SaaS Exits: Are We Seeing the Next Wave?

July 1, 2026 by Harshit Gupta

The global software-as-a-service ecosystem is currently navigating a period of profound structural transition, often characterized by market participants as the great unlocking. Following a multi-year period of constrained liquidity, the convergence of stabilizing interest rates, a massive backlog of private equity-held assets, and the transformative pressure of generative artificial intelligence has initiated a new wave of exit activity. However, this wave does not resemble the speculative frenzy of 2021; instead, it is defined by a rigorous flight to quality, where valuation premiums are reserved exclusively for assets demonstrating operational efficiency and agentic artificial intelligence readiness. While the broader initial public offering market has shown signs of recovery in early 2026, the software sector faces a unique narrative driven by concerns over disruption of traditional seat-based revenue models. This has shifted the primary exit focus toward strategic mergers and acquisitions and secondary market transactions, creating a bifurcated landscape where winners are valued as essential infrastructure and laggards face the pressure of a looming private credit maturity wall.

The Macroeconomic Foundations of the 2026 Exit Wave

The foundational driver of the 2026 exit environment is the stabilization of the global interest rate regime. After maintaining restrictive levels through much of 2024 and mid-2025, the Federal Reserve initiated a series of rate cuts in late 2025, bringing the federal funds rate to a range of 3.50%−3.75% by January 2026. This pivot has materially lowered the cost of debt for leveraged buyouts and provided the pricing certainty required for equity markets to price initial public offerings aggressively. The transition from a period of high volatility to one of navigable clarity has strengthened chief executive officer sentiment, fueling an environment defined by dream deals as industry leaders seek to acquire new capabilities that supercharge their next phase of growth.

Global private equity transaction value reached almost $2 trillion in 2025, up from roughly $1.6 trillion in 2024, even as the number of deals slipped slightly. This indicates a shift toward larger, more complex transactions where conviction is high. The long end of the yield curve, represented by the 10-year Treasury, has settled around 4.0%−4.2%, a level that materially raises the risk-free benchmark against which every acquisition is judged. This higher-for-longer structural reality suggests that long-term yields are unlikely to revert to the artificially suppressed levels of the 2010s, forcing a permanent shift in how software companies manage their burn rates and profitability.

Jurisdiction | Central Bank Rate (Q1 2026) | Trend Direction | 10-Year Treasury/Bond Yield |

United States (Fed) | 3.50%−3.75% | Easing/Stable | 4.0%−4.2% |

Eurozone (ECB) | 2.00% | Stable | 2.2%−2.5% |

United Kingdom (BoE) | 3.75% | Easing | 3.6%−3.9% |

Canada (BoC) | 4.25% | Potential Hike | 3.8%−4.1% |

The world economy is poised for continued expansion across all regions in 2026, with the United States likely to outperform substantially due to reduced tariff drag and tax cuts. However, inflation risks remain despite the easing of rates by central banks. Policy rates are forecast to continue their decline, but the era of near-zero rates is unlikely to return. This divergence in global interest rate paths highlights the need for selective portfolio positioning, as markets remain highly sensitive to trade developments and any indication of a slowdown in the artificial intelligence-driven investment boom.

