Startups Navigating Sanctions and Trade Barriers

June 29, 2026 by Harshit Gupta

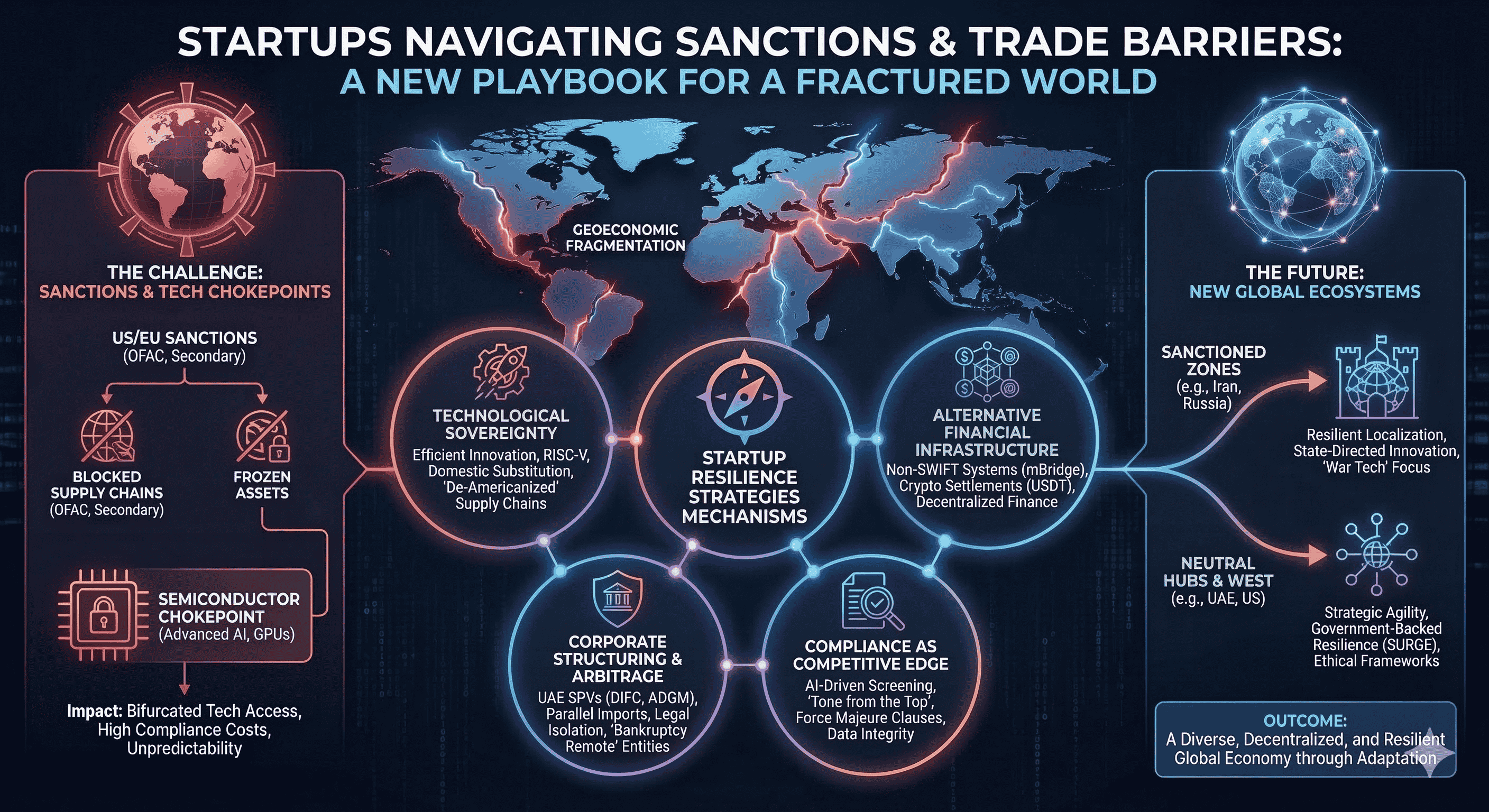

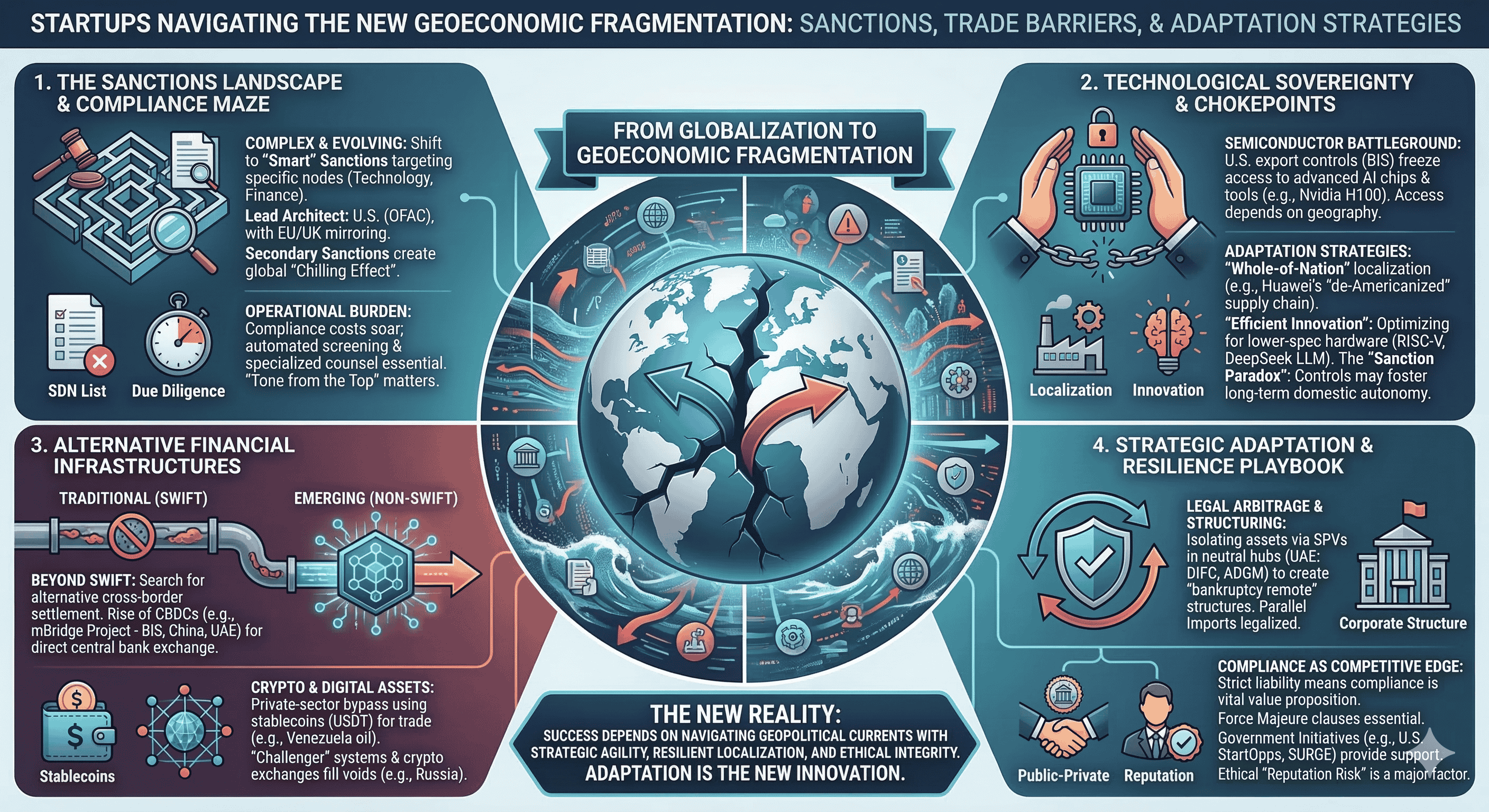

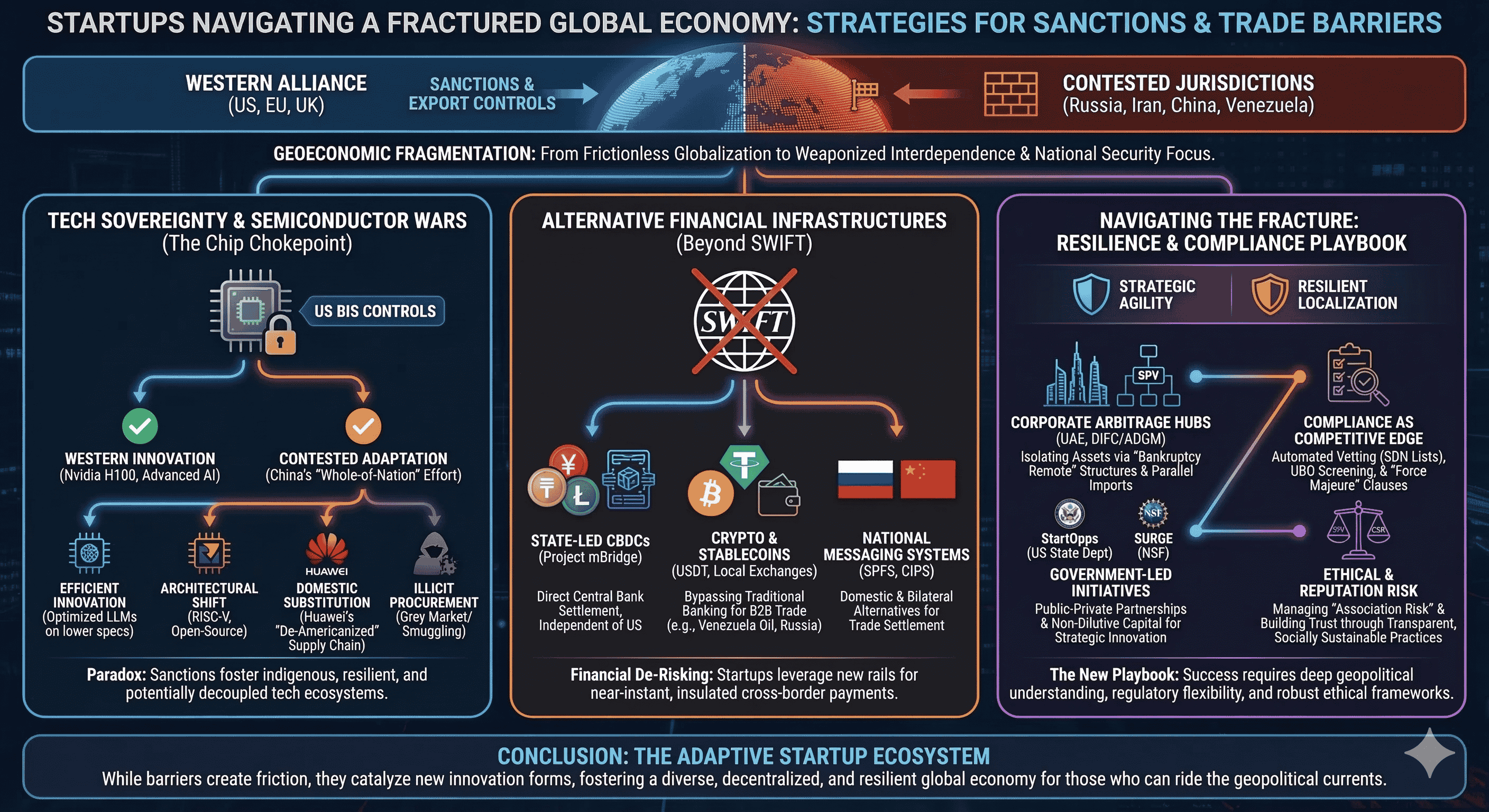

The contemporary global economic order is currently undergoing its most significant structural realignment since the end of the Cold War. The era of frictionless hyper-globalization has been superseded by a paradigm of geoeconomic fragmentation, where trade policy, financial connectivity, and technological standards are increasingly wielded as instruments of national security. For the global startup ecosystem, particularly those ventures operating within or adjacent to contested jurisdictions, this shift has transformed the regulatory landscape from a manageable administrative hurdle into an existential strategic challenge. Startups in jurisdictions such as Russia, Iran, China, and Venezuela find themselves at the epicenter of this transformation, forced to pioneer novel survival strategies that range from localized technological substitution to the adoption of decentralized financial architectures.

