EdTech After the Funding Boom: What’s Left?

June 29, 2026 by Harshit Gupta

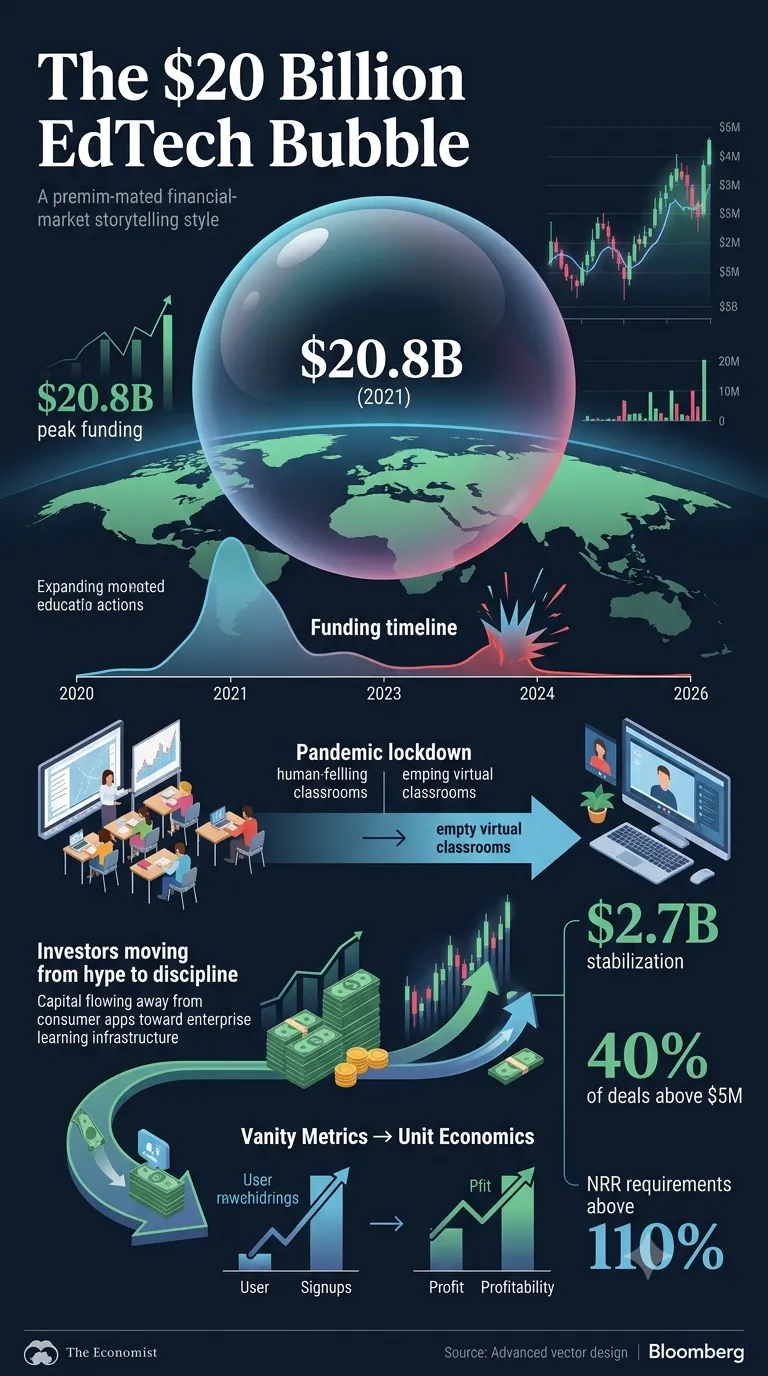

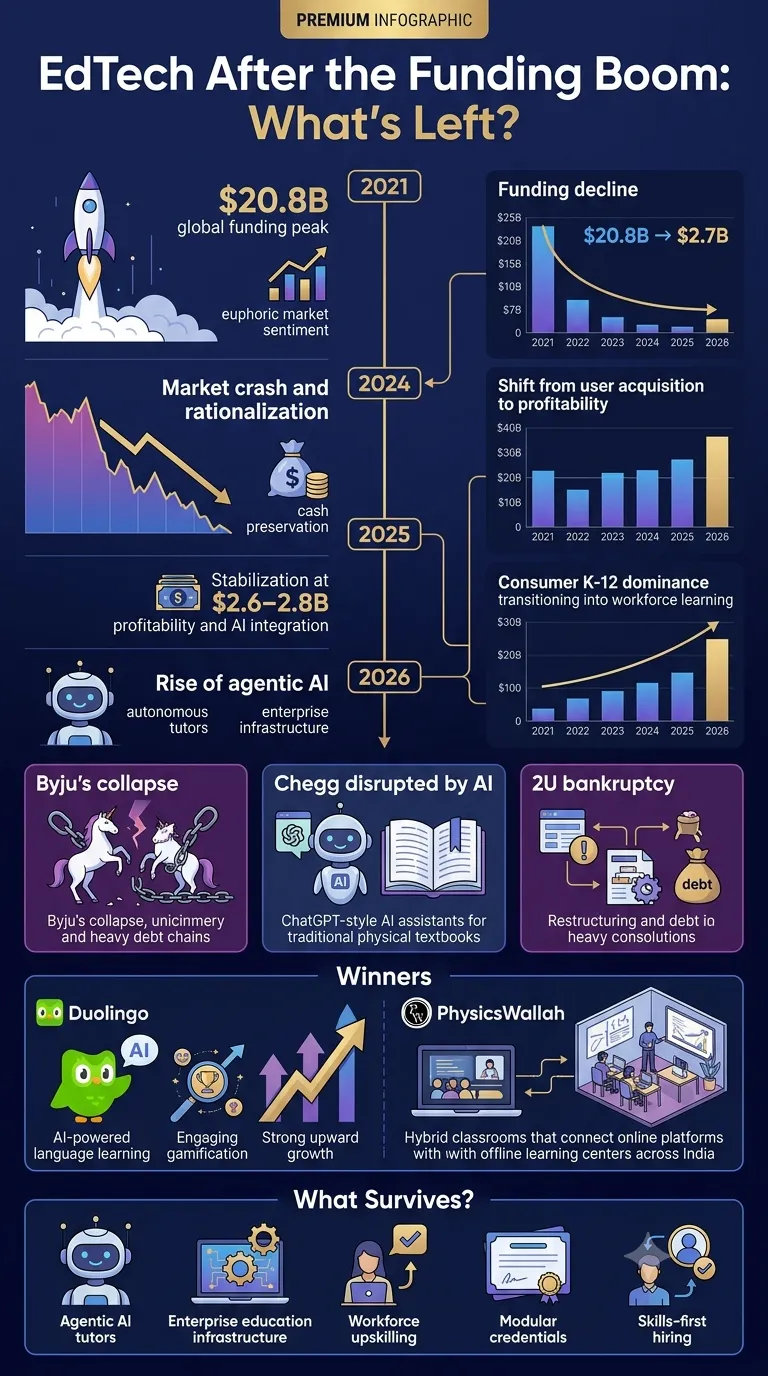

The global education technology sector has transitioned from a period of speculative hyper-growth into a rigorous era of institutional stabilization and technological realignment. The years 2020 through 2021 represented a once-in-a-generation surge, with global edtech funding tripling pre-pandemic levels to reach a zenith of $20.8 billion in 2021. However, the subsequent years have witnessed a profound recalibration. By 2025, the market settled into a more disciplined rhythm, with venture capital investment hitting approximately $2.6 billion to $2.8 billion, reflecting a market that has moved past the emergency period toward a sustainable, outcomes-oriented infrastructure. This structural shift indicates that while the "funding boom" has receded, it has left behind a landscape defined by agentic artificial intelligence, enterprise-grade software integration, and a ruthless prioritization of unit economics over vanity metrics.

The Macro-Economic Hangover and the Capital Reset

The contraction from the $20 billion peaks of 2021 to the $2.6 billion stabilization of 2025 was not merely a reduction in cash flow but a fundamental re-benchmarking of sectoral value. During the boom, capital was dispersed across a wide range of B2C "nice-to-have" tools; in the post-boom phase, capital is concentrated around companies that demonstrate two things simultaneously: credible market traction and a direct link to employability or institutional efficiency.

The investment tone in 2025 and moving into 2026 is one of pragmatism. Venture capital flows now reflect a shift from volume to intention. While deal counts held relatively steady, nearly 40% of all transactions in 2025 sat above the $5 million mark, suggesting a flight to quality. Investors have effectively closed the "confidence gap" by demanding Net Revenue Retention (NRR) levels above 110% and requiring implementation payback within 12 months for top-tier assets.

