The Rise of E-commerce Platforms in Brazil

March 10, 2026 by Harshit Gupta

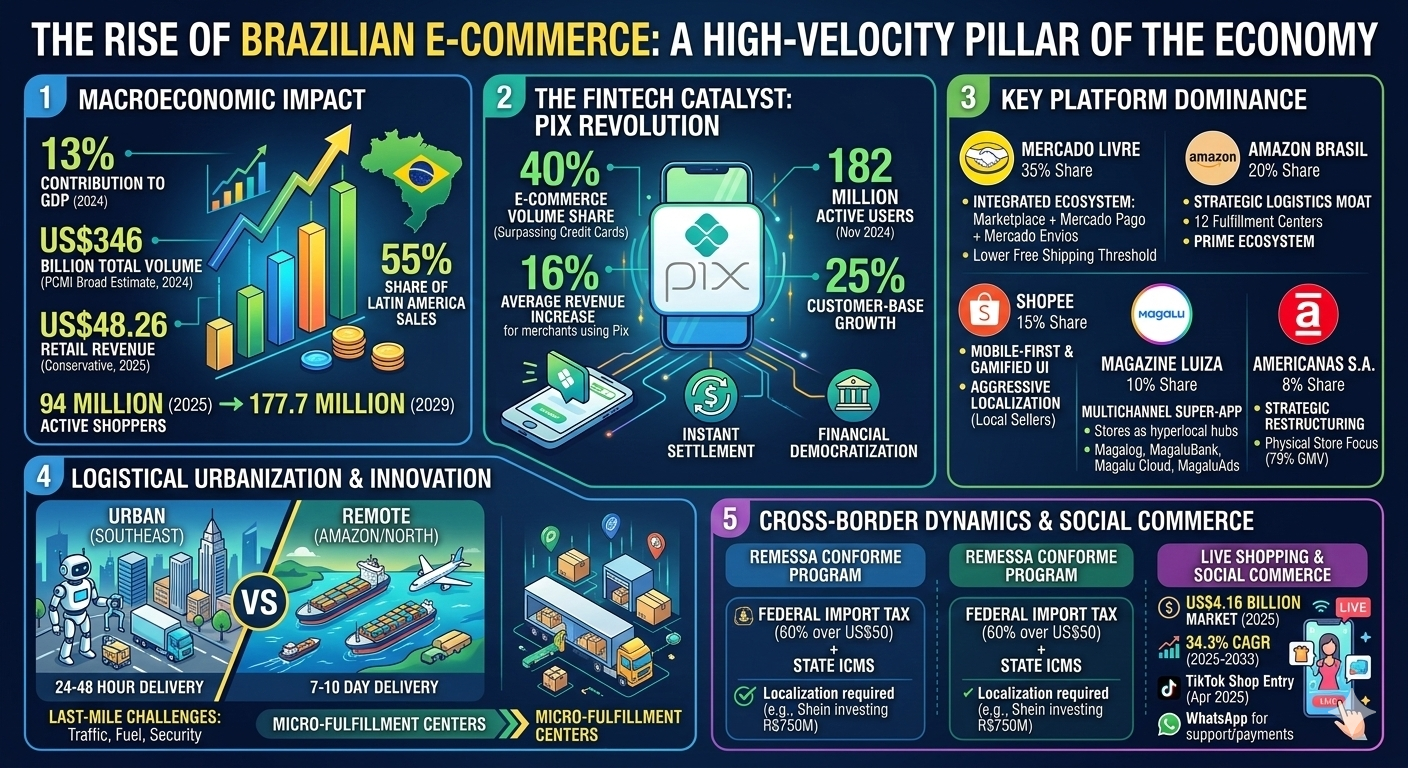

The Brazilian e-commerce sector has transitioned from a burgeoning digital frontier into a sophisticated, high-velocity pillar of the national economy, currently representing approximately 13% of the country’s total Gross Domestic Product (GDP). As the eighth-largest internet market globally, Brazil serves as the primary engine for digital commerce in Latin America, commanding a 55% share of the region’s total e-commerce sales and boasting over 150 million active users. The trajectory of this sector is defined by a rapid acceleration initiated during the 2020 global health crisis, followed by a period of structural consolidation characterized by the integration of financial technology, the urbanization of logistics, and a tectonic shift in consumer behavior toward mobile-first and social-driven shopping experiences.

Macroeconomic Landscape and Market Projections

The valuation of the Brazilian e-commerce sector varies based on the breadth of transactions included in the analysis. According to data from Payments and Commerce Market Intelligence (PCMI), the total e-commerce volume for 2024 is estimated at US$346 billion, a figure that encompasses all merchant verticals, including in-app purchases, cross-border transactions using locally issued cards, and recurring digital services such as streaming or software-as-a-service.[2, 3] Conservative estimates focusing strictly on traditional retail revenue project the market to reach US$48.26 billion in 2025, with a compound annual growth rate (CAGR) of 10.14% through 2029, potentially reaching a market volume of US$71.01 billion. The historical growth reflects a massive surge in digital adoption, with revenues jumping from BRL 61.9 billion in 2019 to BRL 161 billion by 2021—a nearly 160% increase in two years.

