How Startups Are Adapting During the Israel-Hamas War

March 17, 2026 by Harshit Gupta

The global high-technology sector has long regarded the Eastern Mediterranean as a primary laboratory for innovation under pressure. However, the period beginning October 7, 2023, and extending through 2025 represents an unprecedented stress test for the startup ecosystems of both Israel and the Palestinian territories. This report examines the multi-faceted adaptation strategies employed by entrepreneurs, venture capitalists, and government agencies as they navigate a landscape defined by massive military mobilization, infrastructure destruction, and shifting global investor sentiment. The analysis indicates that while the Israeli tech sector has leveraged its "No Matter What" ethos to maintain a position as a global scale-up powerhouse, the Palestinian tech community has transitioned toward a decentralized "Resistance Economy" characterized by digital freelancing and solar-powered resilience.

The Macroeconomic Context and the Two-Engine Paradox

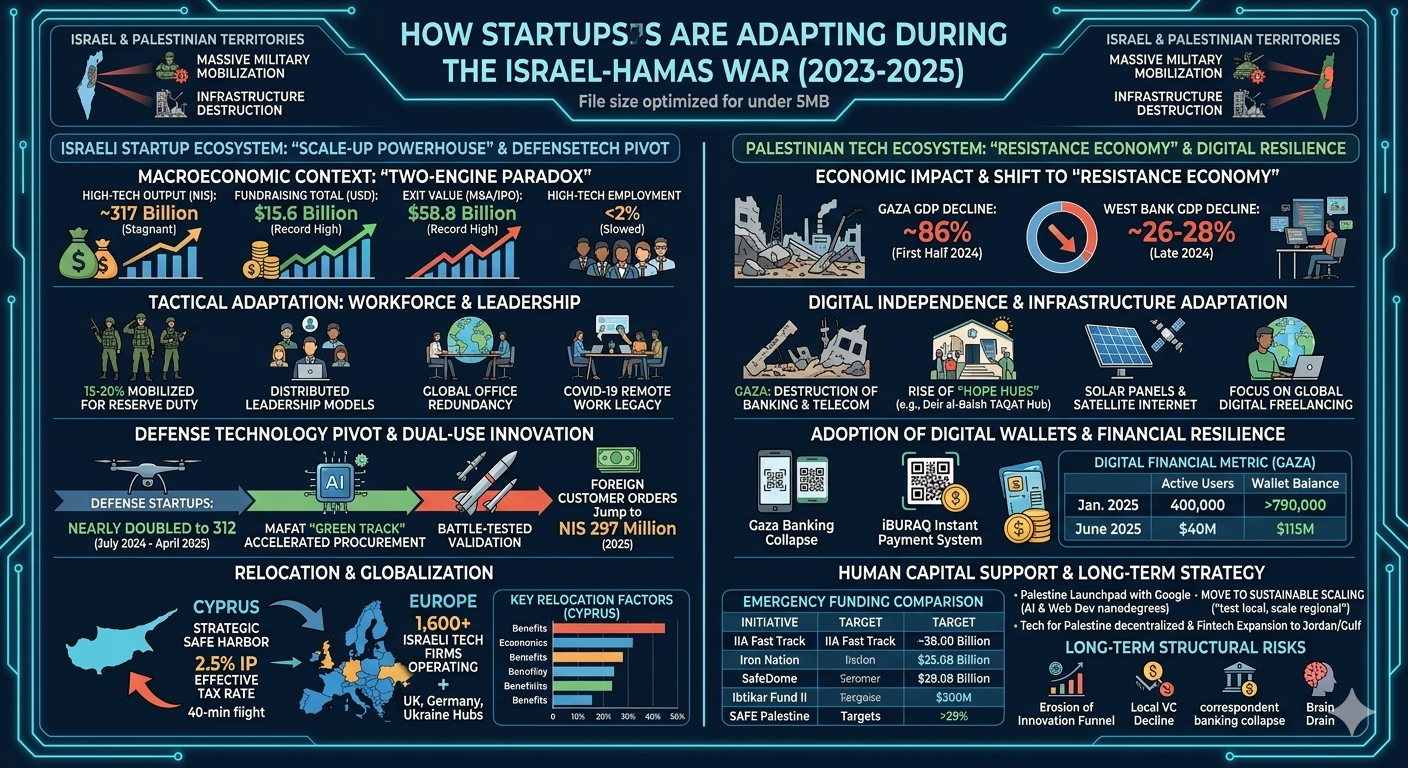

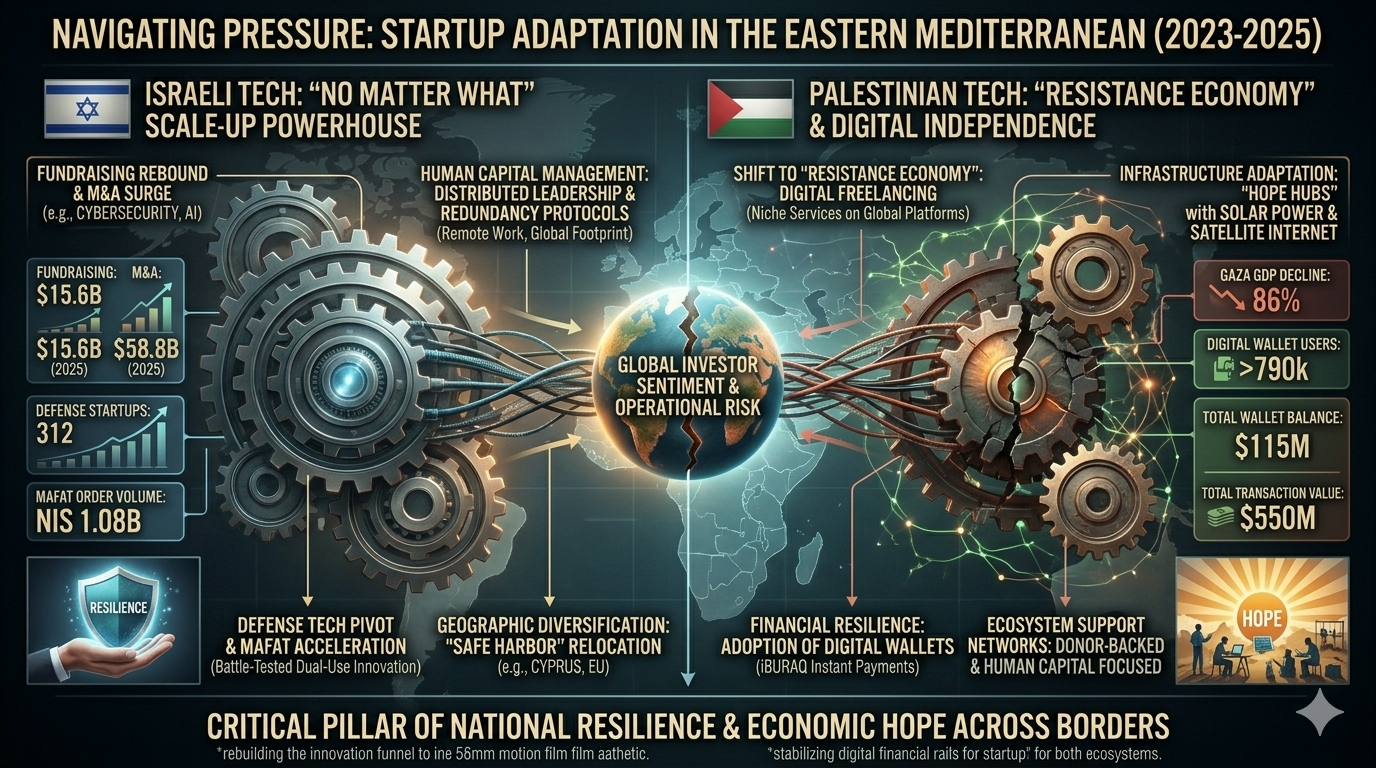

The Israeli high-tech sector entered the conflict period from a position of relative vulnerability. In early 2023, the industry was already grappling with a global venture capital slowdown and domestic political instability stemming from proposed judicial reforms, which led to a 60% decrease in investment compared to 2022. The onset of the war served as a secondary shock, yet by 2025, the sector demonstrated a recovery that some analysts describe as the "Two-Engine Paradox." This phenomenon is characterized by record-breaking fundraising and exit values occurring simultaneously with stagnant domestic output and shrinking research and development employment.

In 2024, the high-tech output remained virtually unchanged at approximately NIS 317 billion, accounting for 17% of Israel's GDP. By the first half of 2025, the sector’s contribution to national exports reached 57%, the highest share ever recorded, although this was partly driven by the sharp decline in other sectors such as tourism. Despite these macro-strengths, the internal sinews of the ecosystem showed signs of strain. High-tech employment growth, which had historically exceeded 5% annually, fell to below 2% between 2023 and 2025.

