Rise of climate tech startups and green innovation

June 22, 2026 by Harshit Gupta

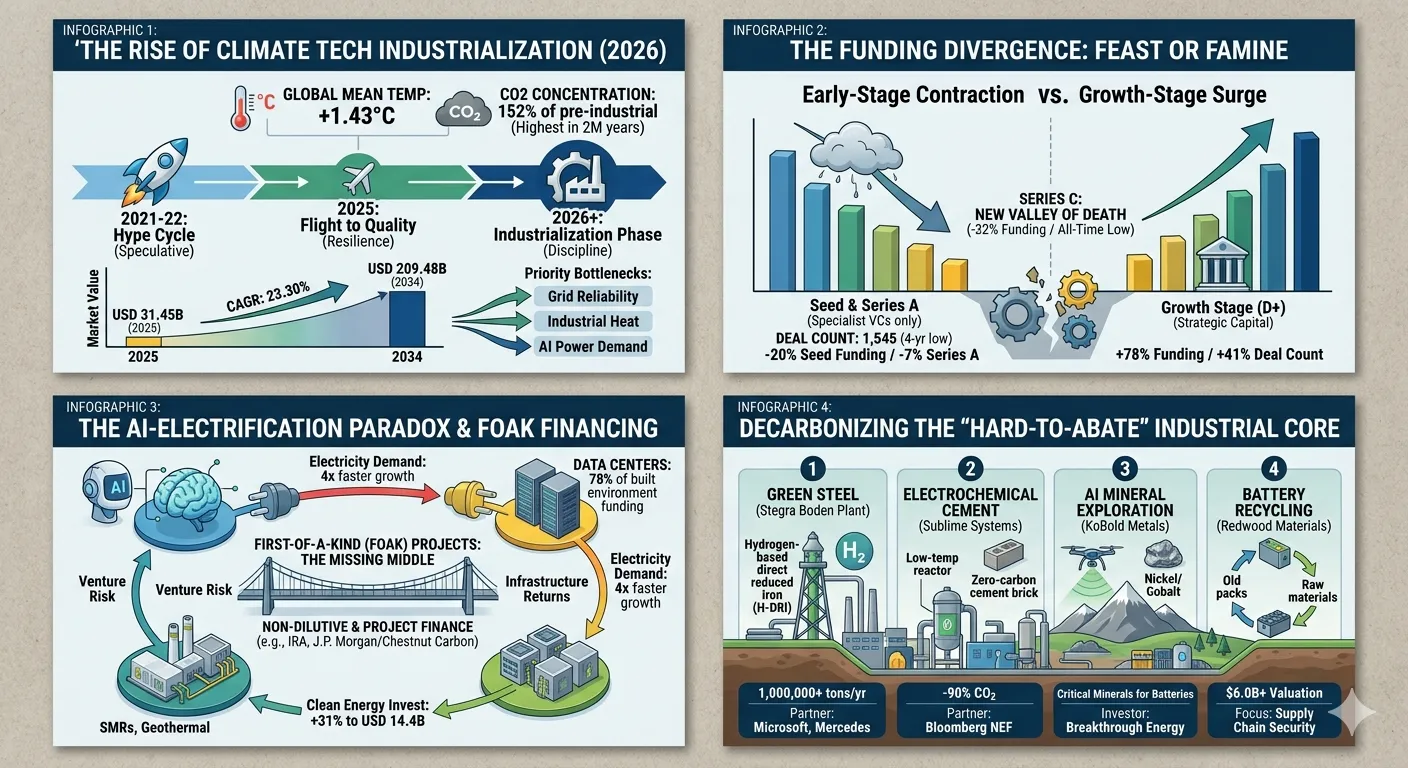

The global climate tech ecosystem in 2026 stands at a critical historical juncture, marking the end of a speculative "hype cycle" and the commencement of a disciplined "industrialization phase." As the planet grapples with an unprecedented energy imbalance—reaching its highest level in a sixty-five-year record—the urgency to scale decarbonization technologies has shifted from an environmental aspiration to a macroeconomic necessity. Global mean surface temperatures have reached approximately $1.43^{\circ}C$ above pre-industrial levels, with carbon dioxide concentrations hitting 152% of pre-industrial levels, the highest in two million years. This physical reality has forced a recalibration of the climate tech market, which was valued at USD 31.45 billion in 2025 and is projected to expand to USD 209.48 billion by 2034, exhibiting a compound annual growth rate (CAGR) of 23.30%.

