Down Rounds in India: The Silent Reality

March 10, 2026 by Harshit Gupta

The Indian startup ecosystem, once the global poster child for hyper-scalability and venture-backed exuberance, has entered a period of profound structural correction. This transformation, often summarized through the lens of a "funding winter," is more accurately characterized as a "Silent Reality" defined by widespread down rounds, aggressive valuation markdowns, and a systemic shift in the power dynamics between founders and investors. Between 2023 and 2026, the narrative of India as the world's third-largest startup hub began to diverge: while the headline figures for total capital raised showed signs of stabilization, the underlying mechanics of these deals revealed a landscape of distressed bridge rounds and a rigorous "flight to quality".

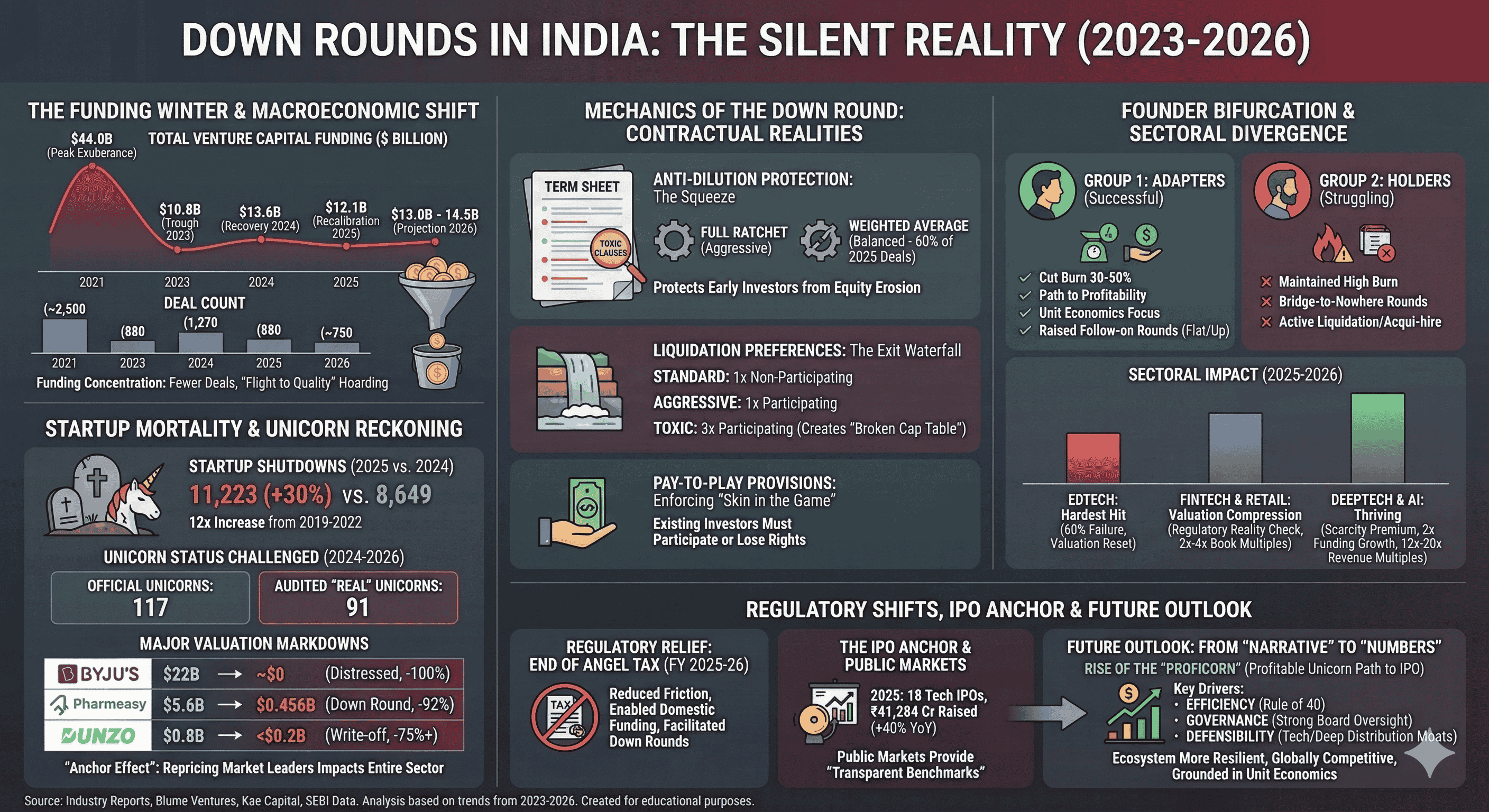

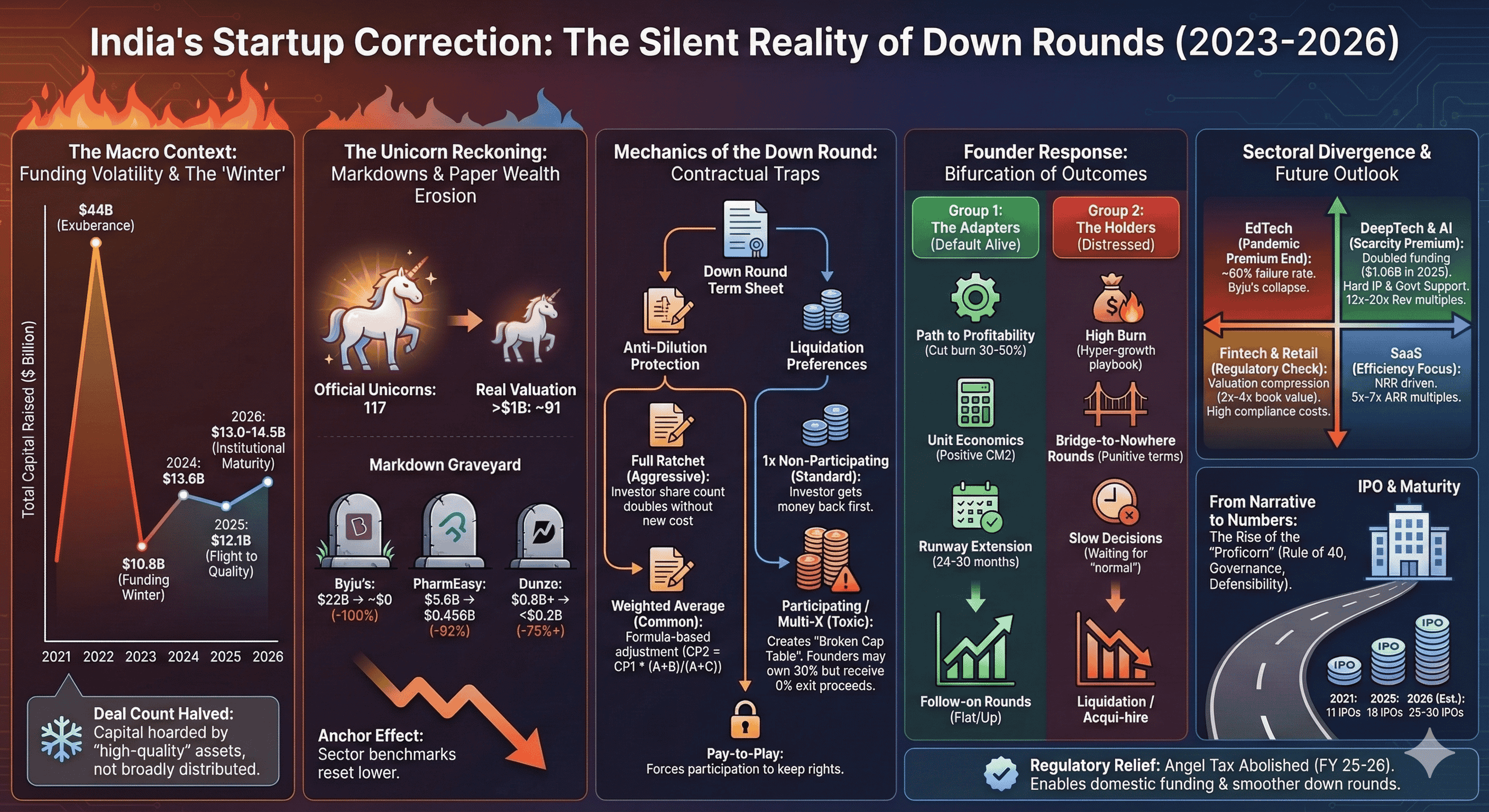

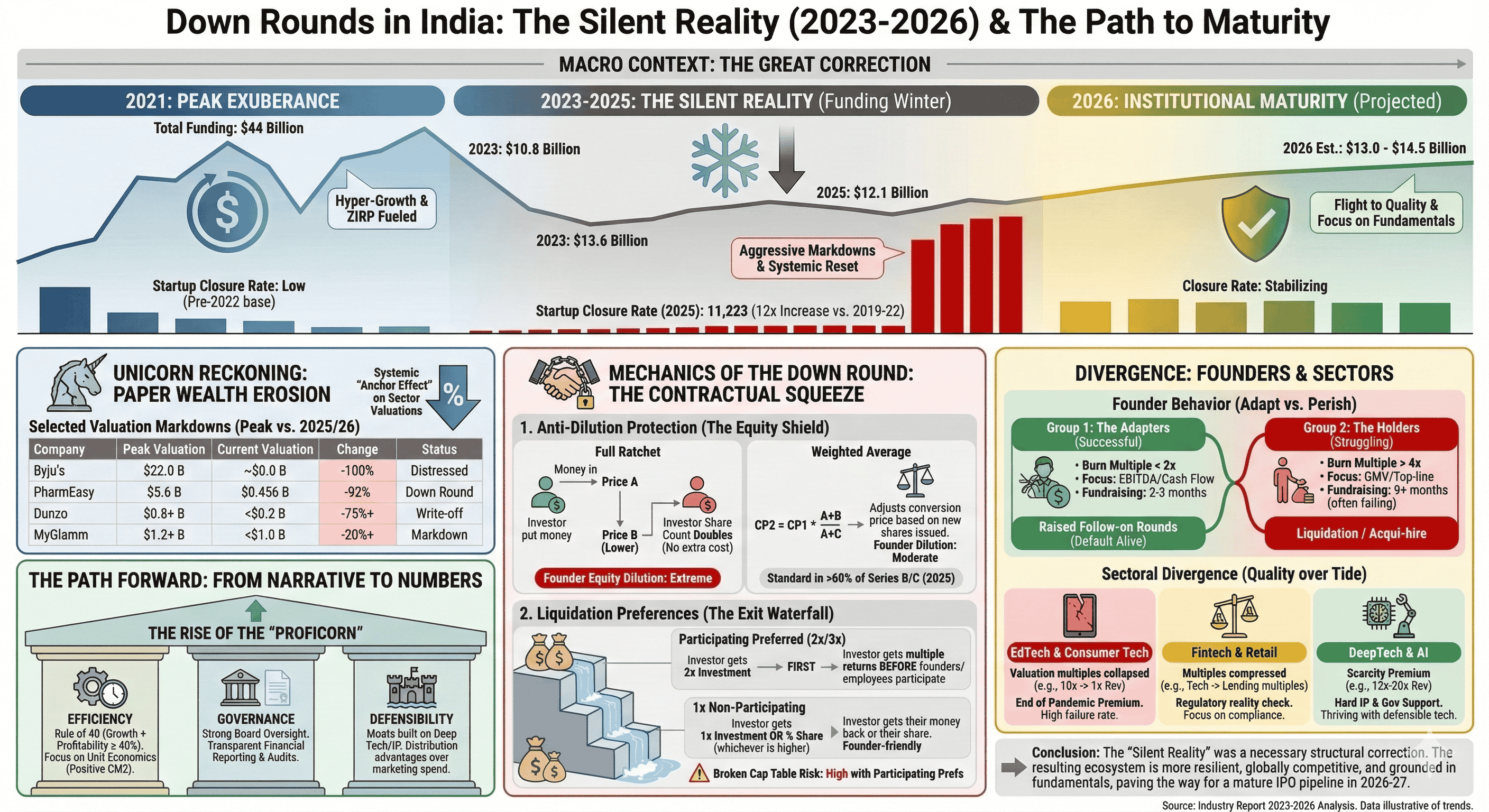

The statistical reality of this correction is stark. In 2025, the ecosystem witnessed a surge in startup mortality, with over 11,223 companies shutting down—a 30% increase from the 8,649 closures recorded in 2024. This mortality rate represents a 12-fold increase compared to the 2019-2022 period, signaling that the excesses of the 2021 liquidity boom have reached a point of final reckoning. This report provides an exhaustive analysis of the mechanisms behind this correction, the evolution of term sheet nuances, and the sectoral divergence defining the Indian venture landscape as it moves into the second half of the decade.

