Funding Freeze: Are VCs Quietly Pulling Out Because of Global Conflicts?

March 21, 2026 by Harshit Gupta

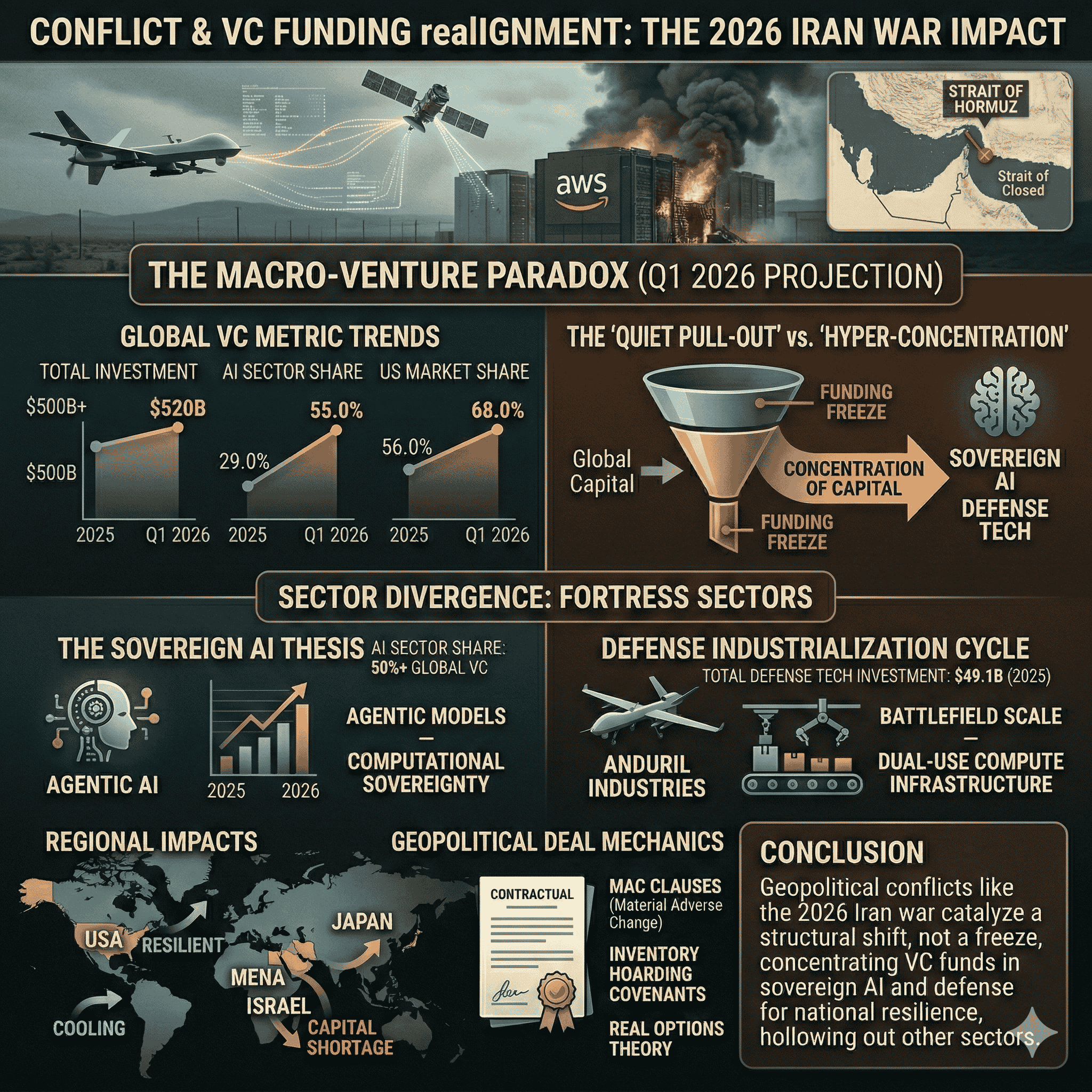

The global venture capital ecosystem in the first quarter of 2026 is currently navigating a period of profound structural transformation, characterized not by a wholesale withdrawal of capital, but by a sophisticated realignment of assets in response to escalating kinetic conflicts and a fracturing international order. While the headline narrative often suggests a "funding freeze" driven by global instability, a granular analysis of deployment data from 2025 and early 2026 reveals a more nuanced reality of hyper-concentration. Total global venture investment actually surged to over $500 billion in 2025, up from $391.9 billion in 2024, yet this liquidity has become increasingly siloed within "fortress sectors" and "geopolitically aligned" geographies. The 2026 Iran war and the subsequent closure of the Strait of Hormuz have acted as the definitive catalysts for this shift, forcing a transition from the "efficiency-first" model of the last decade to a "resilience-first" paradigm that prioritizes sovereign capabilities, defense industrialization, and domestic energy security.