The transition observed in 2025 and 2026 is defined by a "flight to quality," where capital is no longer chasing venture-scale "moonshots" but is instead anchoring itself to proven technologies that address the immediate bottlenecks of the energy transition: grid reliability, industrial heat, and the voracious power demands of artificial intelligence. This maturation is further evidenced by a structural shift in financing, where the "missing middle" between pilot projects and commercial scale is being bridged by innovative non-dilutive capital, milestone-based financing, and strategic corporate partnerships.

The Macroeconomic Evolution of Climate Capital

The climate tech investment landscape has undergone a significant structural rebalancing following the volatility of the 2021–2022 "boom years." The subsequent "bruising reset" was driven by a confluence of rising interest rates, inflationary pressures, and geopolitical instability, which saw total private market investment contract by over 50.2% year-over-year in 2023. However, by 2025, the market demonstrated "quiet resilience," with worldwide venture and growth capital rebounding to USD 40.5 billion—an 8% increase from the previous year. This stabilization, however, masks a profound divergence in capital allocation across different stages of company maturity.

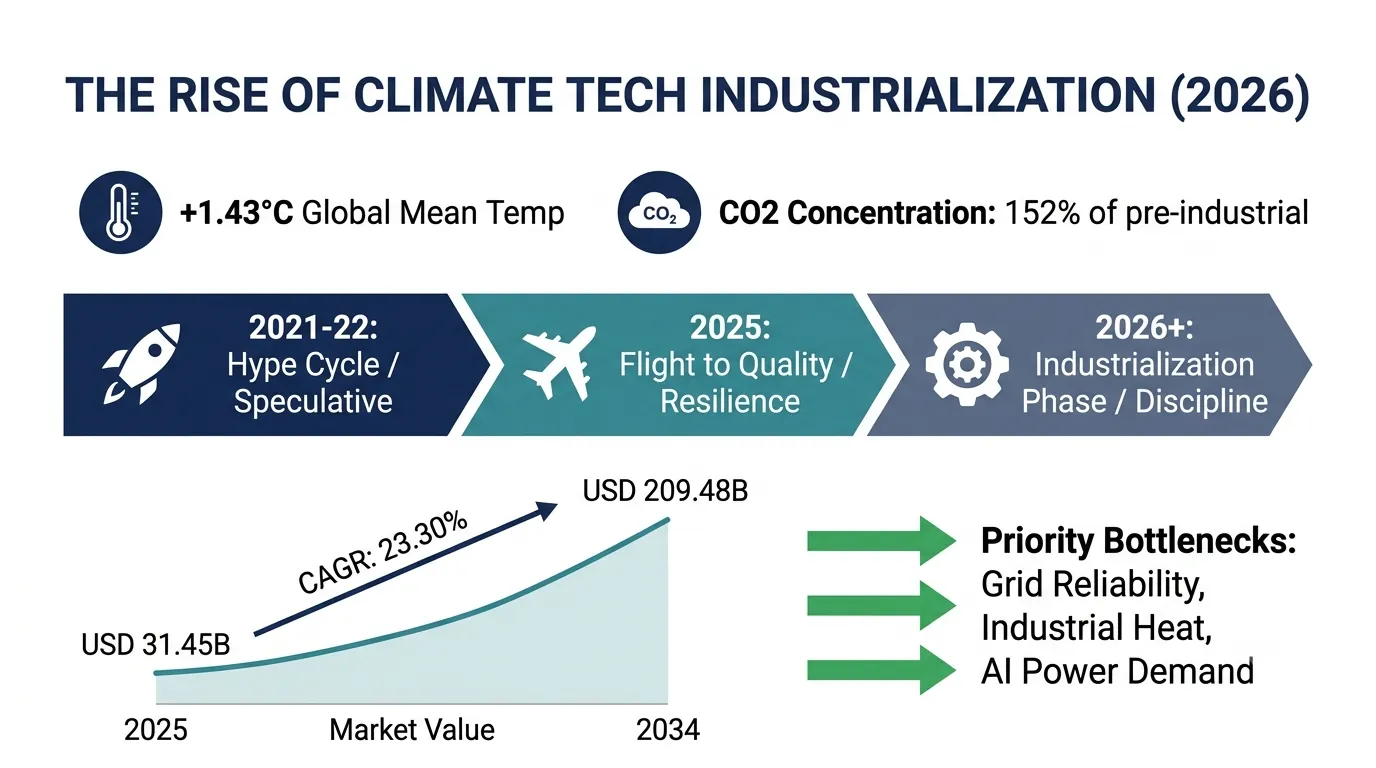

The Funding Divergence: From Seed Contraction to Growth Surge

Investment activity in 2025 and 2026 is characterized by a "feast-or-famine" dynamic. While total funding rose, the actual number of deals fell to a four-year low of 1,545, reflecting a market that is consolidating around a select cohort of category leaders. Early-stage risk appetite has markedly cooled, with Seed and Series A investment totals dropping by 20% and 7%, respectively. This contraction suggests that the "generalist" investors who entered the sector during the peak valuation years have largely exited, leaving specialist funds that are increasingly selective about new entrants.

