AgriTech Startups Transforming Brazil’s Agriculture Industry

June 28, 2026 by Harshit Gupta

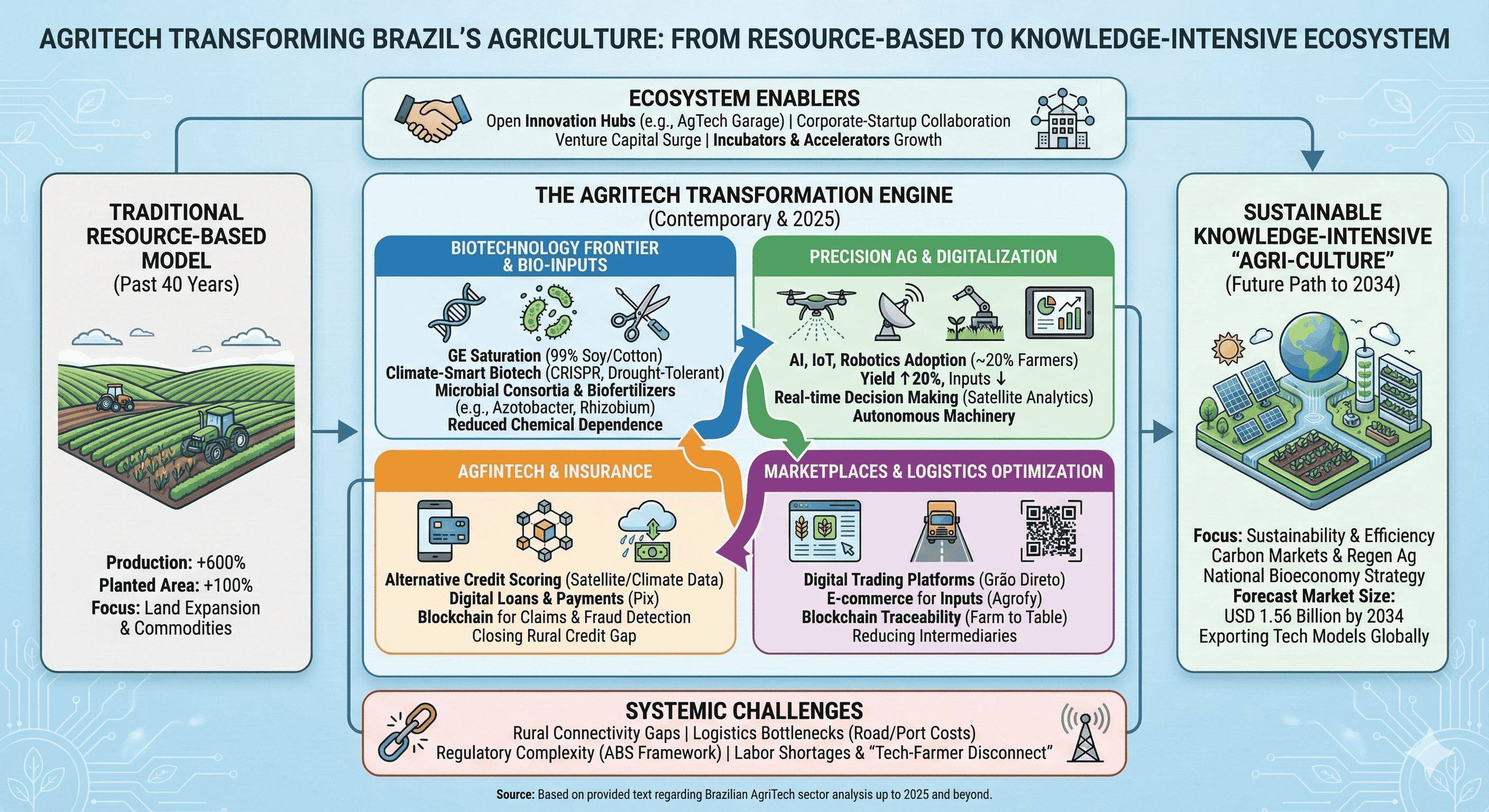

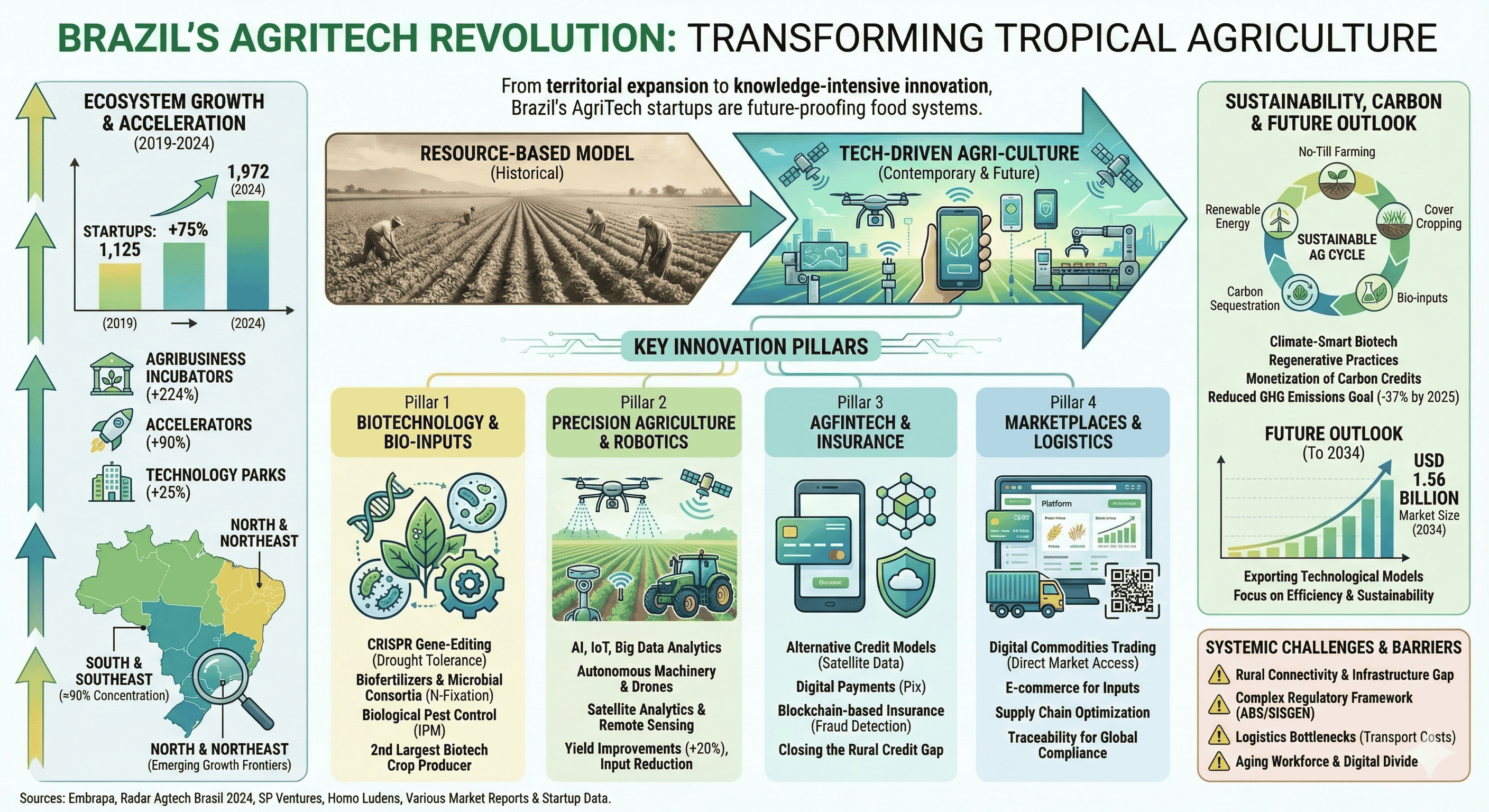

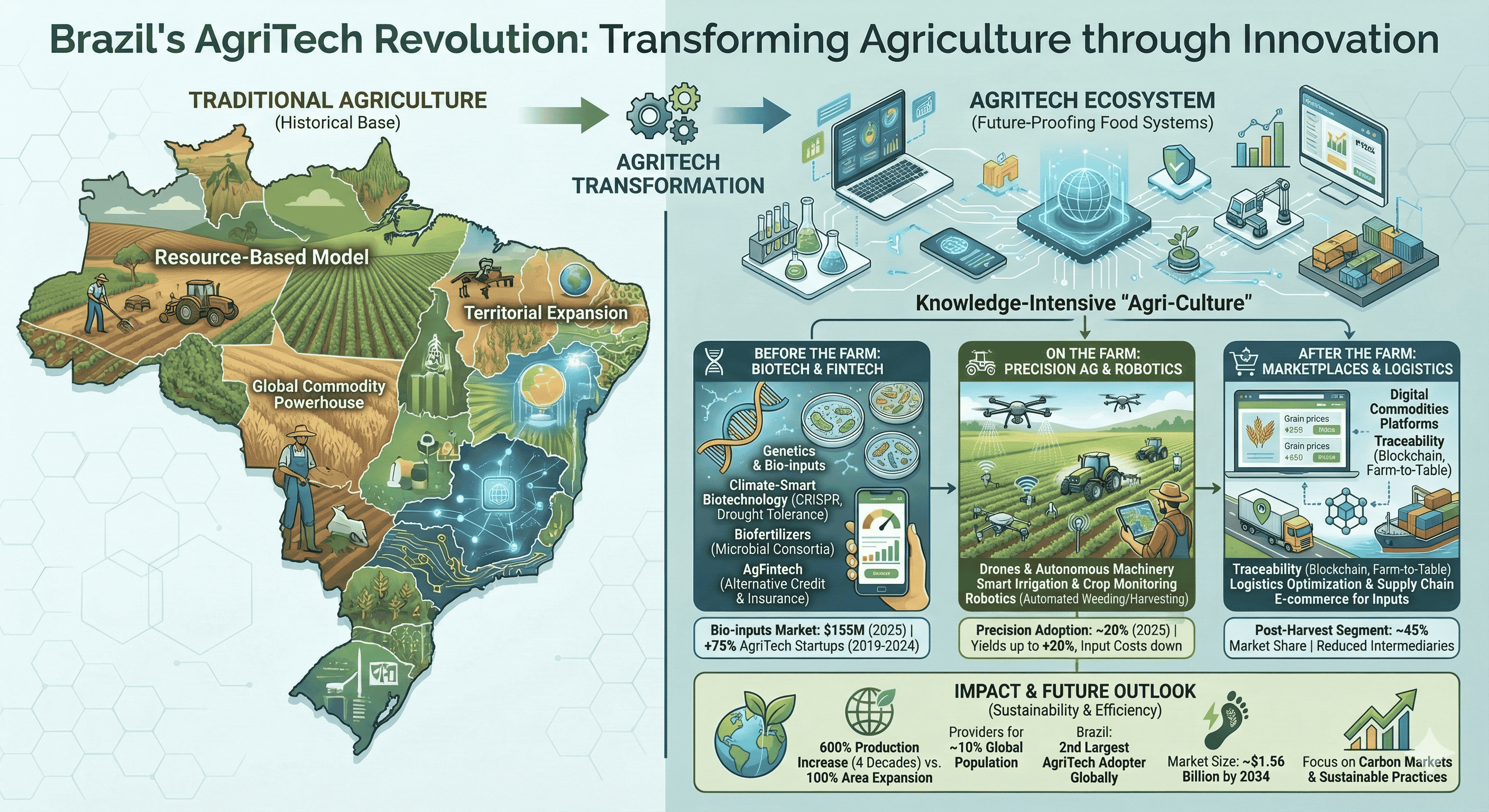

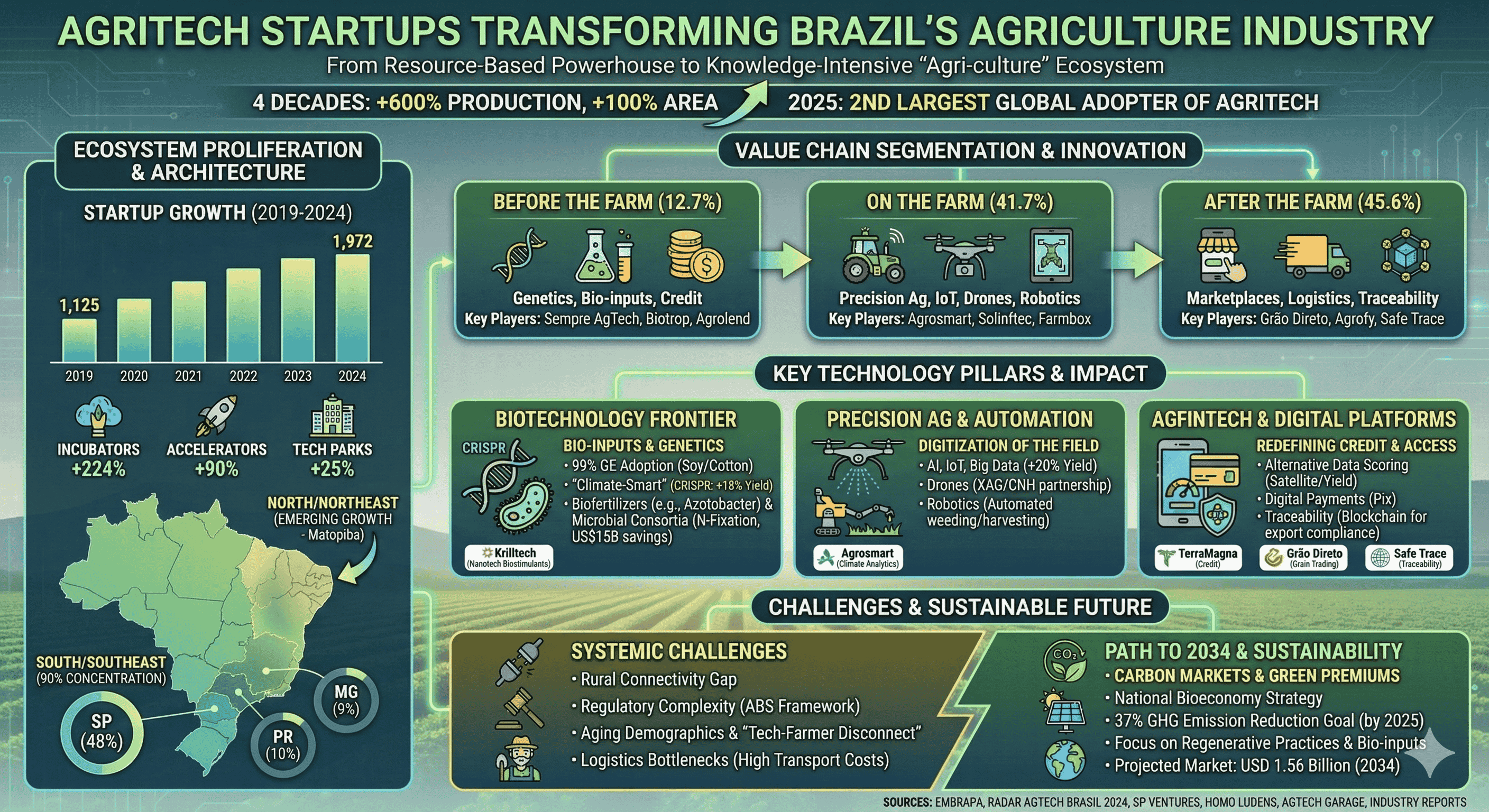

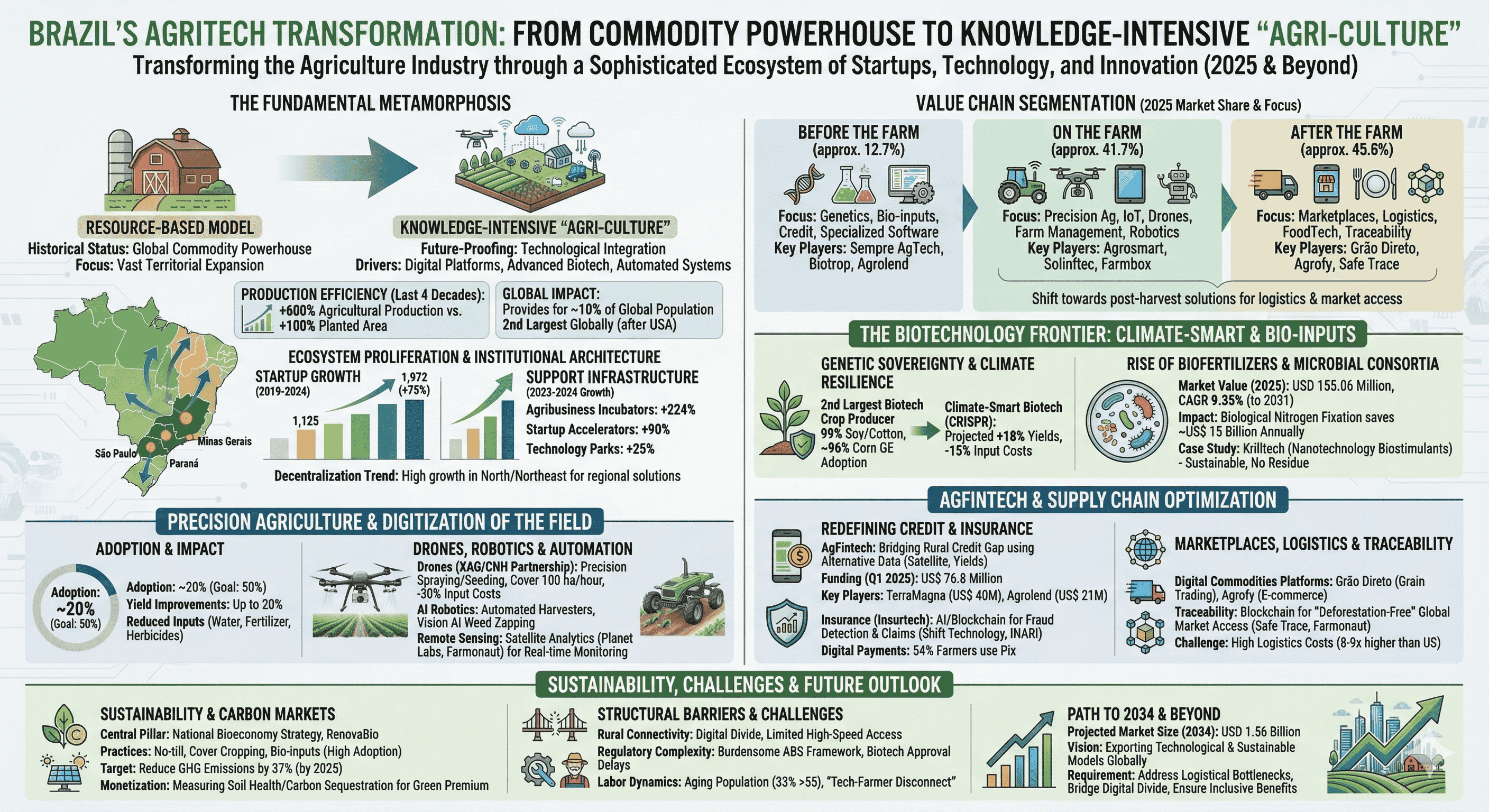

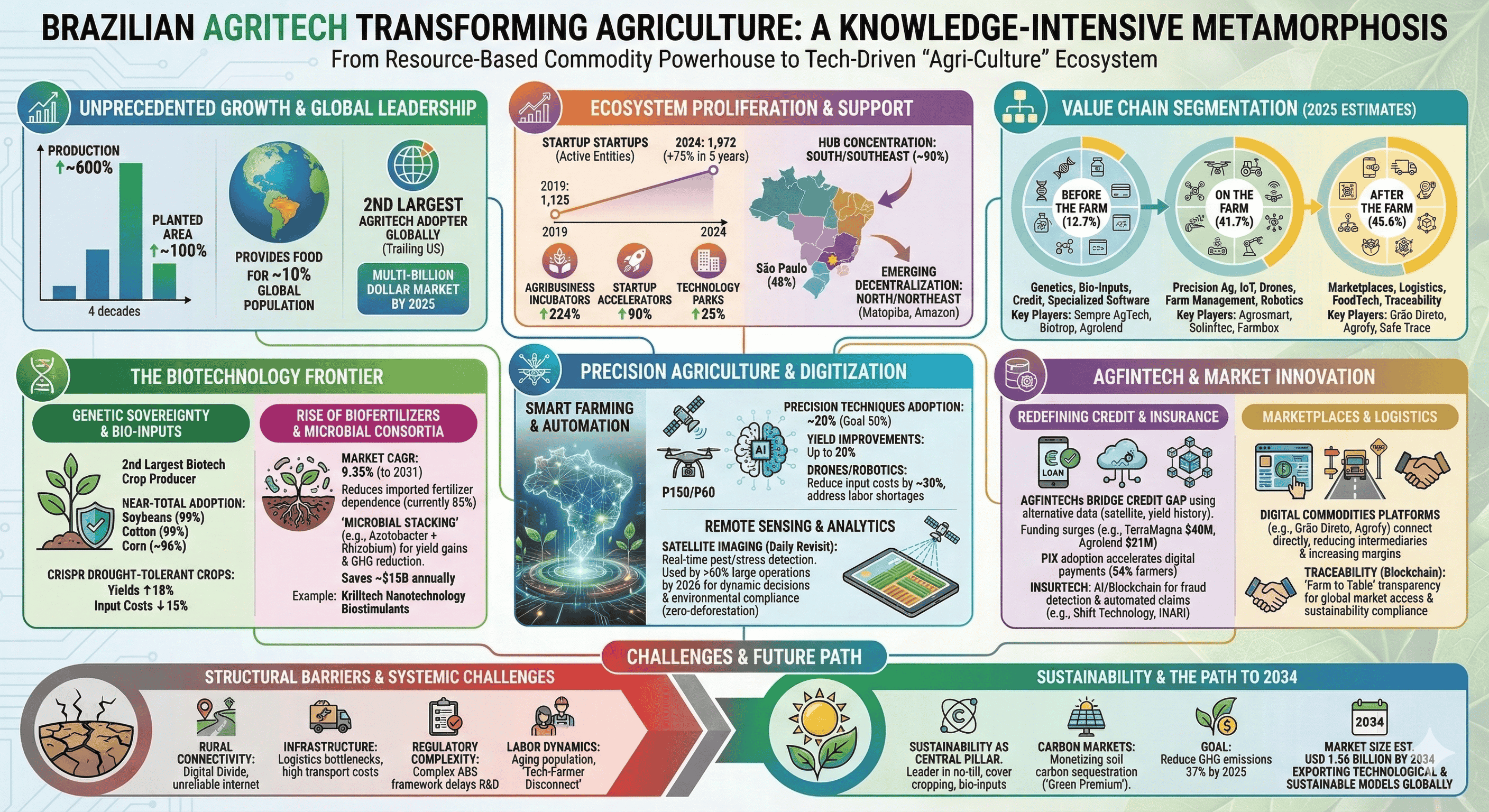

The contemporary trajectory of the Brazilian agricultural sector is no longer defined solely by its vast territorial expansion or its historical status as a global commodity powerhouse; instead, it is undergoing a fundamental metamorphosis into a knowledge-intensive "agri-culture" driven by a sophisticated ecosystem of AgriTech startups. This shift represents a decisive transition from a resource-based economic model to one predicated on technological integration, where digital platforms, advanced biotechnology, and automated systems are utilized to future-proof food systems against the compounding pressures of climate variability and global supply chain volatility. Over the past four decades, Brazil has increased