How Founders Raise Series A Funding in Canada

March 13, 2026 by Harshit Gupta

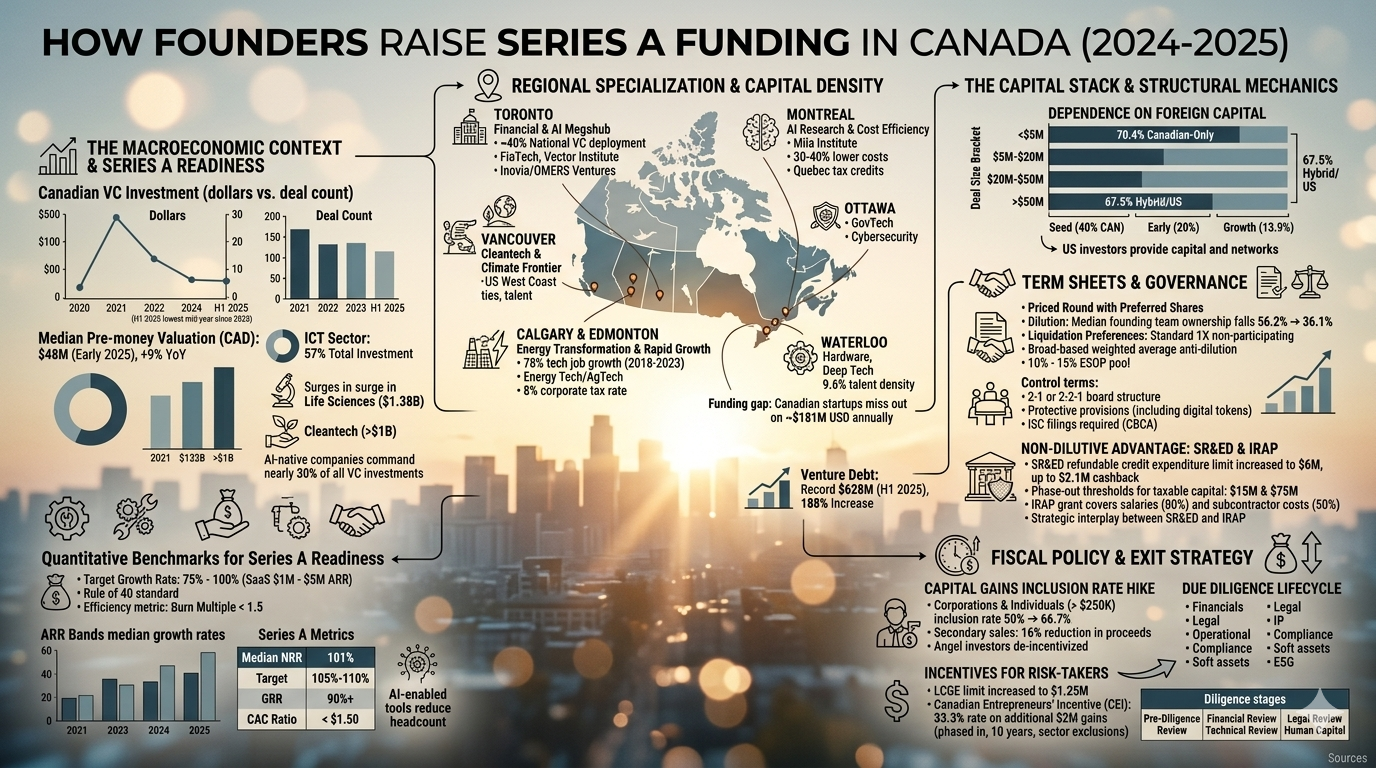

The Canadian venture capital landscape transitioned into a period of profound structural recalibration between 2024 and 2025, moving away from the exuberant valuation peaks of 2021 toward a more measured, efficiency-oriented deployment phase. This evolution is characterized by a "flight to quality," where institutional allocators prioritize sustainable business models and proven unit economics over the speculative top-line growth that defined the previous decade. While the total capital deployed in 2024 reached approximately $8.2 billion—a figure that signals underlying resilience by historical standards—the mechanics of the market reveal an environment that is increasingly selective, concentrated, and dependent on a few high-performance sectors.

