Should Canadian Startups Focus on Global Markets From Day One?

March 13, 2026 by Harshit Gupta

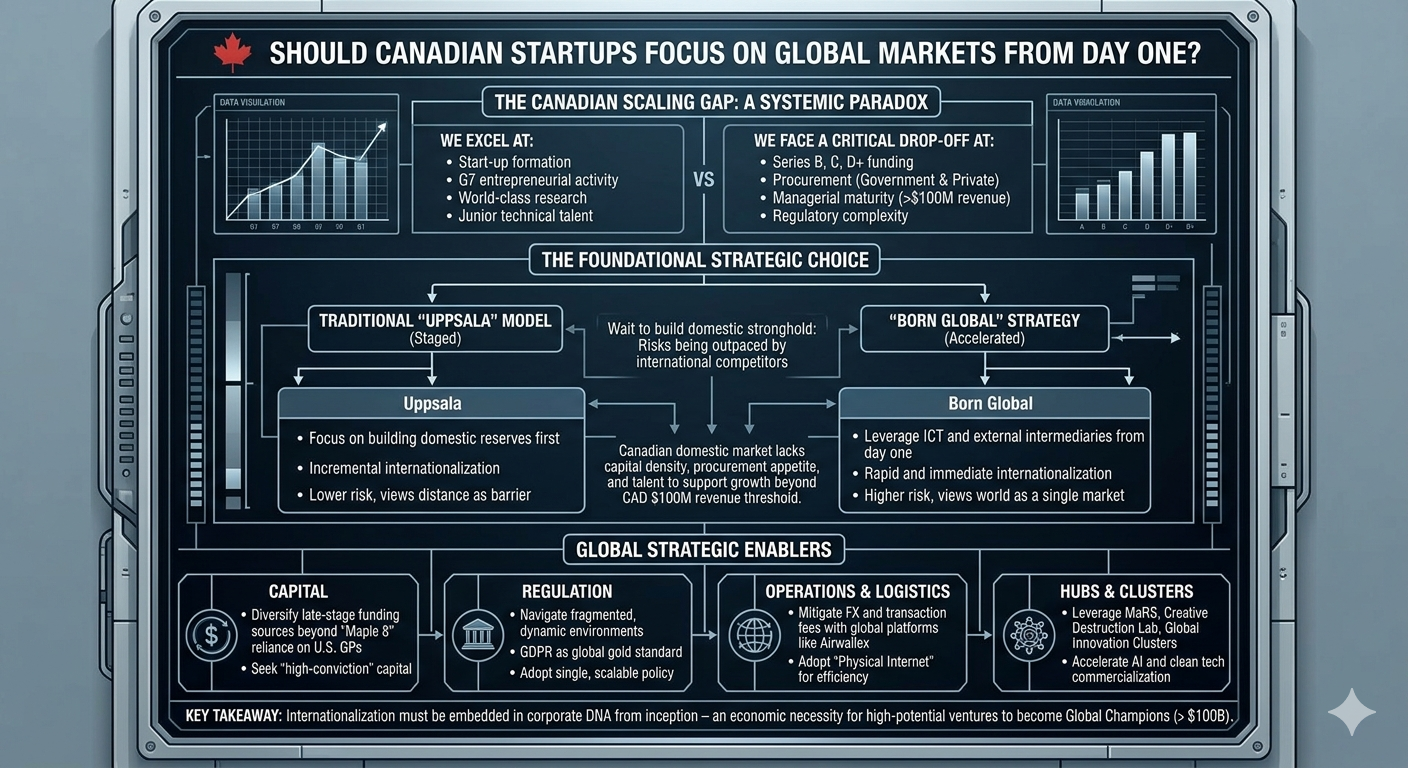

The Canadian innovation ecosystem is currently defined by a profound structural contradiction. While Canada consistently produces world-class research and maintains the highest level of early-stage entrepreneurial activity among G7 nations, it faces a systemic "scaling gap" that prevents domestic startups from maturing into global anchor firms. The central strategic inquiry—whether Canadian startups should focus on global markets from day one—is no longer a matter of preference but an economic necessity dictated by the limitations of the domestic market. For high-potential ventures, particularly in knowledge-intensive sectors like artificial intelligence, biotechnology, and clean energy, the Canadian domestic market lacks the requisite capital density, procurement appetite, and specialized talent to support growth beyond a $\text{CAD } \$100 \text{ million}$ revenue threshold.

