How the Red Sea Crisis Disrupted Global Startup Logistics

July 3, 2026 by Harshit Gupta

The global maritime infrastructure, a network responsible for the movement of over 80 percent of the world’s physical goods, has historically operated on the assumption of frictionless transit through a handful of critical chokepoints. The Red Sea corridor, anchored by the Bab el-Mandeb Strait and the Suez Canal, serves as the primary artery for approximately 12 to 15 percent of global trade and 30 percent of world container traffic. Since late 2023, the systemic destabilization of this corridor by Houthi militant attacks has initiated a "cascading disruption" that extends far beyond the immediate geography of the Middle East, fundamentally altering the operational and financial realities of the global startup ecosystem. For early-stage companies and hardware-centric ventures, the crisis is not merely a logistical delay; it represents a profound shock to capital efficiency, market timing, and supply chain philosophy.

The Anatomy of the Maritime Shock: Mechanism and Magnitude

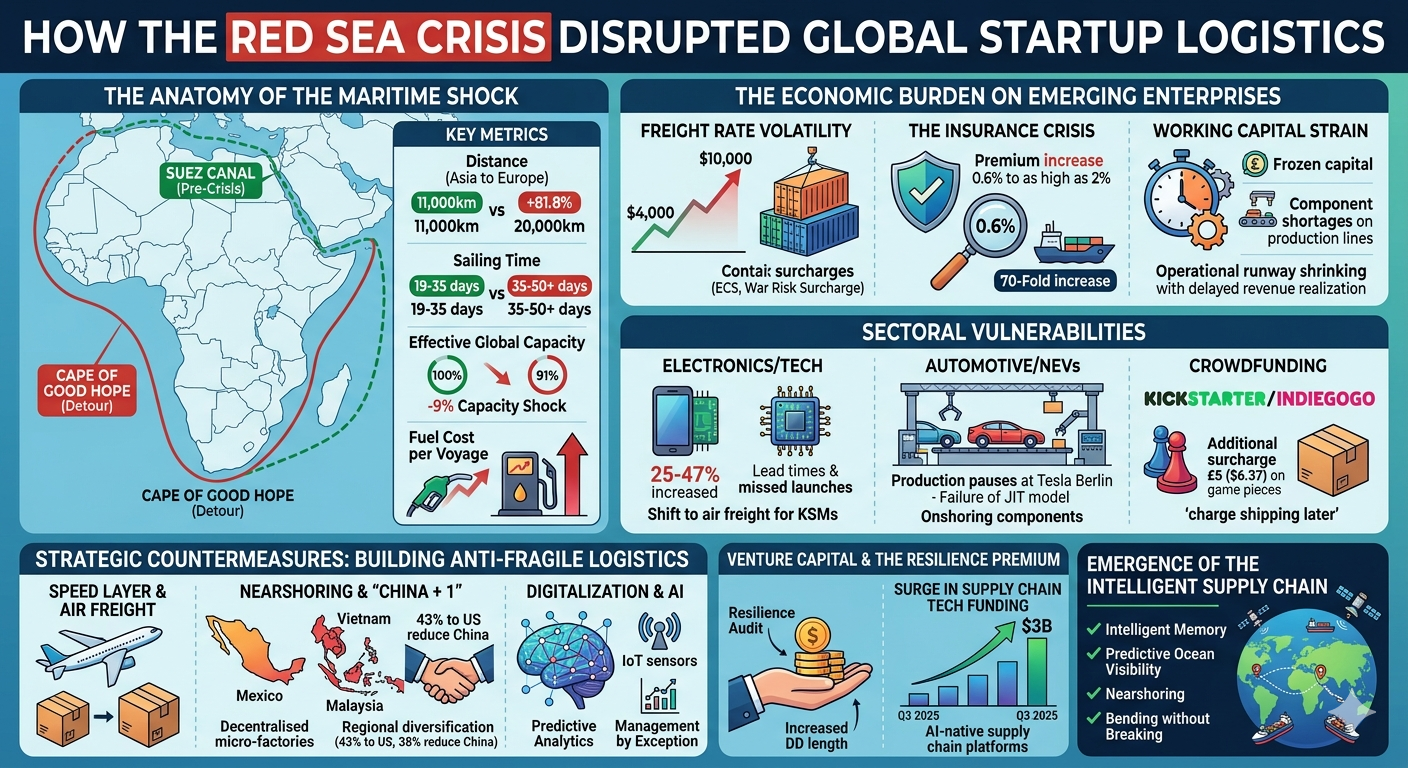

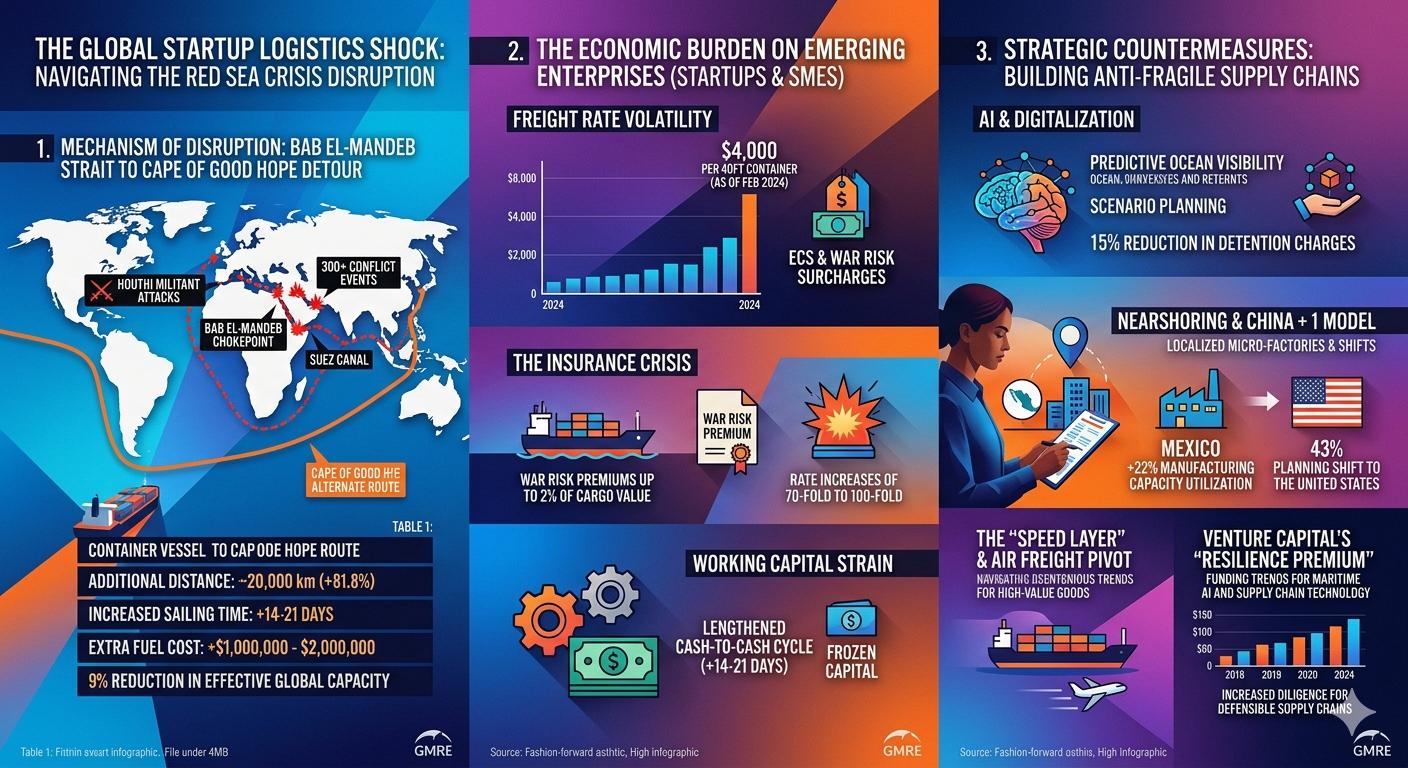

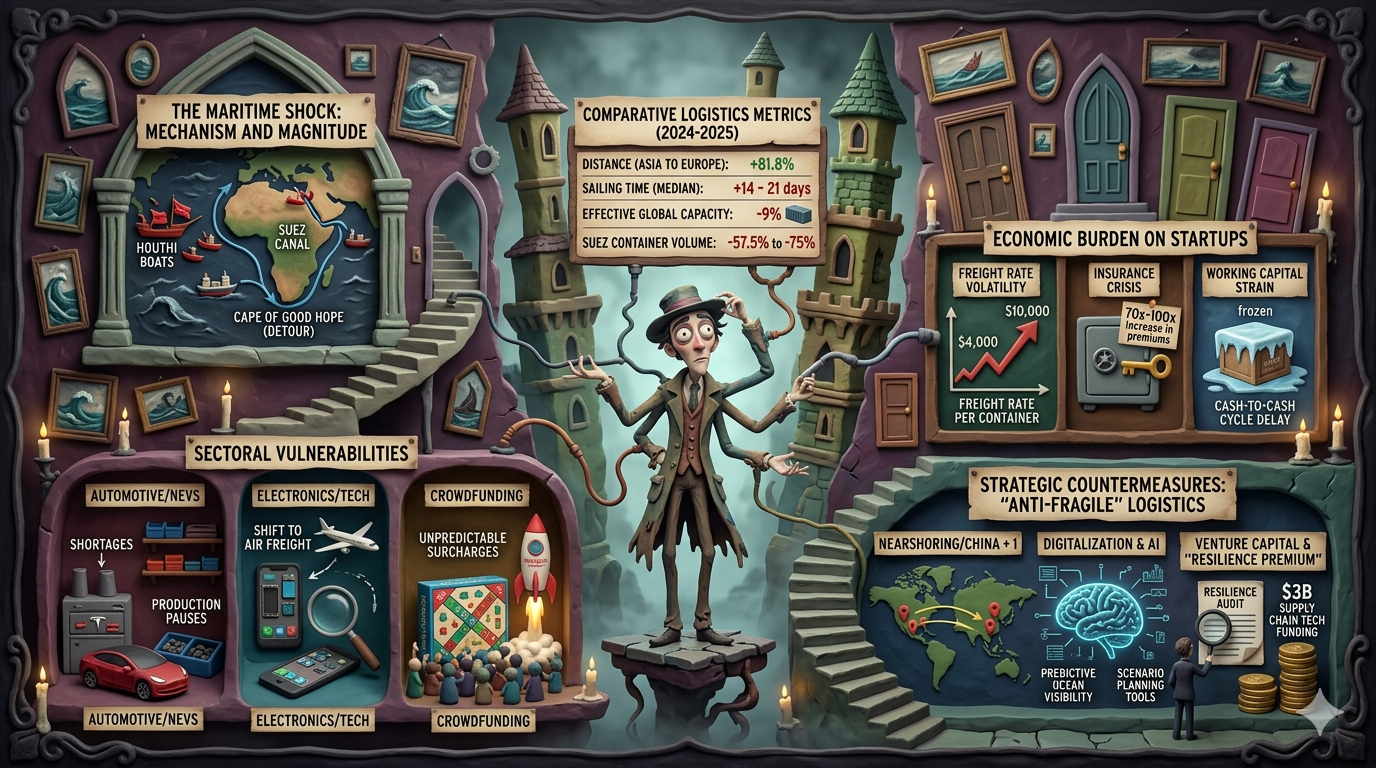

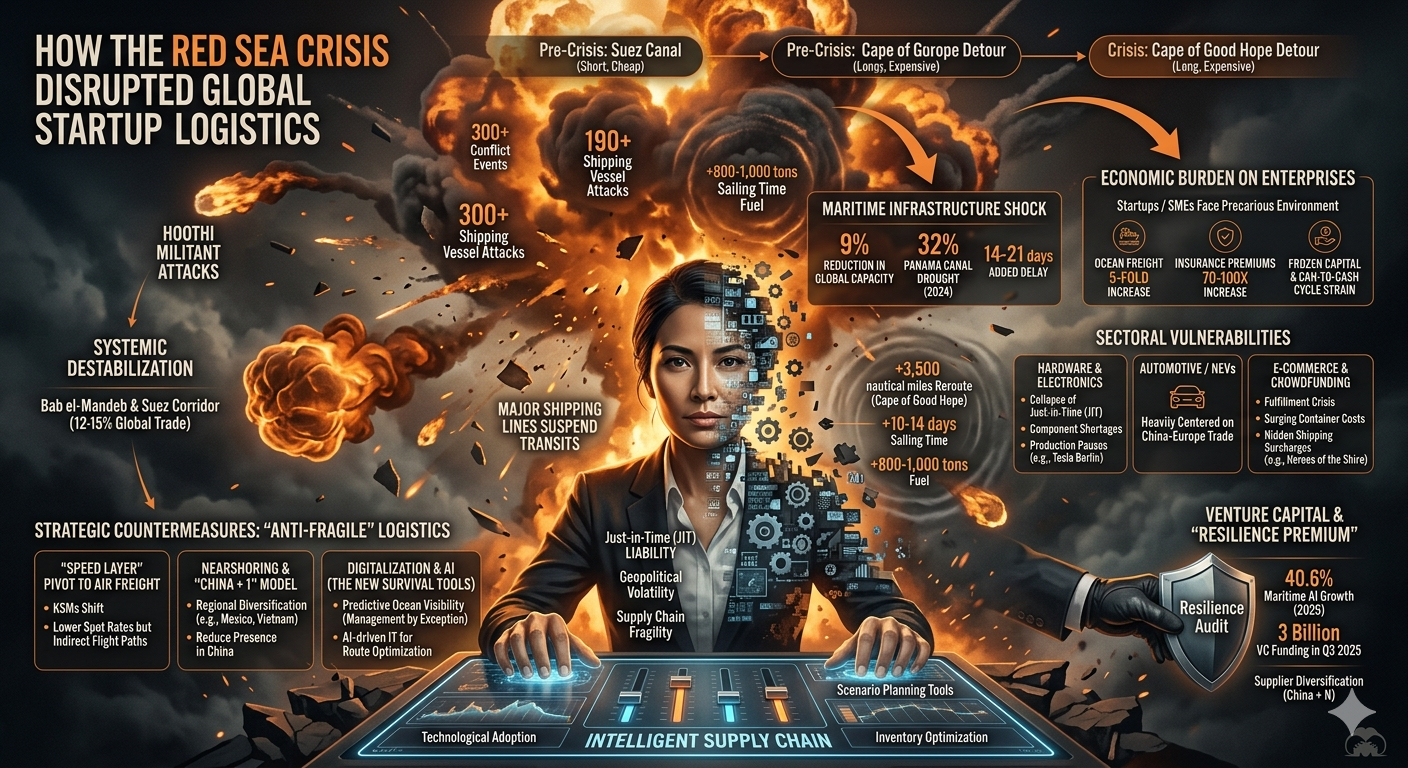

The disruption began in November 2023 when Ansar Allah (Houthi) forces in Yemen intensified attacks on commercial vessels, claiming solidarity with Palestinians in the Gaza conflict. By October 2024, more than 300 conflict events had been documented in the Red Sea, Gulf of Aden, and Northwestern Indian Ocean, resulting in over 190 attacks on shipping vessels. This persistent volatility forced major global shipping lines—including Maersk, MSC, Hapag-Lloyd, and CMA CGM—to suspend transits through the Suez Canal and reroute vessels around the Cape of Good Hope at the southern tip of Africa.

