The Unique Challenges of Building a Startup in Brazil

March 9, 2026 by Harshit Gupta

The Brazilian startup ecosystem in 2026 stands as a profound paradox within the global emerging markets landscape. It is a territory where world-class digital sophistication—typified by the universal adoption of instant payments and a burgeoning pool of 760,000 software developers—collides with an institutional framework of staggering complexity. For founders and investors, the challenge of building a scalable venture in Brazil is defined by the "Custo Brasil" (the Brazil Cost), a systemic accumulation of structural, legal, and economic hurdles that demand a level of operational resilience rarely required in more streamlined markets. As the largest economy in Latin America, Brazil accounts for approximately 55% of the region’s startups and hosts 19 unicorns, yet the path to these milestones is obstructed by a 15% benchmark interest rate, a multi-decade transition to a new tax regime, and a labor code that remains among the most protective in the world.

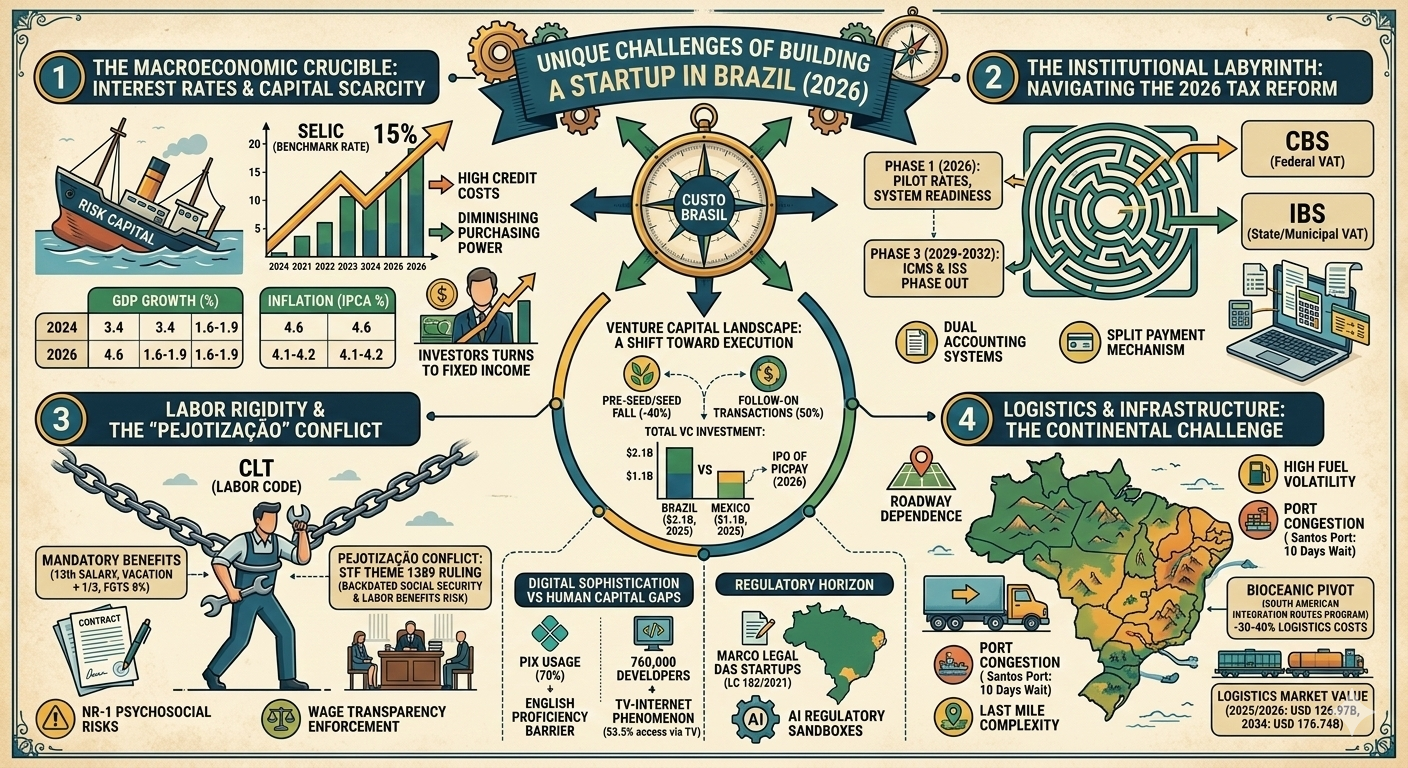

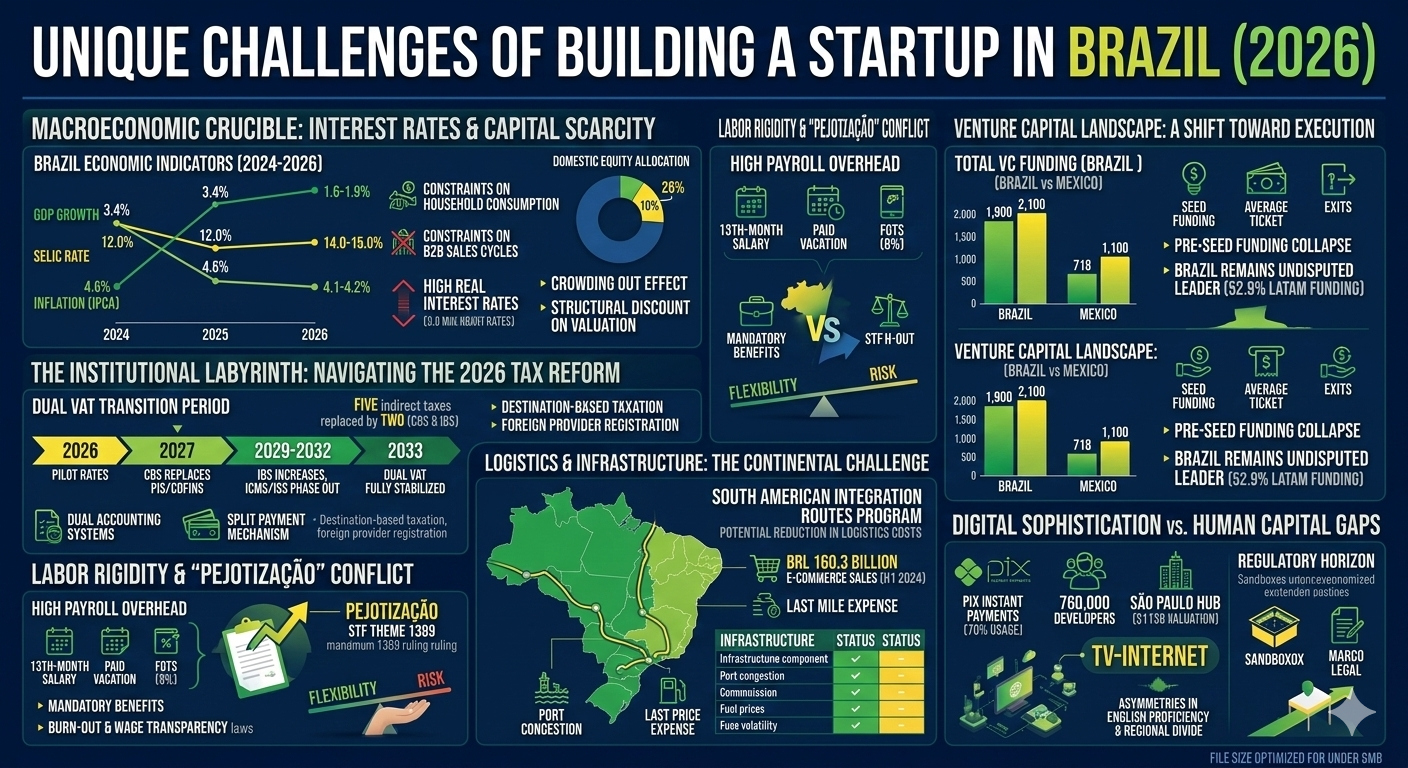

The Macroeconomic Crucible: Interest Rates and Capital Scarcity

The most immediate and pervasive challenge for any Brazilian startup in 2026 is the restrictive monetary environment. The Central Bank of Brazil has maintained the Selic (benchmark interest rate) at approximately 15%, making it one of the highest real interest rates in any major global economy. This policy is not merely a technical adjustment but a fundamental constraint on the availability of risk capital and the growth potential of consumer-facing businesses. The high Selic rate creates a "crowding out" effect, where domestic investors find the risk-adjusted returns of government-backed fixed-income instruments more attractive than equity investments in early-stage ventures.