The transition toward a "Born Global" strategy is a fundamental survival mechanism for firms aiming to achieve enterprise values exceeding $\$1 \text{ billion}$, $\$10 \text{ billion}$, or $\$100 \text{ billion}$. Failing to scale these companies domestically means high-value intellectual property, talent, and wealth flow to foreign platforms instead of anchoring a robust domestic innovation ecosystem. Consequently, the decision to internationalize must be embedded in the corporate DNA from inception, as firms that wait to build a "domestic stronghold" often find themselves outpaced by international competitors who achieve global scale and network effects more rapidly.

The Canadian Scaling Paradox: Structural Barriers to Domestic Growth

Canada does not have a "start-up problem"; it has a "global scale-up problem". The national ecosystem excels at early-stage venture formation but hits a definitive wall as companies attempt to grow past $\$100 \text{ million}$ in revenue. At this juncture, the system frequently abandons them, leading to a "scaling gap" characterized by a critical drop-off in support during Series B, C, and D+ funding rounds. This gap is not merely a financial deficit but a multifaceted failure involving capital formation, procurement, talent maturity, and infrastructure.

The Capital Formation Deficit and the "Maple 8" Externality

A primary barrier to scaling within Canada is the chronic lack of late-stage domestic capital. Today, Canada does not have sufficient capital formation to support its scale-ups, leading to a structural reliance on foreign, primarily U.S.-based, investors for growth rounds. This creates a situation where many Canadian scale-ups are starved for capital or are forced to raise smaller rounds at lower valuations than their U.S. counterparts, thereby reducing their ability to pursue ambitious plans or take necessary risks.

Paradoxically, Canada possesses some of the world's largest pools of capital in the "Maple 8" pension funds, such as the Canada Pension Plan Investment Board (CPPIB), the Ontario Municipal Employees Retirement System (OMERS), and the Caisse de dépôt et placement du Québec (CDPQ). However, these sophisticated funds often exhibit a reluctance to invest directly in Canadian scale-ups. For instance, the CPPIB frequently requires a U.S. lead investor (General Partner) to participate before they will consider a round in a domestic firm. This reliance on foreign validation means that the future of Canadian innovation often depends on a U.S. investor's judgment, an externality that complicates the domestic growth trajectory.

Funding Stage | Canadian Reality | U.S. Tier-1 Ecosystem Comparison |

Pre-Seed & Seed | Highest G7 activity but missing $\sim\$141\text{M}$ annually | Robust deal flow; larger check sizes |

Series A | Canadian seed rounds are consistently 37% to 40% smaller than those in top-tier U.S. cities. | Faster transition to Series B |

Series B, C, D+ | "Crippling deficit" of domestic capital | Capital concentration in high-conviction mega-deals |

Late Stage (Scale-up) | Reliance on U.S. GPs for lead status | Domestic GPs lead global rounds |

The lack of early-stage capital significantly hinders the ability to scale, as smaller seed rounds lead to slower growth and pipeline attrition. Between 2019 and 2024, Canada’s top-tier ecosystems in Toronto-Waterloo, Montréal, and Vancouver lost an estimated $\$66 \text{ billion USD}$ in ecosystem value, measured by their declining market share of global startup funding and exits.

The Procurement Gap and the Absence of Anchor Contracts

A secondary structural challenge is the "procurement weakness" of both the Canadian government and the private sector. Canadian entities are less likely to buy emerging technology from domestic scale-ups than their foreign counterparts. Many founders report that they are forced to win their first enterprise contracts in the United States before any Canadian enterprise or government agency will consider purchasing their solution.

This lack of "anchor contracts" at home prevents startups from achieving the early revenue and product validation necessary for global expansion. Canada currently ranks near the bottom of the OECD for government procurement from domestic innovative firms, and business R&D spending as a percentage of GDP (0.9%) remains significantly lower than the OECD average of 2% and the 4% seen in leading nations like Korea. Without a "Buy Red" culture—similar to the "Buy Blue" mindset in Israel—Canadian companies lack the domestic foundation required to reach the several million dollars in Annual Recurring Revenue (ARR) needed to raise significant capital abroad thereafter.

