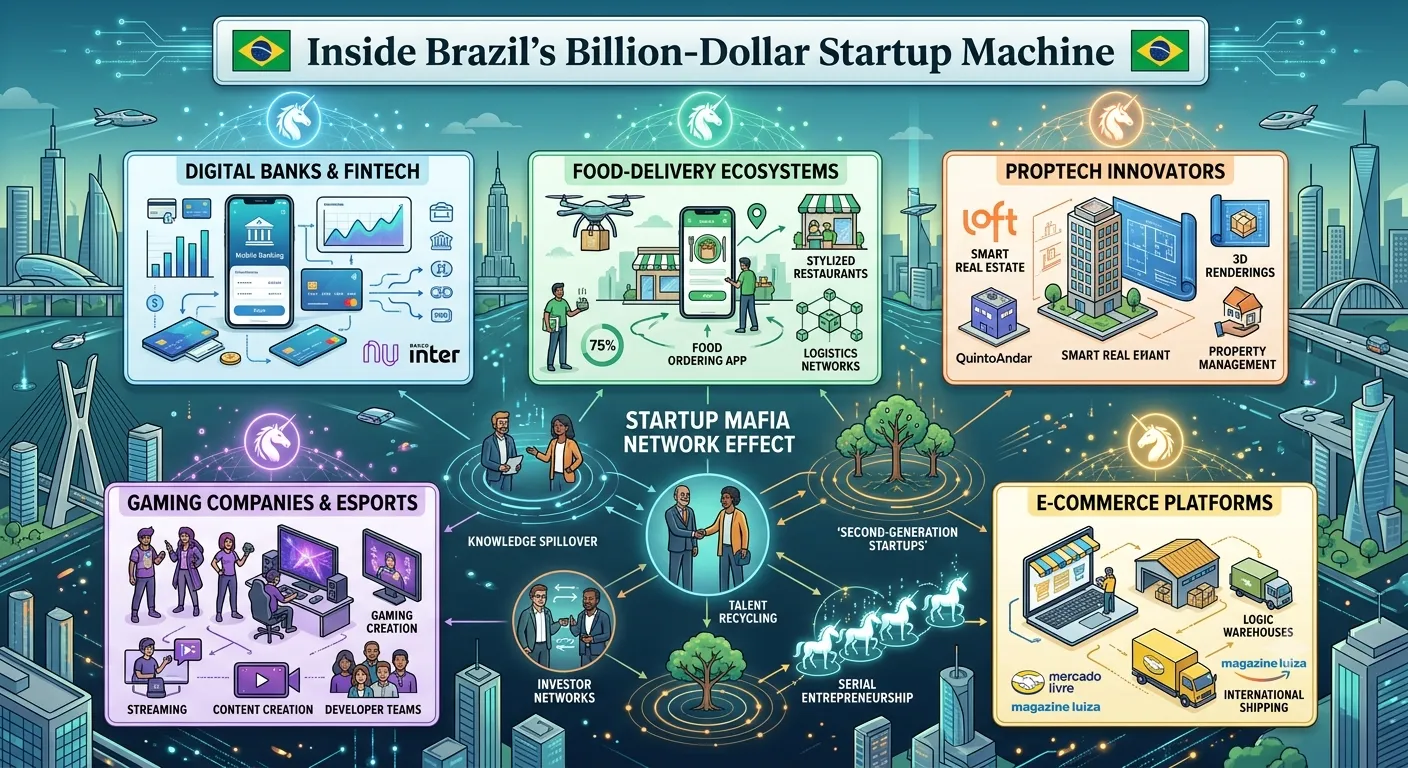

The reach of these companies is unprecedented. Nubank, for instance, reported 110.1 million customers in Brazil by September 2025, a level of penetration that has turned the digital bank into a national utility. Similarly, iFood has become the dominant food-delivery platform in Latin America, connecting a massive network of restaurants and delivery partners through an AI-optimized logistics ecosystem.

