How Generative AI is reshaping early-stage startups

June 23, 2026 by Harshit Gupta

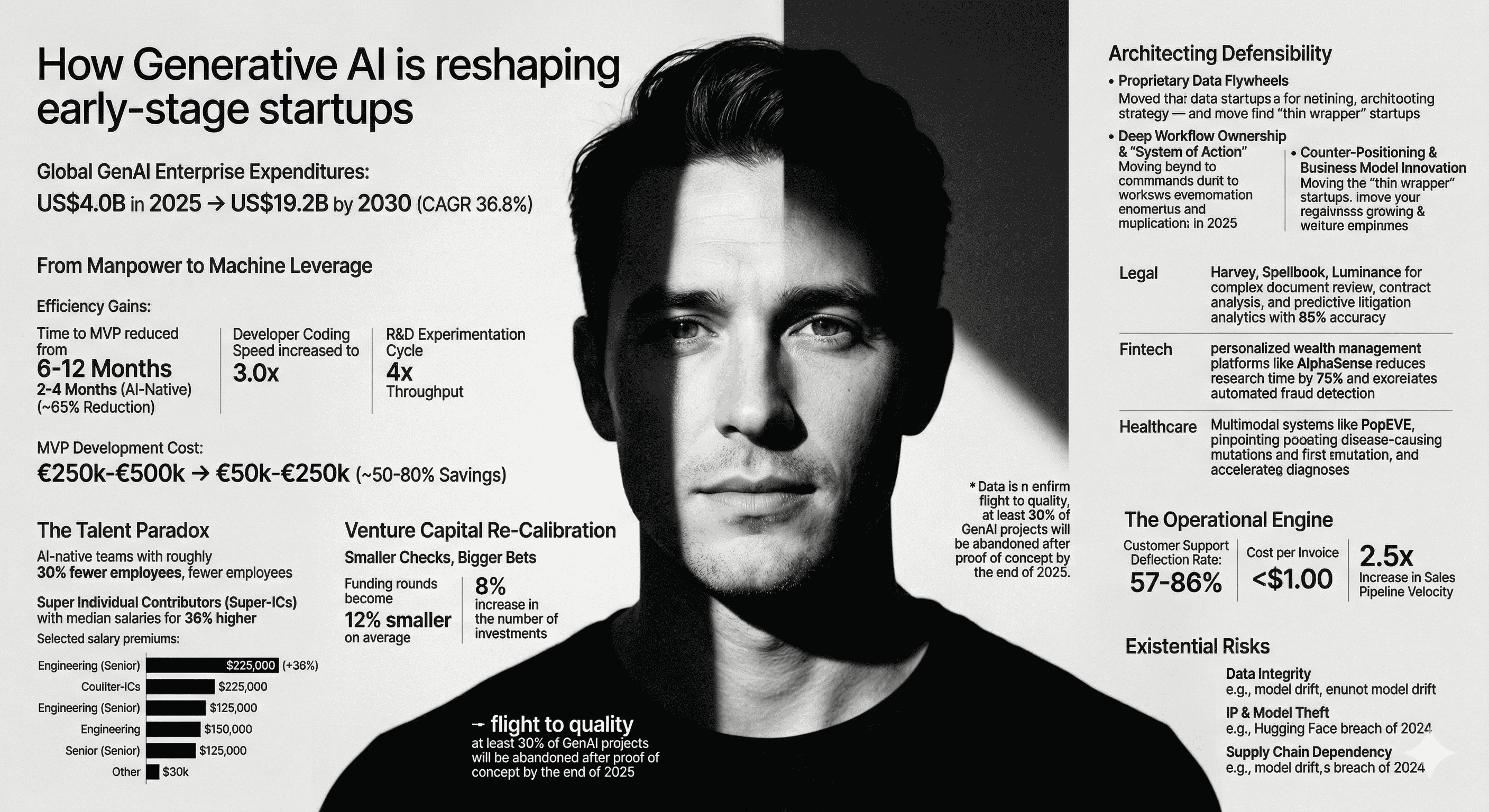

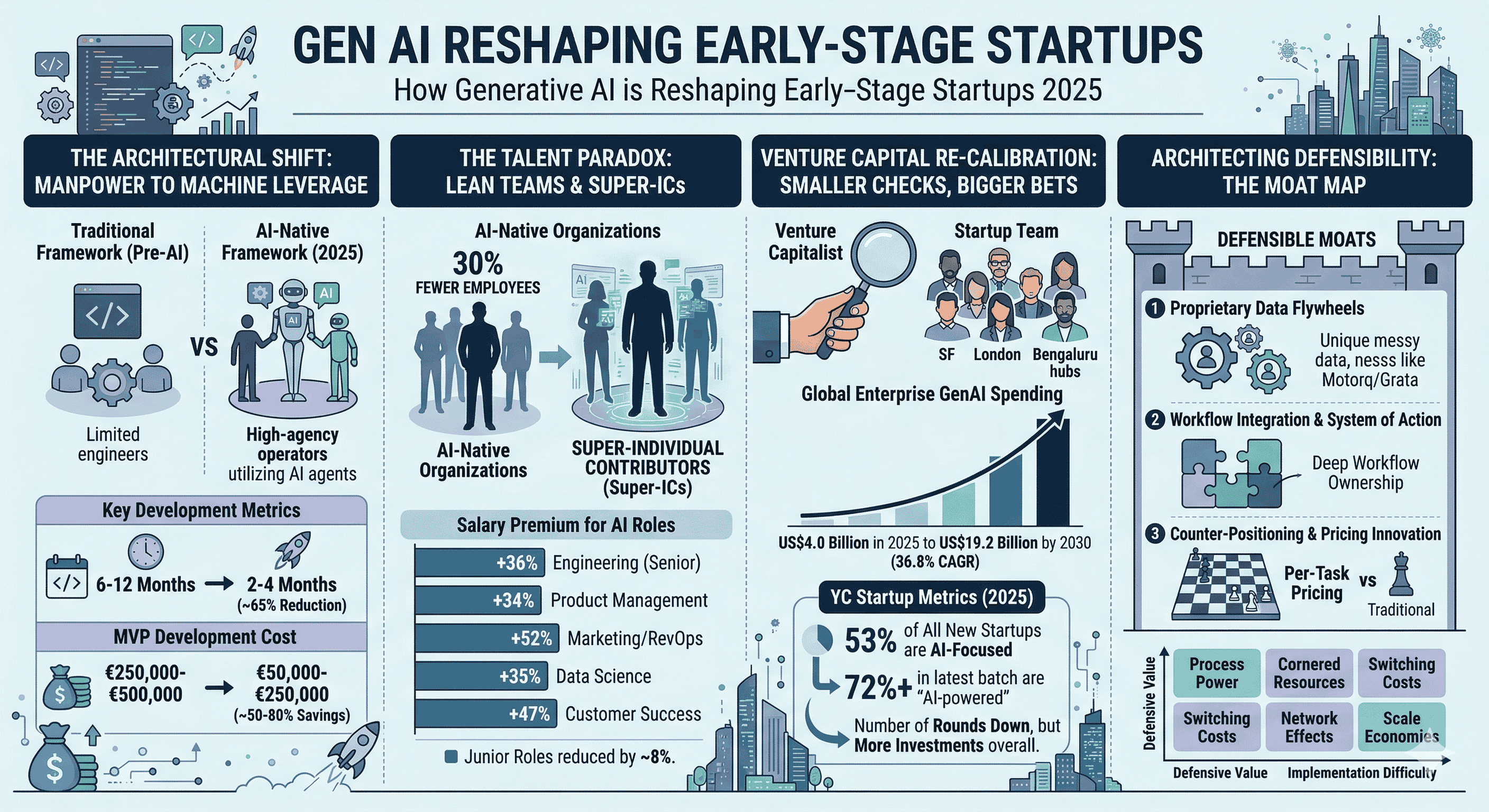

The global startup ecosystem in 2025 has reached a pivotal juncture, where the experimental fervor of previous years has matured into a disciplined structural realignment. This transformation, catalyzed by the rapid proliferation of generative artificial intelligence (GenAI), has fundamentally altered the mechanics of venture creation, the economics of engineering, and the very definition of organizational scale. As enterprises transition from fragmented pilot programs to full-scale production environments, the early-stage startup is no longer merely a vehicle for software delivery but a laboratory for cognitive automation. The current landscape is characterized by a significant surge in spending, with global GenAI enterprise expenditures projected to grow from US4.0billionin2025toUS19.2 billion by 2030, representing a compound annual growth rate (CAGR) of 36.8%. Within this burgeoning market, the early-stage startup serves as both the primary innovator and the most vulnerable participant, navigating a dual reality of unprecedented leverage and existential platform risk.