In the first half of 2025, Canadian venture investment recorded its lowest mid-year total since 2020, with dollars invested down 26% year-over-year. This contraction reflects a broader stabilization trend seen globally, where "growth at any cost" has been replaced by "efficient growth" as the primary mandate for Series A readiness. For founders, the transition to Series A represents the most critical juncture in the startup lifecycle, serving as the bridge between early product-market validation and the aggressive scaling required to penetrate international markets.

The Macroeconomic Context: Market Dynamics 2024-2025

The Series A landscape in Canada is currently shaped by a paradox of rising valuations alongside falling deal counts. The median pre-money valuation for Series A rounds reached $48 million in early 2025, marking a 9% increase from the prior year, even as the number of closed rounds fell by 10%. This indicates that capital is gravitating toward a smaller cohort of "high-potential" startups that can demonstrate significant resilience. The average disclosed deal size in Q1 2024 was $10 million, a 47% increase from the previous year, though still 27% below the five-year average of $13.7 million. By the third quarter of 2024, the average deal size surged to $20.4 million, driven largely by late-stage transactions and a few record-breaking rounds, such as the $1.24 billion growth-stage investment in the legal-tech company Clio.

The Information and Communications Technology (ICT) sector remains the primary engine of the Canadian venture market, accounting for approximately 57% of total investment value. However, 2024 and 2025 saw a significant surge in Life Sciences, which reached $1.38 billion in 2024, and Cleantech, which secured over $1 billion. The emergence of Artificial Intelligence (AI) as a foundational layer has redefined sectoral boundaries; by late 2024, AI-native companies commanded nearly 30% of all venture investments, reflecting a global supercycle of innovation that has fundamentally altered investor expectations for productivity and efficiency.

Metric | 2024 Full Year | H1 2025 | Q3 2025 (YTD) |

Total VC Dollars Invested (CAD) | $8.2B - $8.5B | $2.9B | $4.9B |

Total VC Deal Count | 592 | 254 | 386 |

Average Deal Size (CAD) | $13.3M | ~$11.4M | $14.7M |

Top Performing Sector | ICT (57%) | Life Sciences (Resilient) | ICT (37% of PE, Lead VC) |

Mega-Deals ($50M+) | 24 | 7 | 9 (PE dominance) |

Sources:.

Strategic analysis suggests that the concentration of capital is reaching historical highs. In 2024, the top five venture funds captured 83% of all capital deployed. For founders, this means that the competitive landscape is not just about competing for customers, but for the attention of a diminishing pool of decision-makers. This "top-heavy" structure creates a consensus-driven investment environment, where warm introductions and deep network cultivation have become more critical than ever before.