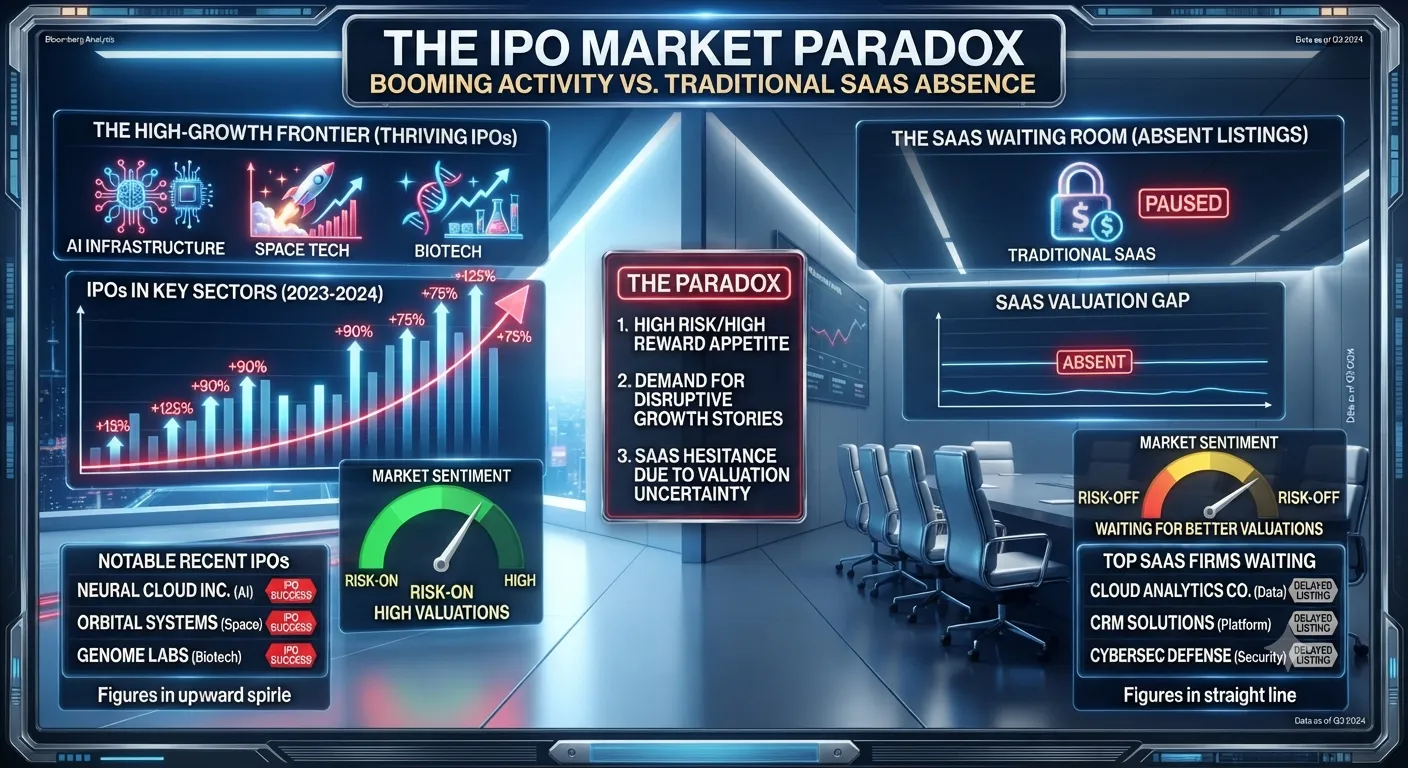

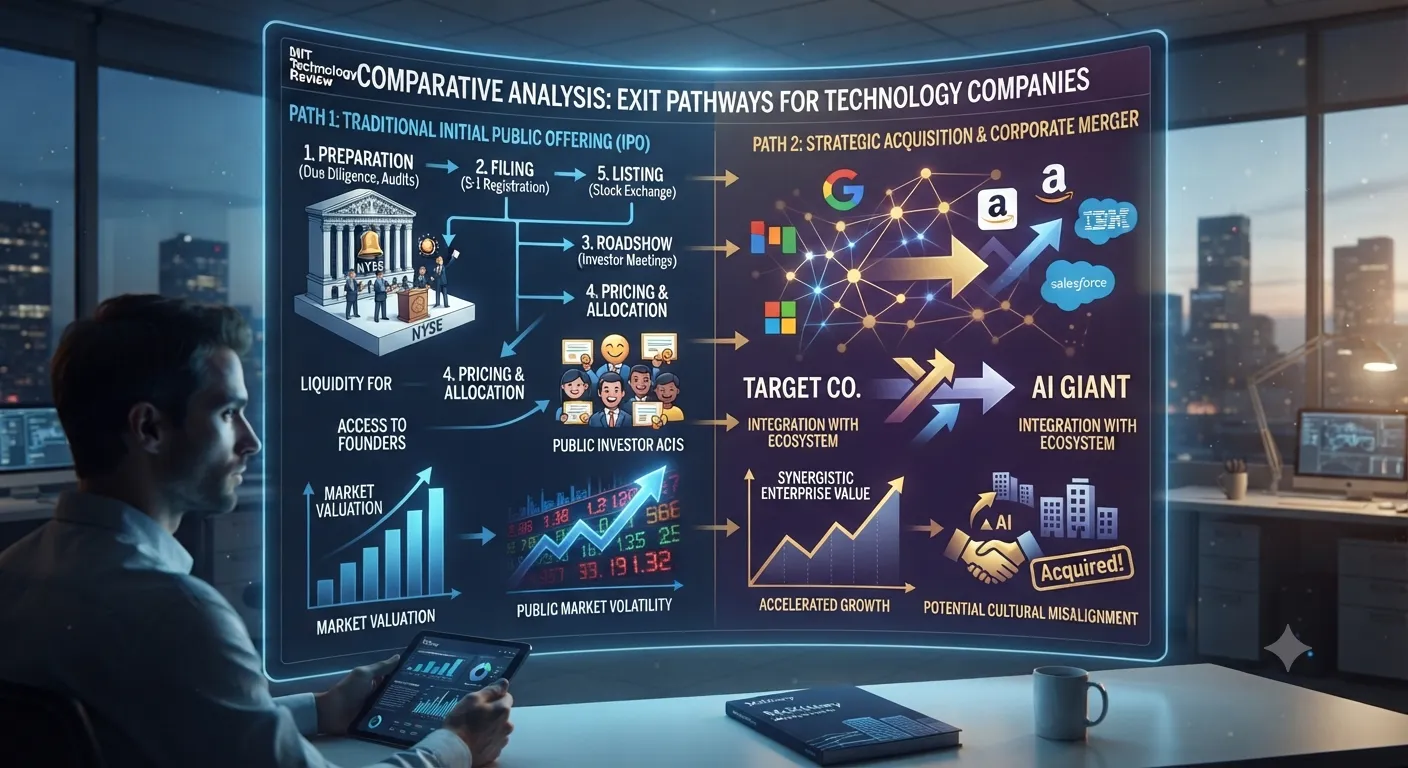

The Initial Public Offering Market Paradox

The initial public offering market in early 2026 presents a statistical paradox. Globally, proceeds from initial public offerings have seen a 21% increase compared to 2024, yet venture-backed software debuts have remained nonexistent. Investors have pivoted away from traditional enterprise software in favor of sectors viewed as resistant to artificial intelligence disruption, such as construction technology, space technology, and biotechnology. In the first two months of 2026, approximately 11 venture-backed companies went public on major exchanges in the United States, raising just over $3 billion, but none were traditional software-as-a-service providers.

Company | Sector | Raising Amount | Day 1 Performance | Status |

EquipmentShare | Construction Tech | $747 Million | +33% | Priced Jan 2026 |

PicPay | Fintech | $434 Million | −5% | Priced Jan 2026 |

York Space Systems | Space Tech | $250 Million | +12% | Priced Feb 2026 |

Liftoff | AdTech | $400 Million | Stable | Withdrawn/Re-filed |

Medline | Healthcare | $7.2 Billion | +15% | Priced Dec 2025 |

The absence of software debuts is notable because enterprise software companies have historically been reliable entrants into the public market. This shift is attributed to an extended selloff in the public software sector fueled by concerns of artificial intelligence-abetted disruption. Furthermore, the poor post-debut performance of 2025 listings has dampened appetite. Design software platform Figma, which went public in mid-2025, has seen its value drop more than two-thirds from its peak, while business travel platform Navan has lost more than half its value since its October 2025 debut.

Despite this sector-specific drought, the broader pipeline remains active with 216 companies seeking to raise approximately $12.4 billion by the end of January 2026. Momentum in initial public offering activity, particularly in the second half of 2025, has created significant optimism for investors, with technology once again setting the pace, though primarily through artificial intelligence infrastructure and mission-critical software. The special purpose acquisition company market also re-fueled in 2025 with nearly 150 new vehicles formed, providing alternative paths to public markets for emerging technology firms.

Strategic Mergers and Acquisitions as the Primary Exit Engine

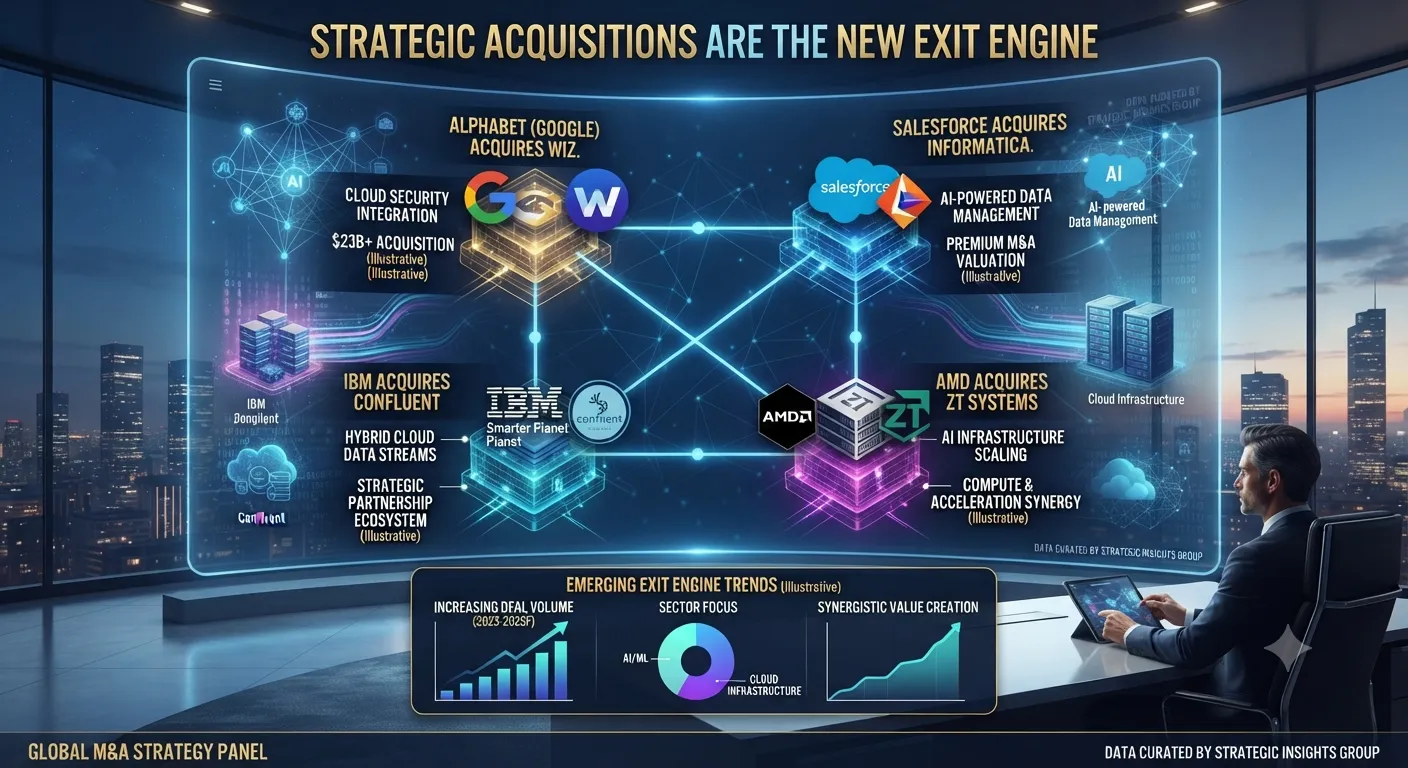

As public markets remain selective for traditional software, the strategic mergers and acquisitions channel has become the primary exit engine. Strategic buyers, under pressure to demonstrate artificial intelligence growth, are aggressively pursuing acquisitions that provide established data sets and governed artificial intelligence infrastructure. The technology mergers and acquisitions segment surged by 77% in late 2025, propelled by deals for artificial intelligence-related assets.

