The Pressure to Raise in Silicon Valley

March 8, 2026 by Harshit Gupta

The startup ecosystem of Bengaluru, historically positioned as the "Silicon Valley of India," has reached a critical juncture where the act of fundraising has transitioned from a strategic milestone to an all-encompassing structural pressure. While the city remains the undisputed leader in Indian venture capital (VC) activity, accounting for approximately 40% to 50% of the country’s total startup funding across the last decade, the nature of "the raise" has been fundamentally altered by the post-2022 "funding winter". This pressure is not merely a financial necessity but a complex intersection of macro-economic fluctuations, escalating operational costs, a fiercely competitive talent market, and a deep-seated cultural obsession with valuation as a proxy for validation. As the ecosystem matures toward a 2025-2026 horizon, the "pressure to raise" has become the defining feature of the Bangalore founder experience, influencing product development cycles, governing hiring practices, and profoundly impacting the mental health of the entrepreneurial community.

The Macro-Economic Foundations of Funding Pressure

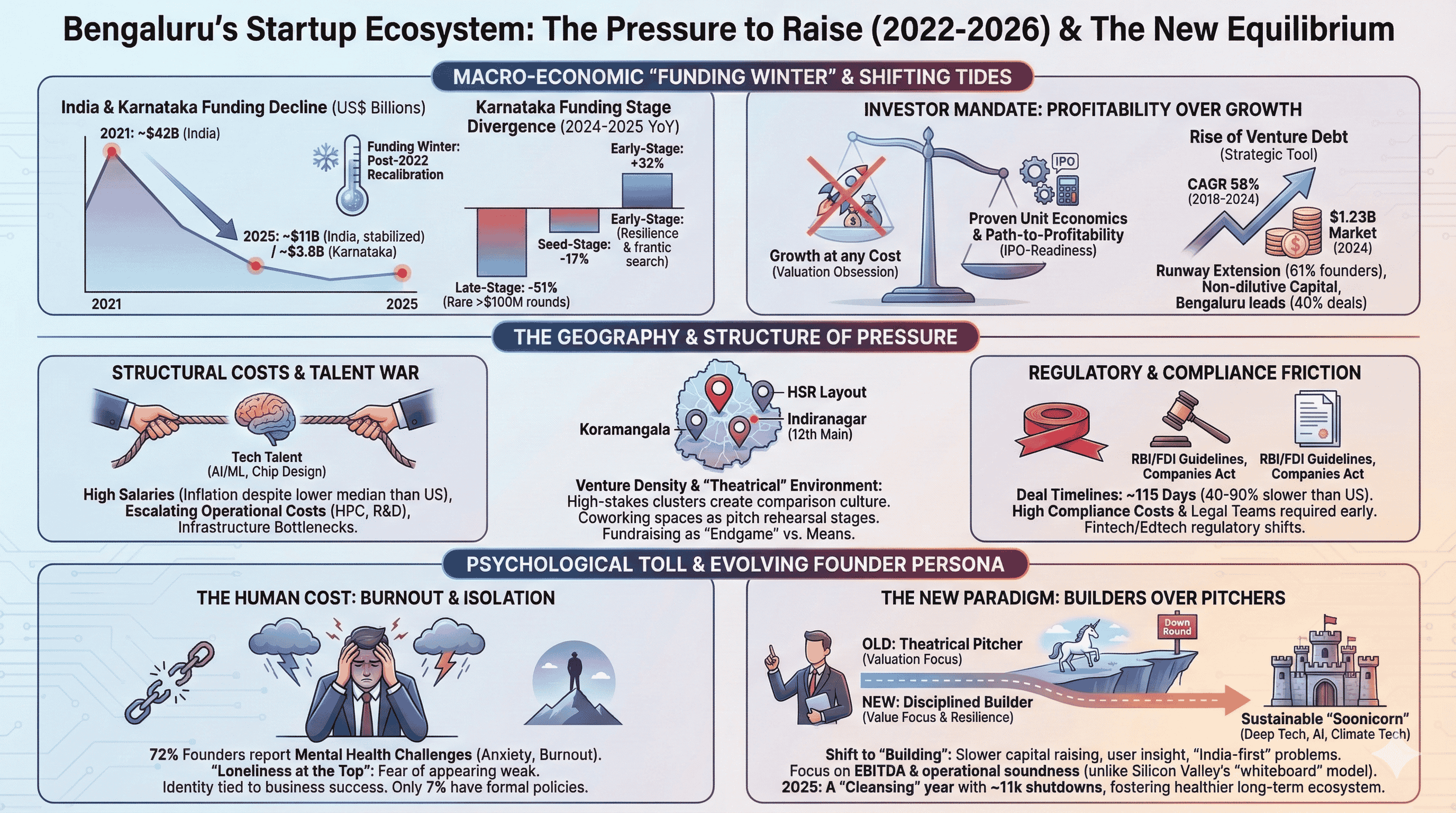

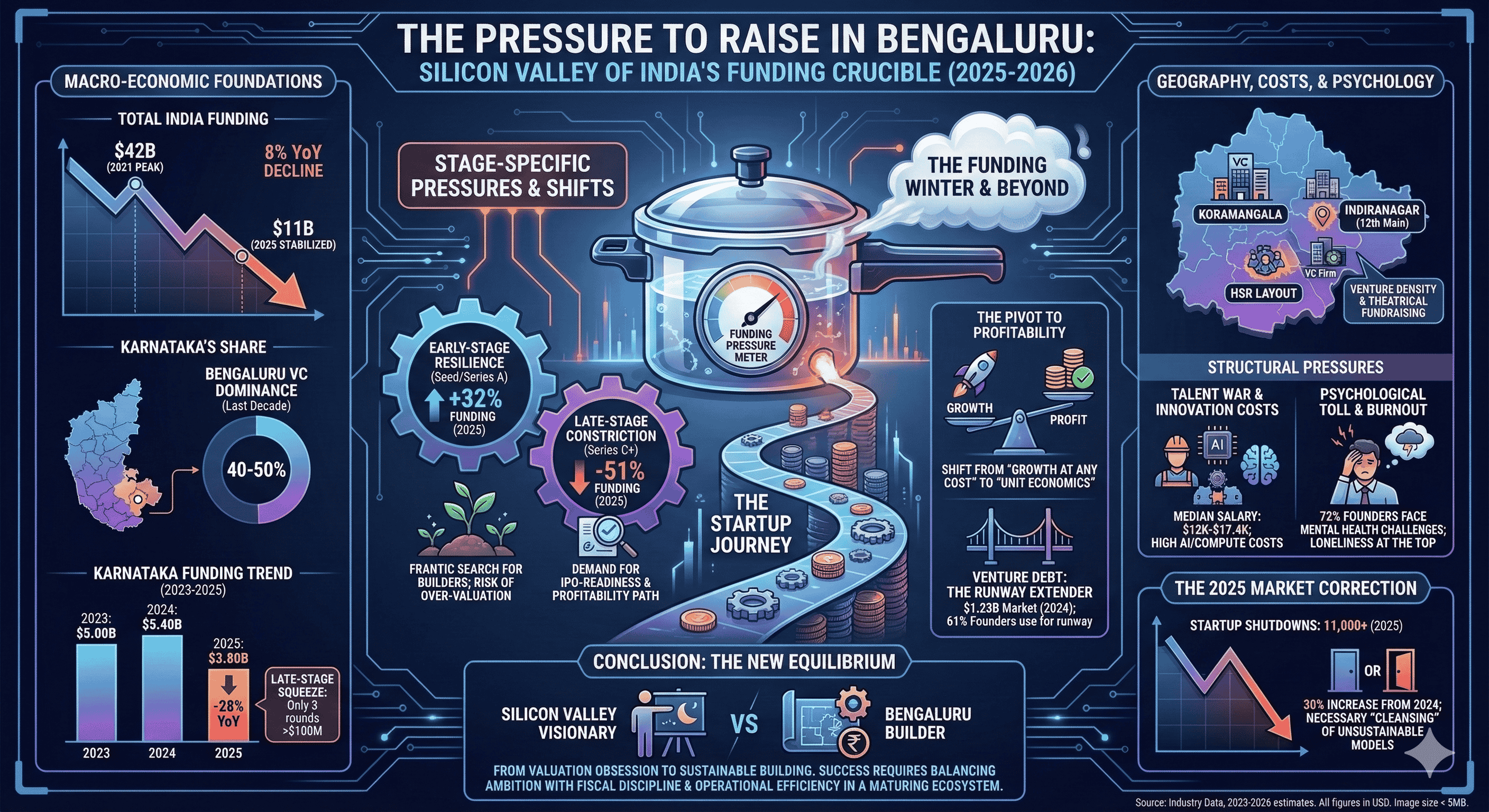

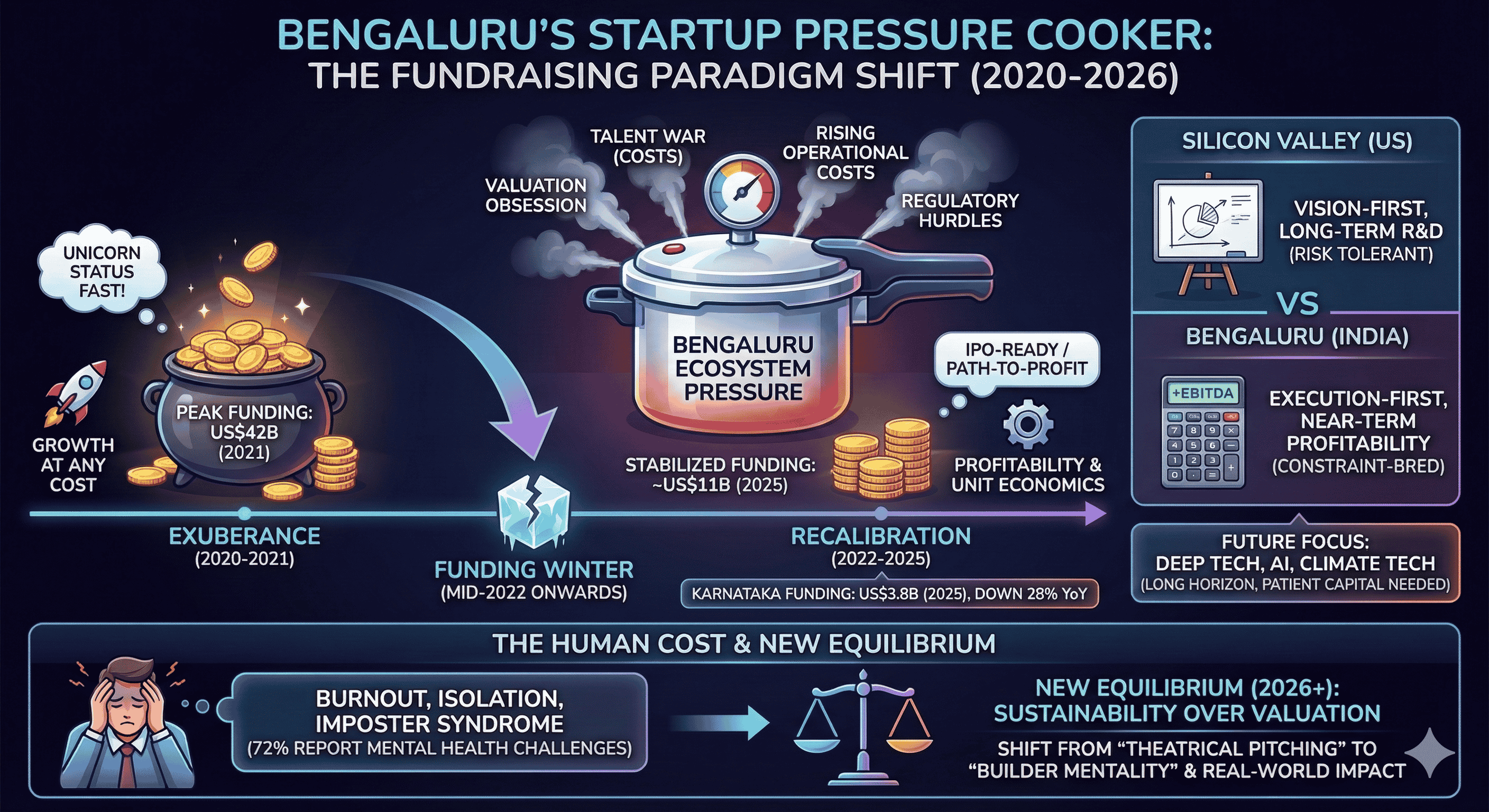

