Angel Networks vs Micro-VCs in Bangalore

March 10, 2026 by Harshit Gupta

The venture capital ecosystem in Bangalore, traditionally the primary engine of India's technological advancement, has undergone a fundamental structural transformation between 2024 and 2026. This evolution is characterized by a distinct bifurcation of the early-stage funding landscape into two sophisticated institutional archetypes: the Angel Network and the Micro-Venture Capital (Micro-VC) firm. While both archetypes target the pre-seed and seed stages of the startup lifecycle, their operational mandates, fiduciary obligations, and risk-underwriting methodologies have diverged to create a more resilient, albeit complex, capital stack. Bangalore, often referred to as the Silicon Valley of India, now hosts a unique density of tech talent and "experiential capital," where repeat founders and senior corporate executives have professionalized the act of early-stage risk-taking. This report examines the mechanics of these two capital providers, their sectoral rotations—particularly toward deep-tech and artificial intelligence—and the macroeconomic and regulatory catalysts that have defined this period of institutionalization.

The Structural Evolution of Early-Stage Risk

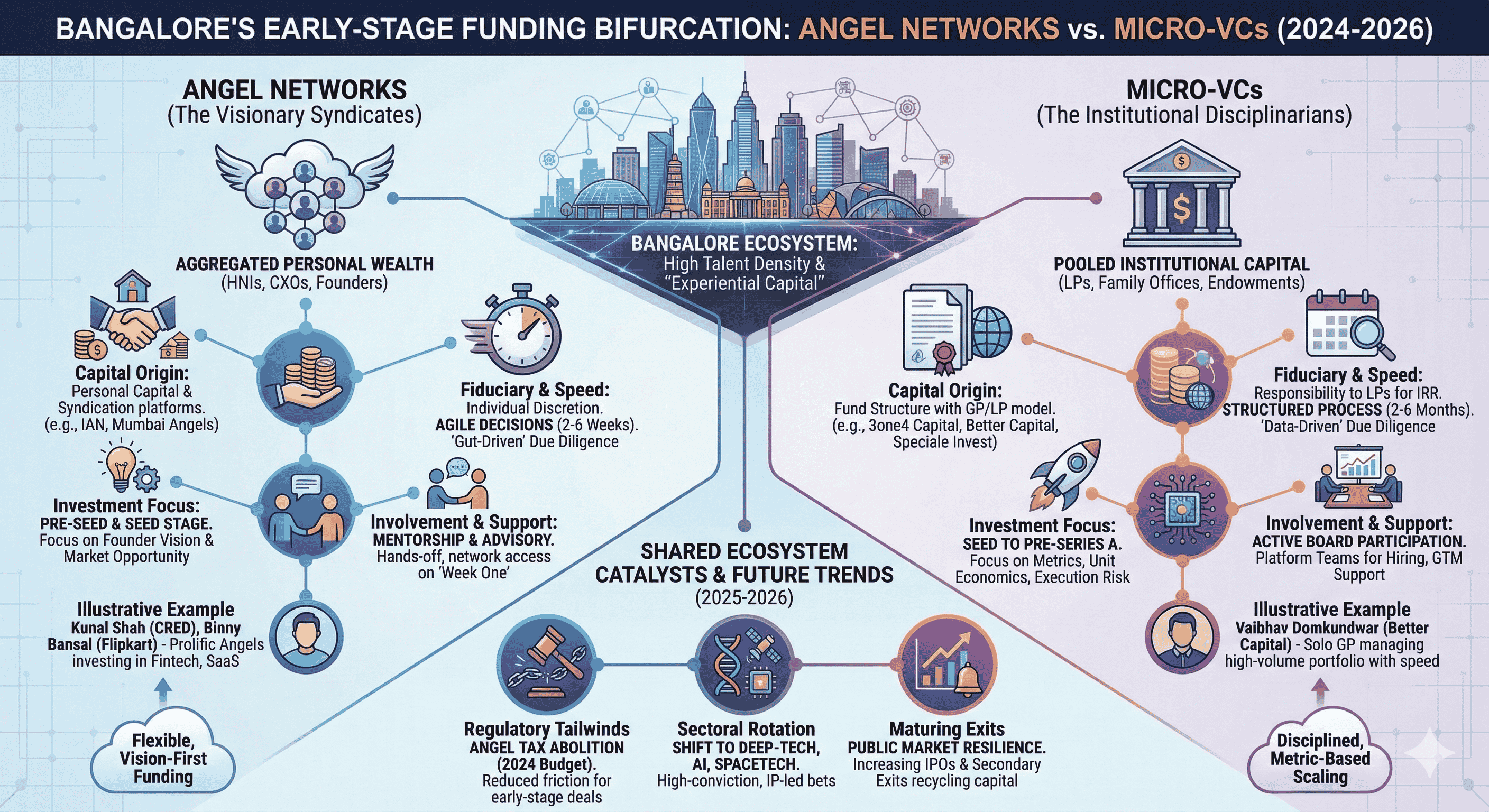

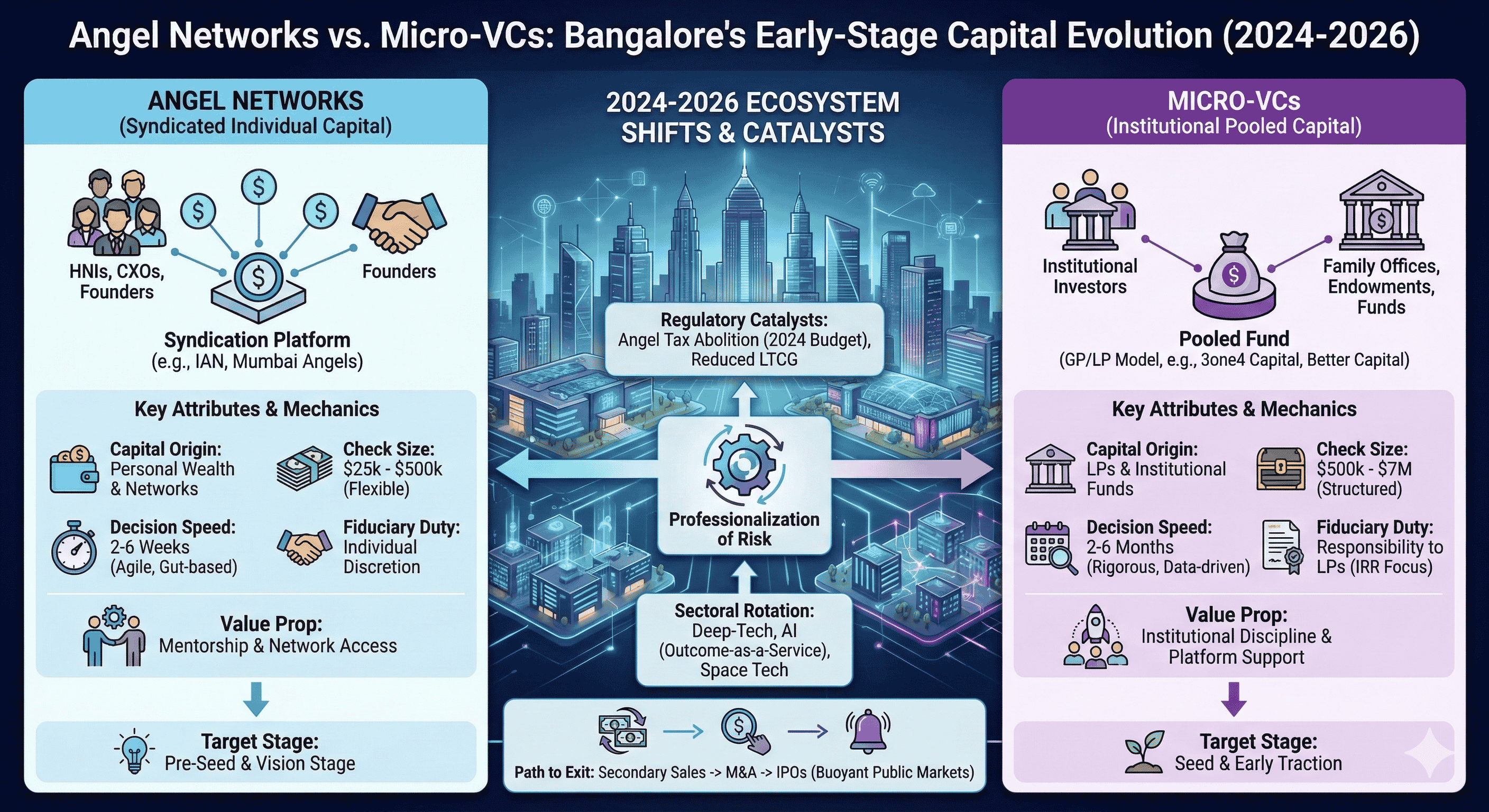

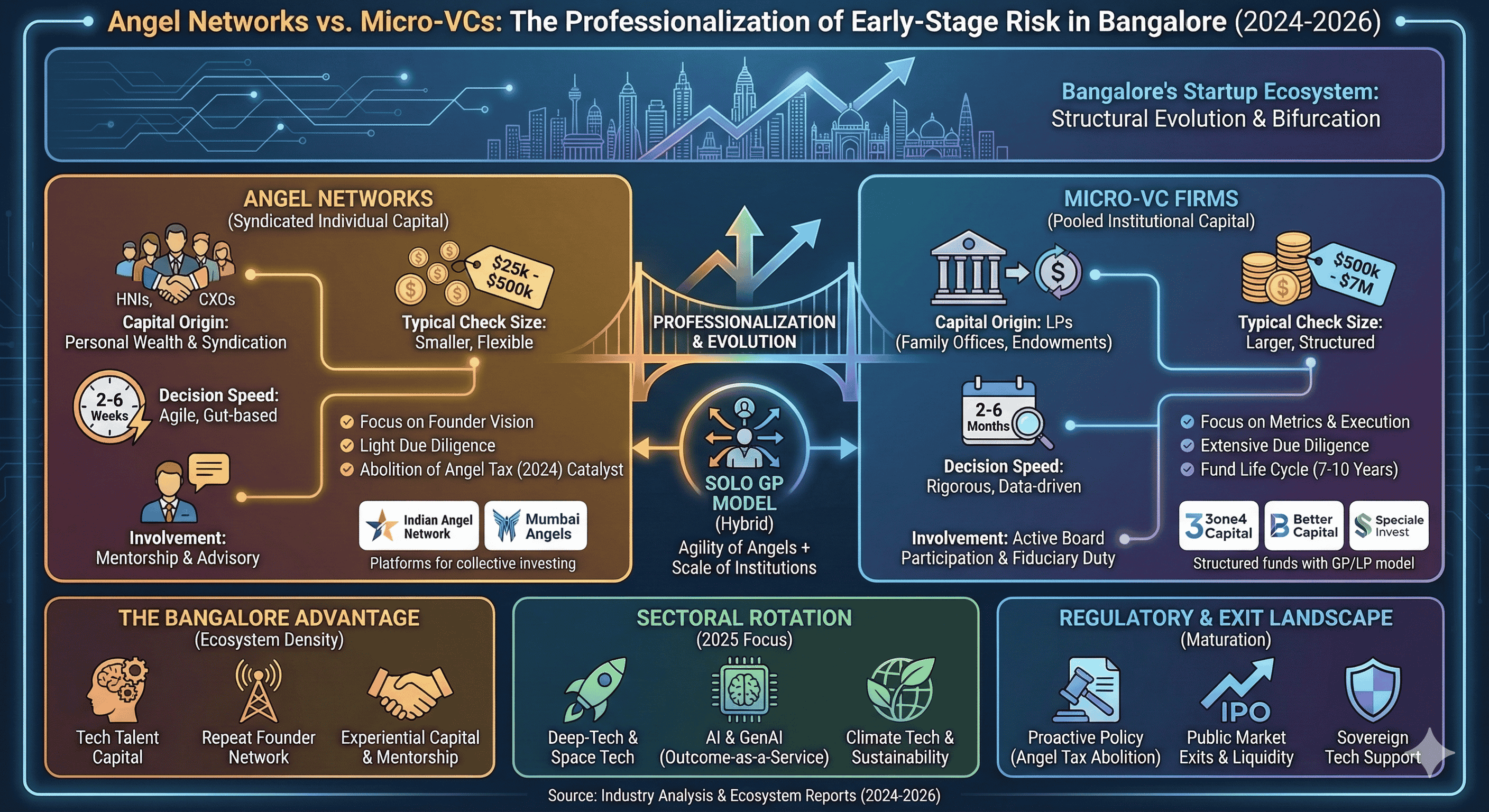

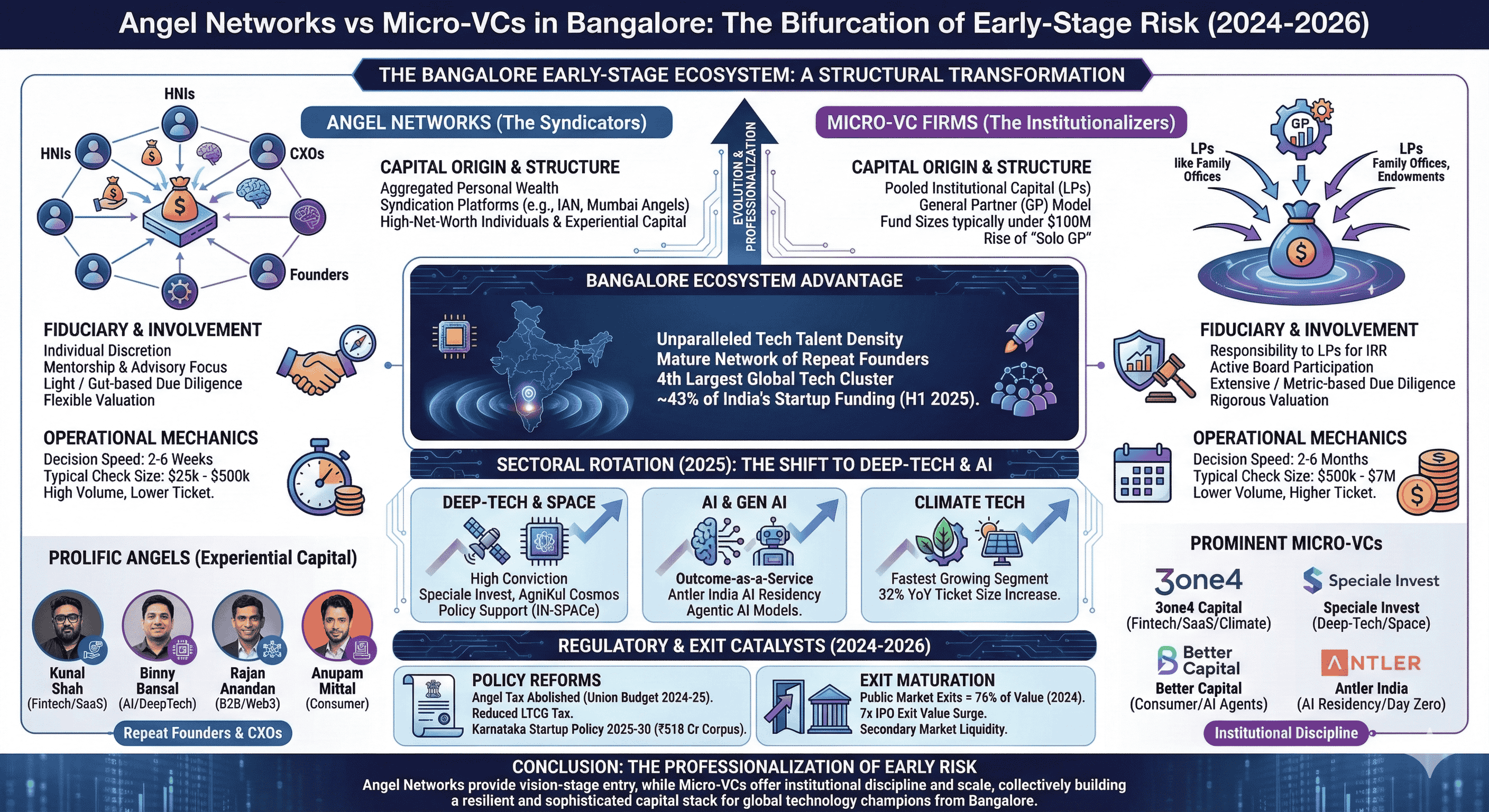

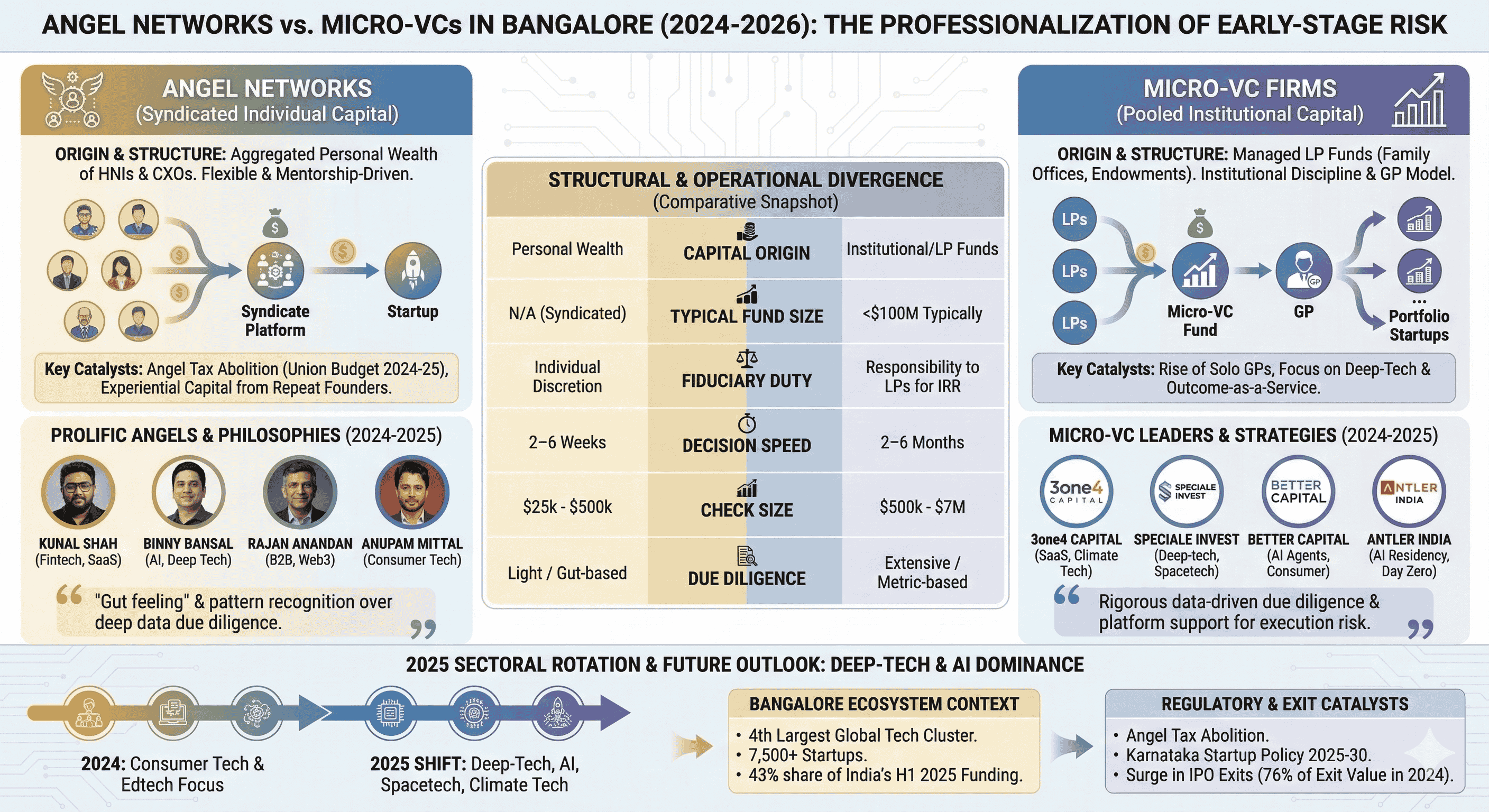

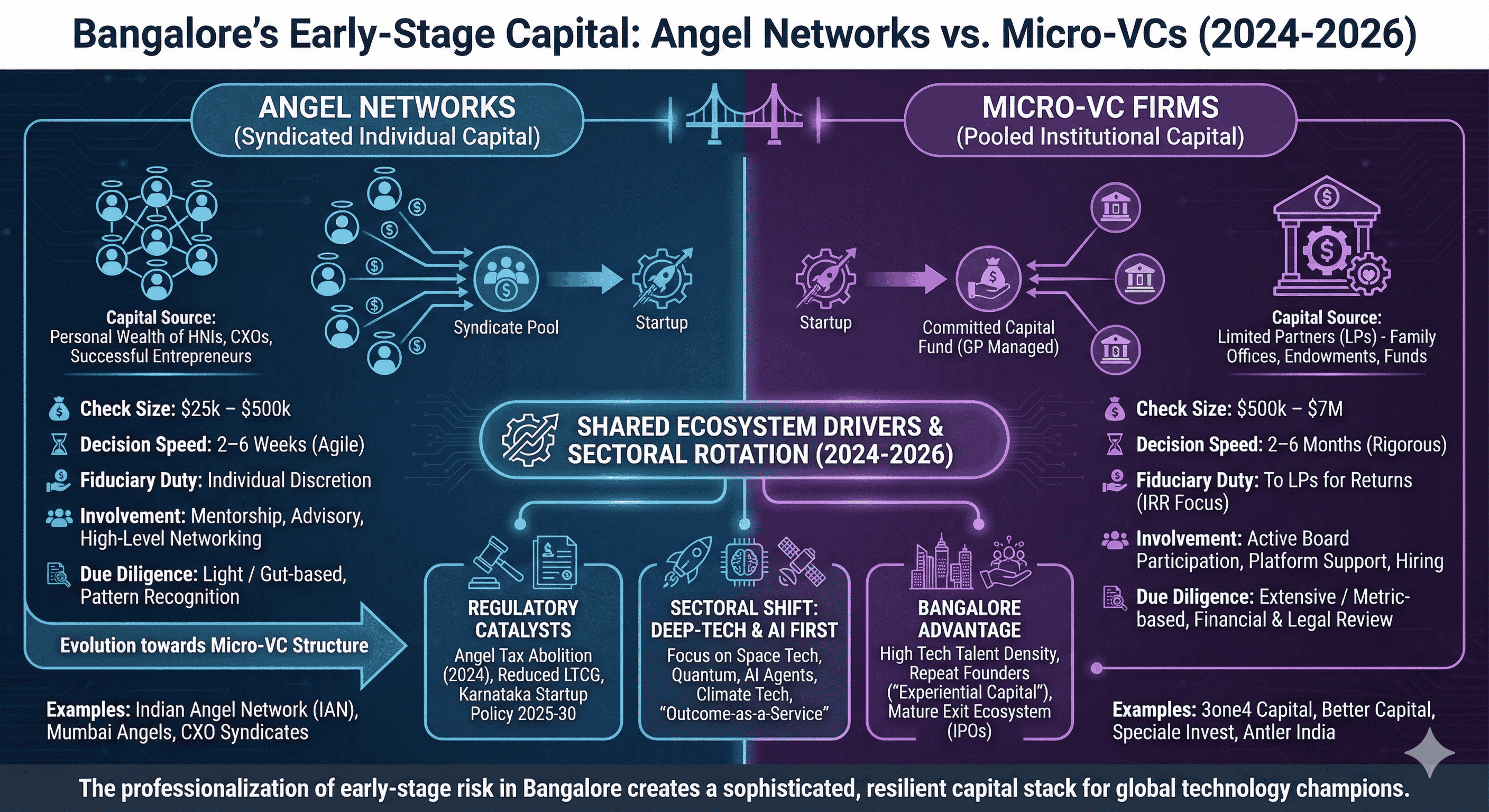

The fundamental distinction between an angel network and a micro-VC lies in the origin of capital and the associated fiduciary architecture. Angel networks in Bangalore, such as the Indian Angel Network (IAN) and Mumbai Angels, operate as syndication platforms that aggregate the personal wealth of high-net-worth individuals (HNIs), senior corporate executives (CXOs), and successful entrepreneurs. These networks serve as discovery and evaluation engines, allowing individual investors to participate in deals with relatively smaller ticket sizes while benefiting from the collective due diligence of the group. The abolition of the angel tax in the Union Budget 2024–25 has served as a primary catalyst for this segment, removing the litigation risk that previously dampened high-valuation pre-seed rounds.