A defining feature of the current cycle is the resurgence of mega-deals, defined as transactions exceeding $10 billion. In 2025, the number of such deals reached 13, exceeding the prior high-water mark set in 2021. Alphabet's $32 billion acquisition of cybersecurity leader Wiz represents the largest acquisition in the company's history and serves as the cornerstone of a security-first artificial intelligence strategy. This deal, finalized in early 2026, followed an initial rejection by Wiz management who had preferred an independent initial public offering. The shift in sentiment occurred as Wiz surpassed $1 billion in annual recurring revenue and regulatory hurdles in the United States began to moderate.

Acquirer | Target | Deal Value | Primary Strategic Driver |

Alphabet | Wiz | $32 Billion | Cybersecurity for Google Cloud |

Salesforce | Informatica | $8 Billion | Agent-ready Data Management |

IBM | Confluent | $11 Billion | Real-time Data Foundations |

IBM | HashiCorp | $6.4 Billion | Multi-cloud Automation |

AMD | ZT Systems | $4.9 Billion | AI Infrastructure Verticalization |

TPG Consortium | Hologic | $18.3 Billion | Healthcare Strategic Repositioning |

The realization that artificial intelligence models do not matter without trusted, governed, and real-time data has driven incumbents to acquire rather than build across the technology stack. Salesforce’s $8 billion purchase of Informatica and IBM’s $11 billion acquisition of Confluent reflect this urgency to secure the data infrastructure strategic moat. Furthermore, the 2026 outlook suggests a 50% higher volume of strategic separations and spin-offs as large companies sharpen their focus to unlock value for shareholders.

