Defense & Dual-Use Tech Is Going Mainstream

March 11, 2026 by Harshit Gupta

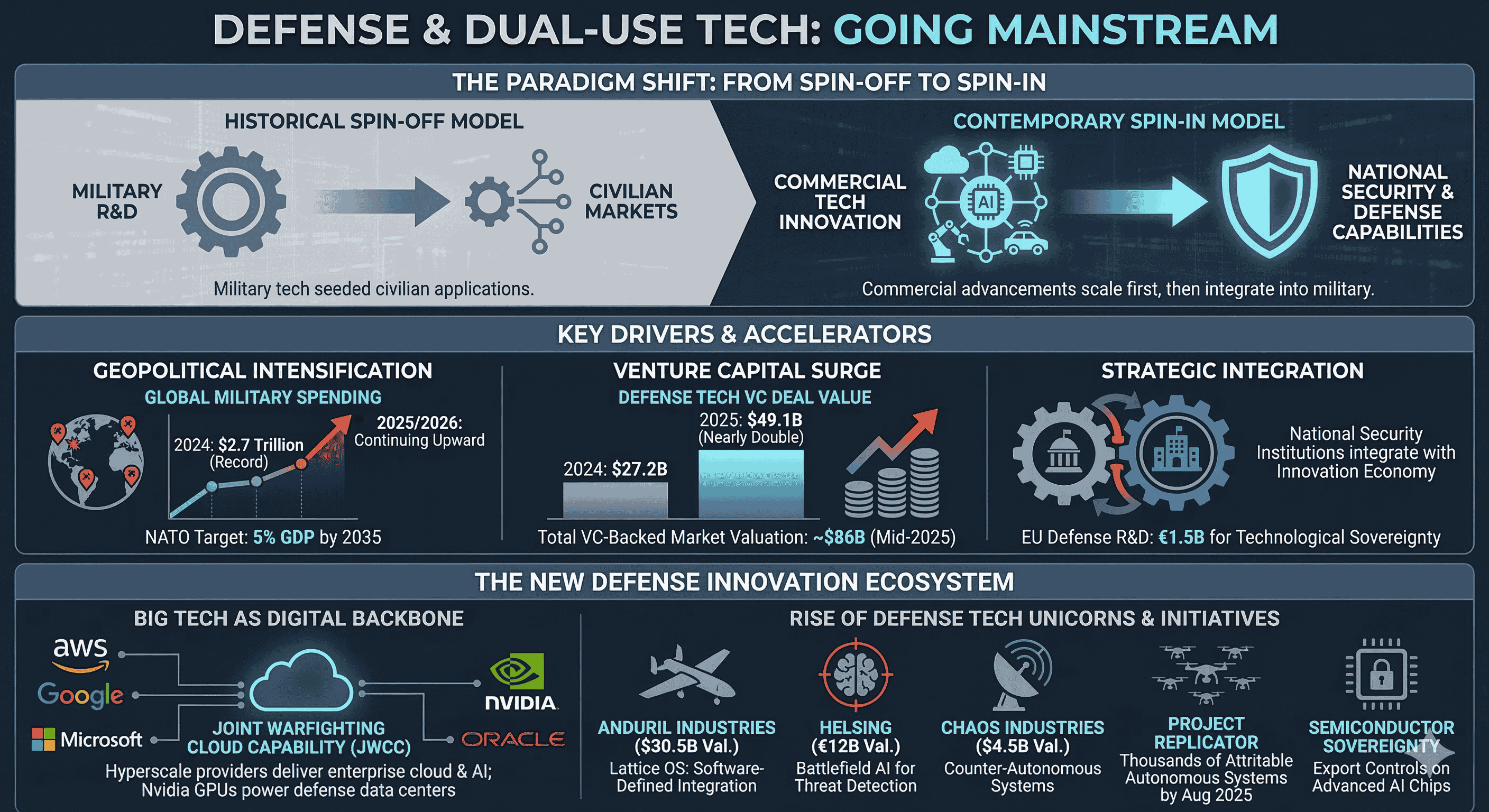

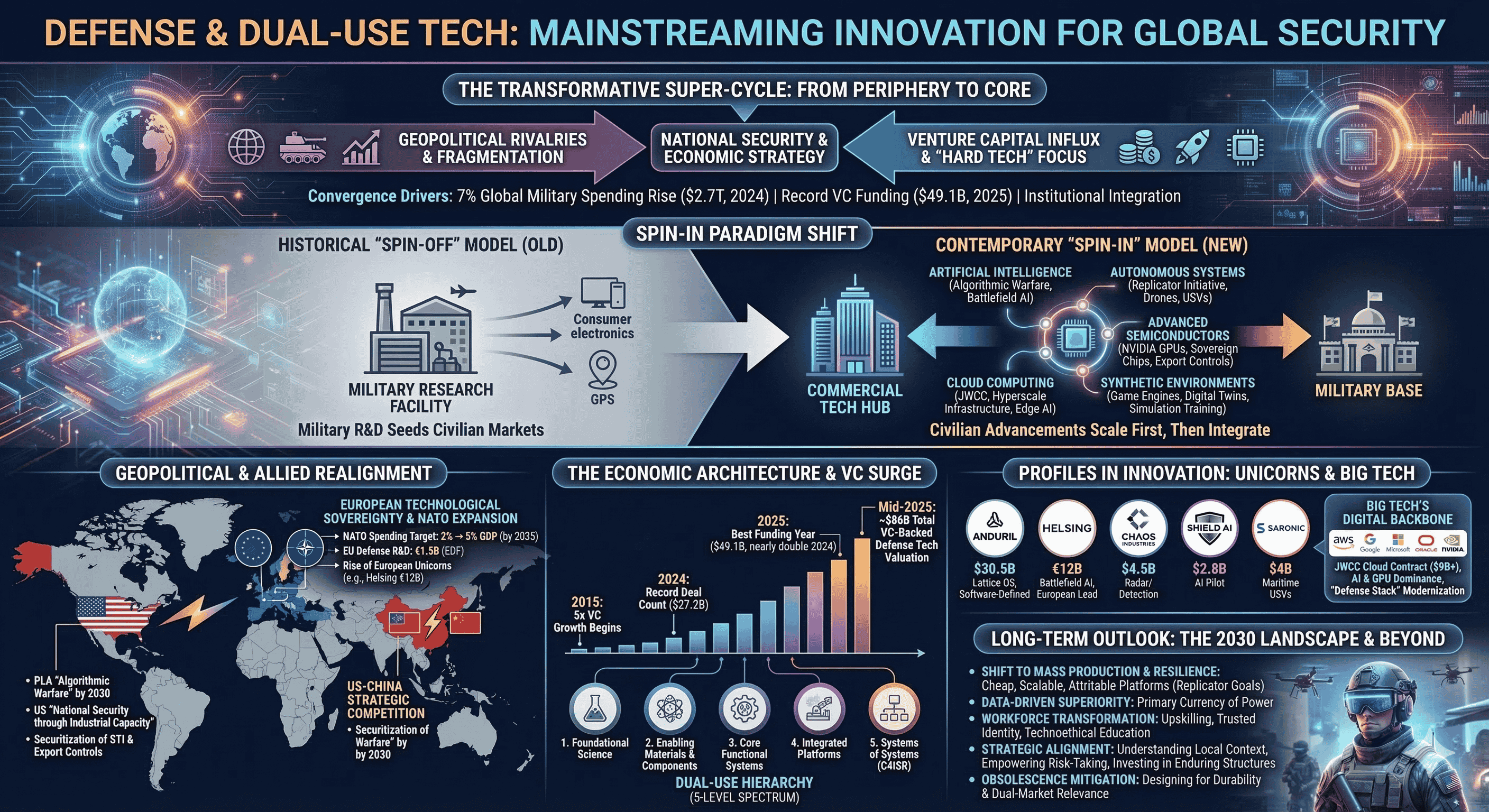

The global defense landscape is currently traversing its most transformative period since the end of the Cold War. This transition is defined by the mainstreaming of dual-use technologies—innovations that serve both civilian and military applications—which have moved from the periphery of the tech sector to the core of national security and economic strategy. This structural shift represents a fundamental reversal of the historical "spin-off" model, where military research once seeded civilian markets. In the contemporary era, the paradigm is one of "spin-in," where advancements in artificial intelligence, autonomous systems, and cloud computing are scaled first in the commercial sector before being integrated into military capabilities. This evolution is driven by a convergence of intensifying geopolitical rivalries, a massive influx of venture capital into "hard tech," and a recognition by national security institutions that they must integrate more deeply into the broader innovation economy to maintain a competitive edge.