Conversely, micro-VCs like 3one4 Capital, Better Capital, and Speciale Invest manage pooled institutional capital from Limited Partners (LPs), including family offices, university endowments, and sovereign wealth funds. This structural difference introduces a layer of institutional discipline; micro-VCs operate under a General Partner (GP) model where the fund manager is tasked with generating outsized returns within a specific fund life, typically 7–10 years. The rise of the "Solo GP" in Bangalore, exemplified by Vaibhav Domkundwar of Better Capital, represents a hybrid approach where a single individual manages a high-volume portfolio with the speed of an angel but the capital scale of an institutional fund. The impact of this shift is visible on the ground, where micro-VCs have stepped in as the market's default early-stage providers, filling a structural vacuum created when larger venture funds slowed first-cheque deployment to prioritize portfolio defense.

Comparative Table of Institutional Attributes

Attribute | Angel Networks | Micro-VC Firms |

Capital Origin | Personal wealth of HNIs/CXOs | Pooled institutional/LP funds |

Typical Fund Size | Not applicable (syndicated) | Under $100 million typically |

Fiduciary Duty | Individual investor discretion | Responsibility to LPs for IRR |

Involvement Level | Mentorship and advisory | Active board participation |

Decision Speed | 2–6 weeks | 2–6 months |

Typical Check Size | $25k to $500k | $500k to $7M |

Due Diligence | Light / Gut-based | Extensive / Metric-based |

The structural shift observed in 2025 indicates that "super angels" are increasingly transitioning into structured micro-VC roles. This evolution allows them to pool resources, diversify their portfolios, and formalize their investment strategies while maintaining the agility that defined their earlier roles. Micro-VCs focus on early-stage investments, targeting startups with high growth potential, often engaging with non-consensus ideas before narratives harden and markets become crowded. Research underscores the competitive edge of micro-VC firms, revealing that they achieve 7.5% higher returns compared to the top quartile of traditional venture capital funds.

The Bangalore Geographic and Talent Density Advantage

Bangalore’s dominance in the Indian startup ecosystem is a function of its unparalleled density of tech talent and a mature network of repeat founders. As of 2023, approximately 25–30% of all angel funding in India flowed through Bangalore-based entities. The city is home to over 7,500 startups and holds the fourth largest technology cluster globally, trailing only Silicon Valley, Boston, and London. This megacity has a diverse population of over 10 million and is the third wealthiest Indian city with a total wealth of $320 billion.

The availability of "experiential capital" is a hallmark of the Bangalore ecosystem. Successful entrepreneurs such as Kunal Shah (CRED), Binny Bansal (Flipkart), and Sujeet Kumar (Udaan) have become prolific investors, providing not just capital but also critical guidance on product-market fit (PMF) and access to elite engineering talent. This creates a virtuous cycle where secondary exits and IPOs redistribute wealth and expertise back into the pre-seed layer. Eighty percent of global IT companies have based their India operations and R&D centers in Bangalore, which has also attracted about $40-45 billion in venture capital over the last decade.

Prolific Angel Investors and Their Philosophies (2024-2025)

Investor | Background / Platform | Core Investment Focus | Notable Portfolio |

Kunal Shah | Founder, CRED | Fintech, SaaS, Consumer Tech | Unacademy, RazorPay, Slice |

Binny Bansal | Co-founder, Flipkart | AI, Logistics, Deep Tech | Inshorts, Hike, Flash |

Rajan Anandan | Peak XV Partners | B2B, SaaS, AI, Web3 | Rapido, InstaMojo, Omnify |

Anupam Mittal | Founder, Shaadi.com | Consumer Tech, Fintech | Ola Cab, Big Basket, Druva |

Sanjay Swamy | Prime Venture Partners | Fintech, Digital Identity | Early bets on India Stack |

Kris Gopalakrishnan | Co-founder, Infosys | Deep Tech, AI, Biotech | Research-driven innovation |

TV Mohandas Pai | ex-Infosys / Aarin | Edtech, Healthtech, SaaS | 3one4 Capital, Aarin Capital |

The density of the ecosystem allows for a unique due diligence process. Because these individuals have built and scaled companies within the same regulatory and logistical framework as the founders they back, their evaluation is often faster and more qualitative. They rely on a "gut feeling" informed by patterns of success and failure observed over decades. This is particularly important for the pre-seed stage where data is sparse and the primary risk is execution rather than market validation.

Decision Engines and Underwriting Methodologies

The methodologies for evaluating risk differ significantly between angel networks and micro-VCs. Angel investors and networks prioritize founder vision and market opportunity, often accepting more flexible valuation methodologies. In contrast, micro-VCs employ more rigorous market-based valuations and comprehensive financial assessments. For micro-VCs, people risk is essentially execution risk, leading to thorough evaluations of team structure, key hires, and organizational gaps.

In a venture capital round, data, revenue, and performance are analyzed to determine if there is sustainable growth. The process is usually carried out by legal or financial firms, making it more costly, often exceeding €10,000. This significant time investment reflects the complexity of evaluating startups, where factors like scalability, market fit, and team resilience are crucial. There is a proven return on investment for deeper diligence; angel investors dedicating over 40 hours to due diligence achieve 7.1x returns versus 1.1x for those spending less than 20 hours.

Due Diligence Framework: Gut vs. Data

Component | Angel Network Approach | Micro-VC Institutional Approach |

Team Assessment | Focus on founder background and vision | Evaluation of role clarity and retention risks |

Market Validation | Qualitative assessment of trends and size | Analysis of CAC, LTV, and PMF metrics |

Financial Review | Light review of burn and runway | Verification of P&L and bookkeeping |

Legal/Compliance | Standard SAFEs or iSAFE notes | Review of IP, contracts, and cap tables |

Timeline | Weeks (streamlined) | Months (rigorous) |

The evolution from super angel to micro-VC reflects a balance between flexibility and structure. While micro-VCs operate with a more formalized framework, they retain the ability to act swiftly, which is an essential trait for early-stage funding. Angel investors, on the other hand, are defined by their willingness to take calculated risks on unproven ventures using personal capital, allowing for greater flexibility but demanding rigorous verification processes from the founder.

