Funding is a trap: The dark side of venture capital

June 23, 2026 by Harshit Gupta

The contemporary narrative of venture capital is often presented through the lens of heroic exceptionalism, where capital injections serve as the primary catalyst for transformative technological progress. However, a rigorous examination of the structural, legal, and psychological realities of the industry reveals a more precarious landscape. For a significant portion of entrepreneurs, venture capital functions not merely as a financial engine but as a sophisticated trap—a mechanism that frequently results in the erosion of founder sovereignty, the destabilization of business fundamentals, and the destruction of personal well-being. This analysis deconstructs the multifaceted "dark side" of venture capital, exploring how its inherent contradictions and misaligned incentives often lead to organizational paralysis and financial marginalization for those who participate in the system.

The Statistical Reality of Venture Attrition

The disconnect between the perceived success of venture-backed startups and their actual performance is mathematically profound. While the industry thrives on the visibility of "unicorns"—privately held companies valued at over $1 billion—research from the Harvard Business School suggests that the vast majority of venture-backed firms never return capital to their investors. This reality is obscured by a "power law" distribution, where a few massive successes compensate for a graveyard of failures.

The Survival and Profitability Disparity

When analyzing the long-term viability of venture-backed versus bootstrapped companies, the data suggests that the aggressive scaling mandates of venture capital often decrease the probability of a firm’s survival. Venture-backed firms operate under a "winner-take-all" mandate, which forces companies to prioritize rapid market capture over unit economic stability. This pressure often results in a "default dead" status, where the company cannot survive without the next infusion of external capital.

