Fintech 2.0 in Bangalore

March 9, 2026 by Harshit Gupta

The financial technology landscape in Bangalore has transcended the initial phase of digitization to enter a more sophisticated, autonomous, and integrated era known as Fintech 2.0. This evolution represents a fundamental shift from fintech as a vertical sector—characterized by standalone apps for payments or lending—to fintech as a horizontal infrastructure that permeates every aspect of the digital economy. Bangalore, as the primary engine of India’s technological advancement, has become the global laboratory for this transition, leveraging its unique density of engineering talent, mature venture capital networks, and a world-class digital public infrastructure (DPI) known as the India Stack. By 2026, the city’s ecosystem has consolidated its status as a leading global fintech node, ranking third globally in funding and first in India for innovation density.

The Conceptual Framework of Fintech 2.0

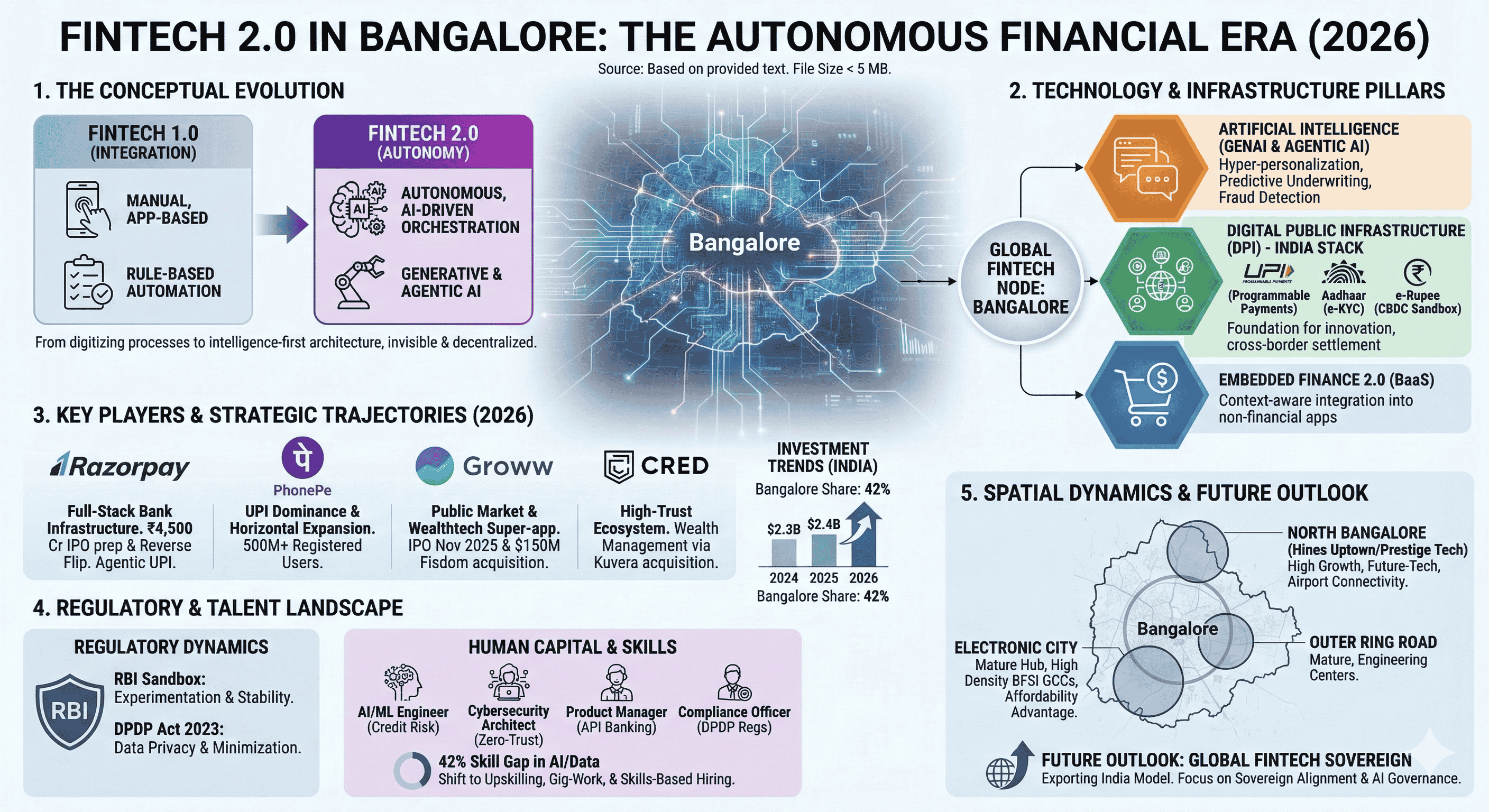

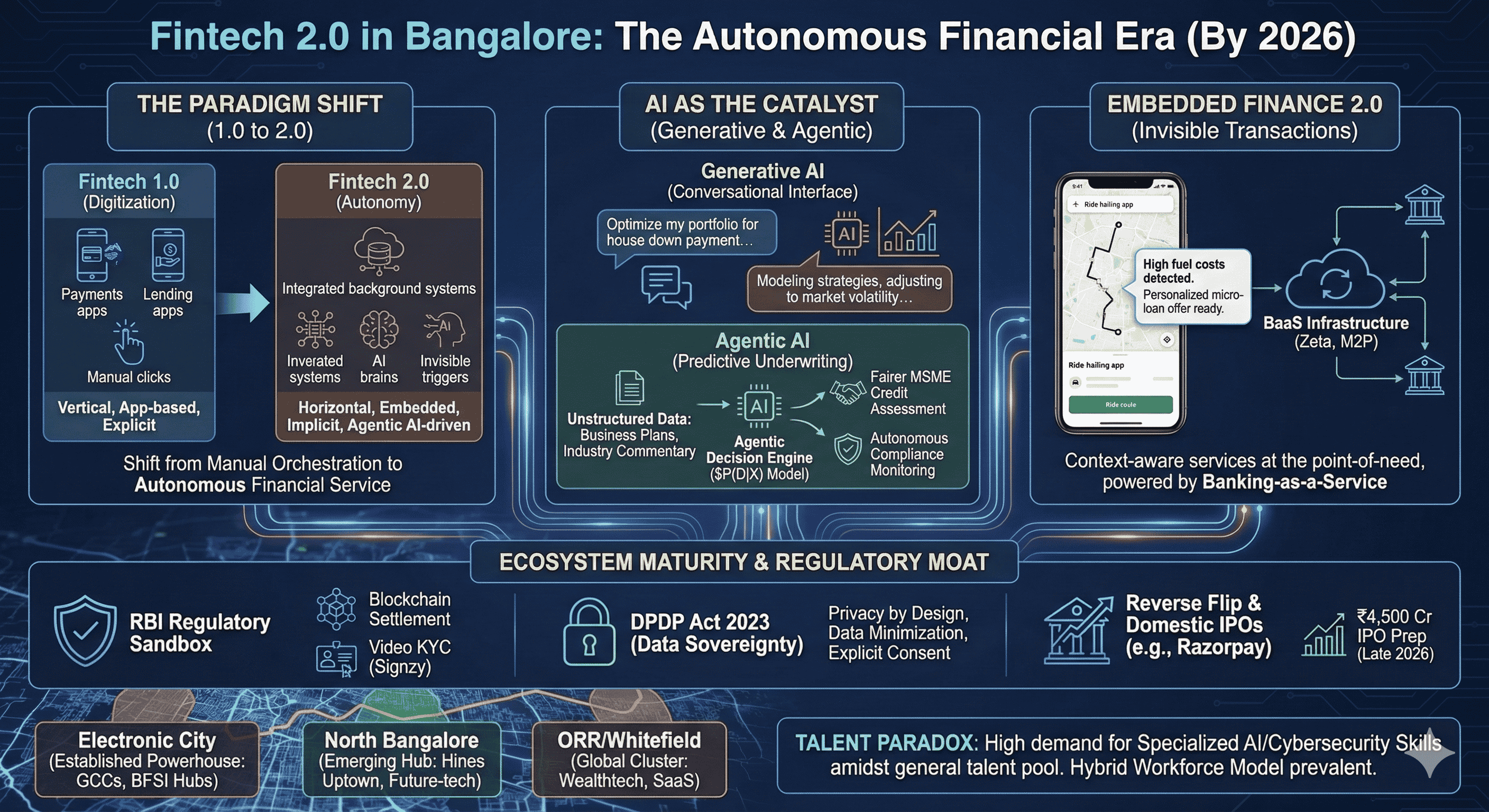

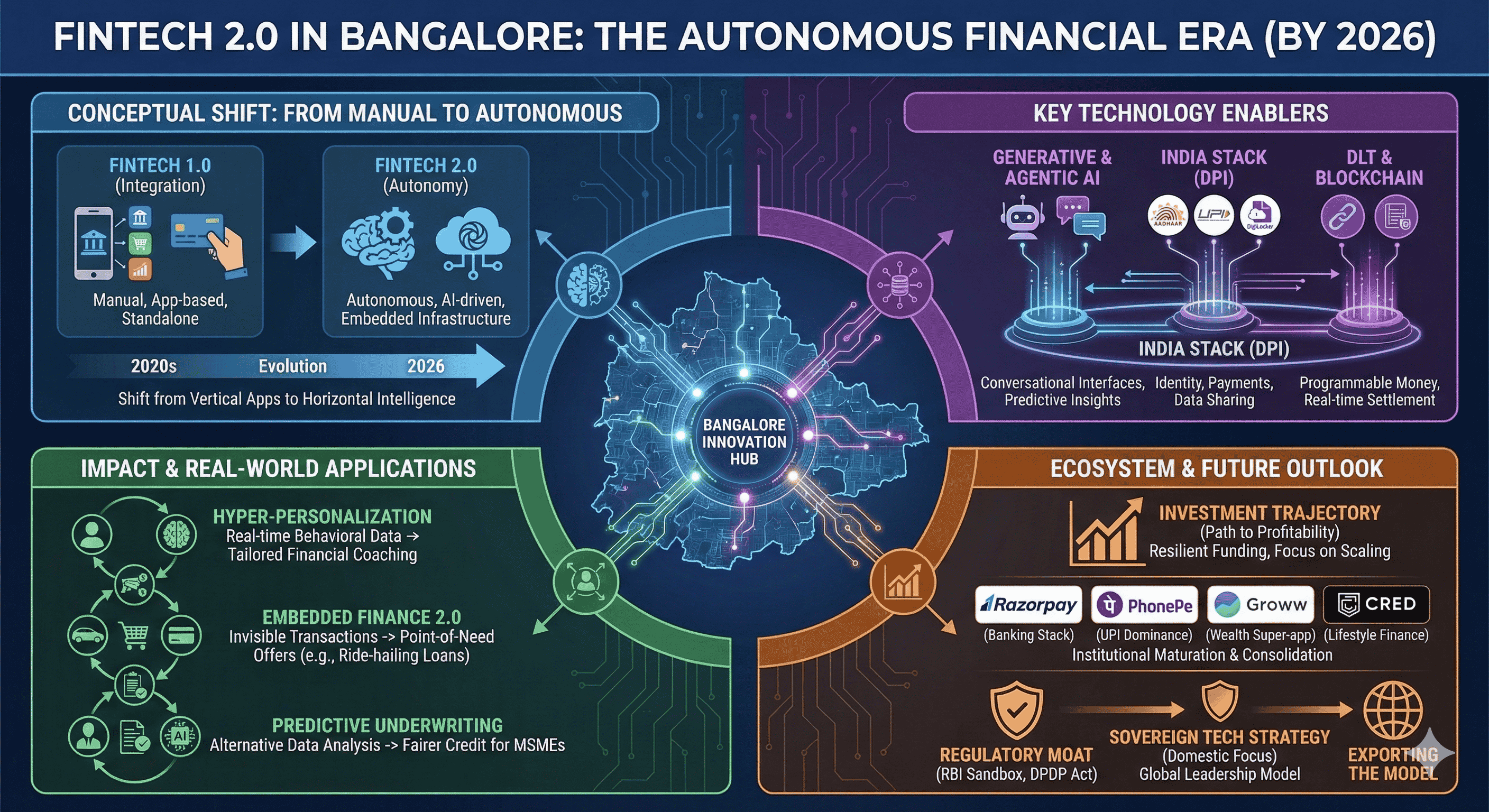

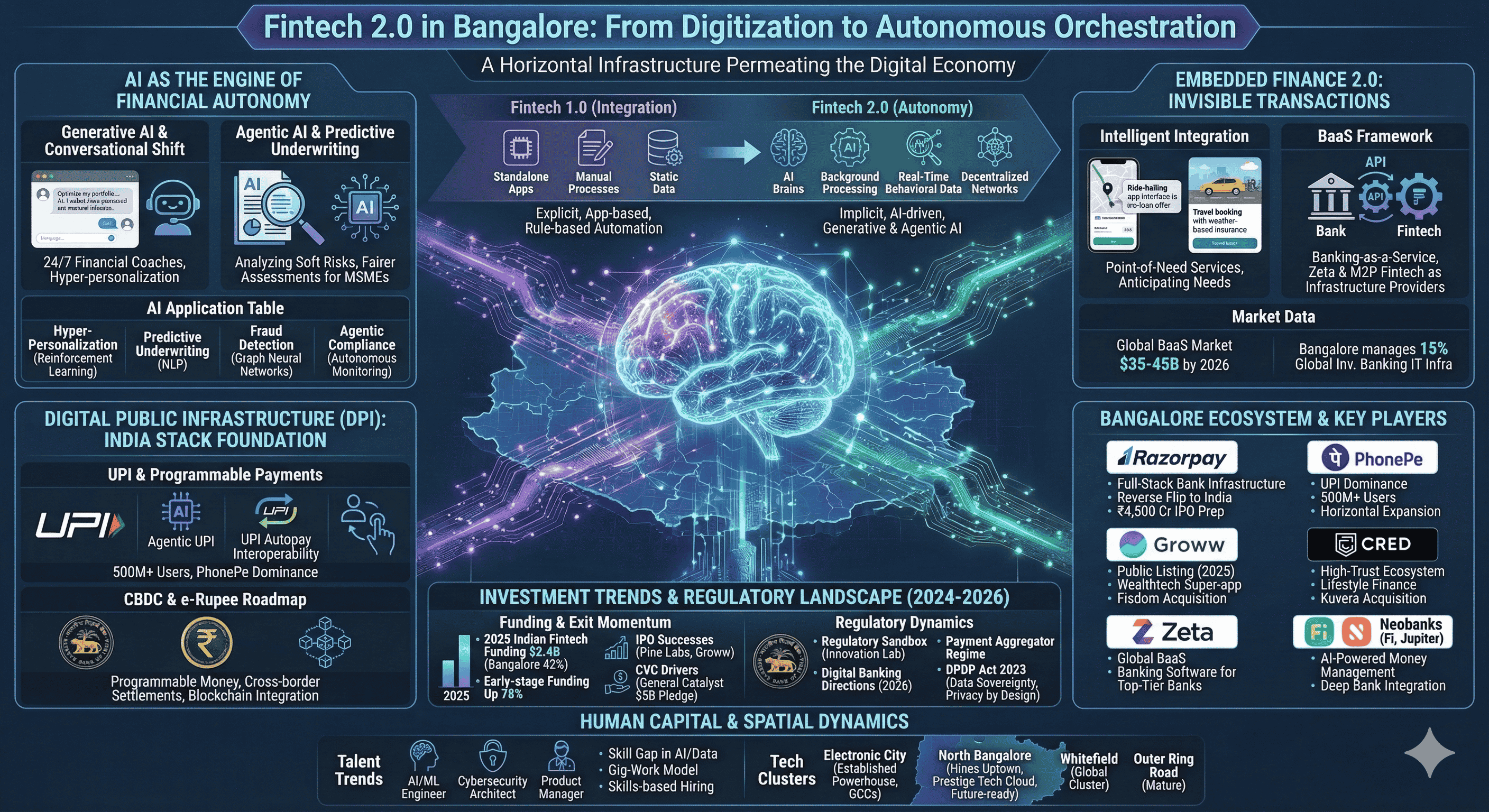

The transition to Fintech 2.0 is defined by the move from manual, user-initiated transactions to autonomous, AI-driven financial orchestration. In the era of Fintech 1.0, the focus was primarily on the "digitization" of existing banking processes—moving bank branches to mobile apps and paper checks to digital wallets. Fintech 2.0, however, is characterized by "intelligence-first" architecture. Here, financial services are not just integrated into platforms; they are context-aware and self-managing.