The Macroeconomic Context and Funding Volatility

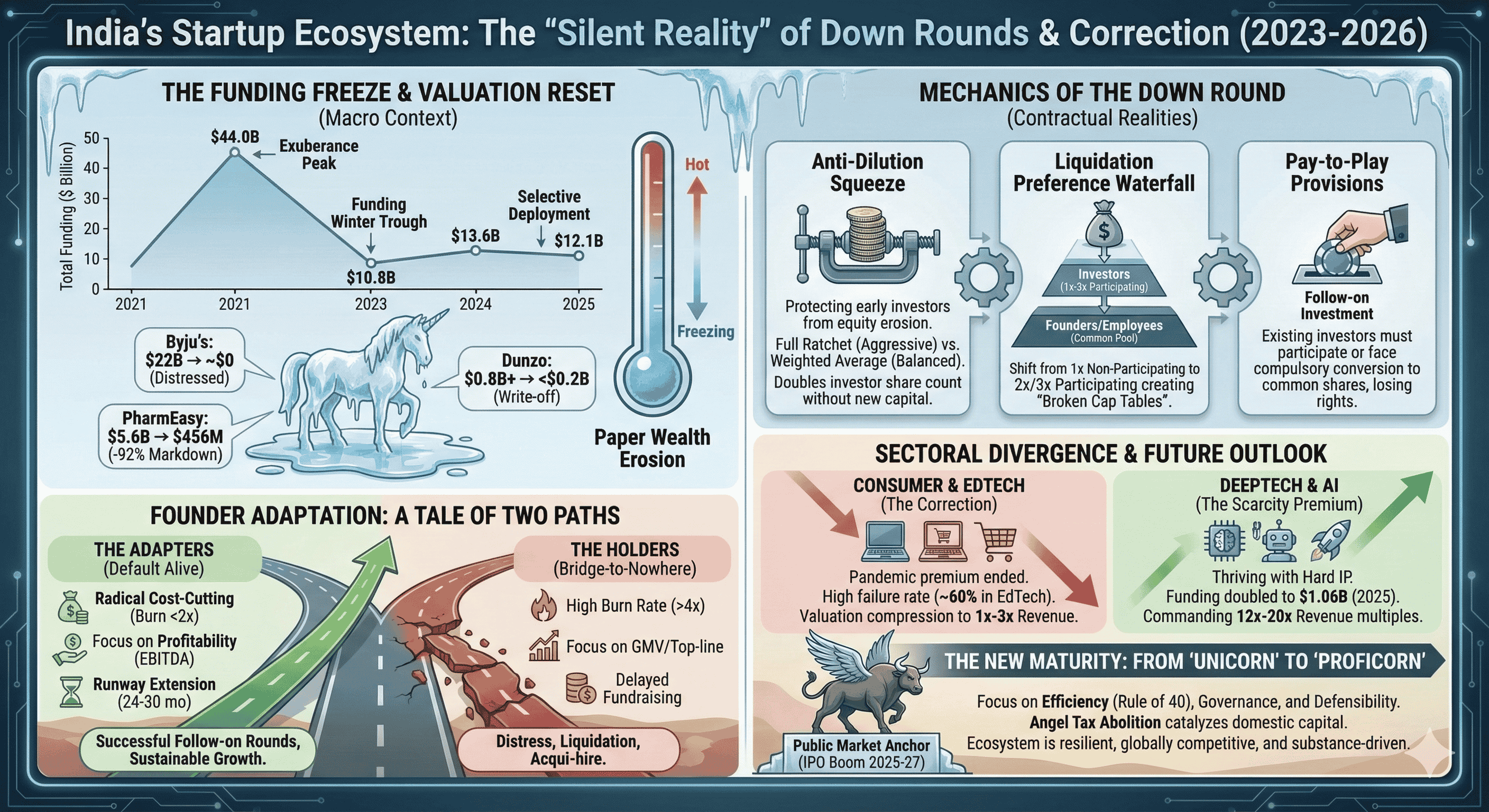

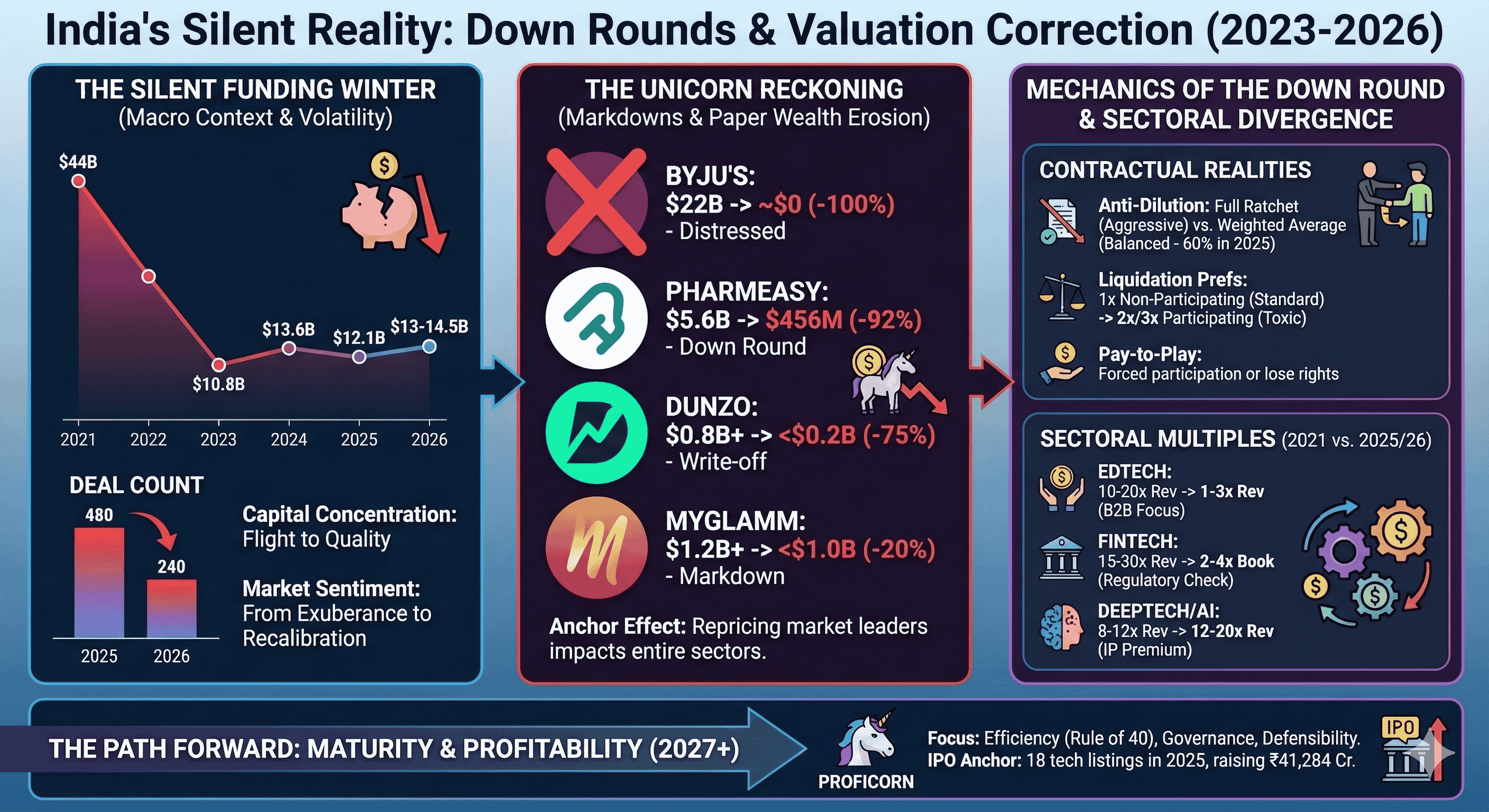

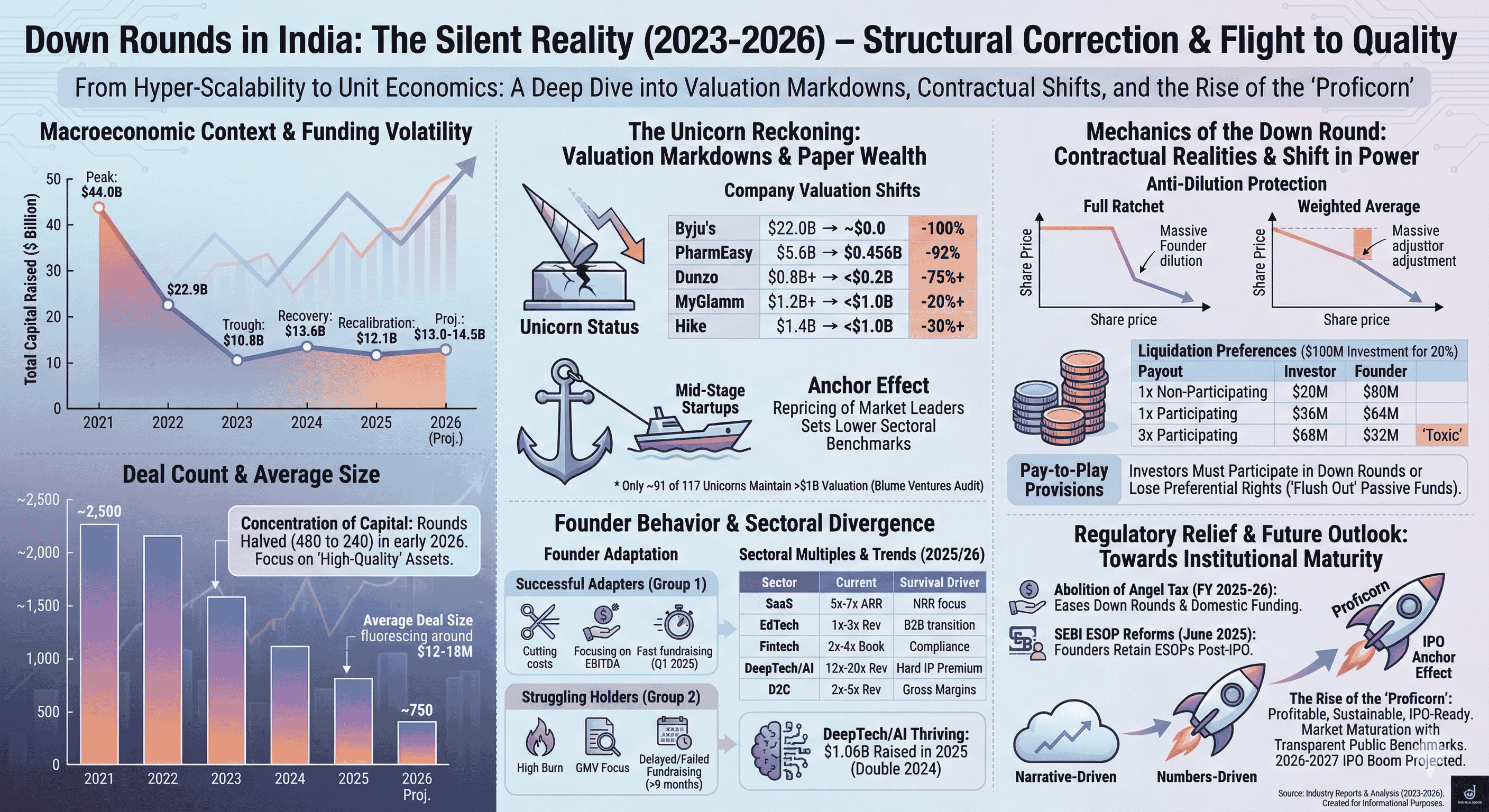

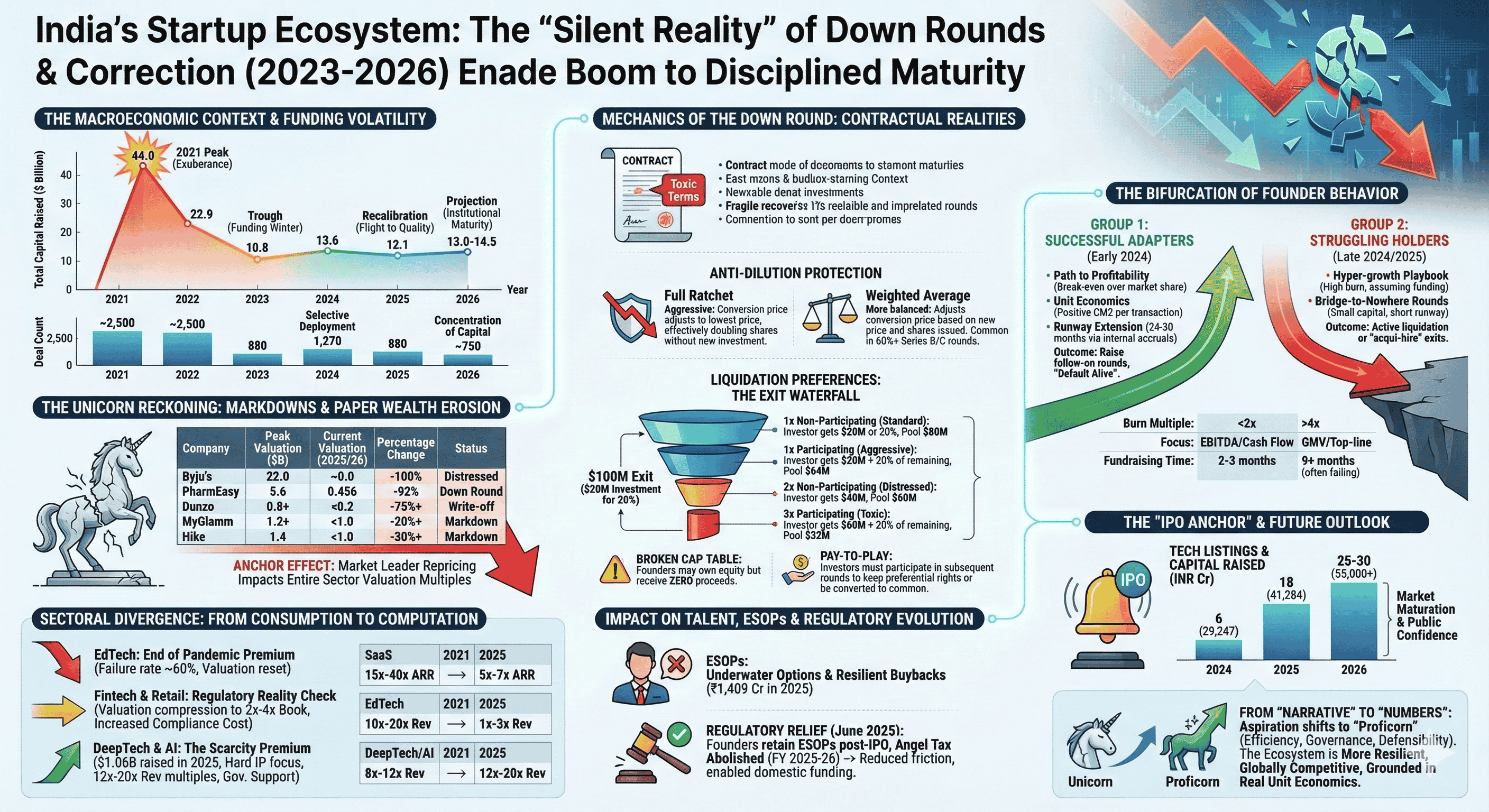

The trajectory of venture capital in India from 2021 to 2026 reflects a classic boom-and-bust cycle followed by a fragile, highly selective recovery. In 2021, the ecosystem peaked with $44 billion in total funding, fueled by zero-interest-rate policies (ZIRP) and a global race for emerging market exposure. By 2023, this figure crashed to $10.8 billion. While 2024 saw a tentative rebound to $13.6 billion, 2025 experienced a cooling effect, with total venture capital funding settling at $12.1 billion.

