The Rise of Tier-2 Founders Moving to Bangalore

March 10, 2026 by Harshit Gupta

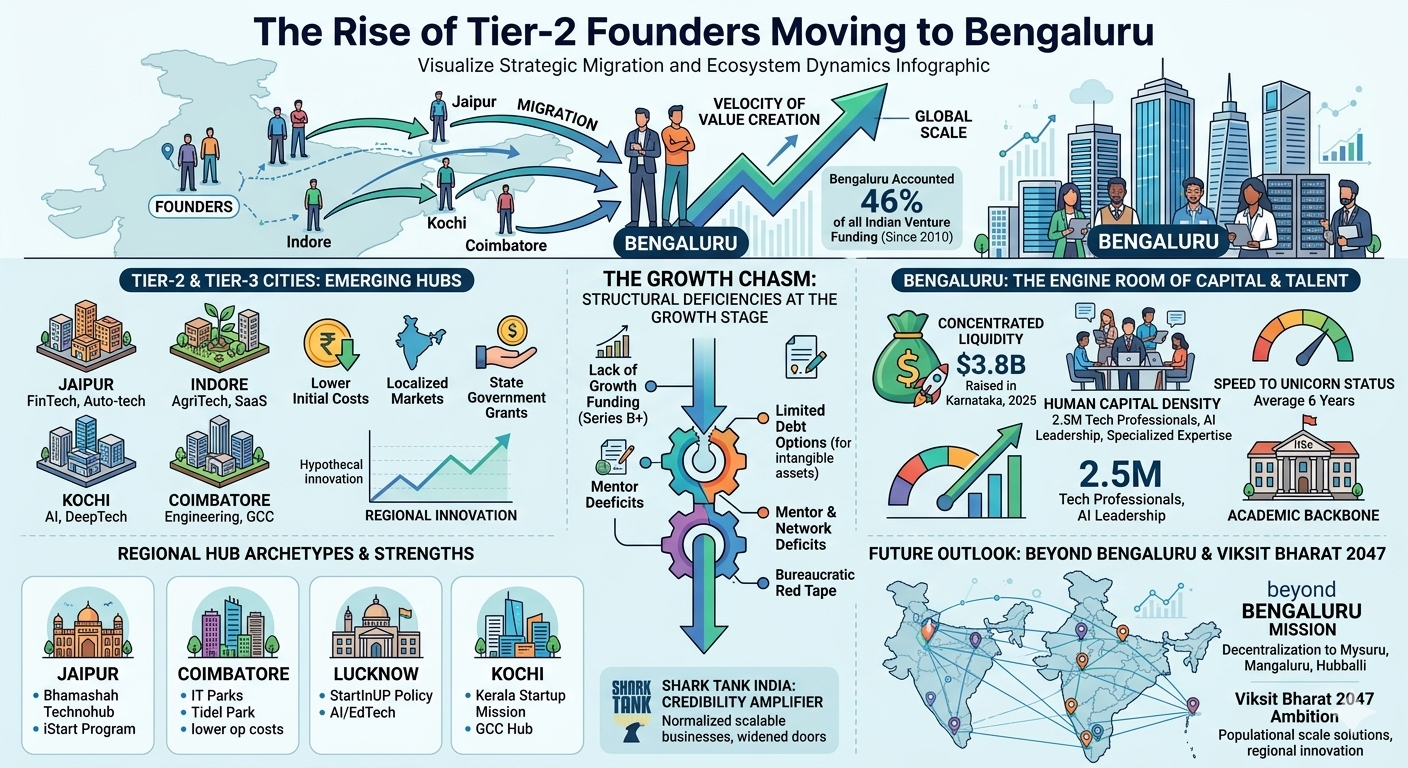

The Indian entrepreneurial landscape is currently defined by a profound geographical paradox. While the democratization of digital infrastructure has enabled nearly fifty percent of the nation’s recognized startups to emerge from Tier-2 and Tier-3 cities, a strategic migration is occurring at the growth stage. Founders from emerging hubs such as Jaipur, Indore, Kochi, and Coimbatore are increasingly relocating their headquarters to Bengaluru to navigate the transition from product validation to global scale. This movement is not a rejection of regional origins but a calculated response to the concentrated liquidity, specialized human capital density, and the "velocity of value creation" that defines the Karnataka capital. As of 2025, Bengaluru remains the undisputed engine room of Indian capital deployment, accounting for forty-six percent of all venture funding raised in the country since 2010. This report examines the structural drivers of this migration, the funding chasm at the growth stage in regional hubs, and the evolving role of Bengaluru as the definitive finisher for India’s high-potential ventures.