In stark contrast, growth-stage investment (Series D and beyond) surged by 78% in 2025, as investors doubled down on companies with proven technology, viable business models, and credible paths to commercial deployment. This concentration of capital indicates that the market is now rewarding execution over experimentation. Series C has emerged as a particularly challenging "valley of death," with deal counts hitting an all-time low as companies struggle to present the rigorous performance metrics now required to unlock growth-stage capital.

Investment Stage | 2025 Funding Trend | Deal Count Change | Strategic Sentiment |

Seed | -20% | -19% | High risk aversion; focus on "proven" founders |

Series A | -7% | -22% | Larger check sizes for fewer companies |

Series B | +7% | Stable | Concentration in emerging sector winners |

Series C | -32% | All-time low | The "new valley of death" for capital-intensive hardware |

Growth (D+) | +78% | +41% | Heavy focus on industrial scale and infrastructure economics |

The Rise of Non-Dilutive and Infrastructure Finance

As climate tech startups move from laboratory prototypes to first-of-a-kind (FOAK) industrial facilities, traditional venture capital is proving insufficient for the scale of capital expenditure required. By 2025, non-dilutive funding, particularly debt, has taken center stage as the dominant form of capital for financing scalable, infrastructure-heavy solutions. This maturation of the ecosystem allows founders to build factories and project assets without excessive corporate dilution, provided they can demonstrate clear revenue models and secure offtake agreements.

Federal programs, such as those enabled by the U.S. Inflation Reduction Act (IRA) and the EU’s Net-Zero Industry Act, have become instrumental in providing milestone-based financing that helps startups bridge the gap from pilot to commercial scale. J.P. Morgan and other institutional leaders have pioneered creative financing solutions, including project financing for carbon removal initiatives like Chestnut Carbon, marking a milestone in the commercialization of the voluntary carbon market.