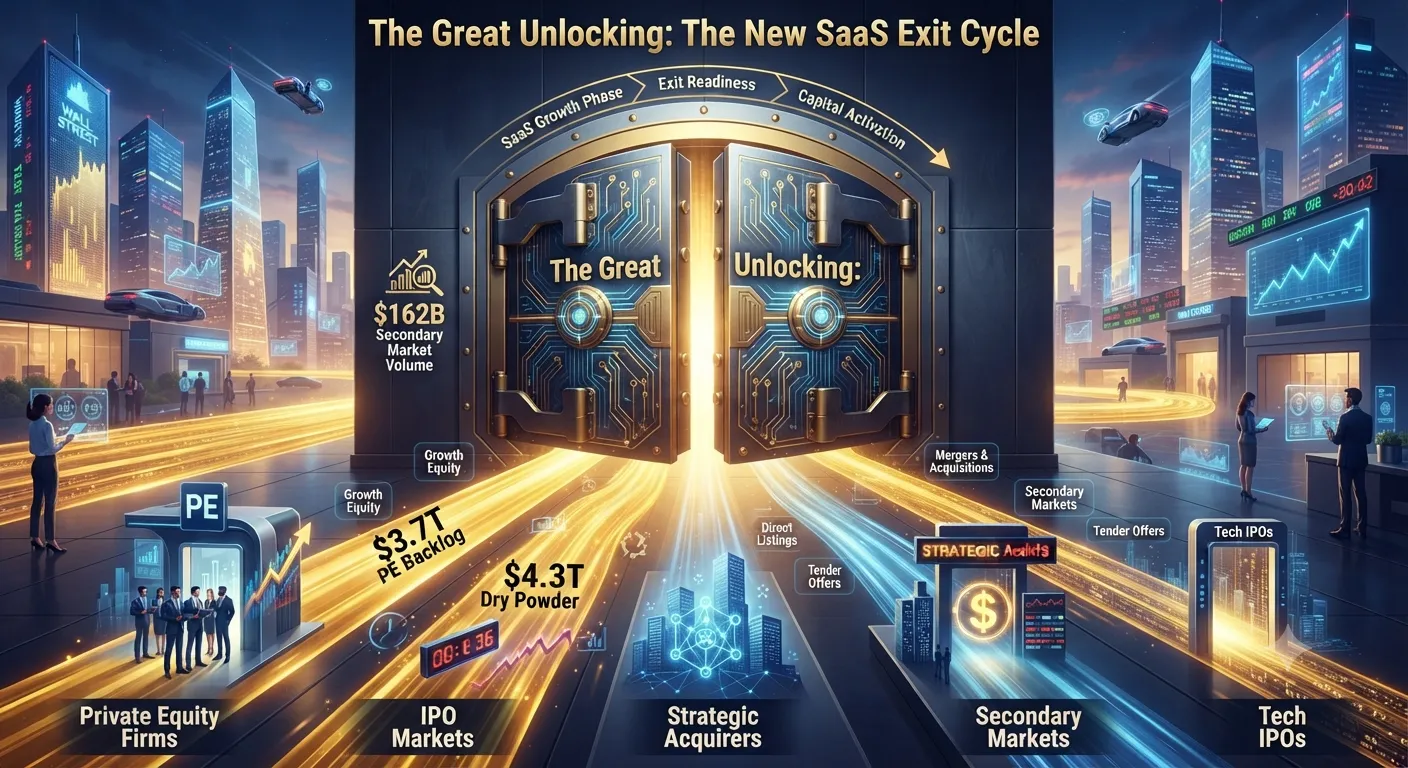

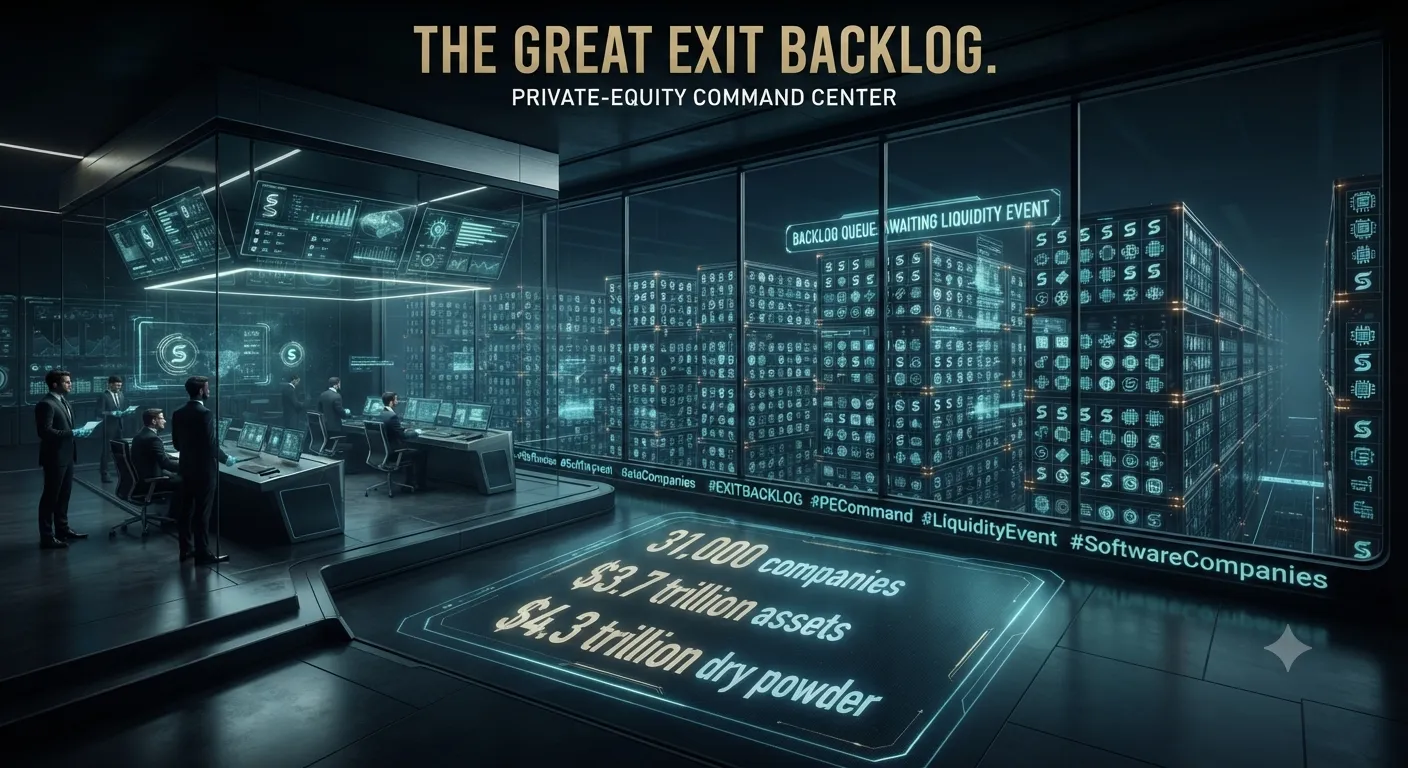

The Private Equity Backlog and the Great Unlocking

Private equity firms are entering 2026 with a record backlog of at least 31,000 companies valued at $3.7 trillion. This accumulation of aging assets has created intense pressure to generate liquidity for limited partners who have faced several years of constrained distributions. In 2025, distributions as a share of total private equity assets under management hit their lowest recorded level at approximately 10%, compared with a historical average of 16%.

The industry's biggest players are moving toward a new phase of measured momentum, with platform buyouts expected to account for at least 25% of total private equity deal activity in 2026. Sponsors face an urgent need to sell assets while simultaneously sitting on $4.3 trillion of dry powder. This dual pressure is driving a flight to quality, where fund managers are willing to pay premium multiples for durability and downside protection in an uncertain macro environment.

To bridge the exit gap, secondary markets are playing an increasingly critical role. Secondary transaction volume rose 45% in 2024 to a record $162 billion and surged another 51% in the first half of 2025. These markets help general partners manage holding periods and recycle capital without waiting for the public markets to fully reopen.

Exit Strategy | 2025 Volume | 2026 Projected Trend | Key Driver |

Trade Sales (Strategics) | $481 Billion | Increasing | Strategic convictions in AI |

Sponsor-to-Sponsor | $217 Billion | Stable | Deployment of dry powder |

IPOs (PE-backed) | $38 Billion | Thawing | Stabilizing rate environment |

Secondaries | $217 Billion | Record Highs | LP demand for distributions |

Take-Privates | $905 Billion (Value) | Consistent | Public market valuation gaps |

The successful $7.2 billion initial public offering of Medline in late 2025 provided a positive signal that private equity-backed firms can achieve substantial liquidity events. However, traditional exits remain a trickle rather than a flood, forcing general partners to utilize structured deals, continuation vehicles, and net asset value lending to create liquidity. Approximately 40% of the dry powder ready for deployment today has been available for over two years, the highest level on record, suggesting that fund managers will eventually be forced to write ever-larger checks to compete for high-quality assets.

Valuation Mechanics and the Post-Pandemic Reset

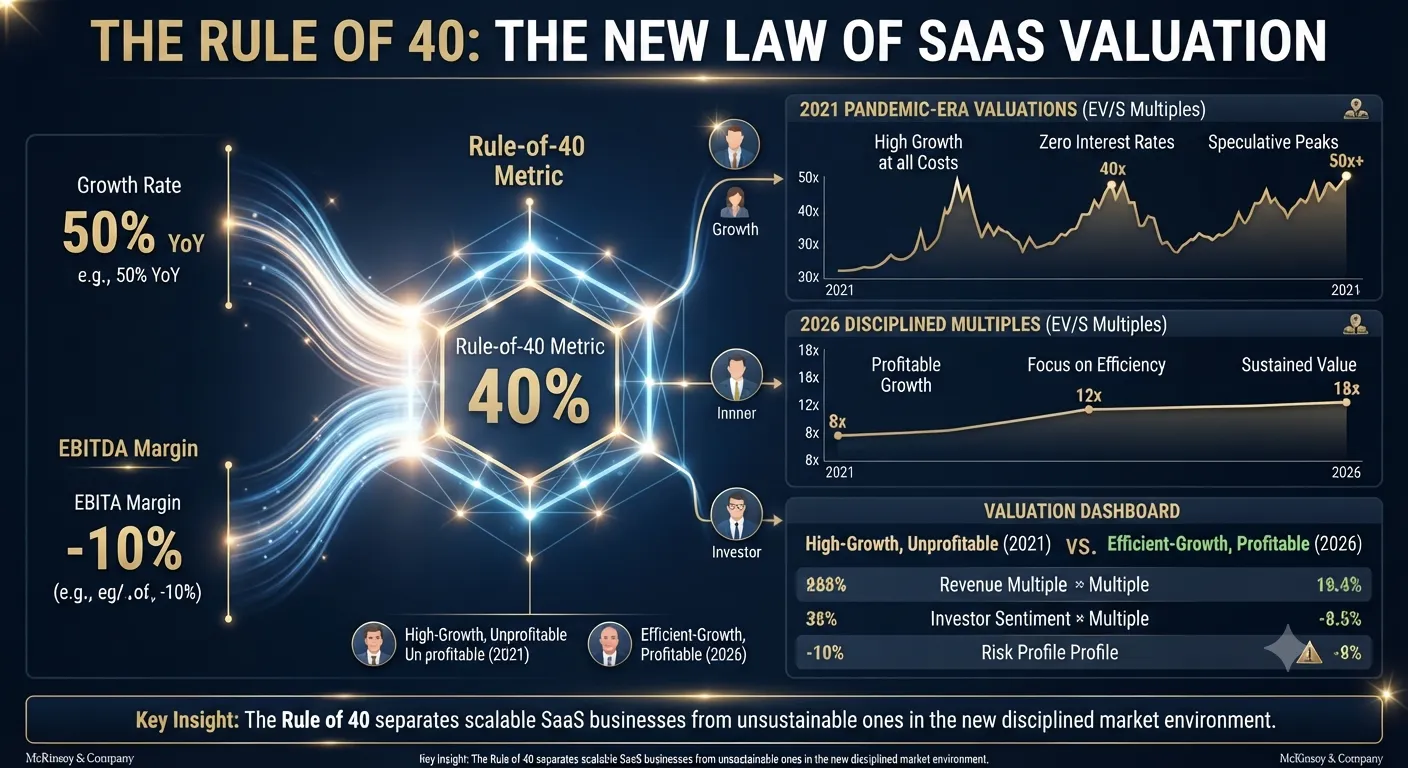

The valuation landscape for software has undergone a fundamental realignment. The pandemic-era digitisation that pushed median growth rates to 31% has faded, with median revenue growth falling to 12.2% by late 2025. In this environment, the market has shifted its primary valuation framework from aggressive revenue expansion to the rule of 40, which balances growth against profitability.

Metric | Pandemic Peak (2021) | Post-Crash Low (2023) | Current Baseline (2026) |

Median Revenue Multiple | 18.0x−19.0x | 4.4x | 4.0x−5.1x |

Top-Quartile Multiple | 30.0x+ | 8.0x | 12.0x−14.5x |

Median Growth Rate | 31% | 17% | 12% |

Median EBITDA Margin | Negative | Break-even | +3% |

Rule of 40 Premium | Discounted | Mandatory | Non-negotiable |

Public software multiples have compressed from approximately 9.0x to 6.0x price-to-sales ratios, reaching levels not seen since the mid-2010s. Currently, public software companies are being taken private at an average of 7.7x annual recurring revenue. Investors are increasingly obsessed with three specific levers: the rule of 40, the artificial intelligence premium, and net revenue retention. A standard software company growing at 30% year-over-year can expect offers in the 5x−7x range, but achieving a 10x multiple now requires a net revenue retention above 120% or a proprietary artificial intelligence moat.