The core attributes of this new paradigm include hyper-personalization, where services are tailored to the individual’s real-time behavioral data; invisibility, where financial interactions occur seamlessly in the background of non-financial activities; and decentralization, where blockchain-based settlement rails provide programmable, immutable transaction layers. The underlying philosophy suggests that the most successful financial service is one that the user does not have to think about.

Attribute | Fintech 1.0 (Integration) | Fintech 2.0 (Autonomy) |

User Interaction | Explicit, manual, app-based | Implicit, autonomous, background-managed |

Data Utilization | Historical, static bureau scores | Real-time, behavioral, alternative data |

Service Model | Vertical (Standalone apps) | Horizontal (Embedded infrastructure) |

Intelligence | Rule-based automation | Generative and Agentic AI |

Trust Model | Institutional/Brand-based | Algorithmic/DPI-based |

This shift is driven by the convergence of several technology stacks: Generative AI (GenAI), which provides human-centric interfaces and predictive insights; Distributed Ledger Technology (DLT), which enables real-time, cross-border settlements; and open API frameworks, which allow for the seamless flow of data between disparate systems.

Artificial Intelligence as the Engine of Financial Autonomy

Artificial Intelligence is the primary catalyst transforming Bangalore's fintech firms from service providers into autonomous orchestrators. The deployment of AI has moved beyond simple fraud detection or chatbots to encompass complex decision-making processes in credit underwriting, wealth management, and regulatory compliance.