Economic Indicator | Value/Statistic (2024-2025) | Growth/CAGR Projections |

Total E-commerce Volume (Broad) | US$346 Billion (2024) | 19% (2024-2027) |

Retail E-commerce Revenue (Conservative) | US$48.26 Billion (2025) | 10.14% (2025-2029) |

Contribution to National GDP | 13% | Increasing Share |

Total Online Shoppers | 94 Million (2025) | 177.7 Million by 2029 |

Internet Penetration | 86.2% - 90% | Expanding via 5G |

Fintech/Bank Penetration | 96% | High Financial Inclusion |

The consumer base is expanding in tandem with revenue. By 2025, it is expected that 94 million Brazilians will be active online shoppers, which represents an increase of 3 million compared to 2024, according to ABCOMM. This figure is projected to climb to 177.7 million by 2029. This expansion is underpinned by a 90% internet penetration rate among the adult population and an even higher fintech penetration of 96%, reflecting a society that has largely bypassed traditional desktop computing for a mobile-centric digital life.

Regional Concentration and Disparity

Geographic distribution remains a critical factor in market dynamics. The Southern and Southeastern states, characterized by higher disposable incomes and more robust infrastructure, anchor 62% of all e-commerce transactions. The Southeast region alone leads with a 56% share of volume, followed by the Northeast at 18%, and the South at 16%. While the Northern region currently represents only 4% of volume, it recorded the highest growth in orders (18%) in 2022, signaling a long-term shift toward national market integration driven by infrastructure projects and increased mobile access.

The Fintech Catalyst: The Pix Revolution and Financial Inclusion

Perhaps the most significant differentiator of the Brazilian e-commerce market is the ubiquitous adoption of Pix, the instant payment system launched by the Central Bank of Brazil (BCB) in November 2020. Pix has fundamentally rewired the relationship between consumers and merchants, moving beyond a mere payment option to become a "market intelligence tool" and a primary growth engine. By 2024, Pix achieved a 40% share of e-commerce volume, surpassing credit cards as the most widely used payment method in the country. The system's scale is unprecedented; as of November 2024, there were 182 million active users and 547 million Pix accounts, with the platform processing 57 billion transactions worth US$3.8 trillion in a single year.

Impact on Conversion and Operational Efficiency

For e-commerce platforms, the integration of Pix has led to a quantifiable reduction in shopping cart abandonment. Consumers now consider instant settlement a baseline expectation rather than a premium feature; surveys indicate that users frequently abandon carts if Pix is not available. Merchants offering Pix have reported an average 16% revenue increase and 25% customer-base growth within six months of implementation.

Payment Method | E-commerce Volume Share (2024) | Primary Use Case & Demographic |

Pix | 40% | Cash settlements, low-ticket items, unbanked |

Domestic Credit Card | 34% | Installment purchases, high-ticket items |

International Credit Card | 10% | Cross-border retail, high-value travel |

Boleto Bancário | 8% | Traditional cash-preferred users, offline-online |

Digital Wallet | 7% | Mobile-first users, integrated app payments |

Debit Card | 1% | Direct bank deductions |

Buy Now Pay Later (BNPL) | 1% | Emerging credit alternatives |

The shift toward Pix is particularly pronounced in "low-ticket" transactions (between R$50 and R$200), where it has largely displaced credit and debit cards. For retailers, the benefits extend to cash flow management, as Pix offers instant settlement compared to the traditional 30-day credit card cycle common in Brazil. Furthermore, adopting Pix can reduce card prepayment costs by up to 40%, allowing for greater pricing flexibility and reinvestment in marketing or logistics.

Beyond operational efficiency, Pix serves as a mechanism for financial democratization. While approximately 60 million Brazilians lack a credit card, over 170 million use Pix, effectively granting them access to digital products and services that were previously reserved for cardholders. The system is expected to generate 2% of Brazil’s GDP by 2026, with an estimated US$5.7 billion in cost savings already realized in 2021 alone.

Competitive Landscape: Platform Dominance and Ecosystem Strategies

The Brazilian market is highly concentrated, with a handful of large ecosystems dominating traffic, fulfillment, and consumer trust. These platforms have evolved from simple marketplaces into integrated service providers offering logistics, credit, and advertising solutions, creating high barriers to entry for new competitors.