The Architecture of Economic Coercion: Mapping the Global Sanctions Landscape

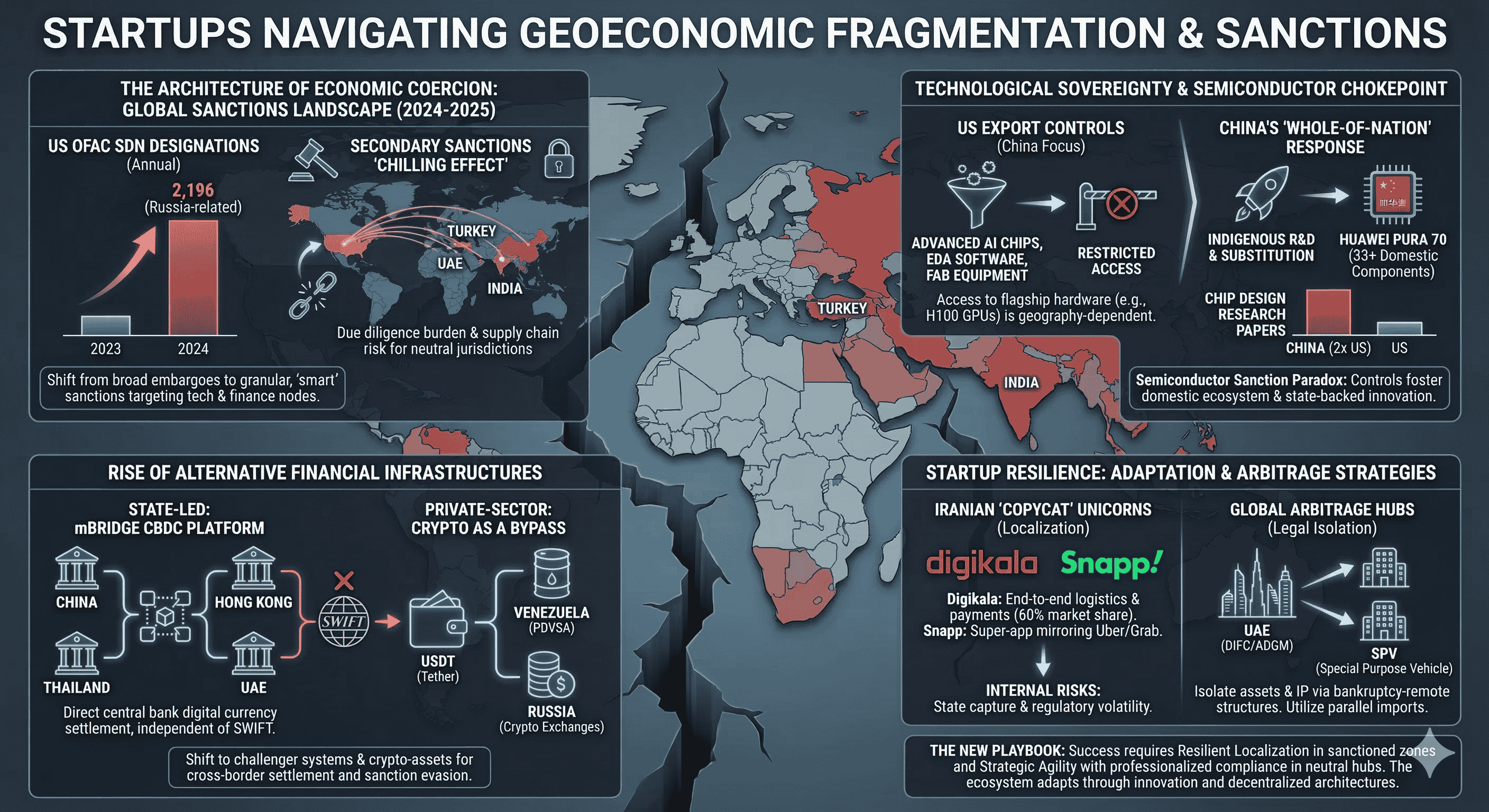

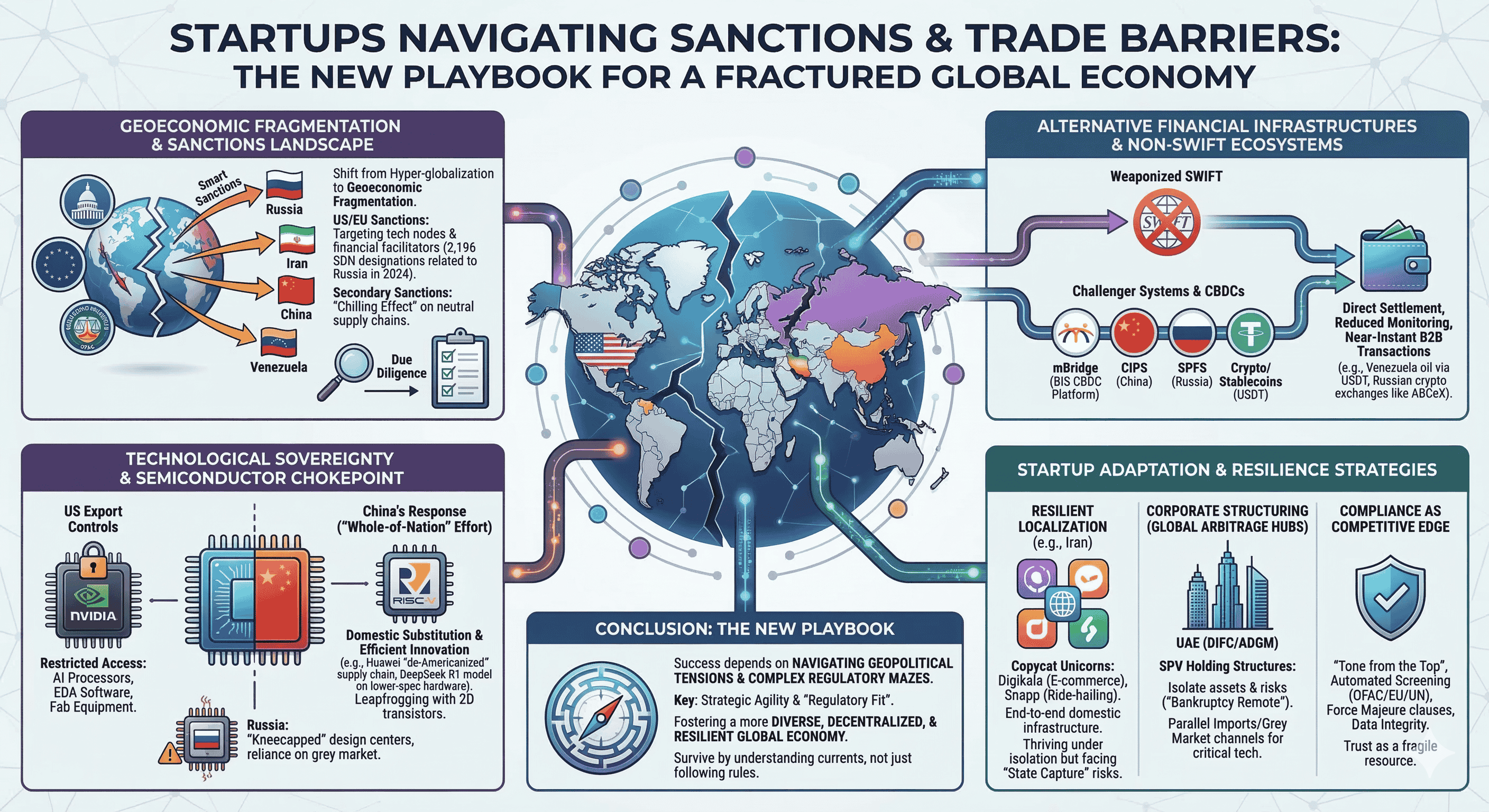

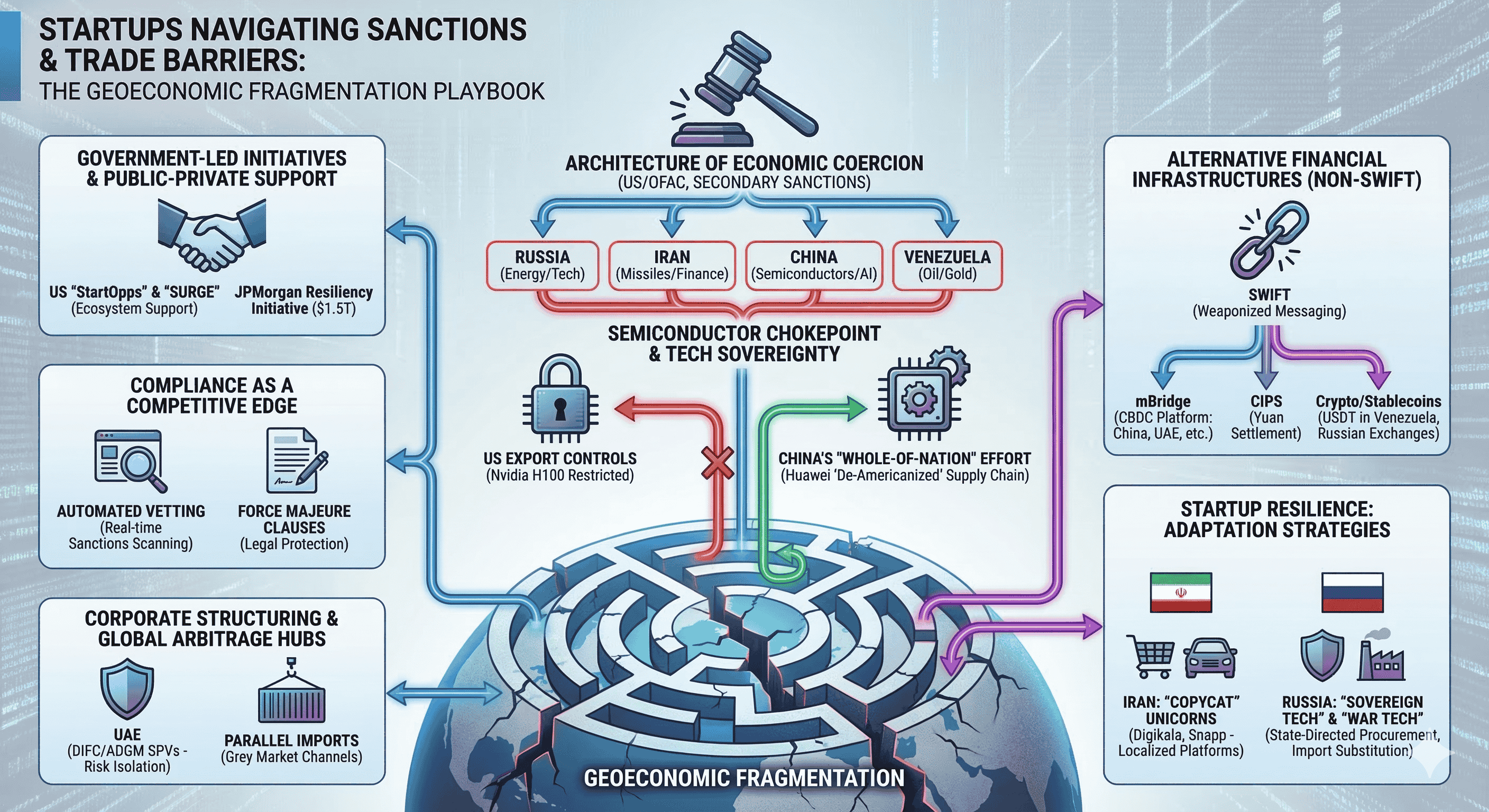

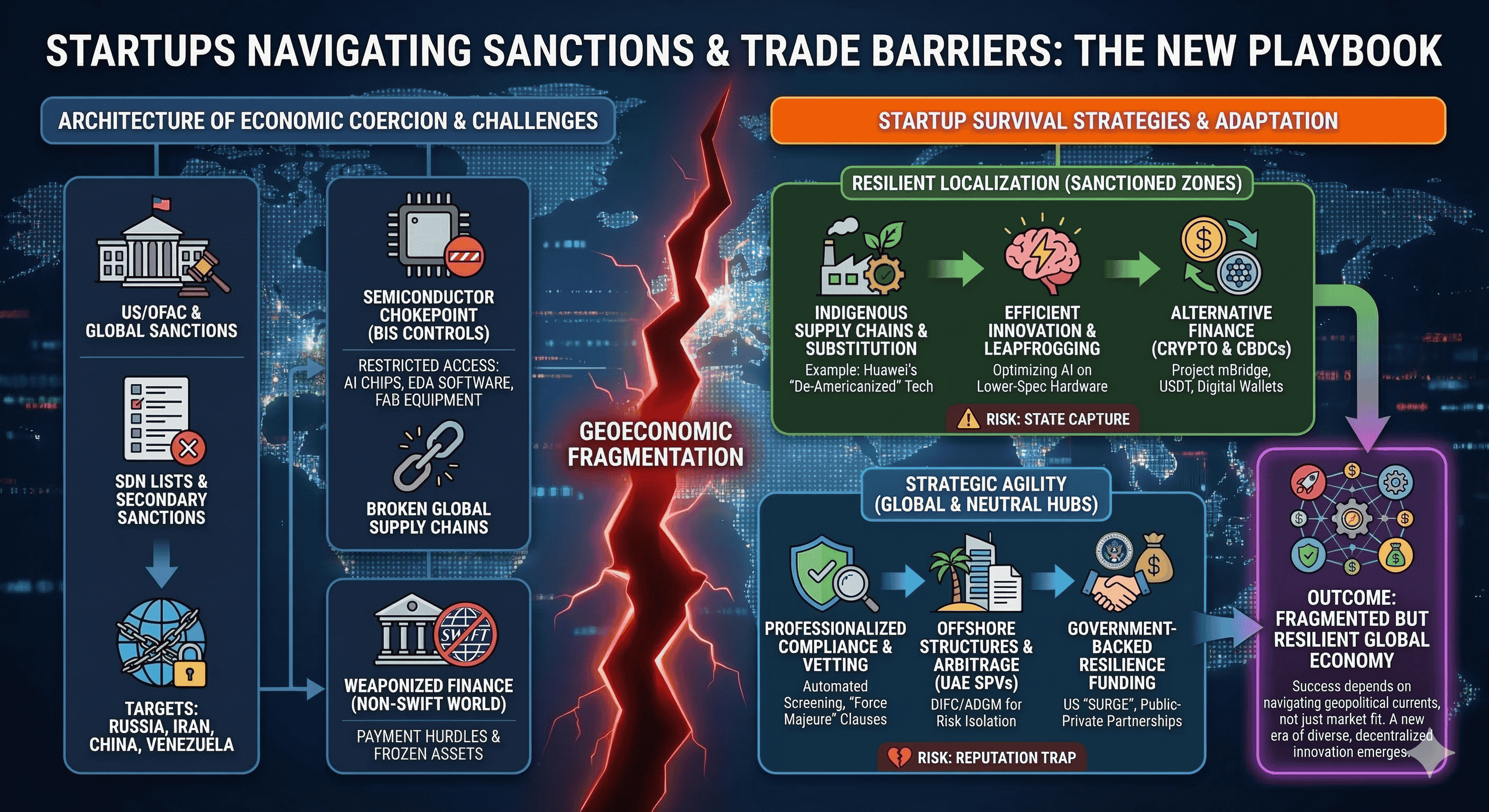

The global sanctions landscape of 2024 and 2025 is characterized by an unprecedented level of complexity and a rapid pace of evolution. The United States, primarily through the Office of Foreign Assets Control (OFAC), continues to serve as the lead architect of these restrictive measures, utilizing the Specially Designated Nationals (SDN) list to target individuals, entities, and entire sectors of the Russian, Iranian, and Venezuelan economies. However, the current era is marked by a shift from broad country-wide embargoes toward more granular, "smart" sanctions that target specific technological nodes and financial facilitators. In 2024, the United States executed 2,196 SDN designations related to Russia alone, signaling a sustained commitment to degrading Russia’s military-industrial complex and harmful foreign activities.

This regulatory environment is further complicated by the emergence of secondary sanctions, which threaten to cut off third-country entities from the U.S. financial system if they engage in "significant transactions" with sanctioned targets. This has created a "chilling effect" throughout global supply chains, as startups in neutral jurisdictions like Turkey, the United Arab Emirates, and India must now perform exhaustive due diligence to ensure that their components or software do not inadvertently find their way into restricted markets. The divergence between major sanctions authorities is also increasing. While the European Union and the United Kingdom have largely mirrored U.S. policy regarding Russia and Iran, subtle disagreements regarding the utility of oil price caps and the role of international institutions suggest a fracturing of the unified G7 front.