Geopolitical Drivers and the New Super-Cycle of Defense Spending

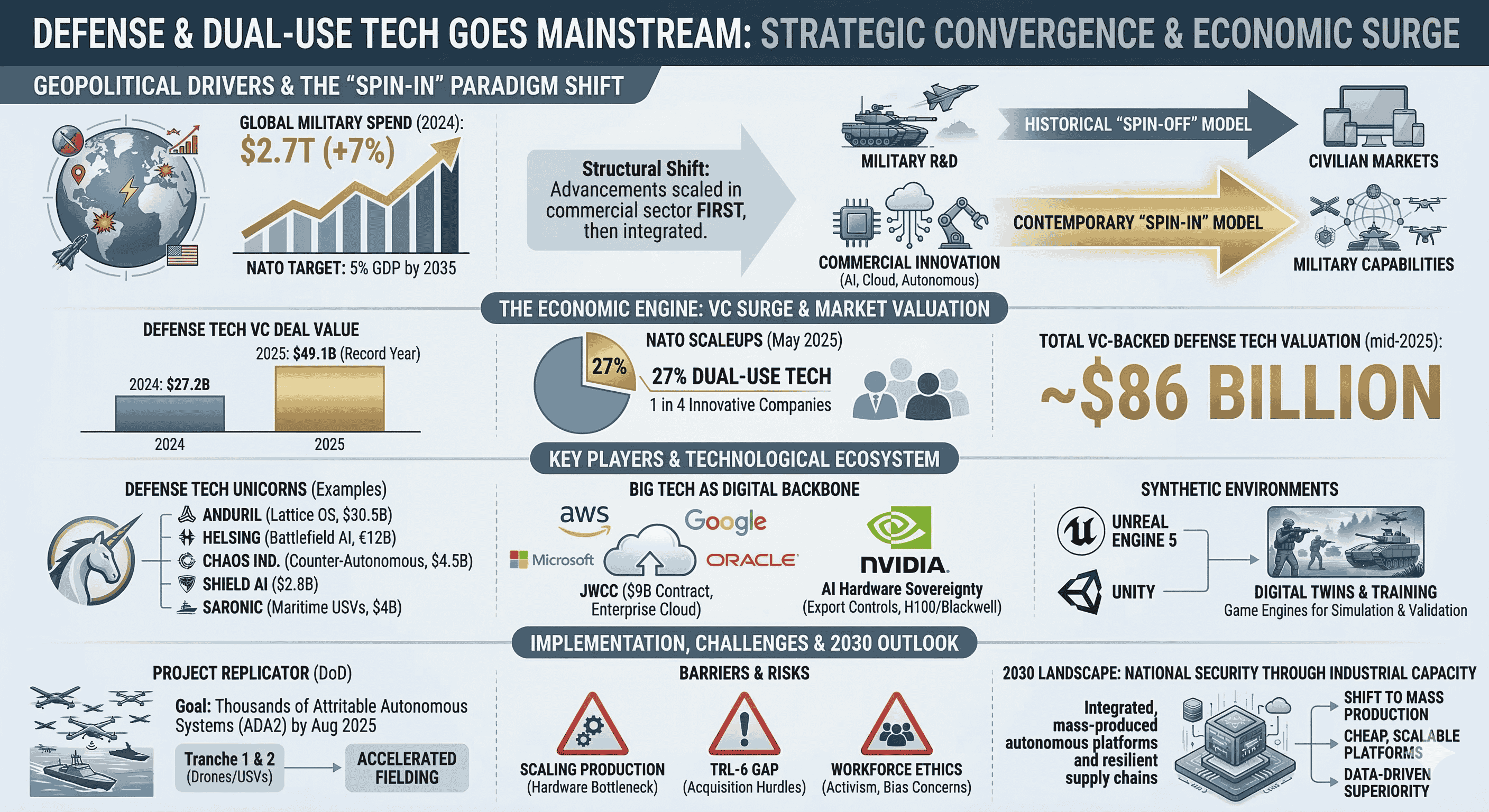

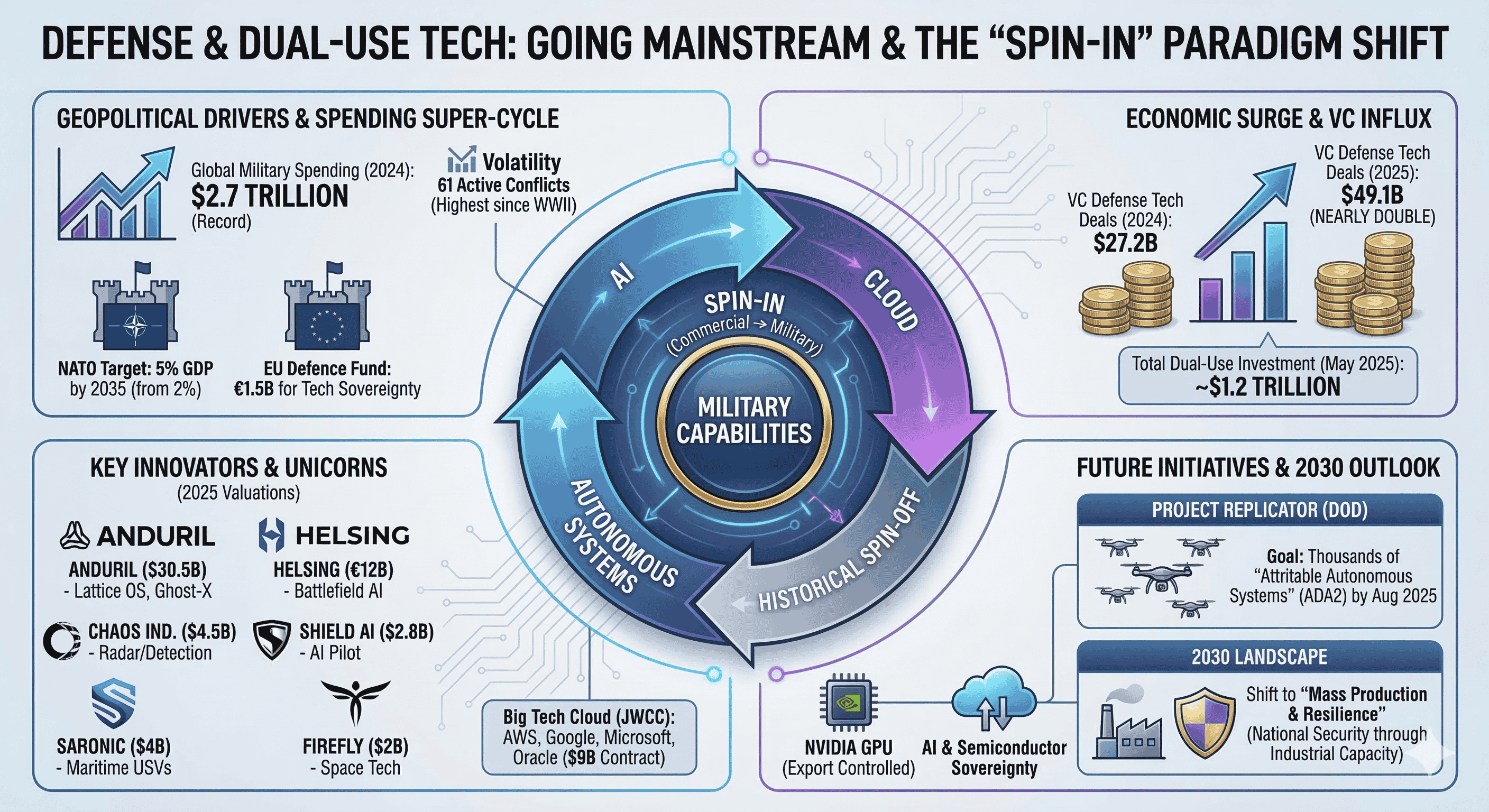

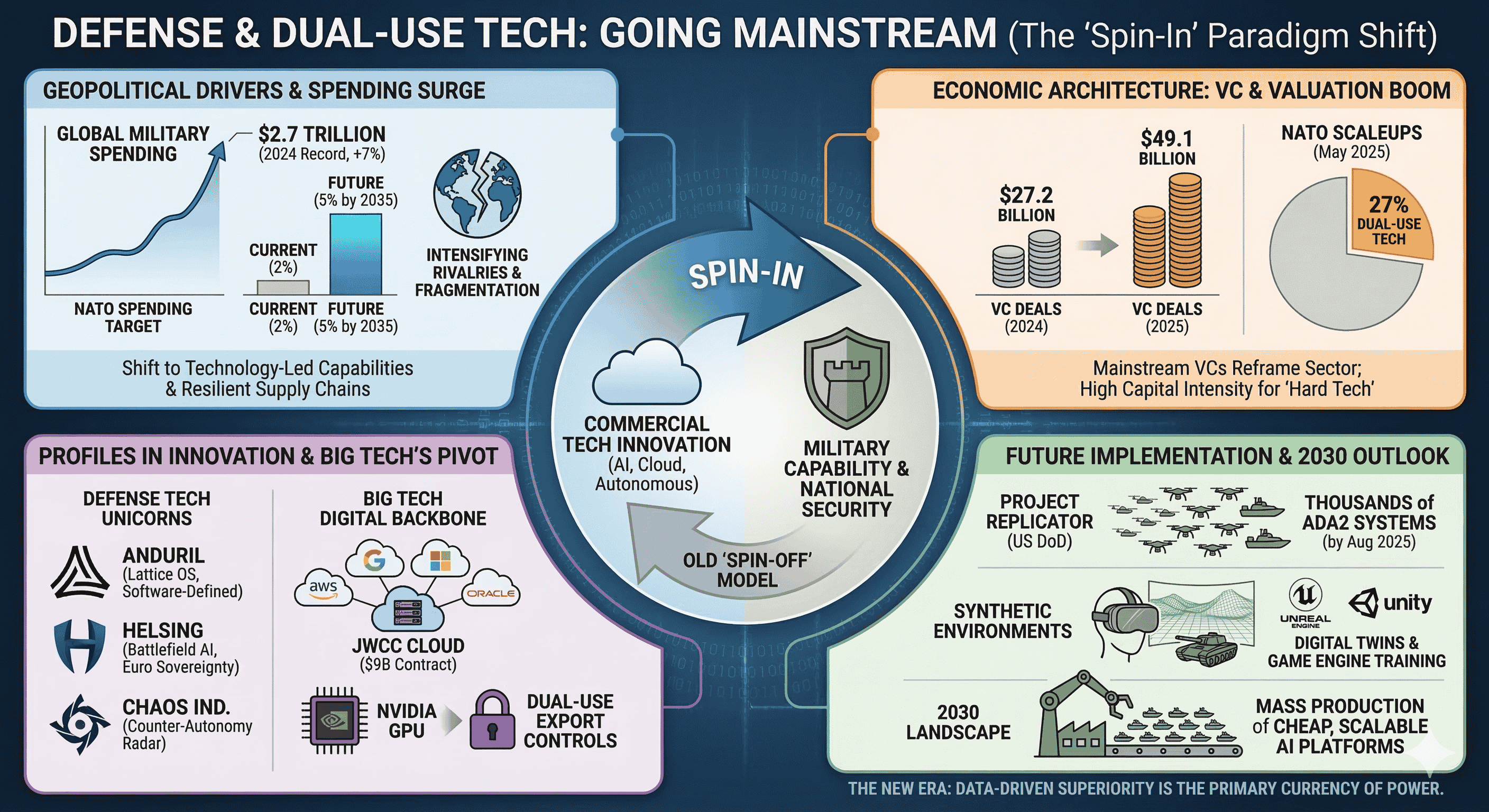

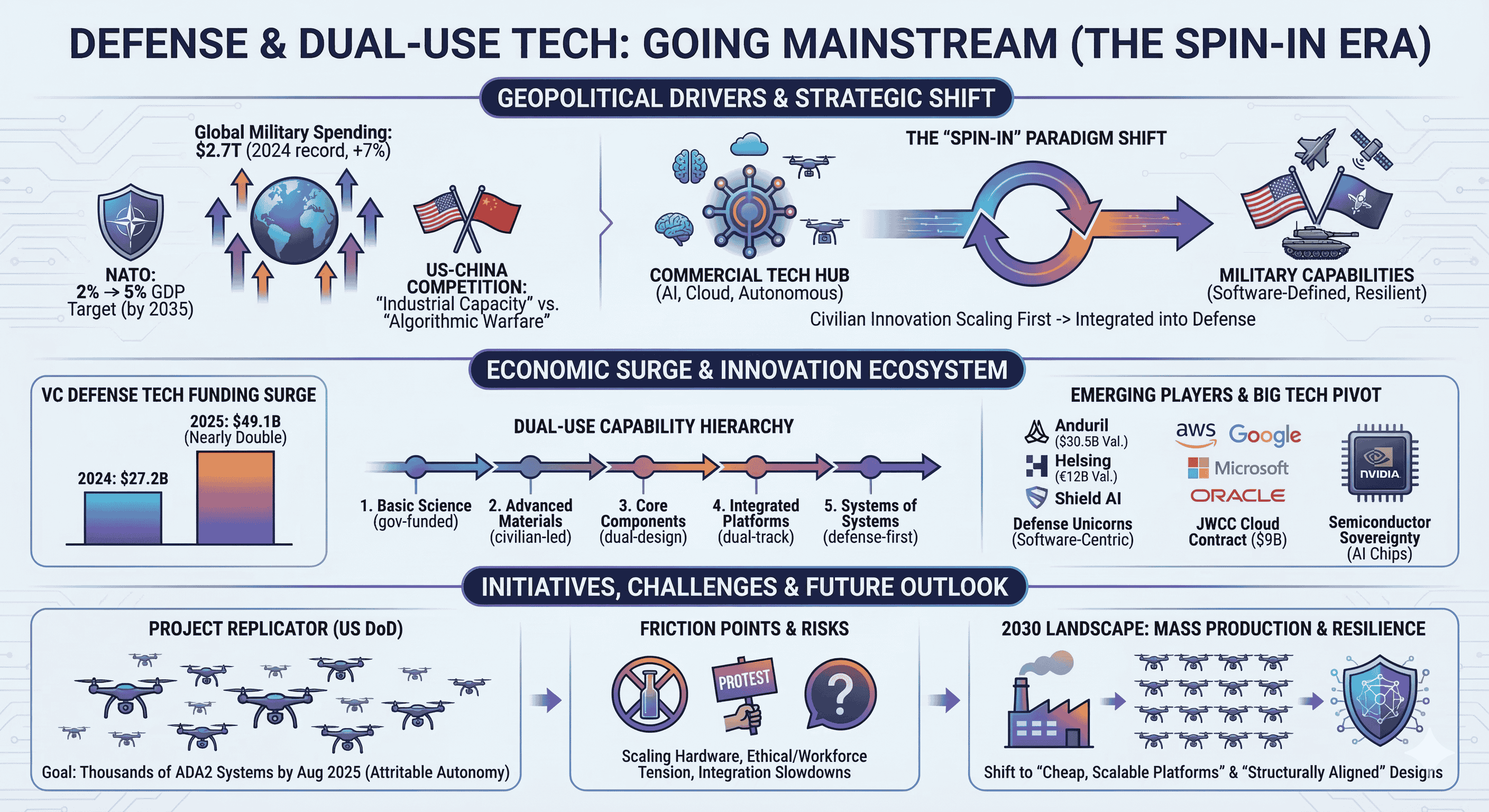

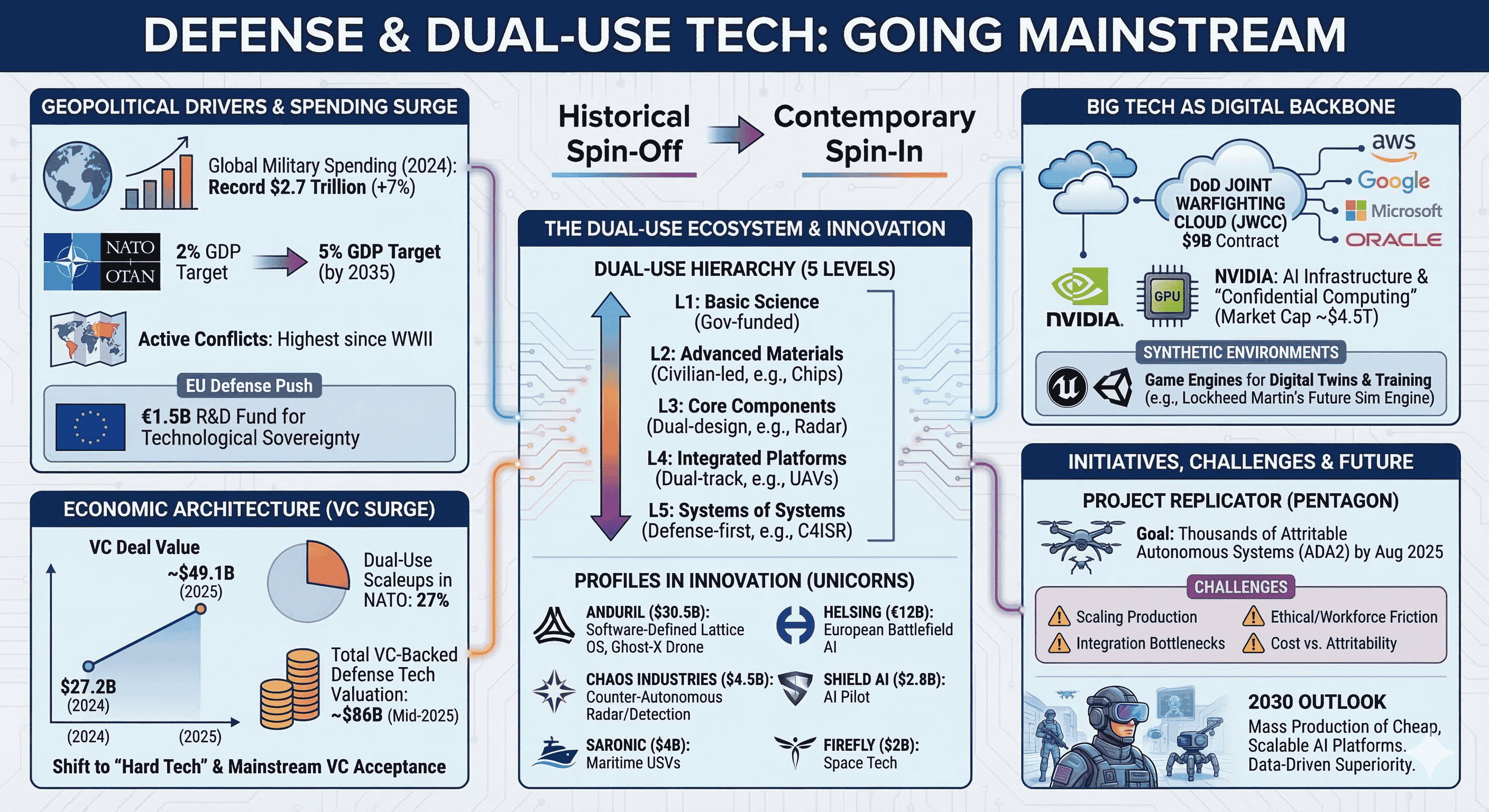

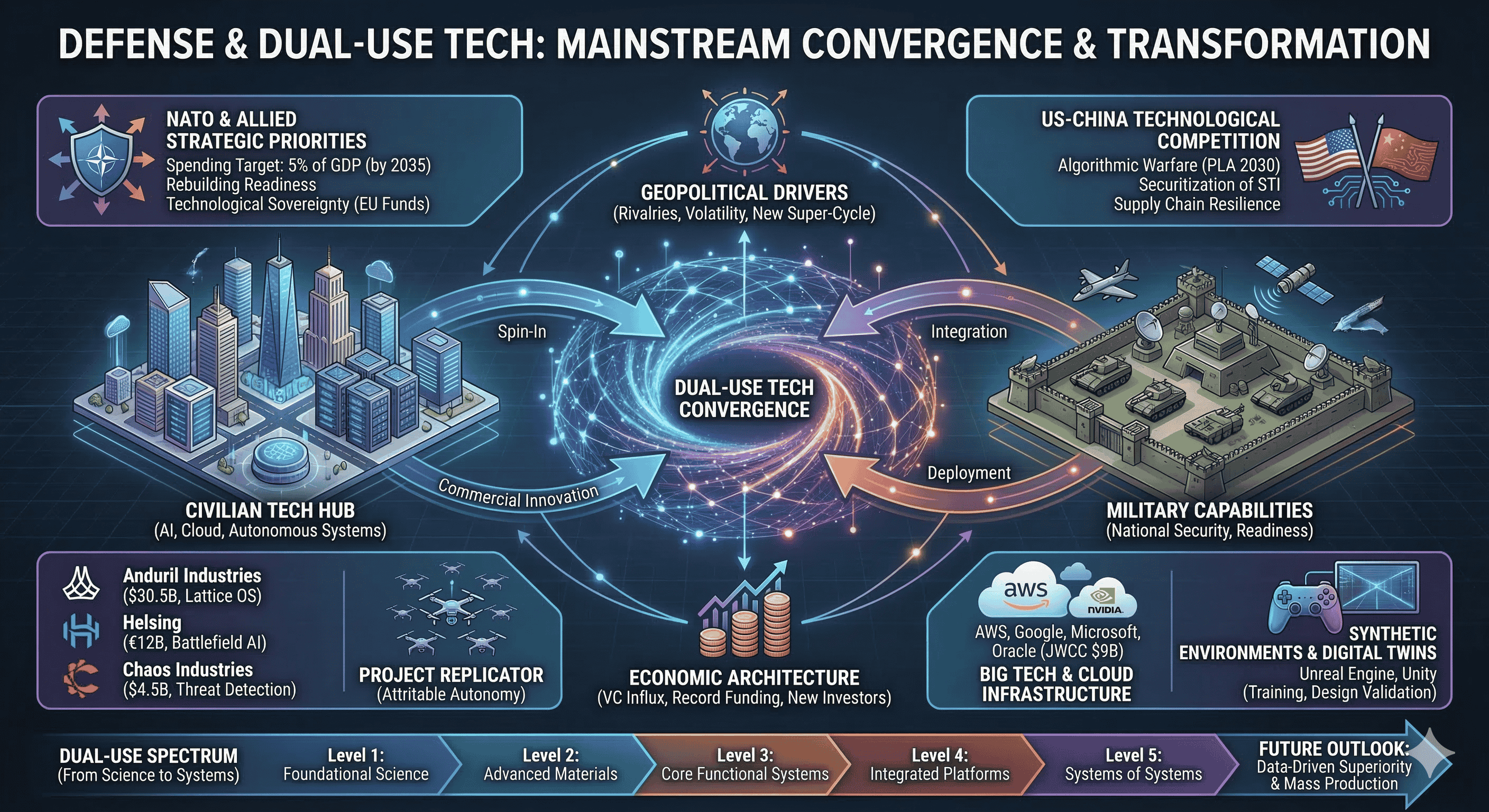

The acceleration of dual-use technology adoption is fundamentally a response to an increasingly volatile global environment. Geopolitical fragmentation has accelerated as military spending increased by 7% globally in 2024, reaching a record $2.7 trillion. This surge is not merely a quantitative increase in traditional hardware but represents a structural shift toward technology-led military capabilities. The world entered 2025 operating in a threat environment where technological evolution outpaced traditional acquisition cycles, necessitating a transition toward software-defined warfare and resilient supply chains.

The Reconfiguration of NATO and Allied Strategic Priorities