Investment Metric | 2021 (Peak) | 2024 (Low) | 2025 (Stabilization) | 2026 (Projected Trend) |

Global VC Funding | $20.8B | ~$2.3B | $2.6B - $2.8B | Moderate growth (~10-11%) |

Primary Focus | User Acquisition | Cash Preservation | Profitability & AI | Agentic AI Integration |

Sector Leader | K-12 Consumer | Rationalization | Workforce Training | Enterprise Infrastructure |

Market Sentiment | Euphoric | Fearful | Pragmatic | Institutionalized |

The "rebalancing moment" of 2025 has favored infrastructure over hype. Digital penetration in sectors like K-12 remains below 5% of total spending, suggesting that while the venture boom has ended, the digital transformation journey is in its early innings. Global expenditure on education is expected to reach $7.3 trillion by 2025, but the sector remains starved of private capital relative to its size, creating a vacuum that only the most efficient and technologically advanced survivors can fill.

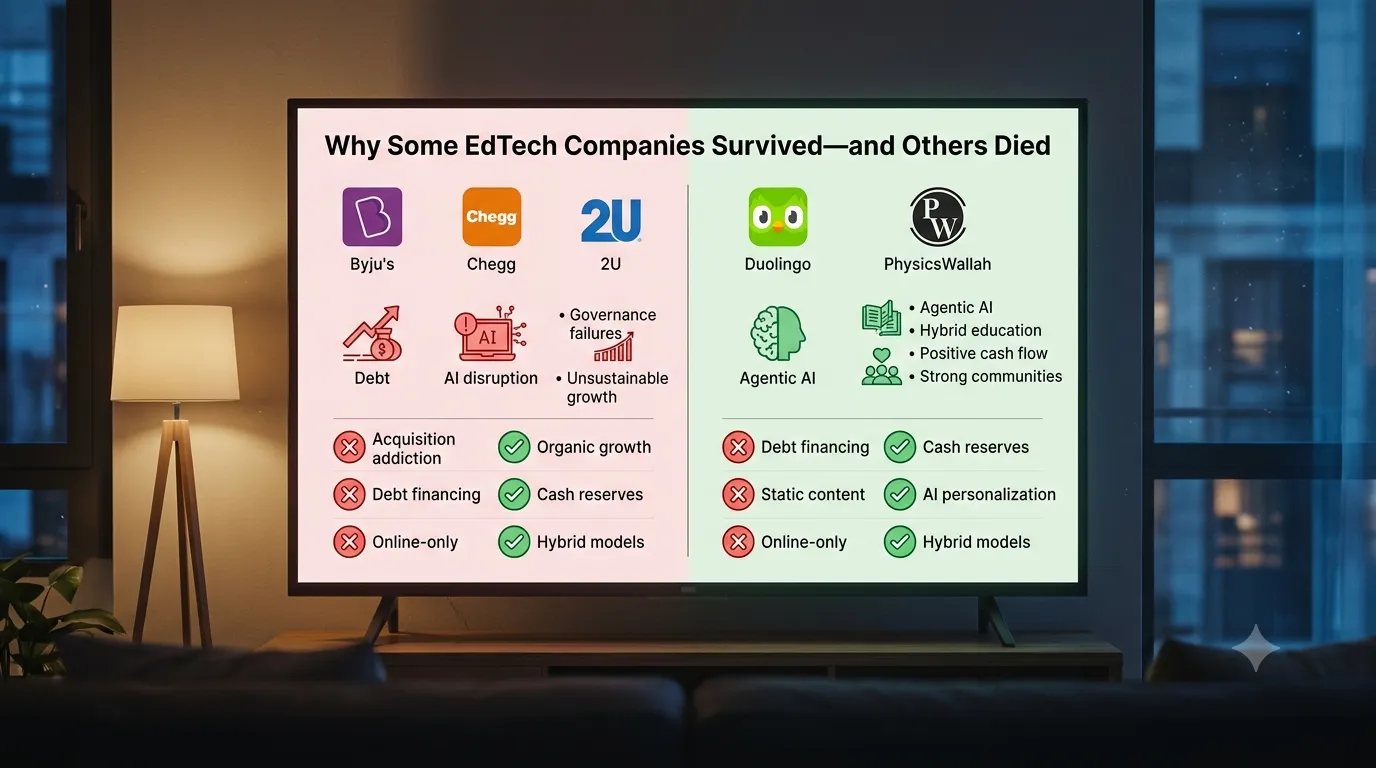

The Failure of the Pandemic Giants: A Forensic Analysis

The most visible consequence of the funding boom’s collapse is the unraveling of legacy "unicorns" that failed to bridge the gap between pandemic-era demand and post-pandemic reality. These failures are categorized by three distinct vectors: governance collapse, technological obsolescence, and unsustainable debt structures.