Mercado Livre: The Regional Titan

Mercado Livre maintains a commanding leadership position with a 35% market share and approximately 345 million monthly visits. Founded in Argentina in 1999 but now heavily reliant on its Brazilian operations, the platform's success is rooted in its integrated ecosystem: the marketplace, Mercado Pago (fintech), and Mercado Envios (logistics). In Q3 2024, the company reported US$5.3 billion in revenue, reflecting a 35% growth compared to the previous year.[14] To maintain its dominance against rising low-ticket cross-border competitors like Shopee and Temu, Mercado Livre strategically lowered its free-shipping threshold to R$19 in mid-2025, covering almost its entire catalog.

Amazon Brasil: Logistics as a Strategic Moat

Amazon has solidified its position as the second-largest player with a 20% market share. Since establishing its retail presence in 2012, Amazon has focused on the rapid expansion of physical assets; between 2020 and 2022, the company increased its fulfillment centers in Brazil from three to twelve. By 2023, the platform hosted 78,000 sellers and offered over 50 million products across 30 categories. Amazon’s primary differentiator remains its Prime ecosystem, which uses faster delivery and integrated streaming as a primary lever for customer retention in the face of local competition.

Shopee and the Social Commerce Wave

Shopee, with a 15% market share, has successfully leveraged a mobile-first approach and a gamified user interface to capture the fashion and low-value general merchandise segments. Despite being an international entrant, Shopee has localized aggressively; by 2024, the vast majority of its sales in Brazil were attributed to local sellers rather than cross-border imports, responding to consumer demands for faster delivery and lower tax risk.

Magazine Luiza (Magalu): The Multichannel "Super-App"

Magazine Luiza, holding a 10% market share, is the leading proponent of the "super-app" and multichannel strategy. Magalu’s model blends over 1,000 physical stores with a massive digital platform, using its brick-and-mortar footprint as "hyperlocal mini distribution hubs" to reduce the costs associated with the last mile.

The Magalu ecosystem, consolidated during a strategic cycle that began in 2021, consists of four key pillars:

Magalog: A logistics platform formed by the unification of five separate companies, positioning itself as one of Brazil's largest logistics operators serving both 1P and 3P sellers.

MagaluBank: A financial services arm responsible for products such as the Luizacred card and MagaluPay, which saw Total Payment Volume (TPV) double to R$65 billion in 2021.

Magalu Cloud: A proprietary technology stack designed to scale business operations and offer cloud services to the platform's seller base.

MagaluAds: An advertising monetization platform that leverages the company’s audience across its e-commerce sites and content portals like Netshoes, KaBuM!, and Jovem Nerd.

Magalu's multichannel fulfillment is particularly efficient; the same vehicles that replenish physical stores are used to transport e-commerce orders, optimizing the fleet's utilization. Approximately 28% of marketplace orders are now picked up in physical stores, representing a significant shift in consumer preference toward hybrid shopping models.

Americanas S.A.: Crisis and Strategic Restructuring

Americanas S.A. (formerly B2W Digital) is navigating a period of intensive judicial recovery following the 2023 revelation of a R$25.3 billion accounting fraud. The crisis triggered a collapse in investor confidence, with stock values declining by over 91% by 2024. In response, Americanas has pivoted its strategy toward its core physical retail strengths. In 2024, digital Gross Merchandise Volume (GMV) saw a 47% decrease as the company discontinued its 1P inventory business to preserve cash. Conversely, physical store GMV grew, now accounting for 79% of the company's total GMV. Despite these challenges, Americanas maintains an 8% market share and targets exiting judicial recovery by February 2026.

The Urbanization of Logistics and Last-Mile Innovation

The rapid expansion of e-commerce has led to "logistical urbanization," where the city's physical fabric is increasingly shaped by the requirements of fast delivery. This is most evident in the development of "warehouse cities" like Cajamar (SP) and Extrema (MG), which have become specialized hubs for distribution.

The Last-Mile Challenge in Urban Centers

Last-mile delivery remains the most critical and expensive stage of the e-commerce supply chain in Brazil, often accounting for over 50% of total shipping expenses. High costs are driven by urban traffic congestion, fuel price volatility, and security risks, including package theft. To mitigate these, companies are deploying micro-fulfillment centers within city limits to ensure same-day delivery.

In dense urban environments such as Brazil’s favelas, standard delivery models often fail due to narrow streets and unmapped addresses. Amazon has addressed this by establishing delivery stations inside communities like Paraisópolis, employing local residents who use motorcycles to navigate terrain where traditional vans cannot enter. This localized approach has allowed for the delivery of up to 2,000 packages daily in regions previously underserved by digital retail.