The 2025 Sectoral Rotation: Deep-Tech, AI, and Space Tech

The funding landscape in Bangalore during 2024 and 2025 has seen a pronounced shift away from traditional consumer internet and edtech toward high-conviction, tech-first sectors. Consumer tech remains the largest sector by funding volume—driven by the breakout theme of quick commerce—but deep-tech and climate tech are the fastest-growing segments. Tech-first sectors (consumer tech, SaaS, and fintech) captured over 60% of total funding in 2024, with climate tech emerging with a 32% year-over-year ticket size increase.

Speciale Invest, a prominent deep-tech focused micro-VC based in Bangalore and Chennai, exemplifies this trend. The firm closed its third fund at ₹600 crore in August 2025 and launched Growth Fund II with a ₹1,400 crore corpus in December 2025. Their portfolio includes several well-known companies in deep-tech such as AgniKul Cosmos, GalaxEye, and QNu Labs. The firm is a pioneer in backing technical founders and AI-driven startups, focusing on sectors such as spacetech, advanced manufacturing, and quantum computing.

Bangalore Startup Funding and Sectoral Trends (H1 2025)

Sector / Indicator | H1 2025 Performance / Status | Key Drivers and Implications |

Fintech & E-commerce | Dominant in total capital | Bangalore remains the global nerve center |

Consumer Tech | $5.4 Billion (2.3x rise) | Quick commerce (Zepto, Meesho) |

Deep-Tech / Space | 200+ emerging startups | Policy support and sovereign tech |

AI & Generative AI | ~1.5x Growth in funding | Applications and outcome-based models |

Bangalore Funding Share | 26% to 43% of India's total | Ecosystem maturity and talent density |

Another innovative model is Antler India’s AI Residency, which provides a high-intensity program designed to back ambitious AI founders from day zero. The program offers ₹4 crore in potential investment for 11% equity, with a decision made in just three weeks. This model highlights the acceleration of the pre-seed cycle, providing substantial perks like $1 million in AI-relevant credits to turbocharge growth even before an investment decision is finalized. Antler India plans to invest $25 million in 50 startups in 2025, continuing its push in AI, deep-tech, fintech, and climate.

The Rise of Outcome-as-a-Service and Agentic AI

A significant insight emerging from the Bangalore micro-VC ecosystem is the transition from traditional SaaS to "Outcome-as-a-Service." As observed by Better Capital, enterprises are moving away from buying software and instead purchasing outcomes powered by AI. This shift became more legible in 2025, with portfolio companies like DPDZero delivering AI-led collections as outcomes and Zoca delivering growth outcomes to small businesses through AI agents. This model suggests a broader global shift where enterprises prioritize cost savings and risk reduction through automation.

Similarly, firms like 3one4 Capital have shifted their focus to technology and data-driven businesses across consumer media, fintech, and digital health. Their Fund IV, an early-stage venture fund, targets consumer internet, SaaS, and climate tech with a median check size between $1.5 million and $3 million. The fund's impact strategy focuses on SME digitization and financial inclusion, as seen in their investments in BetterPlace and Open.

Micro-VC Fund Sizes and Stage Focus (2024-2025)

VC Firm | Founded | Latest Fund Size | Key Focus / Strategy |

3one4 Capital | 2016 | $100M+ (Fund IV) | Fintech, SaaS, Climate Tech |

Speciale Invest | 2017 | ₹1,400 Cr (Growth II) | Deep-tech, Spacetech, Quantum |

Better Capital | 2018 | $100M+ (Solo GP) | Consumer Tech, Fintech, AI Agents |

Java Capital | 2020 | ₹75 Cr (Fund I) | Pre-seed, Idea to Prototype |

Antler India | 2021 | $75M (Inaugural) | AI Residency, Day Zero backing |

Prime Venture Partners | 2011 | $72M (Fund III) | Fintech, Health, Edtech |

India Quotient | 2012 | $60M (Recent) | Indian consumer market |

In this environment, "Outcome-as-a-Service" represents a second-order insight: the commoditization of software tools is forcing startups to move up the value chain by guaranteeing results. For investors, this requires a deeper understanding of the operational dynamics of the industries they target, moving beyond simple tech metrics to evaluate the startup's ability to integrate into complex enterprise workflows.

Institutionalization of the Asset Class: LP and GP Dynamics

The maturation of the Bangalore ecosystem is reflected in the profile of the Limited Partners (LPs) backing these funds. Early-stage funds are increasingly seeing participation from institutional LPs rather than just family offices. For instance, 3one4 Capital Fund IV has received significant backing from the International Finance Corporation (IFC), which committed up to $15 million, not to exceed 20% of the fund’s total capital commitments. British International Investment (BII) also invested in Fund IV, helping it achieve its target size and allowing for follow-on investments that increase the scale of impact.

The GP (General Partner) model is also evolving. Solo GPs like Vaibhav Domkundwar redefine the traditional venture model by maintaining deep engagement with 20–25 companies while managing a portfolio of over 240. This reflects a structural advantage where the GP can make high-conviction, agile decisions without the overhead of a larger firm. Conversely, Speciale Invest has added a third partner, Vijay Jacob, to lead its growth stage investments, signaling a move toward more traditional institutional structures as funds scale.

Structural Differences in Post-Investment Support

The distinction in post-investment involvement remains a critical factor for founders when choosing between an angel and a VC. Angel investors are generally more hands-off, investing in the entrepreneur themselves rather than just the business viability. Some angels act as mentors, sharing their personal networks to open doors on "week one," which is invaluable for niche sectors.

Micro-VCs, however, often have dedicated "platform" teams focused on post-investment support functions such as marketing, talent recruiting, and business development programs. Modern VCs might boast a head of talent who sources executives or a community manager who organizes peer events for portfolio CEOs. This rise in platform teams reflects founders' expectations for firms that can actively help with hiring and partnerships beyond providing capital.

Regulatory Catalysts: The 2024-2025 Policy Landscape

India’s regulatory environment has become significantly more proactive in nurturing the startup ecosystem. The Union Budget 2024–25 was a landmark for early-stage funding, not only for the abolition of the angel tax but also for the reduction of long-term capital gains (LTCG) tax rates and the simplification of foreign venture capital investor (FVCI) registrations. These reforms signaled a positive momentum for the ecosystem, reducing the friction for domestic and international capital flow.

At the state level, the Karnataka Startup Policy 2025–2030, backed by a ₹518 crore corpus, aims to build 25,000 startups, with an intentional push to grow 10,000 of them outside Bangalore to promote regional parity. The policy provides a blueprint for Karnataka's tech ecosystem, which captured $1.7 billion in funding in H1 2025.