its agricultural production by nearly 600% while expanding its planted area by only 100%, a feat of efficiency that underscores the foundational role of technology in maintaining the nation’s status as a provider for approximately 10% of the global population. By 2025, the Brazilian AgriTech market has matured into a multi-billion dollar arena, characterized by a surge in domestic innovation that positions the country as the second-largest adopter of agricultural technology globally, trailing only the United States.

The Institutional Architecture and Ecosystem Proliferation

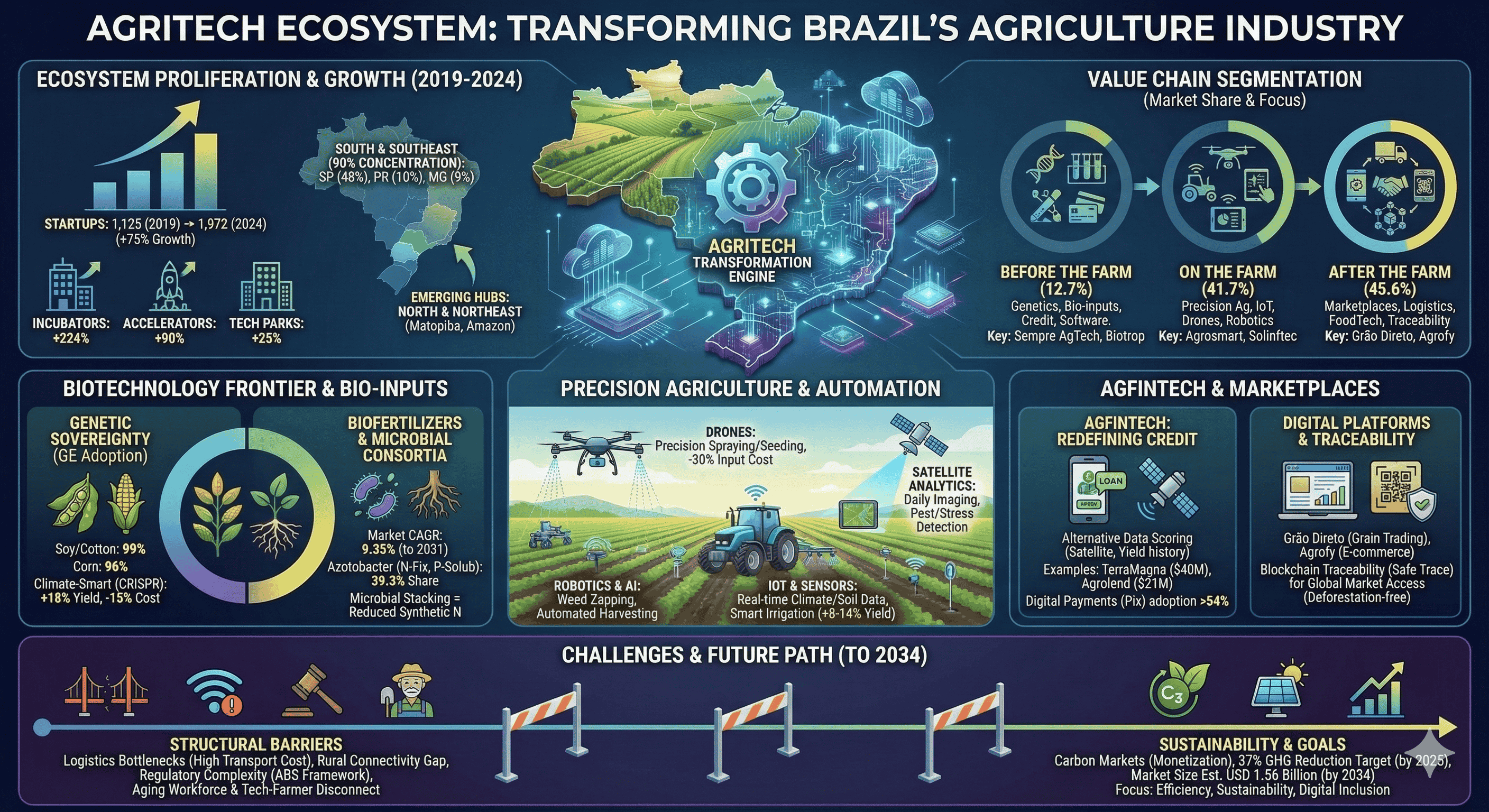

The acceleration of the Brazilian AgriTech ecosystem is meticulously documented in the 2024 edition of the Radar Agtech Brasil report, a comprehensive mapping effort led by the Brazilian Agricultural Research Corporation (Embrapa) in collaboration with SP Ventures and Homo Ludens. This census of innovation reveals a sector in a state of rapid expansion; the number of AgriTech startups in Brazil has increased by more than 75% over a five-year