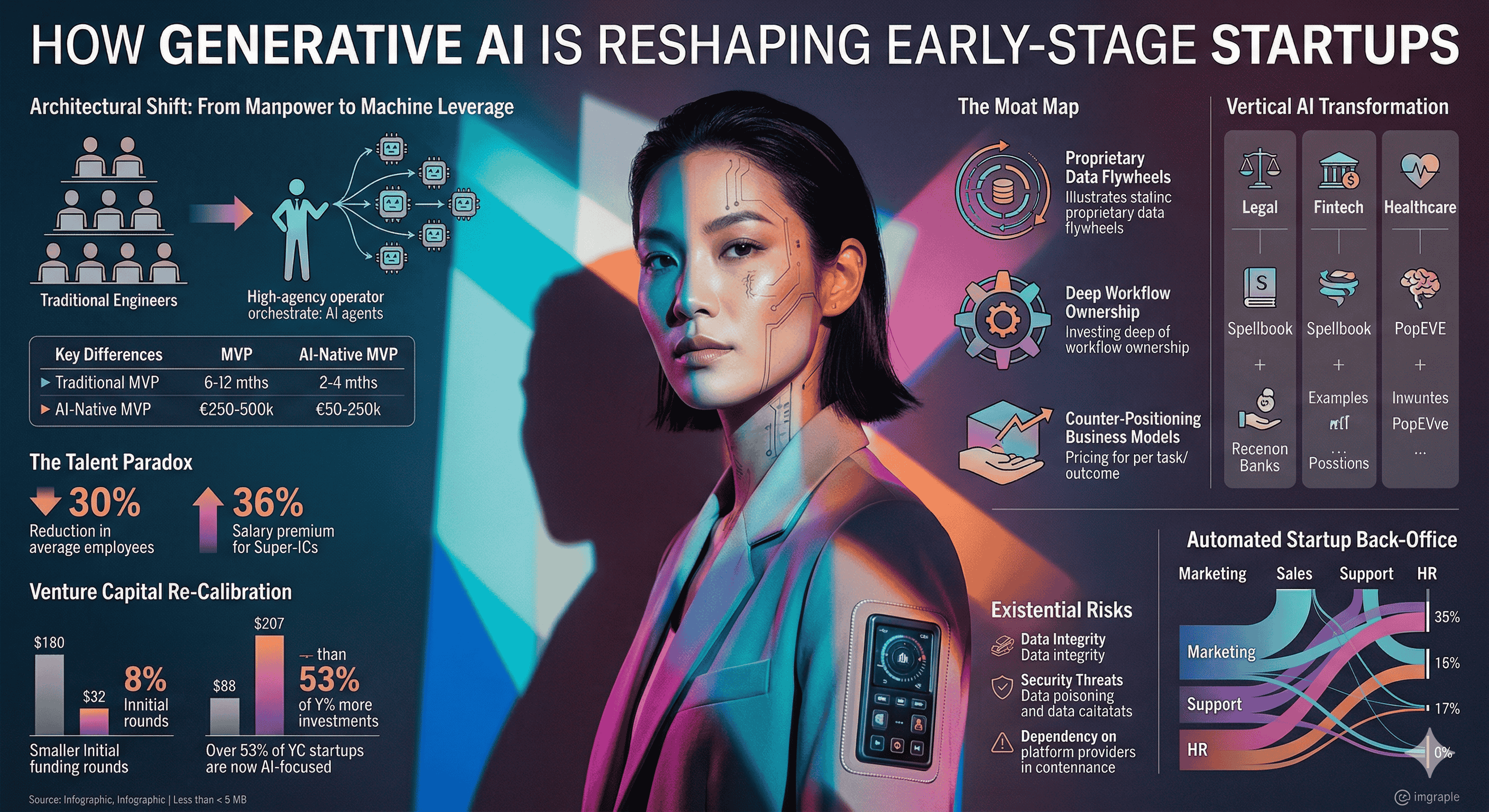

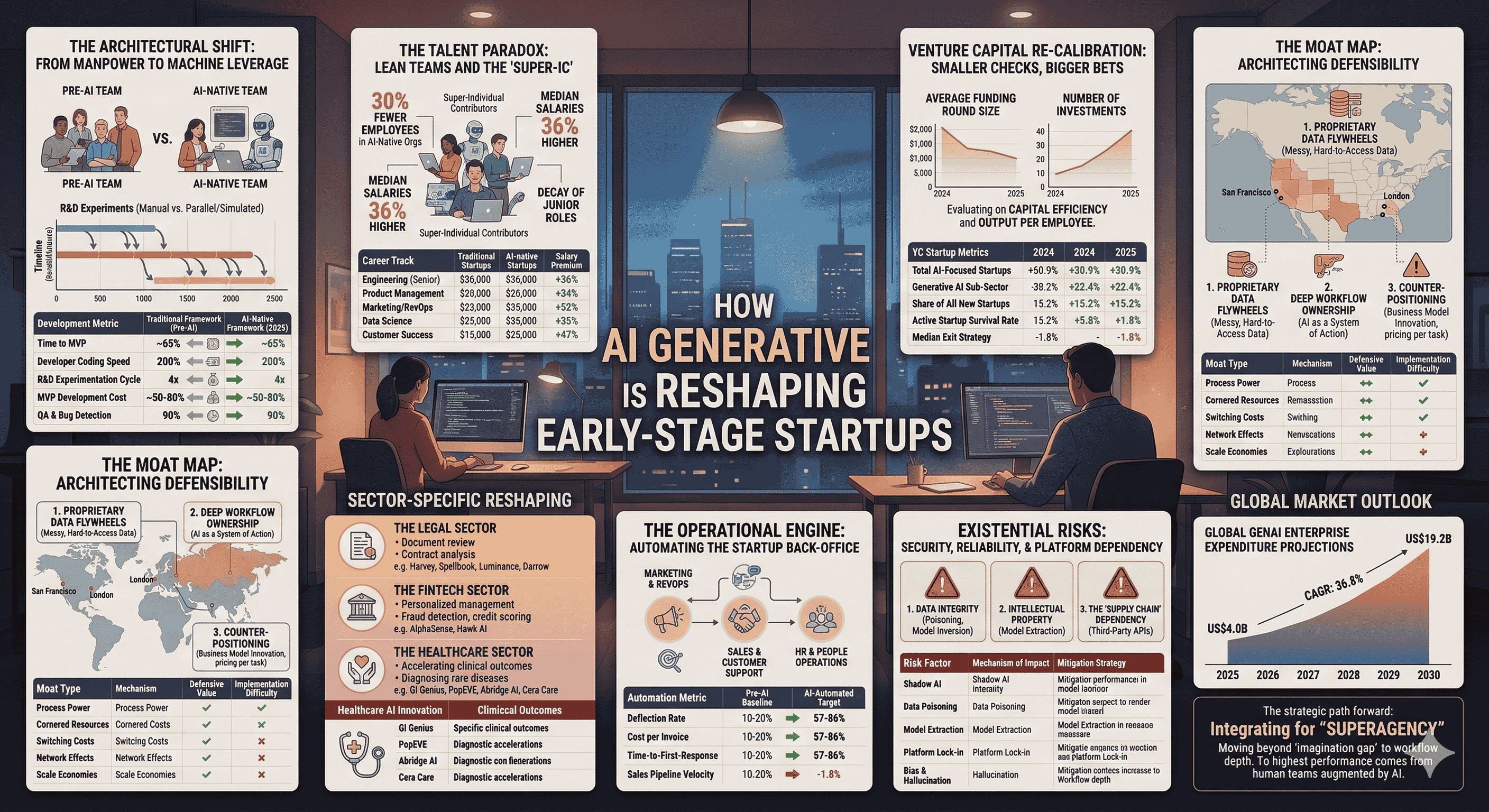

The Architectural Shift: From Manpower to Machine Leverage

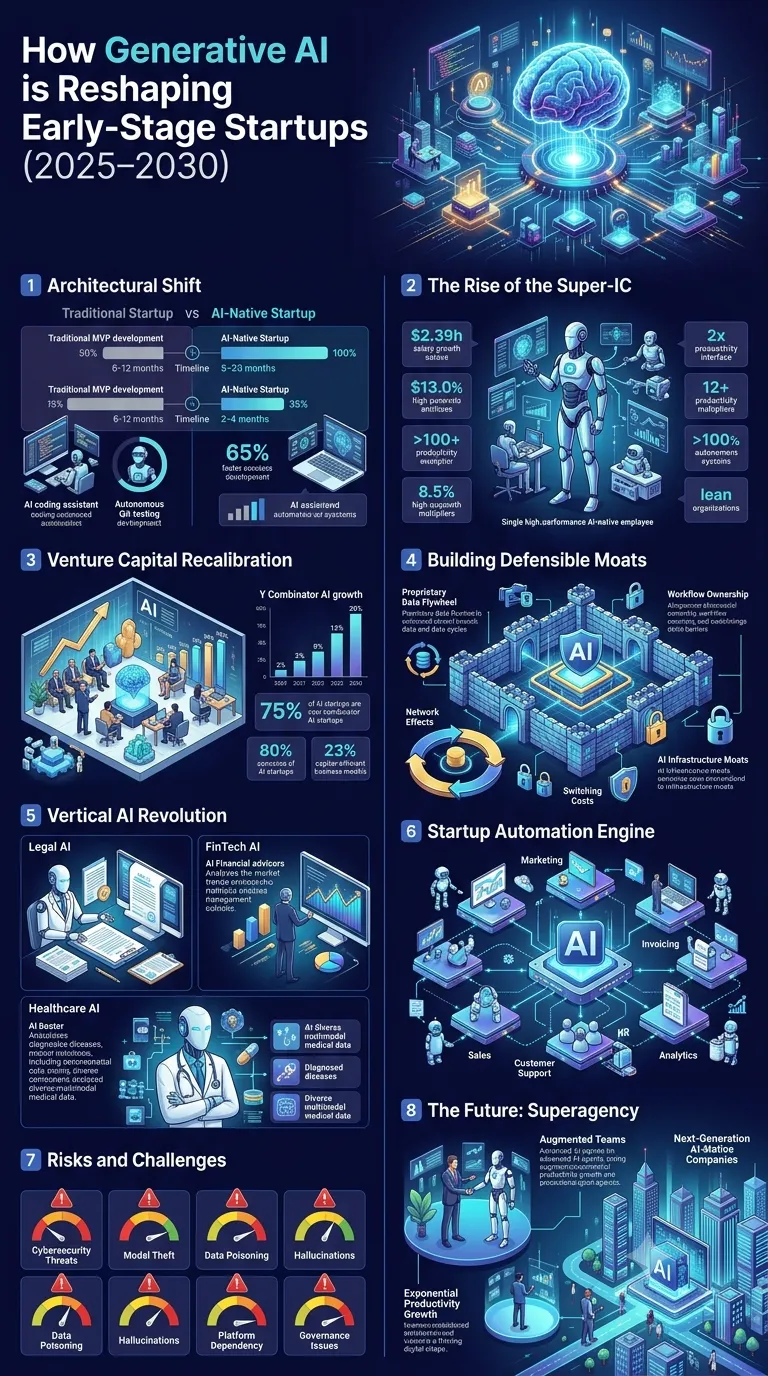

The traditional engineering-heavy model of startup development, which defined the previous two decades of Silicon Valley, has encountered an inflection point. Historically, the velocity of a startup was a direct function of its technical headcount; the more engineers a founder could hire, the faster the product could be brought to market. In 2025, this relationship has decoupled. The emergence of AI-assisted development has shifted the focus from absolute manpower to structural leverage, where the output of a single high-agency operator can rival that of an entire cross-functional team from the pre-AI era.

This shift is not merely a quantitative improvement in coding speed but a qualitative change in the R&D timeline. Generative AI tools have moved beyond simple auto-completion to autonomous simulation, allowing founders to evaluate product-market fit through AI-driven ideation before the first line of code is committed. By analyzing market signals, customer feedback, and competitor strategies, these systems eliminate the "blank-page delay" that often characterizes the early stages of venture formation. The result is a compression of experimentation cycles, where prototypes that once required weeks of manual wireframing and documentation are now generated in days.