NATO members have committed to the most significant defense expansion in modern history, agreeing to raise annual spending targets from 2% to a benchmark of 5% of GDP by 2035. This structural realignment is designed to rebuild readiness after decades of underinvestment and to accelerate the transition toward a technologically advanced posture. In 2024, the global military burden—the share of GDP spent on defense—rose to 2.5%, reflecting a world where physical strength is increasingly reinforced by data-driven superiority.

Europe, in particular, has emerged as a critical hub for defense innovation. The European Union committed €1.5 billion to defense-related research and development through initiatives like the European Defence Fund, aiming for "technological sovereignty". National programs in the United Kingdom, Germany, and the Netherlands have followed suit, with Germany doubling its military procurement budget and the UK pledging hundreds of millions for innovation. This European push is characterized by a desire to develop indigenous capabilities in AI and robotics, reducing dependence on US-dominated platforms.

Geopolitical Metric | 2024 Actual | 2025/2026 Target | Strategic Implication |

Global Military Expenditure | $2.7 Trillion | Continuing Upward | Entry into a new "Super-Cycle" |

NATO Spending Target | 2% of GDP | 5% of GDP (by 2035) | Secular expansion of defense budgets |

Active State Conflicts | 61 | High Volatility | Highest level of conflict since WWII |

EU Defense R&D Budget | €1.5 Billion | Sustained Growth | Pursuit of strategic autonomy |

Global Military Burden | 2.5% of GDP | Increasing | Shift toward high-tech rearmament |

The US-China Technological Competition

The contemporary geopolitical landscape is defined by the strategic competition between the United States and China. This rivalry has moved beyond bilateral trade and investment flows into the realm of emerging critical technologies. China views artificial intelligence as essential for military modernization, with the People's Liberation Army planning to deploy "algorithmic warfare" capabilities by 2030. In response, the US has implemented a "doctrine of national security through industrial capacity," conditioning market access on supply chain resilience and technological alignment with security priorities.

This competition has led to the "securitization" of science, technology, and innovation (STI). Governments are increasingly implementing policies that orient research funding toward economic and national security while introducing restrictions on sharing research with dual-use potential. This environment of "volatility, uncertainty, complexity, and ambiguity" (VUCA) has made dual-use technologies the central element in evolving global security dynamics.

The Economic Architecture of the Dual-Use Surge

The influx of private capital into the defense sector represents a historic shift in investor behavior. Venture capital investments in defense-focused companies grew fivefold in value over the past decade, reaching a record deal count in 2024. By 2025, defense tech startups had their best funding year ever, with the value of venture deals jumping to $49.1 billion, nearly doubling the $27.2 billion recorded in 2024.