period, rising from 1,125 entities in 2019 to 1,972 active companies by early 2024. This quantitative growth is mirrored by a qualitative maturation of the support infrastructure. Between 2023 and 2024, the number of agribusiness incubators in Brazil surged by 224%, while startup accelerators grew by 90%, and technology parks saw a 25% increase. Such a robust institutional framework ensures that early-stage ventures have access to the specialized mentorship and capital required to navigate the unique complexities of tropical agriculture.

Geographically, the ecosystem remains centered in the South and Southeast regions, which collectively host nearly 90% of the country’s AgriTech firms. The state of São Paulo serves as the primary epicenter, containing approximately 48% of these startups, followed by Paraná at 10% and Minas Gerais at 9%. This concentration is largely due to the proximity of leading research institutions, such as the Luiz de Queiroz School of Agriculture (ESALQ/USP), and the presence of major agribusiness corporate headquarters. However, a significant emerging trend in 2025 is the decentralization of innovation. The North and Northeast regions, historically underserved by technological hubs, are currently experiencing the highest proportional growth rates in startup formation. This shift is driven by the need to develop localized solutions for the Matopiba region (the agricultural frontier spanning Maranhão, Tocantins, Piauí, and Bahia) and the specialized requirements of cocoa and fruit production in the Amazon and Northeast biomes.

Segmentation of the Value Chain

The Brazilian AgriTech landscape is traditionally segmented into three operational phases: before, on, and after the farm. As of 2021, the "after the farm" segment was the most populous, comprising 719 startups, followed by "on the farm" solutions with 657, and "before the farm" with 200. By 2025, the proliferation of digital marketplaces and foodtech solutions has further tilted the balance toward the post-harvest segment, reflecting the industry's focus on solving logistics bottlenecks and improving market access.