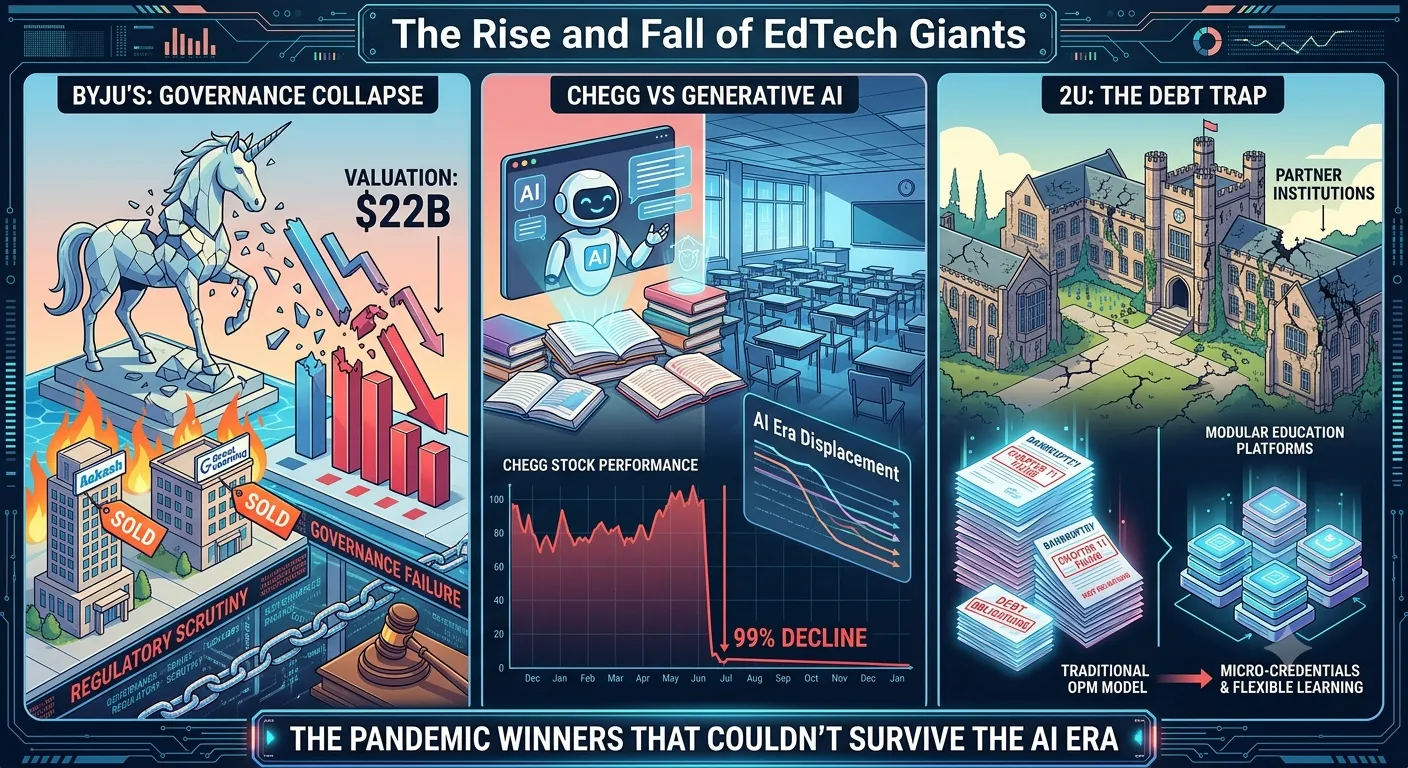

The Governance Collapse: The Case of Byju's

Byju's, once India’s most valuable startup at $22 billion, represents the most significant failure of governance in the history of the sector. The mechanism of its downfall was a combination of aggressive, debt-fueled international acquisitions and a persistent lack of financial engagement with lenders. By early 2026, the company was entangled in insolvency proceedings in India and a $1 billion default judgment in the United States.

The dispute centered on a $1.2 billion Term Loan B facility. Lenders alleged that Byju's Alpha, a US subsidiary, improperly moved $533 million to an obscure Miami-based hedge fund, Camshaft Capital, to hide assets. The legal fallout has been catastrophic; US courts authorized the sale of assets like Tynker and Epic at fractions of their purchase price—Tynker, bought for $200 million, was liquidated for $2.2 million. This "fire sale" underscores the total destruction of equity value that occurs when rapid inorganic growth is not supported by transparent financial controls.

