Distribution Challenges for Canadian SaaS Companies

March 13, 2026 by Harshit Gupta

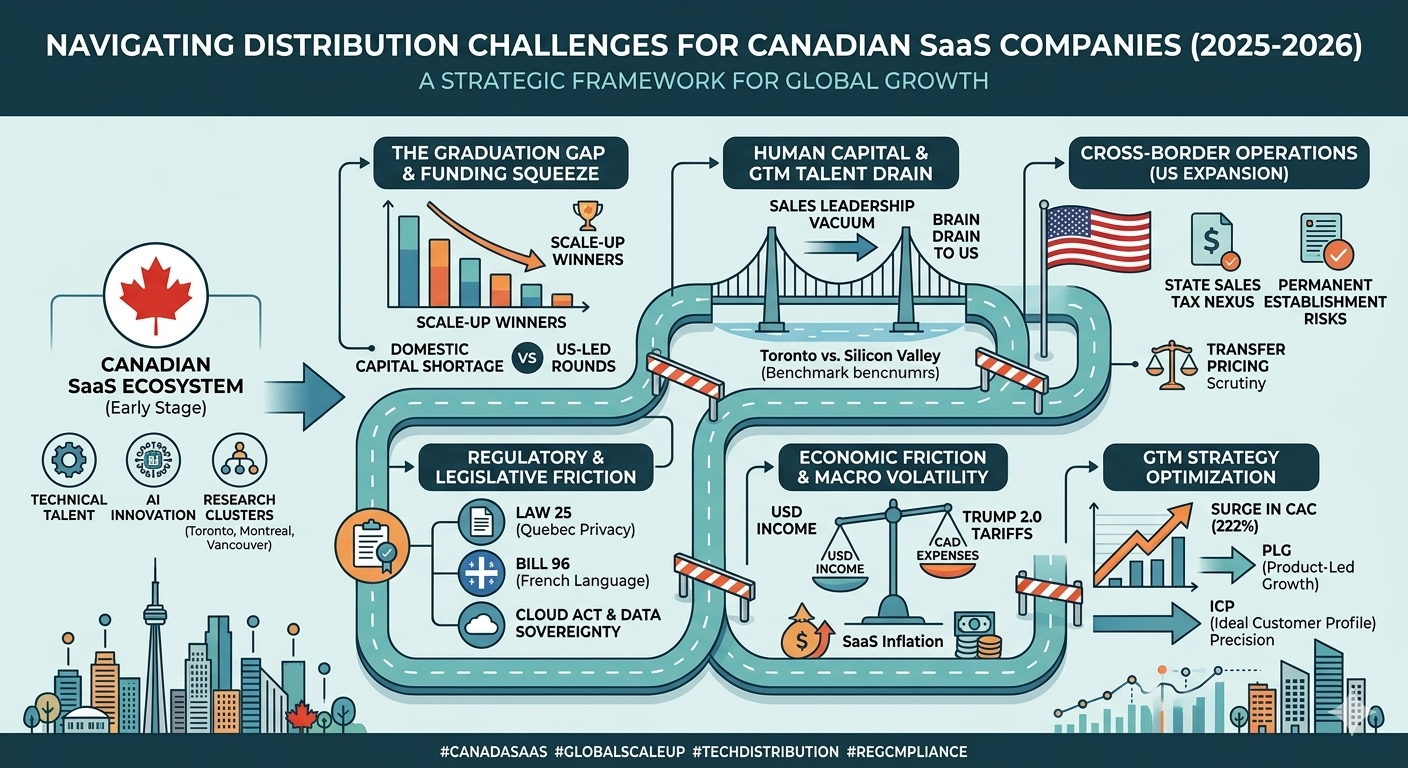

The Canadian Software-as-a-Service (SaaS) ecosystem has entered a period of mature recalibration, transitioning from its historical identity as a nascent collection of technology clusters into a globally competitive, export-driven innovation hub. As of 2025 and looking toward 2026, the sector is defined by its ability to build platforms that are AI-enabled and globally oriented from inception, reflecting a fundamental shift in the Canadian entrepreneurial mindset. However, this maturity is unfolding against a volatile macroeconomic and geopolitical backdrop. Canadian SaaS firms face a unique "scaling paradox": while the domestic environment provides fertile ground for early-stage development through research clusters in Toronto, Montreal, and Vancouver, the transition from a domestic startup to a global enterprise involves navigating a complex landscape of capital shortages, specialized talent drain, and a fragmented regulatory environment.