Prominent Brazilian Unicorns | Valuation (approx.) | Primary Sector | Key Metric |

QuintoAndar | $5.1 Billion | Real Estate / Proptech | Leading residential rental platform; eliminated guarantors. |

C6 Bank | $5.05 Billion | Digital Banking / Fintech | Full suite of digital financial products for SMEs/Individuals. |

iFood | $5.0 Billion | E-Commerce / Delivery | Largest food-delivery platform in LATAM. |

Creditas | $5.0 Billion | Secured Lending / Fintech | Uses homes/cars as collateral for lower-interest loans. |

Nuvemshop | $3.1 Billion | E-Commerce / SaaS | Enables SME e-commerce storefronts across the region. |

Wildlife Studios | $1.0 Billion+ | Gaming / Consumer Tech | Global reach with 4.5 billion+ game downloads. |

The influence of these unicorns extends beyond their own market caps. The "alumni" of successful exits and major funding rounds—such as those from 99, VTEX, and Stone—are now founding a second and third generation of startups. This "mafia" effect accelerates the ecosystem by recycling talent and capital into new ventures that are designed for regional or global scale from day one. This transition from "local growth" to "regional leadership" is perhaps the most significant indicator of Brazil's maturation, as companies like Ebanx and dLocal expand their Brazilian-refined technologies into markets in Africa and Asia.

Institutional Stability and the Legal Framework (LC 182/2021)

A critical component of Brazil’s appeal to international capital is the establishment of a clear and predictable legal framework. The enactment of Complementary Law No. 182, or the "Legal Framework for Startups," represented a landmark moment for the ecosystem. This legislation formalized innovative entrepreneurship as a vector for economic and social development, introducing several mechanisms that provide legal certainty to both founders and investors.

The law specifically addresses the risks associated with angel investment by providing that investors who do not hold management power are not liable for the startup's debts, including labor and tax obligations. This protection has been instrumental in unlocking local private capital, as it mitigates the traditional legal risks that previously deterred wealthy individuals and family offices from investing in high-risk ventures.

Key Feature of LC 182/2021 | Regulatory Impact | Strategic Benefit |

Mútuo Conversível (Convertible Debt) | Formalizes SAFE-like instruments. | Facilitates fast, low-bureaucracy early-stage funding. |

Regulatory Sandbox | Allows for experimental business models. | Enables innovation in highly regulated sectors like health and finance. |

Public Contract for Innovative Solutions (CPSI) | Simplifies government procurement. | Opens the B2G market for startups to solve public problems. |

Bidding Simplification | Reduces requirements for gov contracts. | Increases the competitiveness of small, agile tech firms in state tenders. |

Furthermore, recent judicial clarity has addressed one of the most contentious issues in the Brazilian ecosystem: the taxation of stock options. In late 2025, the Superior Court of Justice (STJ) and the Federal Supreme Court (STF) ruled that stock options generally have a "mercantile" or commercial nature rather than a strictly remunerative one. This ruling implies that Personal Income Tax ($IRPF$) should not be levied at the moment of exercise, but only at the stage of sale when a capital gain is realized. This interpretation is vital for startups that rely on stock options to attract and retain high-level technical talent in a competitive global market, as it prevents the imposition of a massive tax burden on illiquid assets.

Vertical Expansion I: Agribusiness and the Agtech Revolution

Agribusiness remains the engine of the Brazilian economy, contributing approximately 29% of the national GDP in 2025. This sector's integration into the digital economy has created one of the most dynamic Agtech ecosystems in the world. The Brazilian Agtech market reached a value of $638 million in 2025, driven by a record grain harvest of 333 million tons and increasing global demand for sustainable food supplies.

The growth of Agtech is propelled by a combination of improved rural connectivity and proactive government policy. As 5G and satellite internet penetrate deeper into the interior, Brazilian producers are adopting precision farming, remote sensing, and AI-driven analytics to maximize efficiency and adherence to environmental standards. The Ministry of Agriculture’s launch of the Electronic Platform for Agricultural Innovation in late 2025 has further accelerated this trend by connecting startups directly with research hubs and international investors.