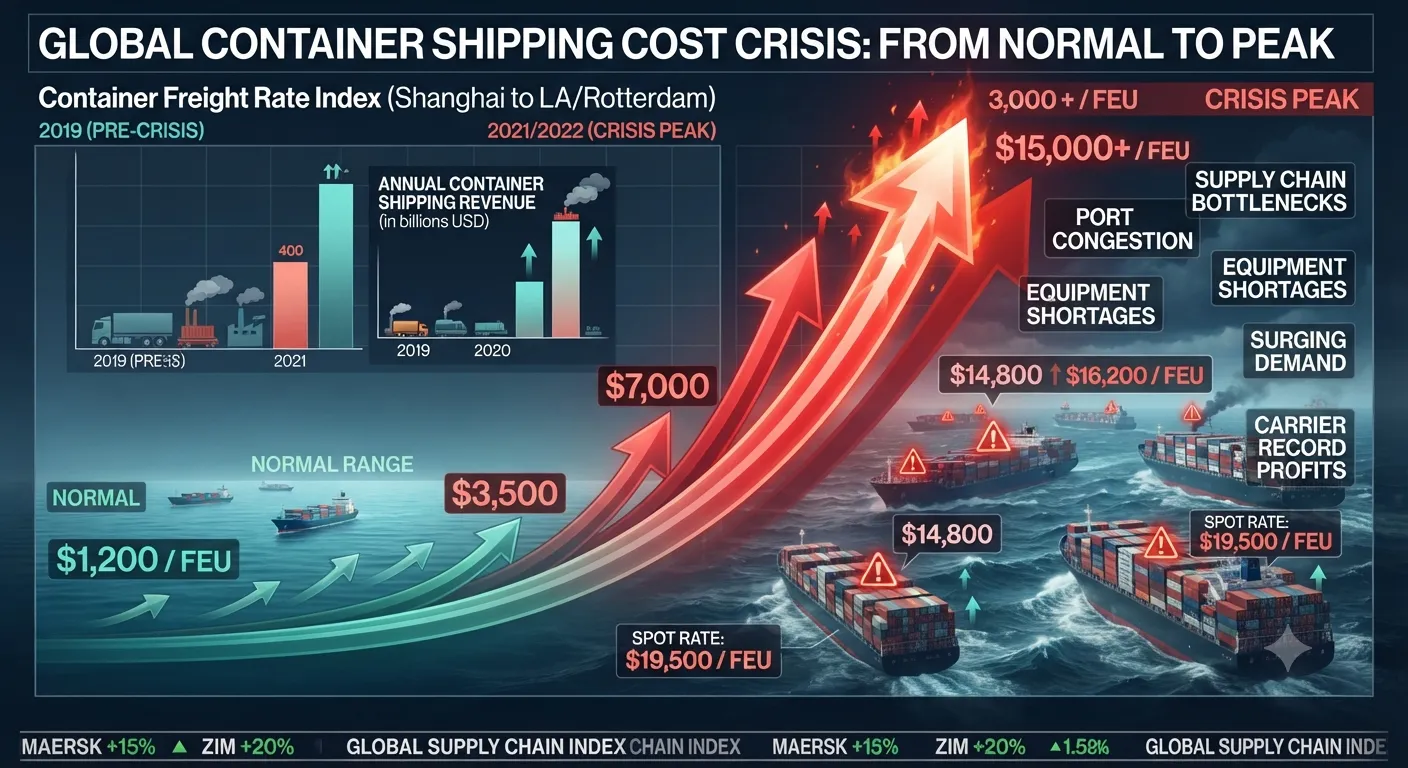

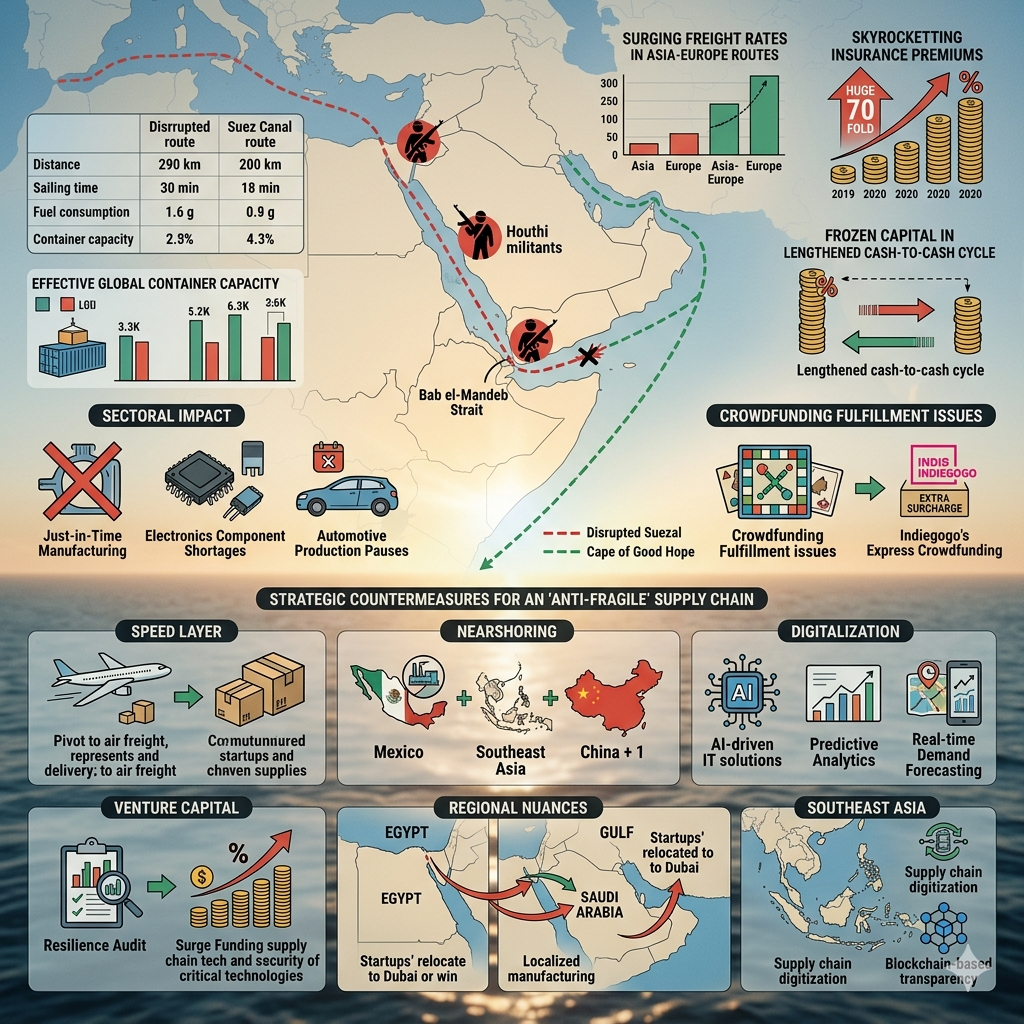

The diversion of maritime traffic around the Cape of Good Hope adds approximately 3,500 nautical miles to a typical voyage between Asia and Europe. This detour is not merely a geographic inconvenience but a multi-dimensional economic burden. For a standard container vessel, the circumnavigation of Africa adds 10 to 14 days of sailing time and consumes an additional 800 to 1,000 tons of fuel. In more extreme cases, transit times from Asia to Northern European or Mediterranean ports have surged from 30-45 days to as many as 75 days.

Table 1: Comparative Logistics Metrics of Major Global Shipping Routes (2024-2025)

Route Metric | Suez Canal (Pre-Crisis) | Cape of Good Hope (Detour) | Change / Impact |

Distance (Asia to Europe) | ~11,000 km | ~20,000 km | +81.8% |

Sailing Time (Median) | 19 - 35 days | 35 - 50+ days | +14 - 21 days |

Fuel Cost per Voyage | Baseline | +$1,000,000 - $2,000,000 | +30% Consumption |

Effective Global Capacity | 100% | 91% | -9% Capacity Shock |

Suez Container Volume | ~4.0M metric tons/day | ~1.7M metric tons/day | -57.5% to -75% |

The implications for global shipping capacity are modeled as a reduction in effective supply. The lengthening of supplier delivery times acts as an adverse supply shock; the rerouting of ships around Africa equates to a roughly 9 percent reduction in effective global container shipping capacity. This reduction occurred simultaneously with a severe drought in the Panama Canal, which also constrained traffic through that vital chokepoint by nearly 32 percent year-over-year in early 2024. The convergence of these events created what industry analysts have termed a "perfect storm" for global logistics.

