The Rise of D2C Brands Built from Bangalore

June 29, 2026 by Harshit Gupta

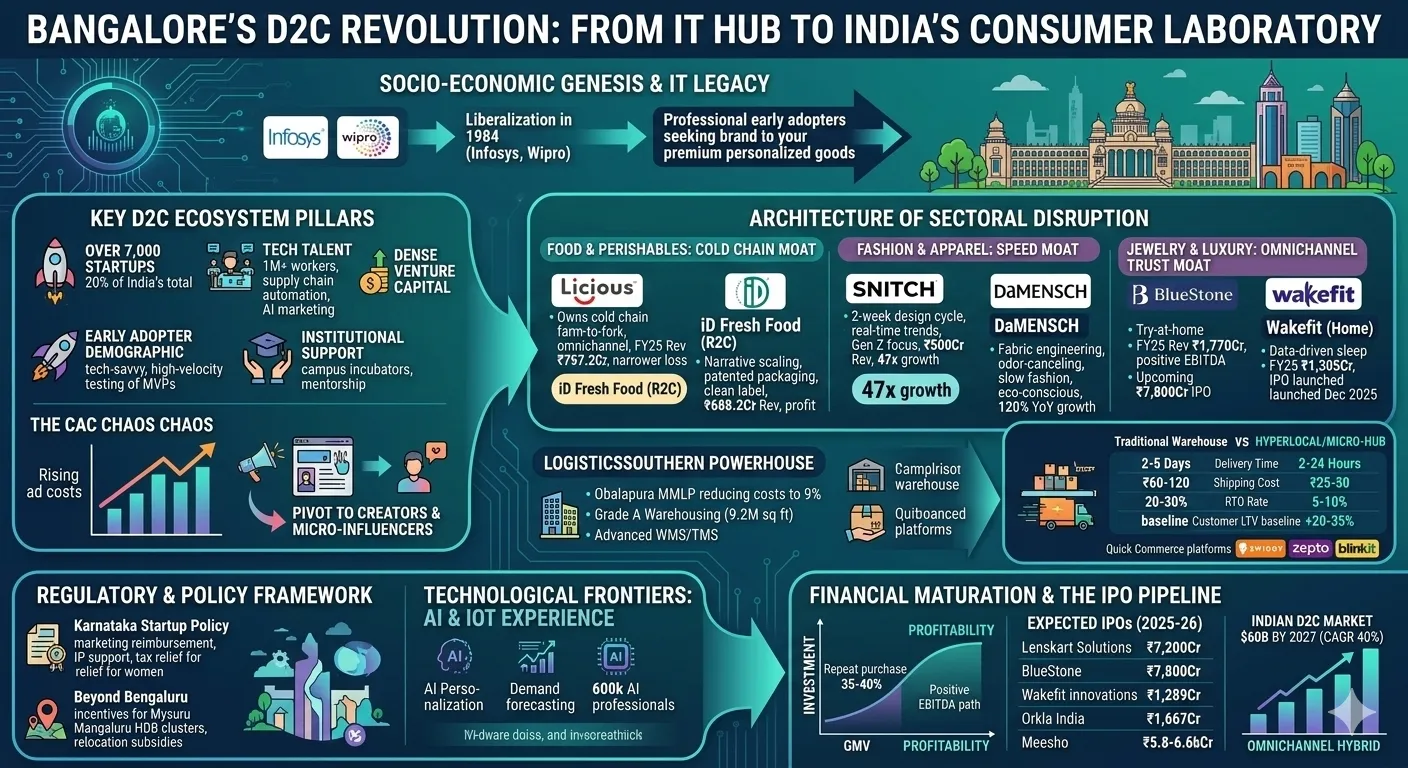

The structural metamorphosis of Bangalore from a post-colonial public sector hub into the definitive epicenter of India’s Direct-to-Consumer (D2C) revolution represents one of the most significant shifts in the global retail landscape. Traditionally celebrated as the "Silicon Valley of India" for its dominance in information technology and software services, the city has successfully leveraged its deep technological roots to architect a new generation of consumer brands. This evolution is not merely an extension of the e-commerce boom but a distinct phenomenon characterized by the convergence of high-density venture capital, a sophisticated talent pool, and a unique urban demographic that serves as a high-velocity testing ground for innovation. Currently housing over 7,000 startups—accounting for approximately 20% of India’s total startup population—Bangalore has become a self-sustaining engine of innovation where digital-first brands can iterate, scale, and eventually disrupt traditional retail legacies.

The Socio-Economic Genesis of the Bangalore D2C Ecosystem

The rise of D2C brands in Bangalore is fundamentally rooted in the city’s historical role as a magnet for engineering and management talent. The shift began as early as 1984 with the liberalization of computer hardware and software exports, which prompted the establishment of headquarters for iconic firms like Wipro and Infosys. These early movers created an environment where education was prioritized over the mere accumulation of wealth, fostering a culture of innovation that would later provide the skeletal structure for the D2C movement. As the IT sector matured, it attracted a demographic of young, highly paid professionals from across the country, creating a resident population of "early adopters" who were comfortable with digital transactions and sought premium, personalized alternatives to mass-market goods.

This demographic dividend was complemented by the "credit card culture" and a splurge-oriented hedonistic attitude that emerged in the first decade of the 21st century. Unlike other Indian metros where traditional wealth might be more conservative, Bangalore’s professional class demonstrated a willingness to experiment with new products, from organic foods to high-end fashion, creating a localized demand curve that D2C founders could exploit. The city’s weather and verdant settings further acted as a "magnet," drawing international companies and talent, thereby globalizing the local consumer’s palate and expectations.