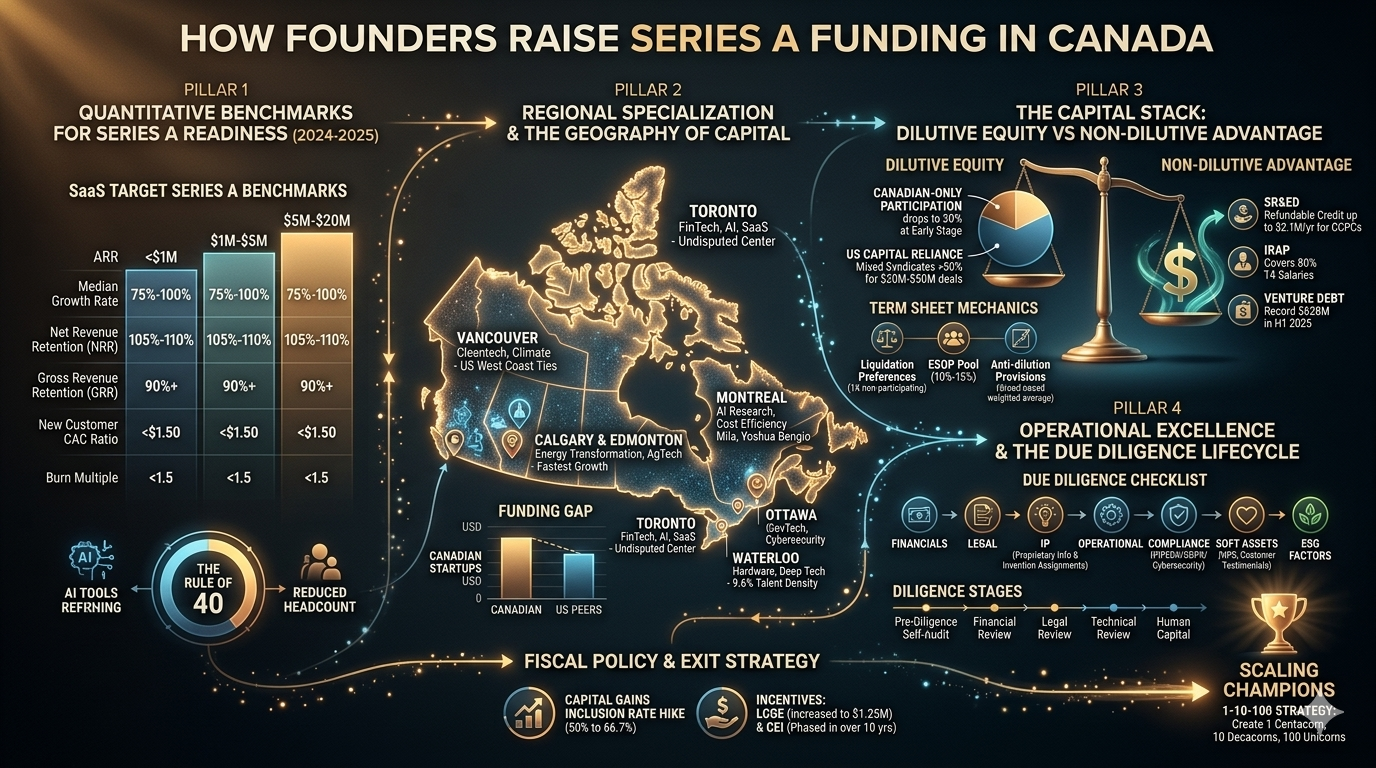

Quantitative Benchmarks for Series A Readiness

The definition of a "successful" Series A candidate has shifted toward companies that demonstrate both high growth and operational efficiency. The Rule of 40—the principle that a company's combined growth rate and profit margin should exceed 40%—has become a standard benchmark for venture-backed entities. While this metric is most commonly associated with companies at the $20 million to $50 million ARR range, investors are increasingly applying its components to Series A candidates.

For SaaS founders, the expectations for revenue growth have stabilized at lower levels compared to the 2021 boom. Median growth rates for companies in the $1 million to $5 million ARR band—the typical Series A sweet spot—were approximately 50% in 2024. However, the "top quartile" of companies in this segment are growing at 100% or more, creating a massive performance gap between average performers and "winners".

Metric | < $1M ARR | $1M - $5M ARR | $5M - $20M ARR | Target Series A Benchmarks |

Median Growth Rate | 100% | 50% | 30% | 75% - 100% |

Net Revenue Retention (NRR) | < 100% | 101% | 105% | 105% - 110% |

Gross Revenue Retention (GRR) | < 80% | 85% | 90% | 90%+ |

New Customer CAC Ratio | $1.76 | $1.76 | $1.85 | < $1.50 |

Burn Multiple | High | 1.5 - 2.0 | 1.0 - 1.5 | < 1.5 |

Sources:.

Efficiency is now scrutinized through the lens of the "Burn Multiple," which measures net cash burn against net new ARR. For a healthy Series A company, a Burn Multiple between 1.0 and 2.0 is considered "good," while a ratio below 1.0 is considered "great". This focus on capital efficiency is partly a reaction to the rising cost of customer acquisition. The median cost to acquire $1 of new ARR stood at $1.76 in 2023, while companies with the highest efficiency (top quartile) target $1.50 or lower. Founders who leverage AI-enabled tools to reduce headcount while maintaining growth are achieving the most significant gains; the median headcount for some high-growth early-stage businesses has reduced from 12 in 2023 to just 7 in 2024.