Performance Metric | Venture-Backed Startups | Bootstrapped Startups |

Five-Year Survival Rate | 10% – 15% | 35% – 40% |

Probability of Reaching Profitability | 5% – 10% | 25% – 30% |

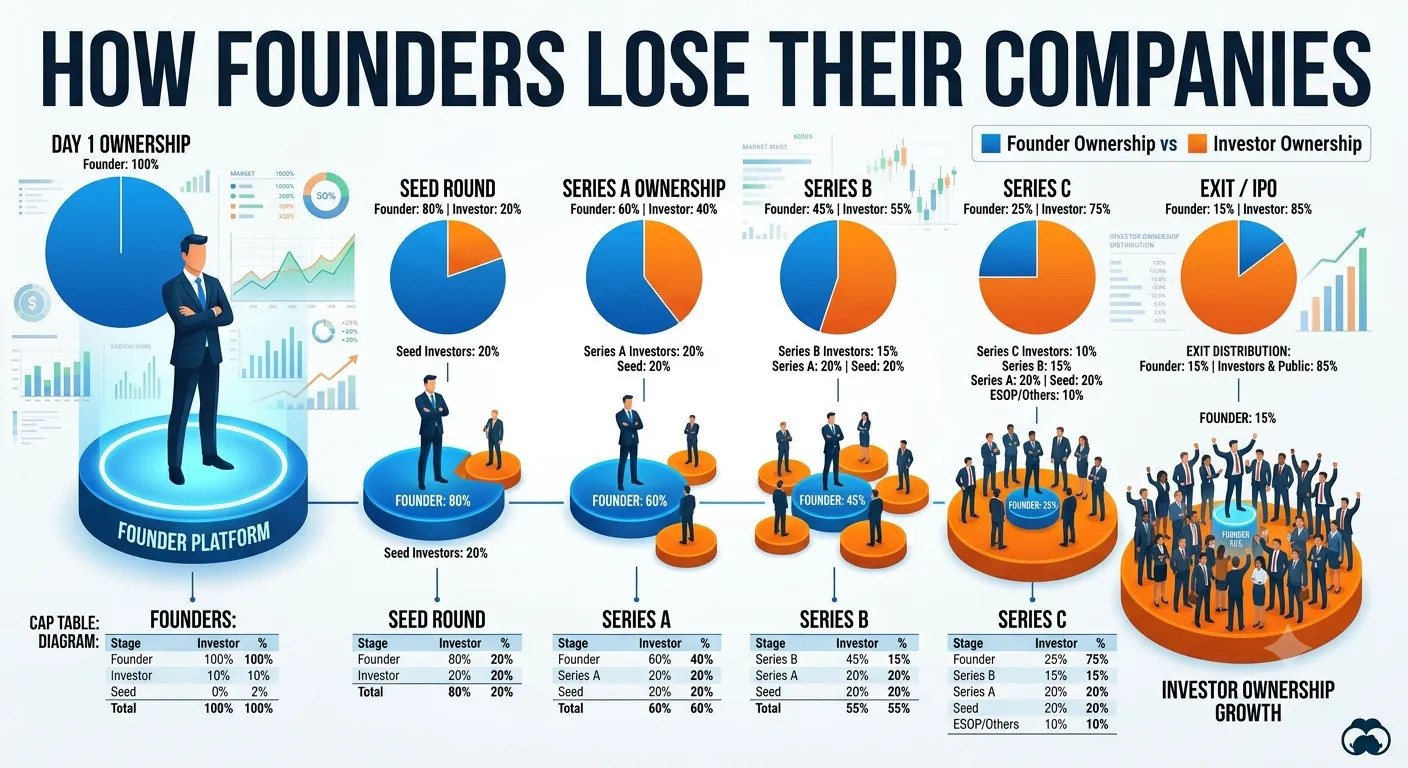

Founder Ownership at Exit (Average) | 18% | 73% |

Cash Return Rate to Investors | 25% (75% Fail) | N/A (Self-Sustaining) |

The implications of this statistical divergence are significant. For many founders, the acquisition of venture capital represents a trade-off where the potential for a massive exit is bought at the cost of a dramatically higher likelihood of total failure. The research suggests that 30% to 40% of venture-backed firms ultimately liquidate their assets, leaving investors and founders with nothing.

The Fund Cycle and the Pressure of Time

Venture capital funds are typically structured as ten-year vehicles. This fixed timeline creates a "ticking clock" that dictates the pace of the companies within the portfolio. Unlike permanent capital or reinvested profits, venture money is "impatient." This structural requirement for liquidity within a specific window forces companies into premature exits or high-risk expansion strategies that may not align with the business's natural development cycle. The need to show progress between fund-raising intervals often leads to "vanity growth"—increases in top-line metrics that mask deteriorating bottom-line health.

