The Future of Canada’s Startup Ecosystem in the Next Decade

June 30, 2026 by Harshit Gupta

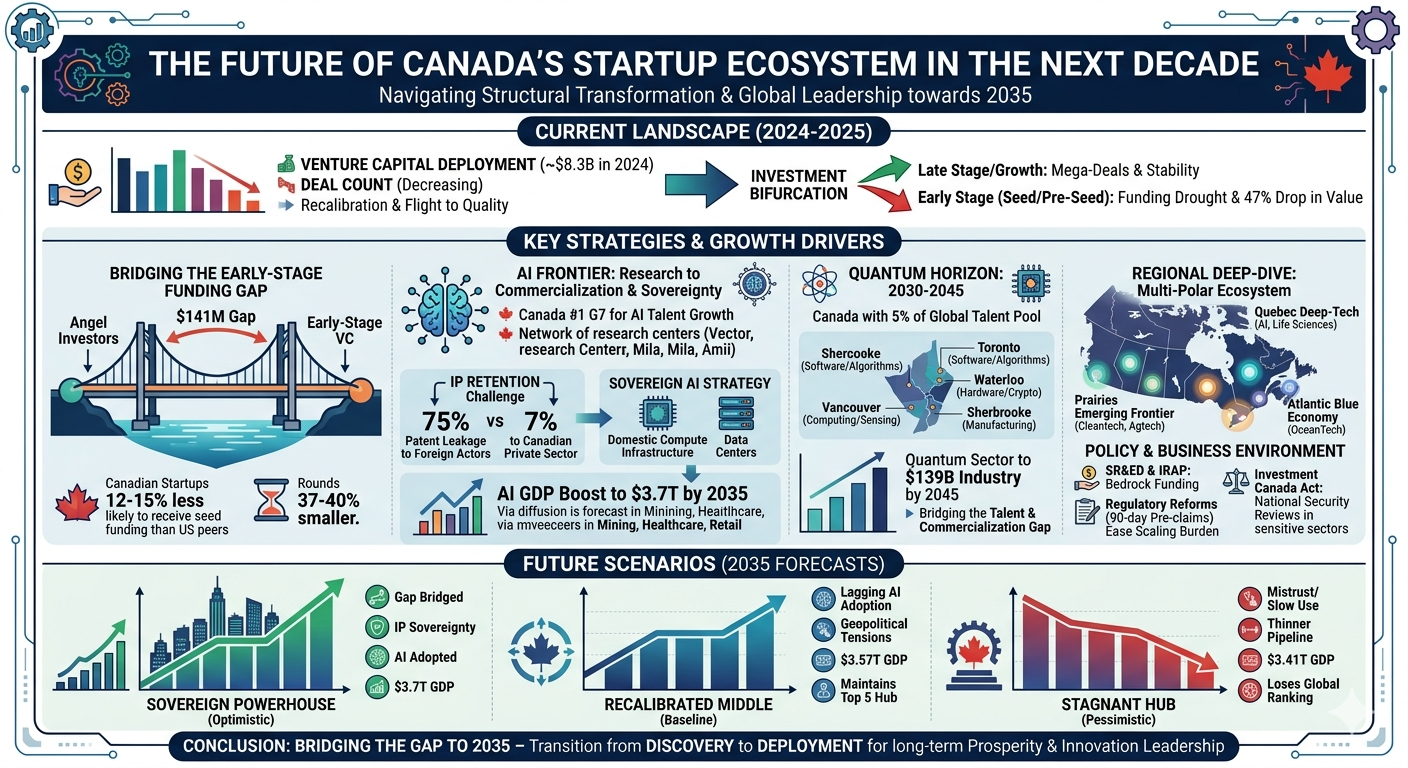

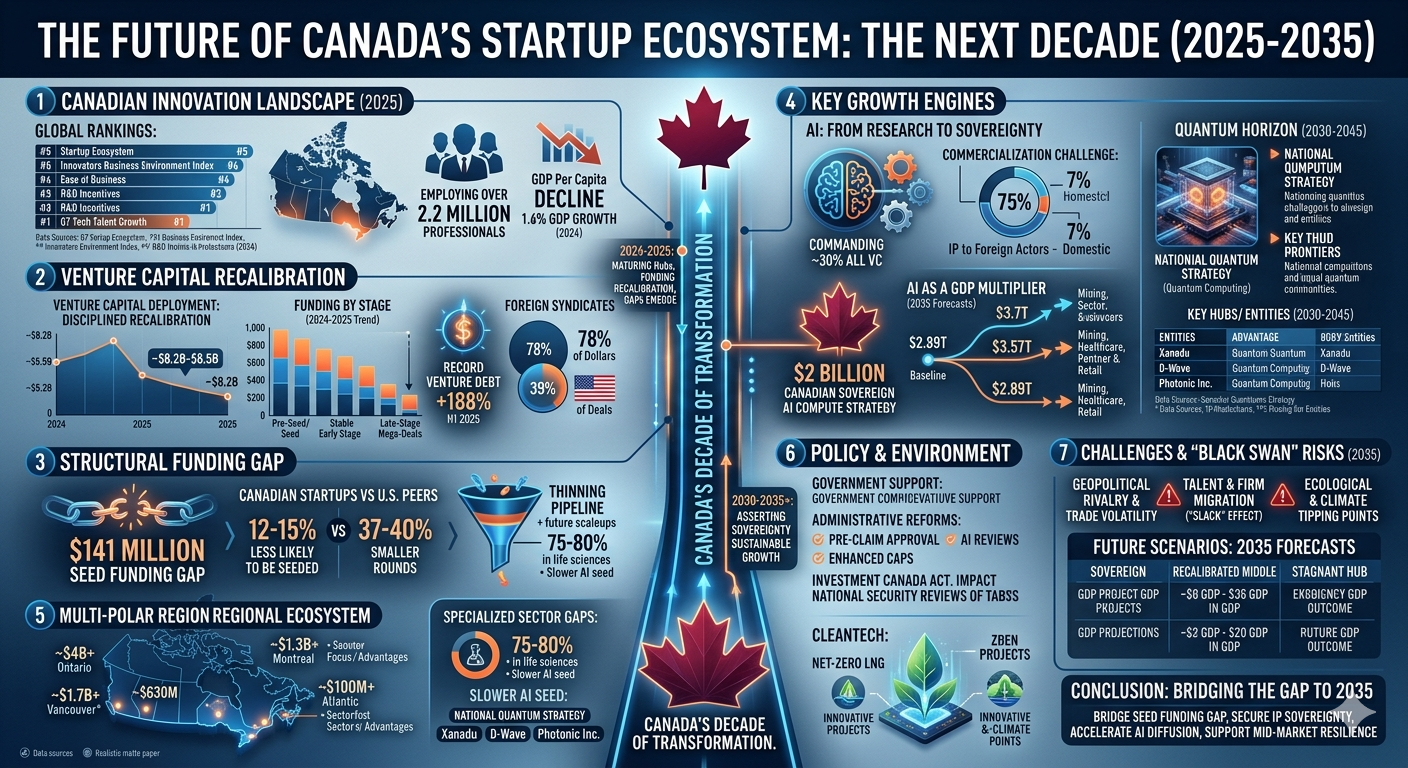

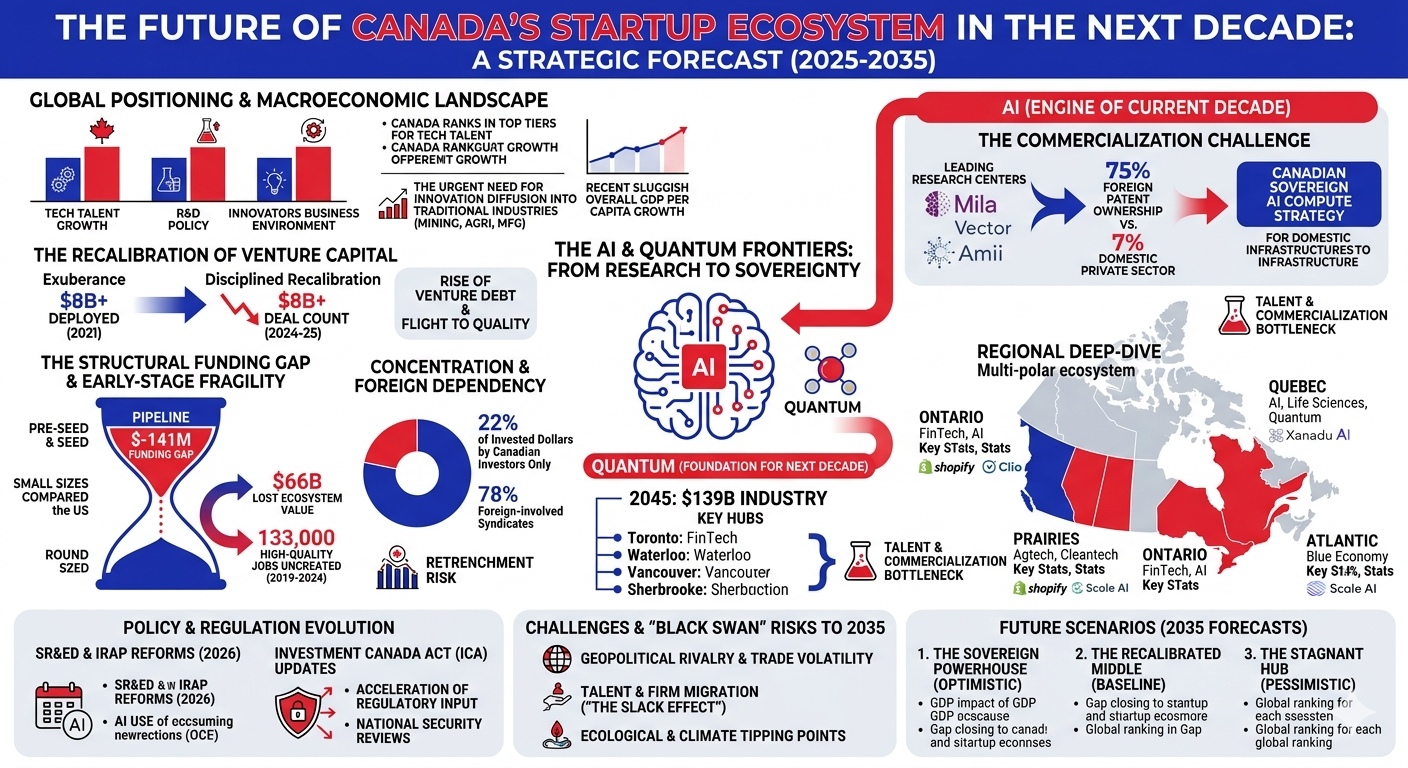

The Canadian startup ecosystem enters the mid-2020s positioned as a critical nexus of global innovation, yet it faces a decade of profound structural transformation. As of 2024 and 2025, Canada maintains a resilient global standing, consistently ranking as the fifth or sixth most attractive environment for technological entrepreneurship globally. This status is supported by a robust deployment of venture capital, which reached approximately $8.2 billion to $8.5 billion in 2024, despite a challenging macroeconomic backdrop defined by high interest rates and geopolitical instability. However, the aggregate success of the ecosystem masks a significant bifurcation between maturing scaleups and a struggling early-stage pipeline. The next ten years will be defined by Canada’s ability to bridge this "capital gap" while simultaneously asserting sovereignty over its world-leading research in artificial intelligence, quantum computing, and the blue economy.