Retention metrics—specifically Net Revenue Retention (NRR) and Gross Revenue Retention (GRR)—serve as the primary indicators of product-market fit. NRR has faced downward pressure for three consecutive years, currently standing at a median of 101% for private SaaS companies. To command a premium Series A valuation, founders must demonstrate NRR in the 105% to 110% range, indicating that existing customers are not only staying but expanding their usage.

Regional Specialization and the Geography of Capital

The Canadian startup ecosystem is not a monolith but a collection of distinct regional hubs with specialized sectoral strengths and differing capital densities. Over 85% of venture capital deployment is concentrated in six primary cities: Toronto, Vancouver, Montreal, Calgary, Ottawa, and Waterloo.

Toronto: The Financial and AI Megahub

Toronto remains the undisputed center of gravity for Canadian venture capital, capturing approximately 40% of all national VC deployment. The city ranks fourth globally in several ecosystem indices and has positioned itself as the third-largest FinTech hub in North America after New York and San Francisco. The "Toronto-Waterloo Corridor" leverages the deep talent pools of world-class universities and the research output of institutions like the Vector Institute to dominate the AI and Enterprise SaaS sectors. Prominent firms like Inovia, Georgian, and OMERS Ventures are headquartered here, providing a mature infrastructure for Series A rounds.

Vancouver: The Cleantech and Climate Frontier

Vancouver has established itself as the primary destination for Cleantech and Climate Tech, attracting international talent focused on sustainability and ocean technology. While the city’s investor density lags behind Toronto, it benefits from strong cross-border ties with the US West Coast and a high quality of life that attracts senior engineering talent. However, Vancouver remains expensive, with operational costs nearing those of major US hubs.

Montreal: AI Research and Cost Efficiency

Montreal is a global powerhouse for AI and Machine Learning research, anchored by the Mila research institute and the influence of pioneers like Yoshua Bengio. The city captured 24% of all Canadian AI funding in 2024. Montreal offers a significant strategic advantage in terms of costs, which can be 30% to 40% lower than in Toronto. Furthermore, Quebec’s provincial tax credits are among the most generous in North America, making it an ideal location for capital-intensive R&D.

Calgary and Edmonton: Energy Transformation and Rapid Growth

Calgary has emerged as the fastest-growing tech hub in North America, with 78% tech job growth from 2018 to 2023. The city specializes in energy transformation, carbon capture, and agtech, leveraging its historical ties to the oil and gas industry. While Calgary still lacks the exit track record of Toronto (boasting only two active unicorns compared to Toronto's 10+), it offers the lowest corporate tax rate in Canada at 8% and a very low cost of doing business.

Hub | Global Ranking | Lead Sectors | Unique Advantage |

Toronto | #20 (#4 Emerging) | FinTech, AI, SaaS | Financial capital, high VC density |

Vancouver | #36 | Cleantech, Software | US West Coast ties, talent |

Montreal | #39 | AI, Gaming, Life Sciences | 30-40% lower costs than Toronto |

Calgary | Top 50 Emerging | Energy Tech, AgTech | Fastest tech growth, low tax (8%) |

Ottawa | Top 80 Emerging | GovTech, Cybersecurity | Proximity to federal agencies |

Waterloo | Part of Corridor | Hardware, Deep Tech | 9.6% tech talent density (highest) |

Sources:.

The regional data highlights a concerning trend: even in top-tier ecosystems like Toronto and Vancouver, "funding" remains the lowest-scoring metric in global rankings. This reflects the "early-stage funding gap," where Canadian startups miss out on approximately $181 million USD annually at the Series A level compared to US peers in comparable cities. This gap forces Canadian founders to look southward, with nearly half of all high-potential Canadian startups now headquartered in the US.

The Role of US Capital and Cross-Border Syndication

The Canadian venture ecosystem is heavily dependent on foreign capital, particularly as deal sizes increase beyond the seed stage. While Canadian-only investor syndicates fuel 70.4% of rounds under $5 million, their participation drops precipitously for larger checks. For rounds between $20 million and $50 million—the range of a robust Series A or Series B—mixed syndicates involving both Canadian and US investors participate in nearly 60% of all deals.

Deal Size Bracket | Canadian-Only Participation | Hybrid (CAN + US) Participation |

< $5M | 70.4% | 16.5% |

$5M - $20M | 39.9% | 39.3% |

$20M - $50M | 25.0% | 59.9% |

> $50M | 12.7% | 67.5% |

Sources:.