Economic Indicator | 2023 Performance | 2024 Performance | 2025 Performance/Projected |

High-Tech Output (NIS) | 315 Billion | 317 Billion | 317 Billion (Stagnant) |

Share of National GDP | 18% | 17% | 17.3% |

Share of Total Exports | 48% | 50% | 57% |

Fundraising Total (USD) | $7.3 Billion | $10.6B - $12B | $15.6 Billion |

Exit Value (M&A/IPO) | $5.6 Billion | $13.4 Billion | $58.8 Billion |

New Startups Founded | ~622 | ~400-500 | Lower than 10-year avg |

The surge in fundraising to $15.6 billion in 2025, a 24% increase over 2024, was heavily concentrated in late-stage companies and specific verticals. Cybersecurity and enterprise software dominated the landscape, accounting for 60% of all capital raised in 2025. This concentration highlights a flight to maturity, as global investors prioritized proven Israeli scale-ups over early-stage ventures. The number of new startups founded in 2024 dropped to approximately 500, nearly half the annual average of the previous decade, signaling a potential long-term bottleneck in the innovation pipeline.

Tactical Adaptation and Human Capital Management

The most immediate challenge for Israeli startups was the mobilization of approximately 15% to 20% of the tech workforce for military reserve duty. This sudden loss of key personnel, often including founders and C-suite executives, forced a radical reorganization of operational workflows to ensure business continuity for global clients.

Distributed Leadership and Redundancy Protocols

Startups adapted by implementing distributed leadership models, shifting critical responsibilities to international offices or non-reserve team members. Where individuals were unavailable, the ecosystem facilitated a "swift handover" process, often supported by industry veterans who volunteered to oversee operations for smaller companies. This collective mobilization within the tech community was essential for maintaining service-level agreements and meeting product development deadlines despite the workforce shortfall.

Evidence suggests that the shift toward remote work, a legacy of the COVID-19 pandemic, provided the necessary infrastructure for this adaptation. Companies leveraged their global footprints to ensure redundancy, with R&D tasks being reallocated to teams in Europe or the United States. For companies with a primarily domestic workforce, the "No Matter What" ethos became a operational standard, where employees remaining on the home front often worked double shifts to cover for those in uniform.

The Role of Military Experience in Corporate Resilience

The unique relationship between the Israel Defense Forces (IDF) and the tech sector provided a structural advantage. Elite intelligence units like 8200 have long functioned as incubators for tech leadership, instilling a culture of adaptive thinking and decision-making under extreme ambiguity. During the war, this "military-to-civilian" talent flywheel was tested in reverse. As career officers exited the military during periods of stagnation or budget cuts, they brought startup-honed skills in rapid iteration and crisis management back to the front lines, creating a reciprocal loop of innovation.

However, the prolonged nature of the conflict led to concerns about "reserve duty fatigue." Some reports indicated that retention of career officers in technical roles fell from 83% in 2018 to 63% by 2024, creating a shortage of mid-level commanders. For startups, the repeated call-ups of essential personnel led to delays in product milestones and an inability to meet some development targets, prompting 33% of firms to report significant daily operational disruptions.

Global Communication Strategies and the Resilience Brand

To counter the perception of risk associated with a war zone, the Israeli tech ecosystem launched a coordinated public relations effort. The "Israeli Tech Delivers No Matter What" campaign was designed to signal reliability to international investors and partners. This messaging emphasized that the sector is a mature, globally integrated engine that remains operational regardless of security challenges.

The success of this strategy is reflected in the continued dominance of American acquirers and investors. In 2025, U.S. buyers led 51% of all M&A deals in the Israeli ecosystem. Major global entities, including Google, NVIDIA, and Johnson & Johnson, continued to execute significant acquisitions, reinforcing the belief that the "Israeli Tech" asset class is fundamentally resilient. NVIDIA's announcement in late 2025 to create a massive R&D center in Northern Israel, capable of hosting 10,000 employees, serves as a cornerstone of this returning confidence.

Communication Tactics for International Partners

Analysis of crisis communication playbooks suggests that successful startups prioritized transparency and frequent updates with their global stakeholders. Key tactics included:

Establishing clear redundancy plans and sharing them with clients to prove that service would not be interrupted.