Key Policy Initiatives and Their Ecosystem Impact

Initiative / Program | Governing Body | Key Benefit / Goal |

Angel Tax Abolition | Government of India | Removed valuation-linked tax on pre-seed deals |

Startup Policy 2025-30 | Karnataka State | ₹518 Cr for 25,000 startups; regional focus |

Space Startup Fund | IN-SPACe / ISRO | Approved Oct 2024 for satellite/launch tech |

Deep Tech Draft Policy | Dept. of Science/Tech | Regulatory sandboxes and IP ownership norms |

Quantum Mission | Govt. of India | ₹6,000 Cr for computing and encryption tech |

FoF for Startups | SIDBI / GOI | ₹10,000 Cr additional corpus announced 2025 |

The establishment of the Space Startup Fund and the National Quantum Mission indicates a strategic shift toward "sovereign technology"—technologies that enhance India's resilience and competitiveness in the global economy. For micro-VCs like Speciale Invest, this aligns with their long-term focus on backing companies that develop scalable intellectual property within India.

The "Funding Winter" and the Recalibration of Valuations

The Indian startup ecosystem faced a "rocky journey" in 2024, with early-stage funding (seed, angel, and Series A) dropping to $3 billion across 1,533 deals—a sharp decline from $4 billion across 2,137 deals in 2023. This contraction, often termed the "funding winter," led to a market recovery characterized by disciplined deployment and sector rotation toward proven models. Investors became increasingly cautious, prioritizing profitability and leaner teams.

However, Bangalore's early-stage engine proved resilient. While larger funding rounds slowed, seed and pre-seed activity remained alive, albeit smaller and faster. The median ticket size in Q1 2025 was $3 million, down from $3.7 million in 2024, reflecting a return to normalized valuations. This valuation discipline is now the "new normal," with investors demanding real traction rather than just expansion potential.

Quarterly Comparison of Startup Funding (Q1 2023–Q1 2025)

Metric | Q1 2023 | Q1 2024 | Q1 2025 |

Total Funding | $12 Billion | $2.2 Billion | $3.1 Billion |

Total Deal Count | 506 | 226 | 232 |

Median Ticket Size | $4 Million | $3.7 Million | $3 Million |

M&A Activity | 100+ | 15+ | 26+ |

Despite the dip in national averages, Bangalore accounted for approximately 43% of total startup funding in H1 2025, maintaining its lead in both deal count and funding value. This concentration of activity suggests that even during a funding winter, Bangalore remains the "warmest place to build," as investors prioritize high-density talent pools where the risk of failure is mitigated by peer learning and available support services.

Exit Trajectories and the Maturation of Public Markets

The success of the angel and micro-VC ecosystem is inextricably linked to the availability of exit routes. In 2024 and 2025, the Indian capital markets showed significant resilience, with public market exits rising to 76% of total exit value. A 7x surge in IPO exit value was fueled by rising liquidity, recovery in tech stock valuations, and a pent-up IPO backlog.

Notable exits and IPOs have power this change. For instance, companies like PhonePe and Razorpay, which were once the beneficiaries of Bangalore’s early-stage angel ecosystem, are now leaders in the digital payment infrastructure, attracting AI-driven R&D and innovative platforms. This maturity allows early-stage investors to achieve high returns, which are then recycled back into the ecosystem. Better Capital reported over 10 profitable exits with returns ranging from 6x to 90x, illustrating the outsized potential of successful pre-seed bets.

The Reopening of the IPO Window and Exit Trends

Exit Metric (2024) | Performance / Data Point | Implications for Investors |

Total Exit Value | $26.7 Billion | 7% increase year-on-year |

Public Market Share | 76% of exit value | IPOs are the primary exit engine |

Exit Deal Volume | 282 Deals | Shift toward higher-value buyouts |

Secondary Exits | 10.4% decline in volume | Market favoring quality over volume |

The buoyant Indian capital markets have impacted PE/VC investor confidence, leading to a surge in buyout transactions, which saw a 39% surge in value in 2024. This shift toward buyouts suggests that the ecosystem is entering a consolidation phase, where larger institutions are acquiring high-quality assets built by early-stage founders and their angel/micro-VC backers.

The Role of Strategic Sequencing for Founders

For founders navigating the Bangalore ecosystem, the choice between raising from an angel network or a micro-VC is often a matter of strategic sequencing. Raising from angels first can help build traction and improve terms for later VC rounds. This "Angel-First" strategy is recommended when a startup has just an MVP or early traction and needs flexible terms and mentorship.

Alternatively, a "Lead-VC with Angel Support" strategy involves having a respected VC lead the round with participation from strategic angels. This provides the institutional support and capital of a VC while retaining the valuable individual mentorship and network access of an angel.

Decision Framework for Early-Stage Fundraising

Stage / Reality | Preferred Investor Type | Reasoning |

Pre-Seed / Concept | Angel Investor / Network | accessible; bet on vision/team |

Seed / MVP Traction | Micro-VC or Angel | Viable for both; focus on speed |

Scaling / PMF Proven | Traditional VC Firm | Need $1M-$10M+; institutional board |

Growth Stage | Late-Stage VC / PE | Aggressive growth for venture outcomes |

The right choice depends on factors like capital needs, growth ambitions, and the desired level of investor involvement. Founders must honestly evaluate their current reality: what meaningful milestones have been achieved and what evidence of product-market fit can be demonstrated. In Bangalore, where the ecosystem is highly networked, angels often act as a bridge, preparing startups for the more rigorous requirements of the micro-VC and larger venture capital layers.

Conclusion: The Professionalization of Early Risk

The period between 2024 and 2026 has solidified Bangalore’s position as a global tier-one startup hub through the professionalization of its early-stage capital markets. The bifurcation into angel networks and micro-VCs has created a specialized infrastructure where risk is underwritten with increasing precision. Angel networks continue to serve as the vital entry point for "vision-stage" startups, leveraging the wealth and experience of Bangalore’s corporate and entrepreneurial elite. Simultaneously, micro-VCs have evolved into sophisticated institutional players, employing data-driven due diligence and robust platform support to back the next generation of global technology champions.