The Dual-Speed Growth Trajectory: Tier-1 Muscle vs. Tier-2 Momentum

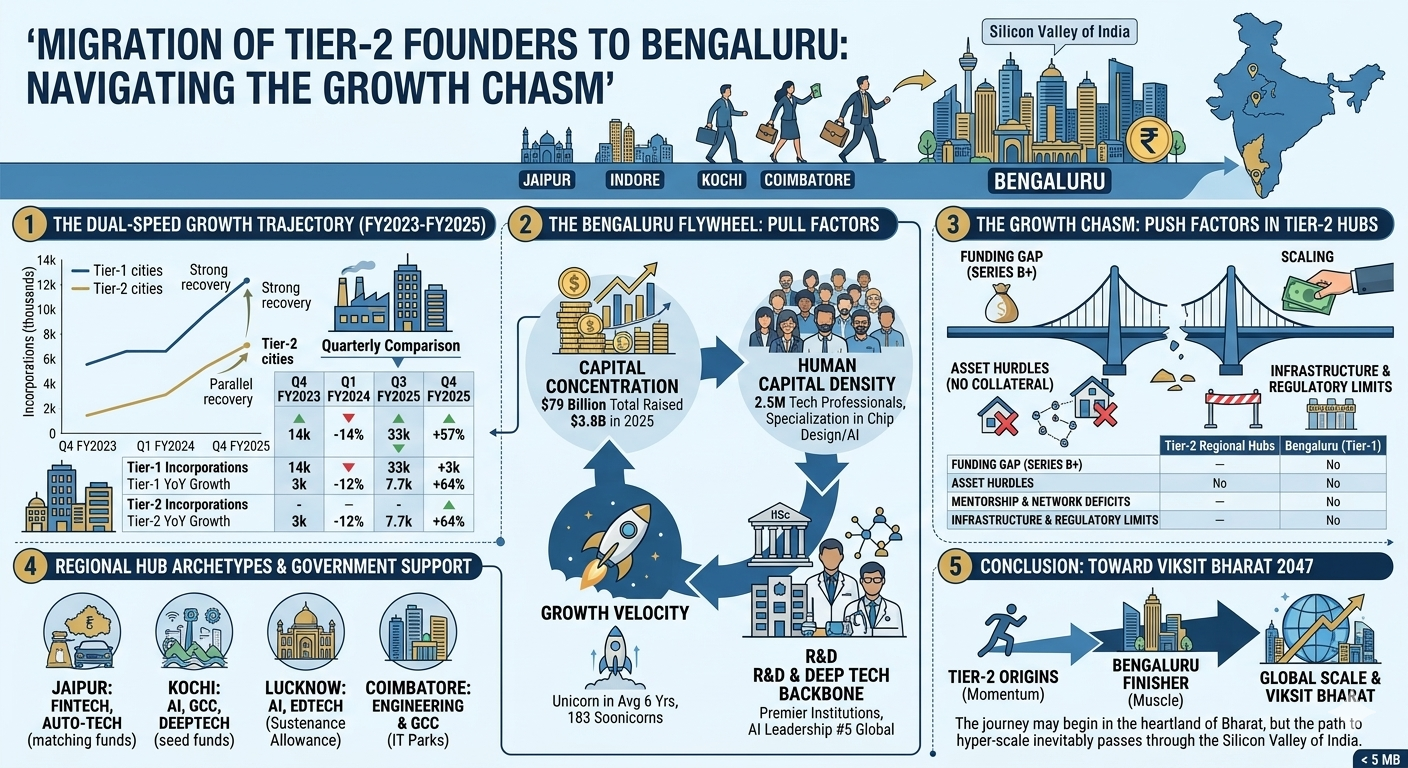

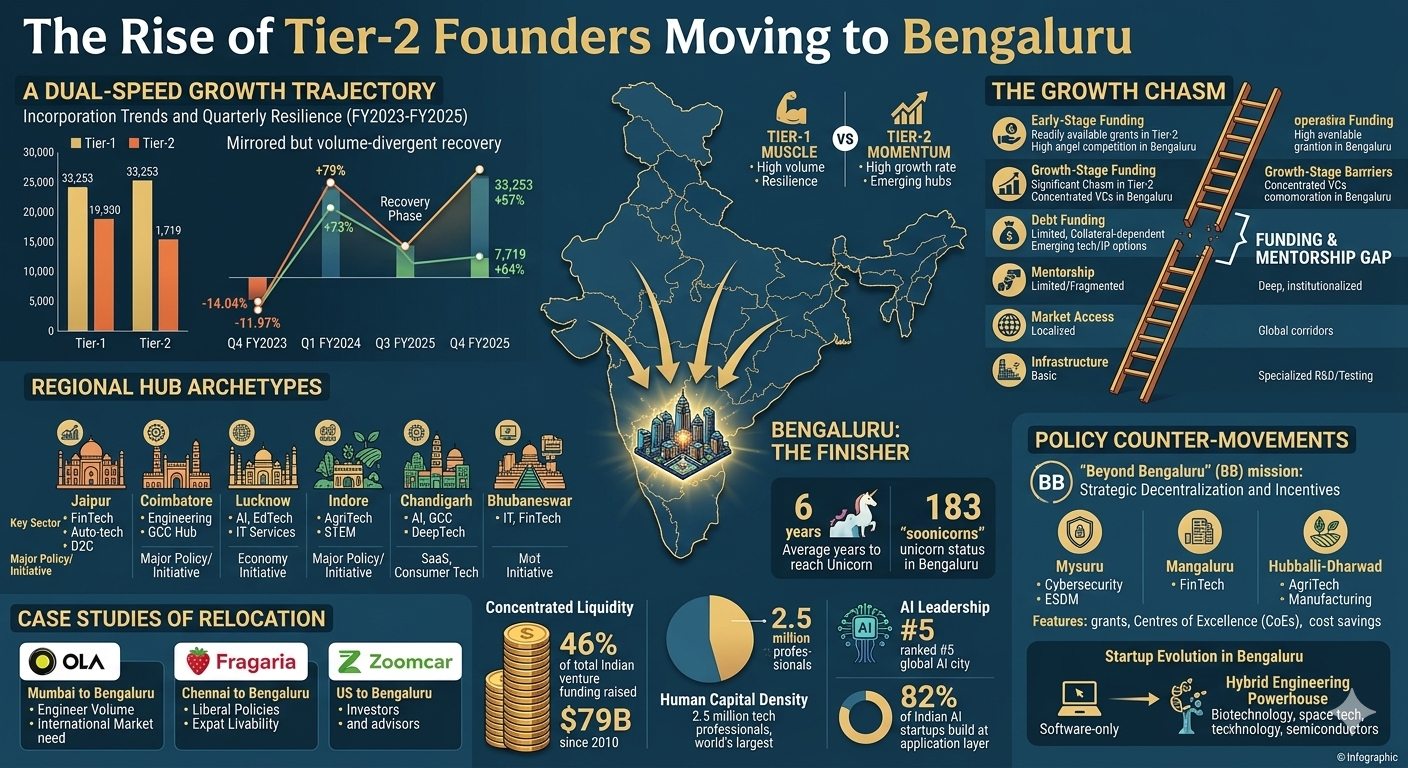

The period between 2017 and 2025 witnessed a dramatic transformation in India’s startup geography. Tier-2 cities doubled their formal incorporations, rising from 10,943 in 2017 to over 23,328 in 2025. This surge represents the steady formalization of regional business landscapes, fueled by over thirty active state-level startup policies. However, the growth intensity and resilience vary significantly between tiers. While Tier-1 cities like New Delhi, Mumbai, and Bengaluru continue to lead in absolute volume, Tier-2 cities such as Jaipur and Lucknow exhibit amplified volatility and cyclical recovery trends.

In the FY2024-2025 resurgence, both tiers showed synchronized recovery following the 2023 downturn. Tier-1 cities experienced a twenty-six percent surge in 2024—the highest annual jump in recent datasets—while Tier-2 cities saw a similar recovery of twenty-five percent. Despite this parity in momentum, the absolute volume of incorporations remains heavily skewed toward the metros. By Q4 FY2025, Tier-1 cities recorded 33,253 incorporations compared to 7,719 in Tier-2 hubs. This volume gap reflects the deeper maturity of the metro ecosystems, which provide the "muscle" required for high-stakes coordination and market entry.