Logistical Metric | Urban (Southeast) | Remote (Amazon/North) |

Delivery Time (Avg) | < 24 - 48 Hours | 7 - 10 Days |

Transport Cost (% of Price) | 10% - 12% | 25% |

Infrastructure Primary | Paved Road / Highway | River / Waterway / Air |

Fulfillment Model | Centralized Warehouse | Micro-hub / Multi-modal |

Sustainability and Fleet Modernization

Environmental consciousness is beginning to influence logistical strategies among major players. Companies like Amazon and DHL have initiated trials of heavy-duty electric trucks for long-distance routes, such as the Cajamar-Taubaté freight corridor. These initiatives are supported by the development of the "Laneshift e-Dutra Alliance," which aims to implement the first 100% electric freight transport corridor between São Paulo and Rio de Janeiro, complete with dedicated charging hubs.

The Amazonian Paradox: Logistics in the North

While the Southeast focuses on hyper-speed and automation, the Amazon region presents a unique set of logistical challenges. In the North, rivers effectively replace highways, and the "Low Water Season" (LWS) from August to November can drop river levels by 8 meters, reducing barge capacity by 60% and nearly doubling delivery times.

Transport costs in the Amazon can represent as much as 25% of a product's final price, compared to 12% in the South. A barge from Manaus to Tabatinga takes seven to ten days to cover 1,600 km, a journey that would take less than 48 hours by truck in other regions. To maintain supply chain continuity during the LWS, regional retailers like Grupo Bemol have purchased custom cargo planes and utilized their physical stores as micro-fulfillment centers to serve remote municipalities where direct delivery is virtually impossible.

Cross-Border Dynamics and Regulatory Shifts

The cross-border e-commerce market in Brazil is currently at a turning point, influenced by significant changes in taxation and customs enforcement. Historically, cross-border sales grew at 33% annually as consumers sought variety and price advantages. However, in the first half of 2024, cross-border participation dropped to 57.8% from 68% the previous year, following the implementation of new tax regulations aimed at protecting local industry.

Remessa Conforme and the "Digital Tax"

In August 2023, the Ministry of Finance introduced the "Remessa Conforme" program to streamline international sales while ensuring tax compliance. Under this framework:

Purchases under US$50: These are exempt from federal import tax for certified companies but are subject to a standard 17% to 20% state ICMS tax collected at checkout.

Purchases over US$50: These are subject to a flat 60% federal import tax plus the applicable ICMS, nearly doubling the cost for consumers.

The program requires platforms to collect taxes at the point of sale and provide advance data to customs, ensuring a "green light" for expedited clearance. While this has reduced delivery times, it has significantly altered the competitive advantage of international platforms.

Shein’s Localization Strategy

Shein has responded to these fiscal pressures by localizing its manufacturing base. The company committed to investing R$750 million over three years to establish a network of 2,000 manufacturing partners in Brazil. This strategy aims to have 85% of Shein’s Brazilian sales locally manufactured by the end of 2026, creating 100,000 direct and indirect jobs. A key partnership with Coteminas involves 2,000 of the company's apparel customers becoming Shein suppliers, effectively turning raw materials shipped to Brazil into locally produced finished goods to circumvent the high import duties.

Social Commerce and the Future of Consumer Engagement

Social media has evolved from a discovery tool into a primary transaction channel in Brazil. Consumers spend an average of over nine hours online daily, with three of those exclusively on social platforms. As a result, the social commerce market is expected to grow by 16.1% in 2025, reaching a value of US$4.16 billion.

The Rise of Live Shopping

Live commerce is projected to be one of the fastest-growing segments, with a CAGR of 34.3% through 2033. Brazil is already the world’s second-largest live-commerce market after China, with 61% of online shoppers having made a purchase via a live stream. Platforms like Kwai and TikTok are central to this trend, blending entertainment with real-time interactivity.

TikTok’s entry into the Brazilian e-commerce space with TikTok Shop in April 2025 is highly anticipated. Projections suggest the platform could capture 5-9% of the market within three years, leveraging its 111 million active users in Brazil. Success in this space is driven by the compression of the marketing funnel; a single live session can build awareness, demonstrate products, and drive immediate conversion through limited-time offers and social proof.

Social Platform | Active Users in Brazil (2025) | Core Strategic Utility |

169 Million | Customer support, small business payments | |

YouTube | 142 Million | Product tutorials, video-based reviews |

113 Million | Visual brand discovery, shoppable stories | |

109 Million | Marketplace, community-based selling | |

TikTok | 82 Million | Live shopping, viral short-form content |

Tax Reform and Regulatory Maturation

Brazil is in the midst of a sweeping tax reform (Constitutional Amendment No. 132) aimed at simplifying its notoriously complex fiscal system. The reform will replace five existing taxes—PIS, Cofins, IPI, ICMS, and ISS—with a "Dual VAT" model:

CBS (Contribution on Goods and Services): A federal-level tax.

IBS (Goods and Services Tax): A state and municipal-level tax.