The Macro-Economic Landscape and Global Positioning

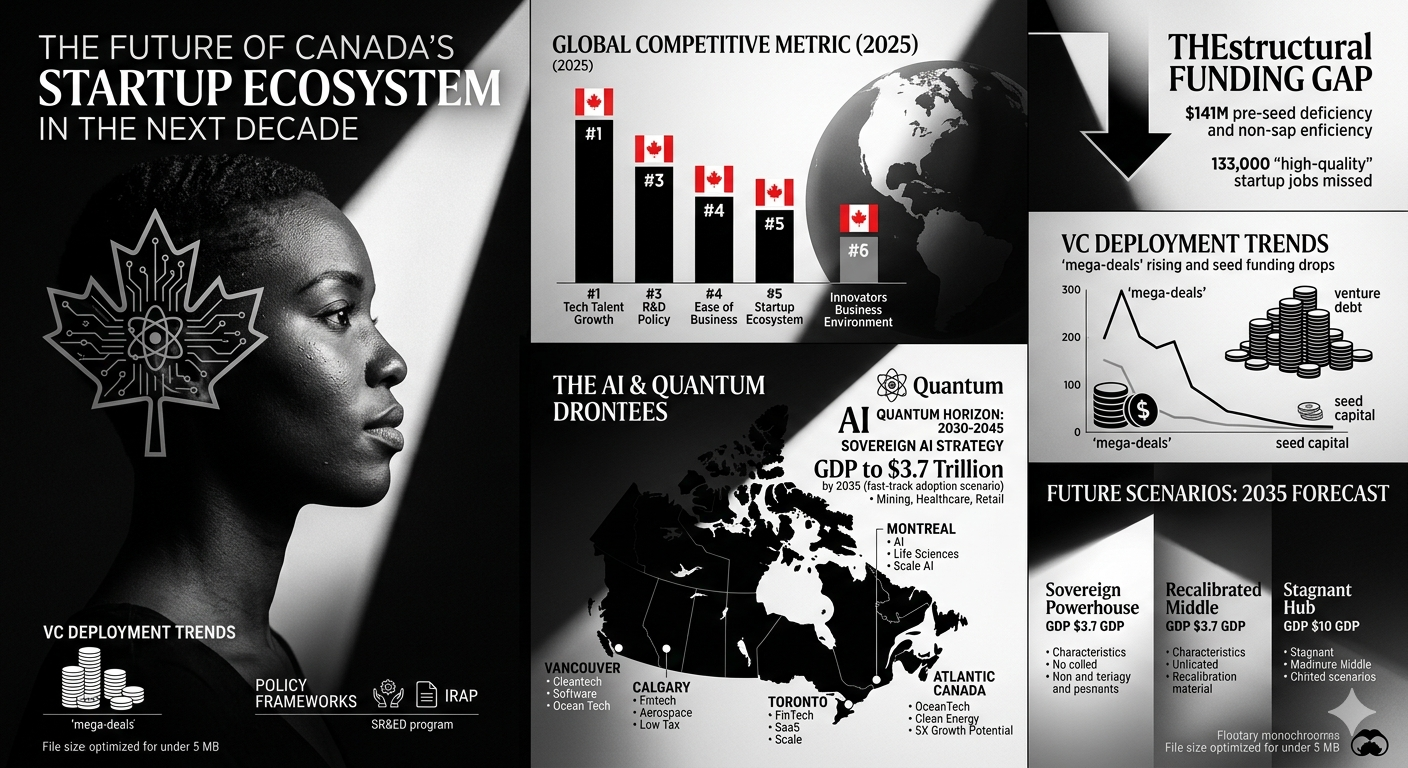

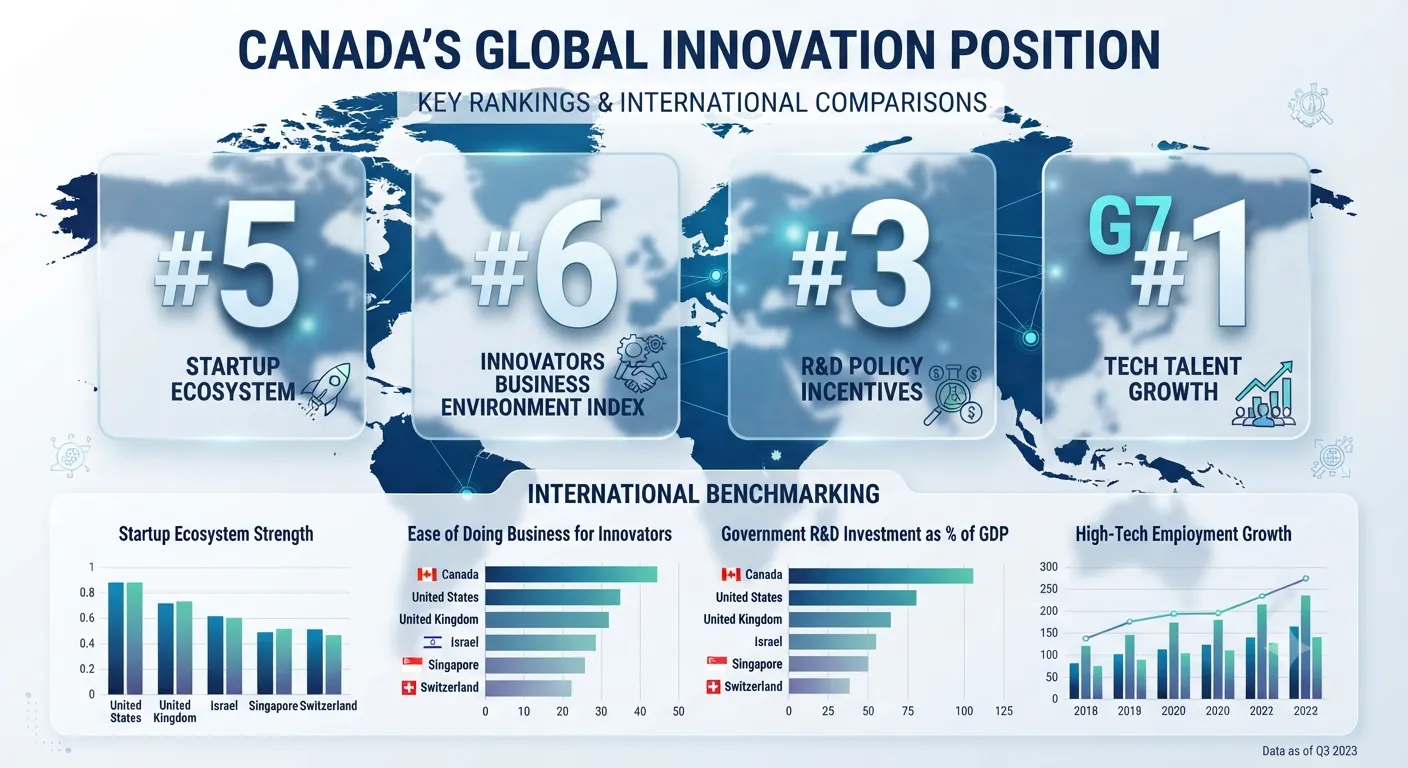

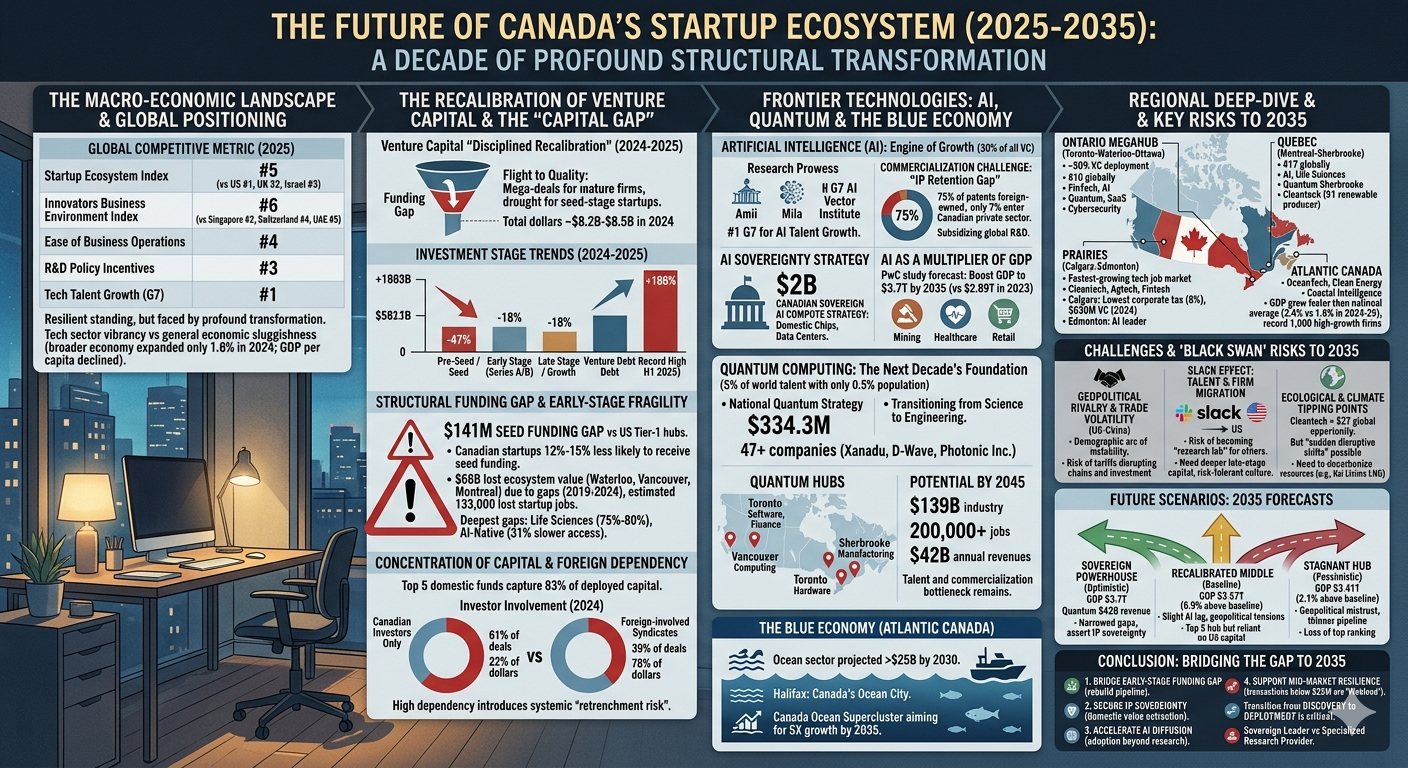

The stability of the Canadian innovation environment is a primary driver of its international competitiveness. According to the Innovators Business Environment Index (IBEI), Canada ranks 6th out of 125 countries, trailing only the United States, Singapore, the United Kingdom, Switzerland, and the United Arab Emirates. This ranking reflects a sophisticated infrastructure of "friction-reducing" policy tools, advanced digital networks, and a highly mobile workforce. Canada’s institutional strength is particularly evident in its regulatory and governance frameworks, where it ranks 4th globally, and its policy incentives, where it ranks 3rd.

Global Competitive Metric (2025) | Canadian Global Rank | Key Peer Competitors |

Startup Ecosystem Index | #5 | U.S. (#1), UK (#2), Israel (#3) |

Innovators Business Environment Index | #6 | Singapore (#2), Switzerland (#4), UAE (#5) |

Ease of Business Operations | #4 | U.S., UK, Singapore |

R&D Policy Incentives | #3 | Israel, U.S., South Korea |

Tech Talent Growth (G7) | #1 | U.S., France, Germany |

The economic contribution of the tech sector is substantial, employing over 2.2 million professionals across various high-growth verticals. Nevertheless, the broader Canadian economy expanded by only 1.6% in 2024, with GDP per capita declining for the second consecutive year. This discrepancy between tech sector vibrancy and general economic sluggishness underscores the urgent need to accelerate the diffusion of innovation from startup hubs into traditional industries such as mining, agriculture, and manufacturing.