Agtech Growth Driver | Operational Context | Future Outlook (2034) |

Sustainable Practices | Demand for regenerative and low-carbon farming tools. | Central to Brazil’s $25B carbon market potential. |

Biosolutions & NPP | Biological inputs for corn/soybean efficiency (e.g., UPL's Nuvita). | Shifts dependency away from chemical fertilizers. |

Autonomous Systems | Partnership between XAG and CNH for multifunctional drones. | Reduces labor costs and chemical waste. |

Market Valuation | $638 Million in 2025. | Projected to reach $1.56 Billion (10.46% $CAGR$). |

The integration of Agtech with the "Green Economy" is perhaps the most significant strategic trend. Brazil’s potential to sequester carbon through nature-based solutions is estimated to be worth billions. By 2025, the carbon credit market reached $2.7 billion, with nature-based removal projects—such as those by the startup Mombak—securing multi-million dollar contracts from global corporations like Google and Microsoft. This transition transforms the Brazilian agricultural sector from a source of emissions into a primary source of climate solutions, attracting a new class of "impact" venture capital.

Vertical Expansion II: Real Estate and the Proptech Surge

The Brazilian real estate market is undergoing a similarly profound transformation through the expansion of Proptech and Contech (Construction Technology). With a residential market size exceeding $106 billion and a commercial market over $92 billion, the opportunities for digitization are immense. Companies like QuintoAndar and Loft have already established themselves as market leaders by streamlining the painful processes of renting and selling residential property.

In 2025, the trend has shifted toward the "Smart Building" and industrialization of construction. Developers are increasingly using Building Information Modeling (BIM), robotics, and modular construction to reduce project delivery timelines by 30-50%. The commercial segment, which accounts for 56% of the Proptech market share, is leading the adoption of AI-powered property management and "Digital Twins" to optimize energy consumption and tenant experience.

Proptech/Contech Innovation | Financial Impact | Operational Benefit |

Digital Twins / AI | 8–12% higher sale valuations. | Real-time space booking and predictive maintenance. |

Modular Construction | 30% lower overall costs at scale. | 90% reduction in site waste and 70% fewer accidents. |

Mobile Platforms | 30% improvement in tenant retention. | Touchless access and instant maintenance requests. |

REIT Expansion | BRL 168 Billion market value (2024). | Diversifies financing sources for large-scale projects. |

The rise of Brazilian Real Estate Investment Trusts (REITs), which grew from BRL 20 billion in 2014 to BRL 168 billion in 2024, has provided a liquid exit for developers and a robust funding source for the next generation of logistics and office infrastructure. As São Paulo maintains its status as the region’s premier logistics hub—with vacancy rates for Class-A facilities dropping below 10%—Proptech startups are finding fertile ground in providing the software "brains" for these physical assets.