The Technological Obsolescence: Chegg and the Generative AI Threat

While Byju's failed on governance, Chegg became the primary casualty of the generative AI revolution. Chegg’s business model—centered on textbook rentals and a proprietary database of expert-answered questions—was directly disrupted by the advent of Large Language Models (LLMs) and AI-driven search engine results.

In 2025, Chegg announced it would cut 45% of its workforce, approximately 388 roles, citing the impact of AI-powered tools and reduced Google traffic. Search engines began providing AI summaries that satisfied student queries without requiring a click-through to Chegg’s platform, leading to a 99% plunge in stock value from its 2021 peak. The company's attempt to pivot toward a $40 billion professional skilling market and an "AI-first" Study model reflects a desperate effort to regain relevance in an era where information has reached a near-zero marginal cost.

The Debt Trap: 2U and the OPM Restructuring

2U, a leader in the Online Program Manager (OPM) space, faced a different post-boom reality: a debt-laden balance sheet in a high-interest-rate environment. After acquiring edX for $800 million in 2021, the company struggled to service its obligations as university demand for traditional revenue-share models cooled.

In mid-2024, 2U entered a "prepackaged" Chapter 11 bankruptcy, shedding over $500 million in debt and emerging in September 2024 as a private entity owned by its lenders. This reorganization signifies the end of the "fully outsourced" degree model. Universities are now moving toward modular, first-party credential programs, and 2U’s emergence as a private company allows it to focus on specialized, career-focused education rather than the high-overhead public market.

The Survivalists: Success Through Personalization and Hybridization

Amidst the wreckage of legacy giants, two companies—Duolingo and PhysicsWallah—have emerged as the definitive blueprints for post-boom success. Their models prioritize deep user engagement, technological moat-building, and operational efficiency.

Duolingo: The AI-First Monetization Engine

Duolingo has successfully navigated the transition from a gamified language app to a $1 billion revenue engine. In 2025, the company surpassed 50 million daily active users (DAUs) and reached a significant milestone of $400 million in net income.

Duolingo Financial Metric | FY 2024 | FY 2025 | YoY Change |

Total Revenue | $748.0M | $1,037.6M | +39% |

Net Income | $88.6M | $414.1M | >100% |

Daily Active Users | 40.5M | 52.7M | +30% |

Adjusted EBITDA Margin | 25.7% | 29.5% | +380 bps |

The core of Duolingo’s success is its "AI-first" strategy, specifically the Duolingo Max subscription tier. Features such as "Explain My Answer" and "Video Call with Lily" (an AI tutor) have driven a 7% penetration rate into the premium tier, pushing subscription revenue to 83% of total income. Furthermore, the company used generative AI to reduce content production time by 80%, demonstrating how AI can be an economic driver rather than just a product enhancement.

PhysicsWallah: The Hybrid Offline-Online Dominance

In the Indian market, PhysicsWallah (PW) has defied the sectoral downturn by doubling down on a hybrid "Vidyapeeth" model. While its competitors faced liquidity crises, PW reported a 34% revenue jump in Q3 FY26, reaching ₹1,082 crore, with net profits rising to ₹102.3 crore.

PhysicsWallah’s strategy centers on aggressive physical expansion, opening 70-75 offline centers per year with a goal of reaching 500 centers by 2028. This model addresses the limits of pure digital engagement in competitive exam prep. By December 2025, the company operated 318 centers, where offline enrollments grew by 36%. PW maintains a cash balance exceeding ₹5,500 crore, positioning it to dominate the South Asian landscape as a national brand that balances digital reach with the credibility of physical classrooms.