The implications for venture capital are significant. As of late 2025, domestic equity allocations in Brazil plummeted to approximately 10% of total investments, a sharp decline from the 26% seen during the liquidity surge of 2020-2021. This shift has led to a structural discount in the valuation of Brazilian startups. Even high-performing entities often trade at a forward price-to-earnings ratio of 8.3x, which is one standard deviation below historical averages. For founders, this means that achieving a "unicorn" valuation requires significantly higher revenue and profitability metrics than would be expected for a peer company in North America or India.

The high interest rate environment also dampens household consumption and corporate spending. GDP growth is projected to slow from 3.4% in 2024 to an estimated 1.6% in 2026. This deceleration is particularly evident in the services sector—the primary engine of the Brazilian economy—which saw growth slow to 1.8% in 2025. Startups operating in the B2C space must contend with a consumer base that faces high credit costs and diminishing purchasing power, while B2B SaaS companies face elongated sales cycles as corporate clients prioritize cash preservation over digital transformation.

Economic Indicator | 2024 (Actual) | 2025 (Estimated) | 2026 (Projected) |

GDP Growth (%) | 3.4 | 2.3 | 1.6 - 1.9 |

Selic Rate (%) | 12.0 | 15.0 | 14.0 - 15.0 |

Inflation (IPCA %) | 4.6 | 4.4 - 5.1 | 4.1 - 4.2 |

Household Consumption Growth (%) | 5.1 | 1.3 | 1.1 |

The Institutional Labyrinth: Navigating the 2026 Tax Reform

