How Sanctions from Recent Conflicts Are Killing Startups

March 18, 2026 by Harshit Gupta

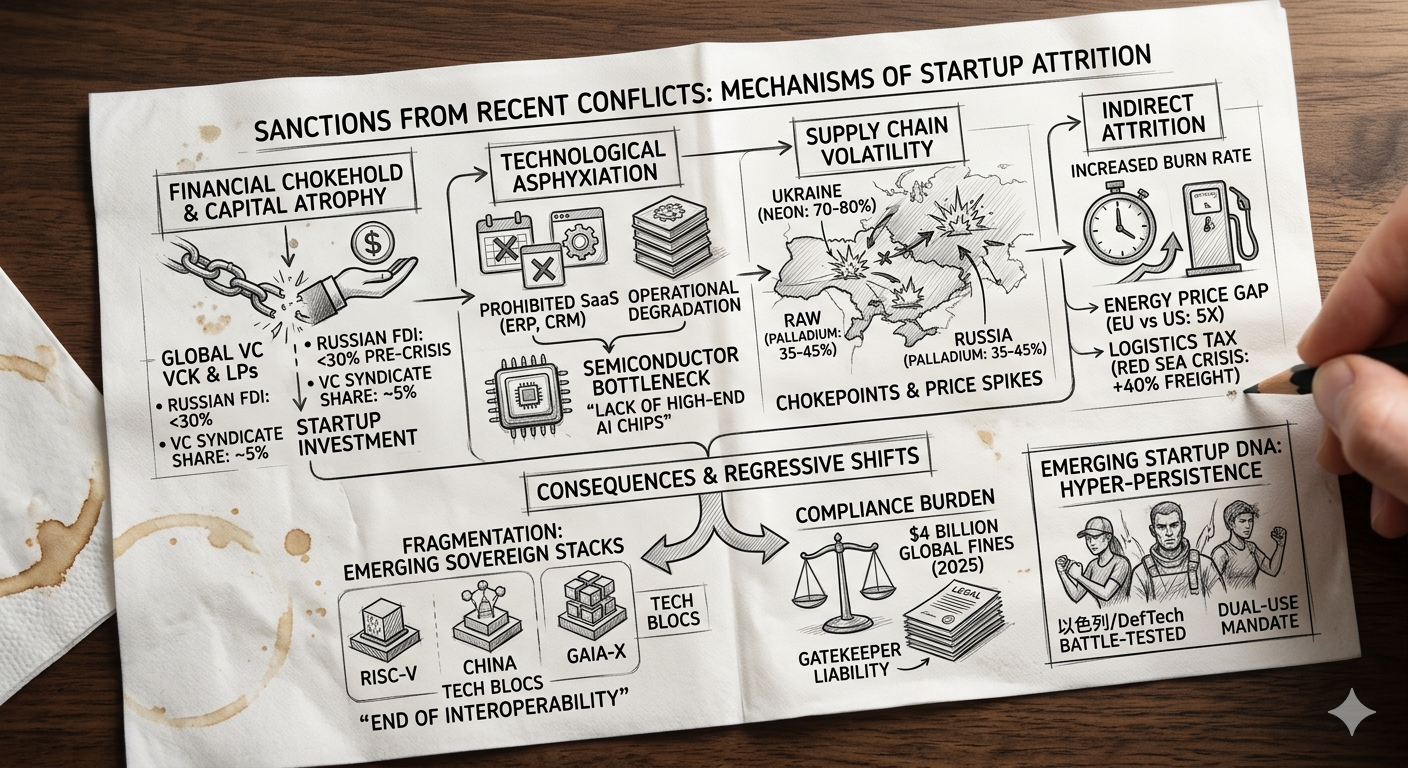

The contemporary global economic order is undergoing a structural transformation characterized by the transition from hyper-globalization to a period of fragmented "fortress economies." Central to this shift is the deployment of comprehensive sanctions regimes as the primary instrument of statecraft in response to recent conflicts, most notably the Russian invasion of Ukraine and rising tensions in the Middle East and the Indo-Pacific. While these measures are designed to degrade the military-industrial base of adversary states, their second- and third-order effects have created a hostile environment for the global startup ecosystem. Startups, which historically thrived on the frictionless flow of capital, talent, and technology, now face an existential crisis. The combination of financial disconnection, aggressive export controls, soaring compliance costs, and supply chain volatility is effectively "killing" startups across both sanctioned and non-sanctioned jurisdictions. This report analyzes the multifaceted mechanisms through which these sanctions are dismantling innovation hubs, hollowing out venture capital (VC) markets, and forcing a regressive shift toward sovereign, non-interoperable technology stacks.

The Financial Chokehold: Capital Atrophy and the Death of Sanctioned Startups

The most immediate impact of recent sanctions has been the abrupt cessation of capital flows into conflict-affected regions. The comprehensive disconnection of major financial institutions from the SWIFT messaging network and the freezing of sovereign assets have not only paralyzed state-led innovation but have also decimated the private venture capital lifecycle. Startups in Russia and Belarus, which once viewed the global market as their primary growth engine, are now trapped within a closed financial loop characterized by distressed valuations and a total lack of exit opportunities.

The Collapse of the Russian Venture Capital Lifecycle

Prior to 2022, the Russian startup ecosystem was moving toward deep integration with Western markets. Founders routinely incorporated in jurisdictions such as Delaware, London, or Cyprus to attract international LPs and facilitate exits via US or European stock exchanges. This model has entirely collapsed under the weight of unprecedented sanctions. Outward foreign direct investment (FDI) from Russia fell by over 50% in 2022 and has remained at just 10% to 30% of pre-crisis levels throughout 2023 and 2024. This withdrawal of capital is not merely a quantitative decline; it represents a qualitative shift in the "DNA" of the startup. Instead of building for global scalability, Russian firms are now forced to align with state-mandated import substitution projects, which prioritize national security over commercial viability.