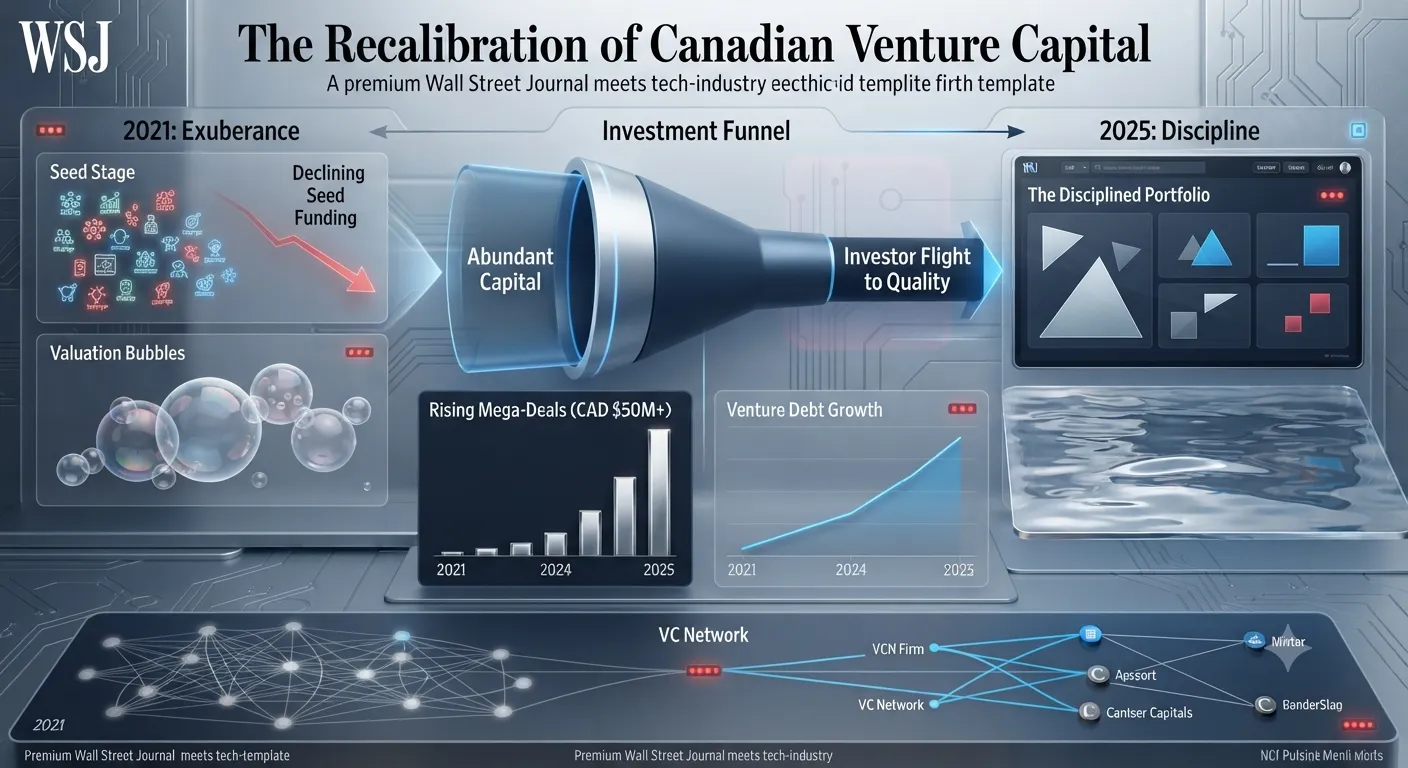

The Recalibration of Venture Capital

The Canadian venture capital market has transitioned from a period of "unprecedented exuberance" in 2021 to a "disciplined recalibration" in 2024–2025. While the total dollars invested remained healthy at over $8 billion, the deal count dropped by roughly 14% to 17%, signaling a flight to quality. Investors are increasingly prioritizing companies with established product-market fit and clear paths to profitability, leading to larger "mega-deals" for mature firms and a corresponding drought for seed-stage startups.

Investment Stage (2024-2025) | Deployment Trend | Change in Value (%) |

Pre-Seed / Seed | Downward | -47% (2024 vs 2023 peak) |

Early Stage (Series A/B) | Steady/Subdued | -18% below 5-year average |

Late Stage / Growth | Sharp Increase | Driven by mega-deals (e.g., Clio) |

Venture Debt | Record High | +188% in H1 2025 |

Data sources:

The rise of venture debt to a record $283 million in Q1 2025 highlights the current fundraising environment. Founders are increasingly utilizing non-dilutive financing to extend runways and avoid "down rounds" as equity markets tighten. This tactical shift is expected to characterize the first half of the coming decade, as the ecosystem works through a backlog of companies that raised capital at high valuations during the post-pandemic peak.