If high interest rates represent the immediate barrier to capital, Brazil’s tax system represents the most significant long-term operational hurdle. Long recognized as the most complex in the world, the Brazilian tax regime is currently undergoing a structural transformation that, while aimed at simplification, introduces a period of unprecedented administrative burden for startups.

The 2026 tax reform introduces a dual Value Added Tax (VAT) model, replacing five fragmented indirect taxes—PIS, COFINS, IPI, ICMS, and ISS—with two new components: the Contribution on Goods and Services (CBS) at the federal level and the Tax on Goods and Services (IBS) at the state and municipal levels. For startups, the challenge lies in the "Test Year" of 2026 and the subsequent seven-year transition period. During this time, companies must operate dual accounting systems, complying with both the legacy and the new regimes simultaneously. This requires a radical reassessment of internal financial governance and a significant investment in automated tax determination tools to handle the shifting rates.

A critical operational change introduced in 2026 is the "split payment" mechanism. Under this new model, the tax portion of any electronic invoice is automatically remitted to the relevant government account at the moment of payment by the customer. While this mechanism is designed to combat evasion, it fundamentally alters the cash flow dynamics of startups. In the previous regime, companies could often utilize tax credits or defer payments to manage short-term liquidity. In the 2026 framework, tax credits for CBS and IBS are only recognized after the corresponding tax has been paid by the supplier, creating a potential working capital gap for companies with low margins or long payment terms.

