Comparison Culture in India’s Startup Scene

March 9, 2026 by Harshit Gupta

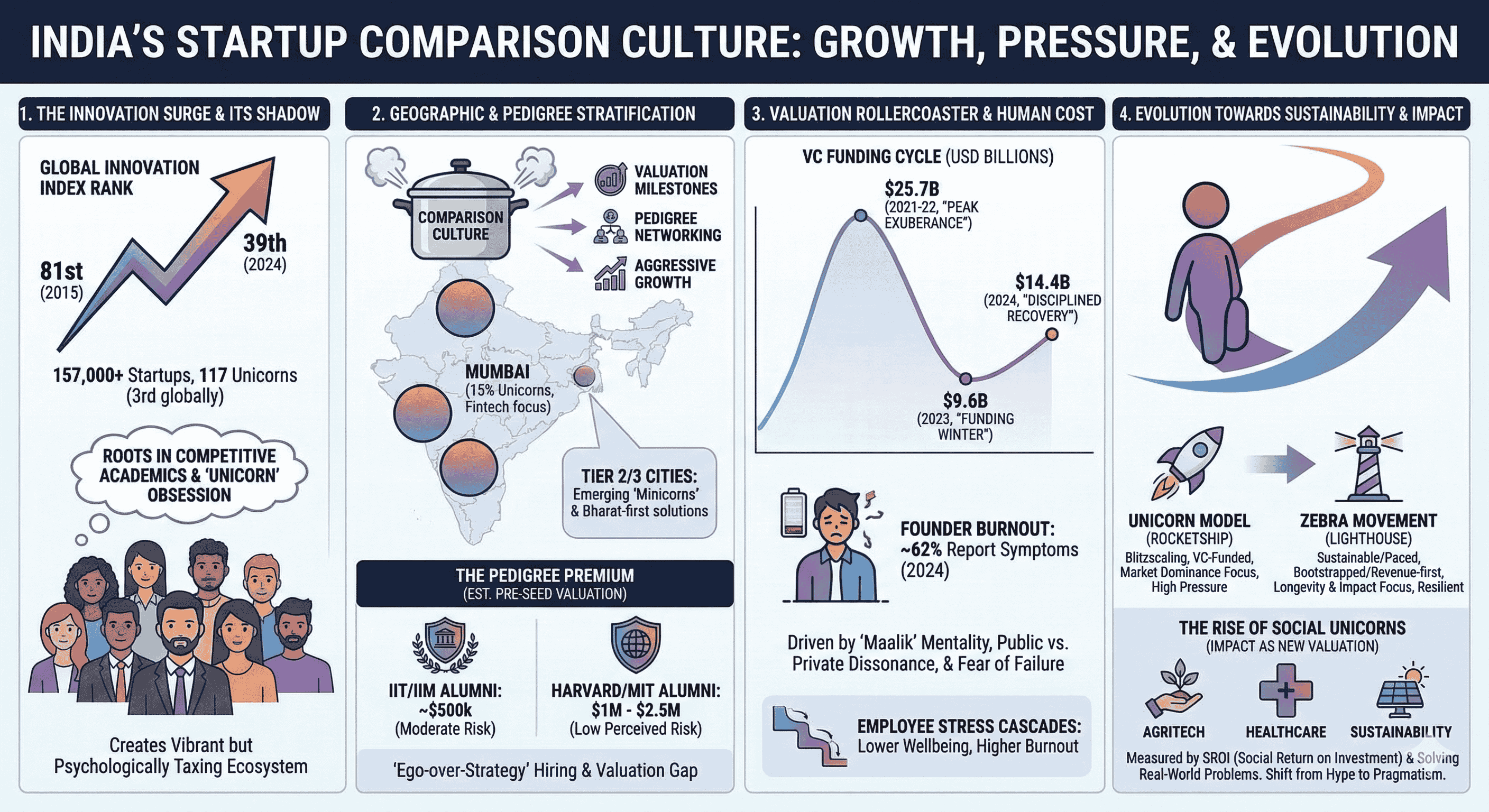

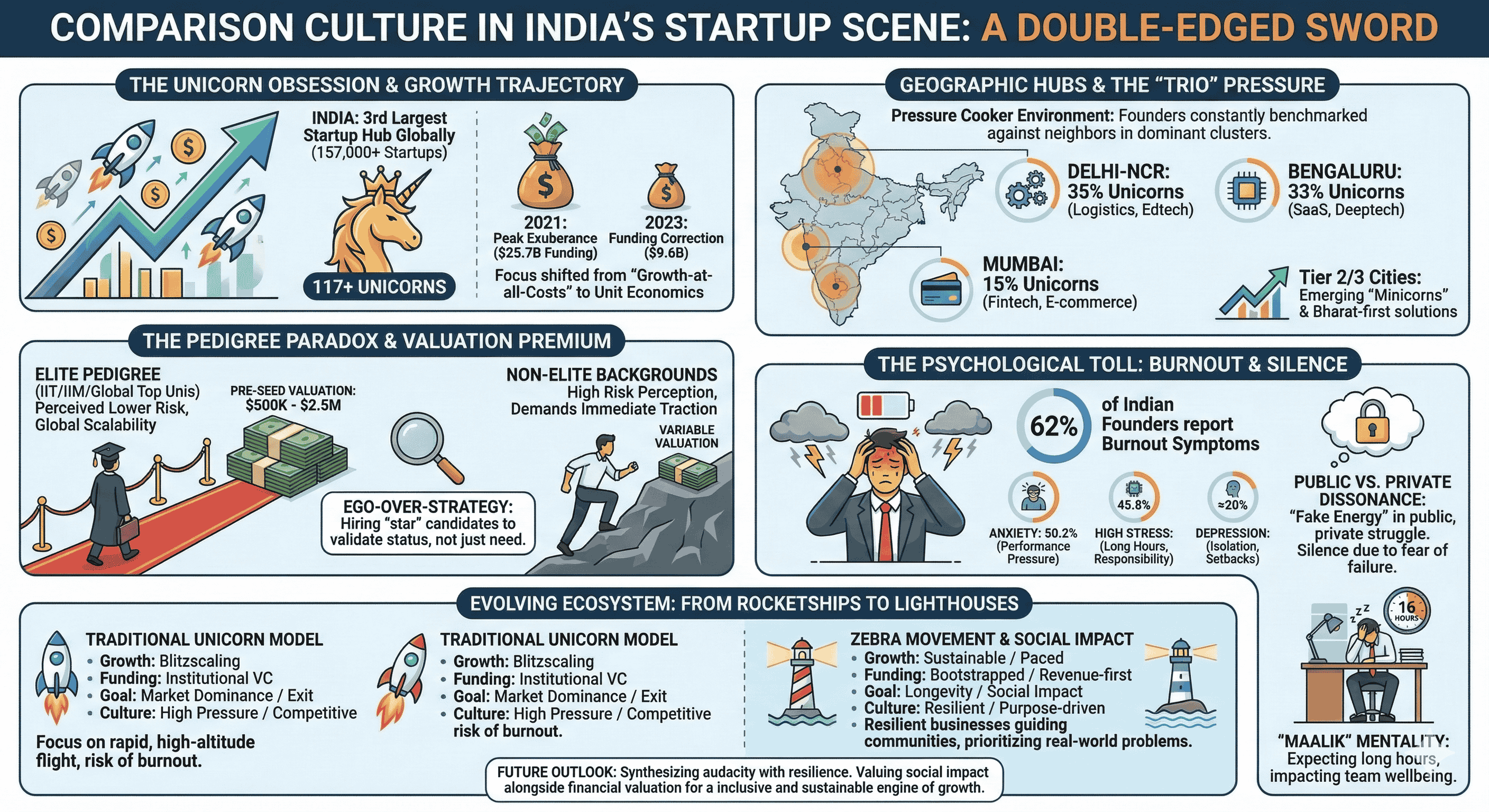

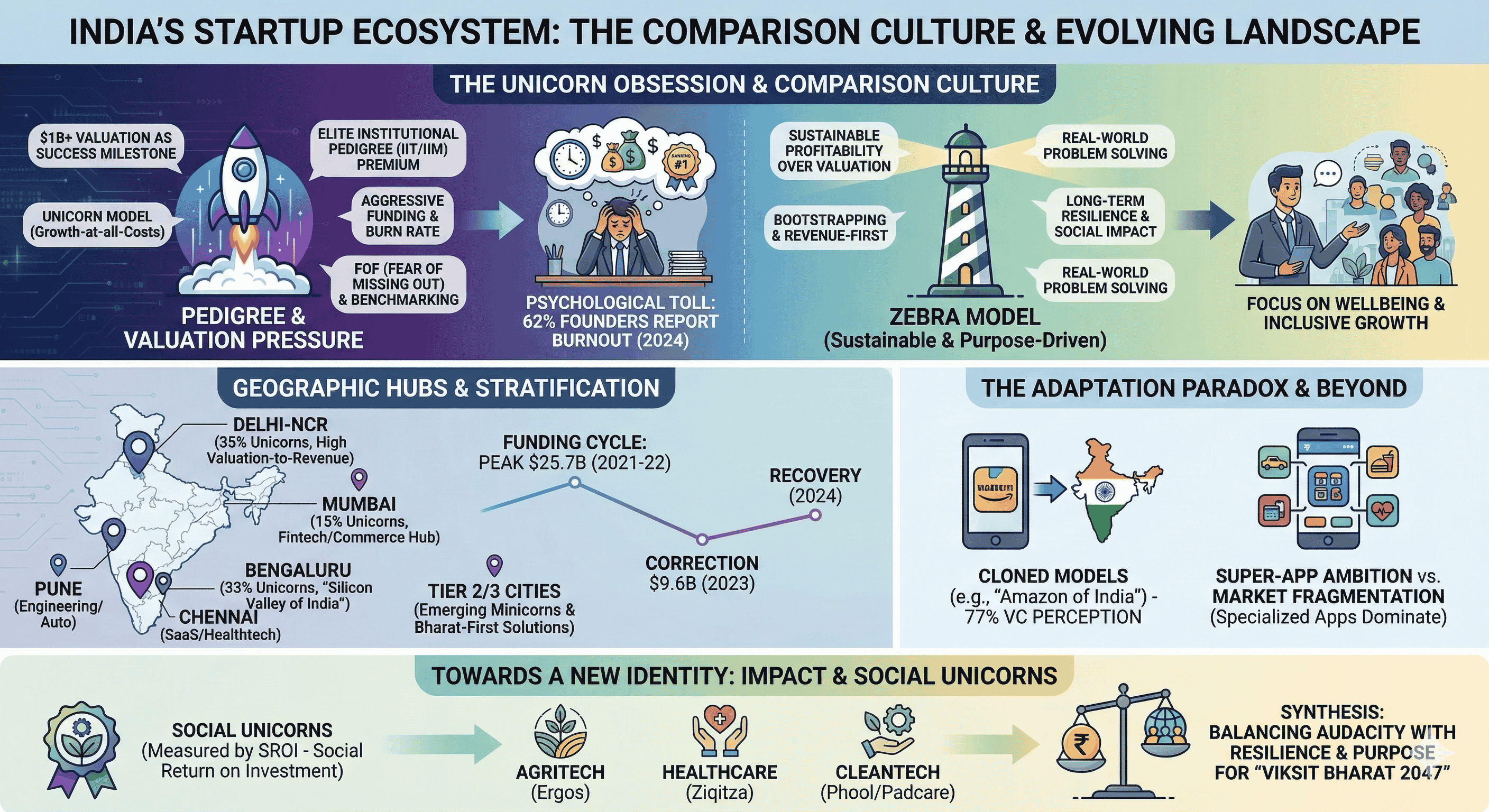

The Indian startup ecosystem has undergone a radical transformation over the past decade, evolving from a nascent collection of ventures into the third-largest startup hub globally. This trajectory is characterized by a dramatic leap in the Global Innovation Index, where India’s ranking moved from 81st in 2015 to 39th in 2024. While the sheer volume of activity—comprising over 157,000 startups and 117 unicorns—is a testament to India's burgeoning digital economy, it has simultaneously fostered a pervasive "comparison culture". This culture, rooted in historical competitive academic structures and fueled by an obsession with "unicorn" status, has become a defining characteristic of how Indian founders, investors, and employees interact with the market. The relentless focus on valuation milestones, pedigree-based networking, and aggressive growth-at-all-costs strategies has created an ecosystem that is as vibrant as it is psychologically taxing.

The Macroeconomic Foundation of the Innovation Surge

The expansion of India's startup scene is deeply linked to structural shifts in the domestic economy and the emergence of a robust middle class. Projections suggest that by 2030, more than 50% of Indian households will earn over INR 500,000 annually, a significant increase from 33% in 2019. This evolution from a purely cost-conscious market to one that seeks innovative, high-quality digital solutions has provided the necessary demand for tech-first sectors like Fintech, SaaS, and E-commerce.

Government initiatives, particularly the Startup India program launched in 2016, have acted as a formalizing force, simplifying regulations and providing tax incentives that have directly contributed to the creation of over 1.55 million jobs. However, this growth has not been uniform across the subcontinent. The geographic concentration of success remains one of the primary drivers of localized comparison culture, as founders in major hubs compete for the same pool of talent, capital, and media attention.

