How Much Equity Should a Technical Co-Founder Really Get?

June 28, 2026 by Harshit Gupta

The determination of equity allocation for a technical co-founder is among the most consequential decisions in the lifecycle of a nascent technology venture. This allocation serves as more than a mere financial division; it is a declaration of the venture’s internal values, a mechanism for long-term incentive alignment, and a primary signal to the institutional investment community regarding the team’s maturity and stability. In the contemporary market of 2025 and 2026, characterized by a massive influx of capital into agentic artificial intelligence, robotics, and deep tech, the frameworks for equity distribution have shifted away from arbitrary heuristics toward rigorous, contribution-based methodologies. This report examines the multi-dimensional factors influencing these allocations, the evolving market benchmarks across global hubs, and the legal and tax structures that define the actual value of a founder's stake.

The Paradigm Shift in Founder Ownership Models

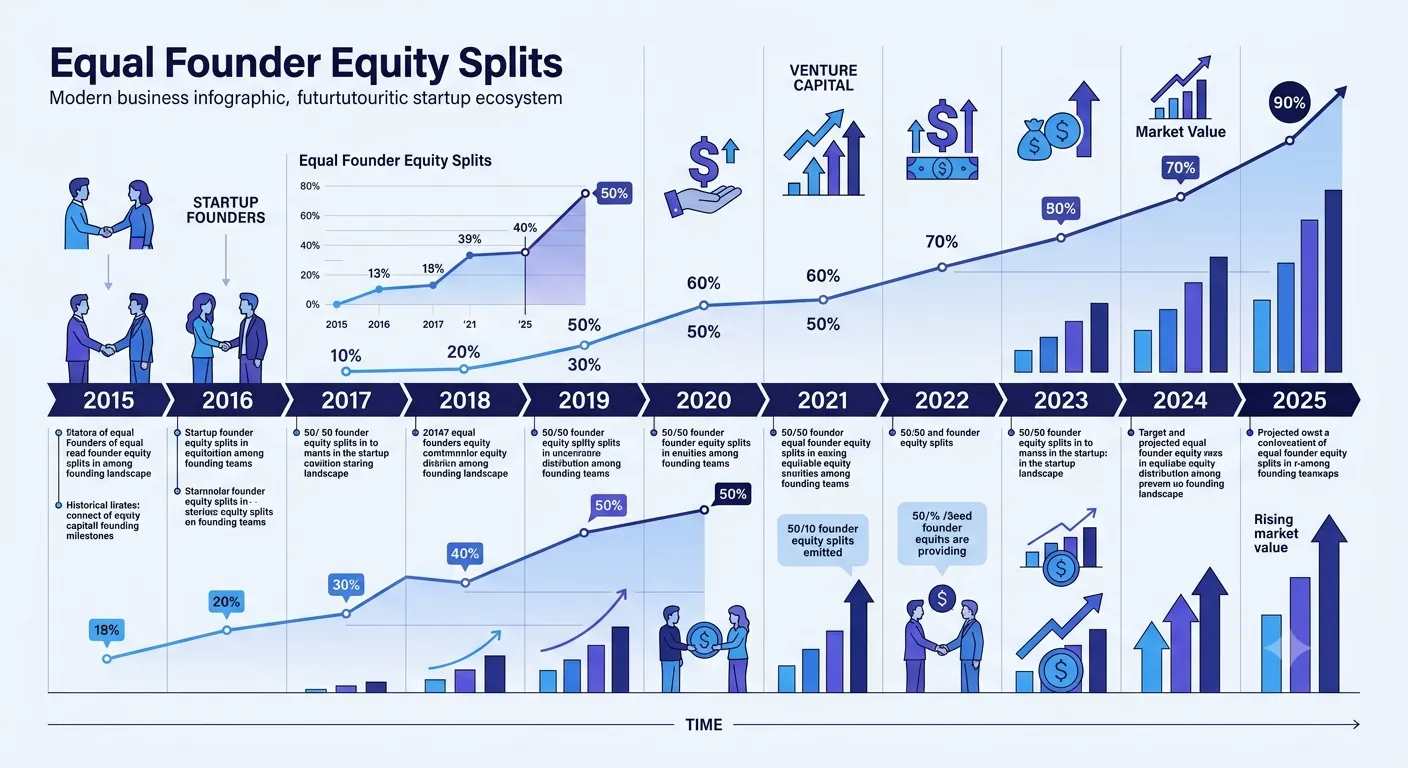

The historical landscape of startup equity was often defined by the "senior" and "junior" founder dynamic, where the originator of the business idea retained a vast majority of the equity while the technical lead was treated as a secondary participant. However, longitudinal data from 2015 to 2024 indicates a decisive movement toward equity parity. In 2015, only 31.5% of two-person founding teams opted for an equal 50/50 split. By early 2024, this figure climbed to 45.9%, and current 2025 projections suggest that equal or near-equal splits have become the modal structure for high-growth startups. This shift is rooted in the realization that the primary value of equity is not to reward the "past idea" but to incentivize the next five to ten years of relentless execution.