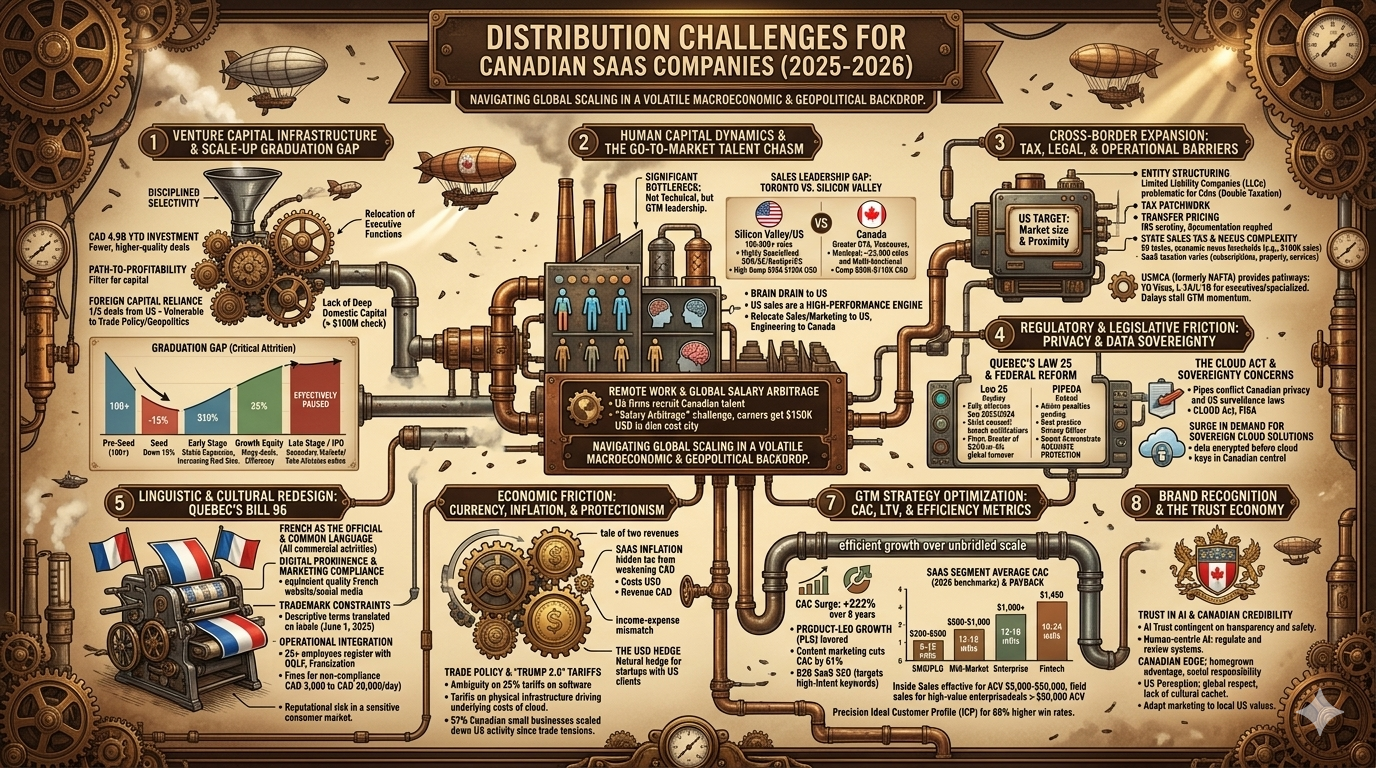

The Venture Capital Infrastructure and the Scale-Up Graduation Gap

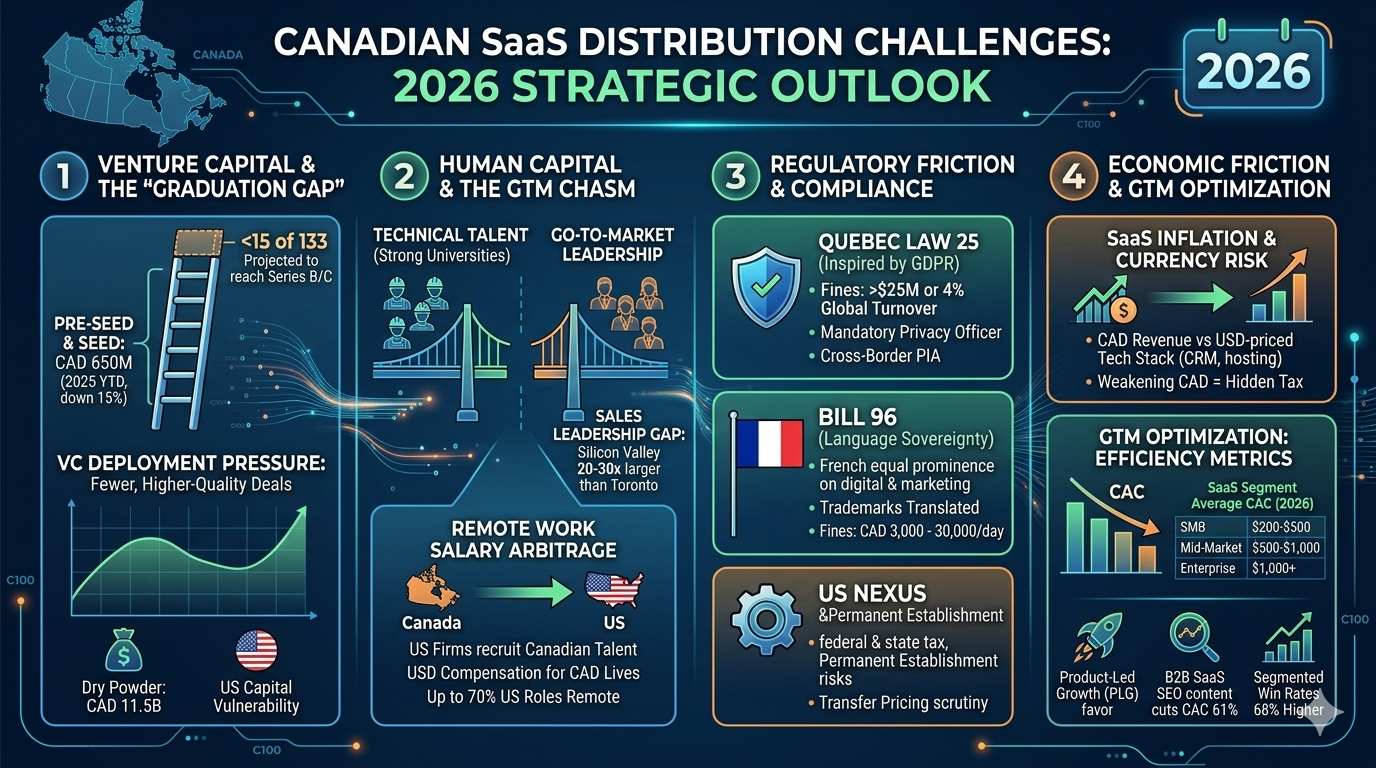

The financial backbone of Canadian SaaS is currently characterized by a state of disciplined selectivity. While total venture investment reached CAD 4.9 billion through the third quarter of 2025, the market is increasingly defined by fewer, higher-quality deals. This trend signals a departure from the "growth at any cost" era, moving toward a model where unit economics and path-to-profitability serve as the primary filters for capital deployment.

Venture Capital Performance and Deployment Pressures

The Canadian venture landscape remains heavily dependent on foreign capital, particularly from the United States, which contributed to approximately one-third of all deals by volume in 2024. This reliance creates a vulnerability to US trade policy and geopolitical instability, as foreign investors may pull back during periods of uncertainty. Despite these risks, domestic institutional support has strengthened. The Venture Capital Action Plan (VCAP) and subsequent initiatives have attracted significant private-sector investment, with Canadian VCs holding approximately CAD 11.5 billion in dry powder as of 2025.

Funding Stage | 2025 YTD Performance (CAD) | Deal Volume Trend | Market Sentiment |

Pre-Seed & Seed | $650 Million | Down 15% vs 2024 | Highly selective; "Price-takers" dominant |

Early Stage | Stable Expansion | Increasing Deal Size | Focus on AI and High-Quality Models |

Growth Equity | Driven by Mega-deals | Concentrated in Winners | Polarized; M&A driven by efficiency |

Late Stage / IPO | Effectively Paused | Secondary Markets Active | Take-private transactions at record highs |

The "graduation gap" remains a critical distribution challenge. For every hundred startups that receive pre-seed funding, only a small fraction reaches the Series B or C stages required for global scale. In the first half of 2025, just 133 pre-seed and seed-stage deals were completed; with typical 10% graduation rates, fewer than 15 of these companies are projected to reach later stages. This attrition is driven by a lack of deep domestic capital pools capable of writing checks exceeding $100 million, forcing firms to seek US-led rounds that often result in the eventual relocation of executive functions and the loss of exit value to foreign markets.