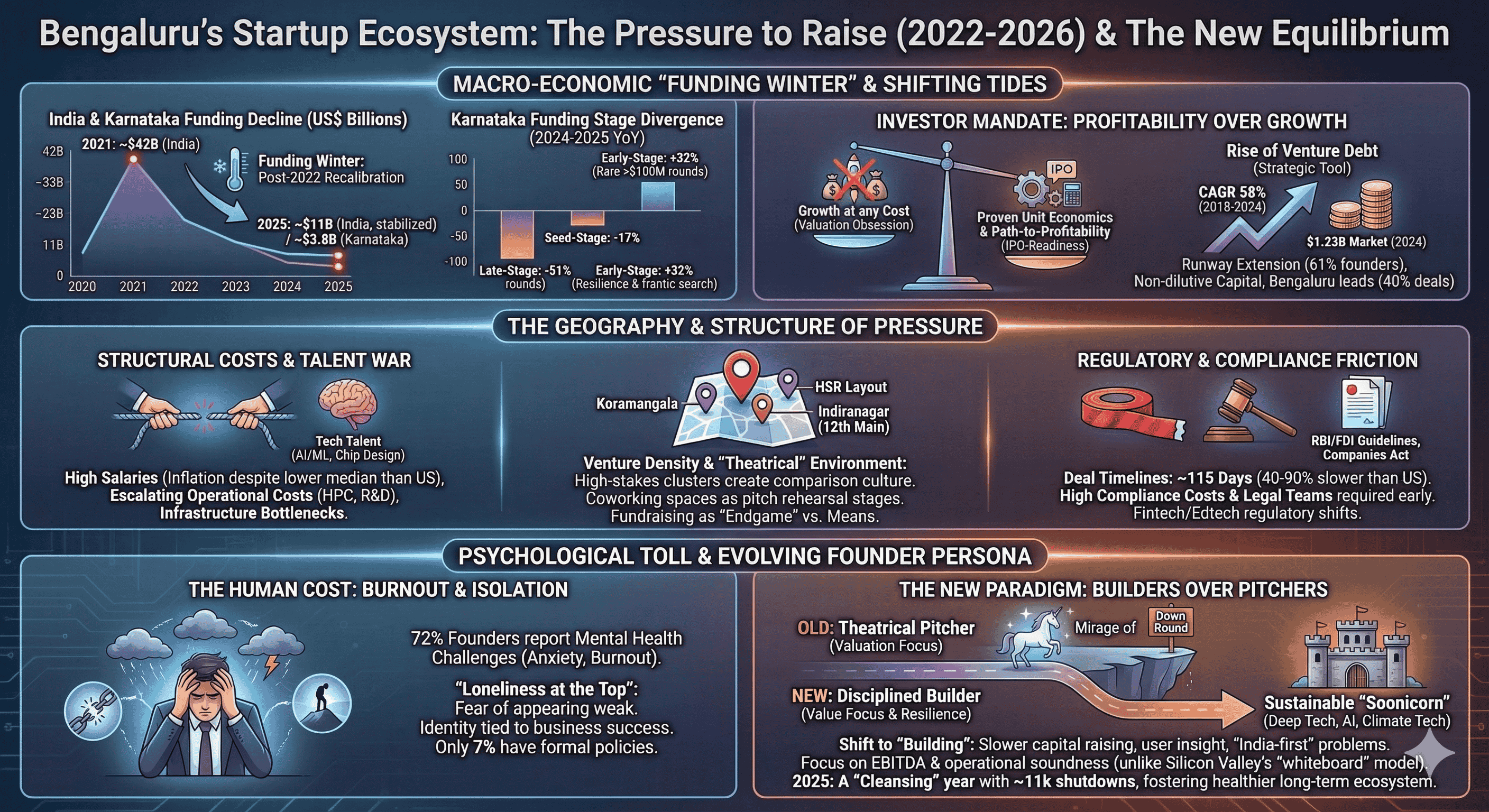

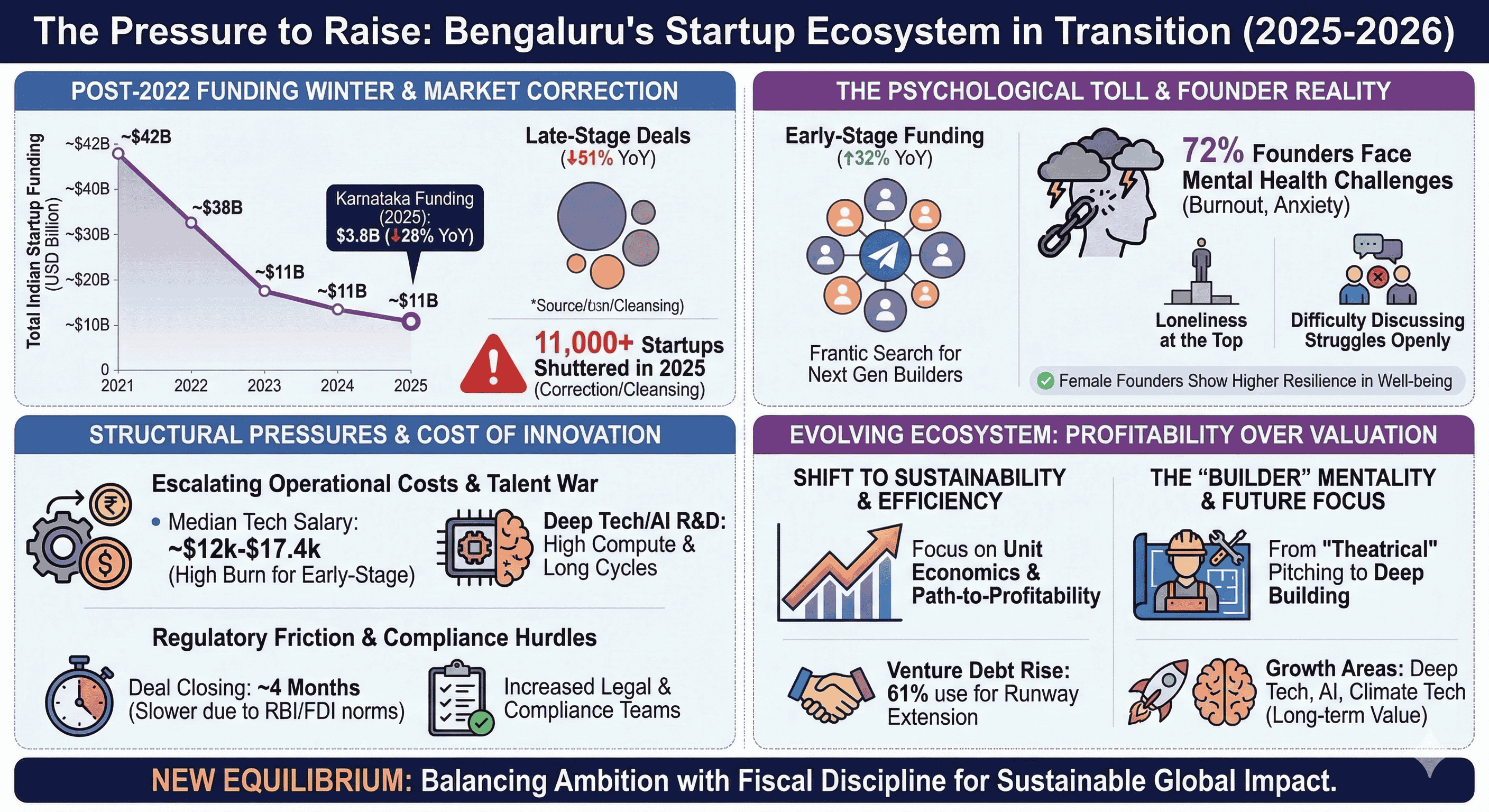

The period following the global pandemic witnessed an unprecedented surge in capital deployment within the Karnataka technology ecosystem, primarily concentrated in Bengaluru. Between 2020 and 2024, Bengaluru-based startups alone attracted a staggering US38billioninventurecapital.[2]However,theexuberanceof2021,ayearinwhichIndianstartupfundingpeakedatUS42 billion, gave way to a systemic recalibration that began in mid-2022 and continued through 2025. By 2025, total Indian startup funding had stabilized at approximately US$11 billion, reflecting an 8% year-on-year decline from 2024 and a significant contraction from the peak years.

This contraction has intensified the pressure on founders to secure capital under increasingly stringent conditions. While capital remains available, investor focus has shifted from "growth at any cost" to proven unit economics, profitability, and sustainable business models. In Karnataka, total funding fell to US3.8billionin2025,representinga281.8 billion—roughly half of its 2024 levels—creating an environment where later-stage startups face immense pressure to demonstrate "IPO-readiness" or path-to-profitability to survive.

Table 1: Comparative Funding Trends in the Karnataka Technology Ecosystem (2023–2025)