Technological Infrastructure: 5G and Data Center Expansion

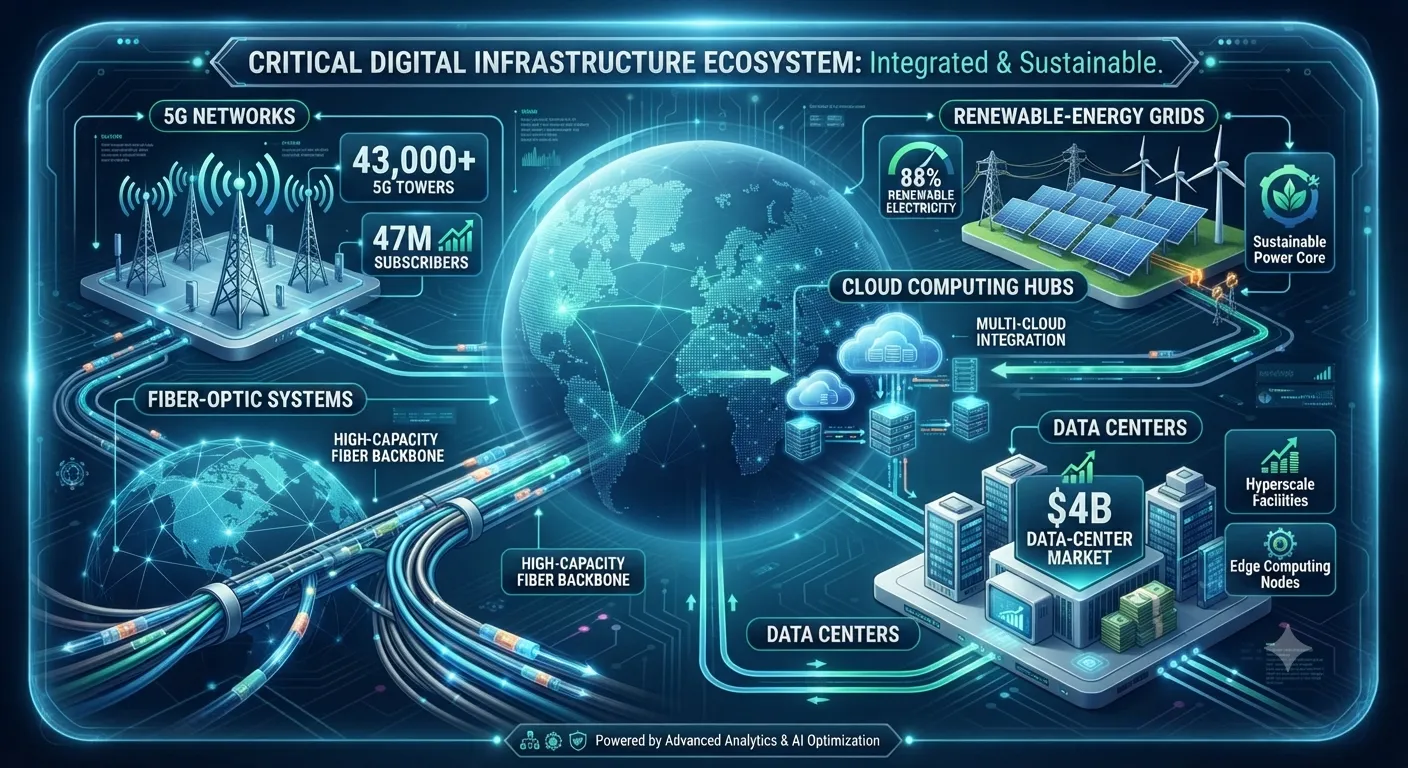

The physical "pipes" of the Brazilian startup powerhouse are expanding at an accelerated rate. The national 5G rollout, which concluded its frequency clearing 14 months ahead of schedule, has provided the high-speed, low-latency connectivity required for advanced digital services. By mid-2025, the leading mobile operators had deployed over 43,000 5G cell sites, covering more than 60% of the population in over 500 municipalities.

Operator | 5G Cell Sites (May 2025) | Population Coverage | 5G Subscriptions |

Vivo | 17,184 | 63.2% | 19.2 Million |

Claro Brasil | 12,595 | 54.0% | 16.1 Million |

TIM Brasil | 13,189 | 62.3% | 11.6 Million |

Total | 42,968 | Average >60% | ~47 Million |

Complementing this mobile connectivity is the boom in the data center market. Brazil has emerged as the data hub for South America, with a market valuation of $4.0 billion in 2025 and an expected $CAGR$ of 9.50% through 2034. This growth is driven by the shift toward cloud computing and the specific demands of AI-driven analytics. Organizations like Scala Data Centers are pioneering the use of advanced infrastructure, such as hollow-core fiber, to achieve the low-latency connectivity necessary for real-time automation and complex workloads.

The availability of clean energy also provides a unique strategic advantage for Brazil’s digital infrastructure. With 88% of its electricity coming from renewable sources, Brazil offers a sustainable base for energy-intensive data centers and industrial plants, making it an attractive destination for multinational tech firms looking to meet ESG commitments while scaling their cloud footprints.

The Fiscal Environment and the Transition to Dual VAT

One of the most significant challenges—and potential opportunities—facing the Brazilian ecosystem is the comprehensive consumption tax reform currently underway. The transition from a fragmented system of five taxes (PIS/Pasep, Cofins, IPI, ICMS, and ISS) to a Dual VAT structure ($CBS$ at the federal level and $IBS$ at the state/municipal level) aims to simplify compliance and eliminate the "tax wars" that have historically complicated interstate operations.