The Role of Academic and Professional Incubators

The transition from software services to product-led entrepreneurship was further accelerated by Bangalore’s educational infrastructure. Engineering and MBA colleges in the city were among the first in India to set up campus incubators. Institutions like IIM Bangalore’s NSRCEL and the Indian Institute of Science (IISc) provided the necessary mentorship and seed capital for budding entrepreneurs to develop their Most Valuable Players (MVPs) and take them to market. This proximity between academia and industry created a seamless pipeline of founders who viewed the D2C model not just as a retail strategy, but as a technological challenge involving complex supply chains and data-driven customer acquisition.

Key Ecosystem Pillar | Influence on D2C Success | Source |

Tech Talent Pool | Availability of over 1 million tech workers for supply chain automation and AI-driven marketing. | |

Early Adopter Demographic | A tech-savvy urban population willing to test and provide feedback on MVPs. | |

Institutional Support | Over 1,000 AI startups and established incubators providing mentorship and early capital. | |

Geographic Centrality | Strategic location in South India providing a gateway to high-consumption southern states. |

Sectoral Analysis: The Architecture of Disruption

The Bangalore D2C landscape is characterized by its sectoral diversity, ranging from highly perishable food items to high-ticket luxury jewelry and ergonomically engineered furniture. Each sector has utilized the city’s unique advantages differently, often building proprietary technology stacks to manage the inherent complexities of the D2C model.