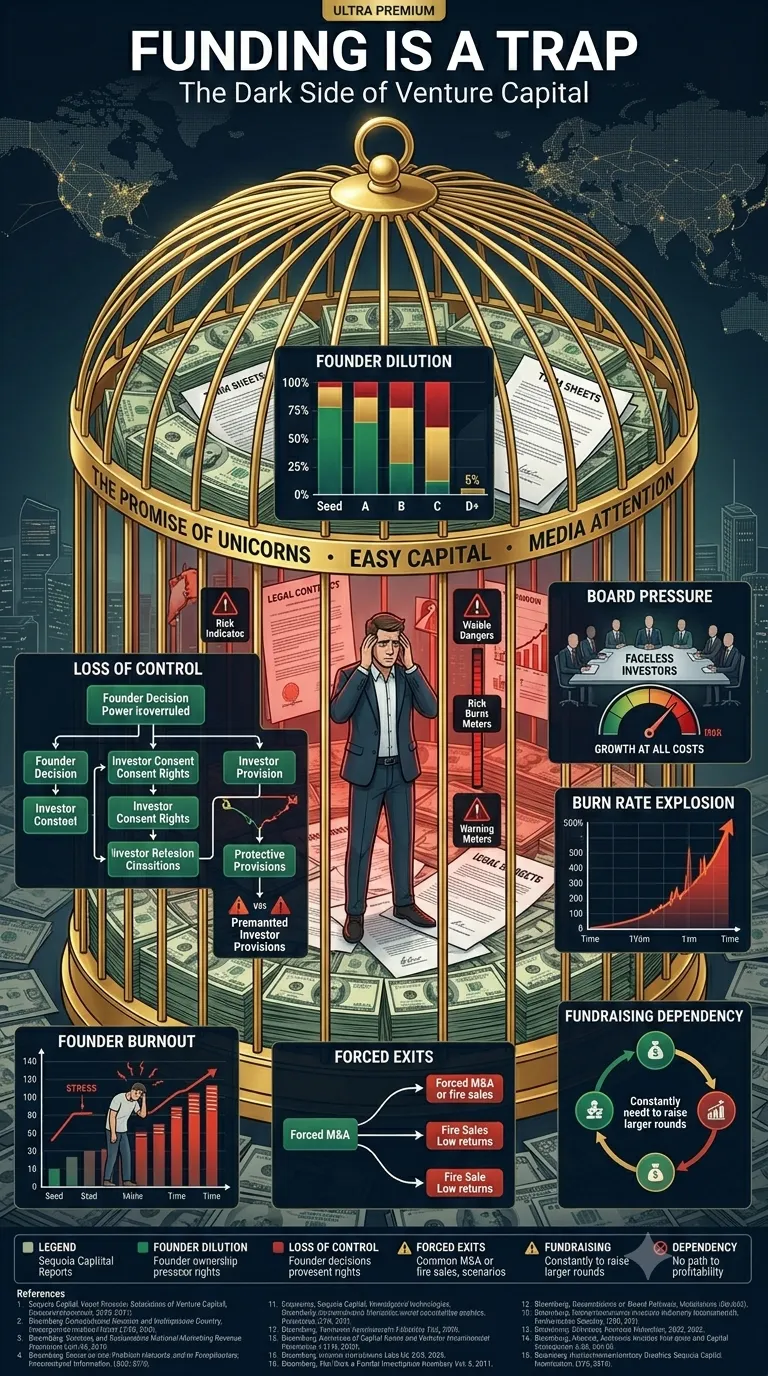

The Economic Architecture of the Trap: Liquidation and Dilution

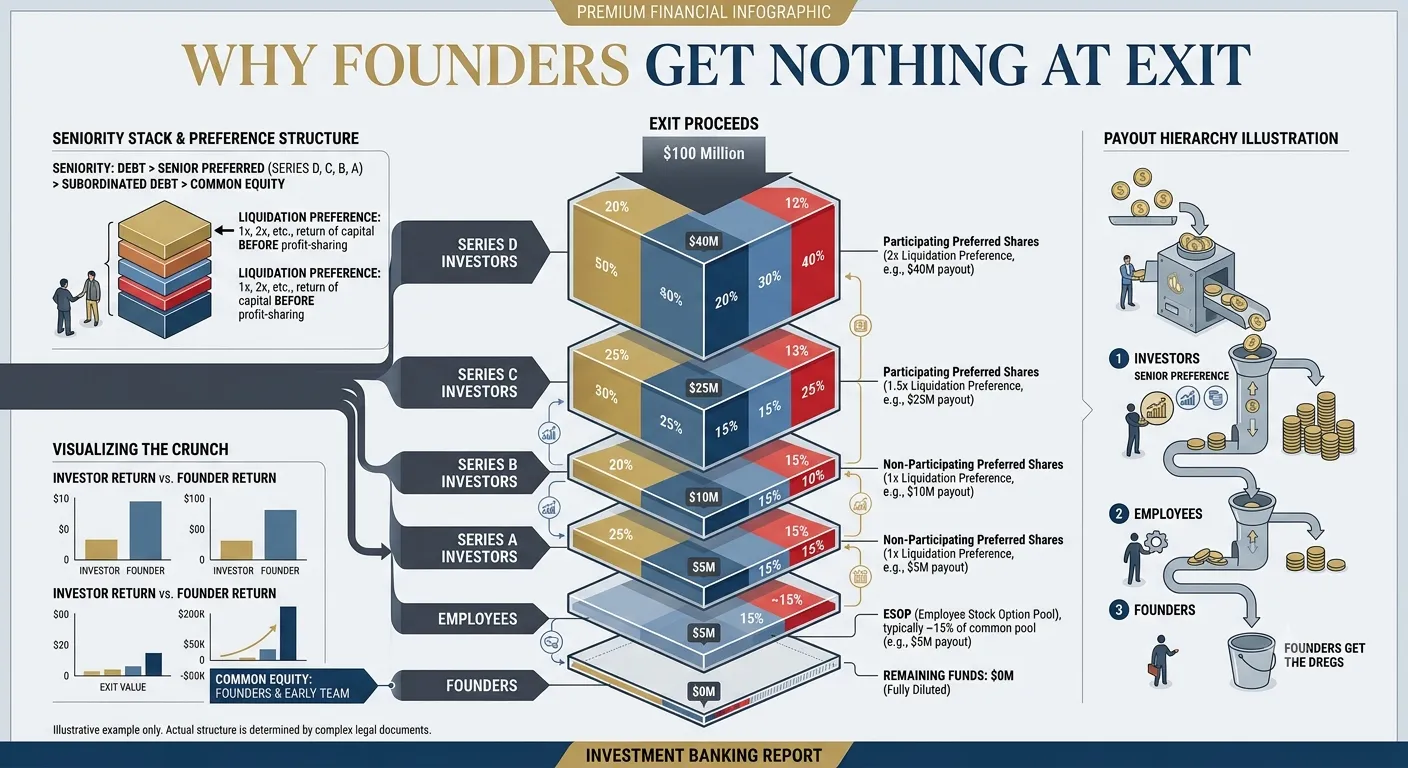

The venture capital "trap" is fundamentally encoded in the legal architecture of the term sheet. While valuation is the most discussed metric during a fundraise, the underlying economic rights—specifically liquidation preferences and participation clauses—often determine the actual distribution of wealth during an exit event.

The Mechanics of Liquidation Preferences

Liquidation preferences act as a form of "investor insurance," ensuring that preferred shareholders recoup their capital before common stockholders (founders and employees) receive any proceeds. In a standard 1x non-participating preference, the investor receives their original investment back or their pro-rata share of the exit, whichever is higher. However, in more aggressive environments or later-stage deals, these preferences can escalate to 2x or 3x, or include participation rights.

Participation rights, often called "double-dipping," allow investors to receive their initial investment back first and then share in the remaining proceeds pro-rata with common shareholders. This can lead to scenarios where an investor with 25% equity captures 40% or more of the exit value.

The Seniority Stack and Stacking Order

The complexity of the "waterfall"—the order in which money is paid out—increases with every subsequent round of funding. Investors in Series B, C, or D rounds often negotiate for "seniority," meaning they are paid before the Series A investors and founders. If a company raises $100 million across several rounds and is sold for $80 million, the senior investors may capture the entire proceeds, leaving the founders and early employees who built the company for years with zero financial return. This "stacking" effect can turn a moderately successful company sale into a personal financial catastrophe for the founding team.

Liquidation Preference Type | Investor Payout Mechanism | Impact on Founder/Common Equity |

Non-Participating (1x) | Higher of: (1) Original investment amount OR (2) Pro-rata share of exit. | Most founder-friendly; protects upside in large exits. |