The "Silent Reality" is most evident in the concentration of capital. In early 2026, data revealed that while total fund value grew by 5% year-on-year, the number of actual funding rounds halved, dropping from 480 to 240. This indicates that capital is no longer being distributed broadly across early-stage experiments but is instead being hoarded by a narrow cohort of "high-quality" assets that have demonstrated a clear path to profitability.

Funding Period | Total Capital Raised ($ Billion) | Deal Count | Average Deal Size ($ Million) | Market Sentiment |

2021 (Peak) | 44.0 | ~2,500 | 17.6 | Hyper-Growth/Exuberance |

2022 (Transition) | 22.9 | ~1,500 | 15.2 | Initial Correction |

2023 (Trough) | 10.8 | 880 | 12.2 | Funding Winter |

2024 (Recovery) | 13.6 | 1,270 | 10.7 | Selective Deployment |

2025 (Recalibration) | 12.1 | 880 | 13.7 | Flight to Quality |

2026 (Projection) | 13.0 - 14.5 | ~750 | 18.0 | Institutional Maturity |

The divergence in these numbers highlights that while the "funding winter" is thawing for a few, it remains a deep freeze for the majority. Investors have shifted their focus from "storytelling" to "execution," requiring founders to present not just a vision, but a defensible business model with healthy unit economics.

The Unicorn Reckoning: Markdowns and Paper Wealth Erosion

The prestige associated with the "Unicorn" status has faced its severest challenge since 2024. While India officially created 117 unicorns, subsequent audits by firms like Blume Ventures suggest that only 91 of these companies truly maintain a valuation above $1 billion. The others are "paper tigers," companies whose last valuation was set during the peak of 2021 and whose current fair market value (FMV) is likely significantly lower.