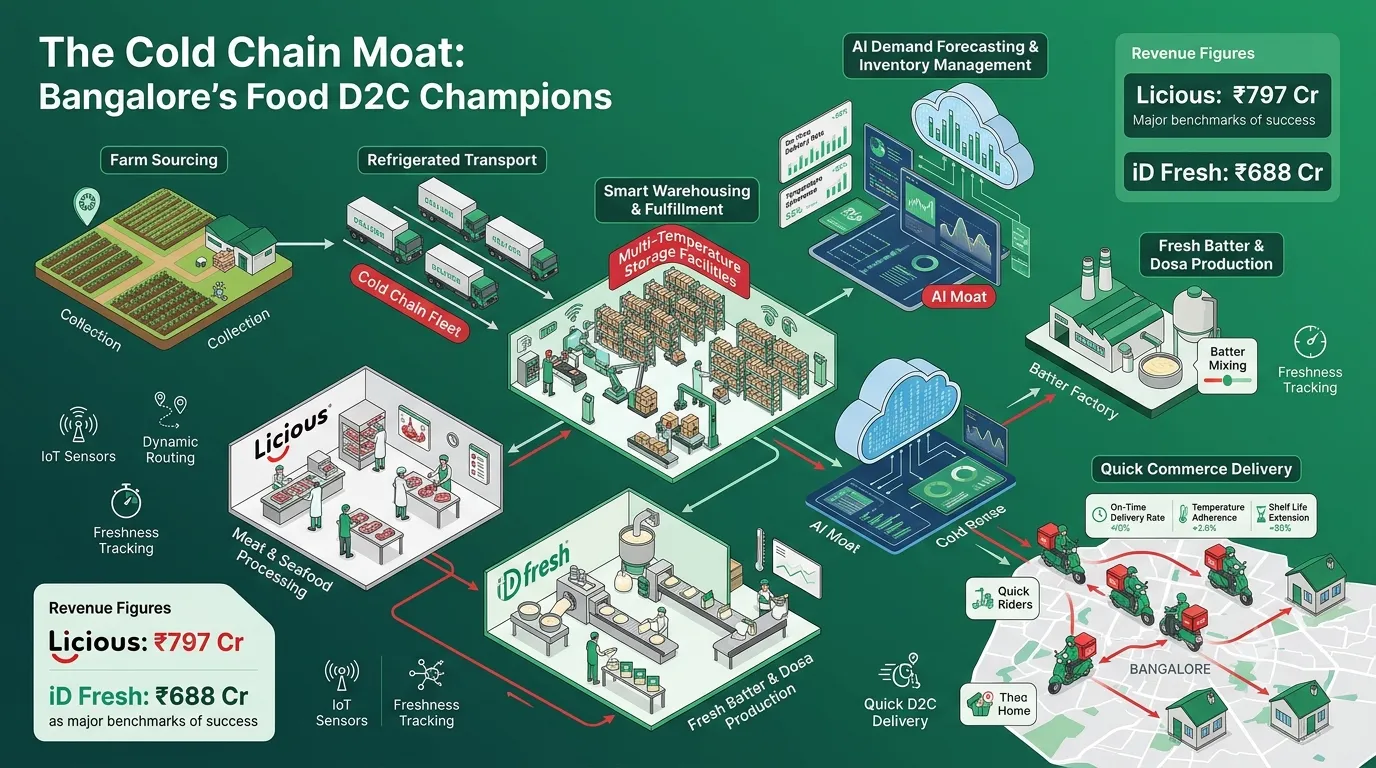

Food and Perishables: The Cold Chain Moat

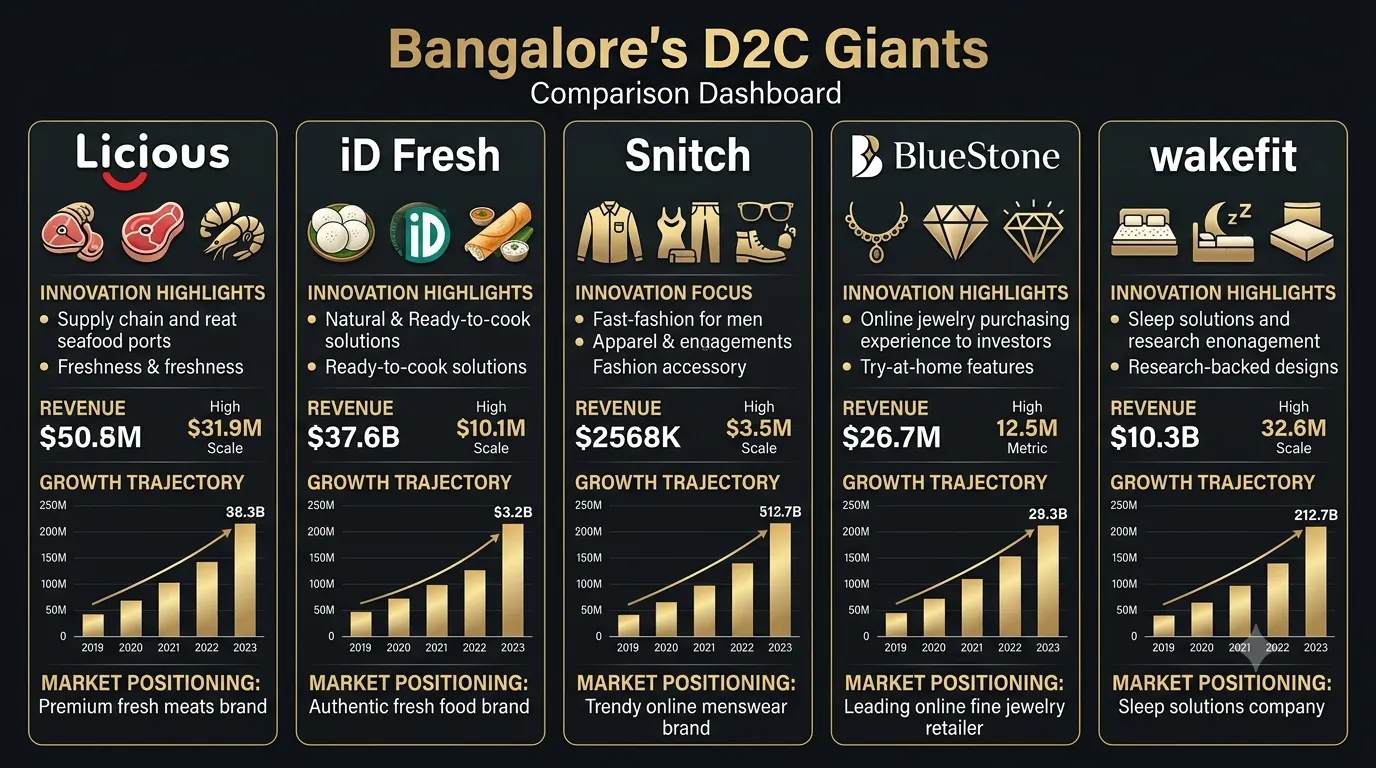

Perhaps the most formidable challenge in the D2C space is the management of fresh, perishable goods. Bangalore-based brands like Licious and iD Fresh Food have built significant market moats by essentially becoming logistics companies that happen to sell food. Licious, founded in 2015 by Abhay Hanjura and Vivek Gupta, revolutionized the unorganized meat and seafood industry by taking complete control of the back-end supply chain. By owning the cold chain from farm to fork, they addressed the critical consumer pain point of hygiene and quality.

The financial trajectory of Licious underscores the broader market shift toward disciplined growth. In FY25, the company reported a 16% increase in operating revenue to ₹797.2 crore, while successfully narrowing its net loss by 27% to ₹218.3 crore. This recovery was driven by an omnichannel strategy that integrated online sales with over 50 physical outlets, including the acquisition of the "My Chicken and More" chain. The brand’s "Licious Flash" service, which offers 30-minute delivery, now serves 60% of its online customers, illustrating the critical role of speed in the D2C value proposition.

iD Fresh Food provides a parallel example of narrative-driven scaling. Starting in 2005 with an investment of just ₹25,000 in a 50 sq ft kitchen, the founders focused on the "freshness" promise. The brand’s evolution was marked by a commitment to "clean-label" products—foods with no preservatives or synthetic additives. By FY25, iD Fresh Food achieved a revenue of ₹688.22 crore and demonstrated a path to sustainable profitability with a profit before tax of ₹26.7 crore. Their success is attributed to a patented daily cold-chain model that ensures fresh batter, parotas, and dairy reach over 45,000 retail outlets across 50 cities.