The domestic venture market has become an "early-stage valley" where capital is scarce and risks are high. Early-stage projects must rely on a shrinking pool of business angels, while later-stage startups that survive are often acquired by domestic corporations at depressed prices. This dynamic has created an unconventional structure where corporations focus on acquiring mature startups rather than fostering a competitive VC ecosystem. Furthermore, high domestic interest rates have made risk-free bank deposits more attractive than tech investments, effectively starving the innovation sector of private capital.

Metric | Pre-2022 Status | 2024-2025 Status |

Russian Outward FDI | Strategic Expansion | 10–30% of Pre-Crisis Levels |

Primary Startup Exit | Western IPO / Global M&A | Domestic Corporate Acquisition |

VC Syndicate Share | Growing / Integrated | ~5% Market Share |

Interest Rate Environment | Moderate / Investment-Friendly | High / Risk-Averse |

The GVA Capital Precedent and Gatekeeper Liability

The financial impact of sanctions extends far beyond the borders of sanctioned states. A critical development in 2025 was the pivot by the Office of Foreign Assets Control (OFAC) toward "gatekeeper liability," targeting the venture capital firms and professional intermediaries that provide the infrastructure for startups. The enforcement action against GVA Capital, a San Francisco-based venture firm, serves as a landmark case. GVA Capital was hit with a $215 million penalty—accounting for approximately 81% of all OFAC penalties in 2025—for knowingly managing and deploying capital connected to sanctioned persons.

This action signals a new era of "regulatory terror" for the VC industry. Startups in neutral or Western jurisdictions are finding their funding rounds collapsed because of "radioactive" capital. If a single limited partner (LP) in a fund is designated, the entire fund’s portfolio becomes subject to intense scrutiny, and in many cases, the startups themselves are forced into liquidation or fire sales as they can no longer clear payments or attract follow-on investment. OFAC has explicitly rejected "form over substance" in these cases, emphasizing that compliance obligations extend beyond formal corporate boundaries to include the interrogation of indirect touchpoints with sanctioned parties.