Generative AI and the Conversational Shift

In 2026, Generative AI has redefined the interface between consumers and their capital. Traditional banking apps, which required users to navigate complex menus, have been replaced by conversational interfaces that understand natural language and context. These systems act as 24/7 financial coaches, analyzing spending patterns to identify savings opportunities or preemptively warning users of potential shortfalls based on upcoming bills.

For example, a user in Bangalore might interact with a neobank assistant to "optimize my portfolio for a house down payment in three years." The AI does not just provide a list of funds; it continuously models and adjusts investment strategies using reinforcement learning, reacting to market volatility and changes in the user's income without further prompting. This democratization of high-touch wealth management is a hallmark of Fintech 2.0, making sophisticated financial planning accessible to the mass market.

Agentic AI and Predictive Underwriting

The emergence of Agentic AI—systems that can independently make decisions and complete tasks—is revolutionizing B2B fintech and credit markets. In credit decisioning, GenAI decision engines now analyze unstructured data, such as business plan narratives, regulatory filings, and industry commentary, alongside traditional structured data like bank statements. This allows lenders to assess "soft" risks, such as revenue concentration or management quality, which are often missed by traditional scoring models.

The technical mechanism involves $P(D|X)$, where the probability of default $D$ is conditioned on a high-dimensional vector $X$ that includes digital footprints and real-time cash flow patterns. In Bangalore, firms are increasingly using these models to serve the MSME (Micro, Small, and Medium Enterprises) sector, providing "fairer" assessments for businesses that lack long-term credit histories but show strong real-time transactional health.

AI Application | Mechanism | Strategic Impact in Bangalore |

Hyper-Personalization | Reinforcement learning on spending data | Increased customer retention and "wallet share" |

Predictive Underwriting | NLP on business plans and GST data | Expansion of credit to "thin-file" borrowers |

Fraud Detection | Real-time graph neural networks | Reduction in false positives and unauthorized transactions |

Agentic Compliance | Autonomous monitoring of regulatory shifts | Lower operational costs and regulatory risk |

Embedded Finance 2.0: The Invisibility of Transactions

Embedded Finance 2.0 (EF2) represents the stage where financial services become context-aware and deeply integrated into daily routines. If Embedded Finance 1.0 was about "plugging in" a payment button, 2.0 is about "embedding intelligence". In Bangalore’s thriving digital economy, this manifests in platforms that anticipate needs.

Mechanisms of Intelligent Integration

The evolution of EF2 is visible in non-financial apps such as ride-hailing, food delivery, and e-commerce. For instance, a driver on a ride-hailing platform may receive a personalized micro-loan offer exactly when the app detects a pattern of high fuel costs and low daily earnings, or a traveler booking a flight might be offered insurance tailored to the specific weather patterns of their destination.