While the reform promises a more transparent and efficient system by 2032, the short-term transition presents operational hurdles. IT companies and startups, which previously benefited from simpler cumulative taxation, may face an increase in the real tax burden, with some estimates suggesting a total VAT rate of approximately 26.5% to 28%. However, the new system allows for the writing off of tax credits on inputs—such as cloud services and hardware—which may encourage greater capital investment in technology.

Tax Reform Phase | Implementation Activity | Strategic Implication for Startups |

2025 | Publication of complementary laws ($CBS$ & $IBS$). | Start of accounting and ERP system restructuring. |

2026 | Approval of special regimes and sector-specific rules. | Finalization of tax strategy for the transition period. |

2027 | Start of $CBS$ (Federal) collection. | Elimination of PIS/Cofins; initial credit recovery. |

2032 | Full implementation of Dual VAT. | Unified, simplified compliance; end of regional tax benefits. |

The reform also introduces a "Selective Tax" (IS) targeting products with negative health or environmental impacts and a "Cashback" mechanism to return taxes to low-income populations, reflecting a modern approach to social-fiscal policy. For startups, the key will be adapting internal processes and ERP systems to the new alphanumeric $CNPJ$ and electronic invoicing requirements, a transition where specialized technology providers like Ecosistemas Global are finding significant demand for their integration services.