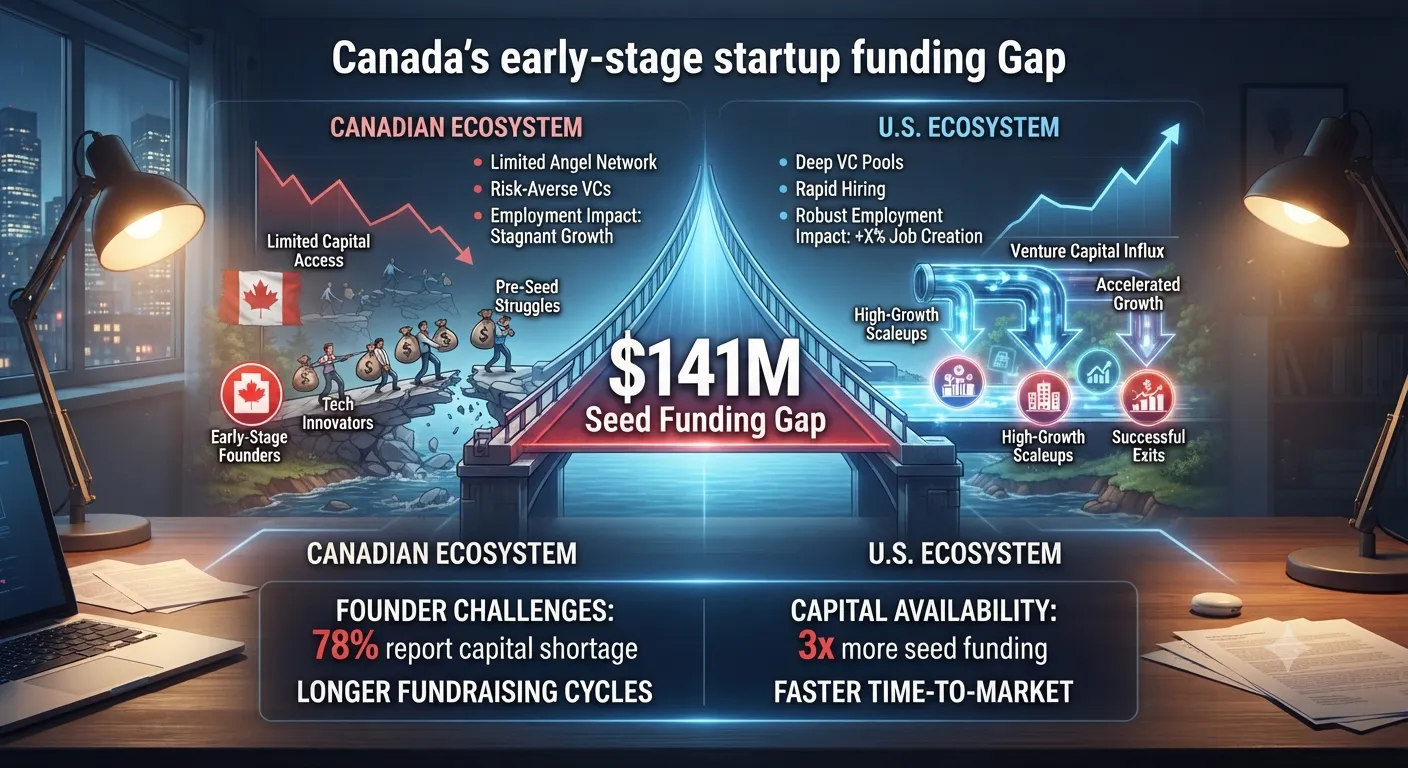

The Structural Funding Gap and Early-Stage Fragility

One of the most concerning trends identified by ecosystem analysts is the widening gap at the earliest stages of the startup pipeline. Between 2019 and 2024, Canada’s top startup hubs—Waterloo, Vancouver, and Montreal—collectively lost $66 billion in ecosystem value relative to global peers due to structural funding gaps. This value loss represents not just capital, but an estimated 133,000 "high-quality" startup jobs that were never created.

The Pre-Seed and Seed Deficiency

Canada faces a documented $141 million funding gap at the pre-seed and seed stages. Canadian startups are 12% to 15% less likely to receive seed funding compared to firms in U.S. Tier-1 ecosystems like New York, Boston, or Los Angeles. Furthermore, when Canadian firms do secure seed capital, the rounds are 37% to 40% smaller than those of their American counterparts. This "thinning" of the pipeline has long-term consequences: fewer companies forming today means a smaller pool of high-potential scaleups for Series C and D investors in 2030.

The gap is particularly severe in specialized sectors. In life sciences, the seed-stage funding gap for Canadian startups compared to U.S. or Swedish firms is 75% to 80%, representing a fourfold widening of the deficit over the last decade. For AI-native startups, the gap is not just in capital but in velocity; Canadian AI firms access seed funding 31% slower than U.S. peers.

Concentration of Capital and Foreign Dependency

A second structural vulnerability is the concentration of capital among a few major players. In 2024, the top five domestic funds captured 83% of all capital deployed, significantly increasing the competition for attention from a smaller number of decision-makers. This concentration is mirrored by a heavy reliance on foreign investment. Syndicates involving foreign investors, primarily from the United States, accounted for 78% of all dollars invested in the Canadian tech sector.

Investor Involvement (2024) | % of Deals (Volume) | % of Invested Dollars |

Canadian Investors Only | 61% | 22% |

Foreign-involved Syndicates | 39% | 78% |

U.S. Investor Participation | 32% | ~54% (H1 2025) |

Data sources:

While foreign participation validates the quality of Canadian innovation, it introduces systemic "retrenchment risk". Geopolitical tensions, new tariff environments, and domestic policy shifts in the U.S. could lead to a sudden withdrawal of late-stage capital, leaving Canadian scaleups without the resources to compete globally.

The AI Frontier: From Research to Sovereignty

Artificial Intelligence (AI) has emerged as the undisputed engine of growth for the Canadian ecosystem, commanding approximately 30% of all venture capital investment. Canada ranks first in the G7 for AI talent growth and is home to over 670 AI startups. This leadership is anchored by world-renowned research centers: the Alberta Machine Intelligence Institute (Amii), Mila in Montréal, and the Vector Institute in Toronto.

The Commercialization Challenge

Despite its research prowess, Canada struggles with "intellectual property (IP) retention." A staggering 75% of patents produced at leading institutes like Vector and Mila end up owned by foreign private actors, with only 7% entering the Canadian private sector. This suggests that Canada is effectively subsidizing the R&D of global tech giants rather than building domestic champions.

To counter this, the federal government has launched the $2 billion Canadian Sovereign AI Compute Strategy. This initiative aims to build the domestic infrastructure—including high-performance chips and data centers—needed to power the AI economy and ensure that Canadian firms can train and deploy models without relying exclusively on foreign-controlled clouds.

AI as a Multiplier of GDP

The potential economic impact of AI adoption is immense. A PwC study predicts that fast-tracking AI integration across the Canadian economy could boost GDP to $3.7 trillion by 2035, compared to $2.89 trillion in 2023. Key sectors expected to benefit include:

Mining and Natural Resources: Utilizing AI and quantum computing to accelerate environmental assessments and resource permitting.

Healthcare: Deploying AI-enhanced medical imaging for disease diagnosis and wearable sensors for chronic condition management.

Retail and Media: Leveraging generative AI for hyper-personalized consumer journeys and automated content creation.

The "middle scenario," where AI adoption lags and global decarbonization goals fall short, suggests a smaller but still significant GDP boost to $3.57 trillion by 2035. The realization of these gains depends on narrowing the AI adoption gap relative to the United States and building public trust in cybersecurity and AI ethics.