Geographic Stratification and the Hub Mentality

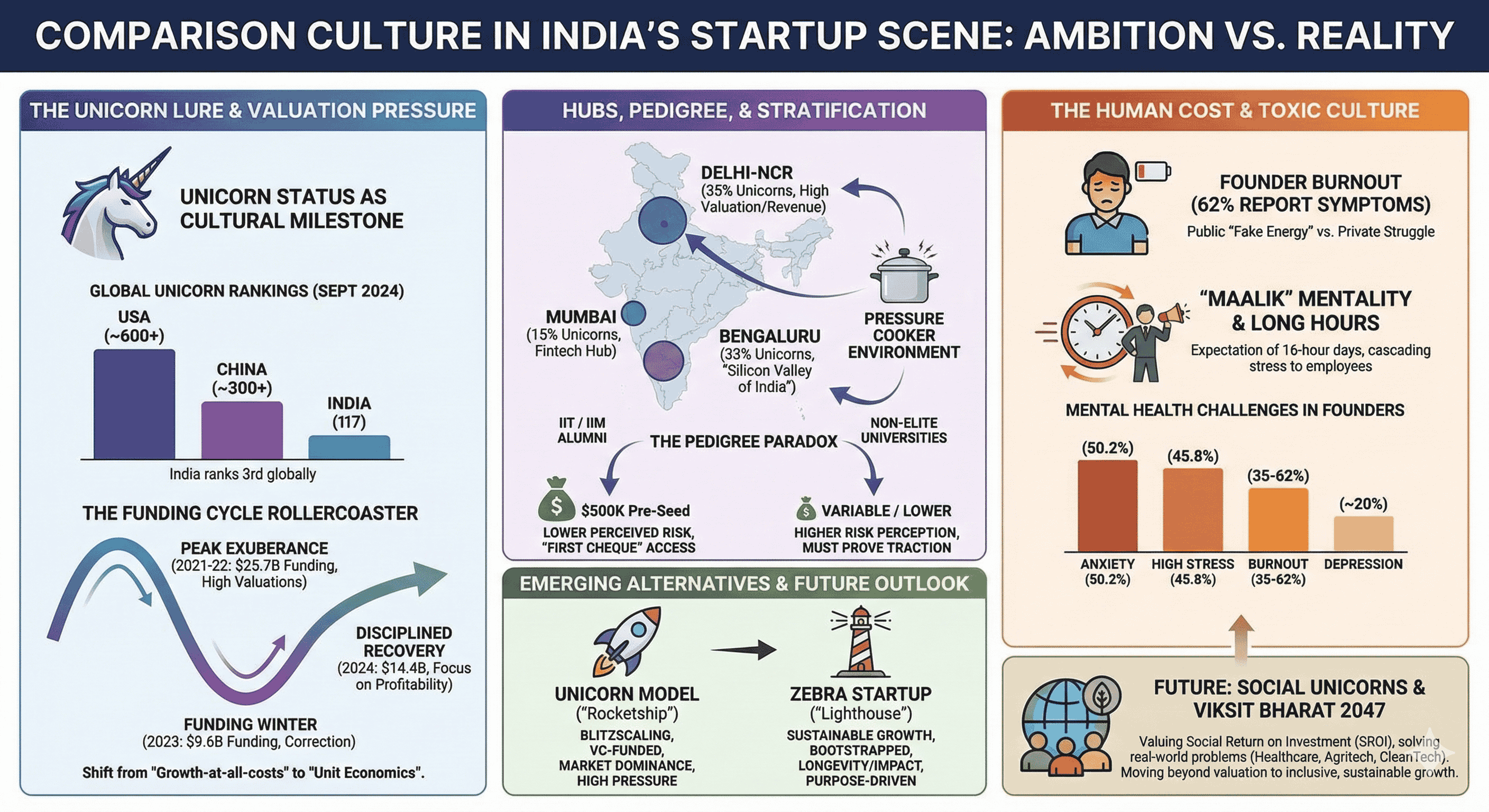

The concentration of startups in Bengaluru, Delhi-NCR, and Mumbai has created a "trio" of dominant clusters that account for the vast majority of unicorn creation and capital inflow. This concentration creates a pressure cooker environment where founders are constantly benchmarked against their neighbors. Bengaluru, often referred to as the "Silicon Valley of India," provides 33% of the nation’s unicorns, while Mumbai contributes 30%. Interestingly, while Bengaluru leads in volume, startups in Delhi-NCR have shown significantly higher valuation-to-revenue ratios, highlighting regional differences in how market potential is perceived and priced.

Hub Location | Share of Unicorns | Share of Minicorns (>$1M) | Dominant Sectors |

Delhi-NCR | 35% | 25% | Logistics, Edtech, Fintech |

Bengaluru | 33% | 29% | SaaS, Consumer Tech, Deeptech |

Mumbai | 15% | 20% | Fintech, E-commerce, D2C |

Chennai | 5% | 5% | Enterprise SaaS, Healthtech |

Pune | 5% | 4% | Engineering, Automotive |

Other Cities | 7% | 17% | Agritech, Manufacturing |

The data indicates that while the top three hubs dominate the valuation narrative, other cities are making significant strides in the "minicorn" category, suggesting a gradual democratization of entrepreneurship. For instance, Tier 2 and Tier 3 cities are now recognized as attractive investment hubs due to lower operational costs and the emergence of "Bharat-first" solutions. As of 2021, the Department for Promotion of Industry and Internal Trade (DPIIT) had recognized startups from 623 of India’s 766 districts, indicating that the spirit of entrepreneurship is penetrating deeper into the rural and semi-urban landscape.

The Pedigree Paradox: Institutional Influence on Founder Behavior

A defining feature of the comparison culture in India is the immense weight placed on institutional pedigree. The competitive mindset instilled by India's academic system, particularly the rigorous selection process for the Indian Institutes of Technology (IITs), translates directly into the entrepreneurial world. Between 2015 and early 2025, close to 6.3% of the 113,360 tech startups founded in India were led by IIT alumni.