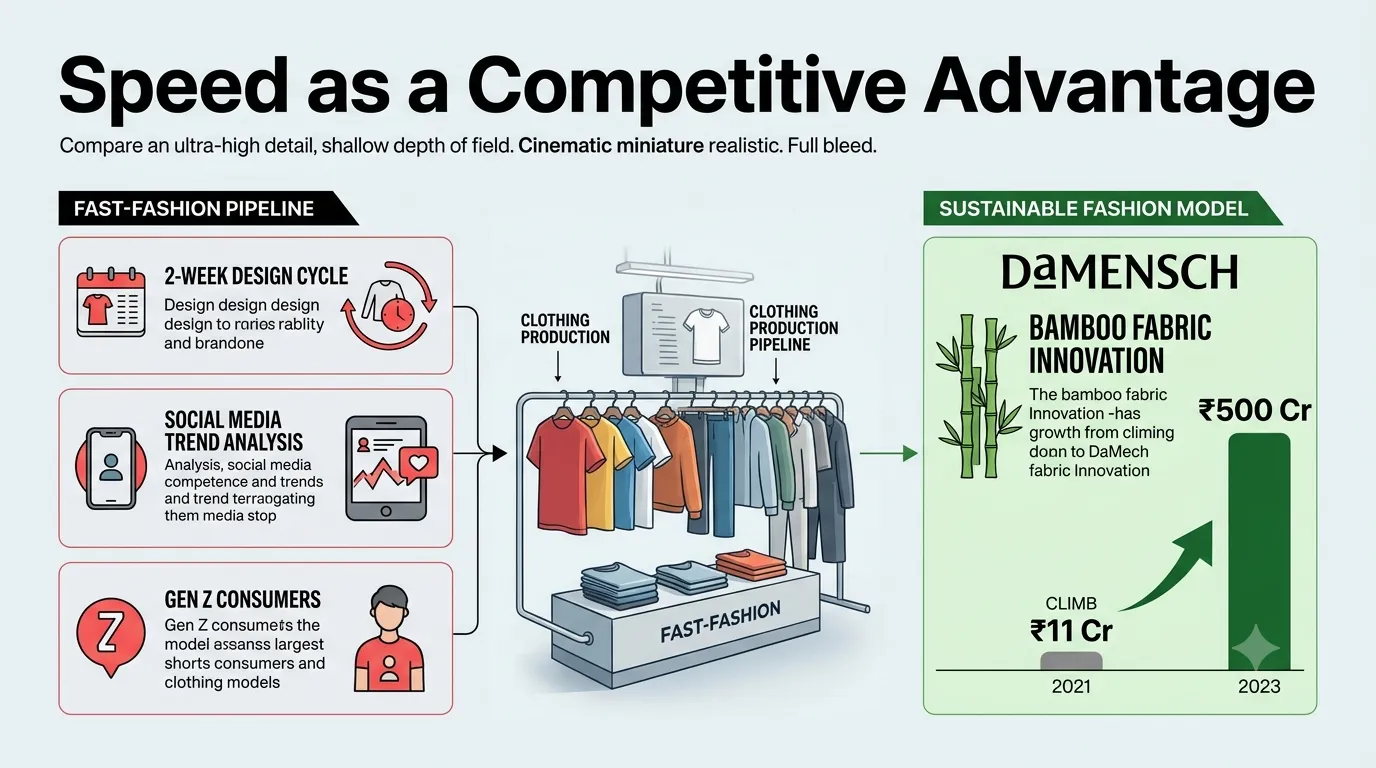

Fashion and Apparel: Speed as a Competitive Moat

In the fashion segment, Bangalore brands like Snitch and DaMENSCH have redefined the relationship between the brand and the consumer by focusing on rapid design cycles and fabric innovation. Snitch, founded in 2020 by Siddharth Dungarwal, has pioneered a "fast-fashion" model in India that rivals global giants. By operating on 2-week design-to-shelf cycles—a fraction of the industry standard—the brand can capitalize on real-time consumer trends identified through social media and web analytics.

Snitch’s growth is emblematic of the city's high-velocity scaling potential. The brand’s revenue surged from ₹11 crore in 2021 to over ₹500 crore in FY25, representing a 47x revenue growth in just four years. This scaling was fueled by a ₹340 crore Series B funding round in June 2025, which valued the company at approximately ₹2,500 crore. The brand’s strategy involves a heavy focus on Gen Z consumers who seek "affordable premium" fashion, and an aggressive move into physical retail with a target of 100 stores by the end of 2025.

DaMENSCH, specializing in men's innerwear and lifestyle essentials, has taken a different approach by focusing on "fabric engineering". Founded in 2018 by Anurag Saboo and Gaurav Pushkar, the brand introduced innovation to a stagnant category with odor-canceling underwear and thermo-regulating vests made from bamboo fibers. The brand reached a ₹100 crore ARR in 2021 and has since expanded into loungewear and casualwear, maintaining a 120% YoY growth rate. Their emphasis on sustainable "slow fashion" and plastic-free packaging from corn-based materials resonates with the city’s increasingly eco-conscious consumer base.

Brand | Sector | Primary Innovation | Revenue Scale |

Licious | Food (Meat) | Proprietary cold-chain and farm-to-fork ownership. | ₹797.2 Cr (FY25) |

iD Fresh Food | Food (R2C) | Patented packaging and daily cold-chain distribution. | ₹688.2 Cr (FY25) |

Snitch | Fashion | 2-week design-to-shelf fast-fashion cycle. | ₹500 Cr (FY25) |

BlueStone | Jewelry | "Try-at-home" service and vertically integrated manufacturing. | ₹1,770 Cr (FY25) |

Wakefit | Home | Data-driven sleep products and bed-in-a-box logistics. | ₹1,305 Cr (FY25) |