Participating (Uncapped) | (1) Original investment amount PLUS (2) Pro-rata share of remaining pool. | "Double-dipping"; significantly reduces founder take-home. |

Capped Participating | (1) Original investment PLUS (2) Pro-rata share, up to a set ceiling (e.g., 3x). | Compromise; limits investor "double-dipping" in large exits. |

Multiple Preference (e.g., 2x) | Investor receives 2x their original investment before common. | Highly punitive; can wipe out common equity in mid-tier exits. |

Cumulative Dividends and Anti-Dilution

Other "silent" economic levers include cumulative dividends and anti-dilution provisions. Cumulative dividends accrue over time, effectively increasing the liquidation preference every year the company remains private. For example, a 6% cumulative dividend on a $10 million investment means that after five years, the investor is owed $13 million before founders receive anything.

Anti-dilution provisions, particularly the "full ratchet" variety, protect investors from "down rounds"—fundraising at a lower valuation than the previous round. If a company raises money at a lower price, the full ratchet provision adjusts the investor's previous conversion price to the new, lower price, resulting in massive, retroactive dilution for the founder. While the "weighted average" method is more common and less punitive, anti-dilution mechanisms ensure that the founder carries the vast majority of the risk associated with valuation fluctuations.

The Governance Dilemma: Control and Displacement

Beyond the economics, venture capital fundamentally alters the governance of a company. Founders often face a "control dilemma": the resources they need to scale (capital, expertise, networks) often require them to cede decision-making authority. Research indicates that startups where founders retain absolute control of the board or the CEO position are statistically less valuable than those that embrace shared governance, yet ceding control introduces the risk of founder displacement and strategic drift.

The Hidden Power of Protective Provisions

Protective provisions grant preferred shareholders "negative control"—the ability to veto specific corporate actions even if they do not hold a majority of the board. These provisions typically cover critical decisions such as:

Issuing new shares or incurring significant debt.