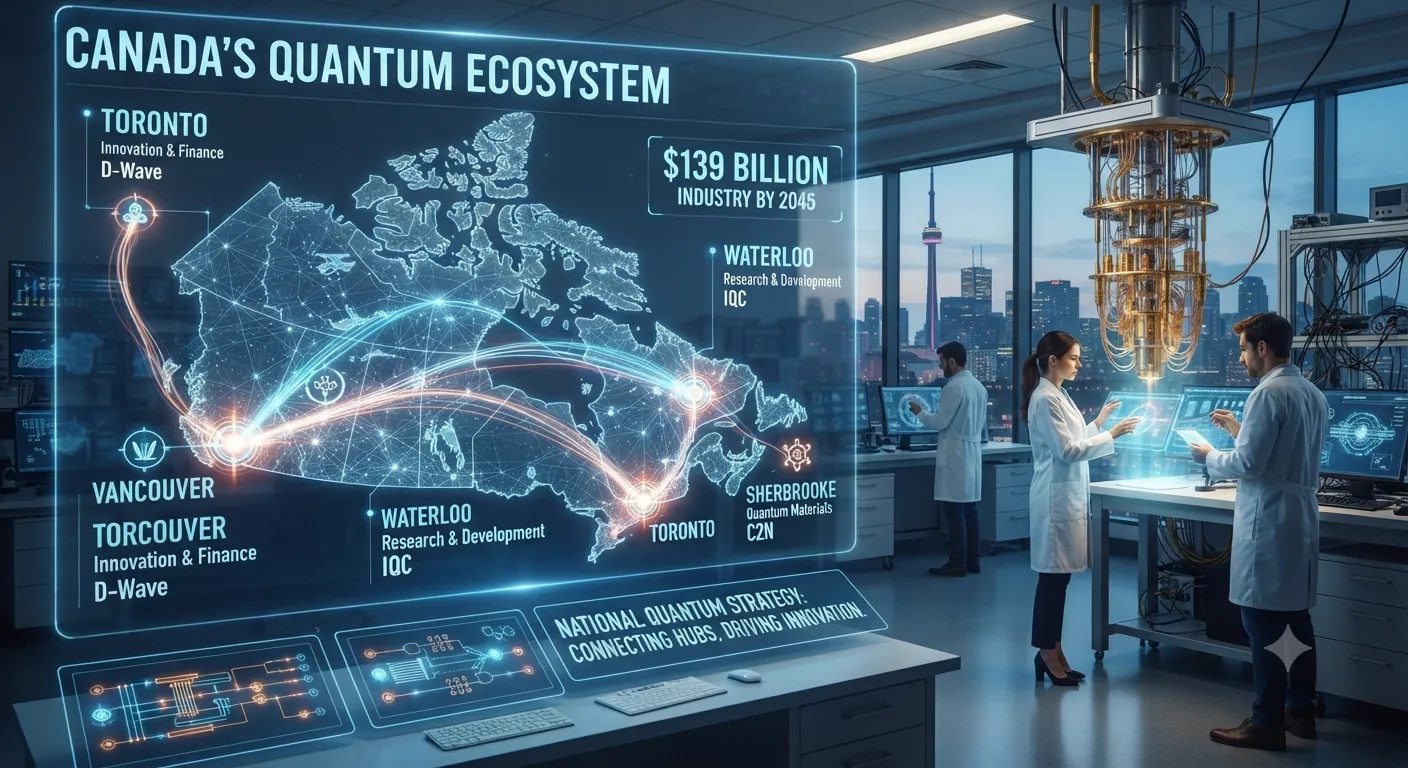

The Quantum Horizon: 2030–2045

If AI is the engine of the current decade, Quantum Computing is the foundation for the next. Canada is a global leader in quantum technologies, holding 5% of the world’s quantum talent pool despite representing only 0.5% of the population. The country’s quantum sector is projected to become a $139 billion industry by 2045, supporting over 200,000 jobs and generating $42 billion in annual revenues.

National Quantum Strategy and Research Excellence

The Canadian government has committed $334.3 million through the National Quantum Strategy to strengthen the foundations of this nascent industry. Unlike AI, which has largely moved into the commercial application phase, quantum technology is transitioning from a "20-year science project" to a "5-year engineering project". Canada's 47+ domestic quantum companies, such as Xanadu, D-Wave, and Photonic Inc., are closely linked to universities and represent a "vibrant commercial ecosystem" that punches well above its weight.

Quantum Hub | Primary Research/Commercial Focus | Notable Entities |

Toronto | Software, Algorithms, Financial Services | Xanadu, 1QBit |

Waterloo | Hardware, Cryptography, Materials | Institute for Quantum Computing |

Vancouver | Computing, Sensing, Ocean Tech | D-Wave, Photonic Inc. |

Sherbrooke | Quantum Manufacturing, Hardware | DistriQ, PASQAL |

The Talent and Commercialization Bottleneck

A significant threat to Canada’s quantum leadership is the shortage of talent. The global quantum talent pool is small—estimated at 4,000 professionals in Canada—and competition for this personnel is fierce. Furthermore, there is a "commercialization gap"; startups must transition from being research labs to deep-tech businesses focused on value creation. Programs like Lab2Market, which connects researchers with mentors and investors, are critical to bridging this divide. Since 2020, Lab2Market has supported 172 startups and raised $47.9 million in investment.

Regional Deep-Dive: A Multi-Polar Ecosystem

The Canadian startup ecosystem is geographically distributed, with distinct regional hubs specializing in specific high-growth verticals. The "distributed network" model has proven to be a strength, allowing cities to build unique competitive advantages based on local expertise and resource abundance.

Ontario: The Megahub (Toronto-Waterloo-Ottawa)

Ontario remains the dominant force in Canadian tech, accounting for roughly 50% of all venture capital deployment. The Toronto-Waterloo corridor ranks #10 globally and is home to over 10 unicorns, including Shopify and Wealthsimple.

Toronto: North America’s third-largest FinTech hub (after NY and SF), attracting 24% of all Canadian startup funding. Its strength lies in payments, lending, and blockchain infrastructure.

Waterloo: A top-tier university ecosystem and a global leader in quantum research and enterprise software.

Ottawa: Tied with the San Francisco Bay Area for the largest concentration of tech talent in North America. It is a powerhouse in SaaS, telecommunications, and cybersecurity.

Quebec: The AI and Deep-Tech Corridor (Montreal-Sherbrooke)

Montreal is ranked #17 globally and is a primary driver of the national AI strategy through the Scale AI supercluster, which received $96 million in project funding in 2024.

Life Sciences: Montreal aims to be a top 5 North American hub by 2027, supported by major projects like Biotech City and the Moderna vaccine facility.

Quantum Sherbrooke: The "DistriQ" zone in Sherbrooke is becoming a center for quantum hardware, featuring a North American flagship factory for PASQAL.

Cleantech: Quebec is the #1 renewable energy producer in North America, providing a low-cost, low-carbon foundation for AI data centers and manufacturing.

The Prairies: The Emerging Frontier (Calgary-Edmonton)

The Prairie provinces are experiencing a tech boom, driven by lower operating costs and a strategic shift from oil and gas to cleantech and agtech.

Calgary: Ranked as the fastest-growing tech job market in North America with 78% growth over five years. It has the lowest corporate tax rate in Canada (8%) and attracted $630 million in VC funding in 2024.

Edmonton: A global leader in reinforcement learning and AI adoption, supported by Amii and the MIT REAP program. It raised over $170 million in VC funding in 2024.

Atlantic Canada: The Blue Economy (Halifax-St. John's)

Atlantic Canada’s tech ecosystem is defined by its "Blue Economy." The ocean sector is expected to grow to over $25 billion by 2030.