Phase | Timeline | Primary Tax Actions |

Phase 1 | 2026 | Pilot rates (CBS 0.9%, IBS 0.1%); mandatory system readiness. |

Phase 2 | 2027 | CBS fully replaces PIS and COFINS; IPI rates reduced. |

Phase 3 | 2029 - 2032 | IBS gradually increases; ICMS and ISS phase out by 10% annually. |

Phase 4 | 2033 | Legacy system fully abolished; dual VAT fully stabilized. |

Source:

Furthermore, the tax reform introduces a destination-based taxation model for e-commerce and digital services. For a startup based in São Paulo selling software to a customer in Manaus, this means navigating the municipal tax rules of the consumer's location rather than the seller's. For foreign digital service providers, the reform mandates direct registration in the Brazilian tax system, shifting the burden of tax collection from the Brazilian customer to the international supplier. This requirement acts as a significant barrier for global startups looking to enter the Brazilian market with lean operations.

Labor Rigidity and the "Pejotização" Conflict

The Brazilian labor market is governed by the Consolidação das Leis do Trabalho (CLT), a framework that provides high levels of worker protection but imposes significant financial and legal risks on startups. Payroll overhead in Brazil is among the highest globally, with mandatory benefits and social security contributions often increasing the total cost of an employee to double their base salary.

Core mandatory benefits include the "13th-month salary" (a full month's bonus paid annually), 30 days of paid vacation with a 1/3 vacation bonus, and mandatory contributions to the Fundo de Garantia do Tempo de Serviço (FGTS), a 8% monthly deposit into a severance indemnity fund. For early-stage startups with limited runway, these fixed costs can severely constrain hiring capacity.

To mitigate these costs, many startups have historically utilized "Pejotização"—the practice of hiring workers as independent contractors through their own legal entities (Pessoas Jurídicas) rather than as formal CLT employees. However, 2026 marks a turning point for this practice. The Federal Supreme Court (STF) is set to rule on Theme 1389, which will establish binding parameters for the legality of such arrangements. This ruling has profound implications; if the court decides against the practice in cases where the relationship exhibits subordination and regularity, startups could face massive liabilities for backdated social security (INSS) and labor benefits.

Beyond financial costs, new regulatory requirements in 2026 increase the complexity of labor compliance. Regulatory Norm No. 1 (NR-1) now mandates that companies include psychosocial risks, such as burnout and work-related stress, in their statutory Risk Management Programs. Additionally, the Ministry of Labor has intensified enforcement of wage transparency laws, where non-compliance can result in fines of up to 3% of the total payroll. These measures reflect a broader shift toward institutionalizing social governance, requiring startups to implement sophisticated HR and legal monitoring systems earlier in their lifecycle than in other jurisdictions.

Logistics and Infrastructure: The Continental Challenge

Building a startup in Brazil requires an understanding of its unique geographic and logistical constraints. As a "continental-sized" nation, Brazil faces significant bottlenecks in connecting its dispersed production hubs to coastal export terminals and urban consumer centers. For e-commerce and logistics startups, the "last mile" is often the most expensive and complex part of the supply chain.

Brazil’s infrastructure remains heavily dependent on roadway transport, which accounts for the vast majority of internal freight. This reliance makes the logistics sector highly sensitive to fuel price volatility and the varying quality of road networks across different states. In the North and Northeast, infrastructure degradation during seasonal weather patterns can lead to significant delays and increased maintenance costs for delivery fleets.

Port congestion is another critical hurdle. The Port of Santos, which handles a significant portion of Brazil’s international trade, frequently experiences vessel wait times of up to 10 days. While digital freight platforms are emerging to optimize trucking efficiency and reduce empty miles, the underlying physical infrastructure often fails to keep pace with the growth of e-commerce, which saw record sales of BRL 160.3 billion in the first half of 2024.

However, 2026 also brings strategic opportunities through the "South American Integration Routes Program." This $10 billion initiative aims to connect Brazil’s industrial and agricultural heartlands with Chilean Pacific ports, creating a land-based alternative to the Atlantic maritime routes. For startups in the agribusiness and industrial sectors, this "Bioceanic Pivot" could reduce logistics costs by 30-40% and shorten transit times to Asian markets, particularly China.