The Managerial Maturity and Talent Gap

While Canada produces an abundance of general-purpose junior technical talent, there is a distinct shortage of senior leadership (VP-level and above) with experience in scaling companies from $\$100 \text{ million}$ to $\$1 \text{ billion}$ and beyond. This "managerial know-how" is the missing ingredient for many young firms. To address this, many high-potential founders gained critical experience working for foreign multinational tech companies (MNCs) like Google, Microsoft, and Ericsson, which serve as training grounds for global skills, networks, and perspectives.

A review of 300 Canadian tech startup founders found that 41% had previously worked for foreign MNCs in Canada. These firms provide foundational experience in global technology trends and help founders identify unfulfilled niches in wider international markets. However, once a startup reaches the scaling phase, the lack of a critical mass of domestic companies with experienced C-suite leaders often compels them to relocate their headquarters to the U.S. or other global hubs to access the talent needed for the next phase of growth.

Theoretical Frameworks: Uppsala vs. Born Global Models

The strategy of internationalization is often debated through the lens of two primary academic models: the Uppsala (staged) model and the Born Global theory. The traditional Uppsala model, originating in the 1970s, suggests that firms should focus on their domestic market first, internationalizing incrementally to markets with lower "psychic distance" (cultural and geographic proximity) as they gain experiential knowledge.

In contrast, the "Born Global" model describes firms that seek significant competitive advantage from international markets from inception. Research indicates that Internet-based firms and those in knowledge-intensive sectors are increasingly adopting the Born Global approach, as digital distribution channels significantly lower the costs and risks of immediate international involvement.

Feature | Uppsala Model (Staged) | Born Global Model (Accelerated) |

Pace | Incremental, slow, and cautious | Rapid and immediate internationalization |

Resource Usage | Focuses on building domestic reserves first | Leverages ICT and external intermediaries from day one |

Risk Tolerance | Low; based on experiential learning | Higher; views the world as a single market |

Market Entry | Focuses on "psychic proximity" | Focuses on global niches regardless of geography |

Founder Profile | Domestic focus | International outlook and prior global experience |

For Canadian startups, the Uppsala model is often unfeasible due to the "small domestic market" constraint. The market in the home country is frequently not large enough to support the scale at which the firm needs to operate to be competitive. Consequently, most high-potential Canadian tech firms fall under the "International New Venture" category, focusing on satisfy global niches from day one to achieve viability.

Sectoral Imperatives: Where Global Focus is Mandatory

The necessity of focusing on global markets from inception varies across sectors, but it is particularly acute in AI, biotechnology, agri-food, and clean technology.

The Artificial Intelligence Gravity Well

In the 2025-2026 landscape, AI has become a "gravity well," capturing nearly 50% of all global venture capital dollars. Canadian AI startups are at the forefront of this trend, with AI-native software accounting for 40% of all software funding. However, to create leading AI champions, firms require access to two critical ingredients that are often "locked" or unavailable in the domestic market: infrastructure and data.

The requirement for massive amounts of computing power (GPUs) and "AI Factories" often forces Canadian AI firms to seek partnerships and infrastructure in the U.S. or other global hubs. Furthermore, as AI moves from experimentation to operational deployment, founders must design for global governance, risk controls, and accountability to meet the expectations of enterprise customers in diverse jurisdictions.

Biotechnology: Relocation as a Consequence of Capital Gaps

Canadian biotech startups face a unique set of systemic challenges, including a lack of affordable wet lab space and a slow, expensive university tech transfer process. Because Canada lacks sufficient specialized life sciences funds to carry companies beyond the startup phase, firms are often "pushed" to look outside Canada for funding earlier than they prefer.

When these startups are forced to take international capital, they are often required to reincorporate and move their headquarters abroad, causing ownership, talent, and long-term value creation to shift away from Canada. This "cycle of loss" results in fewer Canadian-owned successes and a depletion of the leadership expertise needed to reinvest in the next generation of domestic startups.

Agri-Food: A $13-Billion Opportunity

The agri-food sector in Canada represents a major investment opportunity, yet it remains undercapitalized by domestic growth funds. The sector accounts for only 2% of federal government-backed growth and venture funds. Without an ecosystem that can propel promising companies to unicorn status (valued at $1B+), Canadian agri-food startups advance slower than international competitors. Aligning domestic growth capital with the industry's contribution to GDP would require an estimated $13 billion boost in investment by 2030.