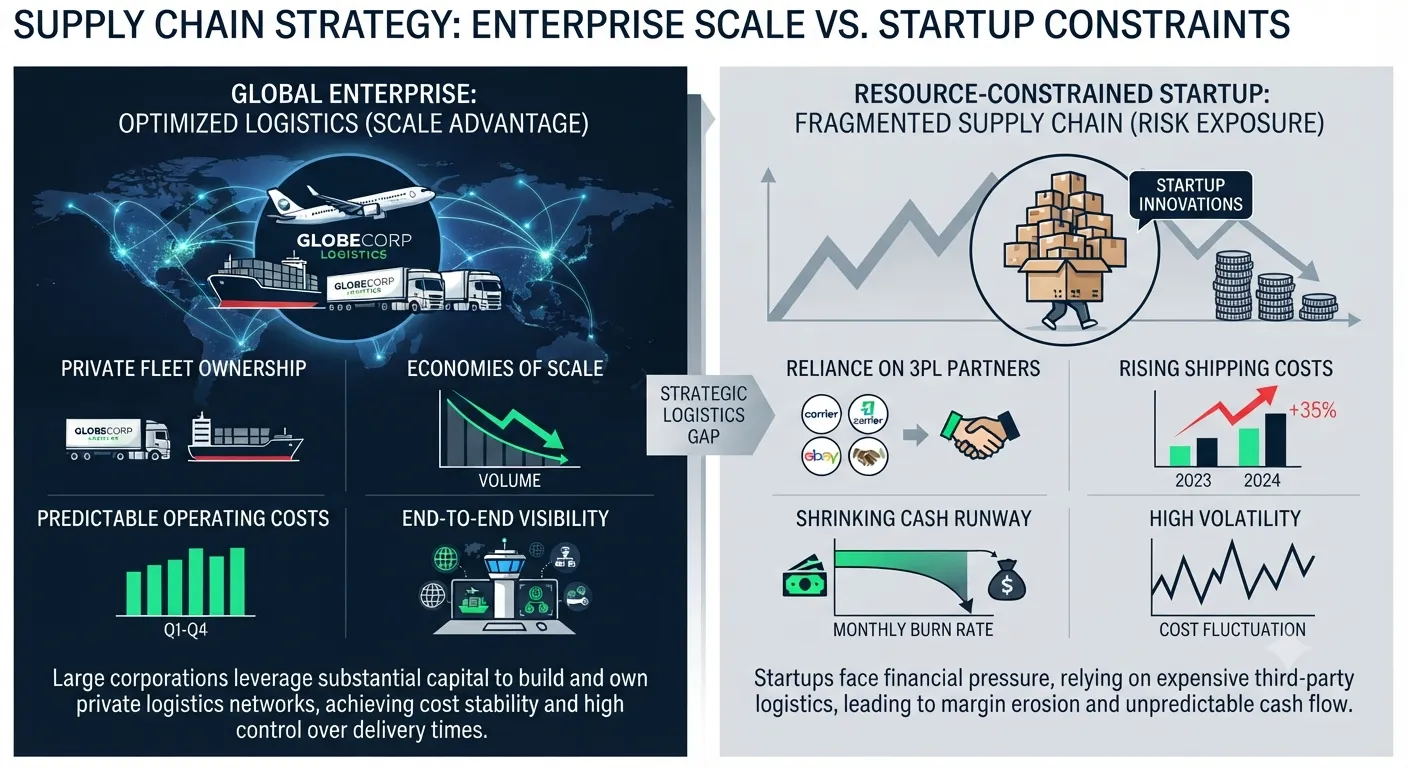

The Economic Burden on Emerging Enterprises

While multinational corporations like Tesla and Volvo possess the scale to absorb shipping cost increases or charter their own vessels, startups and small-to-medium enterprises (SMEs) face a far more precarious financial environment. The crisis has impacted startup financials through three primary vectors: surging freight rates, skyrocketing insurance premiums, and the "frozen capital" of delayed inventory.

Freight Rate Volatility and the Surcharge Regime

Ocean freight costs on key Asia-Europe routes surged nearly five-fold in the immediate aftermath of the initial attacks. By February 2024, the cost of transporting a 40-foot container from Asia to Northern Europe had reached approximately $4,000—a 173 percent increase in just months. Some indices, such as the Drewry World Container Index, briefly spiked to over $10,000 per standard container on certain trade lanes.

Furthermore, carriers introduced a complex regime of surcharges to pass on the costs of rerouting and risk. These include the Emergency Contingency Surcharge (ECS) and the War Risk Surcharge, which can range from $500 to as much as $4,000 per container depending on the carrier and the specific trade lane. Startups, often operating on thinner margins and lacking long-term volume contracts, are frequently forced into the volatile spot market, where these price spikes are felt immediately and acutely.

The Insurance Crisis: A 70-Fold Increase in Risk Premiums

A critical but often overlooked disruption is the collapse of the traditional maritime insurance model for Red Sea transits. For vessels still attempting the passage, war risk insurance premiums escalated from 0.6 percent of cargo value to as high as 2 percent. In the most extreme instances, brokers reported that insurance rates for the Red Sea region increased 70-fold to 100-fold since the crisis began in December 2023. The premium to insure a $100 million container ship jumped from approximately $10,000 to nearly $700,000 per voyage. For a startup shipping high-value electronics or medical hardware, this insurance hike can represent a significant portion of their total landed cost, directly eroding profit margins and reducing competitive pricing flexibility.