Segment | Primary Focus Areas | Market Share (Approx.) | Key Players |

Before the Farm | Genetics, Bio-inputs, Credit, Specialized Software | 12.7% | Sempre AgTech, Biotrop, Agrolend |

On the Farm | Precision Ag, IoT, Drones, Farm Management, Robotics | 41.7% | Agrosmart, Solinftec, Farmbox |

After the Farm | Marketplaces, Logistics, FoodTech, Traceability | 45.6% | Grão Direto, Agrofy, Safe Trace |

The Biotechnology Frontier: Bio-inputs and Genetic Sovereignty

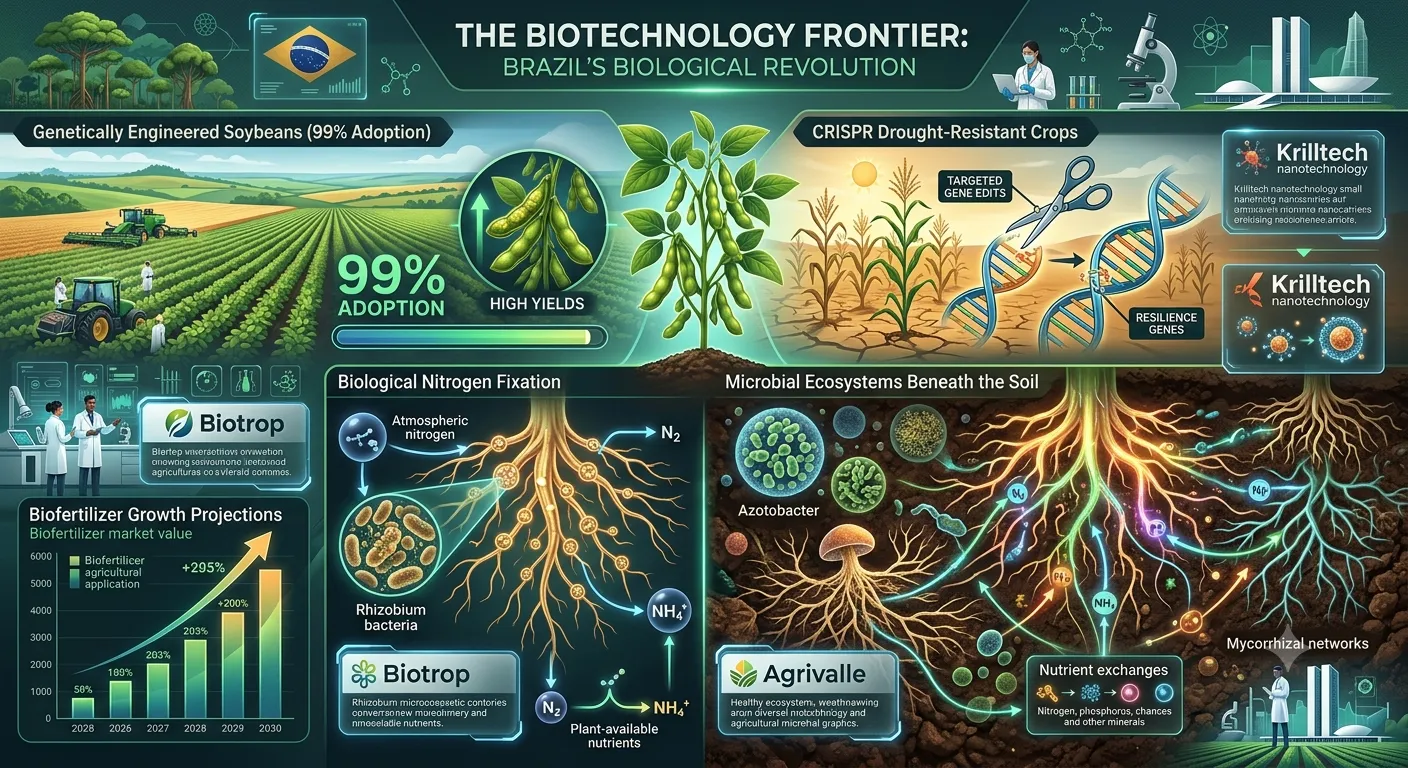

Biotechnology serves as the scientific backbone of Brazil’s agricultural resilience, particularly in the face of escalating pest pressures and climate stress. Brazil is currently the world’s second-largest producer of biotech crops, with 131 events approved for plants and a total of 134 approved traits by 2025. The adoption rate for genetically engineered (GE) traits has reached a state of near-total saturation in key commodities: 99% for soybeans and cotton, and approximately 96% for corn. For the 2024/2025 crop season, it is estimated that 69.6 million hectares are planted with GE seeds, a major contributor to the sustained yield growth that has defined the sector for decades.

The current wave of innovation is moving beyond traditional herbicide tolerance toward "Climate-Smart" biotechnology. This includes the development of drought-tolerant soybean and maize varieties through gene-editing techniques like CRISPR, which are projected to increase yields by 18% while reducing input costs by 15%. Furthermore, the 2025 regulatory landscape saw a historic record in pesticide registration approvals, with 912 products approved, of which 162 were biological products. This shift underscores the industry’s transition away from purely synthetic chemistry toward integrated pest management (IPM) systems that utilize beneficial microorganisms.

The Rise of Biofertilizers and Microbial Consortia

The Brazilian biofertilizer market has entered a period of robust expansion, valued at USD 155.06 million in 2025 and projected to grow at a Compound Annual Growth Rate (CAGR) of 9.35% through 2031. This growth is catalyzed by the volatility of synthetic nitrogen prices and a strategic national push to reduce dependence on imported fertilizers, which currently account for 85% of Brazil's total supply. Startups like Biotrop and Agrivalle are leading this charge, focusing on the industrial multiplication of bacteria such as Azotobacter and Rhizobium. Azotobacter-based products, which facilitate both nitrogen fixation and phosphate solubilization, held a dominant 39.3% market share in 2025, particularly in the acidic soils of the Cerrado where phosphate fixation is a chronic challenge.

The technical advancement in this sector is characterized by "microbial stacking"—the creation of multi-strain consortia that provide synergistic benefits. Field trials conducted by Embrapa in 2024 demonstrated that co-inoculation protocols (e.g., combining Bradyrhizobium japonicum with Azospirillum brasilense) deliver significant yield gains in soybean and corn rotations, while simultaneously reducing greenhouse gas emissions compared to synthetic alternatives. This "biological nitrogen fixation" alone saves Brazilian farmers approximately US$ 15 billion annually.

Biofertilizer Type | 2025 Market Size (Value) | Projected CAGR (2026-31) | Key Soil Benefit |

Azotobacter | USD 60.9 Million | 9.1% | N-Fixation & Phosphate Solubilization |

Rhizobium | Significant | 11.1% | Symbiotic N-Fixation in Legumes |

Mycorrhiza | Emerging | High | Water uptake and Nutrient Scavenging |

PSB (Phosphate Solubilizing) | Growing | 9.5% | Releasing fixed P in acidic soils |

Sources:

Case Study: Krilltech and Nanotechnology

A prime example of high-tech domestic innovation is Krilltech, a startup that emerged from a seven-year research partnership between the University of Brasília (UnB) and Embrapa. Krilltech utilizes nanotechnology to develop biostimulants that are metabolized by the plant without leaving residues in the tissue or soil. These nanoproducts increase photosynthesis rates, optimize water consumption, and serve as delivery mechanisms for essential micronutrients like zinc and iron. Because the production process is efficient and does not require imported equipment, Krilltech represents a model for sustainable, low-cost "green technology" that can compete with multinational incumbents while being tailored specifically for tropical climates.