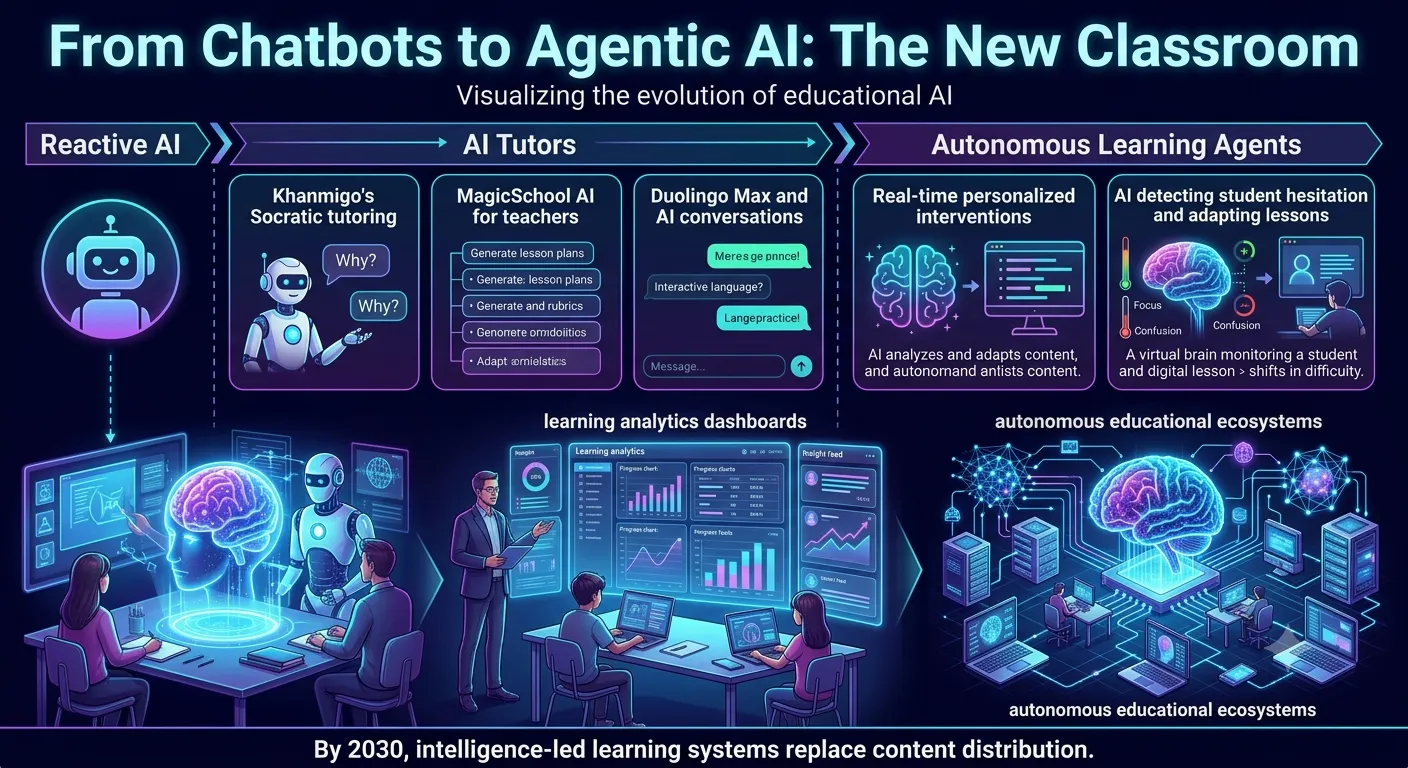

Artificial Intelligence: From Pilot to Agentic Infrastructure

The year 2025 marked the definitive shift from "reactive AI"—basic chatbots that respond to prompts—to "agentic AI". Agentic AI systems are autonomous; they possess the "educational agency" to monitor a student's progress, identify micro-behaviors (such as hesitation on a paragraph), and intervene proactively.

The Evolution of the AI Tutor

The deployment of AI in the classroom has moved from experiment to systemic infrastructure. Khan Academy’s "Khanmigo" scaled from 40,000 to 700,000 students in the 2024-25 academic year, using Socratic questioning to guide learners. Simultaneously, "MagicSchool AI" has become a Swiss Army knife for educators, offering over 60 tools to automate administrative tasks like lesson planning and IEP drafting.

AI Tool Profile | Primary User | Core Function | Business Model |

Khanmigo | Student/Teacher | Socratic Tutoring | Non-profit/District-funded |

MagicSchool | Teacher | Administrative Automation | Freemium/SaaS |

Duolingo Max | Consumer | Immersive Conversation | Premium Subscription |

VED (Vedantu) | Student | Real-time Live Doubt Solving | Hybrid Integrated |

The impact of these tools is measurable. Learners using Duolingo’s Roleplay feature reported a 30% reduction in speaking hesitation, while AI-enabled grading tools like Brisk Teaching provide faster feedback, allowing teachers to focus on mentorship rather than assessment. By 2026, agentic AI is expected to become the mandatory baseline for any educational platform, effectively eliminating the "frustration wall" that leads to student abandonment.