Region/Program | Focus Areas (2024-2025) | Notable Enforcement Trends |

Russia (E.O. 14024) | Energy, Finance, Technology, Mining | Designation of top oil producers Rosneft and Lukoil; focus on LNG and transshipment hubs |

Iran (Counter-Terrorism) | Ballistic Missiles, UAVs, IRGC Finance | Targeting of "shadow fleet" vessels; shift to ballistic missile supply chains |

China (Export Controls) | Advanced Semiconductors, AI, Quantum | Sweeping restrictions on GPU exports and fabrication equipment; focus on "entity list" expansions |

Venezuela (Energy/Mining) | Oil and Gas, Gold, Digital Assets | Partial relaxation via general licenses for energy, but with strict prohibitions on China/Russia links |

Global Themes | Cyber-attacks, Human Rights, Narcotics | Increasing focus on cryptocurrency mixers and ransomware facilitators |

The implications for startups are profound. Unlike multinational corporations with massive legal departments, early-stage ventures often lack the resources to monitor daily updates to the consolidated sanctions lists of the U.S., EU, and UN. Consequently, compliance has become a primary driver of operational costs, as startups must invest in automated screening tools and specialized legal counsel to navigate the shifting boundaries of what is legally permissible. Furthermore, the transition toward "deal-oriented" trade policy—exemplified by the use of tariffs as punitive instruments—adds a layer of unpredictability that undermines long-term venture planning.

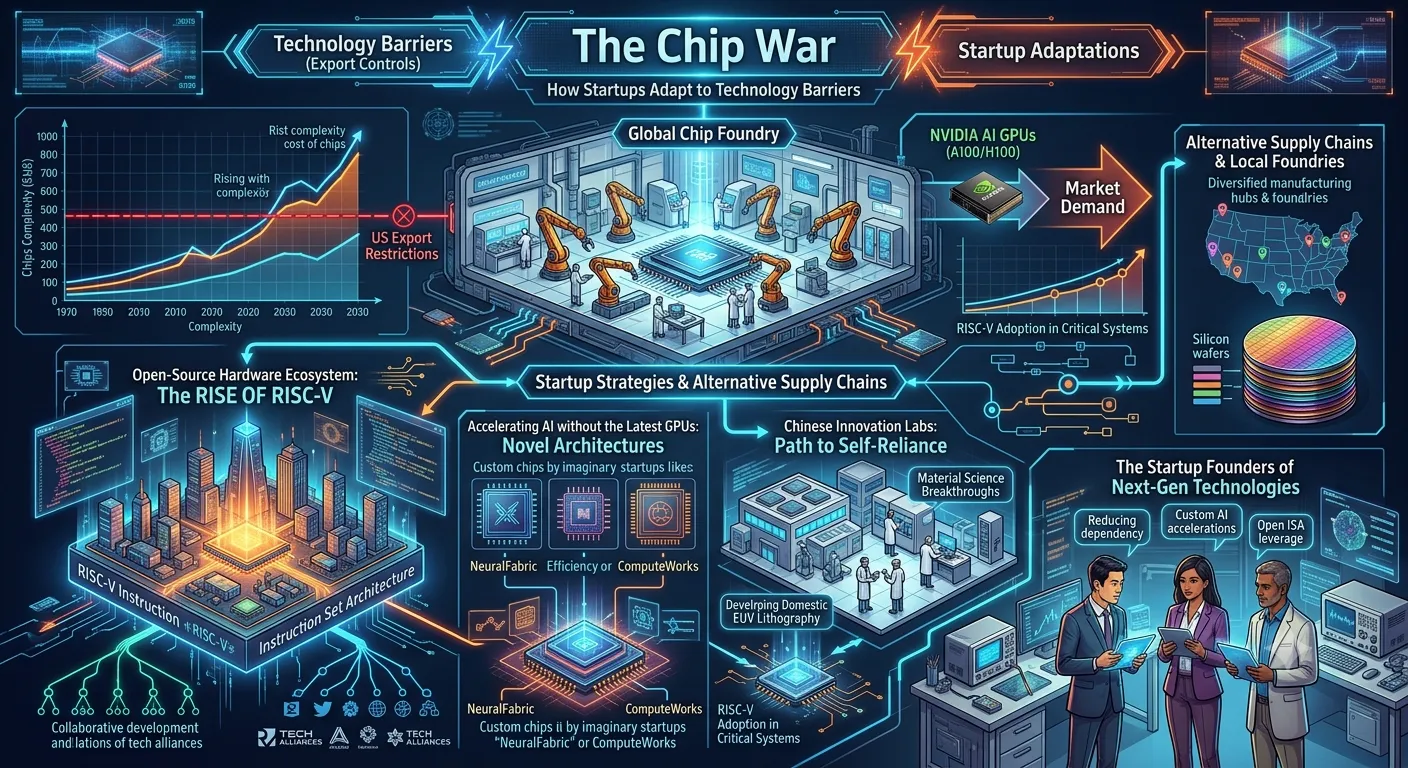

Technological Sovereignty and the Semiconductor Chokepoint

The most intense theater of the modern trade war is the semiconductor industry. In late 2022 and throughout 2023, the U.S. Bureau of Industry and Security (BIS) introduced sweeping export controls designed to freeze China’s ability to develop advanced artificial intelligence and high-performance computing capabilities. These restrictions targeted four critical bottlenecks: advanced AI processors, semiconductor design software (EDA), fabrication capabilities, and access to sophisticated manufacturing equipment. For startups, this has created a bifurcated technological world where access to flagship hardware, such as Nvidia’s H100 GPUs, is no longer a matter of capital, but of geography.

In response, Chinese startups and state-backed entities have embarked on an aggressive "whole-of-nation" effort toward technological self-sufficiency. This strategy involves not just domestic substitution of existing components, but a fundamental rethinking of technological architectures. Firms like Huawei have pioneered "de-Americanized" supply chains; by 2024, the Huawei Pura 70 series smartphone reportedly contained 33 Chinese-sourced components, with only a small fraction of parts remaining subject to foreign export controls. This demonstrates a massive reallocation of resources toward indigenous research and development, with China now producing twice as many research papers on chip design as the United States.

Adaptation Strategy | Mechanism | Key Case Study / Outcome |

Efficient Innovation | Optimizing LLMs for lower-spec hardware | DeepSeek R1 model matches U.S. capabilities with fewer resources |

Architectural Shift | Transition to open-source instruction sets | Alibaba’s adoption of RISC-V to bypass Intel/Arm dependencies |

Physical Buffering | Massive stockpiling prior to restrictions | Chinese firms created multi-year buffers of advanced chips |

Leapfrogging | Exploring 2D and carbon nanotube transistors | Peking University developments in 40% faster 2D transistors |

Illicit Procurement | Shell companies and third-country routing | Smuggling of Nvidia GPUs through Malaysia using front companies |

While the U.S. measures have certainly disrupted Chinese enterprises in the short term, analysts suggest a potential "Semiconductor Sanction Paradox." By cutting off access to global markets, these controls have inadvertently removed the competitive pressure of superior foreign products, giving domestic Chinese startups the market share and government subsidies needed to innovate rapidly. Over the long term, this could foster a more autonomous and resilient semiconductor industry in China that is entirely decoupled from Western influence, potentially destabilizing the global tech ecosystem that previously relied on U.S. leadership.