Selling the company or changing the business model.

Hiring or firing senior executives or changing the board size.

While these are framed as standard protections for minority investors, they can lead to organizational "gridlock." If an investor's fund cycle requires a liquidity event but the founder wants to keep building, the investor can use their veto power to block necessary bridge financing, effectively forcing a sale.

Board Evolution and the Displacement Threshold

As a company raises more capital, the board of directors typically shifts from a founder-majority to an investor-majority or a "balanced" board with independent directors. Once investors control the majority of board seats, the founder effectively becomes an employee of the board.

Funding Stage | Typical Board Composition | Control Dynamics |

Seed | 2 Founders, 1 Investor | Founder Majority; strategic alignment is usually high. |

Series A/B | 2 Founders, 2 Investors, 1 Independent | Balanced; independent director often holds the swing vote. |

Later Stages | 1-2 Founders, 3+ Investors, 1-2 Independents | Investor Majority; founders can be replaced by professional CEOs. |

Case studies of founder displacement, such as the ousting of Travis Kalanick at Uber or Adam Neumann at WeWork, illustrate how board control can be weaponized during periods of crisis or underperformance. In the Uber case, Benchmark Capital sued Kalanick for fraud, alleging he had manipulated board seats to insulate himself from oversight, highlighting the visceral nature of these power struggles.

Agency Theory and Information Asymmetry

The relationship between venture capitalists (the principals) and founders (the agents) is characterized by high levels of information asymmetry. Founders possess intimate knowledge of the company’s daily operations, while VCs rely on reported data and board-level oversight. According to agency theory, the more money a VC invests, the more control they seek to exert to protect against opportunism.

Imprinting and Strategic Control

The stage at which a VC enters a company significantly impacts their ability to "imprint" their priorities. Early-stage investors often establish working relationships that allow for informal monitoring and alignment. However, later-stage investors, facing greater information gaps, often resort to more rigid contractual controls and monitoring mechanisms. Research suggests that when VCs exert excessive control by limiting managerial discretion, it can actually hurt the company’s long-term performance, particularly its IPO outcome, as the founders' ability to iterate and respond to market shifts is stifled by the need for board-level consensus.

The "Sunk Cost" Trap and Over-Monitoring

As an investment fails to meet milestones, VCs often increase their monitoring frequency, which can inadvertently distract founders from operational recovery. This creates a "vicious cycle" where the pressure to perform for the board leads to short-term decision-making, which further degrades the long-term prospects of the business.