The collapse of Byju’s remains the most prominent case study of this period. Once valued at $22 billion, the company saw its valuation slashed to zero by major investors like Prosus in 2024. The rationale provided by investors centered on a total breakdown of financial governance, inadequate information on liabilities, and a deteriorating relationship between founders and the board. This markdown was not an isolated event; PharmEasy similarly saw its valuation drop by 92%, from $5.6 billion in 2021 to $456 million by late 2024.

Company | Peak Valuation ($ Billion) | Current Valuation (2025/26) | Percentage Change | Status |

Byju's | 22.0 | ~0.0 | -100% | Distressed |

PharmEasy | 5.6 | 0.456 | -92% | Down Round |

Dunzo | 0.8+ | <0.2 | -75%+ | Write-off |

MyGlamm | 1.2+ | <1.0 | -20%+ | Markdown |

Hike | 1.4 | <1.0 | -30%+ | Markdown |

These markdowns have systemic ripple effects. When a major unicorn is repriced, it sets a new benchmark for every other company in that sector. This is known as the "Anchor Effect." If the market leader is now valued at 5x revenue instead of 50x, every mid-stage startup in the same domain finds it impossible to justify higher multiples during their next funding round.

Mechanics of the Down Round: Contractual Realities

A down round is formally defined as a funding event where a company issues shares at a lower price than in previous rounds. While simple in theory, the structural implications are often devastating for founders and early employees. In the 2025-2026 environment, these rounds were rarely "clean" equity deals; instead, they were laden with "toxic" terms designed to protect new investors at the expense of all other stakeholders.

Anti-Dilution Protection: The Mathematical Squeeze

The most significant contractual lever in a down round is the anti-dilution clause. These provisions safeguard early investors from equity erosion when new shares are issued at a lower price. Two primary methods dominate the Indian landscape:

Full Ratchet: This is the most aggressive form of protection. If the company issues even one share at a lower price, the original investor's conversion price is adjusted downward to match that new price. For example, if an investor bought shares at ₹100 and the company later raises capital at ₹50, the full-ratchet clause effectively doubles the investor's share count without them paying a single rupee more.

Weighted Average: This is a more balanced approach that considers the number of new shares issued and their price. The formula for the new conversion price is typically:

CP2=CP1×A+CA+B

Where CP2 is the new conversion price, CP1 is the old price, A is the total shares outstanding before the round, B is the shares that would have been issued at the old price, and C is the shares actually issued at the new price.

In 2025, over 60% of term sheets for Series B and C rounds in India featured some form of weighted-average anti-dilution, while Full Ratchet became common only in distressed "last-resort" financing.

Liquidation Preferences: The Exit Waterfall

Another "silent" reality is the shift in liquidation preferences. In a buoyant market, the standard is "1x non-participating," meaning the investor gets their money back or their percentage share of the exit, whichever is higher. However, in the 2025-2026 climate, investors began demanding "Participating Preferred" stock or multiples as high as 2x or 3x.

Preference Type | Investor Payout in $100M Exit (on $20M Investment for 20% stake) | Founder/Employee Remaining Pool | Risk Level |

1x Non-Participating | $20M (Investor chooses 20% of $100M) | $80M | Standard |

1x Participating | $20M + 20% of remaining $80M = $36M | $64M | Aggressive |

2x Non-Participating | $40M | $60M | Distressed |

3x Participating | $60M + 20% of remaining $40M = $68M | $32M | Toxic |

The presence of "participating" or "multi-X" preferences creates what is known as a "Broken Cap Table," where founders may own 30% of the company on paper but receive 0% of the proceeds in an exit scenario because the liquidation waterfall is exhausted by investors.

Pay-to-Play Provisions: Enforcing "Skin in the Game"

The use of "Pay-to-Play" provisions surged in 2025. These clauses require existing investors to participate in subsequent (often down) rounds to keep their preferential rights. If an investor refuses to "follow their money," their preferred shares are compulsorily converted to common shares, stripping them of their anti-dilution protection and liquidation preference. This mechanism was frequently used by lead investors to "flush out" passive or zombie funds from the cap table during bridge rounds.

The Bifurcation of Founder Behavior

The current market environment has created a sharp divide in founder outcomes based on their speed of adaptation. Analysis from firms like Kae Capital identifies two distinct groups of founders in the 2025-2026 era.

Group 1: The Successful Adapters

These founders accepted the reality of the "repricing" as early as late 2024. They implemented radical cost-cutting measures, reducing burn by 30-50% within a single quarter. They focused on:

Path to Profitability: Prioritizing break-even over market share.

Unit Economics: Ensuring that contribution margin (CM2) was positive for every transaction.

Runway Extension: Aiming for 24-30 months of runway through internal accruals rather than external raises.

By early 2026, these founders were able to raise follow-on rounds—often at flat or slightly higher valuations—because they had become "Default Alive".

Group 2: The Struggling Holders

These founders continued to follow the "hyper-growth" playbook of 2021, believing they could not "cut their way to success". They maintained high burn rates, assuming that Series A or B funding would be available on traditional timelines. When the funding did not materialize, they were forced into "Bridge-to-Nowhere" rounds—small injections of capital at punitive terms that were burned through in six months. As of early 2026, many of these startups are either in active liquidation or looking for "acqui-hire" exits.

Metric | Group 1: Adapters | Group 2: Holders | Impact on Valuation |

Burn Multiple | < 2x | > 4x | High burn leads to 70% rejection rate |

Focus | EBITDA/Cash Flow | GMV/Top-line | Efficiency commands a premium |

Fundraising Time | 2-3 months | 9+ months (often failing) | Delay signals distress |

Decision Velocity | Fast (Q1 2025) | Slow (Waiting for "normal") | Adaptation is the new pedigree |

Sectoral Divergence: From Consumption to Computation

The "Silent Reality" has affected different sectors with varying intensity. The "rising tide" of 2021 that lifted all boats has been replaced by a "flight to quality" and specialized intellectual property.