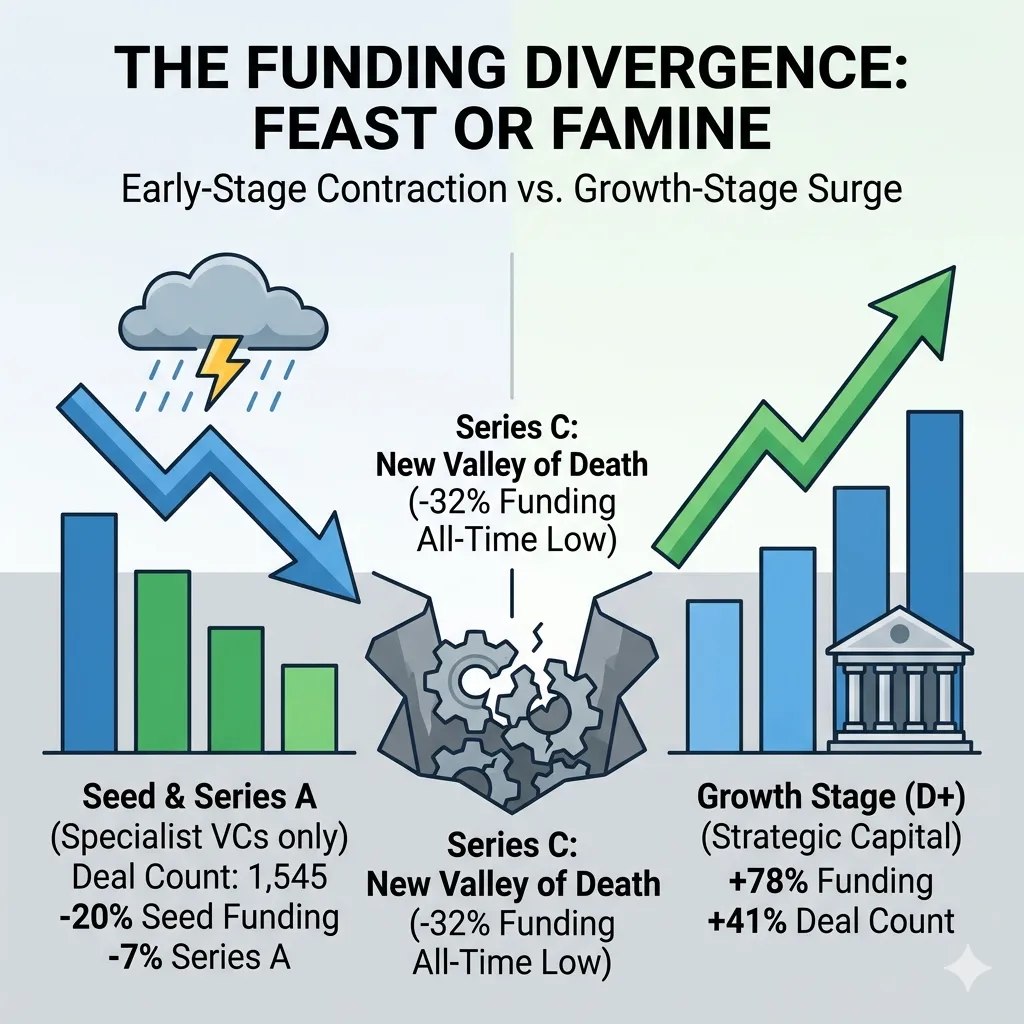

The AI-Electrification Paradox: A Dual Catalyst for Innovation

Artificial Intelligence has emerged as the defining force of climate tech in 2026, creating a unique paradox where the sector’s biggest environmental challenge has become its most powerful investment driver. The massive power requirements of generative AI and giga-scale GPU farms have placed unprecedented strain on global power grids, with data centers consuming 78% of all funding in the built environment sector in 2025.

Data Centers as "Anchor Tenants" for Clean Energy

The surge in data center electricity demand—growing four times faster than overall demand in some regions—is forcing a fundamental redesign of energy infrastructure. This "demand shock" has accelerated investment in grid-scale solutions that can deploy quickly, such as virtual power plants (VPPs) and grid-flexibility software. More importantly, AI firms are increasingly acting as "anchor tenants" for advanced baseload energy, signing massive power purchase agreements (PPAs) that enable the financing of emerging technologies like next-generation geothermal and small modular reactors (SMRs).

Investment in clean energy grew 31% to USD 14.4 billion in 2025, a three-year high driven largely by the scramble to secure reliable power for AI infrastructure. This trend has revitalized sectors that were previously slow to scale. Nuclear fission and fusion funding reached all-time highs as utilities and tech giants alike seek "firm" carbon-free power to supplement intermittent wind and solar.

Generative AI in Materials Science and Industrial Efficiency

While AI consumes vast amounts of energy, its "brain" is being utilized to solve the very problems it creates. Generative AI is revolutionizing materials science by learning the "language of matter," allowing researchers to compress a decade of materials discovery into a few months. AI models are proposal novel molecular structures for higher-capacity batteries, more efficient electrolyzers for hydrogen production, and carbon-sequestering cement.

AI Application | Mechanism of Impact | Sector Benefit |

Materials Project AI | High-fidelity computational simulations | Rapid testing of novel battery/PV compounds |

Grid Optimization | Real-time demand/supply balancing | Enhanced stability for 100% renewable grids |

Building Energy Management | HVAC optimization via digital twins | Up to 40% reduction in GHG emissions |

Predictive Maintenance | Satellite imagery & machine learning | Prevention of fires/outages in transmission lines |

In the built environment, companies like BrainBox AI are leveraging generative AI to minimize HVAC-related greenhouse gas emissions by up to 40%. Similarly, AI-powered robotic systems are transforming the circular economy, identifying and sorting recyclable materials from waste streams with over 99% accuracy, a feat impossible with human labor alone.