Secondary Markets and the Exit Environment

With the IPO market remaining effectively paused through 2025, secondaries and take-private transactions have emerged as essential liquidity mechanisms. The Canadian private equity market saw CAD 56.5 billion invested across 483 transactions in the first nine months of 2025, driven by mega-deals and a shift toward privatizations to avoid the volatility of public markets. For SaaS companies, this means the distribution of ownership is increasingly shifting toward private equity firms that prioritize operational visibility and cash flow over rapid user acquisition.

Human Capital Dynamics: The Go-to-Market Talent Chasm

The most significant bottleneck for Canadian SaaS distribution is not technical capability, but the availability of senior go-to-market (GTM) leadership. While Canadian universities excel at producing technical talent, the country continues to grapple with a profound "brain drain" of software engineers and experienced sales executives to the United States.

The Sales Leadership Gap: Toronto vs. Silicon Valley

A critical challenge for Canadian SaaS is the relative scarcity of sales professionals who have successfully scaled a B2B platform from $10 million to $100 million in ARR. Silicon Valley remains the global benchmark for this expertise, offering an executive "bench" that is 20 to 30 times larger than that of the Greater Toronto Area (GTA).

Metric | Silicon Valley / US | Canada (Toronto, Vancouver, Montreal) |

Projected Sales Leadership Roles (2026) | 100,000+ | ~22,000 |

Total Venture Investment (Regional) | ~$30 Billion | ~$1 Billion (Ontario) |

Sales Model Specialization | Highly Specialized (SDR, AE, RevOps, CS) | Consultative and Multi-functional |

Compensation (Median Total Comp) | $95K - $130K USD (Leaders) | $80K - $110K CAD (Leaders) |

Talent Attrition Risk | High (Fierce competition) | Lower (Stability and Loyalty) |

Data suggests that US sales culture is characterized by high accountability and specialization, utilizing a "high-performance engine" model where SDRs handle outbound and AEs own the close. In contrast, Canadian sales representatives often lean toward a consultative model, which is effective for complex, trust-based sales but can be slower to scale in high-velocity markets. This discrepancy often leads Canadian SaaS founders to relocate their sales and marketing headquarters to the US while keeping their engineering teams in Canada to leverage lower labor costs and high technical quality.

Remote Work and the Global Salary Arbitrage

The rise of remote work has introduced a new dimension to the talent war. Up to 70% of new sales roles in the US offer remote or hybrid options, allowing US-based firms to recruit Canadian talent directly without requiring relocation. This creates a "salary arbitrage" where Canadian companies must compete with US dollar-denominated compensation packages while operating in a Canadian dollar revenue environment. For a Toronto-based engineer or sales leader, the prospect of earning $150,000 USD while living in a lower-cost Canadian city is a powerful incentive that domestic firms struggle to match without sacrificing their own margins.

Cross-Border Expansion: Tax, Legal, and Operational Barriers

For Canadian SaaS companies, the United States represents the primary target for distribution due to its market size and proximity. However, the transition from a domestic to a cross-border operation involves significant legal and fiscal friction.

Entity Structuring and the Tax Patchwork

A recurring mistake among Canadian founders is the assumption that a Canadian corporate structure can be easily duplicated in the US. The US tax system is highly decentralized, requiring compliance at federal, state, and sometimes municipal levels.

Limited Liability Companies (LLCs): While LLCs are popular for US entrepreneurs due to pass-through taxation, they are frequently problematic for Canadian owners. Canada treats LLCs as corporations, while the US treats them as partnerships or disregarded entities, often leading to double taxation and complex reporting.

Permanent Establishment (PE): Under the Canada-US Tax Treaty, a Canadian business becomes liable for US federal taxes if it maintains a "permanent establishment," such as an office or a habitual sales presence. Even without a physical office, the activities of sales personnel or quality control specialists detail to the US can inadvertently trigger PE status.

Transfer Pricing: Intercompany transactions between a Canadian parent and a US subsidiary must follow "arm’s-length" pricing rules. The IRS scrutinizes these transactions closely, and failure to maintain robust documentation can result in penalties ranging from 20% to 40% of the additional tax owed.