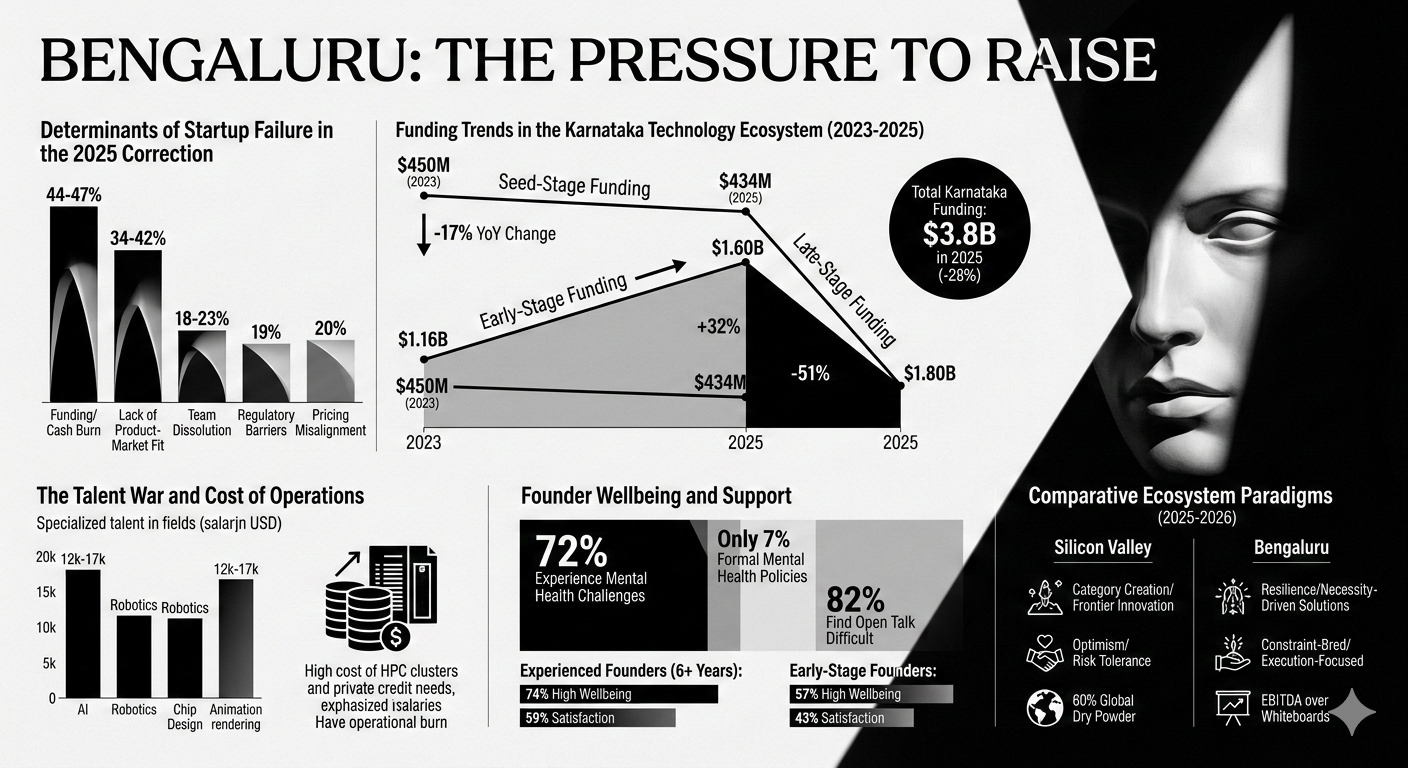

Funding Stage | 2023 Funding (USD) | 2024 Funding (USD) | 2025 Funding (USD) | 2024-2025 YoY Change |

Seed-Stage | $450 Million (est) | $523 Million | $434 Million | -17% |

Early-Stage | $1.16 Billion | $1.21 Billion | $1.60 Billion | +32% |

Late-Stage | $3.39 Billion | $3.66 Billion | $1.80 Billion | -51% |

Total | $5.00 Billion | $5.40 Billion | $3.80 Billion | -28% |

The divergence in funding across stages in 2025 provides a clear indicator of the specific pressures felt by founders. While late-stage deals became rarer—with Karnataka recording only three rounds above US$100 million in 2025 compared to nine in each of the previous two years—early-stage funding showed remarkable resilience, increasing by 32%. This indicates that while the pressure to raise is acute for established players, there is a frantic search for the next generation of "builders" at the seed and Series A levels, often leading to over-valuation at early stages which sets the stage for future "down round" pressures. The Geography of Expectation: Neighborhoods of Performance

The pressure to raise in Bangalore is localized within specific geographical clusters that have become synonymous with high-stakes entrepreneurship. Areas like Koramangala, HSR Layout, and Indiranagar—specifically the 12th Main Road in Indiranagar—host an unusually high density of venture firms, including marquee names like Peak XV Partners, Lightspeed India, and Antler India. This "venture density" creates a hothouse environment where founders are constantly exposed to the fundraising successes of their peers, fostering a culture of comparison and an urgency to close rounds to remain socially and professionally relevant.

This physical proximity between capital and innovation has cultivated a "theatrical" fundraising environment. In coworking spaces across the city, the rehearsal of pitch decks and the updating of LinkedIn titles have become daily rituals. The prevailing narrative often treats fundraising as the "endgame" rather than a means to an end. This has created a warped incentive structure where founders spend more time crafting compelling stories for investors than understanding their users or refining their products.

Table 2: Regional Dominance of Bengaluru in the Indian Tech Landscape (2025)

Metric | Bengaluru Statistics | National Rank/Context |

Total Active Startups | 16,000+ | #1 in India |

Unicorn Count | 53 | 5th Largest Hub Globally |

Software Professionals | 2.5 Million | Largest Tech Workforce Globally |

AI/ML Talent Pool | 50% of India | National Leader |

VC/Angel Population | 1,536 firms / 17k angels | Primary Capital Hub |

The sheer volume of talent and capital in the city creates a self-reinforcing feedback loop. Bengaluru welcomes between 150,000 and 200,000 new technology employees annually, and approximately 25% of the city’s population is employed in the software or startup sector. In this environment, tech innovation is viewed as a basic necessity—often described as the "new roti, kapda, makaan" (food, clothing, and shelter)—highlighting how central the tech economy is to the city's socio-economic identity. Consequently, the inability to raise capital is often perceived not just as a business failure, but as a loss of status within the city’s primary social hierarchy.

Structural Pressures: The Cost of Innovation and the Talent War

One of the primary drivers behind the constant need for capital is the rising cost of operations in Bangalore. Despite being more affordable than global peers like San Francisco, the city’s internal costs have surged. Software salaries in Bengaluru, while lower than in Silicon Valley, have seen significant inflation as startups compete for top-tier talent in specialized fields like AI, robotics, and chip design. The median annual salary of a software professional in Bengaluru is approximately US12,000toUS17,400, which, while lower than international peers, represents a significant burn rate for early-stage companies without consistent revenue.

The "talent war" creates a specific type of fundraising urgency. To attract and retain the best engineers, startups must offer competitive salaries and equity packages. This requires continuous infusions of capital, especially in the early stages when revenue is minimal. Furthermore, the city’s infrastructure bottlenecks, such as high-end rendering costs for animation studios or the prohibitive expense of high-performance computing (HPC) clusters for AI startups, force founders to seek private credit or venture funding to bridge gaps that traditional banks are unwilling to cover.