In Russia, the situation is more dire. The domestic processor industry, led by Baikal Electronics and MCST (Elbrus), was historically dependent on Taiwan’s TSMC for manufacturing. Following the invasion of Ukraine and Taiwan's subsequent imposition of export controls, Russian design centers were effectively "kneecapped," losing access to any node below 32-bit/25MHz technology. Although some "shadow" batches of Baikal-S processors have reached Russia through intermediaries in China or the Middle East, the loss of ARM licenses—due to UK sanctions—means that next-generation Russian chips face massive patent-infringement risks, making them nearly impossible to produce at any legitimate global foundry.

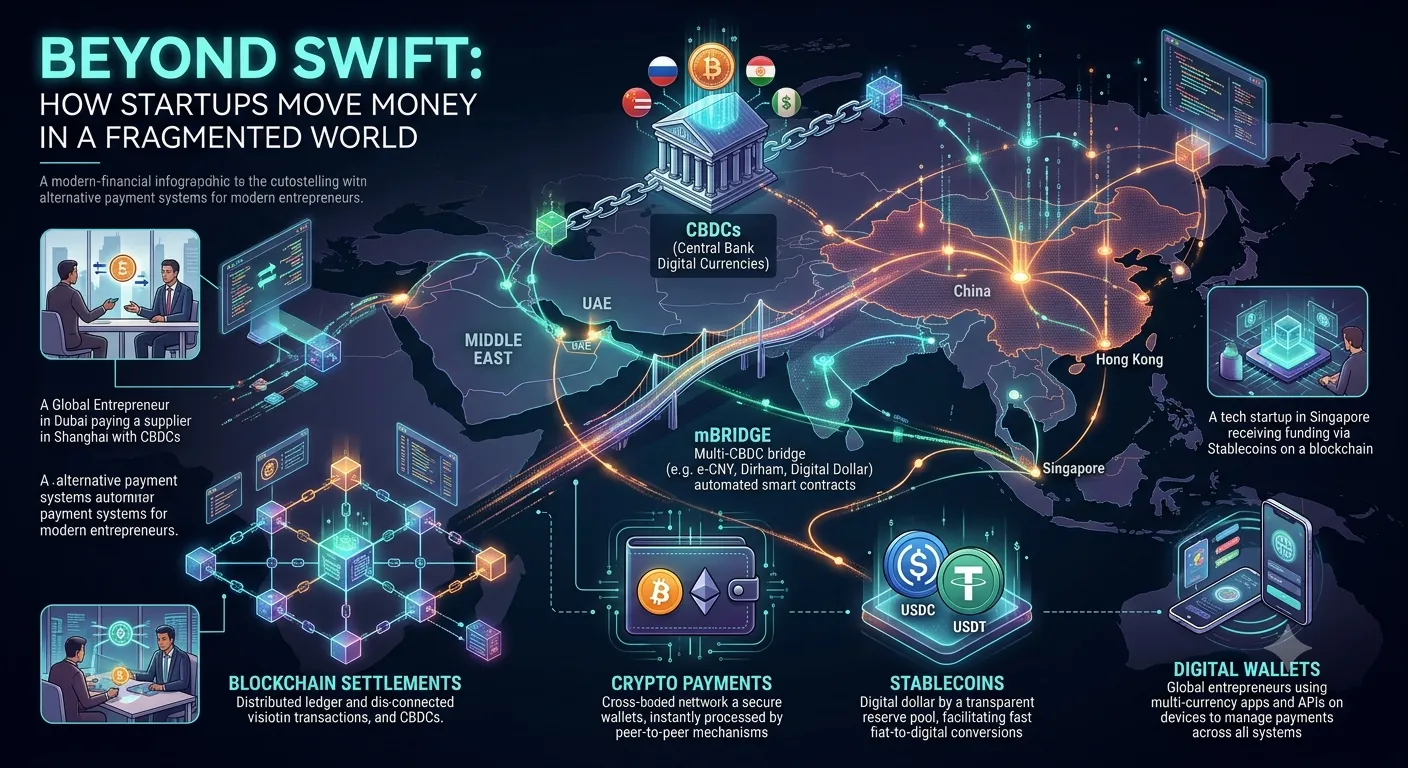

The Rise of Alternative Financial Infrastructures and Non-SWIFT Ecosystems

The weaponization of the SWIFT messaging system has prompted a global search for alternative cross-border payment architectures. For startups in sanctioned jurisdictions, the ability to settle international transactions is the single most significant hurdle to business continuity. This has led to the emergence of "challenger" systems and the rapid development of Central Bank Digital Currencies (CBDCs).

One of the most significant developments is Project mBridge, a blockchain-based wholesale CBDC platform led by the Bank for International Settlements (BIS) Innovation Hub and the central banks of China, Hong Kong, Thailand, Saudi Arabia, and the UAE. By allowing central banks to exchange digital currencies directly on a shared ledger, mBridge bypasses the slow and costly correspondent banking system that underlies SWIFT. For international commercial startups, this could mean near-instantaneous settlement, reduced exchange rate risk, and a significant degree of insulation from U.S.-led financial monitoring.

System/Platform | Technology | Lead Participant(s) | Strategic Objective |

SWIFT gpi/go | Traditional Messaging | Global Banking Consortium | Transparency and speed within existing system |

mBridge | Blockchain / DLT | China, UAE, Thailand, HK | Direct CBDC settlement independent of SWIFT |

CIPS | Real-time Settlement | People's Bank of China | Internationalization of the Yuan for trade |

SPFS | Financial Messaging | Central Bank of Russia | Domestic alternative to SWIFT after 2022 |

RippleNet | Blockchain / XRP | Private / Institutional | Near-instant B2B settlement using crypto-assets |

In tandem with these state-led efforts, private-sector startups are increasingly leveraging cryptocurrency as a bypass for traditional banking. In Venezuela, the state-owned oil company PDVSA began requiring new clients to use digital wallets for spot oil transactions in early 2024, specifically utilizing USDT (Tether), a dollar-pegged stablecoin. This shift occurred after the collapse of the state-backed "Petro" token, demonstrating a preference for globally liquid assets over idiosyncratic state currencies. Similarly, in Russia, a network of cryptocurrency exchanges has filled the void left by sanctioned platforms like Garantex. Platforms such as ABCeX, headquartered in Moscow's Federation Tower, have reportedly processed over $11 billion in crypto-to-ruble transactions, employing aggressive wallet obfuscation and rotation techniques to evade Western monitoring systems.

Case Study: Resilience and Transformation in the Iranian Startup Ecosystem

Iran offers perhaps the most comprehensive case study of how a startup ecosystem can thrive under extreme and sustained economic isolation. Despite decades of sanctions and a recent inflation rate hovering around 40%, the number of startups in Iran grew to over 3,700 by 2025. This resilience is driven by a young, tech-savvy population and a government that has prioritized the "knowledge-based economy" as a means of survival.