This "point-of-need" service model is supported by the Banking-as-a-Service (BaaS) framework, where traditional banks provide the balance sheet while fintechs provide the technology layer. Bangalore-based companies like Zeta and M2P Fintech have become the dominant infrastructure providers for this shift, allowing enterprises to become "fintech-enabled" without obtaining their own banking licenses.

Economic Implications for Businesses and Consumers

For businesses, EF2 provides a powerful mechanism for monetization and customer loyalty. By offering financial services directly within their ecosystems, non-financial companies can capture a greater portion of the customer's lifetime value. For consumers, the primary benefit is the reduction of friction. Financial services are no longer a separate destination but a feature of the experience they are already having.

The global BaaS market, which powers these experiences, is projected to reach $35–45 billion by 2026. Bangalore’s role as a provider of the "plumbing" for this global market cannot be overstated. With 15% of global investment banking IT infrastructure managed directly from the city, Bangalore has become the back-office and innovation lab for the world’s largest financial institutions.

Digital Public Infrastructure: The Foundation of the India Stack

The success of Fintech 2.0 in Bangalore is inseparable from India's Digital Public Infrastructure (DPI). The integration of UPI, Aadhaar, e-KYC, and DigiLocker has created a fertile environment for innovation that is unrivaled globally.

The Evolution of UPI and Programmable Payments

The Unified Payments Interface (UPI) has transitioned from a peer-to-peer transfer tool to a sophisticated payment ecosystem. By 2026, UPI leads transactions for over 500 million registered users, with Bangalore-based PhonePe maintaining a dominant market share. A key innovation in the Fintech 2.0 era is the introduction of "Agentic UPI" payments. In early 2026, Razorpay and NPCI debuted agentic payments for AI assistants, allowing AI entities to execute transactions on behalf of users within predefined limits.

Furthermore, the introduction of UPI Autopay Interoperability allows businesses to manage mandates across different banks and aggregators, significantly increasing the success rates of recurring payments—a critical requirement for the subscription-based SaaS economy in Bangalore.

CBDC and the e-Rupee Roadmap

The Reserve Bank of India’s (RBI) retail Central Bank Digital Currency (CBDC) sandbox has seen significant expansion in 2026. This infrastructure enables "programmable money," where funds can be tagged for specific purposes—such as agricultural subsidies that can only be spent on fertilizers or corporate expense accounts that only work at designated vendors.

For Bangalore’s fintechs, the e-rupee sandbox provides a playground for testing wallet integrations and cross-border settlement solutions. Blockchain-based services, once relegated to the periphery, are being embedded into mainstream apps to facilitate real-time, low-cost international transactions, bypassing the inefficiencies of the traditional SWIFT network.

The Institutional Vanguard: Key Players and Their Trajectories

The Bangalore fintech ecosystem is a dense network of homegrown unicorns, global financial giants, and agile startups. The institutional maturation of the city is best exemplified by the evolving strategies of its lead entities.

Razorpay: From Gateway to Full-Stack Bank Infrastructure

Razorpay has moved far beyond its origins as a payment gateway to become a systemic orchestrator of India’s financial infrastructure. Its "Banking Stack," launched at the Global Fintech Fest 2025, provides banks with high-uptime, intelligent POS systems and biometric card authentication. Razorpay’s decision to move its headquarters from the US back to India (the "reverse flip") and its subsequent preparation for a ₹4,500 crore IPO in late 2026 signal the long-term confidence in the Indian regulatory and public market environment.

The firm's revenue growth reflects this expansion, with FY25 revenue surging 65% to ₹3,783 crore, driven by its RazorpayX banking platform and POS services. The acquisition of a majority stake in POP UPI and the securing of a cross-border payment aggregator license further solidify its position as a multi-dimensional financial powerhouse.

Growth and Consolidation: PhonePe, Groww, and CRED

The trend toward consolidation is a defining feature of the 2025-2026 period. Groww, which listed publicly in late 2025, became one of the first digital-first brokers to reach the public markets, following a $202 million Series F raise. Its acquisition of Fisdom for $150 million was the largest deal of the year, highlighting the shift toward building comprehensive wealth management "super-apps".

PhonePe continues to lead in transaction volume, leveraging its elite engineering talent to redefine digital payments and investing. CRED, meanwhile, has expanded its members-only ecosystem to include rent payments and wealth management, recently acquiring the platform Kuvera to bolster its offerings.

Company | Core 2.0 Strategy | Key Milestone (2025-2026) |

Razorpay | Banking infrastructure & Agentic UPI | ₹4,500 Cr IPO preparation & Reverse Flip |

Groww | Public market expansion & Wealthtech | IPO in Nov 2025 & $150M Fisdom acquisition |

PhonePe | UPI dominance & Horizontal expansion | 500 million+ registered users |

CRED | High-trust ecosystem & Lifestyle finance | Acquisition of Kuvera for wealth management |

Zeta | Global BaaS & Banking software | Core infrastructure provider for top-tier banks |

The Neobank Landscape: Fi and Jupiter

Neobanks like Fi and Jupiter Money have successfully moved into the Fintech 2.0 era by focusing on deep integration with traditional partners like Federal Bank. These platforms distinguish themselves through AI-powered money management tools that feel "almost human," providing users with insights into their spending habits through plain-language commands.