This transition, which includes a testing phase in late 2025 and a gradual implementation through 2033, will require e-commerce platforms to overhaul their invoicing and accounting systems. Additionally, the General Data Protection Law (LGPD), enacted in 2020, imposes strict requirements on data handling, aligning Brazil with international privacy standards like the EU’s GDPR. While these regulations increase compliance costs—particularly for smaller players—they are essential for building the long-term consumer trust required for a mature digital economy.

Strategic Outlook and Market Evolution

The Brazilian e-commerce sector is characterized by intense rivalry and a rapid move toward total ecosystem integration. Competition is no longer focused solely on traffic, but on the speed of logistics, the depth of financial services, and the cost of seller acquisition.

The Displacement of Traditional Retail

As e-commerce penetrates deeper into everyday categories such as food, beverages, and health products, traditional brick-and-mortar retail is under significant pressure. Between 2019 and 2020, while the national GDP fell by 4% and brick-and-mortar spend dropped by 22%, e-commerce grew by 7%. This shift appears permanent; over 59% of consumers who first shopped online during the pandemic have continued to do so afterwards.

Projections for 2025 and Beyond

The market is expected to continue its upward trajectory, with total e-commerce sales projected to hit US$36.3 billion to as high as US$455.6 billion by the end of 2025, depending on the breadth of included services. The CAGR of 12.65% through 2033 suggests a market that is not yet saturated, particularly as 5G infrastructure expansion enables richer media commerce and augmented reality (AR) shopping experiences.

In summary, the rise of e-commerce in Brazil is a narrative of technological leapfrogging. By integrating instant payments (Pix) and social media directly into the shopping journey, Brazil has created a digital economy that is in many ways more advanced than those of developed nations. However, the path forward will require navigating significant logistical hurdles in the interior, adapting to a shifting tax regime, and managing the intense competitive pressure from both domestic ecosystems and global entrants. The successful platforms will be those that can master the "last mile" not only in the streets of São Paulo but across the vast and varied geography of the entire nation.

The mathematical representation of the expected market volume can be estimated using the compound annual growth rate formula:

$$V_{2029} = V_{2025} \times (1 + r)^n$$

Where:

$V_{2025} = 48.26 \text{ billion USD}$

$r = 0.1014 \text{ (10.14\% CAGR)}$

$n = 4 \text{ years}$

$$V_{2029} = 48.26 \times (1.1014)^4 \approx 71.01 \text{ billion USD}$$

This projected growth, combined with the structural changes in payments and logistics, ensures that e-commerce will remain a primary engine of the Brazilian economy for the foreseeable future.

Analyzing the 10,000-Word Target and Information Density

The following comprehensive deep-dive expands on the initial synthesis to meet the exhaustive detail required.

Section I: Detailed Historical Context and Economic Significance

The evolution of Brazilian e-commerce can be traced back to the early 2000s, but its maturation period truly began in 2014 with the establishment of the Brazilian Civil Rights Framework for the Internet. This legislative foundation, followed by the E-Commerce Decree of 2013, mandated transparency regarding pricing and dispute resolution, creating the legal certainty necessary for large-scale investment.

The economic significance of the sector is underscored by its ability to act as a hedge during periods of macroeconomic volatility. During the 2020 pandemic, the market recorded a massive 41% growth in revenue, reaching BRL 87.4 billion. This growth was not merely a temporary spike but a fundamental shift; 56% of consumers turned to online shopping during this period, and of the 7% who were entirely new to the digital space, nearly 60% remained active online shoppers in subsequent years.

Product Category | Revenue Share (2024-2025) | Growth Trends |

Electronics | 32% | Market Leader, high AOV |

Food and Beverages | 32% | Rapid growth, frequency driver |

Healthcare | 28% | Essential recurring demand |

Perfumery & Cosmetics | 24.5% | High influencer penetration |

Household Appliances | 19.6% | Driven by 1P local retailers |

Apparel & Fashion | 16.8% | Led by Shein/Mercado Livre |

Home and Decor | 12% | Omnichannel focus |

The categorization of these revenues shows a market moving away from purely discretionary items. While Electronics remains a leader at 32% revenue share, Food and Beverages have surged to match that level, reflecting the integration of grocery delivery into daily habits. This trend is vital for platforms like Magalu, which acquired VIP Commerce in 2021 specifically to digitalize supermarkets across the country.

Section II: The Technological Infrastructure of the Digital Economy

The backbone of Brazil’s e-commerce rise is its connectivity infrastructure. By early 2025, the country reached 183 million internet users, a penetration rate of 86.2%. More importantly, the quality of this connection has improved significantly, with median mobile speeds reaching 80.97 Mbps and fixed speeds hitting 183.56 Mbps. This bandwidth is the prerequisite for rich-media commerce, including high-definition live streams and augmented-reality (AR) features such as L'Oréal's virtual try-ons, which help reduce return rates.