The Macro-Venture Paradox: Concentration Amidst Volatility

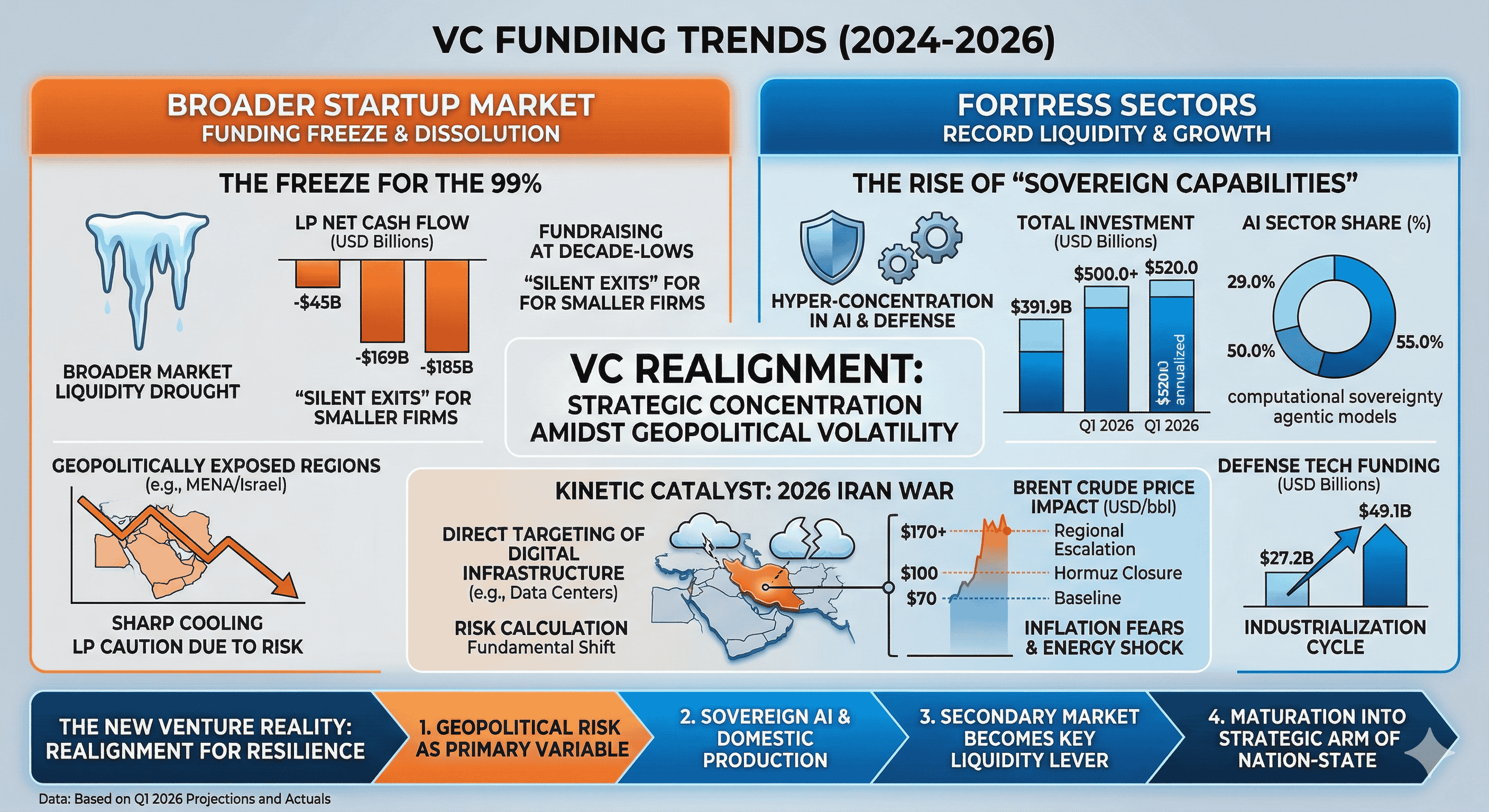

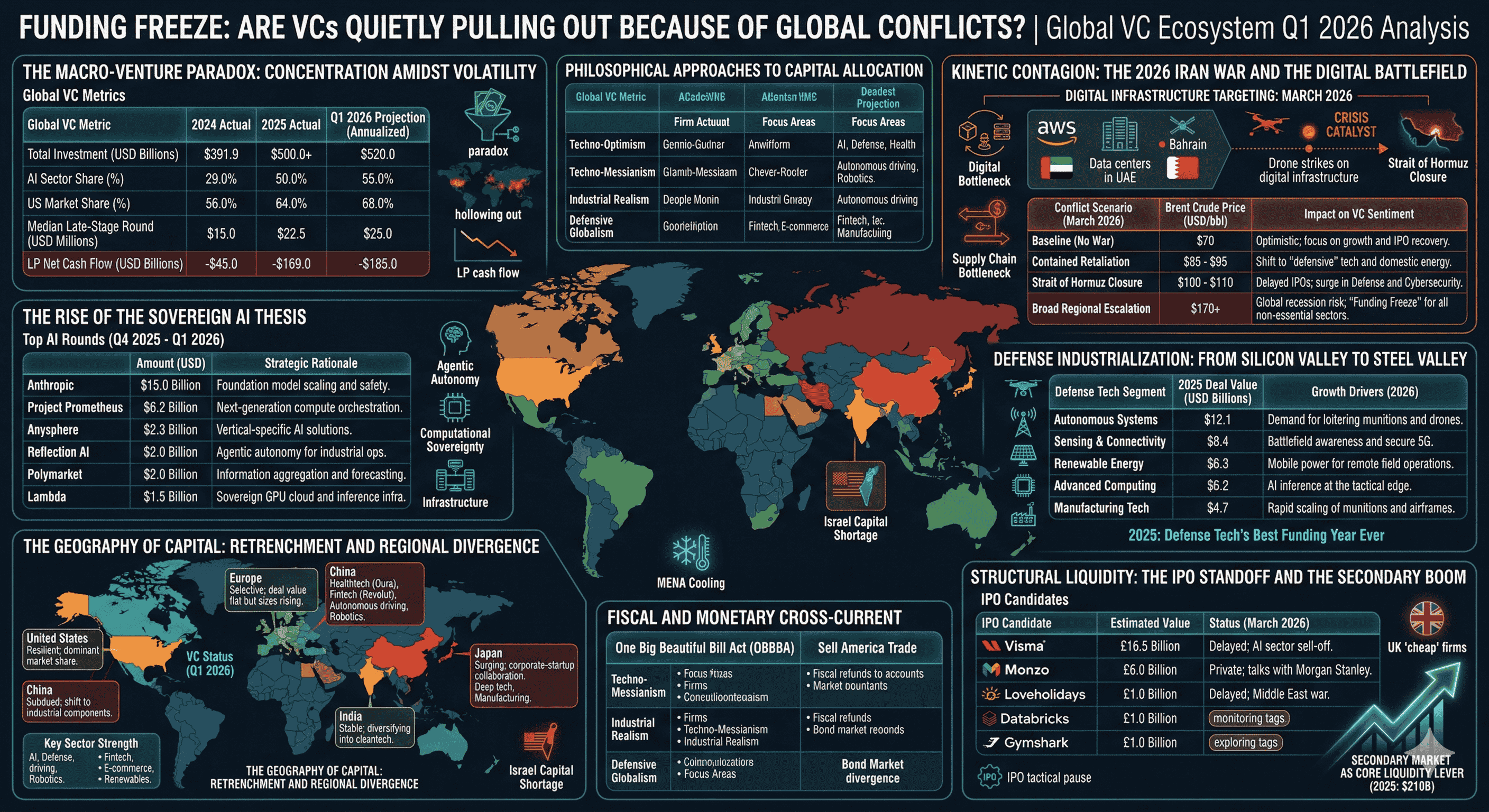

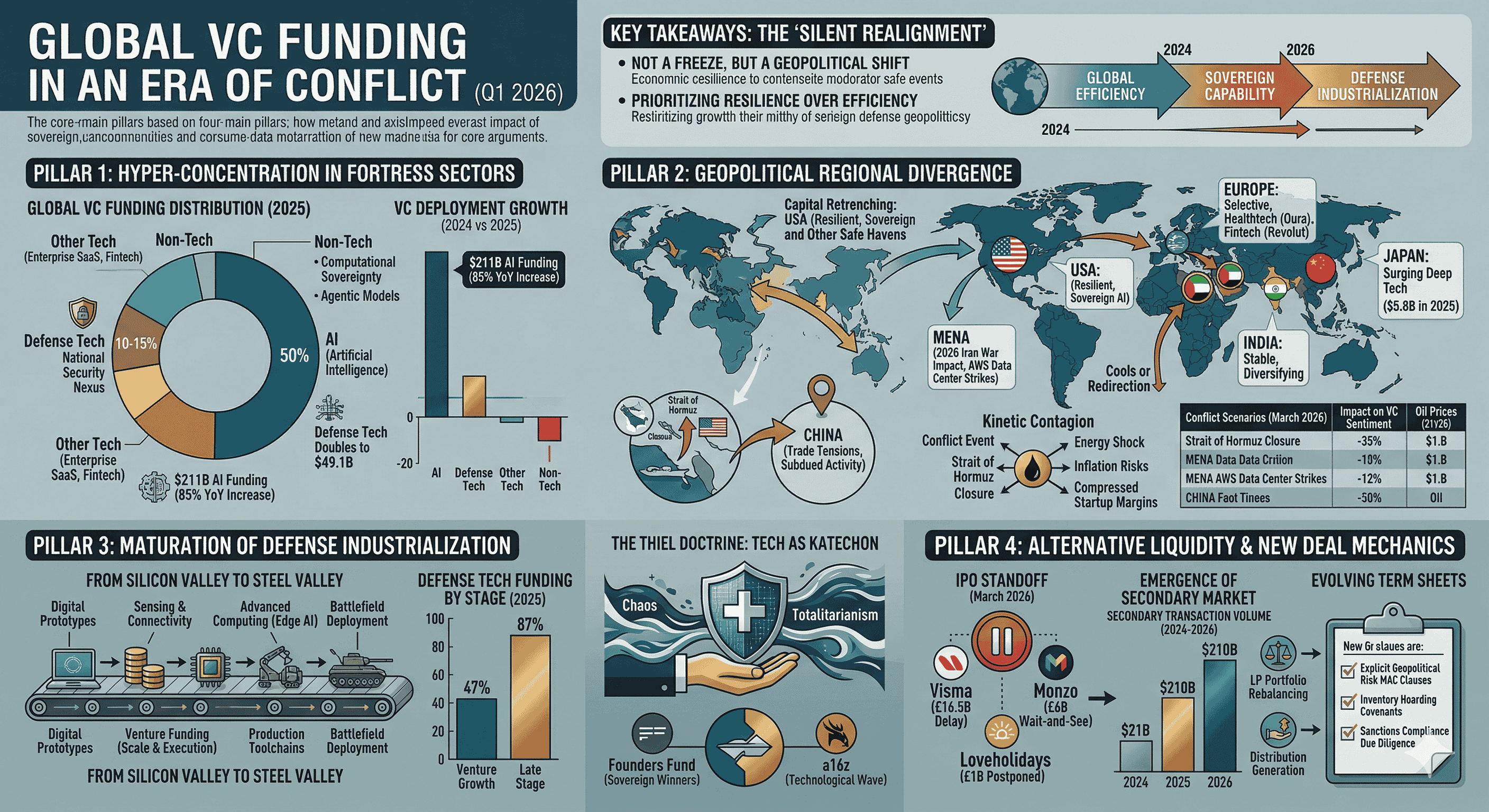

The current investment landscape is defined by a central paradox: record-breaking capital density in elite technology sectors coexists with a severe liquidity drought for the broader startup market. In 2025, the industry witnessed a significant recovery in total deal value, which reached its highest levels in 14 quarters by the end of the year. However, this growth was driven by a shrinking number of high-value transactions. In the United States, roughly 50% of the total deal value in 2025 was concentrated in just 0.05% of completed deals, reflecting a market where venture capitalists are consolidating their bets behind a handful of "category kings" capable of surviving a prolonged era of fragmentation.

This concentration is most visible in the artificial intelligence sector, which captured approximately 50% of all global venture funding in 2025, reaching a total of $211 billion—an 85% increase from the previous year. The underlying driver of this trend is the emergence of AI as a foundational national capability rather than a mere enterprise software category. As the global order divides into competing blocs, the race for "computational sovereignty" has made AI infrastructure and agentic models the primary recipients of risk capital.