Clean Technology and Advanced Manufacturing

In sectors like cleantech and advanced manufacturing, establish a clear path to market is challenging due to high upfront capital requirements and long timelines to prove returns. Canada offers a strategic opportunity for these innovators due to federal and provincial policies supporting decarbonization, such as the Strategic Innovation Fund (SIF) and Scientific Research and Experimental Development (SR&ED) tax incentives. However, the survival of these startups increasingly depends on securing strategic partnerships in global markets that strike a balance between stability and growth potential.

Navigating the Operational and Regulatory Complexity of Global Expansion

While the strategic mandate is global, the operational reality of international expansion involves navigating a "fragmented, dynamic, and far less forgiving" environment than the domestic market.

The GDPR and the Regulatory "Gold Standard"

Expansion into the European Union (EU) requires immediate compliance with the General Data Protection Regulation (GDPR), which has substantial global spillovers. For Canadian businesses, GDPR is more extensive than the domestic Personal Information Protection and Electronic Documents Act (PIPEDA), granting data subjects the "right to be forgotten" and the "right to object to automated decision-making".

Regulatory Aspect | PIPEDA (Canada) | GDPR (EU) |

Consent Model | Implied consent permitted in some contexts | Explicit, unambiguous consent only |

Individual Rights | Access and correction | Access, erasure, data mapping, "privacy by design" |

Max Fines | Context-dependent | Up to 4% of annual global revenue |

Extraterritoriality | Focused on domestic organizations | Applies to any firm offering goods/services to EU |

Canadian organizations that offer goods or services to EU residents must comply with GDPR regardless of physical presence. This often leads firms to update their terms and conditions to meet the most stringent global requirements to maintain a single, scalable policy across all regions. However, the economic impact of GDPR has been documented as a "harm" to firms, hurting performance by imposing costs and reducing the share of individual-level data available for marketing and personalized channels.

Asia and China: The Complexity of the "4P Strategy"

Expanding into Asian markets, particularly China, presents some of the toughest business conditions for Canadian firms. Success in these markets depends on the "4P Strategy":

Potential: Deeply understanding local consumer behavior and the target market.

Proposition: Adapting the value offering to local tastes and buying habits.

Presence: Building trust and networks through local partnerships or a physical presence.

Policy: Leveraging government programs and navigating complex regulatory frameworks.

China's regulatory environment is characterized by frequent changes, such as the 2024 revisions to Company Law and the "negative list" restricting foreign investment in sectors like telecom and education. Furthermore, cultural and communication barriers mean that business talks in Asia often last months or years, requiring Canadian firms to have a long-term outlook and significant upfront capital for licensing and compliance.

The Hidden Costs of International Money Management

Canadian SaaS companies operating globally face a "brutal" math regarding foreign exchange (FX) and transaction fees. Traditional banking FX spreads can devour 3-4% of every international transaction, potentially costing a typical startup CAD $\$2,000$ annually on just $\$50,000$ in international spend. To mitigate these costs, startups are increasingly turning to global payment platforms that offer interbank rates and multi-currency accounts, which can reduce total annual costs to as little as $\$15$.

Platform | International Transaction Fee | FX Spread | Annual Cost Estimate | |

Traditional Bank | 2.5-3% | 1 - 2% | ~ $ 2000 | |

Airwallex | 0 % | Interbank (0.1-0.3\%) | $ 15 (after rebates) | |

Wise Business | 0.35 %- 0.65 % | Mid-market | Varies | |

KOHO Extra | Varies | Market rates | Fixed monthly |

Logistics and the "Physical Internet"

Global expansion stretches supply chains across longer distances, introducing higher logistics costs and exposure to port closures or strikes. The emerging concept of the "Physical Internet"—characterized by standardized containers and shared logistics infrastructure—is gaining traction as a long-term efficiency strategy to improve asset utilization and reduce "empty miles". However, Canadian startups must still manage fragmented planning and limited coordination across trade and sustainability strategies to avoid significant cost overruns.

Strategic Enablers: Hubs, Clusters, and the "Ownership-First" Model

To facilitate the transition to global markets, Canadian startups can leverage a variety of innovation hubs and strategic frameworks.

MaRS Discovery District and Creative Destruction Lab (CDL)

MaRS is Canada's anchor innovation hub, supporting over 1,200 ventures across life sciences, cleantech, and emerging technologies. MaRS-supported companies raised over $\$11 \text{ billion}$ between 2010 and 2024, providing them with the connections to capital and talent needed for international expansion.