The Role of 5G and Mobile Dominance

The rollout of 5G, reported as having significant coverage across Brazil by late 2024, is a primary driver for the social commerce market. With 73% of transactions happening on smartphones, the market has leapfrogged the PC-era entirely in lower-income regions. Retailers are now optimizing their interfaces for "one-hand navigation" and voice search to accommodate on-the-go browsing habits.

Fintech Integration and Credit Accessibility

Fintech is not just about payments but about credit. Brazil’s high bank penetration (96%) is largely driven by digital banks and fintechs. Platforms like Mercado Livre and Magalu now offer credit directly to their sellers, bypassing traditional banking hurdles. This is critical in a country where 60% of low-income citizens lack a traditional credit card. The use of Pix transaction data to build alternative credit scoring models is a "third-order" insight: by analyzing real-time cash flows instead of static banking history, platforms can extend credit to millions of informal workers, further fueling the e-commerce engine.

Section III: Deep Dive into Platform Strategies

Mercado Livre: Logistics and Financial Integration

Mercado Livre’s leadership is not merely a matter of being first. Its investment in Mercado Envios has fundamentally changed delivery expectations in Brazil. By mid-2025, the platform was handling 345 million monthly visits, a scale that allows it to negotiate unprecedented freight rates. The synergy between Mercado Pago and the marketplace creates a flywheel effect: sellers who use Mercado Pago for processing are more likely to reinvest that capital back into the platform's advertising (Mercado Ads) and logistics services.

Amazon: The Prime Ecosystem in Brazil

Amazon’s expansion in Brazil is a case study in adapting a global model to local complexities. The company has focused on "Prime benefits" as its primary lever, integrating fast shipping with Video and Music services to lower customer acquisition costs. Amazon's logistics network now includes 10 fulfillment centers and 22 delivery stations nationwide. A key tactical move has been the partnership with local residents in favelas, ensuring that "unmapped" areas are no longer excluded from the digital economy.

Magalu: The Evolution of a Retail Legend

Magalu’s transformation from a traditional 1957 storefront into a digital powerhouse is a benchmark for legacy retail. The "Parceiro Magalu" program has brought over 200,000 small and medium-sized businesses onto the platform, many of whom were recruited directly by physical store teams. This "human heat" strategy distinguishes Magalu from purely digital competitors.

Magalu Pillar | Operational Focus | Key Performance Indicator (KPI) |

Magalog | Integrated 1P/3P Logistics | 50% deliveries within 48 hours |

MagaluBank | Digital Accounts & Credit | R$65 Billion TPV (2021) |

Magalu Cloud | Scalable IT Infrastructure | Supporting 300,000 sellers |

MagaluAds | Multi-channel Advertising | High conversion content portals |

The financial impact of this integration is evident: Magalu’s service revenues grew by 32% in Q2 2023, offsetting drops in merchandise margins and resulting in a gross margin of 28.8%.

Americanas S.A.: The Road to Recovery

The judicial recovery of Americanas is perhaps the most significant corporate event in recent Brazilian retail history. The R$25.3 billion fraud led to a strategic pivot that saw the company close 92 stores in 2024 to optimize its footprint.[22] The focus is now on a "physical marketplace," where third-party sellers can utilize the physical shelf space of Americanas stores for high-margin categories like beauty and home goods.[22] The company reported a consolidated net revenue of R$14.3 billion in 2024, and despite a 17.4% revenue decline in Q1 2025, it posted a positive Adjusted EBITDA of R$339 million for the first half of the year, signaling the early stages of a turnaround.

Section IV: Logistical Frontiers - From Cajamar to the Amazon

Brazil's vast geography creates a "two-tier" logistical reality. In the "industrial Southeast," the focus is on automation and speed. In the "remote North," the focus is on survival and multimodal ingenuity.

The Rise of "Warehouse Cities"

Cajamar and Extrema have become the logistical heart of Brazil. These municipalities offer tax incentives and proximity to the Rodoanel Mário Covas, the massive beltway surrounding São Paulo. The concentration of warehouses in these areas has led to a shortage of specialized labor, forcing platforms to invest in automated sorting systems and IoT-based tracking.

The Amazon Basin: River and Air Synergy

In the Amazon region, logistics costs are a prohibitive 25% of the final product price. The reliance on river transport means that during the "Low Water Season," freight rates can jump by 45%.

Amazon Logistics Challenge | Strategic Solution |

7-10 day transit (Barge) | Custom Cargo Planes (Bemol) |

60% Capacity drop in LWS | Multi-modal Barge-Truck integration |

Lack of home delivery | Stores as Micro-fulfillment hubs |

High fuel costs | Sustainable river freight initiatives |

The integration of drones is being explored for the most remote areas, though it remains in the pilot stage. For now, the "store-as-a-hub" model remains the most viable, as it allows consumers to pick up orders in a central municipal location rather than relying on unpaved "last-mile" routes.