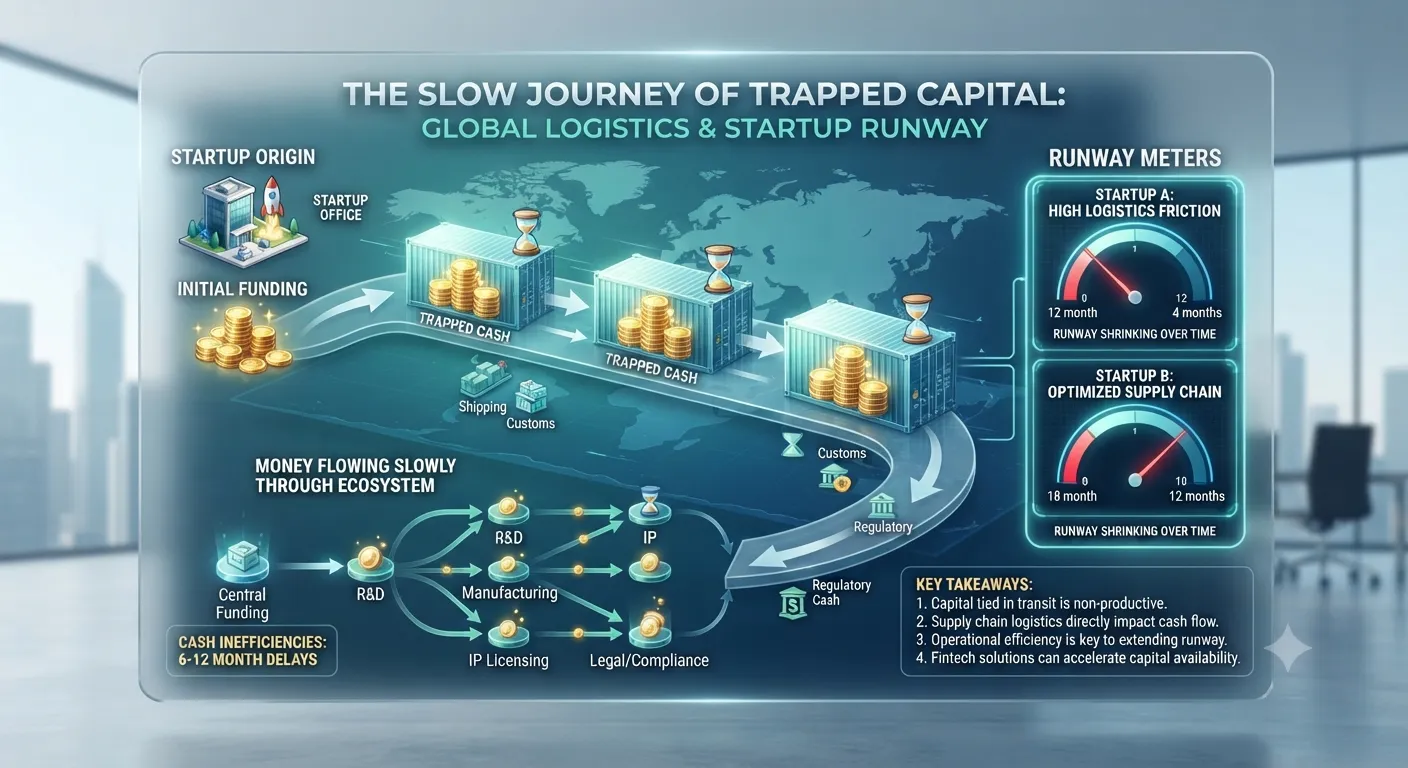

Working Capital Strain and the Cash-to-Cash Cycle

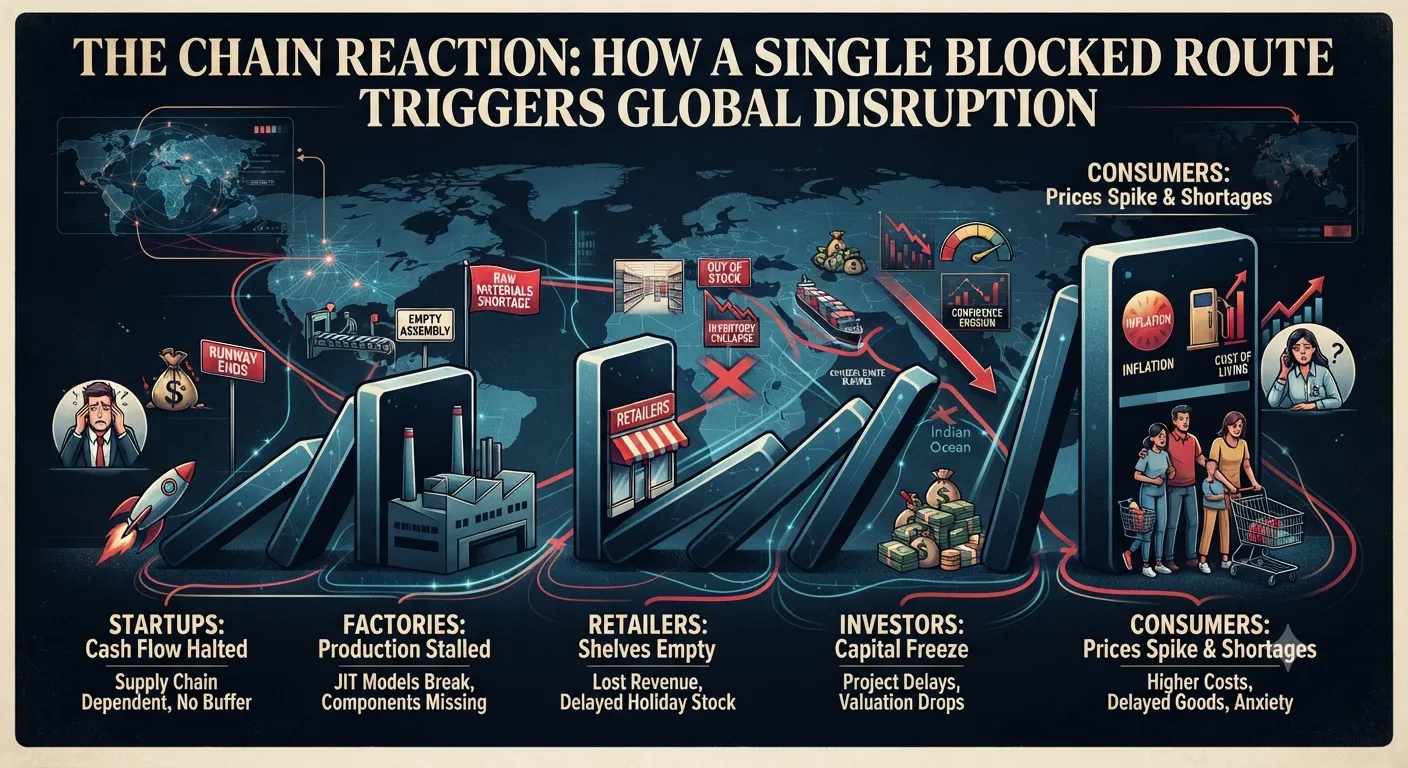

The "hidden" cost of the Red Sea crisis is the lengthening of the cash-to-cash cycle. When goods spend an additional 14 to 21 days at sea, the capital used to produce those goods remains tied up in transit rather than being available for reinvestment in R&D or growth. For a venture-backed startup, this can be catastrophic. If a startup's burn rate is $1 million a quarter and a logistics disruption cuts funding access or revenue realization by 30 percent, their operational runway can shrink by two or more quarters. Delayed shipments also lead to "component shortages on production lines," creating a domino effect that halts downstream assembly and delays the realization of revenue from end customers.

Sectoral Vulnerabilities: Hardware, Electronics, and Crowdfunding

The crisis has disproportionately affected specific startup sectors that rely on "just-in-time" (JIT) manufacturing and highly integrated global supply chains.