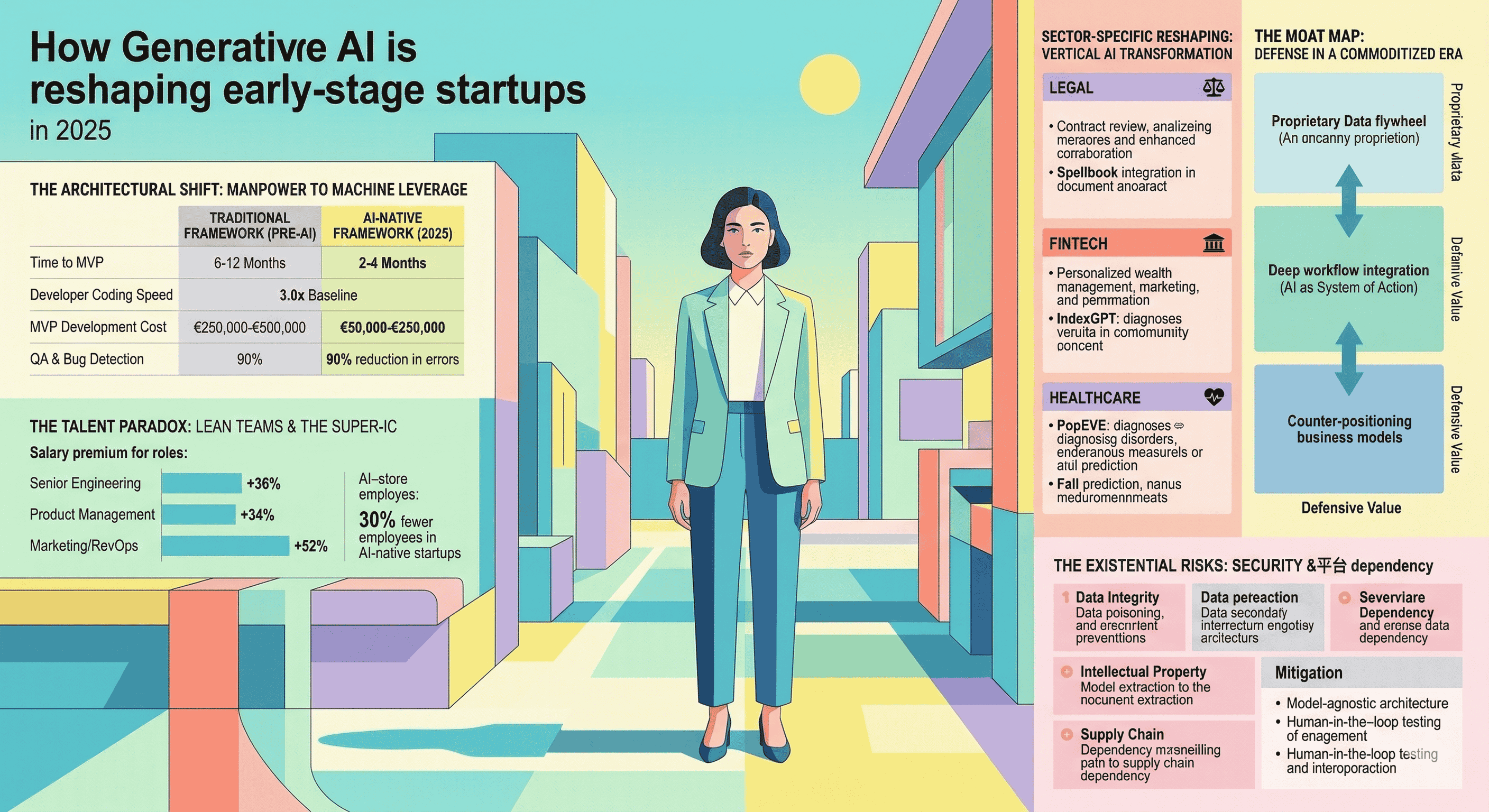

Development Metric | Traditional Framework (Pre-AI) | AI-Native Framework (2025) | Efficiency Gains |

Time to MVP | 6 - 12 Months | 2 - 4 Months | ~65% Reduction |

Developer Coding Speed | Baseline (1x) | 3.0x | 200% Increase |

R&D Experimentation Cycle | Linear/Sequential | Parallel/Simulated | 4x Throughput |

MVP Development Cost | €250,000 - €500,000 | €50,000 - €250,000 | ~50-80% Savings |

QA & Bug Detection | Manual/Automated | AI-Autonomous | 90% Reduction in Errors |

The economic implications of this shift are profound for the early-stage founder. The cost of developing a Minimum Viable Product (MVP) in the European technology ecosystem now typically ranges between €50,000 and €250,000, a significant reduction from the high-capital requirements of the previous decade. This lower barrier to entry has led to a democratization of venture creation, but it has also increased the noise in the market, forcing venture capitalists to look beyond the product itself to the underlying architecture and "learning velocity" of the team.

The Talent Paradox: Lean Teams and the "Super-IC"

As startups require fewer people to achieve the same milestones, the nature of the startup team has undergone a radical redesign. AI-native organizations in 2025 maintain roughly 30% fewer employees than traditional startups at the same stage. This lean structure is not a sign of austerity but of extreme productivity. These organizations are prioritizing "Super Individual Contributors" (Super-ICs)—operators who combine deep technical judgment with the ability to orchestrate an array of AI agents. The compensation for these roles has adjusted accordingly, with median salaries at AI-first startups reaching 36% higher than those at traditional firms.

This "Super-IC" model creates a talent paradox. While the aggregate demand for labor remains stable due to a 7% increase in the total number of active startups, the distribution of that demand is highly skewed toward senior, managerial, and high-agency roles. Junior roles, particularly those focused on execution-heavy tasks like basic debugging, documentation, or initial customer support triage, have seen a decline in demand. Research indicates that startups most exposed to generative AI have reduced employment in these junior roles by approximately 8% since the launch of frontier models like ChatGPT.

Career Track | Traditional Startup Salary | AI-Native Startup Salary | Salary Premium |

Engineering (Senior) | $165,000 | $225,000 | +36% |

Product Management | $145,000 | $195,000 | +34% |

Marketing/RevOps | $115,000 | $175,000 | +52% |

Data Science | $155,000 | $210,000 | +35% |

Customer Success | $95,000 | $140,000 | +47% |

The emergence of these lean, highly paid teams is redefining company culture. Small wins and consistent communication are becoming the bedrock of change management in these organizations, as leaders attempt to align human creativity with automated cognitive functions. However, the risk of "key-man dependency" is heightened in these environments. When a 20-person team is delivering 100-person outcomes, the departure of a single high-agency operator who understands the specific orchestration of the company's AI stack can be catastrophic.