Technological Asphyxiation: Export Controls and the SaaS Dark Age

While financial sanctions cut off the "blood" of startups, technology-specific export controls act as a form of "asphyxiation," denying firms the digital tools and hardware necessary to function. The modern startup is inherently a digital entity, built on a stack of US and European services. The recent expansion of sanctions has targeted this very substrate.

The Systematic Removal of Business Software

In mid-2024, the United States implemented sweeping restrictions on the provision of information technology (IT) and software services to the Russian Federation. This policy, which took full effect in September 2024, prohibits the export, re-export, or sale of a wide array of mission-critical software. For a startup, the loss of these tools is catastrophic, as there are often no equivalent domestic solutions that offer the same level of integration and reliability.

Software Category | Prohibited Services (US to Russia) | Operational Impact |

Enterprise Resource Planning (ERP) | Financial and operational data management | Loss of real-time resource tracking |

Customer Relationship Management (CRM) | Sales and marketing automation | Regression to manual lead management |

Business Intelligence (BI) | Data analytics and forecasting | Inability to perform advanced modeling |

Supply Chain Management (SCM) | Logistics and inventory control | Disruption of "just-in-time" operations |

Computer-Aided Design (CAD) | Engineering and industrial design | Stunting of hardware/R&D cycles |

Startups in sanctioned regions are being forced to accept a "technological downgrade." Migrating from globally supported systems like Oracle or SAP to domestic alternatives often results in performance degradations of up to 50%. Furthermore, the lack of official tech support and the inability to receive security patches have made these domestic systems highly vulnerable to cyber-attacks and technical failures, effectively shortening the lifespan of any tech-dependent firm.

The Semiconductor Bottleneck and the Failure of Import Substitution

For startups in the hardware, AI, or robotics sectors, the "semiconductor catastrophe" is the primary cause of firm attrition. Russia remains fundamentally dependent on Western-designed chips, and the global ban on selling advanced semiconductors has de facto locked domestic startups out of the AI and supercomputing race. While the Russian government has pushed for "import substitution," the reality is that the country lacks the industrial base to produce cutting-edge microelectronics.

Startups are attempting to survive through "parallel imports"—routing chips through intermediaries in countries like China, Hong Kong, or Turkey. However, this "gray market" approach introduces extreme volatility. Prices for basic components have surged, and the lack of a reliable supply chain prevents startups from scaling production. The US Department of Commerce has countered these workarounds using the "Foreign Direct Product Rule" (FDPR), which extends sanctions to any company worldwide that uses American technology or software to produce its goods. This has effectively "scared off" many potential suppliers in third countries, leaving startups with empty inventories and halted R&D cycles.

Supply Chain Volatility: The Neon-Palladium-Antimony Nexus

The impact of conflict-induced sanctions is not confined to the primary belligerents. Startups globally are being "killed" by the collateral damage to the supply chains of critical raw materials. The concentration of certain minerals in conflict zones has created a series of "choke points" that disproportionately affect small, lean startups that lack the bargaining power of multinational giants.

The Neon Scarcity and the Global Chip Shortage

Ukraine historically provided 70% to 80% of the global supply of semiconductor-grade neon. Neon is essential for deep-ultraviolet (DUV) lithography, the laser-based process used to carve patterns into silicon wafers. The destruction of neon purification facilities in Mariupol and the suspension of operations in Odesa triggered a massive supply shock.

While major chipmakers like TSMC and Intel maintained significant reserves, smaller semiconductor startups and electronics firms were hit by price spikes and delivery delays. For a hardware startup with a limited cash runway, a 600% increase in the price of an essential input is often enough to trigger a pivot or bankruptcy. Efforts to diversify neon production have begun in China and the US, but these facilities take years to become commercially viable and certified for high-purity semiconductor use.