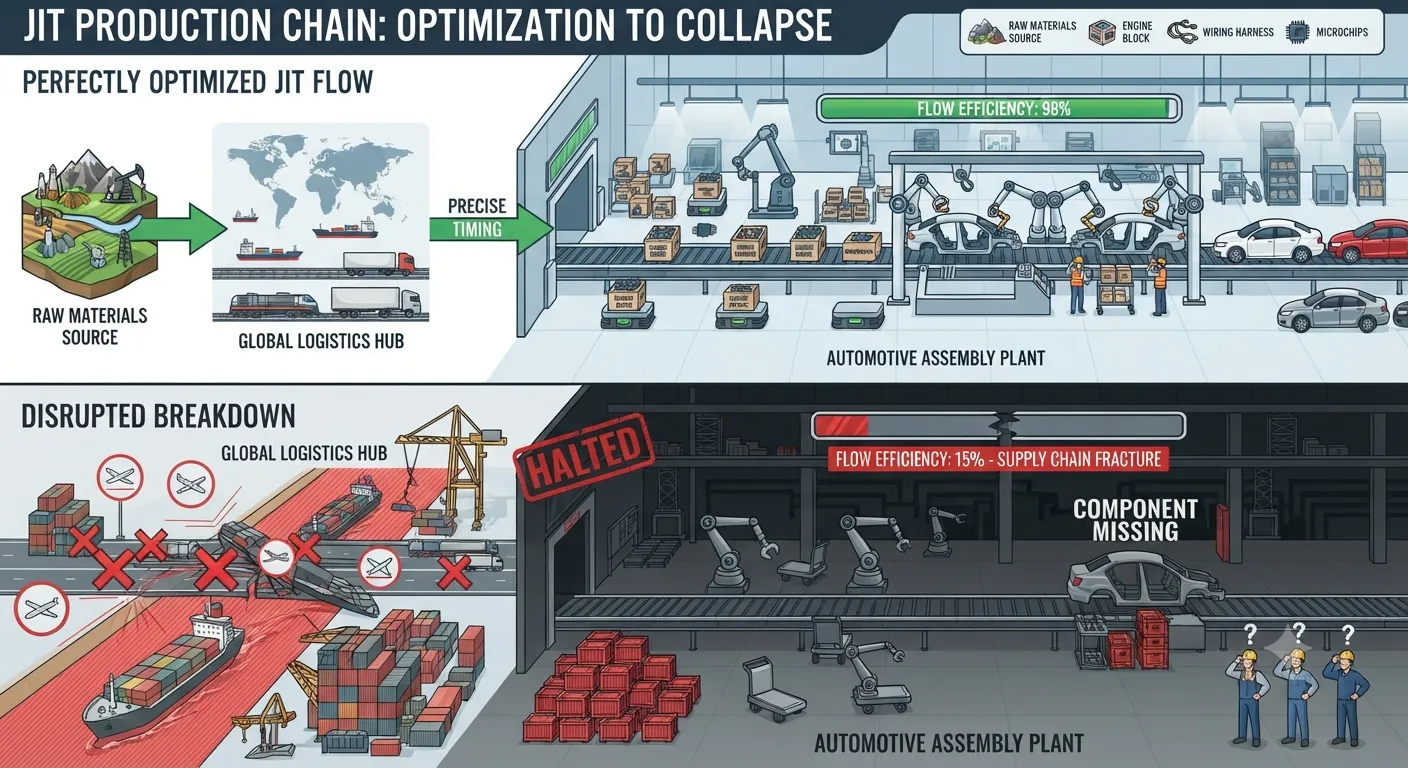

The Collapse of Just-in-Time for Hardware Startups

Startups in the automotive, electronics, and consumer technology sectors were among the first to feel the impact. High-value electronics, while having higher margins to absorb some cost increases, face immense time pressure for product launches. Automotive startups—particularly those in the New Energy Vehicle (NEV) space—are vulnerable because their supply chains are heavily centered on China-Europe trade, which is largely carried by sea.

Several Europe-based auto plants, including Tesla’s factory in Berlin, Germany, were forced to temporarily pause production due to a lack of car parts from Asia. This disruption highlights the fragility of the JIT model, which minimizes inventory levels in favor of timely deliveries—a strategy that becomes a liability in a volatile geopolitical environment.

Table 2: Impact of Red Sea Disruptions on Key Startup-Dominant Sectors (2024-2025)

Industry Sector | Primary Logistical Impact | Key Risk to Startups | Response / Mitigation |

Electronics / Tech | 25-47% increase in lead times | Missing launch windows; stock-outs | Shift to air freight for KSMs |

Automotive / NEVs | Production pauses (Tesla, Volvo) | Failure of JIT assembly model | Onshoring/Nearshoring components |

E-commerce / Retail | 350% increase in Asia-Europe rates | Margin erosion; high churn | Checkout optimization; "pause" options |

Crowdfunding | Unpredictable S&H surcharges | Failure to fulfill to early backers | Moving to "charge shipping later" models |

Agri-tech / Food | Spoilage of containerized perishables | Total loss of inventory value | Sourcing from closer regions |

The Fulfillment Crisis in Crowdfunding