The Creative Destruction Lab (CDL) at the University of Toronto has expanded to 16 global locations, focusing on natural language processing, quantum computing, and AI. CDL’s objective-setting process increases the probability of success for technical founders by providing access to the experience and judgment of those who have built and scaled real companies.

The "Ownership-First" Playbook (Cosgn)

In 2026, a disruptive "ownership-first" model is emerging for Canadian startups. This model, exemplified by firms like Cosgn, allows founders to protect ownership and ship faster than funding cycles by providing execution capacity through service credits without upfront costs or equity dilution. This approach encourages founders to:

Keep control long enough to learn what is real.

Produce evidence (signed LOIs, pilots) before negotiating with VCs.

Build trust mechanics and governance into the product early.

Raise capital only when the company is ready to negotiate from a position of traction.

By anchoring in a stable jurisdiction like Canada—which offers regulatory clarity, stable banking, and framework access like CUSMA—founders can build a "globally trusted launch base" while maintaining operational flexibility through distributed teams.

Global Innovation Clusters and National Strategy

The Government of Canada has invested heavily in Global Innovation Clusters to address complex challenges that no single company can overcome alone. These clusters help SMEs de-risk innovation and expand their global presence. For instance, cluster project partners are more than twice as likely to be high-growth firms compared to the national baseline. Furthermore, the second phase of the Pan-Canadian AI Strategy (PCAIS) allocated $\$275$ million to these clusters to accelerate the commercialization and adoption of AI technologies.

Future Outlook: Building Canadian Global Champions

To solve the scaling gap, Canada must transition from being a nation of startups to a nation of "Global Champions"—firms with greater than $\$100 \text{ billion}$ in enterprise value. This requires a fundamental shift in culture, policy, and strategy.

Recommendations for a Scaling Agenda

Canadian Prosperity Fund: Create a government-backed investment fund capable of writing $\$50–500$ million checks into promising Canadian companies to address the late-stage capital deficit.

"Buy Red" Incentives: Implement tax deductibility for the purchase of Canadian technology to encourage domestic procurement and the creation of anchor contracts.

Regulatory Reform: Simplify and redesign programs like SR&ED to actually work for entrepreneurs, reducing the process burden that bogs down startups.

Cultivating Future Leaders: Deliberately invest in leadership capacity through programs that nurture builders who understand how prosperity is created and how to lead with conviction.

AI Infrastructure: Address the specific barriers in AI by providing available GPUs and "AI Factories" to enable domestic companies to build substantive models.

The Role of Foreign Multinationals

While some advocate for a "Canada-first" approach that reduces the role of foreign firms, evidence suggests that these companies are complementary and additive to the tech economy. Foreign multinationals serve as the primary training ground for the talent that eventually launches successful Canadian startups. Discriminating against these firms could dry up the very jobs that equip Canadian founders with the global skills and networks required for success.

The Resilience of "Bootstrapping"

Canadian founders often bootstrap longer and secure VC funding later than their U.S. counterparts. This contrast can be a strength, as it allows founders to retain control over their vision and strategy for a longer period, making the companies more resilient in the long run. This measured risk, combined with Canada's political and financial stability, offers a unique path forward for founders who want to build sustainable, global impact without the "growth at any cost" pressures that often lead to premature failure.

Synthesis and Conclusion

The evidence overwhelmingly indicates that Canadian startups must focus on global markets from day one to achieve long-term viability and impact. The domestic market is a valuable launchpad for ideation and early validation, but its structural limitations—fragmented capital pools, a risk-averse procurement culture, and a specialized talent shortage—render it insufficient for the scaling phase.

The successful Canadian firms of 2026 are those that have embraced the "Born Global" model, embedding international regulatory compliance and global money management strategies into their foundational operations. By leveraging domestic enablers like the Global Innovation Clusters and hubs like MaRS and CDL, while simultaneously seeking "anchor contracts" and "high-conviction" capital in the U.S. and Europe, Canadian founders can navigate the "scaling gap."

Ultimately, the transformation of the Canadian economy from one heavily weighted toward natural resources to one powered by globally competitive technology firms depends on the ability of startups to scale past the $\$100 \text{ million}$ revenue wall. Achieving this requires not just entrepreneurial ambition, but a coordinated national strategy that concentrates resources on "winners" and fosters a culture that champions and elevates its champions to the global stage. Focusing on global markets from day one is not just an option for Canadian startups; it is the definitive strategic mandate for the next generation of prosperity.