This trend is mirrored at the lifecycle stage level. At the seed stage, Canadian-only participation is 40%, but this falls to 20% at the early stage (A and B rounds) and just 13.9% at the growth stage. The involvement of US investors is strategic; they provide not only capital but also the "inroads" and networks required to capture the US market, which is often 10x the size of the Canadian market.

However, this reliance on US capital creates a "wealth generation gap." When Canadian companies exit via M&A or IPO, a significant share of the generated value leaves the country. Furthermore, the dominance of foreign capital has led to a "consensus" investment model, where even the largest Canadian pension funds, like CPPIB, often wait for a US GP (General Partner) to lead a round before they participate. This has prompted calls for the establishment of a "Canadian Prosperity Fund"—a government-backed entity that could write $50 million to $500 million checks to support domestic scale-ups.

Historical data shows that Canadian investors are most active in US seed rounds but withdraw from the US market during periods of global uncertainty, such as the 2020 pandemic or the 2024-2025 trade tensions. This "inward orientation" during crises suggests that domestic capital is more reliable for early-stage survival, while US capital is the essential fuel for late-stage dominance.

Structural Mechanics: Term Sheets and Governance in Series A

Raising a Series A round in Canada typically involves transitioning from a Common Share structure or SAFEs to a "Priced Round" using Preferred Shares. A term sheet is the preliminary, non-binding document that outlines the economic and control terms of the investment. In Canada, 98.3% of venture financings now use standardized model documents aligned with the CVCA or NVCA, which ensures a predictable legal framework for both founders and investors.

Economic Terms

The most critical economic metric is the valuation, which is expressed on a pre-money or post-money basis. A typical Series A round in 2024-2025 involves significant dilution; the median founding team ownership falls from 56.2% after a seed round to 36.1% at Series A.

Liquidation Preferences: This provision dictates how proceeds are distributed upon an exit. The standard is a 1X non-participating preference, meaning the investor receives their original investment back before common shareholders receive anything.

Anti-dilution Provisions: These protect investors if the company raises a subsequent round at a lower price per share (a "down round"). Broad-based weighted average anti-dilution is the most common standard in founder-friendly deals.

Employee Stock Option Pool (ESOP): Investors usually require the creation or "topping up" of an ESOP pool representing 10% to 15% of the post-money capitalization to attract future talent.

Control and Governance Terms

Control terms define the power dynamics between the board of directors and the management team.

Board Representation: A "2-1" structure (two founder seats, one investor seat) is considered founder-friendly, while a "2-2-1" structure (two founders, two investors, and one independent) is common for larger Series A rounds.

Protective Provisions: These are specific actions that require the consent of the preferred shareholders, such as selling the company, issuing a new class of shares, or changing the primary business line. Modern term sheets now often include protections against issuing digital tokens or blockchain-based assets without consent.

Individual with Significant Control (ISC) Filings: Under the Canada Business Corporations Act (CBCA), corporations must now file information on individuals who own or control at least 25% of the shares or voting rights. This requirement is integrated into the annual filing process and is a key compliance item during due diligence.

Third-order analysis of governance suggests that term sheets set the precedent for all future rounds. If a founder accepts aggressive terms (e.g., full participation or multiple liquidation preferences) at Series A, they create a "negative compounding effect," as subsequent investors will expect at least the same level of protection.

The Non-Dilutive Advantage: SR&ED and IRAP

One of Canada’s most potent competitive advantages for early-stage founders is the robust availability of non-dilutive capital, primarily through the Scientific Research and Experimental Development (SR&ED) tax incentive and the Industrial Research Assistance Program (IRAP). These programs allow founders to extend their runway without additional equity dilution, a factor that effectively reduces the "burn rate" by a third or more.

The SR&ED Program

SR&ED is the largest source of government-funded support for R&D in Canada. It is an entitlement-based program, meaning if the work qualifies, the credit must be issued. For Canadian-controlled private corporations (CCPCs), SR&ED offers a 35% refundable tax credit on eligible expenditures, including salaries, contractor costs, and materials.