Global VC Metric | 2024 Actual | 2025 Actual | Q1 2026 Projection (Annualized) |

Total Investment (USD Billions) | $391.9 | $500.0+ | $520.0 |

AI Sector Share (%) | 29.0% | 50.0% | 55.0% |

US Market Share (%) | 56.0% | 64.0% | 68.0% |

Median Late-Stage Round (USD Millions) | $15.0 | $22.5 | $25.0 |

LP Net Cash Flow (USD Billions) | -$45.0 | -$169.0 | -$185.0 |

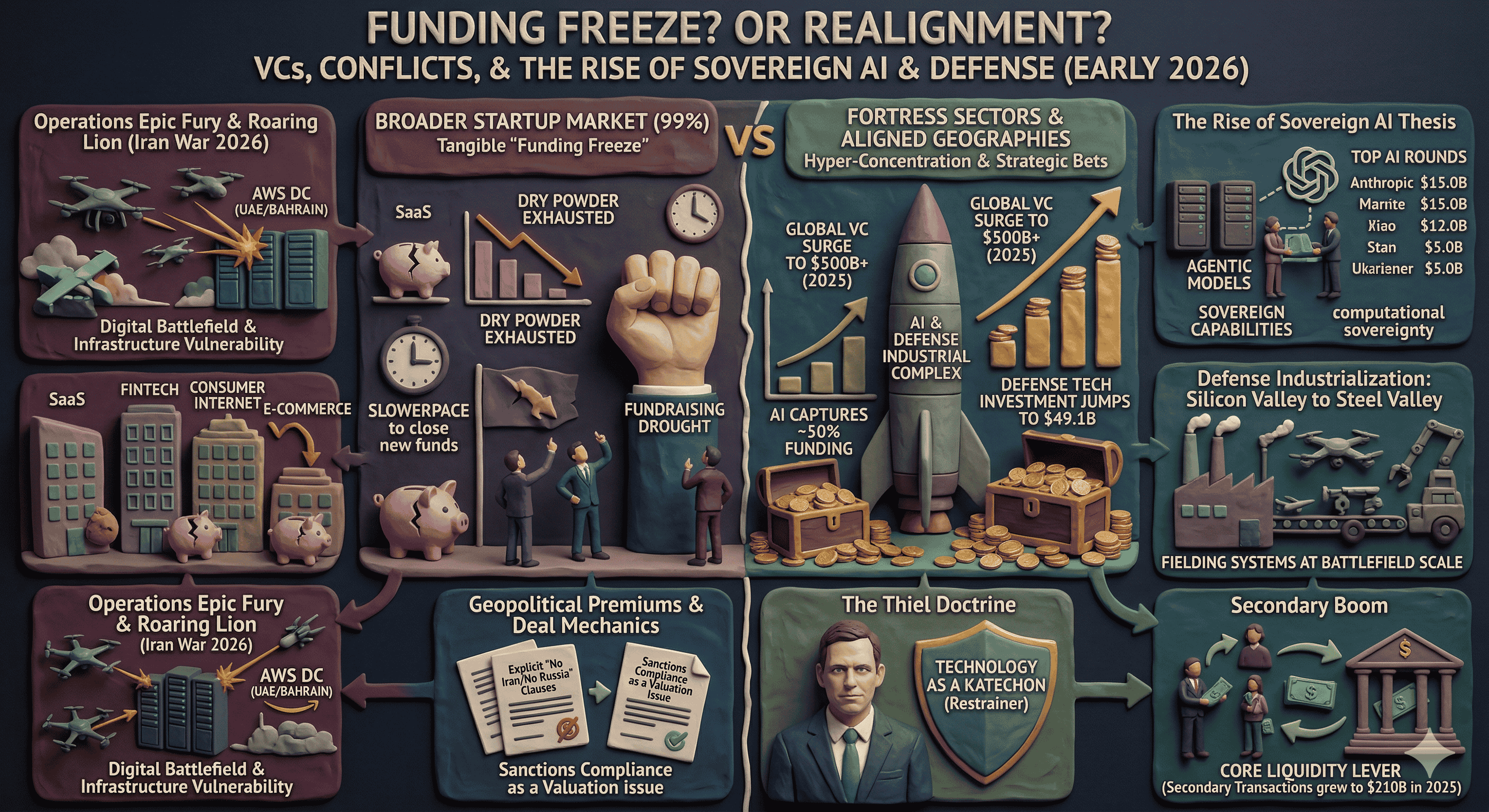

The data confirms that for the 99% of startups outside the AI and defense industrial complex, the "funding freeze" is a tangible reality. Fundraising for new venture funds fell to its slowest pace in a decade in 2025, as Limited Partners (LPs) grappled with negative net cash flows. The time required to close new funds has increased sharply, and many emerging managers who raised capital during the 2021 boom have exhausted their "dry powder" without the ability to secure successor vehicles. This has created a "silent exit" for hundreds of smaller firms, leaving the market increasingly dominated by "mega-funds" with the balance sheets to dictate terms in a volatile environment.

Kinetic Contagion: The 2026 Iran War and the Digital Battlefield

The outbreak of hostilities in the Middle East in early 2026, designated by U.S.-Israeli forces as Operations Epic Fury and Roaring Lion, has fundamentally altered the risk-reward calculus for international venture capital. Unlike previous conflicts that were largely contained to energy markets, the 2026 Iran war has seen the direct targeting of the physical infrastructure of the global digital economy. On March 1, 2026, Iranian drone strikes directly hit two Amazon Web Services (AWS) data centers in the United Arab Emirates and one facility in Bahrain, causing widespread disruption to regional banking, payment systems, and consumer products.

This shift in targeting strategy highlights the vulnerability of the "globalized" cloud model. Gulf nations had invested billions to position themselves as neutral hubs for AI and data processing, attracting giants like Microsoft, Google, and Nvidia. The 2026 strikes have shattered this reputation for safety, prompting a rapid retrenchment of capital back to the United States and other "safe-haven" jurisdictions. The "dual-use" nature of these data centers—which host both civilian and military workloads—has made them legitimate targets under certain interpretations of international law, creating an insurance nightmare for the hyperscalers and their venture-backed tenants.