Palladium, Antimony, and the Clean-Tech Crunch

The volatility extends to other critical minerals. Russia produces 35% to 45% of the world’s palladium, a key component in catalytic converters and semiconductor plating. For startups in the electric vehicle (EV) and automotive tech space, the disruption of palladium supplies has delayed product launches and increased the cost of prototypes.

More recently, China’s decision to restrict exports of antimony—a mineral used in semiconductors and flame retardants—in response to Western sanctions has sent prices surging to nearly $10 times their five-year average. This "mineral war" is forcing startups to abandon cost-efficient global sourcing in favor of "friend-shoring," which, while more secure, is significantly more expensive and requires a total re-engineering of the product lifecycle.

Mineral | Key Producer | Market Share | Primary Use Case |

Neon Gas | Ukraine | 70–80% | DUV Lithography |

Palladium | Russia | 35–45% | Plating / Catalytic Converters |

Antimony | China | Dominant | Semiconductors / Defense |

Rare Earths | China | ~90% (Refining) | High-Performance Magnets |

Indirect Attrition: Energy Costs and Logistics in the European Context

In Europe, the startup ecosystem is facing a "slow death" caused by the indirect consequences of energy sanctions and logistical disruptions. The decoupling of European industry from Russian fossil fuels has introduced a persistent energy price gap that is hollowing out the continent’s innovation base.

The Burn Rate Acceleration

In 2024, EU gas wholesale prices were on average five times higher than in the United States, and industrial electricity prices were 2.5 times higher. For energy-intensive startups—such as those in biotech, material science, or large-scale AI training—this price disparity is a fundamental threat to their global competitiveness. The "burn rate" of a typical European tech startup has increased significantly, not because of growth-related spending, but because of utility and operational costs.

Furthermore, the "industrial slowdown" in Germany and other European hubs has reduced the appetite for B2B tech solutions. When heavy industry cuts power consumption by 13% because of high costs, the startups that provide the software, sensors, and efficiency tools for those industries see their customer base vanish. This has led to a stagnation in power demand, which is a leading indicator of reduced economic activity in the innovation sector.

The Logistics Tax and the Red Sea Crisis

The expansion of geopolitical conflict to the Red Sea has added a "logistics tax" to global trade. War-risk insurance premiums for shipping surged by 100%, and freight costs increased by 40%. For a hardware startup waiting for components or prototypes from Asia, these disruptions mean longer lead times and higher procurement costs. Unlike established corporations, startups do not have the logistical infrastructure or the capital to absorb these costs, leading to missed deadlines and the loss of critical market windows.

Human Capital and the Diaspora of Innovation

The most profound and long-lasting effect of sanctions and conflict is the "brain drain" that is hollowing out established tech hubs and creating a new, fragmented landscape of talent.

The Russian Exodus

The 2022-2025 period has seen the most significant exodus of skilled human capital from Russia in the last 30 years. Over 800,000 Russians have left the country, many of whom were the founders and lead engineers of the nation’s most promising startups. Data from GitHub indicates that 11.1% of Russian software developers listed a new country of residence by late 2022, and those who left were significantly more active and central to global collaboration networks than those who remained.

Country | Est. Increase in Local Devs | Key Attraction Factor |

Armenia | 42% | Visa-free / Tech Hub status |

Georgia | 94% | Geography / Ease of Setup |

Cyprus | 60% | EU access / Tax environment |

Israel | 80,000+ total arrivals | Aliyah / Mature Ecosystem |

While this diaspora has stimulated growth in countries like Armenia, Georgia, and Cyprus, it has decimated the domestic Russian tech sector. Remaining firms are struggling with a severe labor shortage, forcing them to lower job requirements and increasing the failure rate of complex technical projects. The Russian army's depletion of the labor market by 10,000 to 30,000 workers per month for the war effort has further strangled the private sector’s ability to find and retain talent.