Investment Trends and the Capital Cycle (2024-2026)

The funding environment for Bangalore’s fintech sector has transitioned from the "growth-at-all-costs" mindset of the early 2020s to a "path-to-profitability" model in 2026. While global fintech investment saw a decline in deal volume, the total capital deployed in India showed a resilient upward trajectory.

Resurgence of Funding and Exit Momentum

In 2025, Indian fintech funding rose 2% year-on-year to $2.4 billion, with Bangalore capturing 42% of the total. A significant shift occurred in the distribution of this capital: early-stage funding (Series A and B) soared by 78% to $1.2 billion, while seed funding saw a 40% decline. This suggests that investors are increasingly focused on scaling proven, product-led businesses rather than betting on unproven early concepts.

The "exit environment" has also improved significantly. The successful IPOs of mature firms like Pine Labs and Groww have provided the liquidity necessary to reinvigorate the private markets. Venture capital participating activity rose to $29.7 billion globally in 2025, up from $20.9 billion in 2024, with a strong focus on digital assets and AI-native platforms.

Institutional and Corporate Venture Capital

Corporate venture capital (CVC) has become a major driver of the ecosystem. Firms like General Catalyst have pledged $5 billion to the Indian tech ecosystem over the five years starting in 2026, with a significant portion expected to flow into Bangalore’s fintech and deep-tech sectors. This institutional backing provides a "signal" to the market that Bangalore’s fintech models are not just locally viable but globally scalable.

Metric | 2024 (Actual) | 2025 (Actual) | 2026 (Projected/Trend) |

Total Fintech Funding (India) | $2.3 Billion | $2.4 Billion | Upward Trajectory |

Bangalore Share of Funding | 42% | 42% | Maintaining Dominance |

Average Fintech Deal Size | $22 Million | Increasing (Lesser rounds, more capital) | Focus on Mega-deals |

New Unicorns in India | 2 | 3 | Stability in Value Creation |

Global Ranking (Funding) | 3rd | 3rd | Consolidating Position |

Regulatory Dynamics and the Compliance Moat

In Fintech 2.0, regulation is no longer viewed as a hurdle but as a "competitive moat." The Reserve Bank of India (RBI) has led the world in creating a "risk-balanced" supervisory stance that allows for experimentation while protecting systemic stability.

The RBI Regulatory Sandbox: A Laboratory for Innovation

The RBI Regulatory Sandbox has been pivotal in accelerating the launch of new business models. It allows fintechs to test products like blockchain-based vendor financing or offline digital payments in a controlled environment. By 2026, the sandbox has become a signaling mechanism for long-term capital; a successful exit from the sandbox often leads to immediate institutional investment and a faster path to full licensing.

Key successes from the sandbox include the RT360 system for real-time fraud monitoring and advanced video KYC solutions developed by Signzy Technologies, which have significantly lowered the barriers to customer onboarding.

2026 Regulatory Milestones: Digital Banking and Payment Aggregators

The regulatory landscape in 2026 is defined by several major shifts:

Digital Banking Directions (Jan 1, 2026): These new rules establish a common baseline for mobile and internet banking, tightening operational controls and clarifying board-level accountability for fintech-bank partnerships.

Payment Aggregator (PA) Regime: Revised directions cover governance, merchant due diligence, and capital requirements. Bangalore fintechs operating as PAs, such as Razorpay, have undergone corporate restructurings to ensure dedicated compliance with these norms.

Account Aggregator (AA) Expansion: The AA framework now supports broader data portability, empowering fintechs that build interoperable, API-first products to compete on service quality rather than data silos.

Data Sovereignty: The DPDP Act 2023 and Its Operational Impact

The implementation of the Digital Personal Data Protection (DPDP) Act of 2023 represents a paradigm shift for Bangalore's data-driven fintech firms. The Act establishes privacy as a fundamental right and imposes strict obligations on how digital personal data is processed.

From "Collect Everything" to "Data Minimization"

The DPDP framework requires companies to move from a culture of broad data collection to one of "minimize and justify". Fintechs must now provide granular, independent notices to users, explaining exactly what data is being collected and for what purpose. Consent must be explicit and revocable, making the previous reliance on default "opt-in" checkboxes illegal.

For Bangalore’s startups, this has necessitated a complete "product and service redesign." Visibility into data flows is now essential for audits, requiring firms to map exactly how data moves through third-party APIs and vendors. The Act’s extraterritorial application means even foreign entities serving Indian users from Bangalore must comply, effectively making the city a global hub for privacy-aware fintech development.

Financial and Operational Risks

The penalties for non-compliance are severe, with fines reaching up to ₹250 crore for significant violations. This has created a massive market for RegTech (Regulatory Technology) solutions in Bangalore. Startups are increasingly investing in "privacy by design" tools that automate data discovery, classification, and deletion, transforming compliance from a manual burden into an automated feature of their tech stack.

Human Capital: Talent Trends and the War for Specialists

Bangalore is the epicenter of India’s financial services talent, accounting for 35% of the country’s Global Capability Centers (GCCs). However, the shift to Fintech 2.0 has created a profound "talent paradox": while there is a high volume of general applicants, there is a severe scarcity of specialized talent in AI, cybersecurity, and cloud engineering.