Venture Capital Trends and Market Valuations

The total estimated market valuation of VC-backed defense tech firms, excluding major aerospace conglomerates, reached approximately $86 billion by mid-2025. This growth is fueled by "mainstream venture" firms that have dropped previous ethical objections to defense, reframing the sector as a supporter of democratic values and human rights. By May 2025, dual-use tech scaleups made up 27% of the total scaleup population in NATO countries, meaning one in four innovative companies is developing technology with potential military applications.

Investment Data Segment | Q3 2024 | May 2025 | Growth Percentage |

Global Dual-Use Investment | $954.5 Billion | ~$1.2 Trillion | 25% |

Defense Tech Specific Investment | $55.7 Billion | $70.8 Billion | 27% |

Defense Tech Equity Funding | $7.3 Billion | $17.9 Billion | 145% |

VC Defense Tech Exits | $18.2 Billion | $54.4 Billion | 199% |

Active Defense Tech Investors | ~210 Firms | ~300+ Firms | 41% |

The capital intensity of these firms is significantly higher than that of civilian startups. Pure defense tech scaleups raise an average of $80 million, compared to $66 million for dual-use tech and $50 million for purely civilian tech scaleups. This is due to the "hard tech" nature of the sector, which requires long R&D cycles, specialized manufacturing capacity, and navigating outdated acquisition models.

Barriers to Mainstreaming: Fragility and Scaling

Despite the surge in capital, dual-use innovation faces substantial challenges. Startups often suffer from a "not here nor there" syndrome, torn between two demanding markets without fully committing to either, which can dilute strategic focus. Furthermore, most startups lack the infrastructure to scale hardware production to battlefield requirements. Military organizations are often unaccustomed to working with Technology Readiness Level (TRL) 6-stage startups, creating a deployment bottleneck.

Exit opportunities also remain a friction point. While acquisitions by larger firms like Nvidia or defense primes are increasing, national security restrictions often block foreign mergers and acquisitions. This creates a limited pool of local buyers, though public listings like Renk and TKMS signify a growing momentum for transparency and liquidity in the sector.

Defining the Dual-Use Hierarchy: A Five-Level Spectrum

The strategic power of dual-use technologies is realized when they are adapted across both civilian and military domains. Expert analysis identifies a spectrum of five distinct capability categories, ranging from basic science to complex integrated systems.

Level 1: Foundational Science and Process Capabilities

This includes basic research in chemistry, physics, metallurgy, and advanced manufacturing. These technologies are not inherently civil or military and typically emerge from government-funded basic research. Military actors benefit indirectly by shaping strategic research agendas at this level.

Level 2: Enabling Advanced Materials and Components

Materials such as carbon fiber, high-density batteries, and advanced semiconductors serve as the critical building blocks for all modern platforms. In these areas, civilian markets typically dominate the scale, and military actors "top up" investment or create a demand pull through preferential procurement.

Level 3: Core Functional Systems

Radar modules, secure communication blocks, and vision systems represent genuine dual-use convergence. Developers must design these components with military applications in mind from the outset to ensure they meet defense specifications. Government involvement at this stage is proactive, providing targeted funding and validation facilities.

Level 4: Integrated Platforms

This category includes Unmanned Aerial Vehicles (UAVs), rotary aircraft, and tactical ground vehicles. Integration requires early and simultaneous consideration of both civil and defense requirements. Governments support this through dual-track certification frameworks and interoperability testing. However, as procurement decisions move closer to military end-users, solutions can become bespoke and less scalable.

Level 5: Systems of Systems

At the extreme end are complex defense-first solutions like integrated air defense networks and battlefield management platforms (C4ISR). While military use cases dominate initial development, civilian applications may emerge over time in areas like border security and emergency response.

Profiles in Innovation: The Rise of Defense Tech Unicorns

The current transformation is exemplified by a new breed of defense startups that challenge traditional industry giants through speed, software-centric approaches, and substantial venture backing.

Anduril Industries: The Software-Defined Leader

Anduril Industries, valued at $30.5 billion following a record $2.5 billion Series G round in June 2025, has become the poster child for Silicon Valley innovation in defense. The company’s core innovation is the Lattice OS, an AI-enabled operating system that integrates multiple autonomous systems—including the Ghost-X drone and counter-UAS platforms—into a unified battlefield network. Anduril’s approach shifts defense from a hardware-first to a software-defined model, emphasized by its massive drone manufacturing facility in Ohio, which addresses critical US production capacity needs.

Helsing: European Battlefield AI

Helsing has emerged as Europe’s largest defense tech unicorn, with a valuation of €12 billion (~$13.9 billion USD) as of June 2025. Based in Munich, Helsing focuses on developing battlefield AI software for threat detection and decision-making, providing an alternative to US-dominated technology. Its rapid rise represents the continent’s commitment to "technological sovereignty" and has been a primary driver of the 67% increase in European defense tech deal counts.

Chaos Industries and the Threat Detection Revolution

Founded in 2022, Chaos Industries reached a $4.5 billion valuation in just three years. The company specializes in advanced radar technology and communication systems designed to detect autonomous threats like drones and missiles—a mission-critical capability validated by recent conflicts in Ukraine and Gaza. Its $510 million Series D funding in late 2025 reflects the urgent sector need for counter-autonomous weapons systems.

Unicorn Company | Primary Focus | Key Metrics (2025) | Market Importance |

Anduril Industries | Autonomous Systems/Lattice OS | $30.5B Valuation; $2.5B Series G | Software-first battlefield integration |

Helsing | Battlefield AI Software | €12B Valuation; €600M Series D | European technological sovereignty |

Chaos Industries | Radar/Detection Systems | $4.5B Valuation; $510M Series D | Counter-autonomous warfare |

Shield AI | AI Pilot/Autonomous Drones | $2.8B Valuation | AI systems for complex operations |

Saronic | Maritime USVs | $4B Valuation; $600M Series B | Revolutionizing naval warfare |

Firefly Aerospace | Space Tech/Defense | $2B Valuation | Expansion of defense space operations |

Project Replicator and the Future of Attritable Autonomy

The US Department of Defense’s "Replicator" initiative is perhaps the most ambitious effort to field dual-use technology at scale. Launched in August 2023, the goal of Replicator 1.0 is to deliver "all-domain attritable autonomous systems" (ADA2) to warfighters at a scale of multiple thousands by August 2025. These platforms are designed to be affordable and expendable, allowing commanders to tolerate higher risk and counter adversarial buildup in the Indo-Pacific.

Tranches and Technical Implementation

Replicator 1.0 has progressed through two tranches (1.1 and 1.2), selecting maritime and aerial drones for mass manufacturing. By June 2025, defense officials reported that "enormous strides" had been made, with thousands of uncrewed systems delivered to military personnel on an accelerated timeline. The initiative has leveraged the Defense Innovation Unit (DIU) and more than 800 participating companies, with 75% being non-traditional defense contractors.