In 2025, the government implemented key enhancements to SR&ED to support scaling businesses. The Enhanced Refundable Credit expenditure limit was increased from $3 million to $6 million. This means a qualifying startup can now receive up to $2.1 million in cash back per year on their R&D spend. Additionally, the phase-out thresholds for taxable capital were raised to $15 million and $75 million, allowing larger "scale-ups" to retain access to these credits for longer.

The IRAP Grant

Managed by the National Research Council (NRC), IRAP is a grant-based program that requires a formal proposal before the project begins. IRAP covers 80% of internal T4 salaries and 50% of subcontractor costs for technology innovation projects. Grants can range from $50,000 for small projects to $10 million for mid-sized technology innovation.

The strategic interplay between SR&ED and IRAP is crucial. While a founder cannot "double dip" on the same dollar, IRAP and SR&ED are complementary. For example, if a company has $100,000 in R&D salaries and IRAP covers $80,000, the company can still claim the remaining $20,000 of salary plus the 55% "overhead proxy" under SR&ED. This combined approach maximizes the total capital recovered from the government, often exceeding 50% of the total R&D budget.

Venture Debt: A New Record in 2025

Venture debt has emerged as a significant component of the Series A capital stack in Canada. In the first half of 2025, venture debt reached a record $628 million, a 188% increase over the previous year. This growth is driven by founders who want to avoid the 17.9% to 20.9% dilution typical of Series A rounds or who are using debt to "bridge" to a larger round during a period of valuation compression.

Fiscal Policy and the Founder’s Exit Strategy

The fiscal environment in 2024 and 2025 introduced significant changes to the taxation of capital gains, which directly impacts founder liquidity and the attractiveness of secondary sales during a Series A round.

Capital Gains Inclusion Rate Hike

The 2024 Federal Budget proposed increasing the capital gains inclusion rate from 50% to 66.7% for corporations and for individuals on gains exceeding $250,000 annually. This change, while facing political opposition, has been administered by the CRA since June 25, 2024. For a SaaS founder looking to sell shares in a secondary transaction (taking "money off the table"), this effectively represents a 16% reduction in take-home proceeds. Analysts suggest this creates a "timing risk," where founders may feel pressured to raise capital or sell portions of their business before the tax changes are fully solidified or further increased.

Incentives for Risk-Takers

To mitigate the impact of the inclusion rate hike, the government enhanced two key incentives:

Lifetime Capital Gains Exemption (LCGE): The LCGE limit for qualified small business corporation shares was increased to $1.25 million in June 2024. This provides 100% tax-free treatment for the first $1.25 million of gains, a significant benefit for early-stage founders.

Canadian Entrepreneurs' Incentive (CEI): This new incentive reduces the inclusion rate to 33.3% on an additional $2 million of capital gains for "eligible" entrepreneurs. However, the CEI is phased in over ten years ($200,000 per year) and excludes certain sectors like finance and professional services, which may limit its utility for some tech founders.

Third-order psychological analysis reveals that these tax changes have sent a "chill" through the angel investor community. High-net-worth individuals (HNWIs) and angel investors, who typically fund the "pre-Series A" pipeline, are being de-incentivized from taking high-risk early-stage bets. This could lead to a "hollowed-out" pipeline in 2026 and 2027, as fewer companies receive the seed funding necessary to eventually reach Series A maturity.

Operational Excellence and the Due Diligence Lifecycle

In a "cautious and selective" investor market, the due diligence process for a Series A round has become more rigorous and exhaustive. Investors are focusing on "hard due diligence"—the quantifiable facts—as well as "soft due diligence"—the intangible aspects of culture and leadership.

The Due Diligence Checklist

A professional Series A data room must contain a comprehensive set of documents across seven key areas :

Financials: Three years of audited financial statements, a detailed cap table, and financial projections that include both short-term monthly and long-term 5-year forecasts.

Legal: Material contracts with customers and vendors, board minutes, and regulatory compliance filings.

Intellectual Property: A detailed inventory of patents, trademarks, and, crucially, proprietary information and invention assignment agreements signed by all employees and consultants.

Operational: Organizational charts, senior management bios, and internal control policies.