The artificial intelligence premium is highly bifurcated. Thin layers over external large language models, often called artificial intelligence wrappers, are seeing their multiples collapse as retention struggles. Conversely, vertical artificial intelligence companies that solve deep industry problems are trading at 9x−12x annual recurring revenue, with some commanding over 15x. This shift reflects a market that rewards verifiable competitive moats and data advantages rather than broad sector narratives.

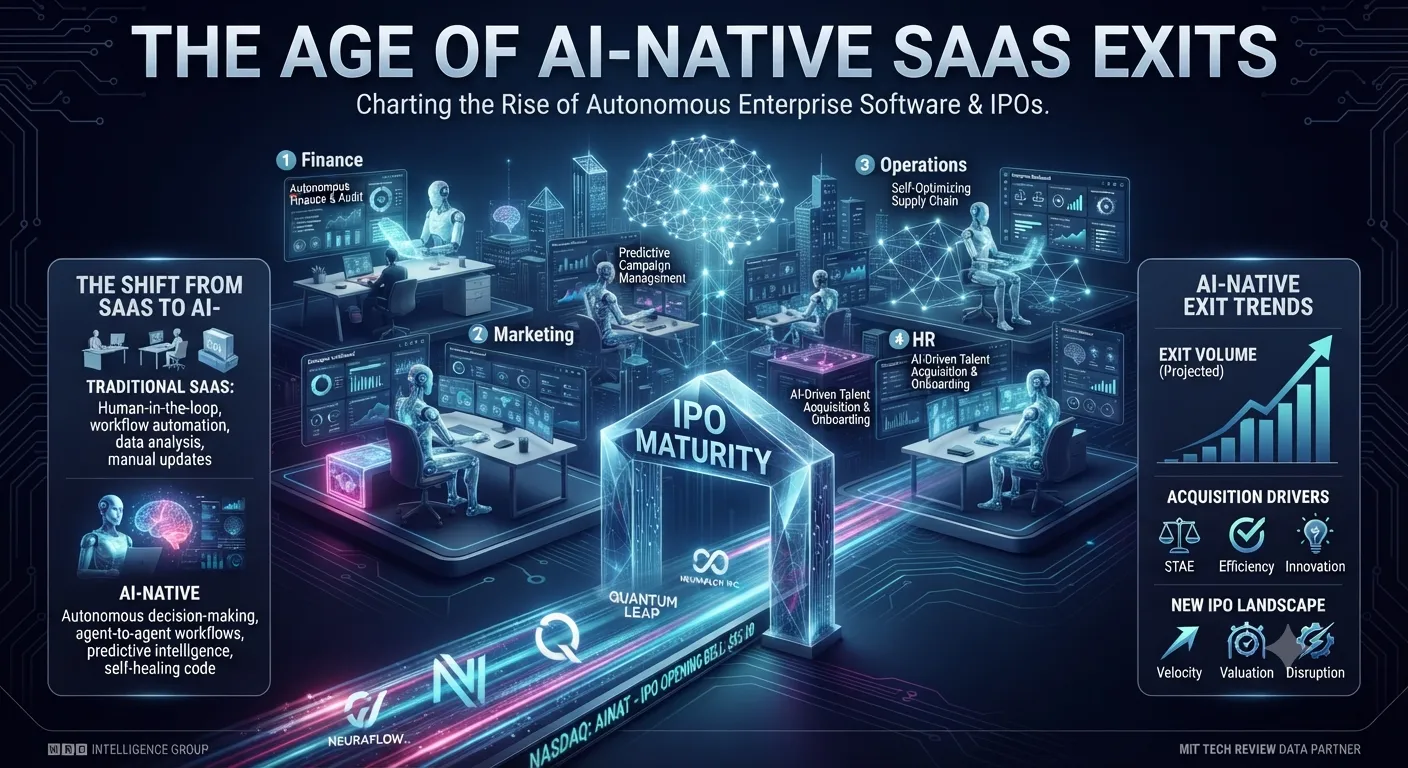

The Artificial Intelligence Disruption Thesis

A primary concern for the software industry in 2026 is whether artificial intelligence constitutes a growth catalyst or a structural threat. Some market participants argue that the software sector is being starved, not killed. While overall information technology budgets are up by approximately 8%, artificial intelligence budgets have increased by over 100% year-over-year. This redirection of funds is often harvested from existing software budgets, leading to flat application counts and declining net new customer numbers.