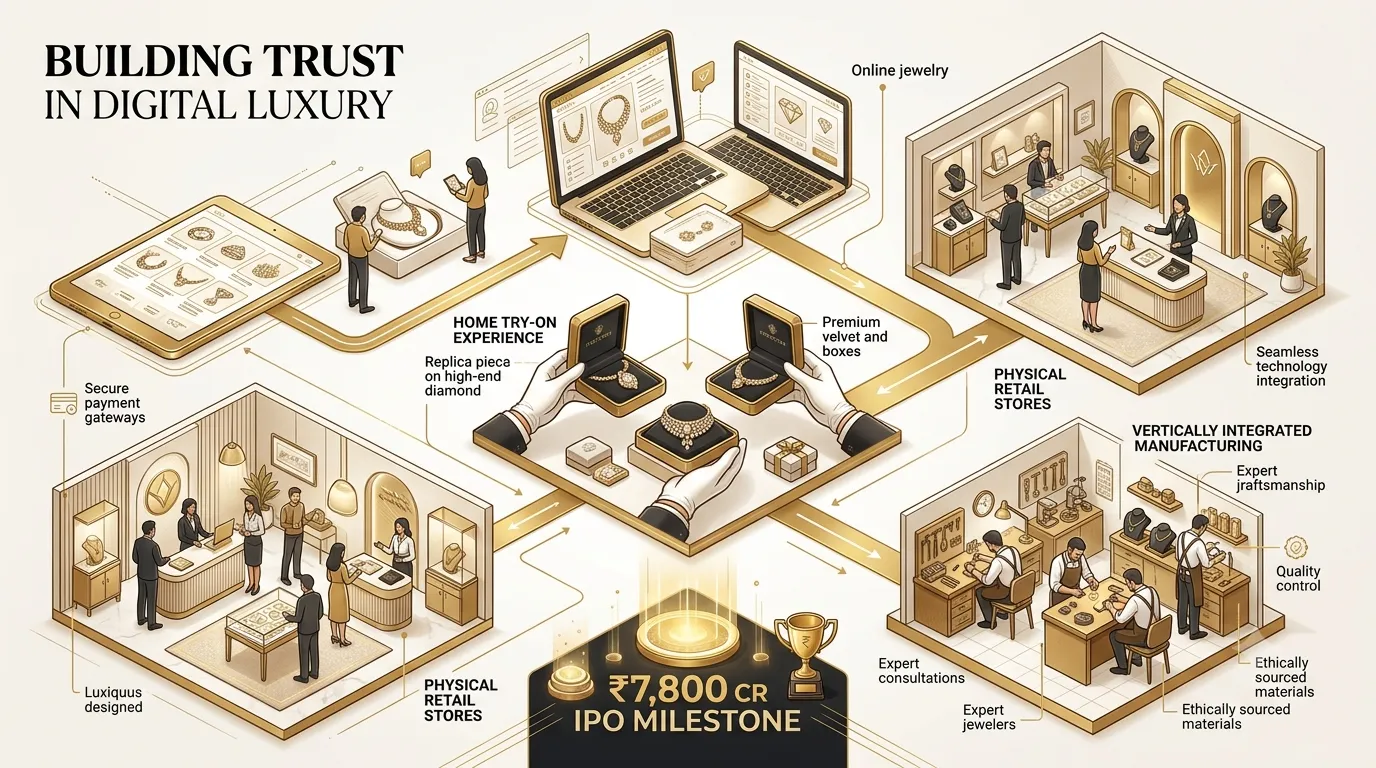

Jewelry and Luxury: The Omnichannel Trust Model

The jewelry sector in Bangalore, led by brands like BlueStone and CaratLane, has managed to digitize one of the most trust-sensitive categories in retail. BlueStone, founded in 2011 by Gaurav Singh Kushwaha, successfully addressed the "trust gap" in online jewelry sales by introducing a unique "try-at-home" service. This model allows customers to browse designs online and have physical samples delivered to their doorstep for a risk-free trial, creating a seamless bridge between digital convenience and physical assurance.

BlueStone’s financial scale reflects the maturity of the city's D2C ecosystem. In FY25, the brand reported a revenue of ₹1,770 crore, a 40% increase from the previous fiscal year. Despite widening net losses to ₹222 crore as it expanded its physical footprint, the company achieved a positive EBITDA of ₹133 crore. The brand’s vertically integrated operations—where 75% of jewelry is produced in-house—allow for a superior "manufacturing-to-shelf" turnaround time compared to traditional jewelers. As of 2025, the brand operates 275 stores across 117 cities, with its upcoming ₹7,800 crore IPO signaling the culmination of its journey from a Bangalore startup to a national leader.