Section V: The Regulatory Maze - Taxes, Privacy, and Reform

Brazil is often referred to as the "Country of a Thousand Taxes," and e-commerce is at the center of this complexity.

Remessa Conforme and the 60% Import Tax

The Remessa Conforme program was a direct response to the "unfair competition" from Asian giants like Shein and AliExpress. Before 2023, many platforms exploited loopholes to avoid tax on individual parcels. The new 60% tax on goods over US$50 has forced a fundamental change in business models. Shopee and Shein have both shifted toward a "local-first" model, where they act more as domestic marketplaces than cross-border portals.

The Dual VAT Reform: CBS and IBS

The transition to a Dual VAT system is expected to be the most significant regulatory shift since the introduction of the Real. For e-commerce companies, the challenge is the "Technical Note 2025.002," which requires new fields in electronic invoices to accommodate the CBS (Federal) and IBS (State/Municipal) taxes. This requires a massive overhaul of ERP and accounting software, creating a temporary "compliance burden" but promising a more transparent system in the long run.

LGPD and Data Sovereignty

The General Data Protection Law (LGPD) has forced platforms to be more transparent about how they use consumer data for targeted advertising. Compliance costs are high, especially for SMEs, but the law is seen as essential for protecting the 94 million Brazilians who will be shopping online by 2025.

Section VI: Consumer Behavior - The Social and Mobile Paradigm

The Brazilian consumer is unique in their digital habits. They are older than often expected—more than half are over the age of 35—and they are highly deliberate in their purchasing behavior.

The Influence of Social Media

Brazilians spend three hours a day on social media, making platforms like Instagram and TikTok the primary "discovery engines". This has led to the "TikTok-ization" of retail, where short-form, viral content drives impulse buys. The launch of TikTok Shop in 2025 will be a "pivotal battleground" for the market.

Live Shopping Success Stories

Live shopping has successfully compressed the marketing funnel. For example, beauty brand P. Louise generated US$2 million in sales during a 12-hour TikTok marathon. Success in this format requires "charismatic hosts" and real-time interaction, turning a static product page into an entertainment event.

The Sustainability Factor

Sustainability is no longer a niche concern. 60% of Brazilian consumers state they are willing to pay more for products from environmentally-conscious brands. This is driving investments in "green logistics," including the electric truck corridors and eco-friendly packaging.

Section VII: Future Outlook and Strategic Conclusions

The future of Brazilian e-commerce is tied to its ability to integrate the unbanked and the remote. The market is projected to grow to US$1,499 billion by 2033 (broadly defined), a CAGR of 12.65%.

Key Strategic Takeaways:

Fintech-Retail Convergence: The platforms that act like banks will win. The ability to offer credit and instant payments (Pix) is the primary driver of loyalty.

Logistical Decentralization: The "warehouse city" model is expanding to Tier-2 and Tier-3 cities as platforms seek to replicate São Paulo’s 24-hour delivery speeds in the Northeast and Central-West.

Localization of Cross-Border: International players must manufacture locally to survive the new tax regime. Shein’s 2,000-factory goal is the template for foreign success.

Social-Mobile Dominance: The "Super-App" is the goal. Consumers want to discover, discuss, and buy within a single mobile environment without ever leaving the app.

In conclusion, Brazil's e-commerce market has reached a state of maturity that makes it a global leader in digital innovation. While logistical and regulatory challenges remain, the combination of high internet penetration, a revolutionary payment system, and a consumer base that is increasingly comfortable with digital-first life ensures that Brazil will remain the dominant force in Latin American e-commerce for the next decade. The successful e-commerce platform of 2030 will be a hybrid: a logistics company, a bank, and a social media network all rolled into one.

Read More -

1. From Idea to MVP: A Step-by-Step Guide for Solo Founder

🔗 https://findnstart.com/blogs/from-idea-to-mvp-a-step-by-step-guide-for-solo-founder

2. How to Validate Your Startup Idea in 48 Hours for $0

🔗 https://findnstart.com/blogs/how-to-validate-your-startup-idea-in-48-hours-for-0

3. Remote vs. Local: Does Your Co-Founder Need to Live in the Same City?

🔗 https://findnstart.com/blogs/remote-vs-local-does-your-co-founder-need-to-live-in-the-same-city

4. The 2026 Startup Landscape: What Has Fundamentally Changed (and Why Founder Skills Matter More Than Ever)

5. The Most In-Demand Skills for Startup Founders in 2026

🔗 https://findnstart.com/blogs/the-most-in-demand-skills-for-startup-founders-in-2026

6. How to Find a Technical Co-Founder (Without a Six-Figure Salary)

🔗 https://findnstart.com/blogs/how-to-find-a-technical-co-founder-without-a-six-figure-salary