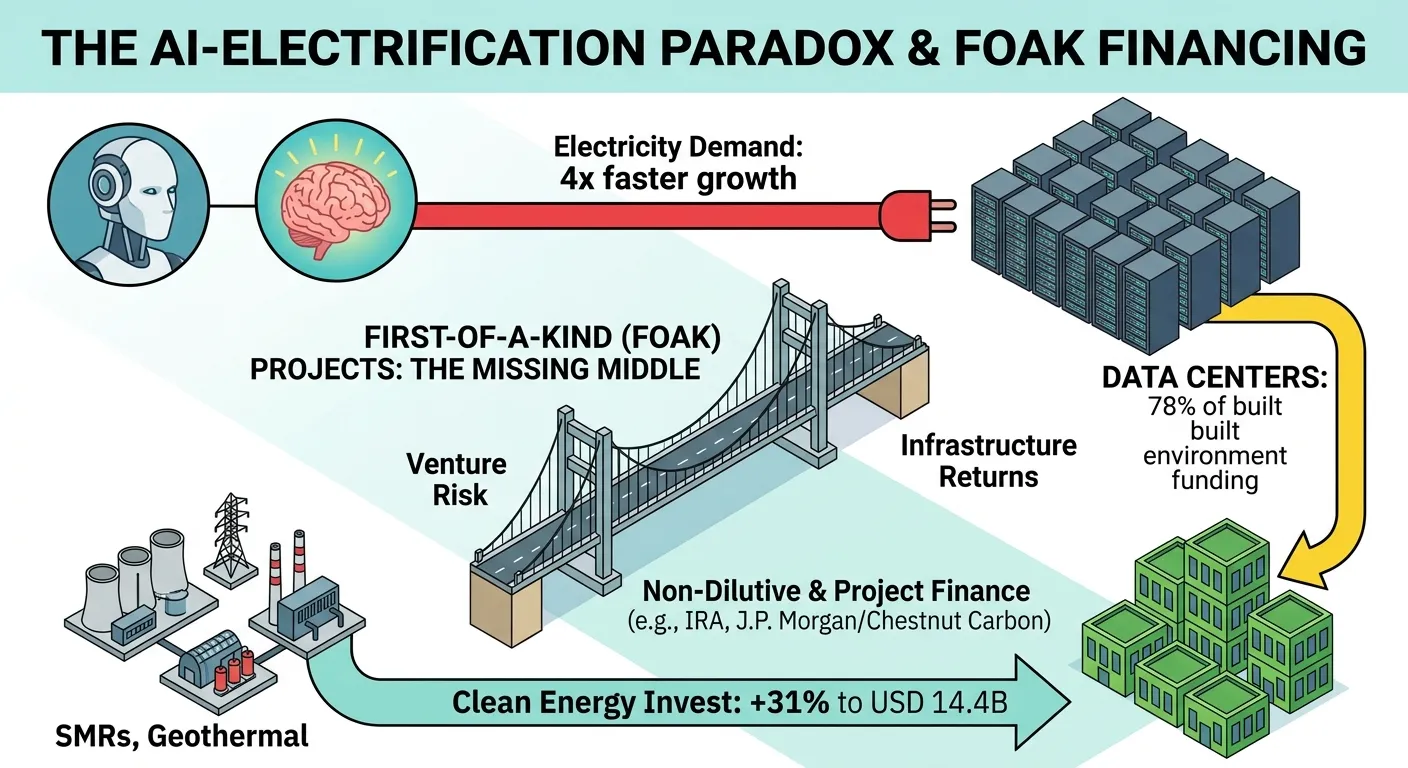

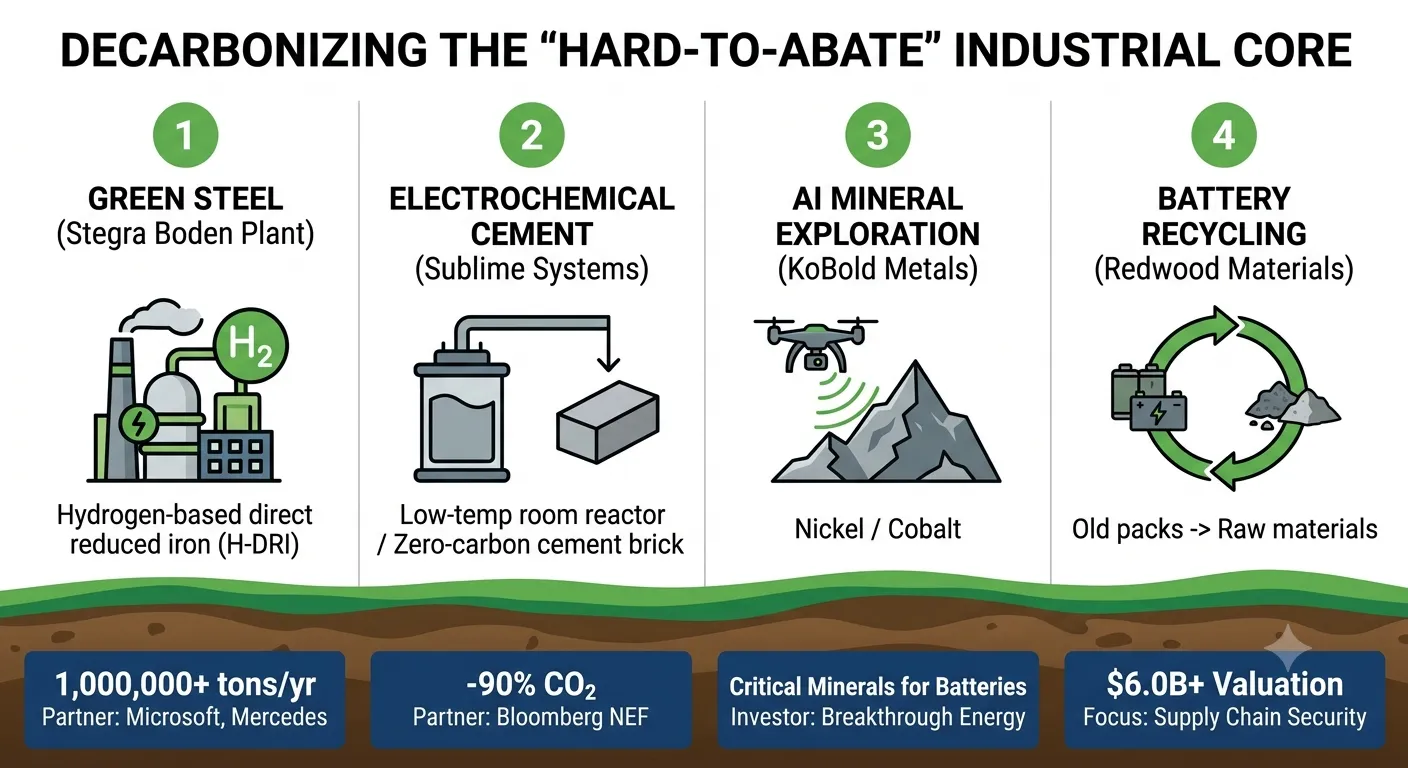

Decarbonizing the "Hard-to-Abate" Industrial Core

Heavy industry—specifically steel, cement, and chemicals—remains responsible for approximately 20% of global emissions and 15% of all industrial greenhouse gases. Decarbonizing these sectors requires high-temperature heat and complex chemical processes that cannot be easily electrified using existing technology. However, 2026 marks a shift toward the first large-scale commercial deployments of green industrial solutions.

The Hydrogen Reset and Green Steel Realities

The "hydrogen hype" of the early 2020s has given way to a leaner, more credible landscape. While green hydrogen was once touted as a universal panacea, the reality of high costs and infrastructure limitations has led to a contraction in the global project pipeline. Nevertheless, hydrogen remains strategically critical for steelmaking. Stegra (formerly H2 Green Steel) is advancing its Boden plant in Sweden, which aims to be the world's largest facility using green hydrogen-based direct reduced iron (H-DRI) combined with electric arc furnaces.

SSAB, another leader in the sector, is converting its Oxelösund mini-mill to electric arc furnaces, with operations expected to begin in early 2027. This transition is supported by a burgeoning market for "fossil-free steel," with companies like Toyota Material Handling Europe and Rheinmetall signing strategic offtake agreements to reduce their own Scope 3 emissions.

Electrochemical Innovation in Cement and Mining

In the cement sector, which accounts for 8% of global $CO_2$ emissions, companies like Sublime Systems are reengineering the production process using an electrochemical approach that operates at ambient temperatures, potentially reducing the carbon footprint by over 90%. This avoids the massive emissions released by traditional limestone-burning kilns.