The "IIT tag" serves as a powerful signal of quality, often acting as a "first cheque" that unlocks access to elite venture capital firms. This institutional filter identifies individuals with remarkable perseverance and tenacity, but it also creates a hierarchy where founders from less prestigious backgrounds must work significantly harder to prove their viability.

The Valuation Premium of the Elite 0.01%

The founder-investor dynamic in India is heavily influenced by the "elite 0.01%" narrative. Founders from top-tier institutions like the IITs or global elite universities such as Harvard, Stanford, and MIT often command a significant valuation premium during early-stage fundraising. This disparity creates a system where the "gap keeps widening" for those who did not crack the competitive exams earlier in their lives.

Founder Pedigree | Estimated Pre-Seed Valuation | Perception of Risk |

IIT / IIM Alumni | $500,000 | Moderate; proven discipline |

Harvard / MIT Alumni | $1M - $2.5M | Low; perceived global scalability |

Non-Elite Universities | Variable; often lower | High; demands immediate proof of traction |

This reliance on pedigree has led to what some observers call an "ego-over-strategy" hiring pattern. Founders often prioritize recruiting "star" candidates from prestigious institutions or major global companies like Google to validate their own status as a "true founder," even when such hires are not strategically necessary. This behavior reinforces a culture of superficial comparisons where the quality of the team's CV is used as a proxy for the startup's actual health and market potential.

The Unicorn Lure: Valuation as a Cultural Milestone

The term "unicorn," originally intended to highlight the rarity of private startups valued at over $1 billion, has been transformed in India into a standard benchmark of success. In 2013, such valuations were exceptional; however, as of September 2024, there are over 1,467 unicorns worldwide, with India ranking third behind the United States and China.

This obsession with billion-dollar valuations is central to the comparison culture. Achieving unicorn status is seen as definitive proof that a founder has built a powerful team and seized a significant market opportunity. However, this narrative often overshadows the importance of sustainable revenue and profitability. Many Indian unicorns invest heavily in growth at the expense of sustainable operations, frequently operating at significant losses to maximize market share.

The Funding Cycle and the Flight to Quality

The investment landscape has experienced a dramatic cycle over the past four years. The 2021-2022 period represented the "peak of exuberance," with funding reaching $25.7 billion and valuations soaring on expectations of perpetual growth. This era saw the rapid minting of unicorns, primarily in e-commerce and fintech. However, the subsequent "correction" in 2023 saw funding plummet by 65% to $9.6 billion as investors shifted their focus from "growth-at-all-costs" to unit economics and profitability.

Year | Total VC Funding (USD) | Deal Volume | Market Sentiment |

2021 | $25.7B | High | Irrational Exuberance |

2022 | $25.7B | High | Peak Valuations |

2023 | $9.6B | 880 Deals | "Funding Winter" |

2024 | $14.4B | 1,337 Deals | Disciplined Recovery |

This normalization has created a bifurcated market. Companies with strong unit economics and clear paths to profitability continue to attract capital at reasonable valuations, while those dependent on perpetual funding at escalating valuations face the risk of down-rounds or closure. A down-round signals weakness to the market, often denting investor confidence and demotivating employees with "underwater" employee stock ownership plans (ESOPs).

The Psychological Toll: Burnout and the Silence of Struggle

The comparison culture in the Indian startup scene has a profound psychological impact on founders and their teams. In 2024, an estimated 62% of Indian founders reported symptoms of burnout. Unlike traditional corporate roles, founder burnout is compounded by the inability to quit; the founder's name is on the cap table, and they are personally responsible for the team they recruited.

The pressure to maintain a public image of constant growth and unwavering positivity creates a "public vs. private dissonance". Founders often feel forced to "fake energy" and pretend everything is fine during investor calls while privately struggling with exhaustion and anxiety. This silence is reinforced by the belief that admitting to burnout or mental health challenges is an admission of failure that could jeopardize future funding rounds.

The "Maalik" Mentality and Organizational Stress

A significant contributor to this toxic work environment is what some describe as the "Maalik" (owner) mentality among Indian founders. This mindset involves a relentless pursuit of growth at any cost, often dismissing the importance of work-life balance. Founders frequently expect employees to work 16-hour days and weekends, fostering a culture where staying late is seen as a sign of commitment rather than a symptom of poor management.

Research indicates that founder stress is not isolated; it cascades through the entire organization. Employees led by highly stressed founders report 16% lower work wellbeing, 14% higher burnout, and 16% lower psychological safety. The most significant stressor for employees is often not the workload itself, but uncertainty about the startup's future and a lack of transparency from the leadership.