Financial Engineering and the Venture Capital Narrative

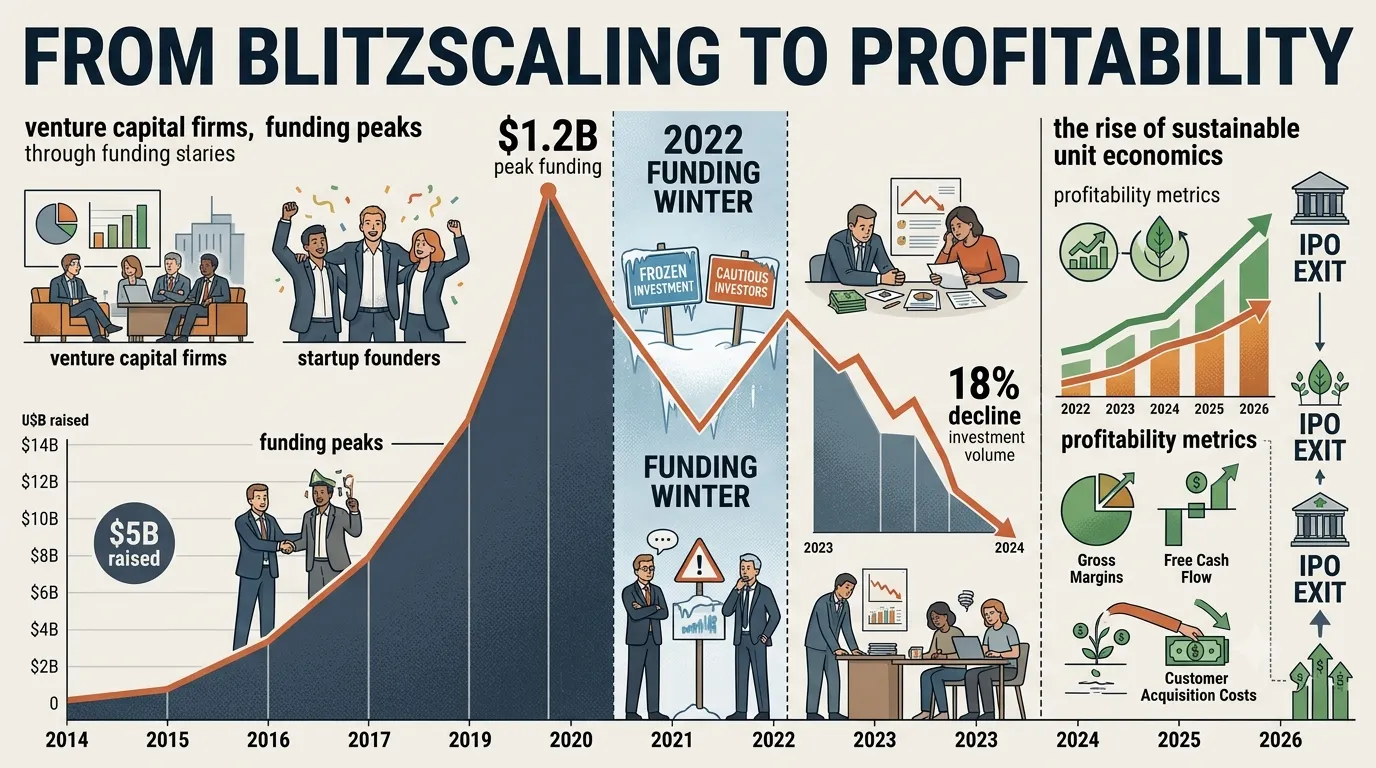

The rapid ascent of Bangalore’s D2C brands would have been impossible without the city’s dense concentration of venture capital and growth equity firms. Between 2014 and 2022, Indian D2C startups raised over $5 billion in funding, with a significant portion of this capital flowing into Bangalore-based enterprises. However, the role of capital has evolved from facilitating "growth at any cost" to demanding "disciplined profitability".

The Evolution of Funding Cycles

The period of 2021 saw peak investment levels, with $1.2 billion invested in the D2C segment in a single year. This influx of capital allowed brands like Wakefit and Licious to reach unicorn status and dominate their respective categories. However, the "funding winter" that began in late 2022 prompted a significant reset. Total venture funding for Indian D2C startups dropped from $930 million in 2023 to $757 million in 2024, representing an 18% decline.

This moderation in capital has forced a shift toward unit economics. Brands that once prioritized Gross Merchandise Value (GMV) now focus on contribution margins and customer lifetime value (LTV). The current investor paradigm favors brands with repeat purchase rates above 35–40% and sustainable EBITDA pathways.

The IPO Pipeline and Exit Strategies

As the D2C ecosystem matures, the focus has shifted toward public market exits. The years 2025 and 2026 are projected to be landmark years for D2C IPOs in India. Wakefit, which reached a revenue of ₹1,305 crore in FY25, launched its ₹1,289 crore IPO in December 2025, valuing the company at approximately ₹6,300 crore. Similarly, BlueStone and Lenskart are preparing for high-value listings that will provide critical liquidity to early-stage venture investors.

MarginEBITDA=RevenueTotalEBITDA×100

For Wakefit in H1 FY26, this calculation illustrates the turnaround in profitability:

MarginEBITDA=7,413.0 Mn1,031.9 Mn×100≈13.92%

Upcoming IPO (Expected 2025-26) | Sector | Estimated Issue Size (₹ Cr) | Source |

Lenskart Solutions | Eyewear | ₹7,200 Cr | |

BlueStone Jewellery | Jewelry | ₹7,800 Cr | |

Wakefit Innovations | Home Décor | ₹1,289 Cr | |

Orkla India (MTR Foods) | FMCG | ₹1,667 Cr | |

Meesho | E-Commerce | ₹5,800–₹6,600 Cr |

Infrastructure: The Physical Backbone of D2C Growth

The geographic concentration of D2C brands in Bangalore is heavily supported by the city’s evolving logistics and warehousing infrastructure. Strategic public and private investments have transformed the city into a "Logistic Southern Powerhouse," enabling the rapid movement of goods across India’s southern states.

Multimodal Logistics and Grade A Warehousing

The construction of the 400-acre Obalapura Multimodal Logistics Park (MMLP), which commenced in 2024, is designed to drastically reduce logistics costs from 13% to 9% of total expenditure. By integrating road, rail, and warehousing, the MMLP facilitates efficient national distribution, linking key industrial corridors like the Bengaluru-Chennai Expressway. Additionally, the AISATS BLR Logistics Park at Kempegowda International Airport—an 8-acre facility opened in 2025—provides specialized cold-chain and bonded storage, which is critical for the expansion of food and pharmaceutical D2C brands.

The city also boasts a massive supply of Grade A industrial and warehousing space, which reached 9.2 million sq ft in 2024. These high-tech facilities utilize advanced Warehouse Management Systems (WMS) and Transport Management Systems (TMS), offering real-time tracking and predictive analytics that D2C brands leverage to minimize stockouts and overproduction.