Table 3: Sectoral Funding Shifts in Karnataka (2024–2025)

Sector | 2025 Funding (USD) | Year-on-Year Trend | Driver of Pressure |

Enterprise Applications | $1.1 Billion | Stable | SaaS efficiency metrics |

Fintech | $1.0 Billion | +47% Rebound | Regulatory compliance/KYC |

Retail Tech | $920 Million | Significant Decline | Consumer cost sensitivity |

Deep Tech / AI | $1.06 Billion (India-wide) | +100% Increase | High R&D/compute costs |

While Delhi-NCR has occasionally surpassed Bengaluru in the number of new startups recognized, Bengaluru remains the leader in quality and high-value creations. The pressure to raise in Bengaluru is often tied to the city's focus on "Deep Tech" and complex technologies which, by their nature, require longer R&D cycles and more patient capital. This creates a "valley of death" for deep tech startups that may require three to five years of research before achieving a successful pilot, yet are often pressured by the domestic investor ecosystem to show immediate revenue or domestic market fit.

The Pivot to Profitability and the Rise of Venture Debt

As the "funding winter" progressed through 2024 and 2025, the mandate for founders shifted from growth to efficiency. Investors began rewarding startups that could achieve significant milestones with optimized headcounts and leaner operations. This shift has led to a surge in interest for venture debt as a strategic tool. India's venture debt market grew at a CAGR of 58% between 2018 and 2024, reaching US$1.23 billion in 2024, with Bengaluru leading the market by accounting for 40% of all deals.

Venture debt is increasingly used by founders to extend their runway between equity rounds without further diluting their ownership. Approximately 61% of founders now highlight venture debt as a preferred tool for runway extension and working capital management. This reflects a maturing ecosystem where founders are prioritizing unit economics and cash cycles over the "valuation obsession" of previous years.

Table 4: Venture Debt Usage and Preferred Milestones (2025)

Metric | Statistic / Outcome |

Market Size (2024) | $1.23 Billion |

Bengaluru Deal Concentration | 40% |

Preferred Use: Runway Extension | 61% of Founders |

Preferred Use: Pre-IPO Bridge | 41% of Founders |

Preferred Use: Inventory/CAPEX | 37% of Founders |

Primary Sectors | Fintech (37%), Consumer (25%), Cleantech (18%) |

The pressure to be "IPO-ready" has also influenced fundraising strategies. With 18 startups tapping public markets in 2025 and at least 12 making successful debuts in 2024, late-stage funding is now heavily contingent on a clear 24–36 month roadmap to a public listing. This requires a focus on corporate governance and path-to-profitability much earlier in a company's lifecycle than was previously standard in the "fail fast" era.

The Psychological Toll: Burnout and the Valuation Trap

The unrelenting pressure to perform, raise capital, and outcompete has taken a severe toll on the mental health of Bangalore's founders. Recent data indicates that 72% of startup founders experience mental health challenges, ranging from anxiety and burnout to clinical depression. Despite the prevalence of these issues, only 7% of startups have formal mental health policies in place, and 82% of the community feels it is difficult to talk openly about these struggles.

The "loneliness at the top" is a recurring theme among Bengaluru's entrepreneurs. Founders often feel they cannot share their fears with employees or investors for fear of appearing weak or jeopardizing their funding. This is compounded by the fact that many founders tie their entire sense of self-worth to their business's success; when the business struggles, their identity is destabilized, leading to profound emotional distress.

Table 5: Entrepreneurial Wellbeing and Support Systems (2024)

Parameter | Experienced Founders (6+ Years) | Early-Stage Founders |

High Wellbeing Report | 74% | 57% |

Satisfaction with Career | 59% | 43% |

Impact of Imposter Syndrome | 31% (Overall) | Significantly Higher |

Low Community Support | 48% (Overall) | 48% (Overall) |

Strong Network Support | 31% (Overall) | 31% (Overall) |

Interestingly, female founders in India have shown higher resilience in certain areas, outperforming their male counterparts in work-life balance (58% vs. 37%) and emotional well-being (68% vs. 55%), despite receiving a disproportionately small share of total venture capital. The lack of community support remains a major hurdle, with nearly half of all founders reporting a lack of adequate support from entrepreneurial networks. This mental health crisis is not just a personal issue but a significant business risk, leading to risky decision-making, creative blocks, and disengaged teams.

The 2025 Market Correction: A Necessary "Cleansing"

The year 2025 has been described as a "watershed moment" for the Indian startup ecosystem, characterized by a profound structural correction. Over 11,000 startups shuttered in 2025—a 30% increase from 2024. While these numbers seem alarming, many industry analysts view this as a necessary "cleansing" of unsustainable business models that were built on the premise of cheap capital rather than actual market need.

Table 6: Primary Determinants of Startup Failure in the 2025 Correction

Determinant | Percentage | Core Underlying Issue |

Lack of Product-Market Fit | 34-42% | Building solutions without validated demand |

Funding/Cash Burn | 44-47% | Weak unit economics and poor runway planning |

Team Dissolution | 18-23% | Co-founder conflict, burnout, and poor hiring |

Regulatory Barriers | 19% | Complex legal/compliance shifts (Fintech/Edtech) |

Pricing Misalignment | 20% | Overestimation of revenue / Unviable models |

High-profile casualties like Dunzo and PharmEasy, which faced significant funding shortages and operational struggles, served as potent case studies for the ecosystem’s lingering challenges. The failure timeline accelerated in 2025, with seven startups shutting down within a year of inception compared to just one in 2024. This shift from "valuation-focused" to "value-focused" investing is expected to create a healthier environment for B2B partnerships and strategic investments in the long term.

Divergence from Silicon Valley: EBITDA over Whiteboards

A critical insight into the pressure to raise in Bangalore comes from its comparison with Silicon Valley. While Silicon Valley was built over five decades with heavy support from defense research and public R&D grants, the Bangalore ecosystem has compressed its growth into less than ten years. This rapid scaling has come at the cost of the "depth" seen in US research institutions and capital pools.

The investment philosophy in Bangalore is notably different. Historically, a Silicon Valley entrepreneur could raise millions based on a "whiteboard sketch" and a vision of global scale. In contrast, a Bangalore founder is more likely to be asked for a three-year EBITDA projection before even completing their first pilot. This "constraint-bred" execution has produced a different archetype of founder—one who is operationally sound and focuses on early validation, but who may also be less inclined to take the massive "moonshot" risks that define the US tech landscape.