7. 5 Red Flags to Look for When Choosing a Startup Partner

🔗 https://findnstart.com/blogs/5-red-flags-to-look-for-when-choosing-a-startup-partner

8. How to Pitch Your Idea to Potential Co-Founders

🔗 https://findnstart.com/blogs/how-to-pitch-your-idea-to-potential-co-founders

9. How to Build a Portfolio that Attracts High-Growth Startup Founders

🔗 https://findnstart.com/blogs/how-to-build-a-portfolio-that-attracts-high-growth-startup-founders

10. Equity vs. Salary: How to Split Ownership with Your First Teammate

🔗 https://findnstart.com/blogs/equity-vs-salary-how-to-split-ownership-with-your-first-teammate

11. Why Joining an Early-Stage Startup is Better Than a Corporate Job

🔗 https://findnstart.com/blogs/why-joining-an-early-stage-startup-is-better-than-a-corporate-job

12. The Future of EdTech: Why Developers and Educators Need to Team Up Now

🔗 https://findnstart.com/blogs/the-future-of-edtech-why-developers-and-educators-need-to-team-up-now

13. The Architecture of Symbiosis: Analytical Perspectives on the Five Habits of Successful Startup Duos

14. Finding a Co-Founder in the AI Space: What Skills Should You Look For?

🔗 https://findnstart.com/blogs/finding-a-co-founder-in-the-ai-space-what-skills-should-you-look-for

15. Overcoming Analysis Paralysis and the Strategic Path to Execution

🔗 https://findnstart.com/blogs/overcoming-analysis-paralysis-and-the-strategic-path-to-execution

16. From College Project to Company: How to Find Your Student Co-Founder

🔗 https://findnstart.com/blogs/from-college-project-to-company-how-to-find-your-student-co-founder

17. How to Start a Startup While Working a Full-Time Job

🔗 https://findnstart.com/blogs/how-to-start-a-startup-while-working-a-full-time-job

18. How to Build a HealthTech Startup Without a Medical Degree

🔗 https://findnstart.com/blogs/how-to-build-a-healthtech-startup-without-a-medical-degree

19. The Solitary Architect: Executive Isolation in Entrepreneurship

20. The 2026 Guide to Launching a SaaS as a Solo Developer

21. What Sustainable Growth Actually Looks Like

🔗 https://findnstart.com/blogs/what-sustainable-growth-actually-looks-like

22. The Early Warning Signs Your Startup Is in Trouble

🔗 https://findnstart.com/blogs/the-early-warning-signs-your-startup-is-in-trouble

23. How to Grow Without Burning Out

🔗 https://findnstart.com/blogs/how-to-grow-without-burning-out

24. The Truth About “Runway” Most Founders Ignore

🔗 https://findnstart.com/blogs/the-truth-about-runway-most-founders-ignore

25. Revenue Solves More Problems Than Funding

🔗 https://findnstart.com/blogs/revenue-solves-more-problems-than-funding

26. What No One Tells You About Being a Solo Founder

🔗 https://findnstart.com/blogs/what-no-one-tells-you-about-being-a-solo-founder

27. Why Smart People Quit High-Paying Jobs to Build Startups (And Why Most Regret It)

28. Why Most Startup Advice on Twitter Is Dangerous

🔗 https://findnstart.com/blogs/why-most-startup-advice-on-twitter-is-dangerous

29. Decision Fatigue: The Silent Startup Killer

🔗 https://findnstart.com/blogs/decision-fatigue-the-silent-startup-killer

30. Fear vs Logic: How Founders Actually Make Decisions

🔗 https://findnstart.com/blogs/fear-vs-logic-how-founders-actually-make-decisions

31. How Overthinking Destroys Early Momentum

🔗 https://findnstart.com/blogs/how-overthinking-destroys-early-momentum

32. Ideas Don’t Scale. Systems Do.

🔗 https://findnstart.com/blogs/ideas-dont-scale-systems-do

33. The First Hire That Actually Matters

🔗 https://findnstart.com/blogs/the-first-hire-that-actually-matters

34. How the First 100 Users Decide Your Startup’s Fate

🔗 https://findnstart.com/blogs/how-the-first-100-users-decide-your-startups-fate

35. Why Your Startup Doesn’t Need Growth — It Needs Focus

🔗 https://findnstart.com/blogs/why-your-startup-doesnt-need-growthit-needs-focus

36. Why Most Startups Die Quietly

🔗 https://findnstart.com/blogs/why-most-startups-die-quietly

37. Lessons Learned Too Late by First-Time Founders

🔗 https://findnstart.com/blogs/lessons-learned-too-late-by-first-time-founders

38. The Myth of the “Overnight Success” Startup

🔗 https://findnstart.com/blogs/the-myth-of-the-overnight-success-startup