The Complexity of State Sales Tax and Nexus

Unlike Canada's relatively streamlined GST/HST system, the US lacks a national sales tax. Instead, each of the 50 states sets its own rules regarding "nexus"—the level of connection that triggers a requirement to collect and remit sales tax. For SaaS companies, this is particularly treacherous because some states tax software subscriptions as tangible personal property, while others treat them as non-taxable services. If a company reaches an economic nexus threshold (e.g., $100,000 in sales in a specific state), it must register and comply with local filing requirements, adding thousands of dollars in annual compliance costs.

Immigration and Workforce Mobility

Scaling a US presence often requires moving key personnel across the border. While the USMCA (formerly NAFTA) provides pathways for certain professionals through TN visas, more complex moves for executives and specialized knowledge staff require L-1A and L-1B visas. These applications can take weeks or months to process and require proof of a "qualifying relationship" between the Canadian and US entities. Delays in visa processing can stall a company’s GTM momentum during a critical expansion phase.

Regulatory and Legislative Friction: Privacy and Data Sovereignty

The Canadian regulatory environment is currently in a state of rapid evolution, with significant implications for SaaS data architecture and international distribution.

The Rise of Law 25 (Quebec's Bill 64) and Federal Reform

Quebec's Bill 64 (Law 25), which became fully effective in September 2023 and 2024, has fundamentally altered the privacy landscape in Canada. Inspired by the EU's GDPR, it introduces strict requirements for consent, data minimization, and mandatory breach notifications.

Provision | Bill 64 (Law 25) Requirement | PIPEDA (Federal) Standard |

Maximum Fines | Greater of $25M or 4% of global turnover | Currently lower (Admin penalties pending in Bill C-27) |

Privacy Officer | Mandatory designation of an individual | Best practice (Required in some sectors) |

Privacy Impact Assessment (PIA) | Required for all cross-border data transfers | Recommended but not prescriptive |

Data Portability | Individual right to move data between entities | Limited under current framework |

Automated Decision Making | Right to transparency and factor disclosure | Emerging focus in AI regulations |

For SaaS companies, Law 25 represents a significant distribution hurdle. Any firm selling into Quebec must ensure that personal information transferred outside the province receives "adequate protection" based on a formal assessment of the legal framework in the destination jurisdiction. This creates a compliance burden for Canadian firms using US-based cloud providers (AWS, Azure, Google Cloud), as they must demonstrate that the data is protected from foreign intelligence access.

The CLOUD Act and Sovereignty Concerns

A major paradox in Canadian SaaS distribution is the conflict between Canadian privacy laws and US surveillance laws like the CLOUD Act and the Foreign Intelligence Surveillance Act (FISA). Even if a Canadian SaaS company stores data on servers located physically in Canada, if the cloud provider is a US-headquartered corporation, the US government can potentially compel access to that data. This has led to a surge in demand for "sovereign cloud" solutions where data is encrypted before entering the cloud and keys remain under the exclusive control of the Canadian organization. By 2026, at least five major cloud providers are expected to offer infrastructure that keeps data strictly within Canadian borders to mitigate these jurisdictional risks.

The Linguistic and Cultural Redesign: Quebec's Bill 96

Quebec’s Bill 96 has introduced a "redesign" of how business is conducted in Canada, mandating French as the official and common language for all commercial activities within the province. This is not merely a translation requirement but a fundamental shift in digital and operational infrastructure.

Digital Prominence and Marketing Compliance

Under Bill 96, French must not be given lesser prominence than any other language on websites, social media, and digital campaigns accessible to Quebec residents. If a SaaS company's website is available in English, it must also be available in French, with "equivalent quality, functionality, and completeness".

Prominence Requirements: French text on digital ads, signage, and packaging must be at least as visible and prominent as English text. In some cases, such as public signage, French must be at least twice the size of other languages.

Trademark Constraints: As of June 1, 2025, any descriptive or generic terms within a non-French trademark (e.g., "Anti-Frizz" or "High Protein") must be translated into French on product labels and packaging. For SaaS products, this extends to user manuals and promotional inserts.

Operational Integration: Companies with 25 or more employees in Quebec must register with the Office québécois de la langue française (OQLF) and implement "francization" programs, which include conducting internal communications and onboarding in French.