Conflict Scenario (March 2026) | Brent Crude Price (USD/bbl) | Impact on VC Sentiment |

Baseline (No War) | $70 | Optimistic; focus on growth and IPO recovery. |

Contained Retaliation | $85 - $95 | Shift to "defensive" tech and domestic energy. |

Strait of Hormuz Closure | $100 - $110 | Delayed IPOs; surge in Defense and Cybersecurity. |

Broad Regional Escalation | $170+ | Global recession risk; "Funding Freeze" for all non-essential sectors. |

The effective closure of the Strait of Hormuz, through which 20% of the world's oil flows, has pushed Brent crude prices to $110 per barrel, reigniting inflation fears that had only recently subsided. This energy shock has a direct causal link to the venture "freeze": rising input costs and supply chain bottlenecks are compressing the margins of hardware and logistics startups, while the resulting upward pressure on interest rates has caused the Federal Reserve to reconsider its rate-cutting cycle. For venture-backed firms, this means the "cost of waiting" for an exit has increased significantly, leading to a wave of opportunistic, buyer-friendly M&A and down-round refinancings.

The Rise of the Sovereign AI Thesis

In the current environment, AI is no longer viewed as a cyclical thematic trade but as a long-term platform shift that is inseparable from national security. Through the third quarter of 2025, AI startups accounted for 65% of all venture deal value, and more than half of the year's new unicorns were AI-native companies. This concentration reflects a strategic belief among the world’s most powerful venture firms—including Founders Fund and Andreessen Horowitz—that dominance in AI is the ultimate hedge against geopolitical instability.

The focus of AI investment in 2026 has pivoted from broad-based Large Language Models (LLMs) toward the "agentic space" and "AI-enabled infrastructure". Agentic models, which are projected to reach human-level performance in complex task execution by the spring of 2026, are seen as the key to maintaining industrial productivity in the face of labor shortages and fractured supply chains. This technological evolution has sparked a massive surge in infrastructure spending; large U.S. tech companies are expected to triple their annual capital investment to over $500 billion by 2026 to support the power and cooling requirements of advanced data centers.

Top AI Rounds (Q4 2025 - Q1 2026) | Amount (USD) | Strategic Rationale |

Anthropic | $15.0 Billion | Foundation model scaling and safety. |

Project Prometheus | $6.2 Billion | Next-generation compute orchestration. |

Anysphere | $2.3 Billion | Vertical-specific AI solutions. |

Reflection AI | $2.0 Billion | Agentic autonomy for industrial ops. |

Polymarket | $2.0 Billion | Information aggregation and forecasting. |

Lambda | $1.5 Billion | Sovereign GPU cloud and inference infra. |

This "AI super-cycle" is creating a "hollowing out" effect in other sectors. Venture dollars are being diverted from consumer internet, enterprise SaaS, and fintech to fund the massive "picks and shovels" of the AI boom, including specialized chips, high-performance data centers, and advanced power management solutions. For firms outside this core AI-defense nexus, the "funding freeze" is an unavoidable consequence of capital being reallocated toward assets with "civilization-level" strategic value.

Defense Industrialization: From Silicon Valley to Steel Valley

The year 2025 was the best funding year ever for defense technology startups, with total investment jumping to $49.1 billion, nearly doubling the $27.2 billion recorded in 2024. This shift marks the transition of defense tech from an exploratory "innovation cycle" to a high-scale "industrialization cycle". In 2026, venture capitalists are no longer just funding prototypes for the Pentagon; they are financing the production toolchains, robotics, and software-augmented manufacturing facilities required to field systems at "battlefield scale".

This maturation of the sector is driven by the realization that allied militaries are increasingly dependent on commercial technology for autonomous systems, sensing, and connectivity. In 2025, venture growth and late-stage VC captured 87% of the capital deployed in defense tech, highlighting a move toward scaled execution. Significant liquidity events, such as Nvidia’s $20 billion licensing and asset deal with Groq, have proven that "dual-use" compute infrastructure can drive massive realized value for early investors.

Defense Tech Segment | 2025 Deal Value (USD Billions) | Growth Drivers (2026) |

Autonomous Systems | $12.1 | Demand for loitering munitions and drones. |

Sensing & Connectivity | $8.4 | Battlefield awareness and secure 5G. |

Renewable Energy | $6.3 | Mobile power for remote field operations. |

Advanced Computing | $6.2 | AI inference at the tactical edge. |

Manufacturing Tech | $4.7 | Rapid scaling of munitions and airframes. |

The narrative around defense investing has undergone a total transformation. Mainstream venture capitalists have largely dropped their previous ethical objections, reframing defense technology as a way to support "democratic values" and "sovereign resilience". Firms like Founders Fund have been at the forefront of this shift, successfully raising a new $6 billion "Growth IV" fund to back "civilization-level companies" like SpaceX, Palantir, and Anduril. These companies are being designed as part of the national foundational infrastructure, capable of structuralizing competition and controlling key nodes of security and intelligence.