Replicator 2.0, announced in September 2024, shifts focus to the warfighter priority of countering small uncrewed aerial systems (C-sUAS). This phase aims to assist with production capacity and system integration, overcoming policies and authorities that have historically slowed technology adoption.

Participating Vendors and "The Gauntlet"

The vendor base for Replicator includes a mix of established startups and specialized hardware makers. In early 2026, the "Drone Dominance Program" identified several vendors for participation in "the Gauntlet," a competitive evaluation event at Fort Benning, Georgia.

Vendor | Primary Capability | Sector |

Kratos SRE, Inc. | Unmanned vehicles/electronics | Established Defense Tech |

Neros, Inc. | Low-cost expendable drones | Mass Production |

Teal Drones Inc. | Small UAS/Blue UAS | Reconnaissance |

Auterion Government Solutions | Drone operating systems | Software/Infrastructure |

Firestorm Labs, Inc. | Modular drone manufacturing | 3D Printing/Rapid Prototyping |

ModalAI, Inc. | Blue UAS development | Component Level |

Swarm Defense Technologies | Multi-domain coordination | Swarm Intelligence |

Risks and Challenges in Replicator

Despite high-level leadership focus, the Replicator initiative has faced significant scrutiny. Reports indicate that some systems have been unreliable or integration with existing command structures has been slow. A 2025 Army memo highlighted "fundamental" security issues in communications modernization efforts led by firms like Anduril and Palantir, labeling them "very high risk" due to concerns over software verification and user control. Furthermore, the cost of "attritable" systems remains a point of contention; for example, the Switchblade 600 kamikaze drone costs over $100,000 per unit, while Ukrainian counterparts developed for similar purposes cost as little as $300.

Big Tech and the Cloud-Driven Military-Industrial Complex

The mainstreaming of defense tech is not limited to startups; it involves the fundamental repositioning of "Big Tech" as the digital backbone of modern warfare. The Department of Defense (DoD) has increasingly relied on commercial cloud and AI providers to modernize its "defense stack".

The Joint Warfighting Cloud Capability (JWCC)

In 2022, the DoD awarded the $9 billion JWCC contract to four hyperscale providers: Amazon Web Services (AWS), Google, Microsoft, and Oracle. By 2025, the JWCC had awarded more than $3 billion in task orders, providing enterprise-level cloud services across all security tiers and classification levels. These services enable "mission-critical reliability" and access to generative AI tools for Sailors and Marines at the tactical edge.

The success of JWCC has led to the development of "JWCC Next," planned for a 2027 award. This sequel aims to open the door to smaller, non-traditional cloud providers and companies offering specialized AI and satellite technologies. The goal is to create a multi-cloud ecosystem that avoids vendor lock-in and accelerates digital transformation.

The Role of NVIDIA and Semiconductor Sovereignty

Nvidia has transitioned from a gaming powerhouse to a central player in military technology, with its market cap reaching $4.5 trillion as its GPUs power the largest defense data centers. The Bureau of Industry and Security (BIS) classifies high-end GPUs like the H100 and Blackwell as dual-use technologies, subjecting them to intense export controls.

In 2025, a new framework for managing global AI diffusion introduced "country tiers" to restrict the export of advanced AI chips and closed-model weights to strategic competitors. Tier 2 countries face absolute caps on H100-equivalent chips, while Tier 3 countries (subject to arms embargos) are largely restricted from importing high-end hardware. Nvidia has responded by introducing "Confidential Computing" features in its Blackwell and Rubin architectures, providing hardware-level protection for sensitive AI models deployed in shared or cloud environments.

Contract/Program | Amount | Leading Recipients | Focus Area |

PROTECTS BPA | $20 Billion | ECS, Valiant, Pueo | AI-enabled cybersecurity |

Army Commercial Software | $10 Billion | Palantir | Data analytics/AI integration |

JWCC | $9 Billion | AWS, Google, Microsoft, Oracle | Hyperscale cloud infrastructure |

WAEDS Task Order | $1.6 Billion | Booz Allen | WMD Intelligence/Data Science |

EMITSA Contract | $1.3 Billion | GDIT | IT Network Modernization |

SCRIPTS BPA | $919 Million | Exiger | Supply chain risk illumination |

Synthetic Environments: Game Engines as Tactical Assets

The "spin-in" of commercial technology is perhaps most visible in the adoption of game engines like Unreal Engine 5 and Unity for military training and digital twins. These tools allow for the creation of photorealistic virtual environments that mirror real-world assets, significantly reducing the cost and risk associated with live training exercises.

Lockheed Martin and the Future Simulation Engine

Lockheed Martin has pioneered the use of Unreal Engine 5 to create a "Future Simulation Engine," which serves as the backbone for its training solutions. This engine creates a digital twin of live exercises, porting physical environments and weapon ballistics into a synthetic world. It has been used for "Flight School Next" to train pilots and has enabled cross-country networked exercises of synthetic UAS, reducing the need for expensive live flight tests.

Digital Twins for Engineering and Logistics

Beyond training, digital twins are used for "design validation" and lifecycle monitoring of complex systems like maritime fleets and aviation assets. Boeing uses Unreal Engine to generate synthetic, annotated data for AI training, which allows engineers to simulate rare "edge cases" that are difficult to capture in the real world. This "shift-left" approach allows software testing to happen concurrently with mechanical design, accelerating product development timelines.

The Human Element: Workforce and Ethical Friction

The mainstreaming of defense tech has created new challenges for the workforce and the ethical governance of innovation. As civilian developers are increasingly tasked with building military systems, the "moral responsibility" of the tech industry has come under intense scrutiny.

Employee Activism and Corporate Backlash

The relationship between Silicon Valley and the Pentagon remains complicated. High-profile protests, such as those at Google regarding "Project Maven," led to the company retreating from initial contracts. However, analysts conclude that such activism is often ineffective at scale because the work typically shifts to other providers like Palantir or Clarifai. Clarifai, in particular, doubled down on defense work, partnering with Crimson Phoenix to enhance AI for the Army despite internal concerns about coding biases and the transition of imagery technology into autonomous weapons systems.

Workforce Transformation and Trusted Identity

The defense sector entering 2026 faces a critical talent shortage, necessitating "workforce transformation" strategies. Upskilling and reskilling programs focus on cyberthreats and the integration of advanced technologies, while "trusted workforce" and identity management systems are essential for operational security. Modern organizations are adopting AI-driven skill assessments and micro-credentialing to identify and fill internal gaps.

Ethics training and "technoethical" education are also becoming standardized. Strategies to prevent the adverse effects of technology in the workplace—such as psychosocial hazards for developers of lethal systems—include ethical technology assessments and foresight analysis. The "decency of work" in the defense sector is now a primary concern for scholars, who emphasize the need for transparency and the ethical treatment of researchers in a VUCA world.

Long-Term Outlook: The 2030 Defense Tech Landscape

As dual-use technology enters a period of higher-risk but higher-reward development, the landscape toward 2030 will be defined by "national security through industrial capacity".