Incorporation Trends and Quarterly Resilience (FY2023-FY2025)

The following table illustrates the synchronized but divergent volume recovery between the two tiers of the Indian startup ecosystem.

Fiscal Quarter | Tier-1 Incorporations | Tier-1 YoY Growth | Tier-2 Incorporations | Tier-2 YoY Growth |

Q4 FY2023 | 14,256 | -14.04% | 3,323 | -11.97% |

Q1 FY2024 | 25,477 | +79% (v Q4) | 5,757 | +73% (v Q4) |

Q3 FY2025 | 21,148 | Recovery Phase | 4,696 | Recovery Phase |

Q4 FY2025 | 33,253 | +57% (v Q3) | 7,719 | +64% (v Q3) |

Data source: Analysis of private market incorporation data and regional growth intensities.

The Bengaluru Flywheel: Pull Factors and the Engine Room of Capital

The primary driver for the migration of Tier-2 founders is the self-reinforcing flywheel of the Bengaluru ecosystem. The city is currently the fastest-growing urban center in the world regarding GDP growth projections for the next fifteen years, positioning it ahead of global peers like Beijing and Shanghai. For a founder moving from a regional hub, Bengaluru offers an immediate upgrade in "growth velocity." Startups based in the city reach unicorn status in an average of six years—significantly faster than the national average—supported by a pipeline of 183 "soonicorns" valued at over $100 million.

Financial Capital and Concentration of Liquidity

Bengaluru’s dominance in capital deployment is staggering. Since 2010, the city’s startups have raised $79 billion, with $70.5 billion deployed in the last decade alone. This accounts for nearly double the capital raised in the next largest Indian hub. In 2025, even as venture capital activity remained disciplined, Karnataka-based tech companies raised $3.8 billion. This concentration of liquidity is not merely a metric of volume but a reflection of the ecosystem’s maturity, depth, and resilience.

Investors in 2025 showed a clear preference for companies with proven business models and scalable technology. For founders in Series A or B stages, being in Bengaluru provides proximity to India’s strongest investor base, ranging from early-stage angel networks to late-stage private equity. This proximity facilitates faster deal closure and provides a buffer against the funding volatility experienced in smaller regional clusters.

Human Capital Density and Specialized Talent

The city’s human capital is arguably its most potent pull factor. Bengaluru anchors the largest tech workforce of any city globally, with 2.5 million technology professionals. For Tier-2 founders building sophisticated products in Deep Tech, AI, or Semiconductors, the talent pool in their home cities is often insufficient for rapid scaling. Bengaluru provides access to:

Specialized Expertise: Over 350,000 professionals specialized in chip design and embedded systems.

AI Leadership: The city ranks #5 globally among AI cities, with eighty-two percent of Indian AI startups building at the application layer to solve real-world complexities.

Academic Backbone: Premier institutions like the Indian Institute of Science (IISc) provide the deep-tech R&D backbone necessary for fundamental intellectual property (IP) creation.

Cost-Efficiency and Talent Arbitrage

While Tier-2 cities offer lower initial costs, Bengaluru provides a unique "talent-cost arbitrage." The city offers high-quality talent paired with global-grade cost-efficiency, allowing startups to scale without the friction of a fragmented workforce. The density of talent ensures that high-potential ventures can scale rapidly, reaching milestones that might take years longer in a talent-scarce regional market.

The Growth Chasm: Why Tier-2 Startups Struggle to Scale Locally

Despite the rise of regional entrepreneurship, the "push" factors driving founders away from Tier-2 cities are rooted in structural deficiencies at the growth stage. While government initiatives have made early-stage funding and grants adequately available, growth-stage funding remains a significant hurdle for non-metro startups.

The Funding Gap and Asset Hurdles

Startups in smaller centers often find it more difficult to access private sector capital once they move past the seed stage. Many of these ventures are profitable but lack the massive scale required to attract venture capital firms that prefer high-growth trajectories. A critical barrier is the lack of tangible assets. Traditional financial institutions and banks in Tier-2 regions are often hesitant to fund startups that lack collateral such as land or machinery. Even under government credit guarantee schemes like CGTMSE, debt funding is scarce for startups whose primary value lies in intangible assets like software or IP.