Leveraging "innovation diplomacy" to frame Israeli tech as a strategic asset for regional stability and normalization, particularly with Gulf States.

Utilizing digital platforms to document business-as-usual operations, such as reaching development milestones or closing sales, to overshadow the martial narrative.

The Defense Technology Pivot and Dual-Use Innovation

A primary structural shift triggered by the war is the rapid expansion of the DefenseTech sector. Between July 2024 and April 2025, the number of startups in the defense sector nearly doubled to 312. This surge was fueled by an immediate operational need for technologies related to drone warfare, AI-driven intelligence, and military medicine.

MAFAT and the Accelerated Procurement Cycle

The Ministry of Defense's Research and Development Department (MAFAT) fundamentally altered its engagement model with the startup ecosystem. By implementing a "green track" that reduced bureaucratic barriers, MAFAT allowed early-stage companies to test and deploy products in active combat scenarios. In 2025, approximately 50% of the defense ministry’s deals were with early-stage companies (pre-seed and seed), a departure from the historical reliance on large defense contractors.

MAFAT Engagement Detail (2025) | Statistic |

Total Startup Order Volume | NIS 1.08 Billion |

Orders Directed to R&D | 35% |

Orders Directed to Equipment | 41% |

Startups Under Contract | 152 |

Total Funding Raised by MAFAT Startups | $1.2 Billion |

This "battle-tested" validation has significant implications for global markets. Israeli startups contracted with MAFAT saw orders from foreign customers jump to NIS 297 million in 2025, as countries like Germany and those in the Gulf sought combat-proven defense technologies. The war has effectively turned the Israeli landscape into a live laboratory for dual-use innovation, where technologies developed for the front line—such as autonomous navigation or remote medical triage—are being rapidly adapted for civilian applications in logistics and health tech.

Relocation Trends and the Globalization of Operations

While resilience has been the primary narrative, the reality of prolonged conflict has driven a significant portion of the ecosystem to diversify its geographic footprint. Approximately 20% of Israeli tech firms moved some operations or personnel abroad during the war. This relocation is often not a total exit but a strategic move to ensure continuity in fundraising and customer management.

Cyprus and Greece as Strategic Safe Harbors

Cyprus has emerged as a leading destination for Israeli startups seeking to protect their personnel and maintain operations with minimal disruption. The island's proximity, favorable tax system, and simplified hiring processes for non-EU software engineers make it an attractive logistical hub. The Cypriot government's Business Facilitation Unit (BFU) provides a "one-stop-shop" for Israeli companies to register and relocate their teams.

Relocation Factor (Cyprus) | Benefit to Israeli Startups |

IP Effective Tax Rate | As low as 2.5% |

Corporate Tax Rate | 5% (Standard) |

Dividend/Capital Gains Tax | 0% |

Regulatory Environment | Minimal state intervention |

Proximity | 40-minute flight from Tel Aviv |

Beyond Cyprus, Israeli firms have expanded their workforce in Europe by an average of 5% annually during the war. As of early 2025, over 1,600 Israeli tech firms were operating in Europe, with the UK, Germany, and Ukraine serving as primary hubs. This geographic expansion is increasingly viewed as a necessary form of "insurance" against domestic volatility and flight restrictions, which hindered travel and capital raising for 75% of surveyed firms.

The Palestinian Tech Ecosystem: Resilience in the Face of Collapse

The impact of the war on the Palestinian tech sector has been catastrophic, yet it has also revealed an extraordinary level of individual and collective resilience. By late 2024, the GDP of the Palestinian territories had fallen by approximately 26% to 28%. In Gaza, the economic halt was near-total, with an 86% decline in GDP during the first half of 2024.

The Shift to a Resistance Economy

Despite the destruction of nearly all physical banking and telecommunications infrastructure in Gaza, the Palestinian tech community has pivoted toward a "Resistance Economy" model. This approach leverages the digital world to bypass physical borders and movement restrictions. Palestinian freelancers and developers have increasingly focused on global online platforms like Upwork, providing high-value niche services such as software programming, translation, and digital marketing.

Hope Hubs and Digital Infrastructure Adaptation

A critical adaptation in Gaza has been the establishment of "Hope Hubs"—provisional co-working spaces equipped with solar panels and satellite internet. One example is the TAQAT hub in Deir al-Balah, founded in April 2024. TAQAT provides young freelancers with the reliable electricity and Wi-Fi necessary to fulfill international contracts while living in displacement camps. These hubs are more than offices; they are seedbeds for social cohesion and economic hope in a landscape of rubble.