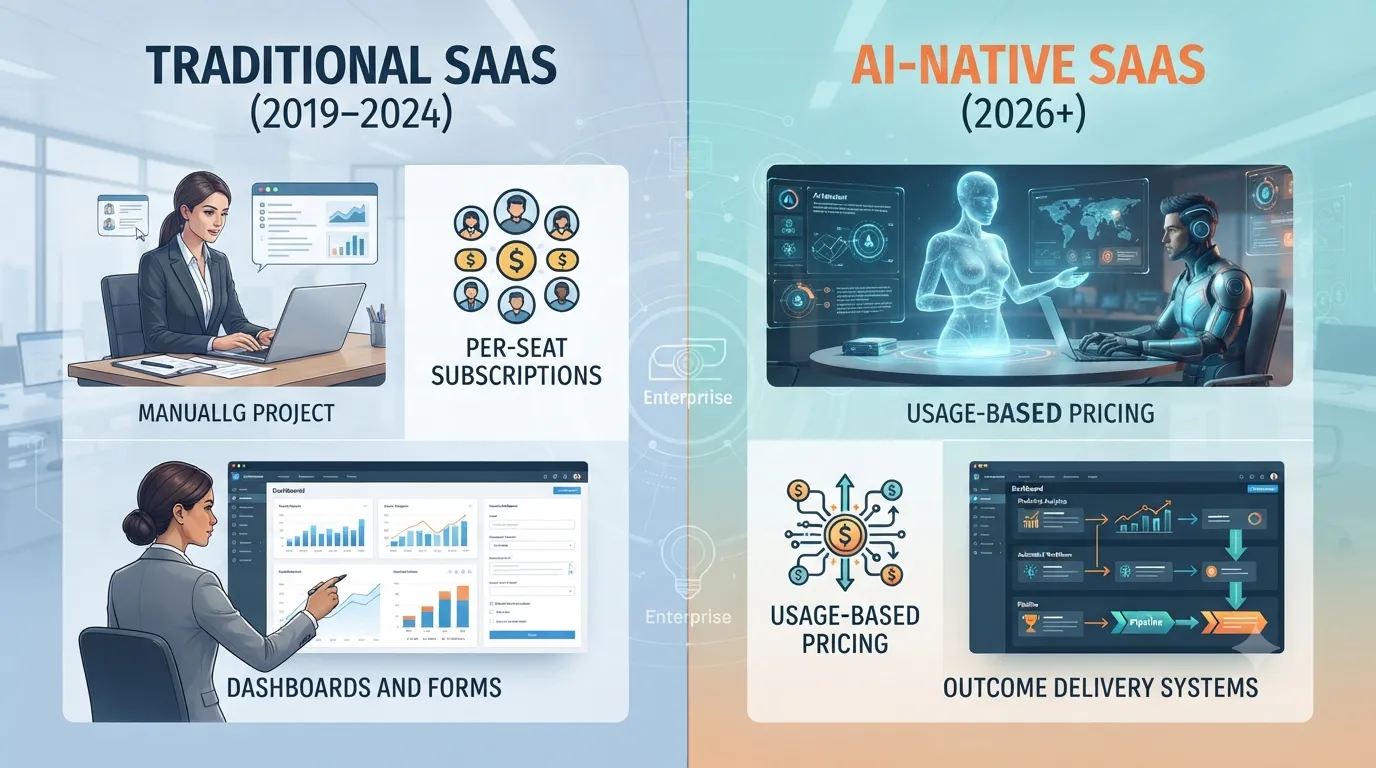

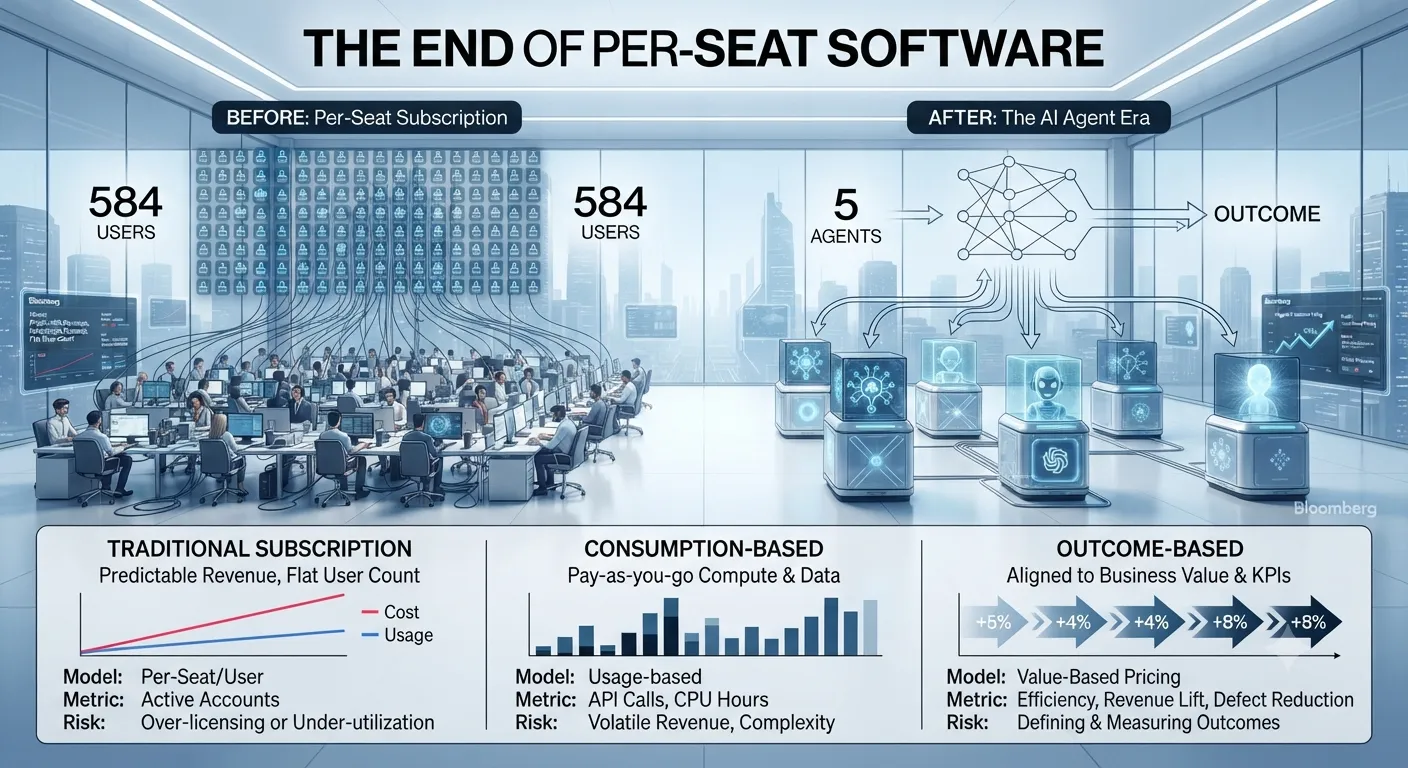

The quiet killer of the traditional software model is the reduction in seat-based revenue. As artificial intelligence agents become capable of executing complex workflows, the human headcount required to operate software decreases. If a small number of artificial intelligence agents can do the work of a large team of sales representatives, the requirement for software seats could drop by as much as 90% for the same work output. Consequently, companies are being forced to pivot toward outcome-based and consumption-based pricing models.

Feature | Traditional SaaS (2019-2024) | AI-Native SaaS (2026+) |

Pricing Model | Per-seat subscription | Usage or outcome-based |

Primary Metric | User engagement | Agentic task completion |

Growth Engine | New customer acquisition | NRR and expansion |

Interface | Forms and dashboards | Agentic/Multimodal |

Value Prop | Productivity tool | Outcome delivery |

Contrastingly, some contrarian views suggest that software will not face extinction but will instead become the critical pathway for enterprises to controllably harness artificial intelligence. Traditional software giants possess deep domain expertise, robust sales channels, and customer trust that startups lack. Artificial intelligence handles creative analysis and produces intelligent data, but this data must still be processed, stored, and executed by deterministic software technology stacks. In this view, established vendors will domesticate artificial intelligence within their extensive platforms, turning a perceived threat into an immense value-driver.

Private Credit as a Hidden Risk to Exits

While equity markets are recovering, the private credit market, valued at $3 trillion, represents a significant hidden risk to software exits in 2026. Private credit underwrote a decade of software buyouts, with an estimated $$600 - $750 billion exposure to the sector. Many of these loans were issued at peak valuations in 2021 and 2022. With current valuations often cut in half, many companies face a maturity wall where they may be unable to repay or refinance their debt.

Distressed debt in the technology sector reached approximately $46.9 billion in early 2026, dominated by software companies. Default rates for United States private credit could hit 13% if artificial intelligence disruption accelerates, significantly higher than projected high-yield default rates. If sponsors cannot refinance existing portfolio companies, they are unable to buy new ones, effectively stalling the primary acquisition exit path. This stress in the financial plumbing has also made venture debt harder to obtain, as the lenders powering that market are often cousins of the private credit funds under stress.

Despite these risks, some institutional investors are buying the dip. Blue Owl, Goldman Sachs, and Blackstone provided a $1.4 billion loan to finance the acquisition of OneStream at a $6.4 billion valuation in early 2026, even amidst sector volatility. This suggests that for high-quality, well-capitalized firms, financing remains available, albeit at wider spreads that reward lender discipline.