Precision Agriculture: The Digitization of the Field

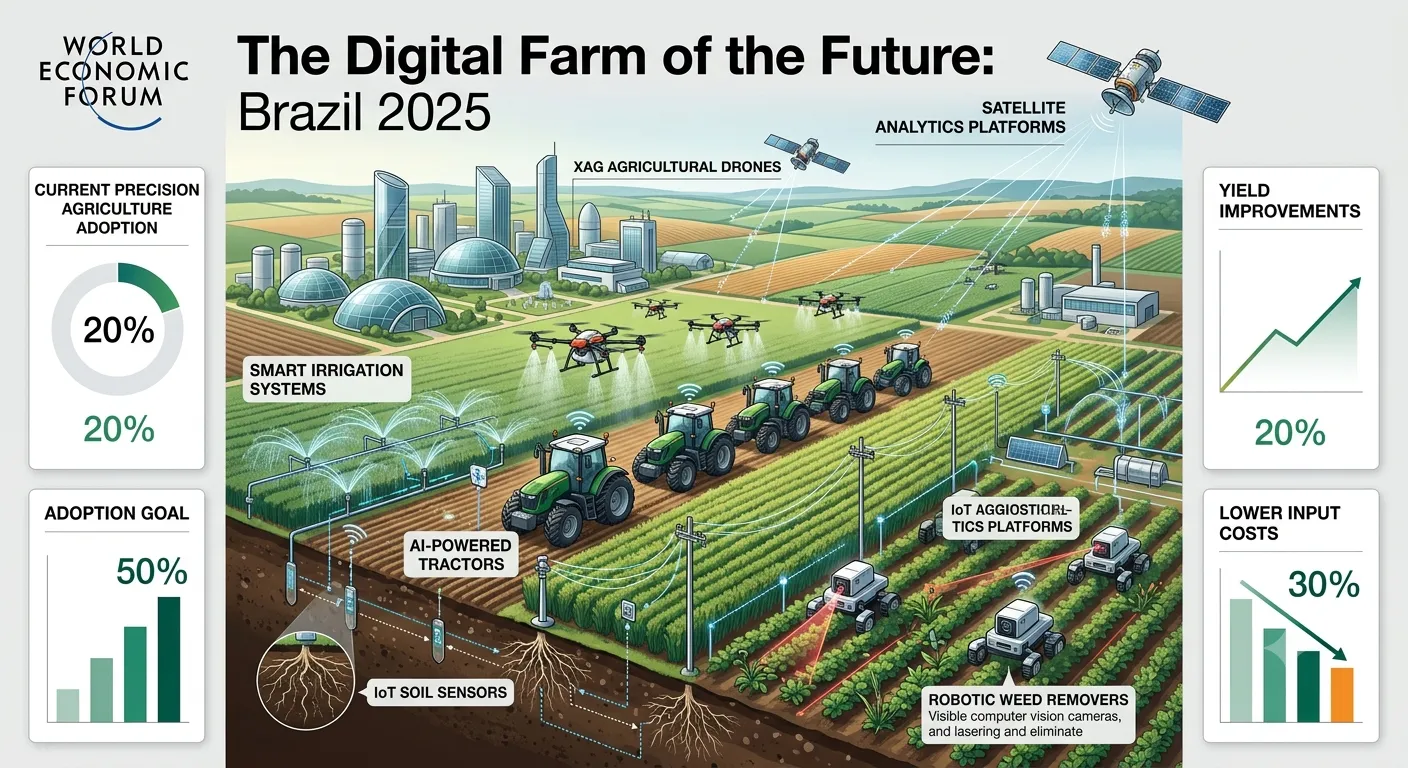

Precision agriculture has moved from an experimental concept to an operational necessity for remaining competitive in the Brazilian grain and sugar-energy sectors. By early 2025, approximately 20% of Brazilian farmers had adopted precision techniques, with government initiatives aiming to increase this figure to 50% through funding programs like the National Policy for Agroecology and Organic Production. These technologies, encompassing AI, IoT, and big data analytics, allow for yield improvements of up to 20% in major crops while reducing the consumption of water, fertilizer, and herbicides.

The core of this digital transformation is the integration of diverse data sources. Platforms like Agrosmart utilize climate and soil sensors to assist more than 100,000 farmers across nine countries in making real-time decisions on irrigation and planting. During the devastating 2024 floods in Rio Grande do Sul, Agrosmart’s predictive alerts allowed farmers to evacuate properties and bring harvests forward, demonstrating the critical role of technology in disaster mitigation and climate adaptation.

Drones, Robotics, and Automation

The use of Unmanned Aerial Vehicles (UAVs) and autonomous machinery has surged as a solution to labor shortages and the high cost of formal employment in rural areas. In 2025, a significant partnership between the drone manufacturer XAG and the machinery giant CNH unveiled specialized drones like the P150, designed for large-scale multi-functional operations, and the P60, a compact model tailored for smallholders. These drones are increasingly used for precision spraying and seeding, covering up to 100 hectares per hour and reducing input costs by up to 30%.

Furthermore, AI-powered robotics are being deployed for tasks traditionally dependent on manual labor. Startups are developing automated harvesters and robotic weeders that use vision AI and 3D deep learning to identify and "zap" weeds at the root without damaging the surrounding crops. This trend is particularly evident in the sugar-energy sector, where startups like AGTech Agrotecnologia provide automated systems for sugarcane planters and fertigation, significantly enhancing operational efficiency.

Technology Application | Estimated Adoption (2025) | Projected Impact (Yield ↑ / Cost ↓) | Sustainability Driver |

Precision Drones | 58% | Yield +12%, Cost -10% | Targeted input application |

Smart Irrigation | 64% | Yield +8-14%, Cost -12% | Water and energy conservation |

AI Crop Monitoring | High | Yield +20% | Early pest/disease detection |

Satellite Analytics | 65% | High | Dynamic decision-making |

Sources:

Remote Sensing and Satellite Analytics

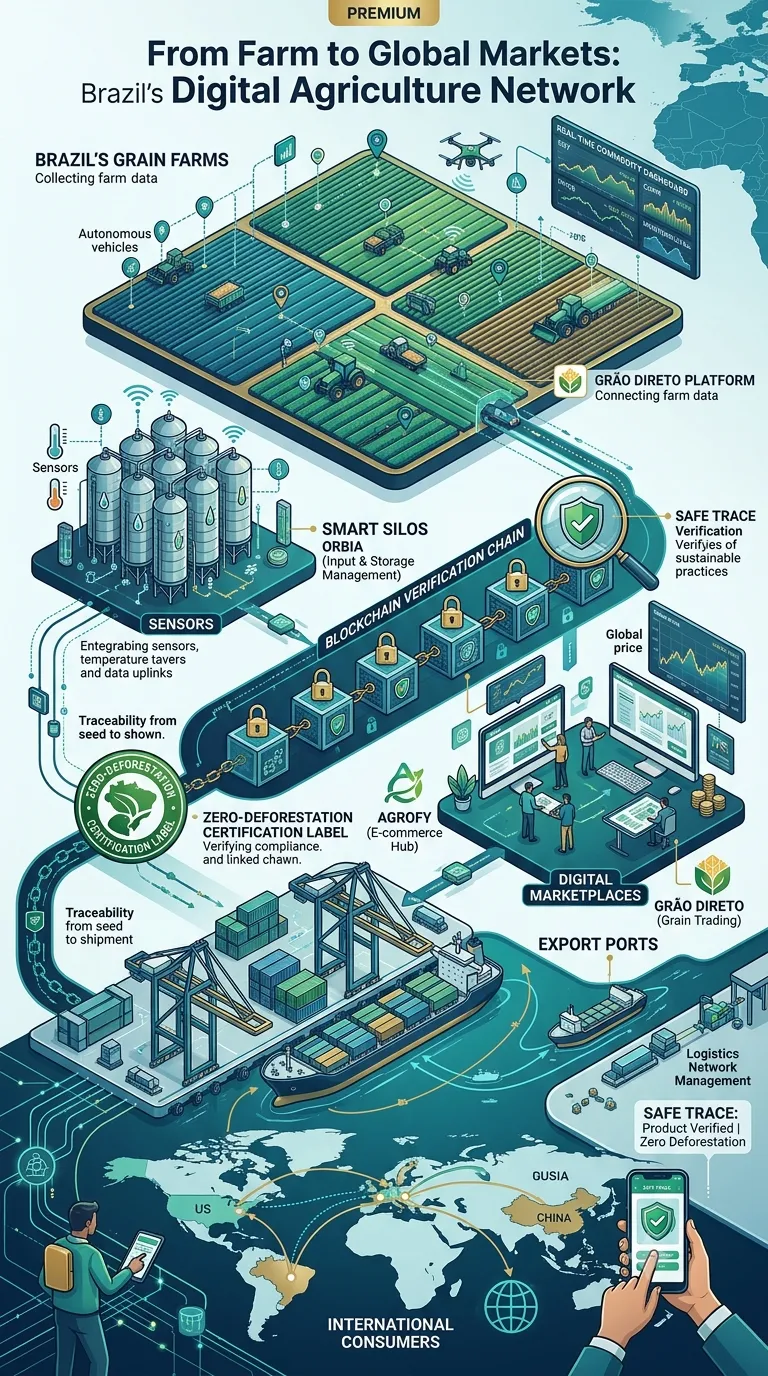

Satellite imaging has become a fundamental tool for macro-level farm management and environmental compliance. Companies like Planet Labs and Farmonaut provide high-resolution imagery with daily revisit capabilities, enabling farmers to flag pest hotspots, nutrient deficits, and water stress in real-time. By 2026, it is projected that over 60% of Brazil’s large agricultural operations will utilize satellite-powered analytics for dynamic decision-making. This technology is also vital for the forestry sector, where LiDAR and satellite monitoring are used for carbon accounting and timber asset management, ensuring compliance with global zero-deforestation standards.

AgFintech: Redefining Credit and Insurance

One of the most profound shifts in the Brazilian AgriTech ecosystem is the emergence of AgFintechs, which are addressing the historic credit gap in rural areas. In Brazil, traditional bank financing can be difficult for small and medium farmers to access, often requiring extensive collateral and long approval times. AgFintech startups are bypassing these hurdles by using alternative data—such as satellite health assessments, historical yield data, and climate sensors—to build proprietary credit scoring models.

Investment in this sub-sector has been significant. In early 2025, Brazilian agrifoodtech funding reached US$ 76.8 million in the first quarter alone, with fintech-related deals like TerraMagna’s US$ 40 million round and Agrolend’s US$ 21 million Series A leading the way. These firms often employ a mix of equity and debt financing to fund their credit portfolios, providing much-needed liquidity to input retailers and farmers alike. The integration of the Pix instant payment system has further accelerated this trend, with 54% of Brazilian farmers now using digital payments—a rate that surpasses the global average.

Insurance and Risk Mitigation

Climate variability, including the extreme droughts and rainfall events seen in 2023 and 2024, has made agricultural insurance more critical than ever. Insurtech startups are utilizing AI and blockchain to revolutionize fraud detection and claims automation. For example, platforms like Shift Technology use machine learning to identify fraudulent patterns in real-time, while cloud-based blockchain systems like INARI allow for transparent, automated insurance operations in emerging markets. This level of data-driven risk management is essential for attracting private capital back into a sector that is increasingly exposed to environmental threats.

AgFintech Leader | Primary Focus | Innovation Mechanism | Impact Scale |

TerraMagna | Credit & Financing | Satellite data for risk assessment | US$ 40M debt/equity round |

Agrolend | Digital Loans | Asset-backed lending via app | US$ 21M Series A |

Kanastra | Fintech Infrastructure | FIDC and back-office automation | R$ 170M Series B (2025) |

Traive | Risk Modeling | AI-driven credit scoring | US$ 17M funding |

Velotax | Tax & Credit | Digital tax compliance for agro | R$ 125M Series A |

Sources:

Marketplaces, Logistics, and Supply Chain Optimization

The Brazilian agricultural supply chain is vast and costly, with logistics—predominantly road transport—accounting for a substantial portion of the total cost of commodities like soybeans. Transport costs in Brazil are estimated to be 8-9 times higher than in the United States, leaving the sector vulnerable to fuel price volatility and infrastructure bottlenecks. To counter these systemic inefficiencies, AgriTech startups are developing digital marketplaces that connect farmers directly to buyers, reducing the number of intermediaries and increasing profit margins.

Digital Commodities Platforms

Grão Direto has emerged as the largest digital grain trading platform in Latin America, connecting thousands of farmers with hundreds of buying companies. By providing real-time quotes and intelligent data access, the platform enables farmers to make informed decisions and trade soybeans, corn, and sorghum more efficiently. The platform also offers corporate solutions that automate barter operations and grain trading, saving time for both sales teams and agribusiness firms like ADM Brazil. Similarly, Agrofy serves as a major e-commerce marketplace for agricultural inputs and equipment, with online agricultural sales in Brazil projected to exceed BRL 11.5 billion in the near future.

Traceability and Global Market Access

Traceability is no longer an optional luxury but a prerequisite for remaining competitive in international markets, particularly as European and Asian buyers demand "deforestation-free" and sustainable products. Blockchain-based traceability solutions are being employed to track produce "from farm to table," ensuring food safety and transparency. Startups like Safe Trace and those integrated into the Farmonaut platform connect growers, exporters, and consumers via immutable digital records that monitor land-use and environmental impact in real-time. This transition from cost-focused to resilience-focused systems is vital for Brazil to maintain its dominant export position.

Platform | Primary Service | Economic Impact | Technology Used |

Grão Direto | Grain Trading | Automates contracts, reduces fees | Real-time market data app |

Agrofy | Ag E-commerce | Direct market access for farmers | Digital marketplace |

Orbia | Inputs & Loyalty | Facilitates barter and points | Loyalty program platform |

Safe Trace | Traceability | Ensures export compliance | Blockchain |

Sources:

The Ecosystem of Open Innovation: Collaboration and Hubs

The rapid growth of the AgriTech sector in Brazil is fueled by a unique culture of open innovation, where established agribusiness giants collaborate with agile startups to solve operational challenges. Hubs such as AgTech Garage in Piracicaba have become the epicenters of this "4th era of innovation," bringing together thousands of startups, farmers, and corporate partners. Programs like "Intensive Connection" (IC) facilitate seven-month journeys of cooperation, where startups gain access to mentorship, networking, and the possibility of proof-of-concept (POC) deals with companies like John Deere, Bayer, and Bunge.

This collaborative model is equity-free, meaning startups are not required to give up ownership to participate, which encourages the best talent to join. The success stories from these hubs include companies like Perfect Flight (aerial application monitoring), Farmbox (farm management), and Cromai (AI for field operations), which have leveraged these connections to scale their solutions across Brazil and into international markets. The impact of these hubs extends beyond technology; they are driving a cultural change within legacy organizations, integrating innovation into legal, HR, and procurement departments.

Structural Barriers and Systemic Challenges

While the technological transformation is impressive, several critical challenges threaten to limit the full potential of Brazil’s AgriTech revolution. These obstacles are physical, regulatory, and demographic in nature, requiring coordinated public and private intervention to overcome.