Ukraine's Resilience and the Innovation Drain Risk

In contrast, the Ukrainian startup ecosystem has shown remarkable resilience, with over 2,600 active startups by 2024, of which 18% were launched after the full-scale invasion. However, Ukraine faces its own "innovation drain." There is a significant risk that the breakthroughs developed on the battlefield—particularly in defense tech—will be commercialized and scaled by foreign entities rather than domestic firms. Without robust intellectual property protections and the ability to retain talent post-conflict, Ukraine risks becoming a mere "pipeline" for foreign defense industries, losing the innovation economy that should underpin its long-term recovery.

The Compliance Burden: Regulatory Hyper-inflation as a Barrier to Entry

Sanctions have introduced a level of regulatory complexity that is inherently biased against small companies. For a startup, the cost of "getting it wrong" is no longer just a fine; it is the death of the company.

The $4 Billion Compliance Landscape

In 2025, global fines for AML (Anti-Money Laundering), KYC (Know Your Customer), and sanctions violations totaled nearly $4 billion. While the total value of fines fell by 18% from 2024, enforcement in Europe and Asia spiked by 767% and 44% respectively, driven by intensified scrutiny of the fintech and digital asset sectors.

For a small fintech startup, the requirement to transition from manual transaction monitoring to automated systems appropriate for their size is a massive capital expenditure. Digital asset firms are overrepresented in these fines, reflecting a sector where growth has outpaced compliance maturity. A notable 2025 case involved a UK firm fined £21 million for failing to conduct due diligence on high-risk customers, demonstrating that even "implausible addresses" in customer sign-ups are now a major regulatory risk.

The SaaS Compliance Trap

The "compliance trap" also affects traditional SaaS and software companies. OFAC’s $3.1 million settlement with a US fintech company in December 2025 was triggered not by a financial transaction, but by the customer support team providing "technical assistance" to users in Iran. This highlights a critical lesson: sanctions compliance is no longer a "legal checkbox" but an "operational control" that must be integrated into every department, from engineering to customer service. For a startup with 50 employees, the need to train and audit every support interaction against evolving sanctions lists is a burden that can stifle growth and scare away investors.

Fragmentation and the Emergence of the Sovereign Stack

The cumulative effect of these sanctions is the dismantling of the global, interoperable tech market and the rise of "sovereign" tech stacks. This "Splinternet" represents the ultimate death of the "Build Once, Deploy Everywhere" startup model.

The End of Interoperability

Sovereignty is no longer a political statement; it has become a commercial requirement. Multinational firms are increasingly being forced to localize not just their compliance, but their entire technology architecture. This means re-tooling AI workflows for different markets, using different models, training data, and hosting environments to satisfy national security requirements.

In Europe, the quest for a "sovereign tech stack" is driven by the fear of over-dependence on American hyperscalers like AWS and Microsoft Azure. According to 2025 data, 74% of Europe’s publicly listed companies rely on US-based tech for essential operations. The EU’s response—projects like GAIA-X and the AI Act—aims to foster homegrown alternatives like Mistral AI, but these efforts often introduce new layers of fragmentation that make it harder for startups to scale globally.

The RISC-V Pivot and Hardware Sovereignty

In sanctioned regions, the shift toward sovereignty is even more radical. Driven by US export controls that severed access to ARM and Intel architectures, China has executed a massive, state-backed migration to RISC-V, an open-source instruction set architecture (ISA). By 2025, Chinese firms like Alibaba’s T-Head had unveiled server-grade RISC-V processors that match the performance of Western proprietary designs.

While proponents of open-source celebrate this as a "masterstroke of jurisdictional engineering," industry analysts warn that the fragmentation of the hardware world is accelerating. Startups that once built software for a single, global hardware standard must now decide which "technological bloc" they will serve. This fragmentation limits the market for any given innovation, increases development costs, and reduces the likelihood of a startup achieving the "escape velocity" needed for a global exit.