Evidence from Gaza Sky Geeks (GSG), a leading Palestinian tech hub, shows that before the war, graduates generated over $20 million in online income annually. While the conflict forced GSG to suspend some activities, the organization has since expanded its training programs in the West Bank and is developing revival plans for Gaza, focusing on upskilling youth in high-demand fields like AI and data analytics.

The Adoption of Digital Wallets and Financial Resilience

The destruction of 56 bank branches and 94 ATMs in Gaza, combined with Israel’s refusal to allow cash transfers, created a total banking collapse. In response, the Palestinian Authority and the PMA introduced the iBURAQ instant payment system in mid-2024. This digital wallet infrastructure has become a primary rail for receiving wages and humanitarian assistance.

Digital Financial Metric (Gaza) | January 2025 | June 2025 |

Active Digital Wallet Users | ~400,000 | >790,000 |

Total Balance in Wallets (USD) | $40 Million | $115 Million |

Total Transactions (iBURAQ) | N/A | 2.8 Million |

Total Transaction Value (USD) | N/A | $550 Million |

This shift toward digital liquidity is a vital adaptation for Palestinian freelancers and startups, allowing them to participate in the global economy even when the local formal economy has effectively ceased to exist.

Emergency Funding and Ecosystem Support Networks

The volatility of the conflict led to the creation of several public and private emergency funds designed to prolong the runway of startups with short cash horizons. In Israel, the Innovation Authority launched a NIS 400 million rapid grant fund in late 2023, while private initiatives like "Iron Nation" and "SafeDome" were established to fill gaps in early-stage funding.

Comparison of Emergency Funding Initiatives

Initiative | Founding Entity | Targeted Support | Funding Mechanism |

IIA Fast Track | Government | Companies with assets & short runway | Rapid grant w/ private match |

Iron Nation | Private VC | Early-stage startups (Seed/Series A) | Impact fund, up to $600k/startup |

SafeDome | Angel/VC | Pre-seed/Seed startups | Emergency bridge funding |

Ibtikar Fund II | International | Early-stage Palestinian startups | $3M EBRD investment in West Bank |

SAFE Palestine | Intersect Hub | West Bank fintech/tech startups | $5M bridge financing facility |

In the Palestinian context, support has been largely donor-backed and focused on human capital. The "Palestine Launchpad with Google" program, relaunched in May 2024, provides nanodegrees in AI and web development to bridge the gap between education and global industry needs. Meanwhile, "Tech for Palestine" has emerged as a decentralized incubator, supporting over 80 projects that build ethical tech alternatives and community-powered platforms for navigating West Bank checkpoints.

Long-term Structural Risks and the "Next Leap"

As the ecosystems move toward 2026, the primary challenge remains the erosion of the innovation funnel. While Israeli fundraising has rebounded, the decline in new startup creation and the sharpness of the drop in local venture capital fundraising—down 80% from its 2022 peak—raises concerns about long-term competitiveness. The average size of Israeli VC funds has dropped to $60–65 million, compared to $90 million in previous years, a decline that is steeper than in the U.S. or Europe.

For Palestinian startups, the "Next Leap" involves moving from survival to sustainable scaling. The "test local, scale regional" model has proven effective, with edtech and fintech firms successfully expanding into Jordan and the Gulf. However, the continued dependence on fragile infrastructure and the risk of correspondent banking collapse remain significant threats to stability.

Conclusion

The adaptation of startups during the Israel-Hamas war has demonstrated a fundamental truth of modern innovation: technology is a critical pillar of national resilience that can operate across borders and through crises. The Israeli ecosystem has evolved into a "scale-up powerhouse," leveraging its defense expertise and global maturity to attract record capital despite unprecedented human and operational costs. Simultaneously, the Palestinian tech community has forged a model of digital independence, using solar power and digital wallets to maintain connectivity and hope in a landscape of economic devastation.

The future of these ecosystems will be defined by their ability to maintain talent and innovation diversity. In Israel, the focus must return to rebuilding the early-stage funnel and preventing a permanent "brain drain" to relocation hubs like Cyprus. In the Palestinian territories, the priority remains the reconstruction of physical infrastructure and the stabilization of the digital financial rails that have become a lifeline for its youth. For both, the war has proven that while markets may be volatile, the ingenious capacity of the startup mindset remains the most resilient asset in the Eastern Mediterranean.