The Skill Gap and the Hybrid Workforce

Studies in 2026 show a 42% skill gap for AI and data roles in BFSI (Banking, Financial Services, and Insurance) GCCs. As technologies like GenAI and blockchain evolve faster than university curricula, companies are forced to prioritize "upskilling over hiring".

A major trend is the integration of the "gig-work" model into the professional workforce. By 2026, 20% of BFSI talent in Bangalore operates through gig or hybrid models, allowing institutions to tap into niche expertise for specific projects without the overhead of permanent hires. Furthermore, the rise of "agentic AI teams" means that human employees are increasingly working alongside autonomous AI agents that handle routine tasks like initial credit filtering or fraud monitoring.

Recruitment in the Age of AI

The recruitment process itself has been disrupted. As candidates use GenAI to polish resumes and "game" interview responses, talent acquisition teams in Bangalore are moving toward "skills-based hiring over degree-based hiring". This involves more practical, hands-on tests—such as project trials or complex case studies—where AI cannot easily supply the answers.

Talent Role | 2026 Demand Trend | Key Required Skills |

AI/ML Engineer | High Intensity | Credit risk modeling, Decision engines |

Cybersecurity Architect | Rapid Expansion | Cloud security, Zero-trust architecture |

Product Manager | Specialized | API banking, UPI ecosystem, CX design |

Compliance Officer | Critical Scarcity | Finance-law crossover, DPDP regulations |

Data Scientist | Sustained High | Graph neural networks, Unstructured data analysis |

Spatial Dynamics: Tech Clusters and Innovation Density

The geographic distribution of fintech in Bangalore is a critical factor in its success. The city is ranked first in India for "fintech innovation density," driven by the concentration of companies in specific tech parks.

Electronic City: The Established Powerhouse

Electronic City remains the technology powerhouse of the city, hosting 35% of the total GCCs and 25% of all BFSI-related office leasing in India. It offers a significant "affordability advantage," with residential prices 20–30% lower than in more central corridors like Whitefield. This has created a self-sustained ecosystem where senior IT leadership and young professionals live in close proximity to major corporate campuses like those of Goldman Sachs (its second-largest global site) and JPMorgan Chase.

Northern Expansion: Hines Uptown and Prestige Tech Cloud

As central corridors like the Outer Ring Road (ORR) become congested, the focus is shifting toward North Bangalore. Upcoming tech parks like Hines Uptown (set for 2026 completion) and Prestige Tech Cloud Park are designed as "future-ready" hubs. These parks emphasize modern architecture, pedestrian-friendly spaces, and integration with natural surroundings, attracting a new generation of fintech startups that prioritize "live-work-play" environments.

Comparisons of Micro-Markets

Micro-Market | Infrastructure Status | Dominant Fintech Profile |

Electronic City | Mature, High Density | Large GCCs, Established BFSI hubs |

Whitefield/ITPL | Global Cluster | Wealthtech, Premium lifestyle finance |

North Bangalore | High Growth, Emerging | Future-tech, Airport-connected startups |

Outer Ring Road | Mature, Saturated | Core engineering centers, SaaS-heavy DNA |

Future Outlook: Bangalore as a Global Fintech Sovereign

The trajectory of Fintech 2.0 in Bangalore points toward a future where the city is not just a participant in global finance but a primary architect of its new rules. The convergence of autonomous AI, programmable digital currency, and a proactive regulatory environment has created a model that is being exported to other emerging markets in Southeast Asia and Africa.

The "Sovereign" Tech Strategy

In 2026, the strategy of many Bangalore fintechs is defined by "sovereign alignment." By relocating headquarters back to India and prioritizing domestic regulatory compliance, firms are positioning themselves to lead the "India model" of finance—one built on public rails, transparent data sharing, and massive scale. Razorpay’s "reverse flip" is the most prominent example of this trend, but it is being mirrored by a broader set of new-age firms preparing for domestic listings.

Challenges and Systemic Risks

However, the transition is not without risks. The sector’s heavy reliance on a concentrated group of shared AI models and cloud providers creates "correlation risk," where a failure in one model could destabilize the broader market. Furthermore, the "black box" nature of complex AI algorithms poses a challenge for governance, necessitating a shift toward "macro-prudential" regulations that focus on the transparency and explainability of automated decisions.

Conclusion

Fintech 2.0 in Bangalore represents the pinnacle of digital financial evolution. By 2026, the city has successfully moved beyond the superficial digitization of money to build an ecosystem where financial services are autonomous, invisible, and deeply integrated into the fabric of life and business. The combination of world-class digital infrastructure, a resilient and mature investment cycle, and a talented, hybrid workforce has made Bangalore the indispensable node of the future global economy. As the city continues to navigate the complexities of AI ethics, data privacy, and global expansion, it remains the primary case study for how a developing economy can leapfrog traditional financial constraints to build a secure, inclusive, and technologically superior future.