Year of Incorporation | 2-Person Team Equal Split (%) | 3-Person Team Equal Split (%) | Median Primary Founder Stake (3-Person) |

2015 | 31.5% | 12.1% | 50% |

2018 | 36.2% | 15.5% | 48% |

2021 | 41.8% | 20.4% | 46% |

2024 | 45.9% | 26.9% | 44% |

2025 (Est.) | 47.5% | 28.5% | 42% |

This narrowing gap reflects a systemic professionalization of the founding process. Modern founders increasingly view the "idea" as a commodity, while viewing the technical ability to build, iterate, and scale a product as the scarcest resource. Furthermore, institutional investors, including Y Combinator and major venture firms, have begun to view unequal splits—specifically those where a technical co-founder holds less than 10%—as a significant red flag. Such a low allocation often suggests that the technical lead is an employee in founder’s clothing, lacking the "skin in the game" necessary to endure the volatility of a startup lifecycle.

Core Determinants of Equity Allocation

The specific percentage of equity a technical co-founder "should" receive is a function of risk, timing, and the specific nature of the technical challenge. The market distinguishes between the "idea stage" where risk is absolute and the "post-revenue stage" where some market validation has already occurred.

Timing and the Risk-Value Continuum

When a technical founder joins a project after the non-technical founder has already built a prototype, secured customers, or raised capital, the "equity price" for the newcomer naturally increases. The non-technical founder has effectively "de-risked" a portion of the venture, justifying a larger share of the remaining pie. Conversely, if both founders quit their jobs on the same day to pursue a blank slate, any split other than 50/50 is difficult to justify from a partnership perspective.