EdTech: The End of the Pandemic Premium

EdTech has been the hardest-hit sector in India, with a failure rate approaching 60% in 2025. The pandemic-driven demand for online K-12 education collapsed with the reopening of physical schools. Companies that failed to transition to hybrid or B2B skill-building models faced immediate valuation resets. The "poster boy" Byju's served as a macro-warning, causing a total withdrawal of capital from capital-intensive consumer edtech.

Fintech and Retail: The Regulatory Reality Check

Fintech remains a major destination for capital, but the nature of that capital has changed. Following a series of RBI interventions in 2024 and 2025 regarding unsecured lending and digital payments, the sector has seen a "valuation compression".

Metric Shift: Valuation benchmarks moved from "tech multiples" (10x-20x revenue) to "lending multiples" (2x-4x book value).

Compliance Cost: Increased regulatory oversight added significantly to the "burn" of startups, forcing a consolidation among mid-stage players.

DeepTech and AI: The Scarcity Premium

In contrast to the carnage in consumer-tech, DeepTech and AI startups are thriving. In 2025, Indian deep-tech startups raised $1.06 billion—double the amount raised in the same period in 2024.

Hard IP: Investors are willing to pay a premium for companies with defensible, hard-to-replicate technology in aerospace, robotics, and semiconductor design.

Government Support: Initiatives like the ₹10,000 crore India AI Mission have provided a floor for investment sentiment in these domains.

Valuation Outliers: While SaaS multiples contracted to 5x-7x ARR, high-performing AI ventures continued to command 10x-15x ARR in 2026.

Sector | 2021 Multiples (Typical) | 2025/26 Multiples (Standard) | Survival Driver |

SaaS | 15x - 40x ARR | 5x - 7x ARR | Net Revenue Retention (NRR) |

EdTech | 10x - 20x Rev | 1x - 3x Rev | B2B/Hybrid Transition |

Fintech | 15x - 30x Rev | 2x - 4x Book | Regulatory Compliance |

DeepTech/AI | 8x - 12x Rev | 12x - 20x Rev | Intellectual Property (IP) |

D2C | 4x - 8x Rev | 2x - 5x Rev | Gross Margins (>65%) |

The Impact on Talent and ESOPs

The valuation reset has not only impacted founders and VCs but has fundamentally altered the value proposition for startup employees. For years, Employee Stock Ownership Plans (ESOPs) were marketed as the path to "generational wealth". However, as valuations plummeted, many vested options became "underwater"—where the strike price is higher than the current market price of the shares.

Despite this, 2025 saw a resilient trend in ESOP buybacks, albeit at smaller scales than the 2021 peak. Approximately 12 startups executed buyback programs worth ₹1,409 crore (~$158 million) in 2025, benefiting 9,265 employees.

Major Payouts: PhonePe led with a liquidity event of ₹700-800 crore for nearly 1,000 employees.

Strategic Allotments: Companies like Capillary Technologies doubled their ESOP pool ahead of their ₹2,250 crore IPO to ensure talent retention during the transition to public markets.

Regulatory Relief for Founders

In a landmark move in June 2025, SEBI introduced reforms allowing startup founders to retain and exercise ESOPs even after being classified as "promoters" for an IPO. This removed a significant hurdle where founders were previously forced to liquidate or restructure their stakes, often at disadvantageous prices, just to meet listing requirements. This shift acknowledges the "maturation" of the Indian startup leadership and encourages long-term alignment.

The "IPO Anchor" and the Role of Public Markets

One of the most defining characteristics of the 2025-2026 landscape is the "IPO Anchor Effect." As private funding became more expensive, startups turned to the public markets for liquidity and validation. In 2025, 18 new-age tech startups went public, raising ₹41,284 crore—a 40% increase in capital compared to 2024.

This surge in IPOs has provided the "transparent benchmarks" that were missing during the 2021 boom. Private investors now anchor their valuation models to these listed peers. If a publicly traded SaaS company in India is trading at a specific multiple of EBITDA, a private Series C company cannot justify a valuation that is wildly divergent from that benchmark.

IPO Year | Number of Tech Listings | Total Capital Raised (INR Cr) | Key Significance |

2021 | 11 | 21,500 | Market Exuberance |

2023 | 2 | 4,200 | IPO Drought |

2024 | 6 | 29,247 | Cautious Return |

2025 | 18 | 41,284 | Market Maturation |

2026 (Est.) | 25 - 30 | 55,000+ | Public Confidence |

The success of these IPOs has also been bolstered by the rise of domestic institutional capital. While Foreign Institutional Investors (FIIs) were net sellers in some quarters of 2025, Domestic Institutional Investors (DIIs) and retail investors emerged as a stabilizing force, deploying more than ₹6 lakh crore into the market.

Regulatory Evolution: The End of the Angel Tax

A major friction point in the "Silent Reality" was the "Angel Tax" (Section 56(2)(viib)), which taxed investments received above fair market value as income for the startup. In a down-round scenario, this tax was particularly problematic as FMV calculations often lagged behind market sentiment, leading to protracted disputes with tax authorities.

The abolition of the Angel Tax effective for FY 2025-26 has been a game-changer for the ecosystem. It has:

Reduced Compliance Friction: Founders no longer need to spend months justifying their valuations to the tax department.

Enabled Domestic Funding: Local angel networks and family offices, which were previously deterred by the tax, have returned to the early-stage market.

Facilitated Down Rounds: Distressed companies can now re-price their equity more freely without the fear of triggering a massive tax liability.

Future Outlook: From "Narrative" to "Numbers"

As the Indian startup ecosystem moves toward 2027, the "Silent Reality" is giving way to a new era of institutional maturity. The "funding winter" did not kill the ecosystem; it killed the "unfundable" business models that relied on infinite liquidity.

The Rise of the "Proficorn"

The new aspiration for Indian founders is no longer just "Unicorn" status, but becoming a "Proficorn"—a profitable, sustainable company with a clear path to IPO. Investors in 2026 are primarily looking for:

Efficiency: Companies meeting the "Rule of 40".

Governance: Strong board oversight and transparent financial reporting.

Defensibility: Moats built on technology or deep distribution rather than marketing spend.