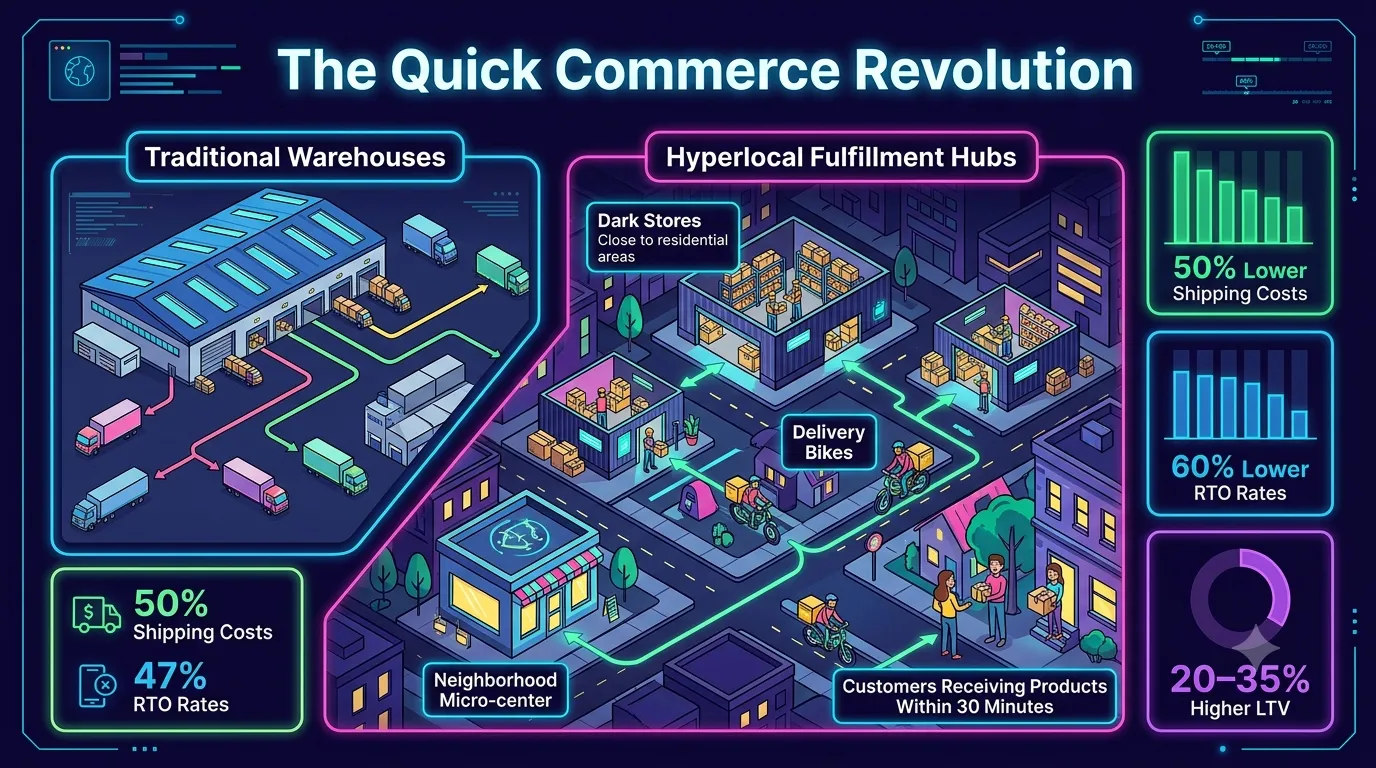

Hyperlocal Fulfillment and Quick Commerce

A defining feature of the current Bangalore retail landscape is the rise of "Quick Commerce". Platforms like Swiggy, Zepto, and Blinkit have reset consumer expectations, with many D2C brands now offering 30-to-60-minute delivery windows in urban clusters. This is made possible through "hyperlocal fulfillment," where brands store inventory in neighborhood micro-fulfillment centers rather than centralized warehouses.

The ROI drivers of this hyperlocal model are substantial. Brands utilizing neighborhood fulfillment have reported a 30-50% reduction in shipping costs and a 40-60% decrease in Return to Origin (RTO) rates. In the fashion segment, where fit and style are subjective, faster delivery ensures the item reaches the customer while their purchase intent is still high, significantly increasing the likelihood of acceptance.

Fulfillment Metric | Traditional Warehouse | Hyperlocal/Micro-Hub | Benefit/Impact |

Delivery Time | 2-5 Days | 2-24 Hours | Higher conversion rates (+15-25%). |

Shipping Cost | ₹60-120 per order | ₹25-50 per order | 30-50% savings on last-mile. |

RTO Rate | 20-30% | 5-10% | 40-60% reduction in returns. |

Customer LTV | Baseline | +20-35% | Improved loyalty due to speed. |

The Regulatory and Policy Framework: Incentivizing Innovation

The Government of Karnataka has been a pivotal partner in the D2C revolution, enacting policies that not only support startups in Bangalore but also encourage the decentralization of innovation across the state.

The Karnataka Startup Policy 2022-2027

This comprehensive framework aims to nurture 25,000 technology-based startups by 2027. For D2C brands, the policy provides a suite of financial and operational incentives:

Marketing Reimbursement: Startups can claim 30% of their international marketing costs (up to ₹5 lakh per year), supporting global expansion efforts for Bangalore-born brands.

Intellectual Property Support: The state offers reimbursements of up to ₹2 lakh for national and ₹10 lakh for international patent and trademark filings.

Tax and Regulatory Relief: Registered startups benefit from exemptions on VAT/CST and GST reimbursements, as well as collateral-free loans for women-led ventures.