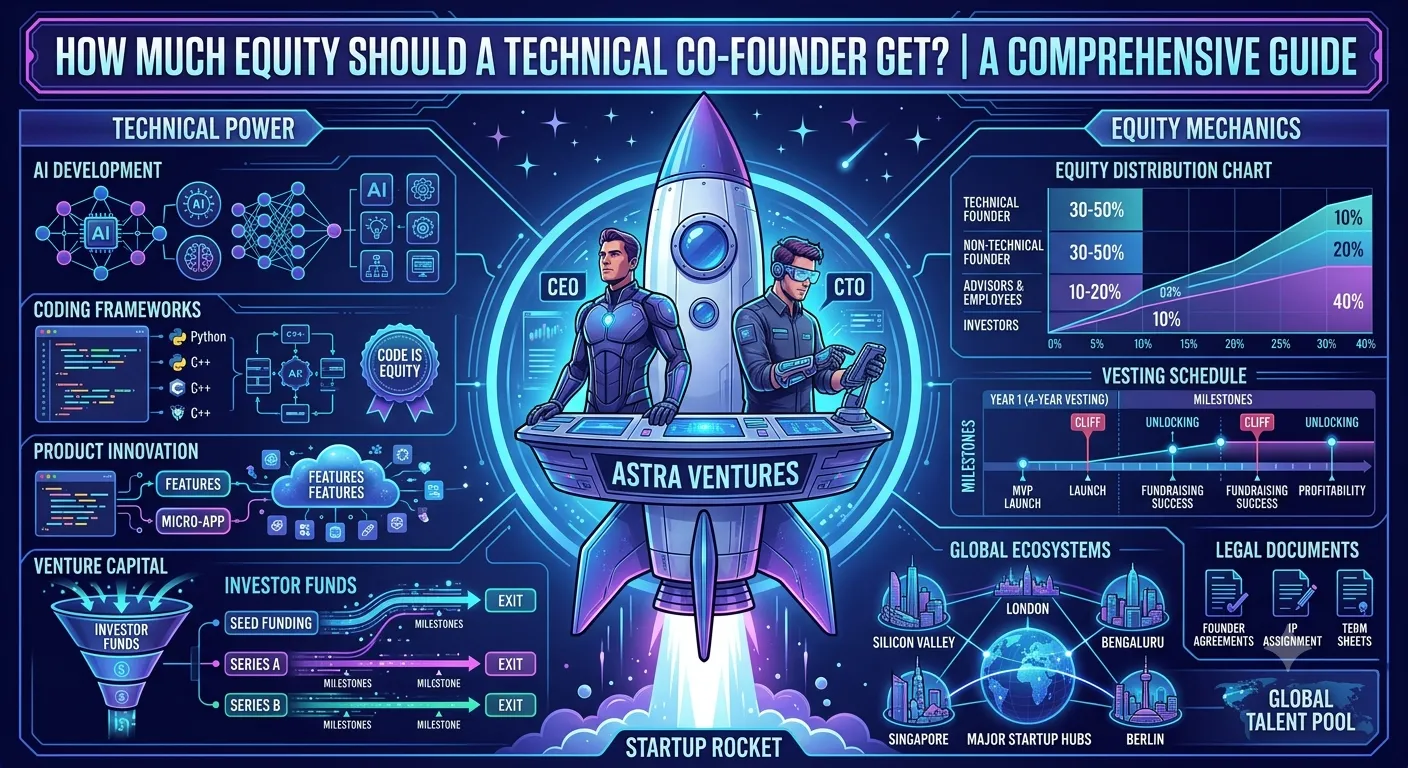

Company Stage at Entry | Risk Profile | Technical Co-Founder Range | Reasoning |

Idea / Pre-Product | Maximum | 40% – 50% | Equal risk, equal future commitment |

Validated MVP (No Revenue) | High | 25% – 35% | Concept proven; build risk remains |

Early Revenue (1k-10k MRR) | Moderate | 15% – 25% | Market fit signals; scaling risk |

Post-Seed Funding | Low | 10% – 15% | Funded runway; execution focus |

Post-Series A | Very Low | 2% – 7% | Hiring CTO vs. Founding CTO |

The 2025 data from Y Combinator batches underscores this tiered reality. Founders entering the accelerator often find that their pre-money valuations are heavily influenced by the presence of a "complete" founding team. A solo non-technical founder is often at a disadvantage, as they lack the internal capacity for rapid iteration, a deficit that can lead to premature equity dilution if they are forced to hire external agencies or dev shops rather than a committed partner.

Sector-Specific Premiums: The AI and Deep Tech Mandate

The 2025–2026 investment cycle is dominated by agentic AI and specialized vertical applications. In these sectors, the "technical" work is not merely a support function for a business model; the technology is the business model. Consequently, technical co-founders in AI command a distinct premium. Analysis of seed-stage valuations in late 2025 shows that AI startups attract a median pre-money valuation of 17.9 million, a 42% premium over non-AI startups.

This premium translates into the equity negotiation room. A technical co-founder capable of building proprietary large language models (LLMs) or complex robotic control systems is often given parity or a majority stake if they bring significant pre-existing intellectual property (IP) to the venture. In contrast, in a consumer marketplace or a simple SaaS utility where the primary challenge is marketing and sales, the business-side founder may retain a 55% to 60% share to reflect the dominance of the go-to-market (GTM) strategy in the company's success.

Methodological Frameworks for Distribution

Founders are increasingly moving away from "handshake deals" toward structured frameworks that attempt to quantify the value of disparate contributions. These frameworks help remove the emotional volatility from the equity discussion, providing a logical basis for the final numbers.

The Weighted Contribution Matrix

The weighted matrix approach assigns a numerical value to different categories of contribution. This recognizes that while "sweat equity" (labor) is vital, other factors such as initial capital, domain expertise, and risk tolerance also have a fair market price.