Halifax: Known as "Canada’s Ocean City," it hosts hundreds of ocean-tech companies and one-fifth of all R&D in the city is tied to marine industries. The Canada Ocean Supercluster aims for a 5X growth potential by 2035.

Regional Momentum: Atlantic Canada’s GDP grew faster than the national average in 2024-25 (2.4% vs 1.6%), with a record 1,000 high-growth firms.

Regional Hub | VC Funding (2024) | Key Growth Sectors | Strategic Advantage |

Toronto-Waterloo | ~$4B+ | FinTech, AI, Enterprise SaaS | Scale, Talent Density |

Montreal | $1.3B+ | AI, Life Sciences, Aerospace | R&D Superclusters |

Vancouver | $1.7B+* | Cleantech, Life Sciences, Software | Asian Gateway, B.C. Hydro |

Calgary | $630M | Fintech, Cleantech, Aerospace | Low Tax, High Liveability |

Atlantic Canada | ~$100M+ | OceanTech, Clean Energy | Coastal Intelligence |

Policy, Regulation, and the Business Environment

Canada’s success in the next decade will depend on evolving its policy framework to support scaling, rather than just starting. The current Innovators Business Environment Index confirms that while it is easy to "launch" a company in Canada, "scaling" remains difficult.

SR&ED and IRAP: The Funding Bedrock

Government programs remain the "integral pillar" of the startup funding stack. The SR&ED tax credit returns up to 35% of R&D expenses, effectively reducing a startup’s burn rate by a third. Meanwhile, the Industrial Research Assistance Program (IRAP) provides non-dilutive funding ranging from $10,000 to $10 million for technology development.

Key administrative reforms scheduled for 2026 aim to reduce the "regulatory burden" for founders, who currently lose an average of 256 hours annually to red tape. These reforms include:

Pre-claim Approval: Reducing processing times from 180 days to 90 days.

AI Integration: Utilizing AI-powered reviews to speed up assessments and reduce unnecessary audits.

Enhanced Caps: Reassessing eligibility under new $6 million caps for domestic R&D expenses.

The Investment Canada Act (ICA) and National Security

A growing trend in the M&A landscape is the "acceleration of regulatory input". Recent updates to the Investment Canada Act have made national security reviews a central component of transaction strategies for foreign buyers. The long-standing 35% "safe harbor" threshold for mergers is being phased out in favor of more involved reviews, particularly in sensitive sectors like AI, quantum, and critical minerals. This reflects a global shift toward protectionism and the "securitization of technology".

Challenges and "Black Swan" Risks to 2035

The 2030–2035 technology horizon scan identifies several systemic challenges that could disrupt Canada’s trajectory.

Geopolitical Rivalry and Trade Volatility

The "superpower rivalry" between the U.S. and China creates a "demographic arc of instability". For Canada, this rivalry threatens traditional trade relationships and investment flows. Increased tariffs—a risk highlighted in 2024-2025 reports—could disrupt global supply chains and dampen investor confidence in Canadian tech, which is heavily reliant on cross-border integration.

The "Slack" Effect: Talent and Firm Migration

A recurring challenge is the "migration of performers" to the United States. Examples like Slack—originally a Vancouver startup that moved to the U.S. for its IPO and eventual acquisition by Salesforce—illustrate the risk of Canada becoming a "research lab" that does not reap the full economic benefits of its output. Retaining top-tier entrepreneurs requires more than favorable R&D conditions; it requires a deep domestic late-stage capital pool and a more risk-tolerant corporate culture.

Ecological and Climate Tipping Points

Climate change is identified as a "systemic" issue that integrates across all innovation disciplines. While cleantech represents a $2 trillion global opportunity, "ecological tipping points" could lead to sudden disruptive shifts in resource availability and infrastructure resilience. Canada’s economy, heavily tied to natural resources, must discover innovative ways to decarbonize production while remaining competitive. Projects like the Ksi Lisims LNG, aiming for net-zero by 2030, represent the scale of technological adaptation required.

Future Scenarios: 2035 Forecasts

Based on current trends, the Canadian startup ecosystem is expected to follow one of three trajectories by 2035:

The Sovereign Powerhouse (Optimistic): Canada narrows the AI adoption gap, bridges the $141M seed funding gap, and asserts IP sovereignty. GDP reaches $3.7 trillion, and the quantum sector achieves its $42B revenue target.

The Recalibrated Middle (Baseline): AI adoption lags slightly, and geopolitical tensions hinder collaboration. GDP growth is a respectable 6.9% above baseline ($3.57 trillion). Canada remains a top 5 hub but continues to rely on U.S. capital for mega-deals.

The Stagnant Hub (Pessimistic): Geopolitical mistrust slows technology use, and the seed-stage funding drought leads to a "thinner" pipeline of scaleups. Growth is limited to 2.1% above baseline ($3.41 trillion), and Canada loses its top-tier global ranking to rising AI hubs in Asia and Europe.

Conclusion: Bridging the Gap to 2035

The next decade represents a period of "extraordinary gifts and capabilities" but also "significant challenges" for Canada. To secure its place as a North American innovation powerhouse, the ecosystem must transition from a focus on "discovery" to a focus on "deployment". This requires:

Bridging the Early-Stage Funding Gap: Incentivizing domestic angel and seed-stage investment to rebuild the pipeline of high-potential firms.

Securing IP Sovereignty: Implementing policies that prioritize domestic IP retention and value extraction, particularly in publicly funded research institutes.

Accelerating AI Diffusion: Moving beyond the "AI research" phase into "AI adoption" across traditional sectors like mining and healthcare to drive national productivity.

Supporting Mid-Market Resilience: Recognizing that while mega-deals capture headlines, 80% of transactions occur below $25 million; the mid-market remains the "lifeblood" of the Canadian economy.

By leveraging its world-class workforce, low-carbon energy profile, and institutional stability, Canada is well-positioned to navigate the global transition toward a data-driven, quantum-enabled, and climate-resilient future. The success of this transition will determine whether Canada enters 2035 as a sovereign leader or a specialized research provider to the global economy.

Want to calculate the equity for your cofounder?

Nail your cap table before you sign. Whether you're splitting equity with a co-founder or planning your next funding round, our Equity Calculator gives you precision in seconds

Equity calculator →