Compliance: Modern-day compliance policies related to data privacy (PIPEDA/GDPR), cybersecurity, and inclusive hiring practices.

Soft Assets: Customer testimonials, net promoter scores (NPS), and evidence of brand reputation.

ESG Factors: 80% of investors are now embedding environmental, social, and governance factors into their strategy, requiring founders to demonstrate a commitment to ethical business practices.

Diligence Stage | Primary Goal | Key Deliverable |

Pre-Diligence | Self-Audit | Cleaned up cap table and IP assignments |

Financial Review | Validate Growth/Unit Economics | LTV/CAC analysis and 5-year model |

Legal Review | Identify Structural Risks | Material contract analysis and CBCA compliance |

Technical Review | Assess Scalability/Security | Code audit and cybersecurity protocols |

Human Capital | Evaluate Leadership Depth | Management interviews and culture assessment |

Sources:.

Founders are encouraged to use automated accounting systems and virtual data rooms that facilitate "pattern recognition"—allowing investors to quickly identify risks or opportunities in large datasets. Being "slow to respond" to due diligence requests is one of the primary reasons for deal fatigue, which can lead to a withdrawal of the term sheet.

Conclusion: The Path Toward Scaling Champions

The Canadian Series A landscape is currently at a critical inflection point. While the country continues to produce world-class research and a steady stream of early-stage startups, it faces a "scaling gap" that prevents many of these companies from reaching $100 million+ revenue targets. This gap is driven by a lack of late-stage domestic capital, a small internal market, and a corporate risk-aversion that prevents Canadian enterprises from being the "first customers" for domestic tech.

To bridge this gap, national strategy must shift toward "concentrating resources on winners". This includes the "1-10-100" strategy: a goal to create 1 centacorn ($100B), 10 decacorns ($10B), and 100 unicorns ($1B) over the next decade. Achieving this will require a "Buy Red" mindset where federal procurement is used as a lever for growth, alongside a tax environment that is globally competitive with the US QSBS system.

For the Series A founder, the 2024-2025 market is a "study in contrasts". It is an environment where capital is available for those who can prove efficiency, where non-dilutive incentives like SR&ED and IRAP provide a unique safety net, and where regional hubs are developing deep sectoral expertise. However, it is also a market where the "bar" for entry is higher than ever, and where the strategic decision to remain in Canada or flip to the US must be weighed against a complex backdrop of shifting tax policies and foreign capital dominance. Success in this landscape requires more than just a great product; it requires the strategic orchestration of capital, legal rigor, and operational excellence.

Read More -

1. From Idea to MVP: A Step-by-Step Guide for Solo Founder

🔗 https://findnstart.com/blogs/from-idea-to-mvp-a-step-by-step-guide-for-solo-founder

2. How to Validate Your Startup Idea in 48 Hours for $0

🔗 https://findnstart.com/blogs/how-to-validate-your-startup-idea-in-48-hours-for-0

3. Remote vs. Local: Does Your Co-Founder Need to Live in the Same City?

🔗 https://findnstart.com/blogs/remote-vs-local-does-your-co-founder-need-to-live-in-the-same-city

4. The 2026 Startup Landscape: What Has Fundamentally Changed (and Why Founder Skills Matter More Than Ever)

5. The Most In-Demand Skills for Startup Founders in 2026

🔗 https://findnstart.com/blogs/the-most-in-demand-skills-for-startup-founders-in-2026

6. How to Find a Technical Co-Founder (Without a Six-Figure Salary)

🔗 https://findnstart.com/blogs/how-to-find-a-technical-co-founder-without-a-six-figure-salary

7. 5 Red Flags to Look for When Choosing a Startup Partner

🔗 https://findnstart.com/blogs/5-red-flags-to-look-for-when-choosing-a-startup-partner

8. How to Pitch Your Idea to Potential Co-Founders

🔗 https://findnstart.com/blogs/how-to-pitch-your-idea-to-potential-co-founders

9. How to Build a Portfolio that Attracts High-Growth Startup Founders

🔗 https://findnstart.com/blogs/how-to-build-a-portfolio-that-attracts-high-growth-startup-founders