Mentorship and Network Deficits

Proximity to networks and mentorship is a luxury that Tier-2 founders often lack. In Tier-1 hubs, a robust community of former entrepreneurs and seasoned professionals actively nurtures new ventures. Startups in regional centers are largely deprived of this "hand-holding," leading to a higher mortality rate within the first two to three years of operation. The lack of local investor networks and smaller mentor pools often forces founders to relocate to Bengaluru to secure the guidance and pilots necessary for national expansion.

Infrastructure and Regulatory Complexities

While cities like Jaipur and Indore have seen infrastructure upgrades, they still lag behind Bengaluru in specialized facilities. Regional hubs often lack robust facilities for prototyping, product testing, field validation, and certification. Furthermore, bureaucratic red tape and regulatory complexities disproportionately affect startups in smaller cities, where local administrative bodies may be less familiar with the specific needs of tech-driven ventures.

Comparison of Operational Barriers: Tier-2 vs. Bengaluru (2025)

Factor | Tier-2/3 Regional Hubs | Bengaluru (Tier-1) |

Early-Stage Funding | Readily available via state grants | High competition for angel/seed |

Growth-Stage Funding | Significant Chasm (Series B+) | Concentrated Liquidity / Many VCs |

Debt Funding | Limited (Collateral-dependent) | Emerging options for tech/IP |

Mentorship | Limited / Fragmented | Deep ecosystem / Institutionalized |

Market Access | Localized / Regional | Global corridors / Corporate HQs |

Infrastructure | Basic (Digital/Connectivity) | Specialized (R&D/Testing/Lab) |

Data source: Synthesis of startup ecosystem challenges and regional disadvantage reports.

The Cultural Shift: Shark Tank India and Perception Normalization

The visibility of Tier-2 founders has been significantly amplified by national media platforms, most notably Shark Tank India. The show has acted as a "credibility amplifier," normalizing the idea that scalable, world-class businesses can originate from anywhere in India. In 2023, non-metro and Tier-2/3 startups accounted for twenty-four percent of all early-stage deals, up from twenty percent in 2022.

While the show has not replaced traditional funding routes, it has "widened the door" by providing founders from states like Rajasthan, Uttarakhand, and Odisha with national exposure. This visibility often leads to inbound interest from angel investors and distributors, even for startups that do not secure a deal on air. However, the ultimate "graduation" of these companies often requires a move to Bengaluru to tap into the high-velocity talent and capital networks that the show highlights but cannot sustain locally.

Regional Hub Archetypes: Strengths and Limitations

Several Tier-2 cities have emerged as specialized innovation clusters, each with unique regional strengths. However, these hubs often reach a "saturation point" where relocation to a metro becomes a strategic necessity for the next phase of growth.

Jaipur: The North Indian Startup Magnet

Jaipur stands out as a primary startup hotspot, housing more than half of Rajasthan’s new-age ventures. Anchored by the Bhamashah Technohub and the iStart program, the city has produced notable successes like CarDekho and Finova Capital. The iStart program provides matching funds up to ₹25 lakhs and sustenance allowances, making it an excellent nursery for seed-stage companies. However, for ventures targeting the global market or requiring specialized deep-tech R&D, the migration to Bengaluru remains a common trajectory.

Coimbatore: The Engineering and GCC Hub

Known as the "Manchester of South India," Coimbatore has transitioned from a manufacturing base to a fast-emerging IT hub. It recorded a twenty-one percent CAGR in new Global Capability Center (GCC) setups over the last five years. Supported by IT parks like TIDEL Park, the city offers thirty to forty percent lower operational and real estate costs compared to Bengaluru. Despite these advantages, Coimbatore often serves as a cost-effective operational center for startups that maintain their strategic and investor relations offices in Bengaluru.

Lucknow: The Policy-Driven Center

Lucknow has become a significant hub in North India, hosting 1,700-1,800 active startups. The state’s "StartInUP" policy offers seed funding, marketing support, and prototype funding. While companies like Arficus and Webllisto Technologies thrive here, the lack of a deep pool of local Series B investors often necessitates a "Bengaluru bridge" for expansion.