Conclusion

The "Silent Reality" of down rounds and markdowns in India between 2023 and 2026 was a necessary phase of consequence. The correction has weeded out speculative ventures and forced a generation of founders to master the fundamentals of business. While the destruction of paper wealth was painful for many, the resulting ecosystem is more resilient, globally competitive, and grounded in the reality of unit economics. As India moves toward its projected 2026-2027 IPO boom, it does so not as a speculative frontier, but as a mature hub for substance-driven innovation.

Read More -

1. From Idea to MVP: A Step-by-Step Guide for Solo Founder

🔗 https://findnstart.com/blogs/from-idea-to-mvp-a-step-by-step-guide-for-solo-founder

2. How to Validate Your Startup Idea in 48 Hours for $0

🔗 https://findnstart.com/blogs/how-to-validate-your-startup-idea-in-48-hours-for-0

3. Remote vs. Local: Does Your Co-Founder Need to Live in the Same City?

🔗 https://findnstart.com/blogs/remote-vs-local-does-your-co-founder-need-to-live-in-the-same-city

4. The 2026 Startup Landscape: What Has Fundamentally Changed (and Why Founder Skills Matter More Than Ever)

5. The Most In-Demand Skills for Startup Founders in 2026

🔗 https://findnstart.com/blogs/the-most-in-demand-skills-for-startup-founders-in-2026

6. How to Find a Technical Co-Founder (Without a Six-Figure Salary)

🔗 https://findnstart.com/blogs/how-to-find-a-technical-co-founder-without-a-six-figure-salary

7. 5 Red Flags to Look for When Choosing a Startup Partner

🔗 https://findnstart.com/blogs/5-red-flags-to-look-for-when-choosing-a-startup-partner

8. How to Pitch Your Idea to Potential Co-Founders

🔗 https://findnstart.com/blogs/how-to-pitch-your-idea-to-potential-co-founders

9. How to Build a Portfolio that Attracts High-Growth Startup Founders

🔗 https://findnstart.com/blogs/how-to-build-a-portfolio-that-attracts-high-growth-startup-founders

10. Equity vs. Salary: How to Split Ownership with Your First Teammate

🔗 https://findnstart.com/blogs/equity-vs-salary-how-to-split-ownership-with-your-first-teammate

11. Why Joining an Early-Stage Startup is Better Than a Corporate Job

🔗 https://findnstart.com/blogs/why-joining-an-early-stage-startup-is-better-than-a-corporate-job

12. The Future of EdTech: Why Developers and Educators Need to Team Up Now

🔗 https://findnstart.com/blogs/the-future-of-edtech-why-developers-and-educators-need-to-team-up-now

13. The Architecture of Symbiosis: Analytical Perspectives on the Five Habits of Successful Startup Duos

14. Finding a Co-Founder in the AI Space: What Skills Should You Look For?

🔗 https://findnstart.com/blogs/finding-a-co-founder-in-the-ai-space-what-skills-should-you-look-for

15. Overcoming Analysis Paralysis and the Strategic Path to Execution

🔗 https://findnstart.com/blogs/overcoming-analysis-paralysis-and-the-strategic-path-to-execution

16. From College Project to Company: How to Find Your Student Co-Founder

🔗 https://findnstart.com/blogs/from-college-project-to-company-how-to-find-your-student-co-founder

17. How to Start a Startup While Working a Full-Time Job

🔗 https://findnstart.com/blogs/how-to-start-a-startup-while-working-a-full-time-job

18. How to Build a HealthTech Startup Without a Medical Degree

🔗 https://findnstart.com/blogs/how-to-build-a-healthtech-startup-without-a-medical-degree

19. The Solitary Architect: Executive Isolation in Entrepreneurship

20. The 2026 Guide to Launching a SaaS as a Solo Developer

21. What Sustainable Growth Actually Looks Like

🔗 https://findnstart.com/blogs/what-sustainable-growth-actually-looks-like

22. The Early Warning Signs Your Startup Is in Trouble

🔗 https://findnstart.com/blogs/the-early-warning-signs-your-startup-is-in-trouble

23. How to Grow Without Burning Out

🔗 https://findnstart.com/blogs/how-to-grow-without-burning-out

24. The Truth About “Runway” Most Founders Ignore

🔗 https://findnstart.com/blogs/the-truth-about-runway-most-founders-ignore

25. Revenue Solves More Problems Than Funding

🔗 https://findnstart.com/blogs/revenue-solves-more-problems-than-funding

26. What No One Tells You About Being a Solo Founder

🔗 https://findnstart.com/blogs/what-no-one-tells-you-about-being-a-solo-founder

27. Why Smart People Quit High-Paying Jobs to Build Startups (And Why Most Regret It)

28. Why Most Startup Advice on Twitter Is Dangerous

🔗 https://findnstart.com/blogs/why-most-startup-advice-on-twitter-is-dangerous

29. Decision Fatigue: The Silent Startup Killer

🔗 https://findnstart.com/blogs/decision-fatigue-the-silent-startup-killer

30. Fear vs Logic: How Founders Actually Make Decisions

🔗 https://findnstart.com/blogs/fear-vs-logic-how-founders-actually-make-decisions

31. How Overthinking Destroys Early Momentum

🔗 https://findnstart.com/blogs/how-overthinking-destroys-early-momentum

32. Ideas Don’t Scale. Systems Do.

🔗 https://findnstart.com/blogs/ideas-dont-scale-systems-do

33. The First Hire That Actually Matters

🔗 https://findnstart.com/blogs/the-first-hire-that-actually-matters

34. How the First 100 Users Decide Your Startup’s Fate

🔗 https://findnstart.com/blogs/how-the-first-100-users-decide-your-startups-fate

35. Why Your Startup Doesn’t Need Growth — It Needs Focus

🔗 https://findnstart.com/blogs/why-your-startup-doesnt-need-growthit-needs-focus

36. Why Most Startups Die Quietly

🔗 https://findnstart.com/blogs/why-most-startups-die-quietly

37. Lessons Learned Too Late by First-Time Founders

🔗 https://findnstart.com/blogs/lessons-learned-too-late-by-first-time-founders

38. The Myth of the “Overnight Success” Startup

🔗 https://findnstart.com/blogs/the-myth-of-the-overnight-success-startup