The Shift Toward Mass Production and Resilience

The period after World War II was maintained by technological superiority—a "Pax Americana" that is now being tested by the rapid commercialization of AI. Future force structures will likely be defined by "cheap, highly scalable platforms" rather than the bespoke, multi-decade acquisition cycles of the past. For example, by 2030, the Army aims to have thousands of fieldable AI-enabled autonomous systems as part of its Replicator goals.

Strategic Recommendations for a Mainstream Era

For national security institutions, the focus must shift from merely administering programs to leading them, with an emphasis on three principles: understanding the local innovation context, empowering institutions to take risks with TRL-6 startups, and investing in enduring structures from talent to procurement.

For private industry, the "spin-in" model requires companies to incorporate resilience, durability, and "obsolescence mitigation" into their designs from the outset to remain relevant to both civilian and military buyers. Those that succeed will be "structurally aligned and operationally trusted," moving beyond invention to the harder problem of translating venture capital into large-scale manufacturing capacity.

The mainstreaming of defense tech is no longer just a trend—it is a surge that is fundamentally reshaping the global tech landscape. Powered by record budgets, a new wave of unicorns, and the strategic pivot of Big Tech, the convergence of the commercial and military sectors is creating an era where data-driven superiority is the primary currency of power.

Read More -

1. From Idea to MVP: A Step-by-Step Guide for Solo Founder

🔗 https://findnstart.com/blogs/from-idea-to-mvp-a-step-by-step-guide-for-solo-founder

2. How to Validate Your Startup Idea in 48 Hours for $0

🔗 https://findnstart.com/blogs/how-to-validate-your-startup-idea-in-48-hours-for-0

3. Remote vs. Local: Does Your Co-Founder Need to Live in the Same City?

🔗 https://findnstart.com/blogs/remote-vs-local-does-your-co-founder-need-to-live-in-the-same-city

4. The 2026 Startup Landscape: What Has Fundamentally Changed (and Why Founder Skills Matter More Than Ever)

5. The Most In-Demand Skills for Startup Founders in 2026

🔗 https://findnstart.com/blogs/the-most-in-demand-skills-for-startup-founders-in-2026

6. How to Find a Technical Co-Founder (Without a Six-Figure Salary)

🔗 https://findnstart.com/blogs/how-to-find-a-technical-co-founder-without-a-six-figure-salary

7. 5 Red Flags to Look for When Choosing a Startup Partner

🔗 https://findnstart.com/blogs/5-red-flags-to-look-for-when-choosing-a-startup-partner

8. How to Pitch Your Idea to Potential Co-Founders

🔗 https://findnstart.com/blogs/how-to-pitch-your-idea-to-potential-co-founders

9. How to Build a Portfolio that Attracts High-Growth Startup Founders

🔗 https://findnstart.com/blogs/how-to-build-a-portfolio-that-attracts-high-growth-startup-founders

10. Equity vs. Salary: How to Split Ownership with Your First Teammate

🔗 https://findnstart.com/blogs/equity-vs-salary-how-to-split-ownership-with-your-first-teammate

11. Why Joining an Early-Stage Startup is Better Than a Corporate Job

🔗 https://findnstart.com/blogs/why-joining-an-early-stage-startup-is-better-than-a-corporate-job

12. The Future of EdTech: Why Developers and Educators Need to Team Up Now

🔗 https://findnstart.com/blogs/the-future-of-edtech-why-developers-and-educators-need-to-team-up-now

13. The Architecture of Symbiosis: Analytical Perspectives on the Five Habits of Successful Startup Duos

14. Finding a Co-Founder in the AI Space: What Skills Should You Look For?

🔗 https://findnstart.com/blogs/finding-a-co-founder-in-the-ai-space-what-skills-should-you-look-for

15. Overcoming Analysis Paralysis and the Strategic Path to Execution

🔗 https://findnstart.com/blogs/overcoming-analysis-paralysis-and-the-strategic-path-to-execution

16. From College Project to Company: How to Find Your Student Co-Founder

🔗 https://findnstart.com/blogs/from-college-project-to-company-how-to-find-your-student-co-founder

17. How to Start a Startup While Working a Full-Time Job

🔗 https://findnstart.com/blogs/how-to-start-a-startup-while-working-a-full-time-job

18. How to Build a HealthTech Startup Without a Medical Degree

🔗 https://findnstart.com/blogs/how-to-build-a-healthtech-startup-without-a-medical-degree

19. The Solitary Architect: Executive Isolation in Entrepreneurship

20. The 2026 Guide to Launching a SaaS as a Solo Developer

21. What Sustainable Growth Actually Looks Like

🔗 https://findnstart.com/blogs/what-sustainable-growth-actually-looks-like

22. The Early Warning Signs Your Startup Is in Trouble

🔗 https://findnstart.com/blogs/the-early-warning-signs-your-startup-is-in-trouble

23. How to Grow Without Burning Out

🔗 https://findnstart.com/blogs/how-to-grow-without-burning-out

24. The Truth About “Runway” Most Founders Ignore

🔗 https://findnstart.com/blogs/the-truth-about-runway-most-founders-ignore

25. Revenue Solves More Problems Than Funding

🔗 https://findnstart.com/blogs/revenue-solves-more-problems-than-funding

26. What No One Tells You About Being a Solo Founder

🔗 https://findnstart.com/blogs/what-no-one-tells-you-about-being-a-solo-founder

27. Why Smart People Quit High-Paying Jobs to Build Startups (And Why Most Regret It)

28. Why Most Startup Advice on Twitter Is Dangerous

🔗 https://findnstart.com/blogs/why-most-startup-advice-on-twitter-is-dangerous

29. Decision Fatigue: The Silent Startup Killer

🔗 https://findnstart.com/blogs/decision-fatigue-the-silent-startup-killer

30. Fear vs Logic: How Founders Actually Make Decisions

🔗 https://findnstart.com/blogs/fear-vs-logic-how-founders-actually-make-decisions

31. How Overthinking Destroys Early Momentum

🔗 https://findnstart.com/blogs/how-overthinking-destroys-early-momentum

32. Ideas Don’t Scale. Systems Do.

🔗 https://findnstart.com/blogs/ideas-dont-scale-systems-do

33. The First Hire That Actually Matters

🔗 https://findnstart.com/blogs/the-first-hire-that-actually-matters

34. How the First 100 Users Decide Your Startup’s Fate

🔗 https://findnstart.com/blogs/how-the-first-100-users-decide-your-startups-fate

35. Why Your Startup Doesn’t Need Growth — It Needs Focus

🔗 https://findnstart.com/blogs/why-your-startup-doesnt-need-growthit-needs-focus

36. Why Most Startups Die Quietly

🔗 https://findnstart.com/blogs/why-most-startups-die-quietly

37. Lessons Learned Too Late by First-Time Founders

🔗 https://findnstart.com/blogs/lessons-learned-too-late-by-first-time-founders

38. The Myth of the “Overnight Success” Startup

🔗 https://findnstart.com/blogs/the-myth-of-the-overnight-success-startup