Read More -

1. From Idea to MVP: A Step-by-Step Guide for Solo Founder

🔗 https://findnstart.com/blogs/from-idea-to-mvp-a-step-by-step-guide-for-solo-founder

2. How to Validate Your Startup Idea in 48 Hours for $0

🔗 https://findnstart.com/blogs/how-to-validate-your-startup-idea-in-48-hours-for-0

3. Remote vs. Local: Does Your Co-Founder Need to Live in the Same City?

🔗 https://findnstart.com/blogs/remote-vs-local-does-your-co-founder-need-to-live-in-the-same-city

4. The 2026 Startup Landscape: What Has Fundamentally Changed (and Why Founder Skills Matter More Than Ever)

5. The Most In-Demand Skills for Startup Founders in 2026

🔗 https://findnstart.com/blogs/the-most-in-demand-skills-for-startup-founders-in-2026

6. How to Find a Technical Co-Founder (Without a Six-Figure Salary)

🔗 https://findnstart.com/blogs/how-to-find-a-technical-co-founder-without-a-six-figure-salary

7. 5 Red Flags to Look for When Choosing a Startup Partner

🔗 https://findnstart.com/blogs/5-red-flags-to-look-for-when-choosing-a-startup-partner

8. How to Pitch Your Idea to Potential Co-Founders

🔗 https://findnstart.com/blogs/how-to-pitch-your-idea-to-potential-co-founders

9. How to Build a Portfolio that Attracts High-Growth Startup Founders

🔗 https://findnstart.com/blogs/how-to-build-a-portfolio-that-attracts-high-growth-startup-founders

10. Equity vs. Salary: How to Split Ownership with Your First Teammate

🔗 https://findnstart.com/blogs/equity-vs-salary-how-to-split-ownership-with-your-first-teammate

11. Why Joining an Early-Stage Startup is Better Than a Corporate Job

🔗 https://findnstart.com/blogs/why-joining-an-early-stage-startup-is-better-than-a-corporate-job

12. The Future of EdTech: Why Developers and Educators Need to Team Up Now

🔗 https://findnstart.com/blogs/the-future-of-edtech-why-developers-and-educators-need-to-team-up-now

13. The Architecture of Symbiosis: Analytical Perspectives on the Five Habits of Successful Startup Duos

14. Finding a Co-Founder in the AI Space: What Skills Should You Look For?

🔗 https://findnstart.com/blogs/finding-a-co-founder-in-the-ai-space-what-skills-should-you-look-for

15. Overcoming Analysis Paralysis and the Strategic Path to Execution

🔗 https://findnstart.com/blogs/overcoming-analysis-paralysis-and-the-strategic-path-to-execution

16. From College Project to Company: How to Find Your Student Co-Founder

🔗 https://findnstart.com/blogs/from-college-project-to-company-how-to-find-your-student-co-founder

17. How to Start a Startup While Working a Full-Time Job

🔗 https://findnstart.com/blogs/how-to-start-a-startup-while-working-a-full-time-job

18. How to Build a HealthTech Startup Without a Medical Degree

🔗 https://findnstart.com/blogs/how-to-build-a-healthtech-startup-without-a-medical-degree

19. The Solitary Architect: Executive Isolation in Entrepreneurship

20. The 2026 Guide to Launching a SaaS as a Solo Developer

21. What Sustainable Growth Actually Looks Like

🔗 https://findnstart.com/blogs/what-sustainable-growth-actually-looks-like

22. The Early Warning Signs Your Startup Is in Trouble

🔗 https://findnstart.com/blogs/the-early-warning-signs-your-startup-is-in-trouble

23. How to Grow Without Burning Out

🔗 https://findnstart.com/blogs/how-to-grow-without-burning-out

24. The Truth About “Runway” Most Founders Ignore

🔗 https://findnstart.com/blogs/the-truth-about-runway-most-founders-ignore

25. Revenue Solves More Problems Than Funding

🔗 https://findnstart.com/blogs/revenue-solves-more-problems-than-funding

26. What No One Tells You About Being a Solo Founder

🔗 https://findnstart.com/blogs/what-no-one-tells-you-about-being-a-solo-founder

27. Why Smart People Quit High-Paying Jobs to Build Startups (And Why Most Regret It)

28. Why Most Startup Advice on Twitter Is Dangerous

🔗 https://findnstart.com/blogs/why-most-startup-advice-on-twitter-is-dangerous

29. Decision Fatigue: The Silent Startup Killer

🔗 https://findnstart.com/blogs/decision-fatigue-the-silent-startup-killer

30. Fear vs Logic: How Founders Actually Make Decisions

🔗 https://findnstart.com/blogs/fear-vs-logic-how-founders-actually-make-decisions

31. How Overthinking Destroys Early Momentum

🔗 https://findnstart.com/blogs/how-overthinking-destroys-early-momentum

32. Ideas Don’t Scale. Systems Do.

🔗 https://findnstart.com/blogs/ideas-dont-scale-systems-do

33. The First Hire That Actually Matters

🔗 https://findnstart.com/blogs/the-first-hire-that-actually-matters

34. How the First 100 Users Decide Your Startup’s Fate

🔗 https://findnstart.com/blogs/how-the-first-100-users-decide-your-startups-fate

35. Why Your Startup Doesn’t Need Growth — It Needs Focus

🔗 https://findnstart.com/blogs/why-your-startup-doesnt-need-growthit-needs-focus

36. Why Most Startups Die Quietly

🔗 https://findnstart.com/blogs/why-most-startups-die-quietly

37. Lessons Learned Too Late by First-Time Founders

🔗 https://findnstart.com/blogs/lessons-learned-too-late-by-first-time-founders

38. The Myth of the “Overnight Success” Startup

🔗 https://findnstart.com/blogs/the-myth-of-the-overnight-success-startup