The Geography of Capital: Retrenchment and Regional Divergence

The "funding freeze" is highly localized, following the fault lines of the current geopolitical conflicts. The Middle East and North Africa (MENA) region, which saw a 95% surge in startup investment in 2025, has faced a sharp cooling in early 2026 as the Iran war threatens its path to recovery. Approximately 20% of MENA venture deals in the previous year featured participation from U.S. investors; this cross-border appetite has plummeted as firms prioritize "geopolitical distance" from the conflict.

In Israel, the venture landscape has been severely impacted by the dual pressures of regional war and a fundraising drought. Israeli funds hit a new low in 2025, struggling to secure fresh capital as international LPs balk at the country’s heightened risk profile. This has resulted in a capital shortage for early-stage startups that have not yet reached "mega-deal" status in AI or cybersecurity. In response, domestic players have launched "emergency funds" to provide a lifeline to firms cut off from foreign capital.

Region | VC Status (Q1 2026) | Key Sector Strength |

United States | Resilient; dominant market share. | AI, Defense, Healthtech. |

Europe | Selective; deal value flat but sizes rising. | Healthtech (Oura), Fintech (Revolut). |

China | Subdued; shift to industrial components. | Autonomous driving, Robotics. |

India | Stable; diversifying into cleantech. | Fintech, E-commerce, Renewables. |

Japan | Surging; corporate-startup collaboration. | Deep tech, Manufacturing. |

Asia presents a different story. While China’s broader venture activity remains hampered by trade tensions and U.S. tariffs, investment is surging in "aligned" markets like Japan, India, and Australia. Japan’s annual VC total reached a near-record $5.8 billion in 2025, while Australia has become a critical hub for AI infrastructure and "dual-use" data centers. This "Ex-America" trade reflects a broader diversification flow as investors seek growth outside of the concentrated U.S. large-cap technology sector.

Structural Liquidity: The IPO Standoff and the Secondary Boom

The exit environment for venture-backed companies in 2026 is defined by "measured optimism" clashing with "extreme volatility." In the fourth quarter of 2025, the IPO window appeared to be opening, with high-profile debuts in the U.S. and India suggesting a return to liquidity. However, the March 2026 military strikes have forced a "tactical pause" for many firms preparing to go public.

In the United Kingdom, the London Stock Exchange (LSE) has seen several major listings delayed. Loveholidays, a £1 billion travel agency float, was postponed specifically due to the Middle East conflict’s impact on travel sentiment. Similarly, the Norwegian software giant Visma has delayed its £16.5 billion float, and the fintech leader Monzo remains in a "wait-and-see" mode despite reaching a £6 billion private valuation. This "hollowing out" effect has made UK firms appear "cheap" to foreign buyers, leading to a record £65 billion in foreign takeovers of UK companies last year.

IPO Candidate | Estimated Value | Status (March 2026) |

Visma | £16.5 Billion | Delayed; AI sector sell-off. |

Monzo | £6.0 Billion | Private; talks with Morgan Stanley. |

Loveholidays | £1.0 Billion | Delayed; Middle East war. |

Databricks | TBD | Monitoring US market volatility. |

Gymshark | TBD | Exploring LSE vs. Nasdaq. |

As traditional exits through IPOs and M&A face regulatory and geopolitical hurdles, the secondary market has emerged as the "core liquidity lever" for the entire ecosystem. Secondary transactions, which grew to $210 billion in 2025, are projected to reach even higher levels in 2026. LPs are increasingly turning to secondaries to rebalance their portfolios and generate the distributions necessary to commit to new venture funds. This normalization of secondary liquidity is favoring "early movers" and primary investors who can offer exit optionality to their founders and early employees.

Deal Mechanics in an Era of Conflict: MAC Clauses and Geopolitical Premiums

The 2026 investment environment has forced a radical evolution in deal structuring. The "standard" term sheet of the last decade is being rewritten to include "geopolitical risk" as a primary variable. The 2026 Iran conflict has highlighted the fact that traditional "Material Adverse Change" (MAC) clauses offer little protection against the broad economic fallout of a regional war.

Buyers and VCs are now demanding "Real Options Theory" approaches to valuation—treating investments as deferrable decisions and demanding "robust contractual protections" that include:

Explicit "No Iran/No Russia" Clauses: Due diligence now extends to mapping beneficial ownership webs and tracing supply chain exposure to shadow fleets and high-risk transshipment hubs.

Inventory Hoarding Covenants: Targets are being encouraged to "front-run" anticipated supply chain disruptions by hoarding inventory, a practice that would have been penalized as "working capital inefficiency" in previous cycles.