The cost of non-compliance is steep. Fines for a first offense range from CAD 3,000 to CAD 30,000 for corporations per day of non-compliance. Beyond financial penalties, companies face significant reputational risk in a "sensitive consumer market" that increasingly prioritizes linguistic sovereignty.

Economic Friction: Currency, Inflation, and Protectionism

Canadian SaaS companies operate in an environment where macroeconomic fluctuations can have an outsized impact on distribution margins.

The Tale of Two Revenues: SaaS Inflation and Currency Risk

"SaaS inflation" has emerged as a significant challenge for Canadian businesses reliant on USD-priced software tools. Because most major SaaS providers price their offerings in USD, a weakening Canadian dollar acts as a hidden tax.

Income-Expense Mismatch: A company generating revenue in CAD but paying for its tech stack (CRM, hosting, email) in USD sees its effective costs rise with every dip in the exchange rate. For example, a $100 USD/month tool that cost $130 CAD at an exchange rate of 1.30 costs $137 CAD at 1.37.

The USD Hedge: Conversely, Canadian startups with significant US clients are naturally hedged. Because they earn in USD, they are insulated from exchange rate volatility and may even benefit from a weaker CAD when converting revenue back to cover Canadian payroll.

Trade Policy and "Trump 2.0" Tariffs

The trade war dynamics of 2025 and 2026 have introduced further uncertainty. While the USMCA generally provides for a tariff-free digital economy, recent executive orders have imposed 25% tariffs on "products of Canada". There is significant ambiguity regarding whether these tariffs will apply to software products transmitted electronically. Even if software is excluded, the tariffs on physical infrastructure—semiconductors, servers, and data center components—are driving up the underlying costs of cloud services, leading to "cloud surcharges" passed down to Canadian SaaS customers. More than half (57%) of Canadian small businesses have scaled down their US-related activity since these trade tensions began, with 14% cutting ties with the US market altogether to focus on domestic supply chains.

GTM Strategy Optimization: CAC, LTV, and Efficiency Metrics

In the current environment, Canadian SaaS firms are under intense pressure from investors to demonstrate "efficient growth" rather than "unbridled scale."

The Surge in Customer Acquisition Cost (CAC)

Global CAC has increased by 222% over the last eight years due to market saturation and rising costs on traditional paid channels like Google and Meta. For Canadian firms, this necessitates a move toward more efficient acquisition motions.

SaaS Segment | Average CAC (2026 Benchmarks) | Payback Period (Months) |

SMB / Product-Led Growth (PLG) | $200 - $500 | 6 - 12 Months |

Mid-Market | $500 - $1,000 | 12 - 18 Months |

Enterprise | $1,000+ | 18 - 24 Months |

Fintech (Vertical-specific) | $1,450 | Varies |

Product-Led Growth (PLG) has become a favored model in Canada, as it typically yields 50% lower CAC than traditional sales-led motions through self-service acquisition and viral loops. Furthermore, content marketing is reported to cut CAC by 61% compared with paid ads, prompting Canadian firms to invest heavily in specialized "B2B SaaS SEO" that targets high-intent keywords rather than general traffic.

Inside Sales vs. Field Sales in a Geographic Giant

Canada's geography—characterized by a small population spread across a massive landmass—dictates a reliance on "Inside Sales." Field sales, involving face-to-face meetings and travel, cost 40% to 60% more per representative than remote inside sales teams. Inside sales is particularly effective for SaaS products with ACVs between $5,000 and $50,000 and sales cycles under 90 days. However, for high-value enterprise deals exceeding $50,000 ACV, the lack of an "executive bench" in secondary Canadian markets like Calgary or Halifax forces companies to either utilize a hybrid model (inside qualification, field closing) or relocate sales functions to high-density US hubs.

The Win Rate and Segmentation Advantage

Precision in defining the Ideal Customer Profile (ICP) has become a primary driver of distribution success. B2B companies with clearly defined segments and industries in their ICP see 68% higher win rates. Segmented email campaigns, tailored to specific geographic or vertical niches (e.g., "Legal-tech for Canadian mid-market"), generate 760% more revenue than non-segmented campaigns. This "smarter growth" strategy allows Canadian firms to maximize their limited GTM budgets by focusing exclusively on high-potential prospects.

Brand Recognition and the Trust Economy

Canadian SaaS companies must also contend with the "personality" of their brands when expanding into the US market.