Table 7: Comparative Ecosystem Paradigms (2025-2026)

Feature | Silicon Valley | Bengaluru (Bangalore) |

Core Philosophy | Category creation / Frontier innovation | Resilience / Necessity-driven solutions |

Cultural DNA | Optimism / Risk tolerance | Constraint-bred / Execution-focused |

Exit Strategy | Long-term R&D / M&A | IPO-ready / Profitability focus |

Government Role | Risk absorber (R&D grants) | Ecosystem operator (Digital Public Infra) |

Funding Access | 60% of global dry powder | Constrained / Highly selective |

This pressure to monetize early is particularly challenging for Deep Tech and AI startups. While the Indian government has launched initiatives like the Rs 10,000 crore Startup Fund of Funds 2.0 and the IndiaAI Mission to support these sectors, the domestic venture capital market still lacks the risk appetite to fund pre-revenue research for a decade or more. This creates a paradox where Bangalore is expected to lead in innovation but is simultaneously pressured to maintain the financial discipline of a much more mature industry.

The Evolution of the Founder Persona: From Pitcher to Builder

The current funding slowdown and market correction are leading to a fundamental shift in the definition of success in the Bangalore ecosystem. There is a growing movement to move away from "theatrical" entrepreneurship toward a focus on "building". This involves raising capital slower, optimizing for user insight rather than capital, and solving deep, "India-first" problems rather than replicating Western models.

Sectors like AI, Climate Tech, and Deep Tech are expected to drive the next wave of growth. Bangalore currently captures 82% of India’s AI application-layer investments, and the city remains a magnet for talent in advanced sectors like chip design, aerospace, and quantum computing. The emergence of "soonicorns" (soon-to-be unicorns) in these sectors—with Bengaluru hosting 39 soonicorns, far ahead of Delhi-NCR’s 30—suggests that the ecosystem is transitioning toward more complex, defensible technologies.

Table 8: Top Bootstrapped and Revenue-Led Success Stories (2024-2025)

Company | Status / Success Metric | Strategy |

Bootstrapped Unicorn (under 3 years) | Profitable from Day One | |

Navi Technologies | Fintech Profitability Success | 17x YoY profit growth (FY24) |

Ixigo | Successful IPO (2024) | 20-year journey of persistence |

Zerodha / Rainmatter | Self-funded Market Leader | Disciplined capital deployment |

LeadSquared | High-velocity SaaS Unicorn | Crushing sales automation |

The pressure to raise is unlikely to dissipate entirely, given the capital-intensive nature of high-tech innovation and the high costs of operating in a premier global hub. However, if the ecosystem continues to prioritize sustainable unit economics and "builder" mentalities, the nature of that pressure may evolve from a frantic search for survival to a strategic pursuit of global scale. The resilience demonstrated by Bengaluru’s startups during the 2023–2025 period suggests that while the city remains a pressure cooker for founders, it is also a uniquely fertile ground for the creation of companies that are both operationally sound and technologically ambitious.

Institutional and Policy Pressures: Navigating the Regulatory Minefield

Beyond the financial and psychological pressures, Bangalore-based founders face a significant regulatory burden that adds friction to the fundraising process. The Indian regulatory framework, encompassing FDI reporting, RBI pricing guidelines, and the Companies Act, adds approximately 2 to 4 weeks to deal closing times compared to Western counterparts. This delay is particularly stressful for startups operating on thin runways, as the timeline to close a funding round in India has stretched to an average of 115 days (~4 months)—40% to 90% slower than in the US.

Furthermore, sectors like Fintech and EdTech have faced intense pressure due to sudden regulatory shifts. The Reserve Bank of India (RBI) has implemented tighter regulations on digital lending and KYC, which contributed to a 75% failure rate among venture-backed Fintech startups in 2025. This regulatory environment forces founders to not only raise capital but also to build substantial legal and compliance teams early in their lifecycle, further increasing their burn rate and the subsequent need for more capital.

Table 9: Impact of Regulatory and Compliance Milestones on Deal Timelines

Milestone | Time Added / Requirement | Impact on Pressure |

RBI Pricing Guidelines | 2-4 Weeks | Delay in capital infusion |

FDI Reporting (FC-GPR) | Post-closing compliance | Administrative burden |

DPIIT Recognition | Prerequisite for tax benefits | High barrier for early startups |

Audited Financials | Mandatory for due diligence | High cost for seed-stage |

Corporate Governance | Series B+ requirement | Shift away from lean models |

The Karnataka state government has attempted to mitigate some of these pressures through initiatives like "Elevate" and the "Idea2PoC" scheme, which have funded over 1,000 startups with grants up to ₹50 lakh. However, these grants are often viewed as "starter" capital, and the pressure remains for founders to eventually transition to private venture funding to achieve meaningful scale. The role of the government as an "ecosystem operator" through the development of Digital Public Infrastructure (UPI, Aadhaar, ONDC) has lowered entry barriers for Fintech and Retail Tech, but the competitive pressure to acquire users on these "digital rails" remains as intense as ever.

Conclusion: The New Equilibrium of Bangalore Entrepreneurship

The cumulative evidence suggests that the "pressure to raise" in Bangalore has reached a new equilibrium. It is no longer a race for inflated valuations, but a quest for the strategic capital necessary to survive a structural market correction. The 11,223 shutdowns in 2025 serve as a stark reminder that capital without a viable business model is a liability.

The Bengaluru ecosystem remains the heart of the Indian startup revolution, hosting 2,467 startups (23% of the national total) and attracting 40% of all startup funding in the first half of 2025. However, the successful founder of the 2026 era will likely be one who balances the ambition of a Silicon Valley visionary with the fiscal discipline of a "constraint-bred" builder. This involves navigating the psychological toll of the talent war, the structural costs of deep-tech innovation, and the regulatory complexities of the Indian market with a focus on long-term sustainability rather than short-term valuation. As the "funding winter" thaws into a more sober and mature spring, the pressure to raise will persist, but it will be increasingly tempered by a culture that values unit economics, operational efficiency, and real-world impact over the theater of the pitch deck.