Specialized Tier-2 Clusters and Government Support (2025-26)

City | Key Sectors | Major Policy/Initiative | Support Mechanism |

Jaipur | FinTech, Auto-tech, D2C | iStart Program | matching funds up to ₹25 lakhs |

Lucknow | AI, EdTech, IT Services | StartInUP Policy | Sustenance allowance, seed fund |

Indore | AgriTech, STEM, SaaS | Super Corridor Parks | MP Startup Policy, MSME grants |

Kochi | AI, GCC, DeepTech | Kerala Startup Mission | Seed funds (₹10L), 18-mo cohorts |

Chandigarh | SaaS, Consumer Tech | Startup Policy 2025 | Seed grants (₹7L), patent reimb. |

Bhubaneswar | IT, FinTech, Manufacturing | Odisha Startup Policy | Infovalley SEZ, tax incentives |

Data source: Regional ecosystem highlights and government scheme analysis.

Case Studies of Relocation: Rationalizing the Move

The migration of founders to Bengaluru is often driven by sector-specific needs that regional hubs cannot fulfill. Analysis of successful relocations reveals consistent themes: the need for engineers, regulatory alignment, and market access.

Ola: The Mumbai to Bengaluru Migration

Ola is a quintessential example of a startup that relocated to recognize ecosystem advantages. While founded in Mumbai, the founders realized that they needed a massive volume of engineers to build their ride-sharing platform quickly. Bengaluru, with its unmatched density of software talent, provided the necessary human capital to scale further and enter international markets. The move allowed Ola to secure $3.8 billion in funding and become a category-defining unicorn.

Fragaria: The Chennai to Bengaluru Shift

The 2025 relocation of Chennai-based agritech startup Fragaria highlights the role of "liberal policies" and climate. Founder Harish Varadharajan cited supportive agriculture laws and "expat livability" as reasons for making the move "inevitable". Despite Chennai’s strong talent and infrastructure, Bengaluru’s thriving ecosystem and market access were seen as critical for building a truly global product.

Zoomcar: The International Move to Bengaluru

The centripetal force of Bengaluru also attracts international founders. David Back and Greg Moran relocated from the US to Bengaluru in 2012 to launch Zoomcar, India’s first car rental company. They recognized that Bengaluru provided the right mix of early-stage investors, such as Mohandas Pai, and technical advisors necessary to pilot a new business model in the Indian market.

The Evolution of the Bengaluru Ecosystem: Deep Tech and AI

As Tier-2 founders arrive in Bengaluru, they find an ecosystem that is itself undergoing a structural evolution. The city has moved from being a "software-only" hub to a hybrid engineering powerhouse, with over forty percent of India’s biotechnology companies and a dominant share in SpaceTech and Semiconductors.

The AI Application Layer

Bengaluru is aggressively capturing the "Application Layer" of AI. While global giants compete on foundational models, Bengaluru’s 2.5 million tech professionals are translating cutting-edge AI into products that solve real-world complexity in SaaS and agentic workflows. Companies like Sarvam AI and Krutrim attract fifty-eight percent of all national AI startup funding, creating a massive gravitational pull for AI-first founders from regional hubs.

Deep Tech and the Return to Hardware

The success of companies like Pixxel in space imagery and Ather in EV mobility demonstrates how Bengaluru supports capital-intensive, R&D-heavy business models. This is a structural evolution driven by talent and specialized capital. With over 350,000 professionals in chip design, the city is moving up the value chain from design support to IP creation, a transition that requires the "patient capital" and deep engineering expertise found primarily in the Karnataka capital.

VC Criteria for Deep Tech and AI Startups (2025-26)

Criteria | VC Focus Area | Importance |

Technical Depth | IP defensibility, proprietary models | Most Critical |

Commercial Viability | Clear GTM, enterprise adoption | High |

Team Quality | Research rigor, founder-market fit | High |

Data Advantage | Proprietary datasets, model performance | Medium-High |

Capital Efficiency | Smart compute usage, unit economics | Critical in 2025 |

Regulatory Fit | Compliance in healthcare, drones, etc. | High (Sector-specific) |

Data source: Investor sentiment and VC checklist for frontier tech.