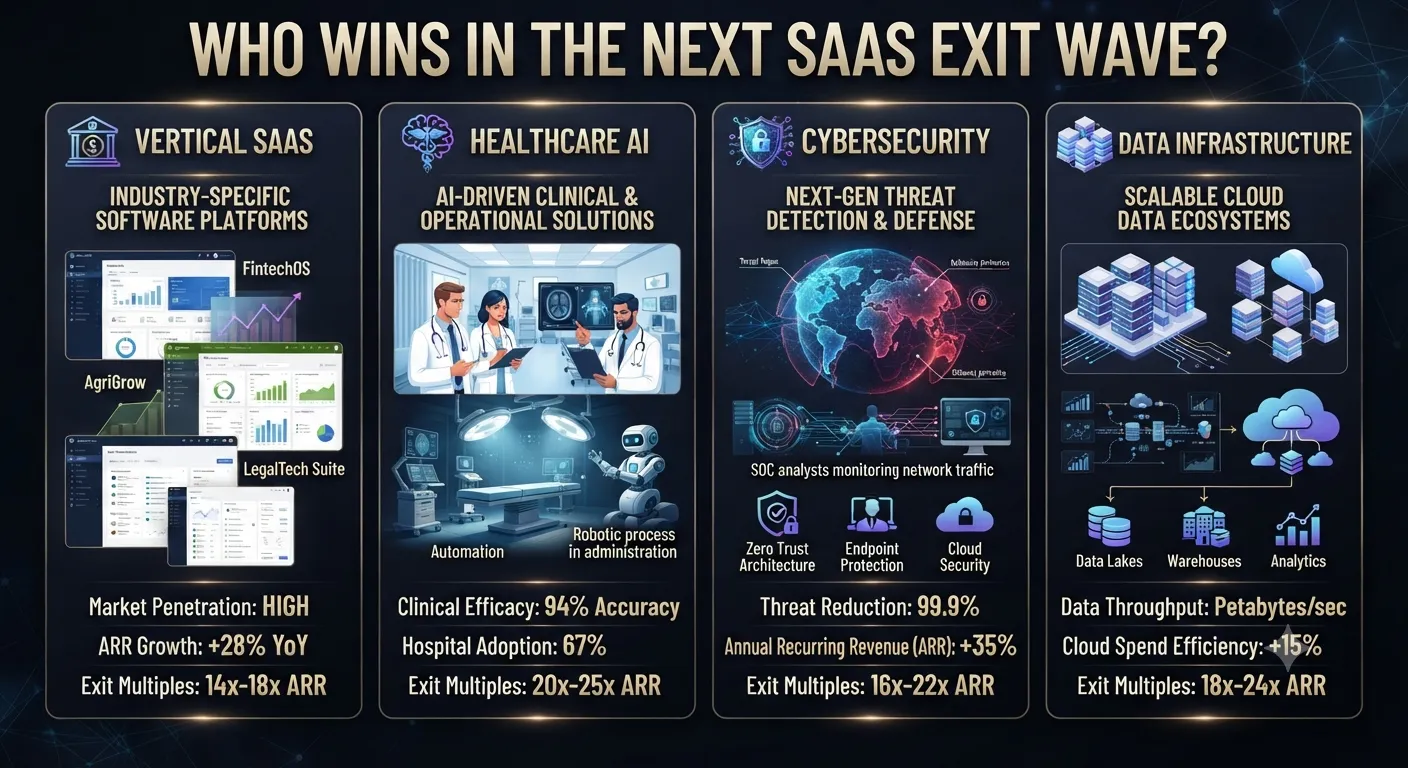

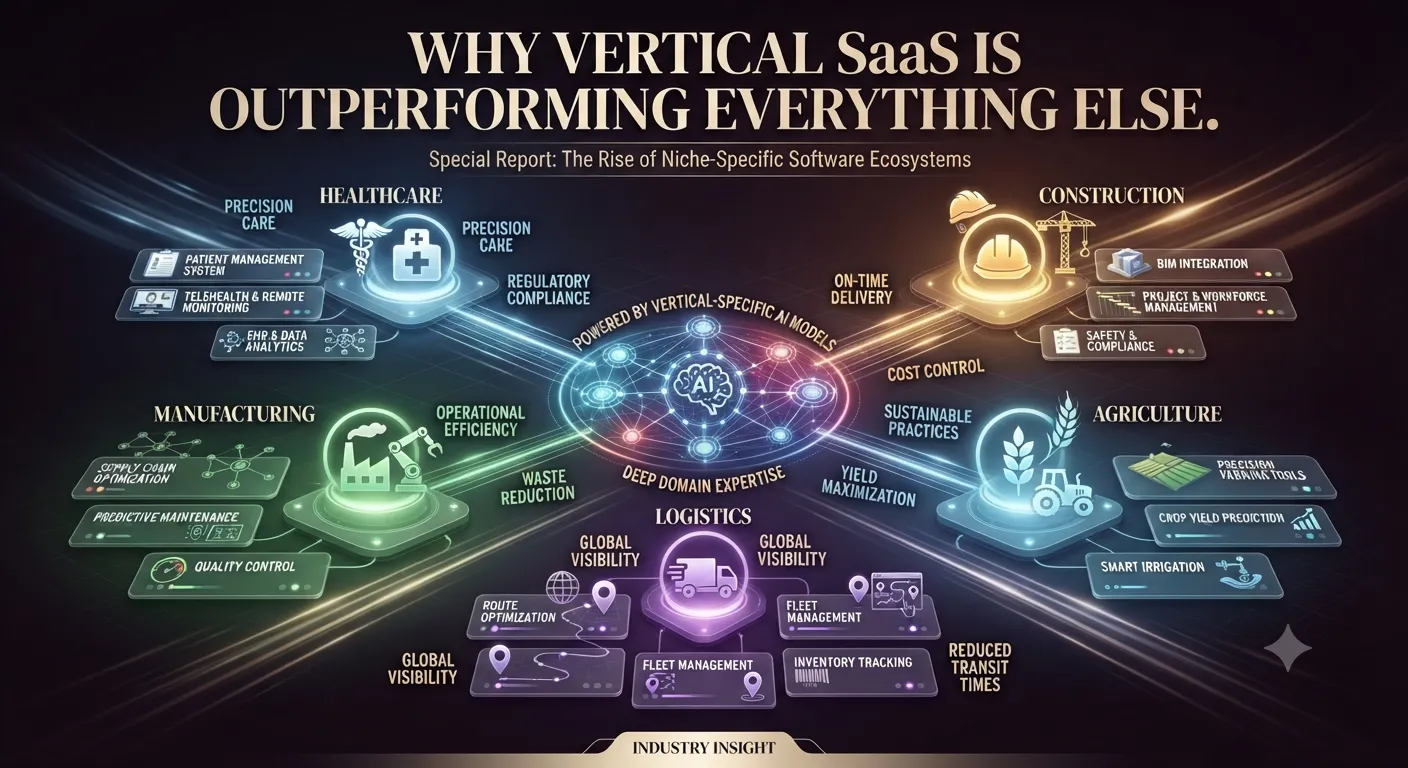

Sector Specificity: Vertical Software and Health Tech

The 2026 exit wave is highly uneven across different sub-sectors. Vertical software, built for specific industries like construction or automotive, is outperforming horizontal software by growing 2−3x faster. Approximately 60% of small businesses now rely on vertical software platforms for daily operations, underscoring the practical impact of industry customization.

Healthcare-focused software-as-a-service has emerged as a particularly resilient niche. Healthcare artificial intelligence companies are reaching $100 million annual recurring revenue in under five years, compared with over ten years for traditional healthcare software. These firms often demonstrate significantly higher revenue per full-time employee, reaching up to $1 million in artificial intelligence-native models compared to $$200,000 - $400,000 in traditional software-as-a-service.