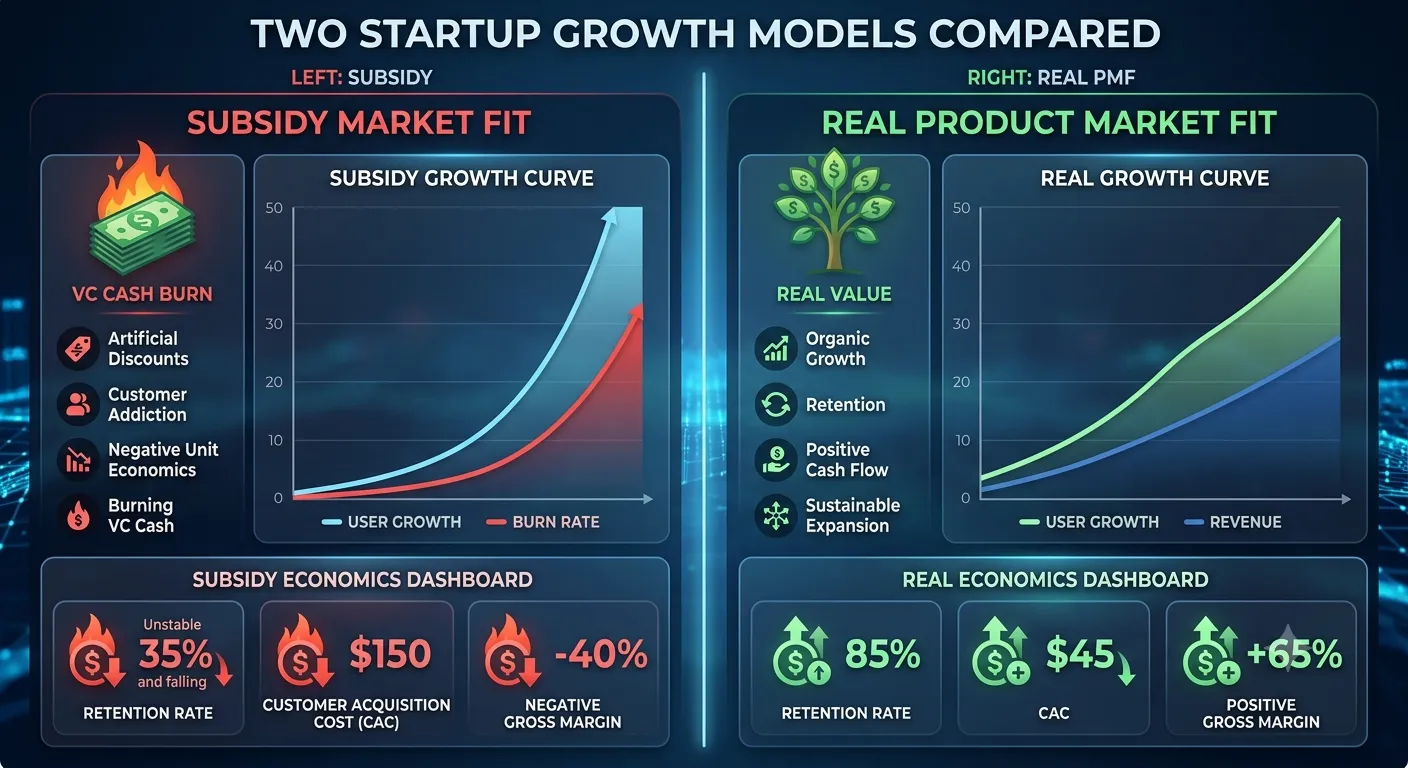

The Growth-at-all-Costs Era and "Subsidy-Market Fit"

For much of the last decade, venture capital operated in an environment of "free capital" driven by low interest rates. This era popularized the "Growth-at-all-Costs" (GAAC) mandate, where companies were encouraged to "blitzscale"—prioritizing speed over efficiency to capture "winner-take-all" markets.

The "Friction Tax" and Operational Implosion

In emerging markets like Latin America, the GAAC model often leads to "operational implosion." Companies attempting to scale rapidly in high-friction environments encounter structural inefficiencies—such as cash-handling costs, fragmented payment rails, and unique fraud patterns—that cannot be solved by software alone. This "Friction Tax" means that as volume increases, costs grow faster than revenue, leading to a negative flywheel where growth actually "breaks the machine".

Subsidy-Market Fit vs. Genuine Product-Market Fit

A primary danger of abundant venture capital is the creation of "subsidy-market fit." This occurs when a company appears to have high demand only because it is using venture capital to subsidize its product's price below the cost of delivery. Consumers become addicted to these subsidized prices, creating an illusion of product-market fit. When the capital stops and the company must raise prices to survive, the demand vanishes. This phenomenon was prevalent in sectors like quick-commerce (e.g., Getir) and ride-hailing, where billions in VC were burned to maintain unsustainable market shares.

Economic Principle | Growth-at-all-Costs (GAAC) | Intelligent Growth |

Unit Economics | Often ignored in favor of top-line growth. | Must be positive or show clear path from day one. |

Profitability | Deferred indefinitely for market share. | Aim for "Default Alive" status as soon as possible. |

Capital Efficiency | Burn-heavy; relies on continuous fundraising. | Frugality; capital used to accelerate proven models. |

Market Approach | "Winner-Take-All" through subsidization. | Own the workflow; focus on Net Revenue Retention. |

The Psychological Burden: The Founder’s "Dark Side"

Entrepreneurship attracts individuals with high levels of energy, imagination, and a need for independence. However, these same traits can have a "dark side." Many founders possess an overriding need for control and a suspicion of authority, which makes the oversight of a VC board particularly galling.

Personality Quirks and Decision-Making Biases

Some entrepreneurs are driven by a need for "applause and recognition," which can jeopardize a company's financial position if they prioritize high-profile marketing or "vanity" metrics over substance. Others scan their environment with a defensive suspicion, anticipating betrayal, which can lead to conflict with co-founders and investors. When these psychological traits meet the high-pressure environment of venture-backed scaling, the result is often a breakdown in leadership efficacy.