Policy Counter-Movements: The "Beyond Bengaluru" Mission

Recognizing the strain of over-concentration, the Karnataka government has launched the "Beyond Bengaluru" (BB) mission. This initiative aims to distribute the digital economy by seeding innovation clusters in emerging hubs like Mysuru (Cybersecurity & ESDM), Mangaluru (FinTech), and Hubballi-Dharwad (AgriTech & Manufacturing).

Strategic Decentralization and Incentives

The BB mission allows startups to scale with lower overheads while retaining access to Bengaluru’s global corridors. Key components include:

Grants for Infrastructure: The government recently released one of its largest grants (₹1.92 crore) to a workspace operator in Mangaluru to boost the local tech cluster.

Centers of Excellence: Sixteen specialized CoEs spanning AI, Cybersecurity, and Aerospace act as bridges between research and commercial application, supporting over 1,000 startups.

Cost Savings: Initiatives like "Mysuru Blue" attract talent by offering ten to thirty-five percent lower operational costs than the capital.

This mission represents a strategic shift toward a hub-and-spoke model, where Tier-2 cities provide the cost-efficient operational base, and Bengaluru serves as the high-velocity finishing school for the global market.

Future Outlook: Toward Viksit Bharat 2047

The migration of Tier-2 founders to Bengaluru is a transitionary phase in the maturation of the Indian ecosystem. As India advances toward its Viksit Bharat 2047 ambition, the startups that will matter most are those that solve root-level systemic problems at population scale. These ventures are increasingly originating from the heart of India—Tier-2 and Tier-3 cities—where founders live amidst the challenges they solve, from agri-tech to telemedicine.

The next decade will likely see the stabilization of a geographically diversified phase. Capital is already beginning to reach innovation clusters rooted in regional strengths, and digital infrastructure has minimized geographic constraints for remote operations. However, until regional hubs can bridge the "Growth Chasm" of late-stage capital and specialized deep-tech R&D, Bengaluru will continue to exert a powerful centripetal force on India’s most ambitious entrepreneurs.

Conclusion: The Finish Line in the Silicon Valley of India

In the 2024-2026 timeframe, the rise of Tier-2 founders moving to Bengaluru is less a departure from their roots and more an embrace of the necessary "muscle" to compete globally. Bengaluru’s status as the 14th best startup ecosystem in the world and the 5th global unicorn hub is a reflection of sustained resilience and scalability. While regional hubs like Jaipur and Coimbatore provide the "momentum" through lower costs and local insights, Bengaluru provides the "engine" through concentrated liquidity and human capital density. For the modern Indian founder, the journey may begin in the heartland of Bharat, but for those seeking hyper-scale, the finish line—and the next funding round—inevitably passes through the Silicon Valley of India.

Read More -

1. From Idea to MVP: A Step-by-Step Guide for Solo Founder

🔗 https://findnstart.com/blogs/from-idea-to-mvp-a-step-by-step-guide-for-solo-founder

2. How to Validate Your Startup Idea in 48 Hours for $0

🔗 https://findnstart.com/blogs/how-to-validate-your-startup-idea-in-48-hours-for-0

3. Remote vs. Local: Does Your Co-Founder Need to Live in the Same City?

🔗 https://findnstart.com/blogs/remote-vs-local-does-your-co-founder-need-to-live-in-the-same-city

4. The 2026 Startup Landscape: What Has Fundamentally Changed (and Why Founder Skills Matter More Than Ever)

5. The Most In-Demand Skills for Startup Founders in 2026

🔗 https://findnstart.com/blogs/the-most-in-demand-skills-for-startup-founders-in-2026

6. How to Find a Technical Co-Founder (Without a Six-Figure Salary)

🔗 https://findnstart.com/blogs/how-to-find-a-technical-co-founder-without-a-six-figure-salary

7. 5 Red Flags to Look for When Choosing a Startup Partner

🔗 https://findnstart.com/blogs/5-red-flags-to-look-for-when-choosing-a-startup-partner

8. How to Pitch Your Idea to Potential Co-Founders

🔗 https://findnstart.com/blogs/how-to-pitch-your-idea-to-potential-co-founders

9. How to Build a Portfolio that Attracts High-Growth Startup Founders

🔗 https://findnstart.com/blogs/how-to-build-a-portfolio-that-attracts-high-growth-startup-founders