Mental Health Challenge | Percentage of Founders Affected | Contributing Factors |

Anxiety | 50.2% | Performance pressure, fear of failure |

High Stress | 45.8% | Long hours, financial responsibility |

Burnout | 35% - 62% | Constant demands, lack of support |

Depression | ≈20% | Isolation, financial strain, setbacks |

Imposter Syndrome | 25% | Social comparison, status pressure |

The "Global Mind Health in 2025" report suggests that young Indian adults (ages 18-34) rank 60th out of 84 nations in mental well-being, highlighting a serious crisis among the core demographic of the startup workforce. Factors such as intense academic competition, employment uncertainty, and social comparison through digital platforms are cited as primary drivers of this psychological strain.

The Adaptation Paradox: Innovation vs. Cloned Models

A recurring theme in the critique of India’s startup culture is the "adaptation paradox." While India has built world-class companies, approximately 77% of venture capitalists believe Indian startups are largely clones of Western companies. This model—often termed "Amazon of India" or "Uber of India"—focuses on brilliant adaptations of successful Western models for the domestic market.

Indian Startup | Global Adaptation Model | Focus Area |

Flipkart | Amazon | Indian E-commerce |

Ola | Uber | Regional Mobility |

Paytm | PayPal / Alipay | Digital Payments |

Zomato | Grubhub | Food Delivery |

The "Flipkart-Amazon Paradox" highlights that while these companies are massive success stories in terms of market share and valuation, they are often fundamentally derivative. The problem is further compounded by a "Global Ambition Gap," where many Indian adaptations remain focused solely on the domestic market, whereas Chinese tech giants like ByteDance (TikTok) and Alibaba have achieved global dominance.

The Super-App Ambition and Market Fragmentation

In contrast to China (WeChat) and Southeast Asia (Grab, Gojek), India has struggled to produce a dominant "super-app". The Indonesian giant Gojek, for instance, operates the equivalent of three Indian unicorns rolled into one, covering everything from ride-hailing to massage services. In India, specialized apps for food delivery (Swiggy, Zomato), travel (MakeMyTrip), and cab-hailing (Ola, Uber) had already established strong category leadership by the time the super-app trend began to gain traction. This fragmentation implies that Indian users are less likely to remain within a single app ecosystem, preferring specialized services that offer a better value proposition.

The Social and Gendered Dimensions of Comparison

Despite India’s status as a global startup powerhouse, there are significant disparities in gender participation. India has the largest startup ecosystem in South Asia, yet it lags behind smaller neighbors like Sri Lanka, Nepal, and Bhutan in terms of the percentage of women founders. Socio-cultural hurdles, VC bias, and a lack of female-friendly infrastructure are frequently cited as the primary reasons for this gap.

Country | Approximate % of Women Founders | Ecosystem Maturity |

Bhutan | 30%+ | Emergent |

Sri Lanka | 25% - 30% | Mature |

Nepal | 25% - 30% | Emergent |

India | 15% - 18% | Global Powerhouse |

Pakistan | 5% - 7% | Developing |

The comparison between India and its neighbors suggests that market size and capital availability are not the only factors driving entrepreneurial inclusivity. Cultural norms regarding family responsibilities and social safety continue to play a disproportionate role in shaping who gets to participate in the high-stakes world of startups.

The Counter-Movement: Bootstrapping and Zebra Startups

As a response to the "growth-at-all-costs" narrative, a quiet revolution is taking place in India, led by founders who prioritize sustainable profitability over billion-dollar valuations. This "profitability-first" movement is exemplified by companies like Zoho and Zerodha, which have achieved massive scale without relying on external venture capital.

The "Zebra" startup philosophy represents a founder-driven alternative to the unicorn model. Zebra startups are described as being "black and white": they are for-profit and for a cause. Instead of disrupting their way to market dominance, Zebras prioritize sustainable growth, equitable ownership, and real-world problem-solving.

The Philosophical Shift: Lighthouses vs. Rocketships

The distinction between the traditional unicorn model and the emerging zebra movement can be synthesized as a choice between building a "rocketship" or a "lighthouse". Rocketships are designed for rapid, high-altitude flight but risk burning out if they attract too much attention without a solid foundation. Lighthouses are resilient businesses that endure over the long term, guiding their communities through market storms.

Feature | Unicorn Startup | Zebra Startup |

Growth Strategy | Blitzscaling | Sustainable / Paced |

Funding Source | Institutional VC | Bootstrapped / Revenue-first |

Primary Objective | Market Dominance / Exit | Longevity / Social Impact |

Cultural Tone | High Pressure / Competitive | Resilient / Purpose-driven |

This movement is gaining traction in hubs like Chennai, where a "bootstrapping-first" approach is encouraged through programs that focus on customer validation and revenue generation before even considering external funding. For many "Bharat" innovators, this approach is more practical than the high-burn models of Silicon Valley-style ventures.

Impact as the New Valuation: The Rise of Social Unicorns

The next chapter of India’s startup story is increasingly being defined not by financial unicorns, but by "social unicorns". A social unicorn is an enterprise that may achieve a billion-dollar valuation but is measured primarily by its social return on investment (SROI)—lives touched, problems solved, and wealth shared inclusively.