Category | Avg. Deal Size (2025) | Growth (YoY) | Key Metric |

Health Tech AI | $29.3 Million | +42% | Revenue per FTE |

Vertical SaaS | $25.0 Million | +15% | Net Revenue Retention |

Horizontal SaaS | $18.0 Million | Flat | Burn Rate/Efficiency |

Cybersecurity | $35.0 Million | +20% | Strategic Moat Value |

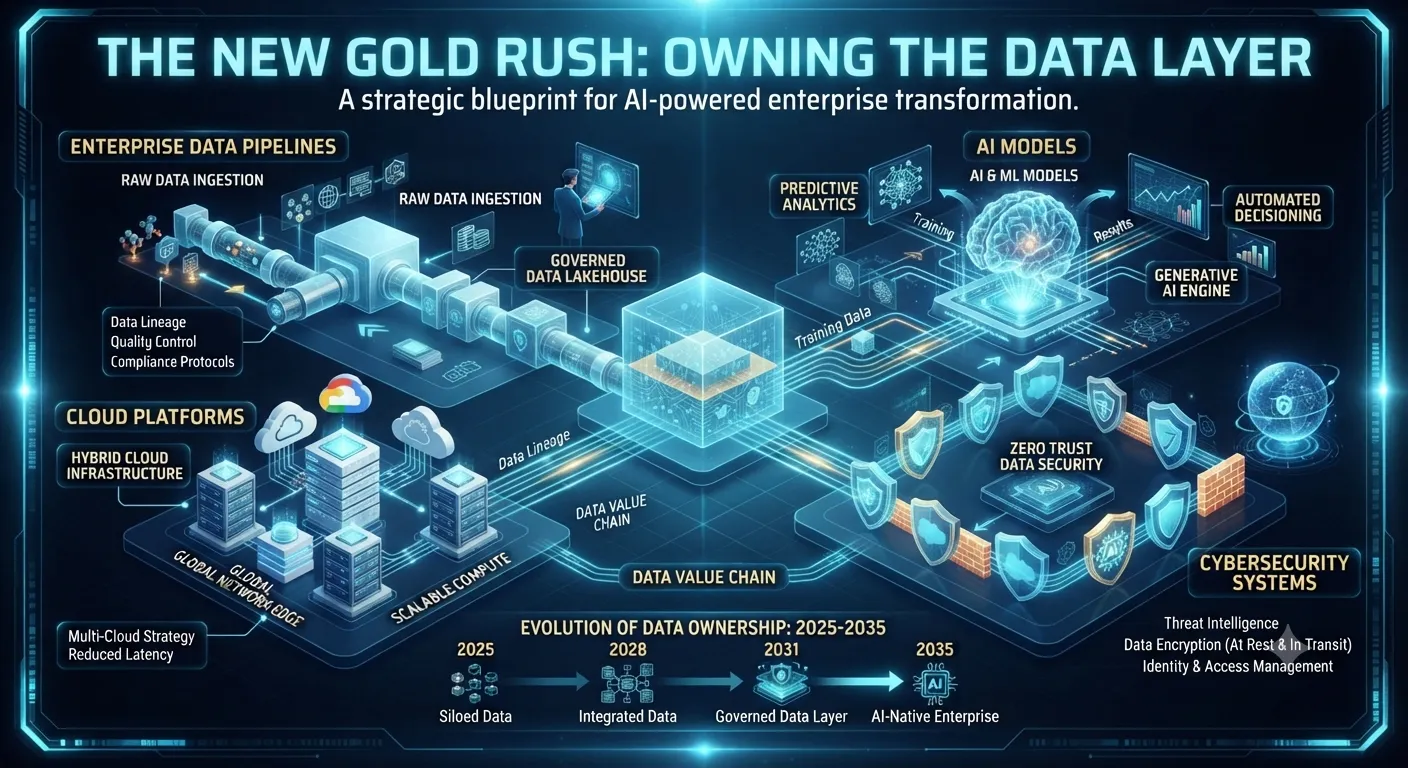

Cybersecurity also remains a high-priority sector for exits, as artificial intelligence developments ripple through the industry creating a wave of dislocation. Beyond the Alphabet-Wiz deal, Palo Alto Networks’ $25 billion acquisition of CyberArk in 2025 highlights the growing premium for scale in the multi-cloud security space. Investors are increasingly favoring companies that own the data layer, as artificial intelligence agents must read from and write to a stable system of record to be effective.

Geopolitical Influences and Regulatory Dynamics

Geopolitical risks and trade tensions remain significant headwinds for exit activity in 2026. Corporations are likely to pass more tariff-related costs along to consumers, which could affect corporate spending on software. Tariff uncertainties have also accelerated nearshoring and influenced cross-border deal-making as international buyers seek to secure a foothold in the United States market.

Regional dynamics show a nuanced picture:

United States: Activity is bolstered by anticipated deregulation and forecasted declines in interest rates, despite tariff uncertainties.

Europe: The market is recovering as monetary easing supports valuations, though issuance remains lower than the United States. The successful Verisure initial public offering in late 2025 demonstrated robust investor confidence in European capital markets.

Asia-Pacific: Japan is seeing a resurgence in take-private deals and carve-outs, while Hong Kong has reestablished itself as a leading venue for large-scale fundraisings.

Middle East: A strong pipeline exists driven by sovereign asset monetization and new frameworks for international listings.

Regulatory transformation is also a key theme. Around the world, regulators implemented reforms in 2025 aimed at strengthening capital markets and attracting listings. In the United States, the Securities and Exchange Commission’s 2026 agenda is focused on capital formation and disclosure reform. However, heightened scrutiny from the Federal Trade Commission and state activism in jurisdictions like California and New York continue to demand operational concessions during large-scale transactions.

The 2026 Pipeline: Anticipated Listings and Growth

The 2026 pipeline for software-as-a-service exits is the strongest in years, characterized by a recalibration of the market's engine rather than just a recovery. Several highly anticipated unicorns are rumored to be targeting listings in mid-to-late 2026.

Company | Estimated Valuation | Category | IPO Status |

SpaceX | $1.5 Trillion | Aerospace/Infrastructure | Rumored Mid-2026 |

OpenAI | $$830B - $$1T | AI Research/Deployment | Rumored Late 2026 |

Anthropic | $$230B - $$350B | AI Large Language Models | Rumored 2026/27 |

Databricks | $$134B - $$160B | Data Lakehouse/AI | Top Candidate 2026 |

Canva | $$ 42B - $$ 50B | Visual Communication | IPO Watchlist 2026 |

Stripe | $$ 100B+ | Payments Infrastructure | Partial IPO Rumored |

Revolut | $$ 45B+ | Fintech | IPO Watchlist 2026 |

Shein | $$ 66B | Consumer E-commerce | Dual-listing Target |

For OpenAI, going public would not just unlock new capital but introduce a new level of accountability and scrutiny regarding the true economics of its massive cloud costs. The company would have to explicitly disclose the 1 trillion in circular financing deals that have obscured its financial health. Similarly, Databricks sits at the center of the world's data ecosystem, and its listing could be one of the most substantial enterprise-software events in recent history.

Investment banks like Goldman Sachs and Morgan Stanley are reporting record pipelines for mega-deals, suggesting that the era of boardroom hesitation is ending. The successful January 2026 initial public offerings of Liftoff and Bob’s Discount Furniture served as canaries in the coal mine, proving that investor appetite for new issues has returned, provided they are built on solid fundamental ground.

The Great Unlocking: Synthesized Conclusions

The structural realignment of 2026 indicates that while we are seeing a next wave of exits, the nature of these exits has fundamentally changed. The market is moving from a period of recalibration toward constructive momentum, supported by rate stability and improving financing conditions.

Strategic Conclusions for Professional Peers

Success in this cycle is defined by the transition from experimentation to full-scale deployment of artificial intelligence. Enterprises are moving beyond isolated features toward reliable artificial intelligence at scale, which requires control planes and execution layers rather than just impressive demos. This maturity is forcing a shift in software economics:

Profitability and Efficiency: The rule of 40 has become the absolute law for valuation premiums. Companies with high growth but limited margins are no longer rewarded as they were in the pandemic era.

Strategic M&A over Public Markets: For the majority of software-as-a-service providers, strategic acquisition remains a more viable path than the initial public offering route, as public markets remain skeptical of traditional seat-based models.

The Dominance of Systems of Record: The winners in the next wave will be those who own the data layer. Artificial intelligence agents are transient, but the governed data sets they operate on represent the durable competitive advantage in 2026.

Secondary Market Maturity: Secondaries have evolved from a niche liquidity tool to a central component of the exit toolkit, essential for managing the record backlog of private equity-held companies.

In conclusion, the 2026 exit wave is a recalibration. It favors established, enterprise-focused businesses with durable revenue models and credible paths to profitability. While the Saas-pocalypse narrative highlights real risks to traditional seat-based models, it also creates opportunities for artificial intelligence-native challengers who can capture redirection in information technology spending. The narrative for 2026 is not one of software's decline, but of its evolution into the governed infrastructure that will power the next phase of the global digital economy. This environment rewards discipline, selectivity, and realistic valuation assumptions, setting the stage for a healthier, more sustainable exit cycle than the speculative frenzy of the previous era.

Protect Your Future: The Precision Vesting Calculator

Don't let a "handshake deal" complicate your exit. Map out your ownership journey with our Vesting Calculator

Calculate Your Vesting Schedule →