Factor | Typical Weight (%) | Evaluation Criteria |

Commitment | 30% | Full-time vs. part-time; opportunity cost of current salary |

Responsibility | 20% | CEO vs. CTO duties; decision-making authority |

Expertise | 20% | Technical skills; domain relationships; prior exits |

Idea / IP | 10% | Originality of concept; existing code/patents |

Capital | 20% | Personal cash investment; funding connections |

In this model, a technical co-founder who is working full-time from day one, bringing a decade of specialized AI experience, but who is not investing personal cash, might score 80 out of 100 on the matrix. If the business founder is also full-time and invests50,000, they might score 90. The resulting equity split would then be proportional to these scores—roughly 47% to 53%.

The Slicing Pie Model: Dynamic Equity Allocation

The Slicing Pie model, pioneered by Mike Moyer, is gaining traction among first-time founders who are uncertain about the long-term commitment of their partners. This model argues that it is impossible to predict the future, and therefore equity should be allocated dynamically based on what people actually do during the bootstrapping phase.

The model operates on "slices" of a pie. Each hour of work is valued at a fair market rate (typically doubled to reflect the risk of non-payment), and each dollar invested is valued at a higher multiplier (often 4x) to reflect the scarcity of cash.

Contribution Type | Multiplier | Strategic Rationale |

Cash (Out-of-pocket) | 4x | Hardest resource to obtain; provides immediate runway |

Non-Cash (Time) | 2x | High risk of zero payout; rewards the "sweat" |

Equipment/Supplies | 2x | Tangible value added; avoids company debt |

Relationships/Intros | 1x-2x | Strategic leverage to accelerate GTM |

This dynamic model is particularly effective at preventing "dead equity"—the scenario where a founder leaves the company after six months but retains 50% of the shares. In the Slicing Pie framework, the moment a founder stops contributing, they stop earning slices, and their percentage of the total pie begins to dilute as the remaining founders continue to work. Once the company raises a "priced round" (e.g., a Series A), the pie "freezes," and the current percentages are locked into the official cap table.

Legal Mechanisms: Vesting, Cliffs, and Governance

A percentage of equity is essentially meaningless without the legal structure that governs its issuance and retention. In the 2025 venture landscape, sophisticated investors view the lack of a formal vesting schedule as a catastrophic failure of governance.

The Industry Standard Vesting Schedule

Vesting ensures that a founder earns their equity over a period of service, typically four years. This protects the company and the other founders from a situation where a partner departs early but remains a major shareholder.

The "One-Year Cliff" is a critical component of this structure. Under a cliff, no shares vest until the founder has completed a full twelve months of service. On the first anniversary, 25% of the total equity vests instantly. The remaining 75% then vests in equal monthly increments (1/48th of the total grant per month) for the following three years. If a technical co-founder is terminated or resigns before the cliff, they leave with 0% equity, allowing the company to redistribute those shares to a replacement.

Reverse Vesting and Repurchase Rights

For founders who are issued shares at incorporation, the concept of "reverse vesting" is utilized. The founder legally owns 100% of their shares from day one, giving them immediate voting and dividend rights. However, the company holds a "right of repurchase." If the founder leaves early, the company can buy back the unvested portion of the shares at a nominal price (e.g., 0.001 per share). This structure is favored for tax reasons and to align founder interests with long-term company growth.

Governance and the "Tie-Breaking" Vote

Equity is not only about financial upside; it is about control. In an equal 50/50 split, there is a risk of governance deadlock where the two founders cannot agree on a critical path, such as a pivot or a funding round. To avoid this, founders often use one of several governance tools:

The 51/49 Split: This creates a clear hierarchy for decision-making while keeping the financial outcomes nearly identical. Typically, the CEO holds the 51% share to facilitate rapid operational decisions.

Board Structures: Founding documents can stipulate that while equity is 50/50, the board of directors (which may include a third neutral party) has the final say on strategic disputes.

Veto Rights: A technical co-founder may have 40% equity but maintain veto rights over specific "technical" matters, such as the sale of IP or changes to the product roadmap.

Regional Analysis: India's Startup Ecosystem in 2025

The Indian venture capital landscape in 2025 has matured significantly, with Bengaluru and Mumbai emerging as dominant hubs for AI and Deep Tech. The "secular India growth story" has driven PE/VC investments to historical highs, with a 37% month-on-month increase in early 2025. For founders in this region, the equity discussion is heavily influenced by the Companies Act, 2013, and the unique tax incentives provided by the DPIIT (Department for Promotion of Industry and Internal Trade).