The sectoral rotation toward deep-tech, space tech, and "Outcome-as-a-Service" AI models demonstrates the ecosystem’s ability to pivot toward high-complexity, high-moat ventures. Supported by progressive regulatory reforms and a resilient public market for exits, the Bangalore early-stage funding engine is no longer just a source of capital; it is a sophisticated ecosystem of mentorship, institutional discipline, and strategic guidance. For founders and investors alike, the key to navigating this landscape lies in understanding the distinct mandates of these two institutional archetypes and leveraging their complementary strengths to build sustainable, globally competitive businesses from the ground up.

Read More -

1. From Idea to MVP: A Step-by-Step Guide for Solo Founder

🔗 https://findnstart.com/blogs/from-idea-to-mvp-a-step-by-step-guide-for-solo-founder

2. How to Validate Your Startup Idea in 48 Hours for $0

🔗 https://findnstart.com/blogs/how-to-validate-your-startup-idea-in-48-hours-for-0

3. Remote vs. Local: Does Your Co-Founder Need to Live in the Same City?

🔗 https://findnstart.com/blogs/remote-vs-local-does-your-co-founder-need-to-live-in-the-same-city

4. The 2026 Startup Landscape: What Has Fundamentally Changed (and Why Founder Skills Matter More Than Ever)

5. The Most In-Demand Skills for Startup Founders in 2026

🔗 https://findnstart.com/blogs/the-most-in-demand-skills-for-startup-founders-in-2026

6. How to Find a Technical Co-Founder (Without a Six-Figure Salary)

🔗 https://findnstart.com/blogs/how-to-find-a-technical-co-founder-without-a-six-figure-salary

7. 5 Red Flags to Look for When Choosing a Startup Partner

🔗 https://findnstart.com/blogs/5-red-flags-to-look-for-when-choosing-a-startup-partner

8. How to Pitch Your Idea to Potential Co-Founders

🔗 https://findnstart.com/blogs/how-to-pitch-your-idea-to-potential-co-founders

9. How to Build a Portfolio that Attracts High-Growth Startup Founders

🔗 https://findnstart.com/blogs/how-to-build-a-portfolio-that-attracts-high-growth-startup-founders

10. Equity vs. Salary: How to Split Ownership with Your First Teammate

🔗 https://findnstart.com/blogs/equity-vs-salary-how-to-split-ownership-with-your-first-teammate

11. Why Joining an Early-Stage Startup is Better Than a Corporate Job

🔗 https://findnstart.com/blogs/why-joining-an-early-stage-startup-is-better-than-a-corporate-job

12. The Future of EdTech: Why Developers and Educators Need to Team Up Now

🔗 https://findnstart.com/blogs/the-future-of-edtech-why-developers-and-educators-need-to-team-up-now

13. The Architecture of Symbiosis: Analytical Perspectives on the Five Habits of Successful Startup Duos

14. Finding a Co-Founder in the AI Space: What Skills Should You Look For?

🔗 https://findnstart.com/blogs/finding-a-co-founder-in-the-ai-space-what-skills-should-you-look-for

15. Overcoming Analysis Paralysis and the Strategic Path to Execution

🔗 https://findnstart.com/blogs/overcoming-analysis-paralysis-and-the-strategic-path-to-execution

16. From College Project to Company: How to Find Your Student Co-Founder

🔗 https://findnstart.com/blogs/from-college-project-to-company-how-to-find-your-student-co-founder

17. How to Start a Startup While Working a Full-Time Job

🔗 https://findnstart.com/blogs/how-to-start-a-startup-while-working-a-full-time-job

18. How to Build a HealthTech Startup Without a Medical Degree

🔗 https://findnstart.com/blogs/how-to-build-a-healthtech-startup-without-a-medical-degree

19. The Solitary Architect: Executive Isolation in Entrepreneurship

20. The 2026 Guide to Launching a SaaS as a Solo Developer

21. What Sustainable Growth Actually Looks Like

🔗 https://findnstart.com/blogs/what-sustainable-growth-actually-looks-like

22. The Early Warning Signs Your Startup Is in Trouble

🔗 https://findnstart.com/blogs/the-early-warning-signs-your-startup-is-in-trouble

23. How to Grow Without Burning Out

🔗 https://findnstart.com/blogs/how-to-grow-without-burning-out

24. The Truth About “Runway” Most Founders Ignore

🔗 https://findnstart.com/blogs/the-truth-about-runway-most-founders-ignore

25. Revenue Solves More Problems Than Funding

🔗 https://findnstart.com/blogs/revenue-solves-more-problems-than-funding

26. What No One Tells You About Being a Solo Founder

🔗 https://findnstart.com/blogs/what-no-one-tells-you-about-being-a-solo-founder

27. Why Smart People Quit High-Paying Jobs to Build Startups (And Why Most Regret It)

28. Why Most Startup Advice on Twitter Is Dangerous

🔗 https://findnstart.com/blogs/why-most-startup-advice-on-twitter-is-dangerous

29. Decision Fatigue: The Silent Startup Killer

🔗 https://findnstart.com/blogs/decision-fatigue-the-silent-startup-killer

30. Fear vs Logic: How Founders Actually Make Decisions

🔗 https://findnstart.com/blogs/fear-vs-logic-how-founders-actually-make-decisions

31. How Overthinking Destroys Early Momentum

🔗 https://findnstart.com/blogs/how-overthinking-destroys-early-momentum

32. Ideas Don’t Scale. Systems Do.

🔗 https://findnstart.com/blogs/ideas-dont-scale-systems-do

33. The First Hire That Actually Matters

🔗 https://findnstart.com/blogs/the-first-hire-that-actually-matters

34. How the First 100 Users Decide Your Startup’s Fate

🔗 https://findnstart.com/blogs/how-the-first-100-users-decide-your-startups-fate

35. Why Your Startup Doesn’t Need Growth — It Needs Focus

🔗 https://findnstart.com/blogs/why-your-startup-doesnt-need-growthit-needs-focus

36. Why Most Startups Die Quietly

🔗 https://findnstart.com/blogs/why-most-startups-die-quietly

37. Lessons Learned Too Late by First-Time Founders

🔗 https://findnstart.com/blogs/lessons-learned-too-late-by-first-time-founders

38. The Myth of the “Overnight Success” Startup

🔗 https://findnstart.com/blogs/the-myth-of-the-overnight-success-startup