Sanctions Compliance as a Valuation Issue: Sanctions are no longer a "back-office formality" but a core factor in determining the cost of equity for any company with meaningful exposure to conflict-prone regions.

The "valuation gap" between sellers anchored to 2025 multiples and buyers pricing in 2026 risks has made earn-outs and milestone-based financing mainstream. For impact-focused funds, this has translated into "impact covenants" that legally bind organizations to specific carbon reduction or social outcomes as a condition of continued support.

The Thiel Doctrine: Technology as a Biblical Restrainer

A significant and often overlooked driver of the current venture realignment is the philosophical shift among key Silicon Valley leaders. Peter Thiel, a co-founder of Palantir and Founders Fund, has articulated a vision of technology as a "katechon"—a biblical restrainer intended to hold back chaos or the emergence of a "one-world totalitarian state". Thiel’s 2026 private lectures in Rome examine the concept of the "Antichrist" as a metaphor for a globalized order that sacrifices individual freedom for the sake of a "false peace".

This "techno-messianism" has direct implications for capital allocation. Founders Fund’s strategy of concentrating capital in a very small number of "civilization-level winners" is a bet on companies that can structurally reduce competition and control key nodes of national infrastructure. While other firms like Andreessen Horowitz (a16z) bet on the "technological wave itself" across crypto, biotech, and enterprise software, the "Thiel Doctrine" focuses on creating monopolies that can directly embed themselves into the security and intelligence apparatus of the state.

Philosophical Approach | Firm Example | Primary Investment Focus |

Techno-Optimism | a16z | Broad-based expansion; decentralized tech. |

Techno-Messianism | Founders Fund | Concentration in "Sovereign" winners. |

Industrial Realism | General Catalyst | Scale, manufacturing, and healthcare infra. |

Defensive Globalism | SoftBank (2025 context) | Market share and international scaling. |

This ideological grounding has made these firms the "preferred partners" for the Pentagon and other Western security agencies. The proximity of venture partners to policymakers and the rotation of senior officials into advisory boards have created a "revolving door" that ensures venture-backed defense startups are at the front of the line for record national security spending, which reached $901 billion in the United States for the 2026 fiscal year.

Fiscal and Monetary Cross-Currents: The OBBBA and the "Sell America" Trade

The venture capital environment is further complicated by the domestic policy agenda in the United States. The "One Big Beautiful Bill Act" (OBBBA), which took effect in early 2026, includes retroactive personal income tax cuts that are expected to provide U.S. households with $80 billion in refunds in the first quarter alone. This massive fiscal impulse is likely to support consumer spending and retail trading activity, providing a short-term "tail-wind" for consumer-facing tech and retail brokerage platforms.

However, this fiscal stimulus is occurring just as the Federal Reserve is undergoing a leadership transition and facing intense political pressure to cut rates despite persistent inflation risks. The appointment of a new Fed chair in May 2026 is viewed as a "critical inflection point" for bond market volatility and the strength of the U.S. dollar.

This has given rise to the "Sell America" trade, where investors move global in bonds and equities to hedge against a potential exodus from U.S. assets. Interestingly, while the Iran war initially boosted the dollar on "safe-haven" demand, U.S. Treasuries have not seen a corresponding surge, as investors fear that higher energy prices and massive fiscal deficits will drive long-term yields higher. This "divergence" between the currency and the bond market is a hallmark of the new, more fragile risk landscape of 2026.

Conclusions: Navigating the New Frontier of Risk

The 2026 "funding freeze" is not a sign of venture capital's decline, but of its maturation into a strategic arm of the modern nation-state. The "quiet pull-out" from global conflicts is, in fact, a loud realignment toward assets that can survive and thrive in a world of persistent kinetic and digital warfare.

For professional allocators and founders, several key takeaways emerge from this transition. First, the era of the "globalized startup" is over; "sovereignty" is now the most valuable feature a company can possess. Whether it is a sovereign AI stack, a domestic defense production line, or a resilient energy storage solution, the market is disproportionately rewarding companies that reduce a nation’s dependence on geopolitically distant partners.

Second, liquidity is becoming a "structured" rather than a "public" phenomenon. The rise of secondaries and the dominance of private credit suggest that the most successful venture-backed companies will stay private longer, utilizing private capital to fund their growth while waiting for the "geopolitical risk premium" in public markets to subside.

Finally, the 2026 Iran war has proven that the "digital battlefield" is real. The targeting of commercial data centers marks a point of no return for the industry. Investors must now incorporate physical security, insurance backstops, and redundant infrastructure into their core due diligence. The venture capitalists who succeed in this era will not be those who avoided the conflicts, but those who anticipated them and built the "katechons" of the digital age.

Want to calculate the equity for your cofounder?

Nail your cap table before you sign. Whether you're splitting equity with a co-founder or planning your next funding round, our Equity Calculator gives you precision in seconds

Equity calculator →