Venture Capital Re-Calibration: Smaller Checks, Bigger Bets

The venture capital industry is adapting its investment thesis to match the shifting economics of the AI era. In 2025, investors are increasingly moving away from "headcount as a proxy for growth." Instead, they are evaluating startups based on their "capital efficiency" and "output per employee". Initial funding rounds have become approximately 12% smaller on average, but the number of investments has risen by 8%, suggesting that VCs are spreading their bets more widely across a larger number of lean, AI-enabled firms.

This trend is most visible in the 2024-2025 Y Combinator (YC) cohorts, where AI-focused startups have grown to account for 53% of all newly created entities, with over 72% of the latest batch being "AI-powered". The geographic distribution of these startups is also shifting. While San Francisco remains the epicenter with 1,330 startups, its dominance is slightly eroding as international hubs like London and Bengaluru solidify their positions, driven by the accessibility of foundational models and remote-first AI development cultures.

YC Startup Metrics | 2024 | 2025 | Percentage Change |

Total AI-Focused Startups | 871 | 1,140 | +30.9% |

Generative AI Sub-Sector | 214 | 262 | +22.4% |

Share of All New Startups | 46% | 53% | +15.2% |

Active Startup Survival Rate | 70.9% | 69.6% | -1.8% |

Median Exit Strategy | Acquisition | Acquisition | Stable |

The decline in the total number of funding rounds—down by an average of 16.7% each month in 2025 compared to 2024—reflects a more cautious and selective investment climate. Investors are no longer funding "AI for the sake of AI." Instead, they are prioritizing startups that demonstrate a clear path to return on investment (ROI) through the deployment of AI at scale. According to Gartner, at least 30% of GenAI projects will be abandoned after proof of concept by the end of 2025 due to poor data quality, escalating costs, or unclear business value, making the "flight to quality" a defining characteristic of current venture activity.

The Moat Map: Architecting Defensibility in a Commoditized Era

The primary existential challenge for the 2025 startup is the rapid commoditization of the application layer. The era of the "thin wrapper"—startups that simply provide a user interface over a public API—is effectively over. These companies, which Stanford research found comprised 41% of YC’s AI startups at one stage, are being "squeezed out" as foundational model providers like OpenAI, Anthropic, and Google move up the stack to integrate features like PDF summarization, meeting analysis, and code generation directly into their base products.

To survive, early-stage startups are employing a diverse array of strategies to build "defensible moats" on top of foundational models. These strategies often involve a combination of proprietary data, workflow integration, and counter-positioning.

1. Proprietary Data Flywheels

The most durable moat remains the "data flywheel," where more users lead to more data, which leads to better models, further attracting more users. However, in the 2025 context, the focus has shifted from "volume of data" to "proprietary, messy, and hard-to-access data". Startups like Motorq, which built direct integrations with major auto original equipment manufacturers (OEMs), or Grata, which uses proprietary M&A intelligence, demonstrate how amassing a unique dataset that is unavailable to public web-crawlers can create a compounding advantage.

2. Deep Workflow Ownership and "System of Action"

Startups that embed their AI directly into the mission-critical workflows of their users—moving from "AI as a feature" to "AI as the system of action"—create high switching costs. This involves mapping the user's entire workflow and building native integrations that eliminate manual handoffs. Once an AI tool is "wired into" a company's custom enterprise ecosystems (CRMs, ERPs, and compliance logic), replacing it would require re-tooling the entire operational infrastructure, which is often seen as a waste of time and resources by enterprise decision-makers.

3. Counter-Positioning and Business Model Innovation

Founders are increasingly using "counter-positioning" to outmaneuver incumbents. This involves adopting strategies or business models that would be self-destructive for a legacy company to copy. A prime example is pricing innovation. While legacy SaaS providers rely on "per-seat" pricing, AI-native startups are pricing per task or per outcome. Because efficient AI reduces the number of employees needed, an incumbent adopting this model would effectively cannibalize its own revenue.

Moat Type | Mechanism | Defensive Value | Implementation Difficulty |

Process Power | Production-grade reliability (the 99% accuracy challenge) | High | Very High |

Cornered Resources | Regulatory certifications/hard-to-replicate assets | Medium | High |

Switching Costs | Deep workflow integration/Consumer memory | High | Medium |

Network Effects | More users = Better models = More users | Very High | High |

Scale Economies | Large up-front capital/Infrastructure requirements | High | Very High |