The Iranian ecosystem is dominated by "copycat" unicorns—startups that have built localized versions of global platforms blocked by sanctions. Digikala, often called the "Amazon of Iran," has achieved unicorn status with a valuation exceeding $1.2 billion. Because it could not access global payment gateways or logistics providers, Digikala was forced to build its own end-to-end infrastructure, delivering to 99% of Iran and integrating over 396,000 retailers from outside the capital city of Tehran. Similarly, Snapp has evolved into a "super-app" mirroring the functionality of Uber and Grab, facilitating 2 million daily rides and expanding its service range to include food delivery and telemedicine.

Iranian Startup | Sector | Local Adaptation Strategy | Market Impact (2025) |

Digikala | E-commerce | Custom end-to-end logistics and payment network | 60% market share; $500M annual revenue |

Snapp | Ride-hailing | Super-app model; launching EV fleets for sustainability | 50 million rides per year; Azerbaijan expansion |

ZarinPal | Fintech | Primary alternative to PayPal; processing 3M transactions | Supports 60% of Iran’s digital economy |

Cafebazaar | App Marketplace | "Iranian Google Play"; vital for local distribution | Millions of users; backbone for app economy |

Torob | E-commerce | AI-driven price comparison across 130,000 stores | 25 million monthly users |

However, this success is increasingly under threat from internal pressures. In late 2024 and 2025, there were significant moves to transfer majority shares of independent startups to quasi-governmental or state-affiliated communication operators like Hamrah-e Aval and Irancell. Critics argue that this represents a "state capture" of the digital economy, potentially turning these platforms into tools for surveillance or money laundering. Furthermore, the enforcement of strict social laws, such as the Chastity and Hijab Law, led to the temporary shutdown of several major startups in 2023 and 2024 after employees posted photos without mandatory headscarves on personal social media. This internal regulatory volatility, combined with international sanctions, makes the Iranian ecosystem a unique environment where startups must navigate the demands of both global isolation and local authoritarianism.

Russia’s Transition to a "Sovereign" Tech Economy

Following the 2022 invasion of Ukraine, the Russian startup landscape underwent a profound transformation. The mass exit of over 500 Western brands—from Apple and McDonald's to Nokia and SAP—initially created a sense of "import substitution" optimism among domestic entrepreneurs. By 2025, however, the reality has proven more complex. While some Russian retailers like Melon Fashion Group have successfully taken up the space vacated by Inditex (Zara), they remain heavily dependent on factories in China and continue to operate with Swedish shareholders.

The Russian venture capital market has fundamentally changed its structure. Foreign capital has practically disappeared, replaced by business angels and corporate venture funds focused on "technological sovereignty". The volume of investments in early-stage startups has seen a significant recovery—doubling in 2024—driven by the need for localized solutions in cybersecurity, AI, and robotics. However, Russia lacks a traditional defense venture capital ecosystem; instead, the Kremlin has established a state-directed procurement machine where the government is the sole customer and financier. Promsvyazbank (PSB) has been designated as the primary "defense bank" to insulate major lenders like Sberbank and VTB from sanctions while servicing military-industrial cash flows.

For technology startups, the focus has shifted toward the "war tech" sector. The Kremlin has directed state giants like Rostec to form venture funds to scout for small, innovative companies that can provide high-tech solutions in IT and electronics for the state's 800-plus military enterprises. This "venture veneer" hides a reality where failure is punished with bankruptcy and loss of state-backed loans, rather than just the loss of investor confidence.

Corporate Structuring and the Role of Global Arbitrage Hubs

To survive in this fractured landscape, startups have become masters of corporate engineering. The goal is to isolate assets, intellectual property, and financial flows from the "toxic" jurisdictional risks associated with sanctioned countries. The United Arab Emirates (UAE) has emerged as the premier global destination for this type of legal arbitrage.

The Dubai International Financial Centre (DIFC) and the Abu Dhabi Global Market (ADGM) offer streamlined frameworks for the creation of Special Purpose Vehicles (SPVs). These entities function as passive holding companies that allow startups to isolate financial and legal risks. In the UAE, an SPV can hold equity in subsidiaries across multiple jurisdictions, effectively creating a "bankruptcy remote" structure that protects parent company assets from creditors or sanctions authorities.

Hub/Jurisdiction | Key Offering | Advantage for Startups |

ADGM (Abu Dhabi) | SPV Holding Structures | 100% foreign ownership; common law framework |

DIFC (Dubai) | "Prescribed Companies" | Bankruptcy remote; access to 0% corporate tax free zones |

DMCC (Dubai) | Tech-specific Free Zones | Simplified licensing for crypto and digital assets |

Puerto Rico (U.S.) | Act 60 Incentives | Tax credits; insulation from non-U.S. tariffs |

Mauritius | Africa-focused Holding | Favorable tax treaties and investment protection |

A key strategy employed by hardware startups is the use of "parallel imports" or "grey market" channels. Parallel imports involve purchasing genuine, legally manufactured goods in a low-price market (such as Kazakhstan or Uzbekistan) and reselling them in a high-price or sanctioned market (like Russia) without the brand owner's permission. This practice, while controversial, has been legalized by the Russian government to ensure the continued supply of critical technologies. For startups, this creates a niche for "logistic entrepreneurs" who can manage the complex, multi-legged shipping routes required to bypass official distribution systems.