As India looks toward "Viksit Bharat 2047," there is a growing consensus that the unicorn race should not be the defining narrative of its success. Instead, the ecosystem should broaden its lens to celebrate startups addressing challenges in healthcare, rural livelihoods, and climate resilience. Global capital is already shifting in this direction, with ESG-aligned assets projected to cross $40 trillion by 2030, representing over 25% of global assets under management.

Pioneers of the Impact Narrative

Several Indian startups have already begun to demonstrate the viability of the social unicorn model. These companies leverage deep-science and technology to create non-linear impact while maintaining sustainable business models.

Impact Startup | Mission Area | Key Outcome |

Ergos | Agritech | Agri-storage and finance for small farmers |

Ziqitza | Healthcare | Affordable ambulance services in underserved areas |

Barefoot College | Rural Development | Training rural women as solar engineers |

Phool | Sustainability | Circular economy via floral waste recycling |

Padcare | Health/Environment | Sustainable menstrual waste management |

By aligning profit with purpose, these ventures show that sustainability can go hand-in-hand with commercial opportunity. The rise of "green zebras" in the CleanTech sector further illustrates how Indian innovators are addressing global challenges like carbon emissions and waste-to-value while building scalable enterprises.

Organizational Maturity and the Future of the Ecosystem

The Indian startup ecosystem is entering its "adulthood," trading the hype of its teenage years for grown-up pragmatism. This maturity is reflected in a shift toward leaner organizational structures and a tighter scrutiny of operating costs. The widespread adoption of AI is further influencing this shift, as founders build "AI-first" startups that are designed to achieve significant milestones with optimized headcounts.

However, the transition to a professionalized workforce remains a challenge. Many Indian startups still operate with a "Founder's Mentality," which can be a source of strength in the early stages but a liability as the company scales. Professional managers often struggle to maintain the "sense of insurgency" and clear mission that defines the founding team, sometimes drowning the company in functional excellence programs that lack a coherent strategic focus.

The Evolution of Venture Capital

Venture capital in India has matured from a mere source of funding into a driving force of the economic narrative. VCs today provide strategic guidance, hiring support, and market access, helping startups navigate the complexities of a fragmented market. However, the "milestone pressure" exerted by VCs remains a double-edged sword, driving rapid scaling while often necessitating high-burn strategies that can lead to layoffs if market conditions shift.

VC Contribution | Positive Impact | Potential Risk |

Capital Infusion | Enables rapid global scaling | Pressure for unsustainable burn |

Strategic Mentorship | Navigates regulatory barriers | Potential for board-founder conflict |

Network Access | Opens doors to global partners | Over-reliance on "warm introductions" |

Brand Credibility | Attracts top-tier talent | Inflated valuations / Bubble risk |

As global funds pull back, domestic Indian capital is stepping up to ensure that the ecosystem does not face a terminal funding gap. This shift toward domestic resilience is a positive indicator for the long-term stability of the Indian innovation economy.

Conclusion: Synthesizing a New Indian Startup Identity

The "comparison culture" in India’s startup scene is a complex phenomenon that is simultaneously a driver of intense growth and a source of significant systemic stress. The obsession with unicorn status and institutional pedigree has created a high-performance environment that has put India on the global map. However, the human cost of this competition—manifested in record levels of burnout and mental health struggles—cannot be ignored.

The future of the Indian ecosystem likely lies in a synthesis of these competing forces. The audacity and global vision of the unicorn model must be tempered with the resilience, frugality, and purpose-driven focus of the zebra movement. As founders move beyond the "rankings" of their academic years and begin to value social impact alongside financial valuation, the Indian startup scene will evolve into a more inclusive and sustainable engine of national growth. Whether India builds "rocketships" or "lighthouses," its ability to innovate for the "next billion" while caring for its own people will be the ultimate measure of its entrepreneurial success.

Read More -

1. From Idea to MVP: A Step-by-Step Guide for Solo Founder

🔗 https://findnstart.com/blogs/from-idea-to-mvp-a-step-by-step-guide-for-solo-founder

2. How to Validate Your Startup Idea in 48 Hours for $0

🔗 https://findnstart.com/blogs/how-to-validate-your-startup-idea-in-48-hours-for-0

3. Remote vs. Local: Does Your Co-Founder Need to Live in the Same City?

🔗 https://findnstart.com/blogs/remote-vs-local-does-your-co-founder-need-to-live-in-the-same-city

4. The 2026 Startup Landscape: What Has Fundamentally Changed (and Why Founder Skills Matter More Than Ever)

5. The Most In-Demand Skills for Startup Founders in 2026

🔗 https://findnstart.com/blogs/the-most-in-demand-skills-for-startup-founders-in-2026