The "Beyond Bengaluru" Initiative

To mitigate urban stress and tap into regional talent, the state launched the "Beyond Bengaluru" initiative. This program targets emerging clusters like Mysuru, Mangaluru, and Hubballi-Dharwad-Belagavi (HDB), providing specific incentives for brands to establish operations outside the capital.

Infrastructure Subsidies: Startups relocating to these clusters can receive a 50% reimbursement on office rent (up to ₹2 crore) and a 30% property tax rebate for three years.

Talent Incentives: A "talent relocation reimbursement" of up to ₹50,000 per employee is available to help companies move their core teams to Tier-2 cities.

Sectoral Clusters: The state is setting up dedicated "Global Innovation Districts" and incubators for AI, Biotech, and AVGC (Animation, Visual Effects, Gaming, and Comics) in these regional hubs.

As of 2025, the "Beyond Bengaluru" policy has resulted in the establishment of 138 new companies and 35 expansions in regional clusters, creating nearly 10,000 jobs and positioning cities like Mysuru as potential hubs for specific niches like sustainable fashion or organic agro-processing.

Technological Frontiers: AI and the D2C Experience

Bangalore’s emergence as the "Silicon Valley" of D2C is most evident in the integration of Artificial Intelligence (AI) across the entire value chain. With over 600,000 AI/ML professionals, the city provides the largest pool of AI talent outside the United States, allowing brands to implement sophisticated technologies that are often unavailable to their global counterparts.

AI in Personalization and Demand Forecasting

Modern D2C brands in Bangalore utilize AI to deliver hyper-personalized shopping experiences. By analyzing millions of data points—from browsing history to clickstream patterns—brands like Snitch can serve personalized product recommendations that significantly increase conversion rates. Furthermore, AI-powered demand forecasting helps brands like Licious manage highly complex, perishable inventories, reducing waste and ensuring that products are always available when a customer orders.

IoT and Smart Supply Chains

The Internet of Things (IoT) has also become a critical tool for logistics optimization. Connected tracking devices provided by firms like Jimi IoT offer real-time visibility into inventory levels and supply chain efficiency. This technology allows D2C brands to monitor the temperature of perishable goods during transit, ensuring the integrity of the cold chain and building consumer trust through transparency.

Challenges and Strategic Tactical Shifts

Despite the favorable environment, the Bangalore D2C ecosystem faces a series of structural challenges that have necessitated tactical shifts in how brands operate.

The "CAC Chaos" and the Pivot to Creators

For several years, D2C growth was fueled by aggressive performance marketing on platforms like Meta and Google. However, rising competition and auction saturation have led to "CAC chaos," where the cost of acquiring a new customer often exceeds the initial order value. Brands have responded by behaving more like "digital creators" and less like traditional advertisers.

By investing in short-form video (Reels) and influencer partnerships, brands like Snitch have managed to drive up to 50% of their traffic through organic channels. Today, over 70% of D2C brands use creators to drive sales, with 54% of brands allocating up to 25% of their marketing budget to micro-influencers who deliver 5x-6x higher engagement than celebrity endorsements.

Unit Economics and Operational Discipline

The funding moderation has brought unit economics to the forefront. A healthy D2C brand in Bangalore is now expected to maintain gross margins between 40% and 60%. However, after accounting for shipping, packaging, and high Return-to-Origin (RTO) rates (which can reach 20-30% in fashion), these margins can drop precariously. Brands are increasingly using Virtual CFO services to implement tighter financial controls and ensure that every "additional sales rupee" contributes to the bottom line through operating leverage.

Analytical Synthesis and Future Outlook

The trajectory of D2C brands built from Bangalore suggests that the ecosystem is entering a phase of "structural maturation." The era of blitz-scaling through subsidized growth is ending, replaced by a period where operational excellence and omnichannel depth are the primary drivers of value.

The Emergence of the "Omnichannel Hybrid"

The future of D2C in Bangalore is not purely digital. The most successful brands—BlueStone, Wakefit, Licious—have all recognized that physical retail is essential for capturing the "non-digital" segments of the market and building deep consumer trust. We are seeing the rise of the "omnichannel hybrid," where digital discovery fuels offline purchase, and offline showrooms drive online repeat orders.

The Role of Quick Commerce as a Growth Lever

Quick commerce has transitioned from being a convenience for grocery delivery to a major discovery and sales channel for D2C brands. For categories like personal care and snacking, quick commerce platforms now account for 10-25% of urban revenues for scaled brands. This channel not only improves inventory turns but also reduces the brand's dependence on expensive paid digital acquisition.

Projections for 2025-2030

The Indian D2C market is projected to reach $60 billion by 2027, growing at a CAGR of 40%. Bangalore will likely remain the vanguard of this growth, but the next wave of innovation will be driven by "DeepTech" startups focusing on sustainability, ethical sourcing, and hyper-customization. The "Beyond Bengaluru" initiative will decentralize this growth, creating a "hub and spoke" network of regional innovation centers that will help Karnataka maintain its competitive edge on the global stage.

In summary, the rise of D2C brands in Bangalore is a story of technological convergence. By merging the software expertise of the past with the retail demands of the future, the city has created a new economic template for the digital age. As these brands move toward public listings and international expansion, they will continue to redefine what it means to be a "modern consumer brand" in an increasingly connected world. The Silicon Valley of India has successfully transitioned into the Consumer Laboratory of the World, and its impact on the global retail narrative is only just beginning.

Protect Your Future: The Precision Vesting Calculator

Don't let a "handshake deal" complicate your exit. Map out your ownership journey with our Vesting Calculator

Calculate Your Vesting Schedule →