Infrastructure Component | Current Status (2025/2026) | Strategic Objective (2030+) |

Average Port Dwell Time | 3.2 Days | 2.5 Days |

Electronic Customs Capability | 72% | 85% |

Road Network Coverage | 1.7M Kilometers | Expansion of Paved Arteries |

Logistics Market Value | USD 126.97 Billion | USD 176.74 Billion (by 2034) |

Source:

The Venture Capital Landscape: A Shift toward Execution

The venture capital market in Brazil has moved past the "growth at all costs" era of 2021 into a more disciplined, execution-focused cycle. Total venture investment in 2025 reached approximately $2.1 billion, representing a gradual recovery but still well below the historical peaks. Investors have become significantly more selective, with 50% of all early-stage checks in recent years going toward follow-on transactions rather than new opportunities.

A concerning trend for the long-term health of the ecosystem is the collapse of pre-seed funding, which fell by 40% in capital and 39.4% in deal count in 2025. This creates a narrowing pipeline for future Series A and B rounds. Conversely, growth-stage deals (Series C+) have also contracted, with investors demanding rigorous operational excellence and a credible path to profitability before committing late-stage capital.

Despite these constraints, Brazil remains the undisputed leader in Latin American VC, attracting 52.9% of all regional funding in 2025. The maturity of the market is evidenced by a surge in exit activity, which reached $4.9 billion across 63 transactions in 2025. The early 2026 IPO of PicPay on the Nasdaq signaled a cautious return of the public market for high-quality Brazilian tech assets, albeit at more conservative valuations that reflect the current high-rate environment.

Funding Stage | 2024 (US$M) | 2025 (US$M) | % Change |

Pre-Seed/Seed | 110 | 66 | -40.0% |

Total VC (Brazil) | 1,900 | 2,100 | +10.5% |

Total VC (Mexico) | 718 | 1,100 | +53.2% |

Avg. Ticket (Brazil) | 5.2 | 5.6 | +7.7% |

Source:

Digital Sophistication vs. Human Capital Gaps

Brazil’s digital prowess is a significant competitive advantage. The country boasts one of the world’s most advanced instant payment systems, Pix, which is used by 70% of the population and has democratized financial services just six years after its launch. Brazil also has the largest pool of software developers in Latin America—estimated at 760,000—and produces more IT graduates annually than many European nations.

However, this talent pool is characterized by deep asymmetries. While Brazil ranks well in competitive programming (14th-17th globally), English proficiency remains a significant barrier for global integration. Furthermore, the digital divide remains stark. Although 89.1% of the population uses the internet, access is unevenly distributed across income levels and regions. A unique challenge for Brazilian startups is the "TV-internet" phenomenon: more than half of internet users (53.5%) access the web via a TV, a rate that is significantly higher among lower-income households. This has profound implications for user experience design, particularly for Edtech and productivity startups, as a large portion of the target audience may lack a personal computer for complex interactions.

The concentration of tech talent is also geographically skewed. São Paulo remains the dominant hub, valued at $113 billion and ranking among the world’s top 30 ecosystems. Other hubs like Florianópolis and Recife offer specialized strengths—Florianópolis in B2B SaaS and Recife in IT services and urban innovation—but the "brain drain" to São Paulo or international markets remains a persistent threat for regional startups.

The Regulatory Horizon: Marco Legal and AI Sandboxes

To foster innovation in the face of institutional complexity, Brazil has implemented the "Marco Legal das Startups" (Supplementary Law 182/2021). This framework provides much-needed legal certainty for angel investors and formalizes investment instruments like convertible debt. It also introduced the concept of the "regulatory sandbox," allowing startups to test innovative products under a controlled environment with temporary regulatory exemptions.

In 2025 and 2026, these sandboxes have become critical for the development of emerging technologies like AI. The National Data Protection Authority (ANPD) launched an AI regulatory sandbox in 2025, prioritizing projects that use generative AI to solve public sector challenges or foster Brazilian "AI sovereignty" through Portuguese-language models. In the insurance sector, the SUSEP sandbox has already enabled 21 innovative projects to receive temporary authorization, with several successfully transitioning to permanent licensure by late 2025.