The mining industry is also being transformed by climate tech. KoBold Metals is utilizing AI-driven mineral exploration to locate the critical mineral deposits—nickel, cobalt, and lithium—needed to power the global battery supply chain. This "AI-enhanced mining" is essential for securing the raw materials required for the energy transition while minimizing the environmental impact of extraction.

Hard-to-Abate Innovator | Core Technology | Strategic Partner/Investor |

Stegra | H-DRI Green Steel | Microsoft Climate Innovation Fund, Mercedes-Benz |

Boston Metal | Molten Oxide Electrolysis (MOE) | Microsoft, BHP |

Sublime Systems | Electrochemical Cement | Bloomberg NEF Pioneer |

KoBold Metals | AI Mineral Exploration | Breakthrough Energy Ventures, T. Rowe Price |

The First-of-a-Kind (FOAK) Financing Bottleneck

The most significant hurdle for green innovation in 2026 is the successful financing and execution of First-of-a-Kind (FOAK) commercial-scale projects. These projects represent the "missing middle" because they carry venture-level technology risk but offer infrastructure-style returns, making them a poor fit for both traditional venture capital and conservative infrastructure funds.

Modularity as a Risk Mitigant

A key finding in 2026 is the inverse correlation between technological modularity and cost overruns. Data from recent FOAK projects suggests that modular technologies, such as solar power and energy storage, have significantly lower mean cost overruns (1-8%) compared to bespoke, complex systems like nuclear power, which can see overruns of 120% or more.

Investors are increasingly prioritizing "modular hardware" that can be scaled like "Lego blocks". This approach allows for faster iteration cycles and "learning-by-doing," which accelerates cost reductions. Companies like Rondo Energy, which uses modular thermal batteries to store excess renewable electricity as high-temperature heat, exemplify this trend.

Data-Driven Scale-Up Strategies

To unlock private capital for FOAK projects, the industry is moving toward a "Project Readiness Level" (PRL) framework. This framework scores projects based on a combination of Technology Readiness (TRL), Adoption Readiness (ARL), and the maturity of the "Balance of Plant". By using historical benchmarking and reference class forecasting, developers can build more robust risk profiles that satisfy the requirements of non-dilutive capital providers.

Strategic EPC (Engineering, Procurement, and Construction) segmentation is also emerging as a best practice. By separating the engineering phase from construction, firms can better align incentives and reduce the likelihood of the schedule delays and cash shortages that have derailed previous FOAK efforts.

Regional Dynamics and the Geopolitics of Clean Tech

The transition to a low-carbon economy is no longer just an environmental project; it is a fundamental reshaping of global trade and industrial power. 2026 is characterized by "policy whiplash" and the emergence of regional "coalitions of the willing" that prioritize energy security and industrial competitiveness over global climate multilateralism.

The European Union: Carbon Border Adjustments and Labor Re-skilling

The European Green Deal continues to be the most comprehensive policy framework for green innovation. A watershed moment arrives in January 2026 with the definitive implementation of the Carbon Border Adjustment Mechanism (CBAM). This carbon tariff ensures that importers of carbon-intensive goods pay a price equivalent to that paid by domestic producers under the EU Emissions Trading System (ETS).

The EU is also focused on the social dimension of the transition. Studies suggest that between 150,000 and 500,000 workers will need to be re-skilled annually to support the expansion of the EV, wind, and solar sectors. This re-skilling effort, while costly (estimated at EUR 350 million to EUR 1.4 billion per year), is seen as essential for maintaining social legitimacy and avoiding political backlash against the Green Deal.

China and the Asia-Pacific: The Manufacturing Hegemon

The Asia-Pacific region has emerged as the "climate pivot point," warming at twice the rate of the rest of the world but also acting as the global hub for clean tech manufacturing. China has shifted its climate policy focus toward global leadership in clean technology rather than near-term emissions cuts, leveraging its massive advantages in AI and energy manufacturing to dominate the "electrotech" era.

In Southeast Asia, cross-border electricity trade is expanding, with initiatives like the Laos-Thailand-Malaysia-Singapore interconnection allowing land-constrained markets to import renewable power. Meanwhile, countries like Japan and South Korea are reviving their nuclear programs to meet the surging power demands of AI and data centers while maintaining energy security.