The Sweat Equity Framework in India

In the Indian context, "sweat equity" refers to shares issued at a discount or for non-cash consideration in exchange for know-how or intellectual property. The regulatory framework for these shares is stricter than in the US, requiring independent valuations by registered valuers.

Regulation Category | Standard Limit | DPIIT-Recognized Startup Limit |

Annual Issuance Cap | 15% of paid-up capital | 15% of paid-up capital |

Lifetime Issuance Cap | 25% of paid-up capital | 50% of paid-up capital |

Lock-in Period | 3 years | 3 years |

Company Age Requirement | 1 year post-incorporation | No minimum (under certain rules) |

The relaxation of the lifetime cap to 50% for DPIIT-recognized startups is a massive boon for technical co-founders. It allows them to earn a significant majority of the company without the immediate need for a cash infusion, provided they can demonstrate "value addition" through their technical expertise.

Perquisite Tax and the Deferral Mechanism

One of the most complex aspects of Indian founder equity is the perquisite tax under Section 17(2)(vi). When shares are allotted to a founder at a discount, the difference between the Fair Market Value (FMV) and the price paid is taxed as "salary income" (a perquisite).

In 2025, Rule 3D introduced a gross income threshold of ₹8 lakh for this taxability. If a founder's total income is below ₹8 lakh, sweat equity shares may not attract immediate perquisite tax. However, for most high-skilled technical founders, the income will exceed this threshold. To address the liquidity crisis this creates (paying tax on non-liquid shares), the government provides a "tax deferral" for eligible startups under Section 80-IAC. This allows the tax to be postponed until the founder sells the shares, leaves the company, or after 48 months from the assessment year—whichever is earliest.

Market Salaries and Equity Compression

The rise of the "Indian Global IT Powerhouse" has created a high-salary floor for technical talent. In 2024–2025, senior engineers with 6 years of experience frequently command base salaries of ₹60–70 LPA (Lakhs Per Annum). When a founder transitions from such a role to a startup, the equity negotiation often pivots on how much of this salary is being "sacrificed."

Founder Profile | Cash Compensation | Equity Expectation |

Equity-First Founder | ₹0 - ₹12 LPA | 35% – 50% |

Balanced Founder | ₹20 LPA - ₹40 LPA | 15% – 25% |

Salary-First Lead | ₹50 LPA+ | 5% – 10% |

Data suggests that "founding engineers" (the first 1-3 hires) typically receive around 1% equity, whereas a "founding CTO" who takes a massive pay cut expects a double-digit slice.

Regional Analysis: The United States and the 83(b) Election

The US startup market remains the global benchmark for equity structures, particularly regarding the tax optimization of founder shares. For a technical co-founder in a Delaware C-Corp, the Section 83(b) election is the single most critical legal filing.

The Mechanism of Section 83(b)

Under standard IRS rules (Section 83(a)), a founder is taxed on the value of their shares as they vest. If a founder receives 1,000,000 shares that vest over 4 years, and the company’s valuation grows from1 million to 100 million during that time, the founder will owe ordinary income tax on the value of the shares at each vesting milestone. This creates a "tax nightmare" where the founder owes millions in taxes on shares they cannot yet sell for cash.

An 83(b) election allows the founder to "accelerate" their tax obligation to the date of the grant. Because the value of the company at the very beginning is nominal (often0.0001 per share), the founder pays tax on a negligible amount.

Filing Timeline | Tax Rate | Future Implication |

Within 30 Days | Ordinary Income at Grant | Capital gains on all future appreciation |

Missed Deadline | Ordinary Income at Vesting | Massive tax bills at high valuations; no liquidity |

This election "locks in" the tax basis. Any subsequent growth in the company's value is then treated as a "capital gain" rather than "ordinary income," resulting in significantly lower tax rates (typically 20% vs. up to 37% or more). Institutional investors conduct rigorous due diligence on 83(b) filings, as a missing election can create a "ticking time bomb" of tax liability for the company's primary leaders.

The Investor Perspective: Cap Table Health and Equilibrium

Venture capitalists do not seek to maximize their own equity at the expense of the founders; rather, they seek a "healthy" cap table that can withstand multiple rounds of dilution while keeping the core team motivated.

The Standard Dilution Lifecycle

Founders must understand that their initial percentage is not what they will own at exit. Each funding round typically dilutes the existing shareholders by 10% to 25%.