Tech Bloc | Key Architecture | Strategic Goal | Regulatory Framework |

Western / G7 | x86 / ARM / AWS | Global Security / ESG | OFAC / GDPR / EU AI Act |

China / Russia | RISC-V / Domestic Cloud | Self-Reliance / Sovereignty | State Mandates / FDPR evasion |

Israel / DefTech | Hardened / Dual-Use | Resilience / Persistence | Military Integration |

Europe | GAIA-X / Mistral | Autonomy / Privacy | Digital Markets Act / Data Act |

The Pivot to Persistence: The New Startup "DNA"

In response to this hostile environment, the "DNA" of the successful startup is changing. The focus is shifting from "hyper-growth" to "hyper-persistence." This is most evident in the rise of Defense Technology (DefTech) and battle-tested innovation hubs.

The Israeli "Stress-Tested" Model

Israel provides a blueprint for the post-sanctions startup ecosystem. In 2025, the Israeli tech sector raised $11 billion and delivered $17.8 billion in exits despite prolonged geopolitical stress. The ecosystem has rebranded itself to global LPs as a "stress-tested allocation," focusing on AI-native infrastructure, cybersecurity, and "system hardening".

Startups in this environment are not building "edge features"; they are building "control layers" designed to operate independently of fragile global dependencies. This includes hardware-software hybrids for logistics and industrial operations, where "defense DNA" becomes enterprise-critical for global buyers willing to pay for reliability under stress.

The Rise of DefTech and the Dual-Use Mandate

The conflict in Ukraine has catalyzed a global "DefTech Frontier." Ukraine’s Brave1 platform is currently supporting over 200 AI-powered defense technologies, including autonomous "drone swarms" and battlefield intelligence systems. This surge in wartime innovation is not just about military hardware; it is about creating a "WINWIN" strategy where AI integration in the public sector and defense becomes a strategic export.

However, this shift toward dual-use and defense technology represents a fundamental departure from the "Silicon Valley" model. Startups in this space are more beholden to government contracts and national security mandates, which can limit their commercial flexibility and make them primary targets for retaliatory sanctions.

Strategic Synthesis and Outlook

The era of "startup killing" sanctions has permanently altered the landscape of innovation. The evidence gathered across multiple conflict zones and regulatory updates between 2022 and 2025 indicates that the global startup ecosystem is no longer a single, unified entity. Instead, it has bifurcated into two distinct tracks: those that thrive on global interoperability and those that survive through sovereign persistence.

Key Conclusions for the 2026 Innovation Landscape

First, the "Compliance Barrier" has become the primary filter for startup survival. The massive increase in regulatory fines and the shift toward "gatekeeper liability" mean that startups must prioritize compliance from day one, often at the expense of product development. The "GVA Capital Action" serves as a permanent warning to VCs that their role as financial intermediaries carries significant geopolitical risk.

Second, the "Mineral and Energy Wars" have exposed the fragility of the "lean" startup model. Startups can no longer assume that critical inputs—whether neon gas or high-end GPUs—will be available or affordable. This is forcing a move toward regionalized, flexible supply chains, which increases the capital requirements for any hardware-based innovation.

Third, the "Brain Drain" is redrawing the map of innovation. The exodus of developers from Russia has created new tech clusters in the Caucasus and Central Asia, but it has also introduced a layer of "geographic risk" as these new hubs remain vulnerable to regional instability.

Finally, the "Sovereign Stack" is the new reality. The end of the "Build Once, Deploy Everywhere" model means that the next generation of successful startups will be those that can navigate a patchwork of non-interoperable environments. Whether it is the RISC-V pivot in the East or the GAIA-X initiative in the West, startups must now build for specific geopolitical blocs rather than a global market.

While sanctions have undoubtedly "killed" thousands of startups through financial starvation, technological denial, and regulatory burden, they have also birthed a new, more resilient—though more fragmented—breed of firm. The startups of 2026 and beyond will be defined not by their ability to disrupt the world, but by their ability to endure it.

Want to calculate the equity for your cofounder?

Nail your cap table before you sign. Whether you're splitting equity with a co-founder or planning your next funding round, our Equity Calculator gives you precision in seconds

Equity calculator →