These initiatives demonstrate a proactive stance from the Brazilian government to modernize its regulatory framework. However, the impact of these sandboxes is often limited by a lack of coordination across different federal and state agencies, leaving startups to navigate a "patchwork" of regulations even within supervised environments.

Regional Dynamics: The Multi-Polar Ecosystem

While São Paulo state remains the "gateway" for innovation, accounting for 55% of the country’s deep tech ventures, Brazil is increasingly a multi-polar ecosystem.

Florianópolis: Known as a "model for mid-sized hubs," the city’s tech sector contributes 25% of its GDP. Its strength lies in knowledge-intensive, B2B-focused software ventures with deep university ties.

Recife (Porto Digital): This hub has revitalized the city’s historic center, growing from two companies to 475 in 25 years. It is a global leader in integrating academic research with corporate innovation, particularly in enterprise IT and creative industries.

The Amazon Hubs (Belém, Manaus): Driven by the hosting of COP30 in 2025, these cities are emerging as centers for biotechnology, regenerative agriculture, and carbon credit innovation.

This regionalization allows startups to build solutions tailored to specific local industries—such as Agtech in the Central-West or Biotech in the North—but it also complicates the scaling process, as startups must adapt to varying municipal regulations and logistics capabilities.

Conclusion: Strategy in a High-Friction Environment

Building a startup in Brazil is not for the faint of heart. It requires a nuanced understanding of a "dual-VAT" tax transition, a resilient approach to 15% interest rates, and a proactive legal strategy to manage the rigidities of the CLT labor code. However, the rewards for those who navigate this labyrinth are substantial. Brazil’s massive domestic market, combined with its leadership in digital finance and its role as a "green powerhouse" in the global energy transition, offers a unique platform for high-impact innovation.

The startups that succeed in Brazil are those that treat regulatory and institutional challenges as core product features rather than external hurdles. By leveraging the "Brazil Stack" of digital infrastructure and adopting a "compliance-first" mentality, founders can build ventures that are not only dominant in South America but are also fundamentally prepared for the complexities of other global emerging markets. The "Custo Brasil" is undeniable, but the "Opportunity Brazil" remains one of the most compelling narratives in the technological future of 2026.

Read More -

1. From Idea to MVP: A Step-by-Step Guide for Solo Founder

🔗 https://findnstart.com/blogs/from-idea-to-mvp-a-step-by-step-guide-for-solo-founder

2. How to Validate Your Startup Idea in 48 Hours for $0

🔗 https://findnstart.com/blogs/how-to-validate-your-startup-idea-in-48-hours-for-0

3. Remote vs. Local: Does Your Co-Founder Need to Live in the Same City?

🔗 https://findnstart.com/blogs/remote-vs-local-does-your-co-founder-need-to-live-in-the-same-city

4. The 2026 Startup Landscape: What Has Fundamentally Changed (and Why Founder Skills Matter More Than Ever)

5. The Most In-Demand Skills for Startup Founders in 2026

🔗 https://findnstart.com/blogs/the-most-in-demand-skills-for-startup-founders-in-2026

6. How to Find a Technical Co-Founder (Without a Six-Figure Salary)

🔗 https://findnstart.com/blogs/how-to-find-a-technical-co-founder-without-a-six-figure-salary

7. 5 Red Flags to Look for When Choosing a Startup Partner

🔗 https://findnstart.com/blogs/5-red-flags-to-look-for-when-choosing-a-startup-partner

8. How to Pitch Your Idea to Potential Co-Founders

🔗 https://findnstart.com/blogs/how-to-pitch-your-idea-to-potential-co-founders

9. How to Build a Portfolio that Attracts High-Growth Startup Founders

🔗 https://findnstart.com/blogs/how-to-build-a-portfolio-that-attracts-high-growth-startup-founders

10. Equity vs. Salary: How to Split Ownership with Your First Teammate

🔗 https://findnstart.com/blogs/equity-vs-salary-how-to-split-ownership-with-your-first-teammate