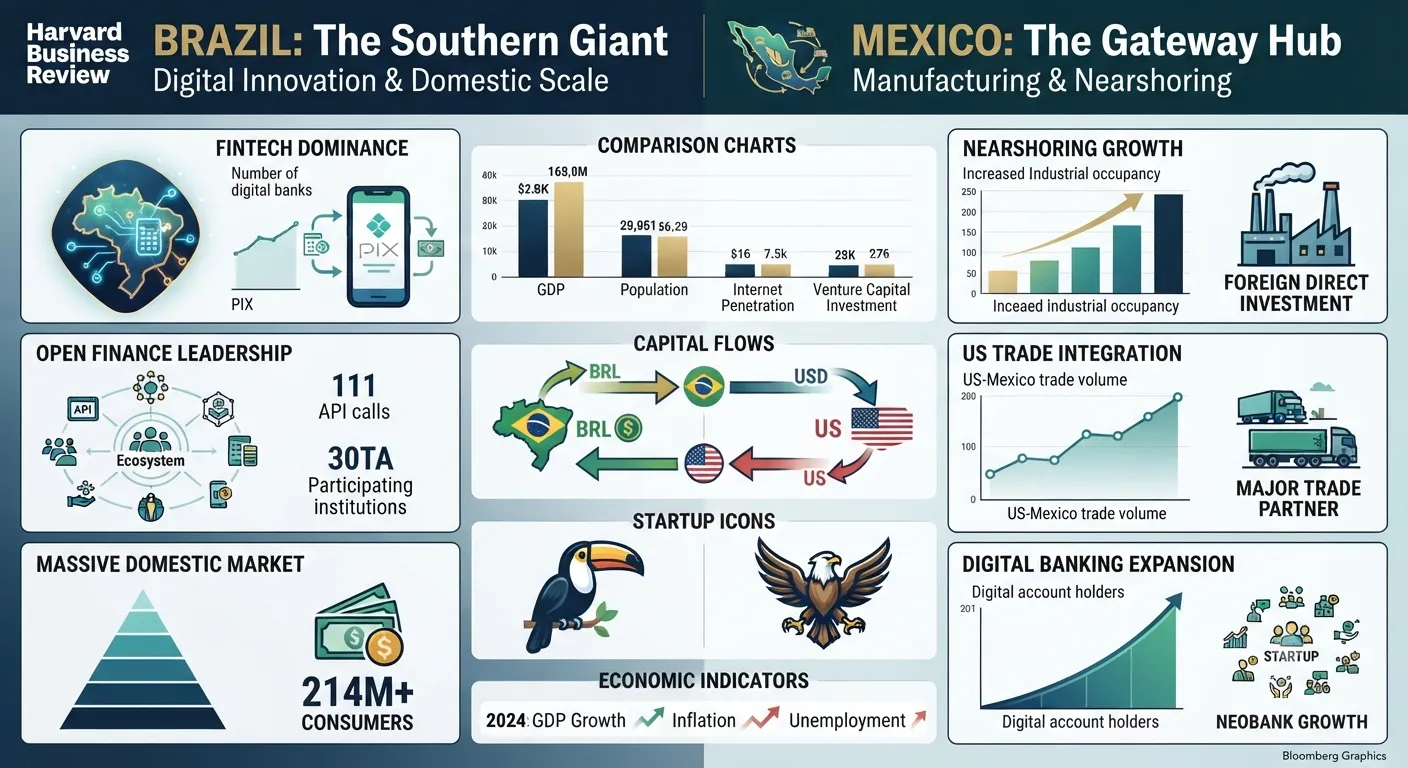

Regional Competition: Brazil vs. Mexico and the Rising Tide

The narrative of Brazil as a startup powerhouse is increasingly a comparative one. The competition with Mexico for regional dominance has intensified, creating a "bipolar" innovation landscape in Latin America. In early 2025, Mexico achieved a historic milestone by overtaking Brazil in total venture capital dollars for a single quarter, driven by massive rounds for digital banking platforms. This surge was fueled by Mexico’s proximity to the United States and a push for financial inclusion in its own massive, underbanked market.

However, the Brazilian ecosystem remains structurally more mature. São Paulo remains the region's undisputed tech hub, with a "deep talent pool" and an internal economy that provides a more resilient base than Mexico’s export-heavy model. Furthermore, Brazil's regulatory leadership—particularly in Open Finance and instant payments—has set a global benchmark that Mexico and other nations are only beginning to replicate.

Startup City (Global Rank) | Country | Fintech Global Rank | Ecosystem Score Relative to Next Best |

São Paulo (#23) | Brazil | #5 Worldwide | 8x higher than Rio de Janeiro. |

Mexico City (#43) | Mexico | #13 Worldwide | Centralized but growing faster in fintech. |

Bogotá (#62) | Colombia | Top 100 | Dynamic, highest regional growth rate. |

Buenos Aires (#77) | Argentina | Top 100 | Strong human capital; macroeconomic risk. |

Other ecosystems like Colombia and Chile are also finding their niches. Colombia boasts the highest growth rate in the region at over 22%, while Chile is rebounding from years of decline through active policy and improved access to talent. Argentina, despite its ongoing currency volatility and high inflation, continues to "punch above its weight" in terms of innovation capacity, consistently producing high-level developers and founders who are resilient to market shocks.

Conclusions: The Strategic Outlook for 2030

The ascension of Brazil as Latin America's startup powerhouse is the result of a rare convergence of market scale, visionary regulation, and a cultural embrace of digital transformation. By 2025, the ecosystem has moved beyond its "emerging" phase to become a mature, institutionalized pillar of the global technology economy. The "Brazil Stack" has created a level of transaction efficiency that rivals developed economies, while the country’s natural resources and renewable energy matrix provide a unique foundation for the next wave of green technology and AI infrastructure.

The challenges that remain—primarily the complexity of the tax transition and the persistence of high interest rates—are being addressed through systemic reforms and a maturing domestic capital market. The "VC Winter" of the early 2020s has left the ecosystem more resilient, with founders now focused on profitability and specialized, high-value solutions. As we look toward 2030, Brazil is not just competing to be the leader of Latin America; it is positioning itself to be a primary architect of the global digital economy, exporting its refined financial technologies and sustainable innovations to the rest of the world. For international investors and corporate partners, the question is no longer whether to be in Brazil, but how to deeply integrate into an ecosystem that is increasingly setting the pace for the global south.

Protect Your Future: The Precision Vesting Calculator

Don't let a "handshake deal" complicate your exit. Map out your ownership journey with our Vesting Calculator

Calculate Your Vesting Schedule →