Funding Stage | Median Valuation (YC 2025) | Founder Dilution per Round | Combined Founder Stake |

Pre-Seed / Formation | 5M -10M | 0% | 100% |

Seed Round | 15M -25M | 15% – 20% | 75% – 85% |

Series A | 50M -100M | 20% – 25% | 55% – 65% |

Series B | 250M+ | 15% – 20% | 40% – 50% |

By the time a company reaches a Series B round, the median founding team collectively owns 23% to 36% of the company. If two founders start with a 50/50 split, they may each own 10% to 15% at the growth stage. If the technical co-founder started with only 10%, they might own less than 2% by Series B—a level that VCs worry is insufficient to keep a highly-skilled CTO from being "poached" by a larger competitor or a new startup.

The Pre-Money Option Pool Requirement

A common negotiation point with investors is the "Option Pool Shuffle." Investors usually require that the company create an Employee Stock Option Pool (ESOP) of 10% to 15% before the investment is made. This means the dilution from the option pool is borne entirely by the founders, not the new investor. Technical founders should be aware of this "hidden" dilution and factor it into their initial split discussions.

Negotiation Strategy: Balancing the Technical and Business Leads

The negotiation between co-founders is the first major test of the company's culture. A technical co-founder should approach the discussion with a focus on their "replacement cost" and "strategic necessity," while a business founder should focus on "de-risking" and "fundability".

The Case for the Technical Founder

In 2026, a technical co-founder’s leverage is at an all-time high due to the complexity of the current tech stack. A business founder with a "good idea" for an AI startup is effectively powerless without a lead who can architect the data infrastructure and fine-tune models. The technical lead should emphasize:

Architecture Debt: The cost of rebuilding a "v1" built by an agency is often higher than building it correctly from scratch.

Hiring Magnetism: A strong technical founder is the primary factor in attracting top-tier engineering talent, which is the company's most expensive and critical resource.

R&D Risk: The technical lead carries the burden of proving that the product is even possible to build, a risk that is significantly higher in Deep Tech than in traditional SaaS.

The Case for the Business Founder

Conversely, the non-technical founder often carries the "rejection risk." They are the ones pitching to 100 investors to get one "yes," cold-calling customers, and managing the legal and administrative "grunge work" that allows the technical founder to focus on code. They should emphasize:

Market Validation: Evidence of paying customers or a waitlist of 10,000 users significantly increases the company's valuation and reduces the technical founder's risk.

Capital Access: If the business founder has a track record of raising millions from top-tier VCs, they are providing a "funded runway" that is far more valuable than a speculative idea.

Strategic Moats: Building a sales engine or a brand can often be a more durable moat than software, which can be replicated by a well-funded competitor.

Conclusion: Synthesizing the 2026 Equity Standard

The consensus among market participants, data providers, and legal experts is that the "fair" amount of equity for a technical co-founder is increasingly moving toward parity. The 2025–2026 era of startups requires a level of technical sophistication that makes the CTO a true peer to the CEO.

For founders initiating this journey, the following strategic principles should guide the final agreement:

Prioritize Future Commitment Over Past Idea: Equity should be viewed as a tool to lock in the next decade of a technical leader's life. Any split that feels "stingy" is a threat to the venture's longevity.

Institutionalize Fairness Through Vesting: Regardless of the split, use a four-year vesting schedule with a one-year cliff. This provides the ultimate "safety valve" for all parties.

Optimize for Tax Early: In the US, file the 83(b) election within 30 days. In India, seek DPIIT recognition and 80-IAC certification to defer perquisite taxes.

Adopt a Tiered Benchmark: Use 40%–50% for idea-stage co-founders, 20%–30% for post-MVP co-founders, and 5%–15% for post-funding technical leaders.

Focus on "Equitable" Rather Than "Equal": If one founder provides100k in cash and the other provides only labor, a 50/50 split is not equitable. Use a weighted matrix or the Slicing Pie model to account for these tangible differences.

By treating equity as a strategic instrument rather than an emotional prize, founding teams can build the foundation of trust and alignment necessary to navigate the complexities of the global technology market in the years to come.

Protect Your Future: The Precision Vesting Calculator

Don't let a "handshake deal" complicate your exit. Map out your ownership journey with our Vesting Calculator

Calculate Your Vesting Schedule →