The crowdfunding ecosystem, including platforms like Kickstarter and Indiegogo, has been hit by a "lunacy" in shipping prices compared to a decade ago. Small-scale publishers and first-time hardware creators lack the upfront capital to navigate surging container costs.

One notable case study is the Heroes of the Shire board game project. As a first-time publisher, the creator faced a situation where the project was not projected to break even due to escalating fulfillment costs. To avoid leaving games stranded in China, the publisher was forced to implement an additional surcharge of £5 ($6.37) for all backers—a decision necessitated by the fact that container costs from China had surged by approximately $2,300 per container. This highlights a growing trend in crowdfunding where shipping fees are hidden and charged after the initial campaign, often to the frustration of backers.

In response to these systemic delays, Indiegogo announced "Express Crowdfunding" in February 2025. This new format eliminates the platform’s historical two-week delay between campaign end and shipping address collection, allowing creators to ship products while campaigns are still live. This structural change was driven by high-profile failures, such as the Ayaneo gaming handheld campaign, which was delayed by 10 days due to platform policy requirements, causing it to miss critical holiday shipping windows.

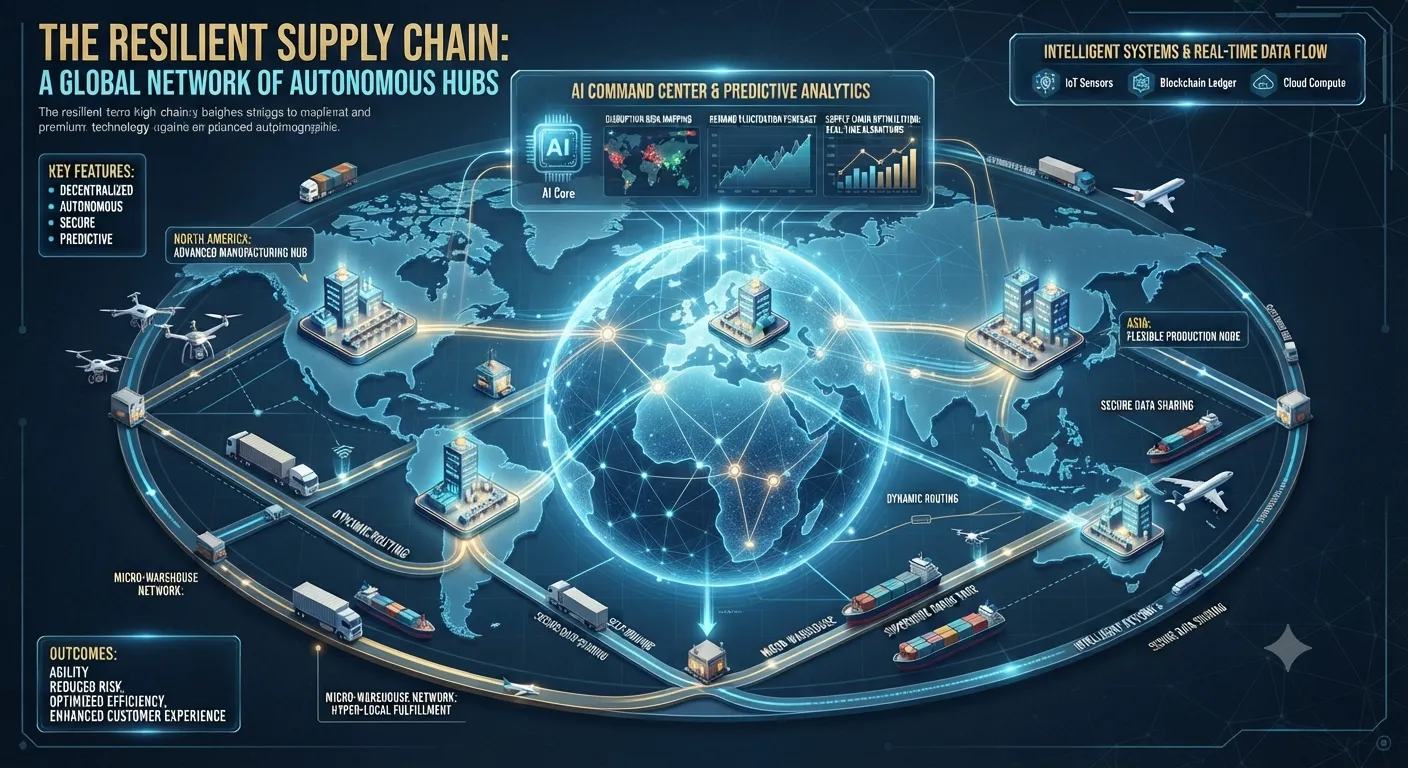

Strategic Countermeasures: The Transition to "Anti-Fragile" Logistics

To survive the prolonged instability, startups are moving beyond simple risk mitigation toward the construction of "anti-fragile" supply chains—networks that are not only resistant to shocks but can adapt and improve because of them.