6. How to Find a Technical Co-Founder (Without a Six-Figure Salary)

🔗 https://findnstart.com/blogs/how-to-find-a-technical-co-founder-without-a-six-figure-salary

7. 5 Red Flags to Look for When Choosing a Startup Partner

🔗 https://findnstart.com/blogs/5-red-flags-to-look-for-when-choosing-a-startup-partner

8. How to Pitch Your Idea to Potential Co-Founders

🔗 https://findnstart.com/blogs/how-to-pitch-your-idea-to-potential-co-founders

9. How to Build a Portfolio that Attracts High-Growth Startup Founders

🔗 https://findnstart.com/blogs/how-to-build-a-portfolio-that-attracts-high-growth-startup-founders

10. Equity vs. Salary: How to Split Ownership with Your First Teammate

🔗 https://findnstart.com/blogs/equity-vs-salary-how-to-split-ownership-with-your-first-teammate

11. Why Joining an Early-Stage Startup is Better Than a Corporate Job

🔗 https://findnstart.com/blogs/why-joining-an-early-stage-startup-is-better-than-a-corporate-job

12. The Future of EdTech: Why Developers and Educators Need to Team Up Now

🔗 https://findnstart.com/blogs/the-future-of-edtech-why-developers-and-educators-need-to-team-up-now

13. The Architecture of Symbiosis: Analytical Perspectives on the Five Habits of Successful Startup Duos

14. Finding a Co-Founder in the AI Space: What Skills Should You Look For?

🔗 https://findnstart.com/blogs/finding-a-co-founder-in-the-ai-space-what-skills-should-you-look-for

15. Overcoming Analysis Paralysis and the Strategic Path to Execution

🔗 https://findnstart.com/blogs/overcoming-analysis-paralysis-and-the-strategic-path-to-execution

16. From College Project to Company: How to Find Your Student Co-Founder

🔗 https://findnstart.com/blogs/from-college-project-to-company-how-to-find-your-student-co-founder

17. How to Start a Startup While Working a Full-Time Job

🔗 https://findnstart.com/blogs/how-to-start-a-startup-while-working-a-full-time-job

18. How to Build a HealthTech Startup Without a Medical Degree

🔗 https://findnstart.com/blogs/how-to-build-a-healthtech-startup-without-a-medical-degree

19. The Solitary Architect: Executive Isolation in Entrepreneurship

20. The 2026 Guide to Launching a SaaS as a Solo Developer

21. What Sustainable Growth Actually Looks Like

🔗 https://findnstart.com/blogs/what-sustainable-growth-actually-looks-like

22. The Early Warning Signs Your Startup Is in Trouble

🔗 https://findnstart.com/blogs/the-early-warning-signs-your-startup-is-in-trouble

23. How to Grow Without Burning Out

🔗 https://findnstart.com/blogs/how-to-grow-without-burning-out

24. The Truth About “Runway” Most Founders Ignore

🔗 https://findnstart.com/blogs/the-truth-about-runway-most-founders-ignore

25. Revenue Solves More Problems Than Funding

🔗 https://findnstart.com/blogs/revenue-solves-more-problems-than-funding

26. What No One Tells You About Being a Solo Founder

🔗 https://findnstart.com/blogs/what-no-one-tells-you-about-being-a-solo-founder

27. Why Smart People Quit High-Paying Jobs to Build Startups (And Why Most Regret It)

28. Why Most Startup Advice on Twitter Is Dangerous

🔗 https://findnstart.com/blogs/why-most-startup-advice-on-twitter-is-dangerous

29. Decision Fatigue: The Silent Startup Killer

🔗 https://findnstart.com/blogs/decision-fatigue-the-silent-startup-killer

30. Fear vs Logic: How Founders Actually Make Decisions

🔗 https://findnstart.com/blogs/fear-vs-logic-how-founders-actually-make-decisions

31. How Overthinking Destroys Early Momentum

🔗 https://findnstart.com/blogs/how-overthinking-destroys-early-momentum

32. Ideas Don’t Scale. Systems Do.

🔗 https://findnstart.com/blogs/ideas-dont-scale-systems-do

33. The First Hire That Actually Matters

🔗 https://findnstart.com/blogs/the-first-hire-that-actually-matters

34. How the First 100 Users Decide Your Startup’s Fate

🔗 https://findnstart.com/blogs/how-the-first-100-users-decide-your-startups-fate

35. Why Your Startup Doesn’t Need Growth — It Needs Focus

🔗 https://findnstart.com/blogs/why-your-startup-doesnt-need-growthit-needs-focus

36. Why Most Startups Die Quietly

🔗 https://findnstart.com/blogs/why-most-startups-die-quietly

37. Lessons Learned Too Late by First-Time Founders

🔗 https://findnstart.com/blogs/lessons-learned-too-late-by-first-time-founders

38. The Myth of the “Overnight Success” Startup

🔗 https://findnstart.com/blogs/the-myth-of-the-overnight-success-startup