Rural Connectivity and Infrastructure

Despite the rising digital maturity of farmers, a significant "digital divide" remains. Restricted availability of dependable internet and digital services in remote farming areas has historically hindered the implementation of advanced IoT and AI tools. While satellite internet providers like Starlink are beginning to bridge this gap, consistent high-speed access is still not universal. Furthermore, the aforementioned logistical bottlenecks in ports, highways, and railways increase operational costs and time-to-market, reducing the overall economic efficiency of the sector.

Regulatory Complexity and the ABS Framework

The regulatory environment, particularly regarding biotechnology and biodiversity, is a significant hurdle for domestic startups. Brazil’s Access and Benefit-Sharing (ABS) framework, which governs access to genetic resources from Brazilian biodiversity, is often described as burdensome and unpredictable. Complex requirements and delays in approving benefit-sharing agreements create legal uncertainty that can discourage investment and trade. This regulatory friction can lead to "jurisdiction shopping," where companies move their R&D activities to countries with simpler or more predictable rules, potentially eroding Brazil’s share in the global biodiversity-based biotech market.

Labor Dynamics and the "Tech-Farmer Disconnect"

The Brazilian rural population is aging and shrinking, with the rural share of the population declining from 15.3% in 2012 to 12.7% in 2022. Over 33% of farmers are now above the age of 55, and there is a distinct lack of generational renewal as younger people migrate to urban centers. This trend pressures producers to adopt automation but also creates a barrier for those who lack the digital literacy to operate advanced systems. Additionally, there is a recognized "tech-farmer disconnect," where many startups focus on sophisticated, capital-intensive technologies to attract venture capital, often overlooking the practical, low-cost needs of the millions of smallholder farmers who form the backbone of Brazil's internal food supply.

Barrier Category | Specific Challenge | Economic Consequence | Potential Mitigation |

Infrastructure | Port/Road bottlenecks | Logistics are 30-40% of soy cost | PPPs for intermodal transport |

Connectivity | Rural "Last Mile" access | Limits real-time IoT and AI | Expansion of 5G/Satellite internet |

Regulatory | ABS/SISGEN Framework | Delays biotech R&D | Simplification of benefit-sharing |

Labor | Aging farmer demographic | 33% of farmers > 55 years old | Re-skilling and youth incentives |

Financial | High initial tool cost | US$ 10k-15k per basic solution | Embedded AgFintech subsidies |

Sources:

Sustainability, Carbon Markets, and the Path to 2034

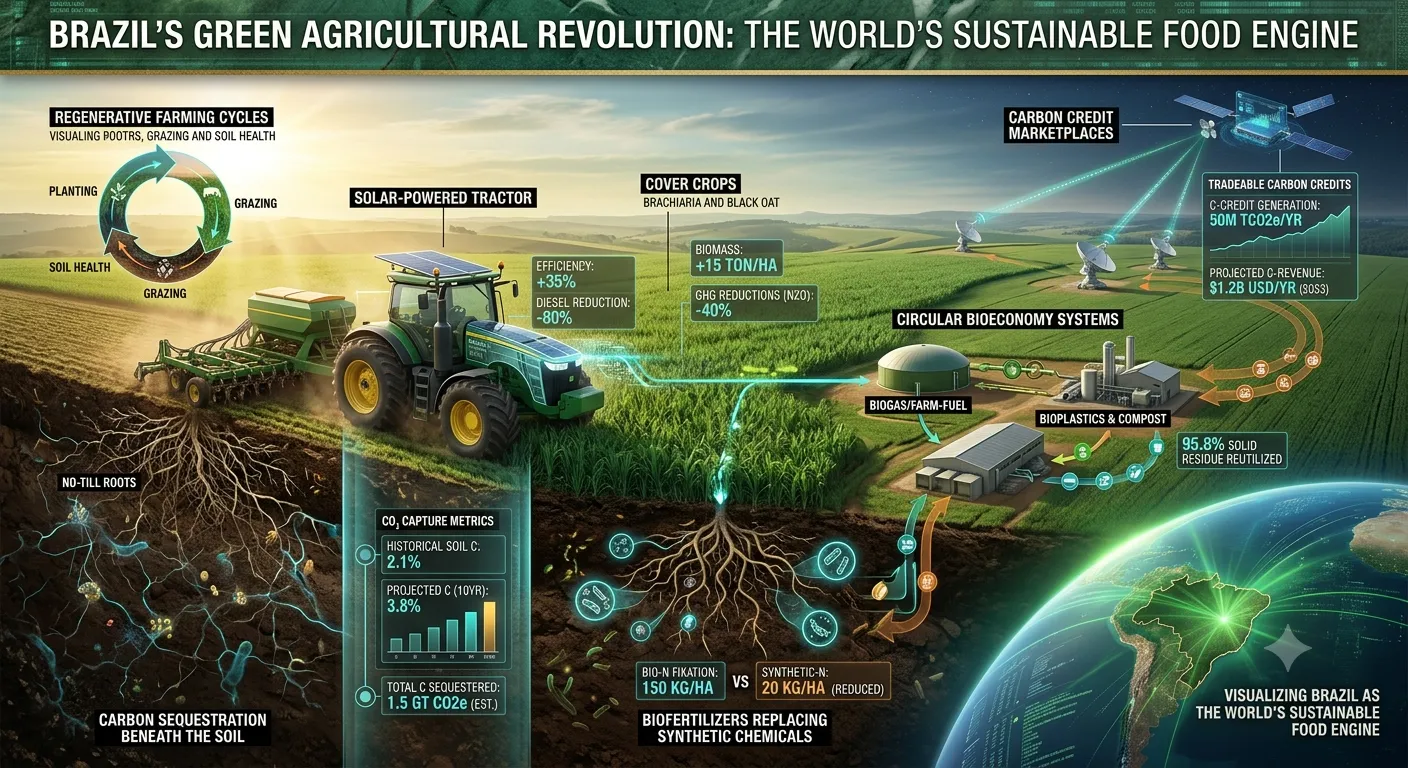

Sustainability is no longer a peripheral ethical concern but the central pillar of Brazil's agricultural strategy for 2025 and beyond. Brazilian farmers are already world leaders in sustainable practices, such as no-till farming, cover cropping, and the use of bio-inputs, which are adopted at rates more than double those of the US and Europe. The National Bioeconomy Strategy and programs like RenovaBio are further anchoring the market for biofertilizers and renewable energy solutions.

The next frontier is the monetization of carbon credits. While regenerative agriculture enhances the soil's capacity to retain carbon, the difficulty lies in proving "additionality" and "permanence" to international verifiers. Startups are developing specialized tools to measure soil health and carbon sequestration accurately, which could generate a "green premium" for Brazilian products in global markets. By 2025, the Brazilian government committed to reducing greenhouse gas emissions by 37%, a target that is driving investment in solar-powered machinery and precision farming tools.

Conclusion

The transformation of the Brazilian agriculture industry by AgriTech startups is a testament to the nation's ability to innovate under the pressure of tropical complexity. From the industrialization of beneficial bacteria to the deployment of AI-powered drones and the digitization of agricultural credit, these startups are rebuilding the "rails of finance" and the "logic of production" for the global food system. The future of the Brazil AgriTech market is robust, with an expected market size of USD 1.56 billion by 2034 and a continued focus on sustainability and efficiency. However, for this potential to be fully realized, the industry must address the systemic logistical bottlenecks, bridge the rural digital divide, and ensure that the benefits of technology reach both the soybean giants of Mato Grosso and the smallholder farmers of the Northeast. As Brazil moves toward 2030, it is not merely producing more food; it is exporting the very technological and sustainable models that will define the future of global agriculture.

Protect Your Future: The Precision Vesting Calculator

Don't let a "handshake deal" complicate your exit. Map out your ownership journey with our Vesting Calculator

Calculate Your Vesting Schedule →