India: The Regulatory and Policy Laboratory

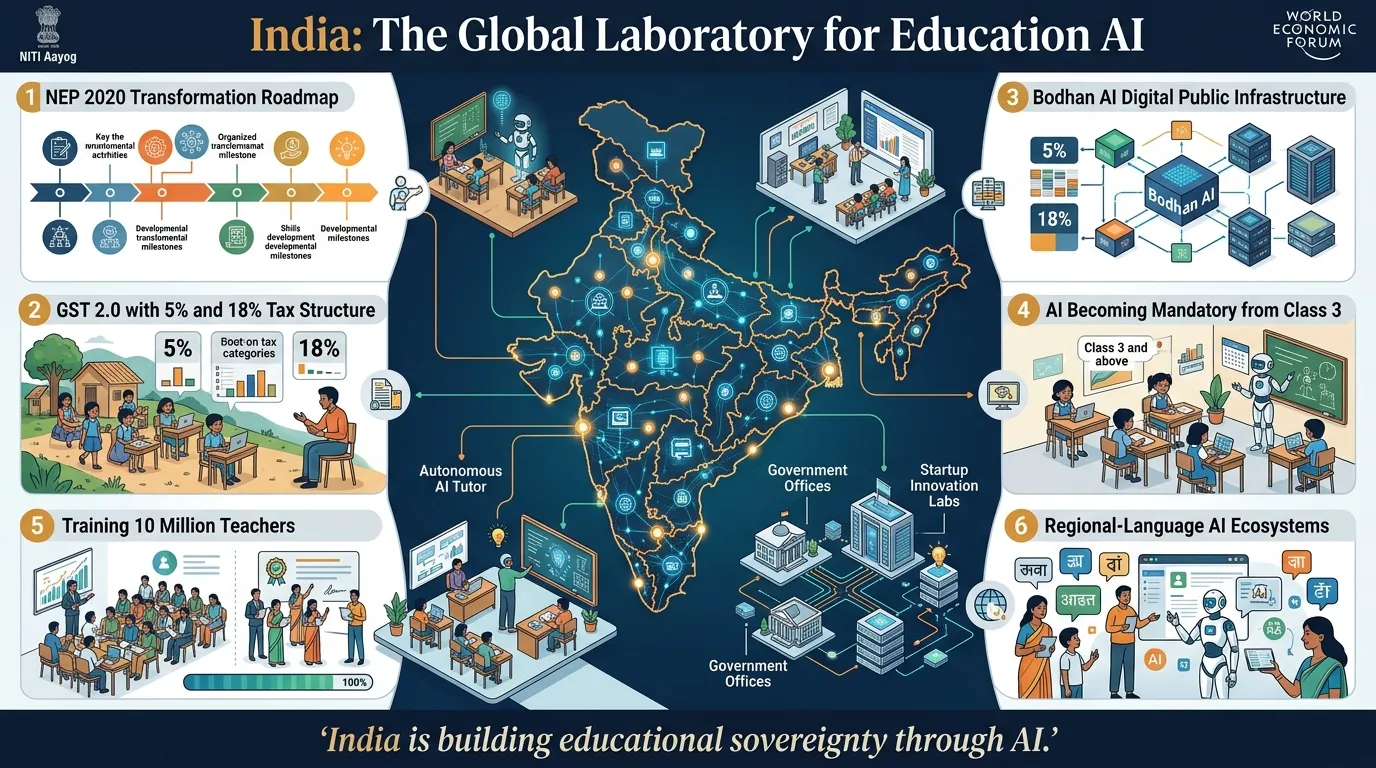

India has emerged as a critical laboratory for the post-boom era, characterized by bold policy initiatives and significant tax reforms. The National Education Policy (NEP) 2020 has acted as a catalyst for these changes, pushing the country toward a digital-first educational identity.

GST 2.0 and the Commercial Reclassification

Effective September 22, 2025, India implemented "GST 2.0," a structural reform that simplified the tax regime into a two-slab structure of 5% and 18%. This reform has significant implications for EdTech:

18% GST: Applied to commercial online coaching (UPSC, JEE, NEET), non-accredited certificate/diploma courses, and private skill development.

Exemptions: Services provided by government-recognized educational institutions to their students remain exempt. Crucially, skill development training provided by the NSDC or its partners was reinstated as exempt in January 2025.

This tax structure forces EdTech firms to either align with formal institutional curricula to achieve exemption or build enough value to justify the 18% tax burden on individual learners.