Trust in AI and Canadian Credibility

Canada’s reputation for stability, credible corporate governance, and strong privacy alignment provides a "trust signal" for global partners. This is particularly relevant in the era of Generative AI (GenAI). According to the 2026 Telus AI Trust Atlas, 85% of Canadians and 89% of Americans are now using AI, but trust is contingent on transparency and safety.

Human-Centric AI: 90% of respondents in both countries want AI regulated and companies to review systems for potential harms before launch.

The Canadian Edge: Canadian firms that lean into their homegrown advantage—demonstrating social responsibility, inclusivity, and ethical sourcing—are increasingly rewarded by younger consumers (Gen Z and Millennials) who have a particularly negative view of US corporate influence and "ego-driven" trade policy.

US Perception of Canadian Brands

While Canadian companies are viewed with "global respect," they often struggle with a lack of "cultural cachet" compared to Silicon Valley giants. Some brands adopt a "dual citizenship" approach, maintaining the same logo but adapting their marketing message to resonate with local US values. However, successful expansion requires more than just translation; it requires a genuine understanding of local standards. For instance, Tim Hortons has famously struggled to capture the US market despite multiple attempts, while A&W Canada has thrived by adapting its menu to local preferences for grass-fed beef and higher-quality ingredients—a lesson in the importance of localized GTM strategy.

Synthesis and Strategic Outlook for 2026

The distribution landscape for Canadian SaaS is undergoing a fundamental transformation. The focus has shifted from "growth at any cost" to a strategy of "visibility, efficiency, and optionality".

Core Thematic Drivers of the 2026 Environment

The Regulatory Surcharge: Compliance with Law 25 and Bill 96 is no longer an optional "check-the-box" activity; it is a primary driver of product architecture and GTM expense. Companies that fail to internalize these requirements early face significant daily fines and the risk of being excluded from the Quebec market—a vital component of the national economy.

The AI Baseline: AI is no longer a differentiator; it is the "table stakes" for distribution. Companies must leverage AI not just in their products, but in their sales processes to counteract the rising CAC and the shortage of experienced human sales leaders.

The Strategic USD Hedge: For Canadian SaaS, the path to stability lies in aggressive US market entry to establish a USD revenue base that can offset the "SaaS inflation" caused by a fluctuating CAD. This requires navigating the complex "nexus" of state-level taxes and immigration hurdles.

The Mid-Market PE Shift: As IPO activity remains sluggish, the "distribution" of exits is shifting toward private equity. This prioritizes firms that can show clear profitability and a disciplined LTV:CAC ratio (typically 3:1 or better), favoring "smart growth" over high-burn expansion.

The Canadian SaaS ecosystem remains resilient, with a deep well of technical talent and a growing cohort of "unicorns" crossing the nine-figure revenue threshold. However, the next phase of growth will be determined by how effectively these companies can bridge the "graduation gap"—the transition from local innovative startups to sophisticated global scale-ups capable of navigating the geopolitical and regulatory friction of the modern North American market. Success in 2026 and beyond will belong to the founders who view GTM strategy and regulatory compliance not as obstacles, but as the last true competitive moats in a world of rapidly commoditizing technology.

Read More -

1. From Idea to MVP: A Step-by-Step Guide for Solo Founder

🔗 https://findnstart.com/blogs/from-idea-to-mvp-a-step-by-step-guide-for-solo-founder

2. How to Validate Your Startup Idea in 48 Hours for $0

🔗 https://findnstart.com/blogs/how-to-validate-your-startup-idea-in-48-hours-for-0

3. Remote vs. Local: Does Your Co-Founder Need to Live in the Same City?

🔗 https://findnstart.com/blogs/remote-vs-local-does-your-co-founder-need-to-live-in-the-same-city

4. The 2026 Startup Landscape: What Has Fundamentally Changed (and Why Founder Skills Matter More Than Ever)

5. The Most In-Demand Skills for Startup Founders in 2026

🔗 https://findnstart.com/blogs/the-most-in-demand-skills-for-startup-founders-in-2026

6. How to Find a Technical Co-Founder (Without a Six-Figure Salary)

🔗 https://findnstart.com/blogs/how-to-find-a-technical-co-founder-without-a-six-figure-salary

7. 5 Red Flags to Look for When Choosing a Startup Partner

🔗 https://findnstart.com/blogs/5-red-flags-to-look-for-when-choosing-a-startup-partner