Read More -

1. From Idea to MVP: A Step-by-Step Guide for Solo Founder

🔗 https://findnstart.com/blogs/from-idea-to-mvp-a-step-by-step-guide-for-solo-founder

2. How to Validate Your Startup Idea in 48 Hours for $0

🔗 https://findnstart.com/blogs/how-to-validate-your-startup-idea-in-48-hours-for-0

3. Remote vs. Local: Does Your Co-Founder Need to Live in the Same City?

🔗 https://findnstart.com/blogs/remote-vs-local-does-your-co-founder-need-to-live-in-the-same-city

4. The 2026 Startup Landscape: What Has Fundamentally Changed (and Why Founder Skills Matter More Than Ever)

5. The Most In-Demand Skills for Startup Founders in 2026

🔗 https://findnstart.com/blogs/the-most-in-demand-skills-for-startup-founders-in-2026

6. How to Find a Technical Co-Founder (Without a Six-Figure Salary)

🔗 https://findnstart.com/blogs/how-to-find-a-technical-co-founder-without-a-six-figure-salary

7. 5 Red Flags to Look for When Choosing a Startup Partner

🔗 https://findnstart.com/blogs/5-red-flags-to-look-for-when-choosing-a-startup-partner

8. How to Pitch Your Idea to Potential Co-Founders

🔗 https://findnstart.com/blogs/how-to-pitch-your-idea-to-potential-co-founders

9. How to Build a Portfolio that Attracts High-Growth Startup Founders

🔗 https://findnstart.com/blogs/how-to-build-a-portfolio-that-attracts-high-growth-startup-founders

10. Equity vs. Salary: How to Split Ownership with Your First Teammate

🔗 https://findnstart.com/blogs/equity-vs-salary-how-to-split-ownership-with-your-first-teammate

11. Why Joining an Early-Stage Startup is Better Than a Corporate Job

🔗 https://findnstart.com/blogs/why-joining-an-early-stage-startup-is-better-than-a-corporate-job

12. The Future of EdTech: Why Developers and Educators Need to Team Up Now

🔗 https://findnstart.com/blogs/the-future-of-edtech-why-developers-and-educators-need-to-team-up-now

13. The Architecture of Symbiosis: Analytical Perspectives on the Five Habits of Successful Startup Duos

14. Finding a Co-Founder in the AI Space: What Skills Should You Look For?

🔗 https://findnstart.com/blogs/finding-a-co-founder-in-the-ai-space-what-skills-should-you-look-for

15. Overcoming Analysis Paralysis and the Strategic Path to Execution

🔗 https://findnstart.com/blogs/overcoming-analysis-paralysis-and-the-strategic-path-to-execution

16. From College Project to Company: How to Find Your Student Co-Founder

🔗 https://findnstart.com/blogs/from-college-project-to-company-how-to-find-your-student-co-founder

17. How to Start a Startup While Working a Full-Time Job

🔗 https://findnstart.com/blogs/how-to-start-a-startup-while-working-a-full-time-job

18. How to Build a HealthTech Startup Without a Medical Degree

🔗 https://findnstart.com/blogs/how-to-build-a-healthtech-startup-without-a-medical-degree

19. The Solitary Architect: Executive Isolation in Entrepreneurship

20. The 2026 Guide to Launching a SaaS as a Solo Developer

21. What Sustainable Growth Actually Looks Like

🔗 https://findnstart.com/blogs/what-sustainable-growth-actually-looks-like

22. The Early Warning Signs Your Startup Is in Trouble

🔗 https://findnstart.com/blogs/the-early-warning-signs-your-startup-is-in-trouble

23. How to Grow Without Burning Out

🔗 https://findnstart.com/blogs/how-to-grow-without-burning-out

24. The Truth About “Runway” Most Founders Ignore

🔗 https://findnstart.com/blogs/the-truth-about-runway-most-founders-ignore

25. Revenue Solves More Problems Than Funding

🔗 https://findnstart.com/blogs/revenue-solves-more-problems-than-funding

26. What No One Tells You About Being a Solo Founder

🔗 https://findnstart.com/blogs/what-no-one-tells-you-about-being-a-solo-founder

27. Why Smart People Quit High-Paying Jobs to Build Startups (And Why Most Regret It)

28. Why Most Startup Advice on Twitter Is Dangerous

🔗 https://findnstart.com/blogs/why-most-startup-advice-on-twitter-is-dangerous

29. Decision Fatigue: The Silent Startup Killer

🔗 https://findnstart.com/blogs/decision-fatigue-the-silent-startup-killer

30. Fear vs Logic: How Founders Actually Make Decisions

🔗 https://findnstart.com/blogs/fear-vs-logic-how-founders-actually-make-decisions

31. How Overthinking Destroys Early Momentum

🔗 https://findnstart.com/blogs/how-overthinking-destroys-early-momentum

32. Ideas Don’t Scale. Systems Do.

🔗 https://findnstart.com/blogs/ideas-dont-scale-systems-do

33. The First Hire That Actually Matters

🔗 https://findnstart.com/blogs/the-first-hire-that-actually-matters

34. How the First 100 Users Decide Your Startup’s Fate

🔗 https://findnstart.com/blogs/how-the-first-100-users-decide-your-startups-fate

35. Why Your Startup Doesn’t Need Growth — It Needs Focus

🔗 https://findnstart.com/blogs/why-your-startup-doesnt-need-growthit-needs-focus

36. Why Most Startups Die Quietly

🔗 https://findnstart.com/blogs/why-most-startups-die-quietly

37. Lessons Learned Too Late by First-Time Founders

🔗 https://findnstart.com/blogs/lessons-learned-too-late-by-first-time-founders

38. The Myth of the “Overnight Success” Startup

🔗 https://findnstart.com/blogs/the-myth-of-the-overnight-success-startup