The "Speed Layer" and the Pivot to Air Freight

For high-value, low-volume sectors like pharmaceuticals and advanced electronics, startups have implemented a "Speed Layer" strategy. This involves shifting critical "Key Starting Materials" (KSMs) to air freight immediately to bypass maritime chokepoints. While air cargo spot rates from China to the U.S. plummeted in early 2025 to pre-pandemic levels (~$2.98 per kg), the overall demand for air freight remains elevated due to the growth of e-commerce and the need for supply chain stability.

However, air freight is not a panacea. Avoiding conflict zones near the Red Sea requires longer, more indirect flight paths, resulting in higher fuel costs and scheduling complexities. Startups are increasingly using AI-driven IT solutions to optimize these routes, allowing them to reroute proactively rather than reactively.

Nearshoring and the "China + 1" Model

The Red Sea crisis has accelerated the structural trend of "de-globalization" and regionalization. Startups are reconsidering their dependence on trans-Pacific and Asia-Europe maritime routes, moving toward nearshoring and onshoring.

Mexico has emerged as a primary beneficiary of this shift for North American startups, with a 22 percent increase in manufacturing capacity utilization as companies move production closer to their home markets. Similarly, Southeast Asian nations like Vietnam, Indonesia, and Malaysia are gaining traction as manufacturing alternatives, though they now face their own challenges from shifting U.S. tariff policies.

Regional Diversification: 43 percent of supply chain leaders are planning to shift more footprint to the United States over the next three years, while 38 percent plan to reduce their presence in China.

Decentralized Manufacturing: OEMs and startups are exploring "decentralized micro-factories" with plug-and-play assembly modules. This allows for localized production that is more responsive to regional demand and less vulnerable to international waterway closures.

Digitalization and AI: The New Survival Tools

In 2025, artificial intelligence has moved from an experimental "hype" phase to a core operational necessity for manufacturing and logistics startups. Advanced AI platforms are being utilized for predictive analytics, real-time demand forecasting, and inventory optimization.

Startups like Windward and Portcast provide "Predictive Ocean Visibility," allowing supply chain leaders to identify exactly which containers need attention due to port congestion or rerouting. This "Management by Exception" approach allows small teams to manage massive disruptions effectively, reducing manual updates by 80 percent and detention charges by 15 percent.

The physics of this technological shift can be expressed through the integration of IoT and AI. By analyzing real-time data from millions of supply chain sources across 200 countries, startups can model "Scenario Planning" tools to assess alternate routing options dynamically.

Venture Capital and the "Resilience Premium"

The Red Sea crisis has profoundly influenced venture capital (VC) sentiment and due diligence requirements in 2025. Investors are no longer just looking for growth; they are prioritizing "defensible" supply chains and resilient operating models.

New Due Diligence Standards

Venture capital firms have added a "Resilience Audit" to their standard due diligence process. For cross-border deals, particularly in sensitive sectors like semiconductors and AI, the length of due diligence increased by an average of 20 to 30 percent in 2025. Founders must now demonstrate:

Supplier Diversification: A "China + N" strategy that avoids single-country dependence.

Stress-Tested Assumptions: Modeling how the company would survive a 40 percent reduction in corporate profits or a 70-fold increase in insurance premiums.

Geopolitical Monitoring: Proactive monitoring of maritime news and the inclusion of "international waterway closure" as a specific Force Majeure event in contracts.

The Surge in Supply Chain Tech Funding

The market for maritime AI reached $4.3 billion in 2025, growing at a rate of 40.6 percent annually. In Q3 2025, venture capital deal value in supply chain tech hit $3 billion—a 26.1 percent quarter-over-quarter increase. Late-stage and venture-growth rounds for companies building AI-native supply chain platforms, such as Auger and Augment, led this funding charge. Startups focusing on "Security of Critical Technologies"—including quantum and AI chips—saw their funding more than double in 2025 to reach $2.4 billion.

Regional Nuances: MENA and Southeast Asia

The crisis has created both challenges and opportunities for startups in regional hubs.

Egypt and the Gulf: A Strategy of Adaptation

Egypt’s startup ecosystem has been battered by the loss of Suez Canal revenue, which normally accounts for a significant portion of the country's fiscal income. However, this instability has forced a pivot toward regional expansion and better regulatory frameworks. Egyptian startups are increasingly relocating their headquarters to Dubai or Riyadh to access Gulf investors and more stable capital markets while maintaining operations in Egypt for talent and high-skilled migration.

Saudi Arabia has used the crisis to accelerate its Vision 2030 goals, offering grants of $300,000 to $900,000 for startups that contribute to localized manufacturing and resilient logistics. Chip design startups like Rimal Semiconductors are outsourcing manufacturing to international foundries (Taiwan, Korea) while retaining Saudi ownership of IP, a strategy specifically designed to navigate the "increasingly fragmented" global semiconductor supply chain.

Southeast Asia: The Manufacturing Alternative

Southeast Asia continues to benefit from "China decoupling," but the Red Sea crisis has underscored the vulnerability of its maritime trade lanes to Europe and the U.S. East Coast. Startups facilitating manufacturing in Vietnam and Indonesia are increasingly focusing on "Supply Chain Digitization," using tools for real-time visibility and blockchain-based transparency to attract global buyers who are wary of long-range maritime disruptions.

Conclusion: The Emergence of the Intelligent Supply Chain

The Red Sea shipping crisis of 2023–2025 has been a watershed moment for the global startup community. It has exposed the inherent fragility of the cost-optimized, "Just-in-Time" logistics paradigm and replaced it with a mandatory requirement for resilience and agility. Startups that have navigated this period successfully are those that have embraced a tripartite strategy of technological adoption, geographic diversification, and financial stress-testing.

As 2025 draws to a close, the "new normal" for startup logistics is characterized by "Intelligent Memory" in product data management, the widespread use of AI for predictive ocean visibility, and a strategic shift toward nearshoring and decentralized manufacturing. The ability to "bend without breaking" in the face of geopolitical instability has become the ultimate competitive advantage, ensuring that the next generation of global startups can survive the turbulent waters of the Red Sea and beyond.

Want to calculate the equity for your cofounder?

Nail your cap table before you sign. Whether you're splitting equity with a co-founder or planning your next funding round, our Equity Calculator gives you precision in seconds

Equity calculator →