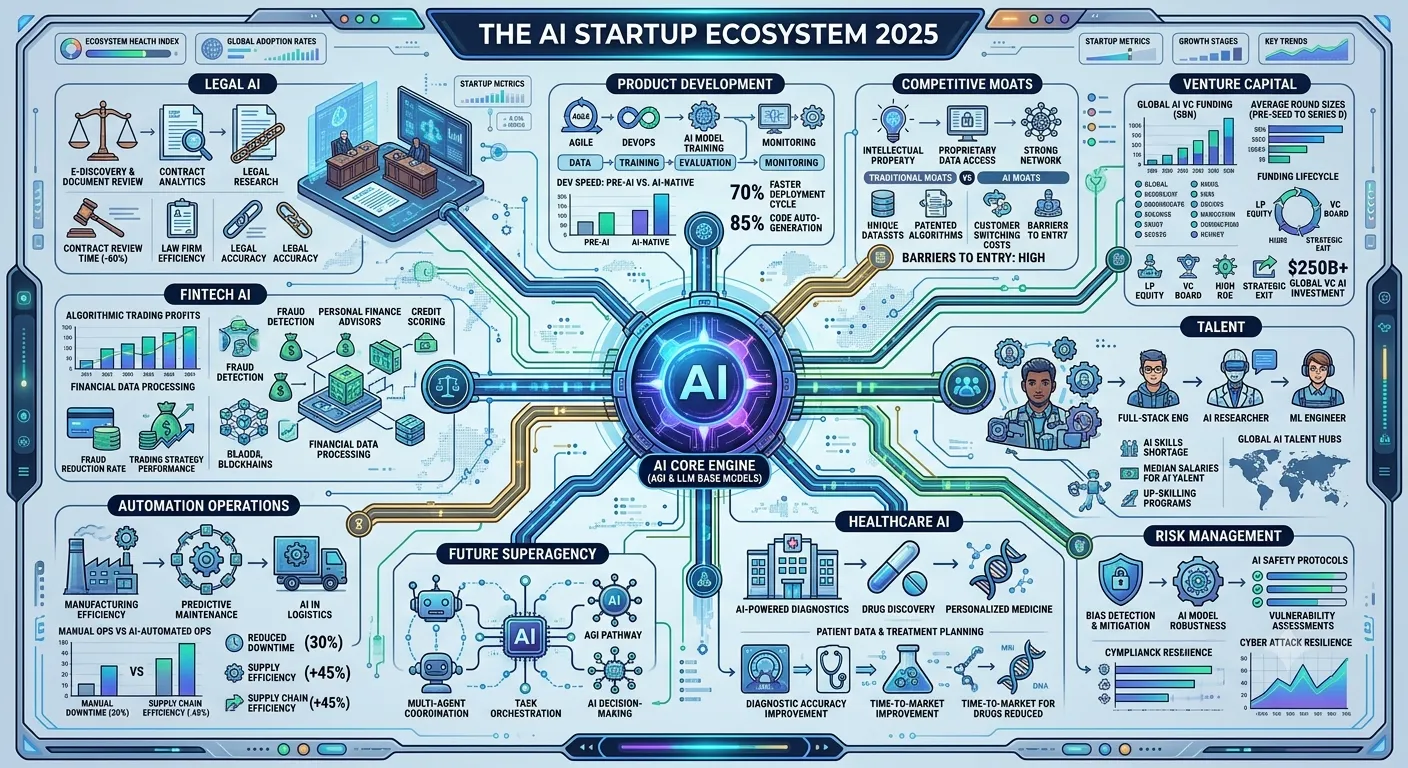

Sector-Specific Reshaping: The Vertical AI Transformation

The impact of generative AI is not uniform across all sectors. In 2025, several high-value industries are undergoing a "metamorphosis" as startups apply vertical-specific AI to solve long-standing inefficiencies.

The Legal Sector: From Research to Reasoning

In the legal profession, the adoption of generative AI has transitioned from cautious experimentation to an essential competitive requirement. AI-native legal startups are now capable of handling complex document review, contract analysis, and predictive litigation analytics with 85% accuracy or higher. Tools like Harvey, which handles research and due diligence for Am Law 100 firms, and Spellbook, which integrates GPT-powered contract drafting directly into Microsoft Word, are redefining the role of the associate lawyer.

Legal AI Tool | Primary Function | Core Strength | Market Position |

LegalOn | Contract Review | Pre-built attorney playbooks | Best Overall |

Harvey | General Assistant | Multi-practice area coverage | Elite Firms |

Luminance | M&A Due Diligence | Anomaly flagging across 100k+ docs | Specialist |

Spellbook | Contract Drafting | MS Word native integration | Drafting Leader |

Darrow | Risk Analysis | Alerting lawyers to actionable violations | Litigation Intelligence |

The American Bar Association reports that 31% of legal professionals now use GenAI personally at work, a figure expected to rise as restrictive law firm policies are lifted. The strategic shift is clear: firms are no longer asking if AI can do the work, but how they can justify a billable-hour model when AI can save up to 240 hours per year per lawyer.

The Fintech Sector: Democratizing Sophistication

Fintech startups in 2025 are using generative AI to democratize access to sophisticated financial services that were once reserved for high-net-worth individuals or large institutions. This includes personalized wealth management platforms like AlphaSense, which reduces research time by 75%, and IndexGPT by JPMorgan Chase, which identifies thematic investment baskets through automated keyword generation.

In fraud detection, startups are moving toward "Explainable AI" to monitor transactions in real-time. Hawk AI, for instance, uses machine learning to spot suspicious patterns while minimizing false positives, significantly reducing the burden on compliance teams. Furthermore, the use of generative AI in credit scoring—leveraging behavioral insights derived from smartphone metadata—is helping to provide financial inclusion for the "unbanked" or those without traditional credit histories.

The Healthcare Sector: Accelerating Clinical Outcomes

Healthcare remains one of the most high-stakes arenas for generative AI. Startups are moving from text-based models toward multimodal systems capable of analyzing images, genomics, and real-time patient vitals simultaneously. A landmark example is PopEVE, an AI model introduced in late 2025 that evaluates genetic variants to pinpoint disease-causing mutations, surfacing diagnoses for one-third of previously undiagnosed patients with severe developmental disorders.

Healthcare AI Innovation | Startup/Provider | Clinical Outcome |

GI Genius | Medtronic | Colorectal polyp detection (FDA Cleared) |

Amina (Symptom Triage) | Riseapps/Black Doctor | Diagnostic process accelerated by 65% |

AccuRhythm AI | Medtronic | Filtering heart rhythm alerts (reduced false positives) |

Ambient Scribing | Abridge AI | Real-time automated medical note generation |

Fall Prediction | Cera Care | Predicts 83% of falls in advance |

Generative AI is also transforming the "diagnostic odyssey" in rare diseases. By generating synthetic data to augment imbalanced or privacy-restricted datasets, startups can train more accurate machine learning models without compromising patient confidentiality.