Region | Primary Policy Driver | 2026 Strategic Focus |

European Union | CBAM / Green Deal | Leveling the carbon playing field; labor re-skilling |

China | Global Tech Leadership | Dominating the supply chain for batteries & solar |

USA | Inflation Reduction Act (IRA) | Domestic manufacturing & mineral security |

Japan | Power Market Reform | Nuclear restart & corporate renewable PPAs |

India | Grid Integration Program | Stabilizing 200+ GW of renewables by 2026 |

Adaptation, Resilience, and the Circular Economy

While mitigation (reducing emissions) has historically captured the majority of climate tech funding, 2026 sees a rapid expansion into adaptation and resilience. "The playbook," as defined by industry leaders, is to "decarbonize what we can and adapt to what we cannot".

The Water Tech Breakout

Water technology is poised for a breakout in 2026, moving from a niche environmental concern to a core business continuity issue. Droughts and water scarcity are increasingly recognized as operational risks for heavy industry, agriculture, and data center cooling. Investment is flowing into smart leak detection, low-energy desalination, and advanced filtration for safe water reuse.

Climate Risk Intelligence and Disaster Finance

The translation of complex climate science into the language of financial risk has become a multi-billion dollar opportunity. Companies like Jupiter Intelligence use AI to model the probability of extreme weather events—floods, wildfires, and heatwaves—down to the level of individual assets. In Emerging Asia, governments are shifting from reactive, fragmented disaster financing to ex-ante, market-based instruments that build institutional resilience.

This shift is also seen in the rise of "climate fintech," where green bonds and insurance modeling are used to mobilize capital for resilient infrastructure. The integration of mobile money ecosystems in regions like sub-Saharan Africa—where USD 1.4 trillion was transacted in 2025—provides a blueprint for how digital financial services can empower underserved populations to invest in climate-resilient agriculture and energy access.

The Future of Mobility: Beyond the Electric Car

While low-carbon mobility remains the largest segment of climate tech by deal value, the focus is expanding beyond passenger electric vehicles (EVs). 2026 sees significant strides in decarbonizing "hard-to-electrify" transport, including aviation and long-haul shipping.

Sustainable Aviation and Heavy Transport

Sustainable Aviation Fuel (SAF), produced from waste-based ethanol or synthetic pathways, is projected to reduce airline emissions by up to 80%. LanzaJet and other leaders have secured partnerships with major airlines to begin commercial-scale production. In the regional flight sector, companies like ZeroAvia are developing hydrogen-electric powertrains to overcome the energy density limitations of batteries in aircraft.

Battery technology itself is evolving toward higher performance and circularity. Redwood Materials, founded by former Tesla executives, is building a closed-loop supply chain by recycling lithium-ion batteries to recover critical minerals like nickel, cobalt, and lithium. This "urban mining" reduces the need for virgin extraction and significantly lowers the carbon footprint of battery production.

Mobility Innovator | Core Technology | 2026 Milestone |

Redwood Materials | Battery Recycling | $6.0B+ valuation; closed-loop supply chain |

LanzaJet | Sustainable Aviation Fuel (SAF) | Operational Freedom Pines Fuels facility |

ZeroAvia | Hydrogen-Electric Aviation | Commercial certification for 19-seat aircraft |

BETA Technologies | Electric Aircraft & Charging | $2.1B IPO; focus on fleet charging |

Conclusion: A Pivot Toward Profitability and Scale

The landscape of climate tech in 2026 is defined by a hard-earned maturity. The "green premium" is no longer an acceptable cost for most corporations; instead, the market is rewarding technologies that provide "green discounts" through enhanced efficiency and operational resilience. The entry of CFOs into the climate conversation has professionalized the sector, moving it from the periphery of corporate social responsibility to the core of financial strategy.

As we look toward 2030, the success of the energy transition will depend on our ability to solve the FOAK project finance challenge and to integrate AI not just as a consumer of power, but as the primary optimizer of a complex, decentralized, and decarbonized global economy. The "industrialization of climate tech" is not merely a market trend; it is the fundamental economic transformation required to secure a sustainable future in a state of climate emergency. The companies that thrive in this new era will be those that prioritize execution over experimentation and profitability over promise.

Want to calculate the equity for your cofounder?

Nail your cap table before you sign. Whether you're splitting equity with a co-founder or planning your next funding round, our Equity Calculator gives you precision in seconds

Equity calculator →