11. Why Joining an Early-Stage Startup is Better Than a Corporate Job

🔗 https://findnstart.com/blogs/why-joining-an-early-stage-startup-is-better-than-a-corporate-job

12. The Future of EdTech: Why Developers and Educators Need to Team Up Now

🔗 https://findnstart.com/blogs/the-future-of-edtech-why-developers-and-educators-need-to-team-up-now

13. The Architecture of Symbiosis: Analytical Perspectives on the Five Habits of Successful Startup Duos

14. Finding a Co-Founder in the AI Space: What Skills Should You Look For?

🔗 https://findnstart.com/blogs/finding-a-co-founder-in-the-ai-space-what-skills-should-you-look-for

15. Overcoming Analysis Paralysis and the Strategic Path to Execution

🔗 https://findnstart.com/blogs/overcoming-analysis-paralysis-and-the-strategic-path-to-execution

16. From College Project to Company: How to Find Your Student Co-Founder

🔗 https://findnstart.com/blogs/from-college-project-to-company-how-to-find-your-student-co-founder

17. How to Start a Startup While Working a Full-Time Job

🔗 https://findnstart.com/blogs/how-to-start-a-startup-while-working-a-full-time-job

18. How to Build a HealthTech Startup Without a Medical Degree

🔗 https://findnstart.com/blogs/how-to-build-a-healthtech-startup-without-a-medical-degree

19. The Solitary Architect: Executive Isolation in Entrepreneurship

20. The 2026 Guide to Launching a SaaS as a Solo Developer

21. What Sustainable Growth Actually Looks Like

🔗 https://findnstart.com/blogs/what-sustainable-growth-actually-looks-like

22. The Early Warning Signs Your Startup Is in Trouble

🔗 https://findnstart.com/blogs/the-early-warning-signs-your-startup-is-in-trouble

23. How to Grow Without Burning Out

🔗 https://findnstart.com/blogs/how-to-grow-without-burning-out

24. The Truth About “Runway” Most Founders Ignore

🔗 https://findnstart.com/blogs/the-truth-about-runway-most-founders-ignore

25. Revenue Solves More Problems Than Funding

🔗 https://findnstart.com/blogs/revenue-solves-more-problems-than-funding

26. What No One Tells You About Being a Solo Founder

🔗 https://findnstart.com/blogs/what-no-one-tells-you-about-being-a-solo-founder

27. Why Smart People Quit High-Paying Jobs to Build Startups (And Why Most Regret It)

28. Why Most Startup Advice on Twitter Is Dangerous

🔗 https://findnstart.com/blogs/why-most-startup-advice-on-twitter-is-dangerous

29. Decision Fatigue: The Silent Startup Killer

🔗 https://findnstart.com/blogs/decision-fatigue-the-silent-startup-killer

30. Fear vs Logic: How Founders Actually Make Decisions

🔗 https://findnstart.com/blogs/fear-vs-logic-how-founders-actually-make-decisions

31. How Overthinking Destroys Early Momentum

🔗 https://findnstart.com/blogs/how-overthinking-destroys-early-momentum

32. Ideas Don’t Scale. Systems Do.

🔗 https://findnstart.com/blogs/ideas-dont-scale-systems-do

33. The First Hire That Actually Matters

🔗 https://findnstart.com/blogs/the-first-hire-that-actually-matters

34. How the First 100 Users Decide Your Startup’s Fate

🔗 https://findnstart.com/blogs/how-the-first-100-users-decide-your-startups-fate

35. Why Your Startup Doesn’t Need Growth — It Needs Focus

🔗 https://findnstart.com/blogs/why-your-startup-doesnt-need-growthit-needs-focus

36. Why Most Startups Die Quietly

🔗 https://findnstart.com/blogs/why-most-startups-die-quietly

37. Lessons Learned Too Late by First-Time Founders

🔗 https://findnstart.com/blogs/lessons-learned-too-late-by-first-time-founders

38. The Myth of the “Overnight Success” Startup

🔗 https://findnstart.com/blogs/the-myth-of-the-overnight-success-startup