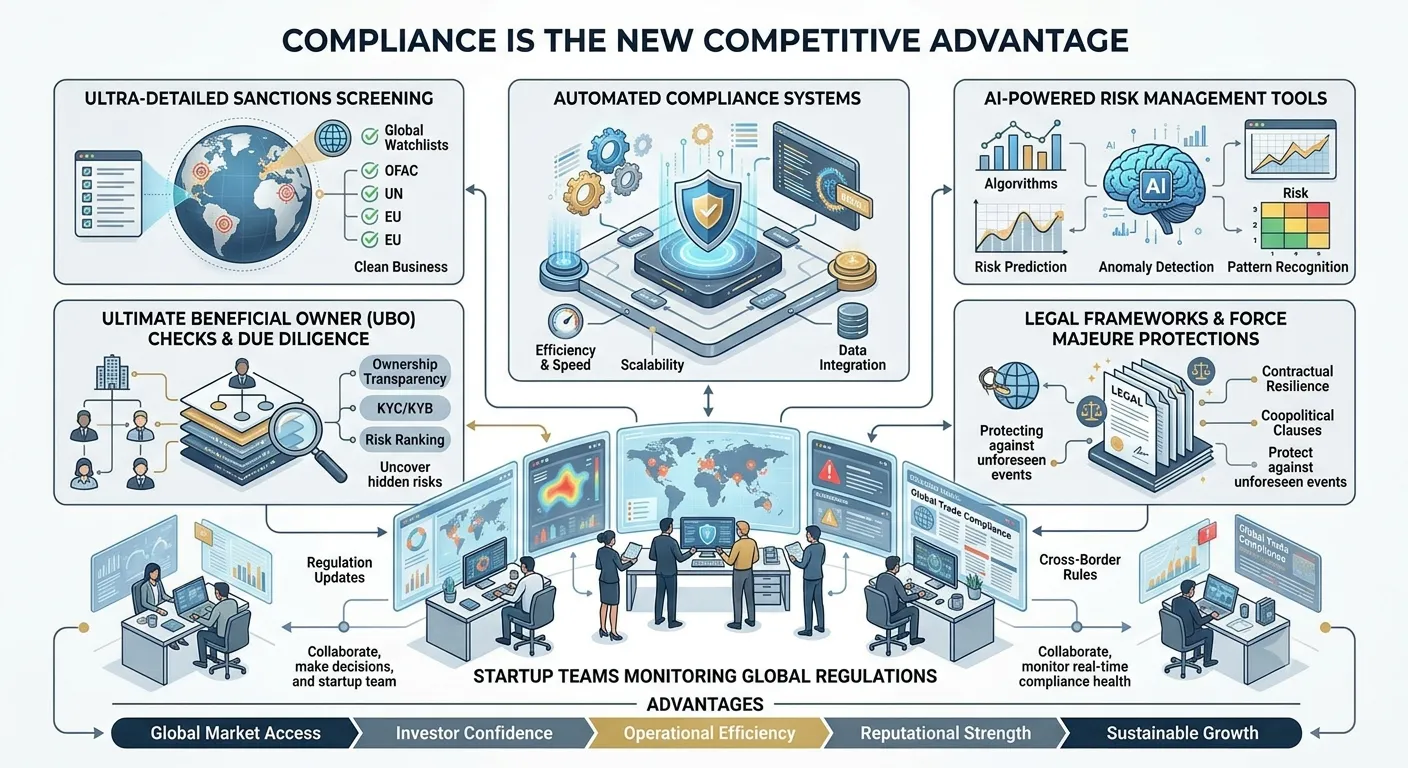

Compliance as a Competitive Edge: Technical and Legal Strategies

In the current environment, a startup’s compliance program is no longer just a legal requirement; it is a vital part of its value proposition to investors and partners. Regulatory authorities in North America and Europe have signaled a move toward "stricter liability," where even unintentional violations of sanctions can lead to massive fines or loss of access to the global banking system.

Modern compliance for startups centers on the "Tone from the Top"—demonstrating a management commitment that prioritizes sanctions adherence as a core value. This involves conducting a multi-layered risk assessment that identifies vulnerabilities across customers, supply chains, and geographic locations. Startups are increasingly turning to automated solutions that scan global sanctions lists (OFAC, EU, UK, UN) in real-time to catch "red flags" before a transaction is completed.

Compliance Pillar | Action Item | Rational/Implication |

UBO Screening | Identify Ultimate Beneficial Owners | Prevents violations of the "50% Rule" for sanctioned owners |

Force Majeure | Update contractual language | Protects against liability if sanctions prevent performance |

Automated Vetting | Real-time screening of all counterparties | Captures rapid updates to SDN lists and entity bans |

Data Integrity | Scrubbing and validating customer data | Reduces false positives and ensures auditability |

Employee Training | Regular briefings on sanctions evasion | Mitigates the risk of "insider" circumvention |

A critical, and often overlooked, aspect of compliance is the "Force Majeure" clause in international contracts. Startups are now advised to explicitly list sanctions as a Force Majeure event, providing them the legal right to suspend or terminate obligations if unforeseen regulatory changes hinder performance. This is particularly relevant for startups in the energy and tech sectors, where a sudden designation by OFAC could otherwise leave a company liable for breach of contract.

Government-Led Initiatives and Public-Private Resilience

Recognizing the strategic importance of startups, several governments have launched initiatives to support innovation in the face of geoeconomic challenges. The U.S. Department of State, in collaboration with leading accelerators like Y Combinator and Techstars, formed "StartOpps," a public-private partnership aimed at catalyzing U.S. business expansion in emerging markets and strengthening global startup ecosystems. This initiative focuses on "3Cs of engagement": Connect, Catalyze, and Collaborate, providing startups with the technical assistance and networking needed to scale in difficult regulatory environments.

Domestically, the U.S. National Science Foundation (NSF) Directorate for Technology, Innovation and Partnerships (TIP) has invested millions into the "SURGE" (Supporting U.S. Regional Growth and Entrepreneurship) program. SURGE is designed to sustain momentum in high-potential innovation ecosystems, providing structured resources, tools, and a national network of connections to help startups in sectors like AI and cybersecurity maintain their competitive edge. Similarly, JPMorganChase announced a $1.5 trillion "Security and Resiliency Initiative" in late 2025, which includes up to $10 billion in direct equity and venture capital investments for startups in critical industries such as defense tech, energy independence, and frontier technologies.

These initiatives suggest a move toward "Integrated Deterrence," where the health of the domestic startup ecosystem is seen as a prerequisite for national security. By providing non-dilutive capital (grants) and phased support through programs like SBIR and STTR, governments are attempting to ensure that strategic innovation continues even as trade barriers rise.

Ethical Implications and the Reputation Risk Trap

The pursuit of survival in sanctioned or "grey" markets presents startups with a profound set of ethical dilemmas. The most significant is the "Reputation Risk Multiplier," where even minor or unintentional associations with sanctioned entities can lead to a collapse in brand value and investor trust. For startups in the tech and defense sectors, being perceived as supporting or enabling a sanctioned regime can be a "lethal blow," cutting them off from Western venture capital and talent pools indefinitely.

Moreover, the relationship between startups and research institutions is under increasing scrutiny. Academic partnerships in jurisdictions like the UK and U.S. are now often governed by Research Ethics Committees (URECs) that prioritize the reputational protection of the university over the academic freedom of the researcher. Startups that spin out of university labs may find their activities restricted if they are deemed "embarrassing" or if they involve collaborations with commercial organizations that do not have robust ethical safeguards.

This has led to a growing emphasis on Corporate Social Responsibility (CSR) and "Social Sustainability" as core components of startup strategy. Businesses that adopt ethical frameworks go beyond mere legal compliance, focusing on transparency and fairness to build long-term value and corporate resilience. In a fragmented world, "trust" has become a fragile but essential resource; startups that can demonstrate ethical integrity are better positioned to navigate the complexities of global trade and secure the loyalty of eco-conscious and socially-aware consumers.

Conclusion: The New Playbook for the Fractured Economy

The geoeconomic shifts of the 2020s have fundamentally rewritten the playbook for startup growth. The assumption of a "flat world" has been replaced by the reality of a "fractured world," where success depends on a startup’s ability to navigate deep-seated geopolitical tensions and complex regulatory mazes.

For startups in sanctioned zones, the focus must be on Resilient Localization. This means building end-to-end domestic supply chains, utilizing alternative financial rails like CBDCs and crypto-assets, and pivoting toward "efficient innovation" to overcome hardware constraints. However, this path requires a cautious approach to state intervention, as the risk of "state capture" remains a constant threat to independent entrepreneurship.

For startups in the West and in neutral hubs like the UAE, the key is Strategic Agility. This involves professionalizing compliance as a core competency, leveraging offshore structures for risk isolation, and proactively seeking government-backed resilience funding. The ability to "pivot" is no longer just about product-market fit; it is about "regulatory fit"—the capacity to reconfigure a business model overnight in response to a new executive order or a sudden shift in trade alliances.

Ultimately, the global startup ecosystem is demonstrating a remarkable capacity for adaptation. While sanctions and trade barriers create significant friction, they also serve as catalysts for new forms of innovation—fostering the development of a more diverse, decentralized, and resilient global economy. The startups that survive this era will not be those that simply follow the rules, but those that understand the underlying geopolitical currents and build the flexibility to ride them.

Protect Your Future: The Precision Vesting Calculator

Don't let a "handshake deal" complicate your exit. Map out your ownership journey with our Vesting Calculator

Calculate Your Vesting Schedule →