10. Equity vs. Salary: How to Split Ownership with Your First Teammate

🔗 https://findnstart.com/blogs/equity-vs-salary-how-to-split-ownership-with-your-first-teammate

11. Why Joining an Early-Stage Startup is Better Than a Corporate Job

🔗 https://findnstart.com/blogs/why-joining-an-early-stage-startup-is-better-than-a-corporate-job

12. The Future of EdTech: Why Developers and Educators Need to Team Up Now

🔗 https://findnstart.com/blogs/the-future-of-edtech-why-developers-and-educators-need-to-team-up-now

13. The Architecture of Symbiosis: Analytical Perspectives on the Five Habits of Successful Startup Duos

14. Finding a Co-Founder in the AI Space: What Skills Should You Look For?

🔗 https://findnstart.com/blogs/finding-a-co-founder-in-the-ai-space-what-skills-should-you-look-for

15. Overcoming Analysis Paralysis and the Strategic Path to Execution

🔗 https://findnstart.com/blogs/overcoming-analysis-paralysis-and-the-strategic-path-to-execution

16. From College Project to Company: How to Find Your Student Co-Founder

🔗 https://findnstart.com/blogs/from-college-project-to-company-how-to-find-your-student-co-founder

17. How to Start a Startup While Working a Full-Time Job

🔗 https://findnstart.com/blogs/how-to-start-a-startup-while-working-a-full-time-job

18. How to Build a HealthTech Startup Without a Medical Degree

🔗 https://findnstart.com/blogs/how-to-build-a-healthtech-startup-without-a-medical-degree

19. The Solitary Architect: Executive Isolation in Entrepreneurship

20. The 2026 Guide to Launching a SaaS as a Solo Developer

21. What Sustainable Growth Actually Looks Like

🔗 https://findnstart.com/blogs/what-sustainable-growth-actually-looks-like

22. The Early Warning Signs Your Startup Is in Trouble

🔗 https://findnstart.com/blogs/the-early-warning-signs-your-startup-is-in-trouble

23. How to Grow Without Burning Out

🔗 https://findnstart.com/blogs/how-to-grow-without-burning-out

24. The Truth About “Runway” Most Founders Ignore

🔗 https://findnstart.com/blogs/the-truth-about-runway-most-founders-ignore

25. Revenue Solves More Problems Than Funding

🔗 https://findnstart.com/blogs/revenue-solves-more-problems-than-funding

26. What No One Tells You About Being a Solo Founder

🔗 https://findnstart.com/blogs/what-no-one-tells-you-about-being-a-solo-founder

27. Why Smart People Quit High-Paying Jobs to Build Startups (And Why Most Regret It)

28. Why Most Startup Advice on Twitter Is Dangerous

🔗 https://findnstart.com/blogs/why-most-startup-advice-on-twitter-is-dangerous

29. Decision Fatigue: The Silent Startup Killer

🔗 https://findnstart.com/blogs/decision-fatigue-the-silent-startup-killer

30. Fear vs Logic: How Founders Actually Make Decisions

🔗 https://findnstart.com/blogs/fear-vs-logic-how-founders-actually-make-decisions

31. How Overthinking Destroys Early Momentum

🔗 https://findnstart.com/blogs/how-overthinking-destroys-early-momentum

32. Ideas Don’t Scale. Systems Do.

🔗 https://findnstart.com/blogs/ideas-dont-scale-systems-do

33. The First Hire That Actually Matters

🔗 https://findnstart.com/blogs/the-first-hire-that-actually-matters

34. How the First 100 Users Decide Your Startup’s Fate

🔗 https://findnstart.com/blogs/how-the-first-100-users-decide-your-startups-fate

35. Why Your Startup Doesn’t Need Growth — It Needs Focus

🔗 https://findnstart.com/blogs/why-your-startup-doesnt-need-growthit-needs-focus

36. Why Most Startups Die Quietly

🔗 https://findnstart.com/blogs/why-most-startups-die-quietly

37. Lessons Learned Too Late by First-Time Founders

🔗 https://findnstart.com/blogs/lessons-learned-too-late-by-first-time-founders

38. The Myth of the “Overnight Success” Startup

🔗 https://findnstart.com/blogs/the-myth-of-the-overnight-success-startup