10. Equity vs. Salary: How to Split Ownership with Your First Teammate

🔗 https://findnstart.com/blogs/equity-vs-salary-how-to-split-ownership-with-your-first-teammate

11. Why Joining an Early-Stage Startup is Better Than a Corporate Job

🔗 https://findnstart.com/blogs/why-joining-an-early-stage-startup-is-better-than-a-corporate-job

12. The Future of EdTech: Why Developers and Educators Need to Team Up Now

🔗 https://findnstart.com/blogs/the-future-of-edtech-why-developers-and-educators-need-to-team-up-now

13. The Architecture of Symbiosis: Analytical Perspectives on the Five Habits of Successful Startup Duos

14. Finding a Co-Founder in the AI Space: What Skills Should You Look For?

🔗 https://findnstart.com/blogs/finding-a-co-founder-in-the-ai-space-what-skills-should-you-look-for

15. Overcoming Analysis Paralysis and the Strategic Path to Execution

🔗 https://findnstart.com/blogs/overcoming-analysis-paralysis-and-the-strategic-path-to-execution

16. From College Project to Company: How to Find Your Student Co-Founder

🔗 https://findnstart.com/blogs/from-college-project-to-company-how-to-find-your-student-co-founder

17. How to Start a Startup While Working a Full-Time Job

🔗 https://findnstart.com/blogs/how-to-start-a-startup-while-working-a-full-time-job

18. How to Build a HealthTech Startup Without a Medical Degree

🔗 https://findnstart.com/blogs/how-to-build-a-healthtech-startup-without-a-medical-degree

19. The Solitary Architect: Executive Isolation in Entrepreneurship

20. The 2026 Guide to Launching a SaaS as a Solo Developer

21. What Sustainable Growth Actually Looks Like

🔗 https://findnstart.com/blogs/what-sustainable-growth-actually-looks-like

22. The Early Warning Signs Your Startup Is in Trouble

🔗 https://findnstart.com/blogs/the-early-warning-signs-your-startup-is-in-trouble

23. How to Grow Without Burning Out

🔗 https://findnstart.com/blogs/how-to-grow-without-burning-out

24. The Truth About “Runway” Most Founders Ignore

🔗 https://findnstart.com/blogs/the-truth-about-runway-most-founders-ignore

25. Revenue Solves More Problems Than Funding

🔗 https://findnstart.com/blogs/revenue-solves-more-problems-than-funding

26. What No One Tells You About Being a Solo Founder

🔗 https://findnstart.com/blogs/what-no-one-tells-you-about-being-a-solo-founder

27. Why Smart People Quit High-Paying Jobs to Build Startups (And Why Most Regret It)

28. Why Most Startup Advice on Twitter Is Dangerous

🔗 https://findnstart.com/blogs/why-most-startup-advice-on-twitter-is-dangerous

29. Decision Fatigue: The Silent Startup Killer

🔗 https://findnstart.com/blogs/decision-fatigue-the-silent-startup-killer

30. Fear vs Logic: How Founders Actually Make Decisions

🔗 https://findnstart.com/blogs/fear-vs-logic-how-founders-actually-make-decisions

31. How Overthinking Destroys Early Momentum

🔗 https://findnstart.com/blogs/how-overthinking-destroys-early-momentum

32. Ideas Don’t Scale. Systems Do.

🔗 https://findnstart.com/blogs/ideas-dont-scale-systems-do

33. The First Hire That Actually Matters

🔗 https://findnstart.com/blogs/the-first-hire-that-actually-matters

34. How the First 100 Users Decide Your Startup’s Fate

🔗 https://findnstart.com/blogs/how-the-first-100-users-decide-your-startups-fate

35. Why Your Startup Doesn’t Need Growth — It Needs Focus

🔗 https://findnstart.com/blogs/why-your-startup-doesnt-need-growthit-needs-focus

36. Why Most Startups Die Quietly

🔗 https://findnstart.com/blogs/why-most-startups-die-quietly

37. Lessons Learned Too Late by First-Time Founders

🔗 https://findnstart.com/blogs/lessons-learned-too-late-by-first-time-founders

38. The Myth of the “Overnight Success” Startup

🔗 https://findnstart.com/blogs/the-myth-of-the-overnight-success-startup