The Operational Engine: Automating the Startup Back-Office

While product innovation often garners the most attention, the most immediate impact of generative AI on early-stage startups is the radical automation of core business functions. This allows lean teams to operate with the capacity of much larger organizations.

Marketing and RevOps

AI tools now handle the entire marketing cycle, from audience segmentation based on intent to dynamic content creation and ROI tracking. Startups that automate these processes report significant uplifts in conversion rates and a reduction in the content cycle time, allowing them to iterate on their go-to-market strategies in real-time.

Sales and Customer Support

The integration of AI into Sales Development and Revenue Operations has transformed CRMs from static databases into living ecosystems. Lead enrichment and buyer intent signals are updated automatically, while outreach sequences are generated and personalized in minutes. In customer support, startups are achieving "deflection rates" of 57% to 86% through intelligent chatbots, allowing their human teams to focus on complex, high-value interactions.

Automation Metric | Pre-AI Baseline | AI-Automated Target | Impact on Growth |

Deflection Rate | 10 - 20% | 57 - 86% | Drastic reduction in Support CAC |

Cost per Invoice | ~$10.00 | <$1.00 | Massive Operational Efficiency |

Time-to-First-Response | Hours | Seconds | Improved Customer NPS |

Sales Pipeline Velocity | Baseline | 2.5x Increase | Faster Revenue Realization |

Human Resources and People Operations

AI-driven tools in HR are improving talent acquisition by accelerating candidate sourcing and ranking on platforms like LinkedIn. Beyond recruitment, startups are using AI to track employee engagement sentiment and flag early signs of burnout, a critical function in high-pressure, lean startup environments. By automating repetitive tasks like document completion and scheduling, HR teams can focus on strategic workforce planning and fostering a culture of innovation.

The Existential Risks: Security, Reliability, and Platform Dependency

The reshaped startup landscape is not without its perils. The speed of AI adoption has often outpaced the development of robust security and governance frameworks, leaving early-stage firms vulnerable to a new class of threats.

1. Data Integrity and Adversarial Attacks

Startups are increasingly vulnerable to "data poisoning," where malicious actors inject corrupted data into public or shared datasets used for training. This can result in biased or inaccurate outputs that erode customer trust. Furthermore, "model inversion attacks" allow attackers to reverse-engineer sensitive training data, such as patient medical records or financial details, creating enormous liability for startups in regulated sectors.

2. Intellectual Property and Model Theft

Machine learning models represent the core intellectual property for many startups. However, competitors or cybercriminals can engage in "model extraction attacks," repeatedly querying an AI system to replicate its decision-making patterns without access to the original training data. Protecting these "cornered resources" requires sophisticated throttling, watermarking, and continuous API monitoring.

3. The "Supply Chain" Dependency

The reliance on third-party APIs (OpenAI, Anthropic, Google) introduces a systemic risk. If a foundational provider experiences a breach, as Hugging Face did in June 2024, or if they update their model in a way that changes its behavior ("model drift"), any startup built on that infrastructure can suffer catastrophic failure. Moreover, as foundational models integrate more capabilities, they risk becoming "aggregators" that squeeze out the middle layer of startups.

Risk Factor | Mechanism of Impact | Mitigation Strategy |

Shadow AI | Unauthorized employee use of personal AI tools | Strict governance & observability logs |

Data Poisoning | Intentional injection of corrupted training data | Data verification & anomaly detection |

Model Extraction | Reverse-engineering IP via API queries | Query throttling & output watermarking |

Platform Lock-in | Dependence on a single model provider's API | Model-agnostic/Hybrid architecture |

Bias & Hallucination | Outputs that are legally or ethically problematic | Human-in-the-loop & rigorous testing |

The Strategic Path Forward: Integrating for "Superagency"

As the startup ecosystem matures toward late 2025 and 2026, the focus is shifting from "AI as a tool" to "Superagency"—empowering humans to unlock AI's full potential by redesigning workflows around collaborative human-AI teams. Research indicates that while individuals using AI can produce higher quality work than those without it, the highest performing results (the top 10% of innovative solutions) come from human teams augmented by AI.

This suggests that the future of the early-stage startup lies not in the complete replacement of human labor but in its radical enhancement. The "expertise silos" of the past are dissolving, as AI expands problem-solving capabilities across broader employee populations, allowing those with less technical experience to achieve performance levels comparable to specialized colleagues.

The Convergence of Ambition and Reality

The reconfiguration of early-stage startups by generative AI is an ongoing process of "Silicon Synthesis," where technical capability, organizational design, and market strategy are being merged into a single, cohesive engine of innovation. The startups that thrive in this era are those that recognize that AI is not a destination but a transformative force that demands a new kind of institutional architecture.

By moving beyond the "imagination gap," targeting strategic workflow depth, and building proprietary data flywheels, these ventures are creating competitive moats that are increasingly difficult for legacy incumbents to penetrate. However, the path is fraught with challenges—from wafer-thin margins and intense platform dependency to a labor market in a state of painful transition.

As spending on GenAI continues to scale and the technology moves from the periphery to the core of enterprise infrastructure, the distinction between "startups" and "AI startups" will eventually vanish. In the final analysis, every successful company formed in the post-2023 era will be an AI-native organization, defined by its ability to synthesize human judgment with automated intelligence to create value at a scale and velocity previously unimaginable in the history of global commerce.

Want to calculate the equity for your cofounder?

Nail your cap table before you sign. Whether you're splitting equity with a co-founder or planning your next funding round, our Equity Calculator gives you precision in seconds

Equity calculator →