The Bodhan AI Initiative and DPI

The Ministry of Education announced "Bodhan AI" in 2026, a Digital Public Infrastructure (DPI) for the education sector. Bodhan AI provides startups with reliable APIs to build models and deliver AI-led applications tailored to Indian values and languages. This move toward "AI-sovereignty" ensures that India is not just a consumer of global AI models but a creator of homegrown solutions for teacher capacity building and personalized lesson plans.

Starting in the 2026-27 academic year, India will also introduce AI as a mandatory subject from Class 3 onwards. This involves training over one crore teachers and developing textbooks that treat AI and computational thinking as basic literacy, preparing the future workforce for a technology-driven economy.

Higher Education and Workforce Learning: The Strategic Anchors

The post-boom phase has seen a clear divergence between the traditional degree market and the "employability" market. Higher education has entered a phase of stabilization, while workforce learning has become the sector’s primary growth engine.

The Modularization of Higher Ed

Institutional investment in higher education is now focused on core infrastructure: student success platforms, credentialing tools, and integrated financial-aid systems. The trend of fully outsourced degree programs is fading, replaced by first-party modular credentials. Universities are increasingly seeking to modernize their "systems of record" to manage cost pressures and declining undergraduate enrollment—which saw a 5.6% drop in fall 2023.

Workforce Learning as Enterprise SaaS

Workforce learning is currently the most attractive segment for investors, behaving like classic enterprise SaaS with low churn and high lifetime value (LTV). Capital is clustering around:

Skills Intelligence: Mapping employee competencies to future job requirements.

Vertical EdTech: Industry-specific training stacks in healthcare, cybersecurity, and manufacturing that include compliance narratives.

Work-Integrated Learning: Platforms that directly connect job-aligned training with hiring pipelines.

Notable deals like Workday’s $1.1 billion acquisition of Sana and Simspace’s $39 million raise for cybersecurity training reflect the market’s appetite for job-aligned learning infrastructure.

Investment Discipline and the M&A Super-Cycle

The "metrics over momentum" era has transformed the role of private equity and strategic acquirers. In 2024 and 2025, the market was anchored by massive "take-private" transactions that signaled a consolidation of scaled education software.

The Great Consolidation

Major M&A Transaction | Acquirer | Disclosed Value | Strategic Rationale |

PowerSchool | Bain Capital | $5.6B | Dominance in K-12 cloud infrastructure |

Instructure | KKR | $4.8B | Scaling the Canvas LMS for hybrid models |

Transact Campus | Roper Technologies | $1.5B | Integrating campus tech and payment stacks |

HolonIQ | QS (Quacquarelli Symonds) | Undisclosed | Enhancing market analytics and data |

Sana | Workday | $1.1B | AI-powered knowledge and enterprise learning |

These deals are important not just for their size, but because they signify a flight to "full-stack" platforms. Acquirers are building ecosystems where a single provider handles learning, administration, analytics, and billing. This consolidation is driven by margin pressure; as schools and enterprises trim their vendor lists, firms with the most comprehensive "all-in-one" offerings gain the most bargaining power.

The Road Toward 2030: Cognitive Analytics and Just-in-Time Hiring

Looking toward the end of the decade, the EdTech sector is shifting from "content distribution" to "intelligence-led learning systems". The focus for 2027-2030 will be on:

Neuroeducation: Using cognitive analytics to create a bridge between digital platforms and neural learning patterns.

Skill-Centric Labor Markets: The final convergence of education and WorkTech, where hiring is done "just-in-time" based on real-time portfolio data rather than static degrees.

Digital Sovereignty: Nations like India and those in Europe will increasingly prioritize "Green Learning" and ethical AI frameworks that solve the "black box" accountability crisis in automated grading and assessment.

Conclusion: What’s Left?

What remains after the funding boom is an industry that has matured out of its "experimental" infancy and into a "pragmatic" adulthood. The speculative energy that fueled the rise of unsustainable unicorns has been replaced by an "outcome economy".

The winners of the post-boom era are the "infrastructure players"—those who provide the essential rails for institutional operations and the agentic AI that personalizes learning at scale. While the collapse of Byju's and the decline of Chegg serve as cautionary tales of governance and technological blindness, the resurgence of PhysicsWallah and the AI-driven profitability of Duolingo demonstrate that education technology is more essential than ever. With global digital spend projected to reach $404 billion by late 2025, the sector has moved from being a pandemic-era substitute to becoming the permanent, intelligent architecture of global education.

Protect Your Future: The Precision Vesting Calculator

Don't let a "handshake deal" complicate your exit. Map out your ownership journey with our Vesting Calculator

Calculate Your Vesting Schedule →