8. How to Pitch Your Idea to Potential Co-Founders

🔗 https://findnstart.com/blogs/how-to-pitch-your-idea-to-potential-co-founders

9. How to Build a Portfolio that Attracts High-Growth Startup Founders

🔗 https://findnstart.com/blogs/how-to-build-a-portfolio-that-attracts-high-growth-startup-founders

10. Equity vs. Salary: How to Split Ownership with Your First Teammate

🔗 https://findnstart.com/blogs/equity-vs-salary-how-to-split-ownership-with-your-first-teammate

11. Why Joining an Early-Stage Startup is Better Than a Corporate Job

🔗 https://findnstart.com/blogs/why-joining-an-early-stage-startup-is-better-than-a-corporate-job

12. The Future of EdTech: Why Developers and Educators Need to Team Up Now

🔗 https://findnstart.com/blogs/the-future-of-edtech-why-developers-and-educators-need-to-team-up-now

13. The Architecture of Symbiosis: Analytical Perspectives on the Five Habits of Successful Startup Duos

14. Finding a Co-Founder in the AI Space: What Skills Should You Look For?

🔗 https://findnstart.com/blogs/finding-a-co-founder-in-the-ai-space-what-skills-should-you-look-for

15. Overcoming Analysis Paralysis and the Strategic Path to Execution

🔗 https://findnstart.com/blogs/overcoming-analysis-paralysis-and-the-strategic-path-to-execution

16. From College Project to Company: How to Find Your Student Co-Founder

🔗 https://findnstart.com/blogs/from-college-project-to-company-how-to-find-your-student-co-founder

17. How to Start a Startup While Working a Full-Time Job

🔗 https://findnstart.com/blogs/how-to-start-a-startup-while-working-a-full-time-job

18. How to Build a HealthTech Startup Without a Medical Degree

🔗 https://findnstart.com/blogs/how-to-build-a-healthtech-startup-without-a-medical-degree

19. The Solitary Architect: Executive Isolation in Entrepreneurship

20. The 2026 Guide to Launching a SaaS as a Solo Developer

21. What Sustainable Growth Actually Looks Like

🔗 https://findnstart.com/blogs/what-sustainable-growth-actually-looks-like

22. The Early Warning Signs Your Startup Is in Trouble

🔗 https://findnstart.com/blogs/the-early-warning-signs-your-startup-is-in-trouble

23. How to Grow Without Burning Out

🔗 https://findnstart.com/blogs/how-to-grow-without-burning-out

24. The Truth About “Runway” Most Founders Ignore

🔗 https://findnstart.com/blogs/the-truth-about-runway-most-founders-ignore

25. Revenue Solves More Problems Than Funding

🔗 https://findnstart.com/blogs/revenue-solves-more-problems-than-funding

26. What No One Tells You About Being a Solo Founder

🔗 https://findnstart.com/blogs/what-no-one-tells-you-about-being-a-solo-founder

27. Why Smart People Quit High-Paying Jobs to Build Startups (And Why Most Regret It)

28. Why Most Startup Advice on Twitter Is Dangerous

🔗 https://findnstart.com/blogs/why-most-startup-advice-on-twitter-is-dangerous

29. Decision Fatigue: The Silent Startup Killer

🔗 https://findnstart.com/blogs/decision-fatigue-the-silent-startup-killer

30. Fear vs Logic: How Founders Actually Make Decisions

🔗 https://findnstart.com/blogs/fear-vs-logic-how-founders-actually-make-decisions

31. How Overthinking Destroys Early Momentum

🔗 https://findnstart.com/blogs/how-overthinking-destroys-early-momentum

32. Ideas Don’t Scale. Systems Do.

🔗 https://findnstart.com/blogs/ideas-dont-scale-systems-do

33. The First Hire That Actually Matters

🔗 https://findnstart.com/blogs/the-first-hire-that-actually-matters

34. How the First 100 Users Decide Your Startup’s Fate

🔗 https://findnstart.com/blogs/how-the-first-100-users-decide-your-startups-fate

35. Why Your Startup Doesn’t Need Growth — It Needs Focus

🔗 https://findnstart.com/blogs/why-your-startup-doesnt-need-growthit-needs-focus

36. Why Most Startups Die Quietly

🔗 https://findnstart.com/blogs/why-most-startups-die-quietly

37. Lessons Learned Too Late by First-Time Founders

🔗 https://findnstart.com/blogs/lessons-learned-too-late-by-first-time-founders

38. The Myth of the “Overnight Success” Startup

🔗 https://findnstart.com/blogs/the-myth-of-the-overnight-success-startup