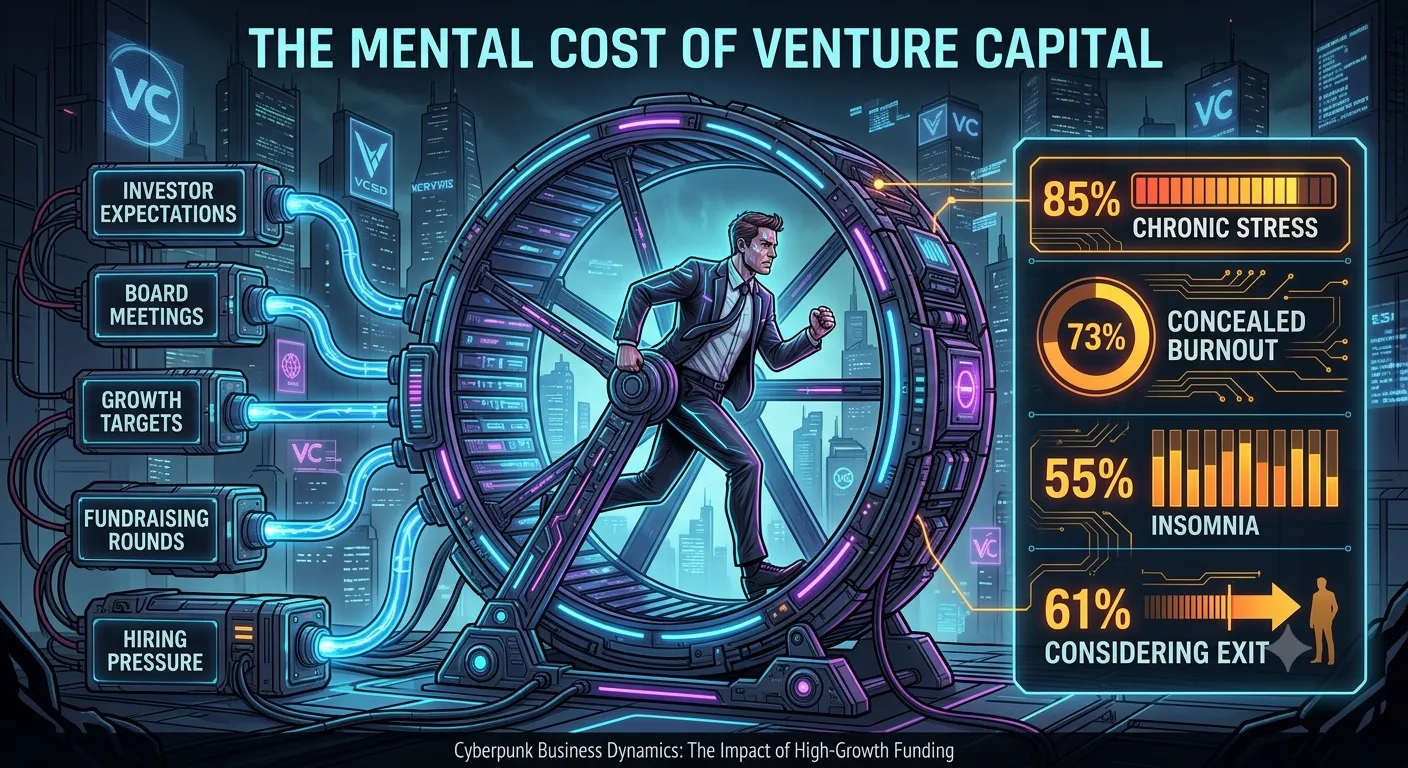

Performance Masking and "Shadow Burnout"

In 2024 and 2025, research increasingly highlighted the mental health crisis within the startup ecosystem. Approximately 76% of founders report that venture capital has negatively impacted their mental health. More critically, 73% of tech founders report "performance masking"—the act of concealing burnout and psychological distress to maintain an image of "strength" for investors and employees.

Founders fear that admitting to mental health struggles will trigger "founder displacement" clauses or a loss of investor confidence. This creates "shadow burnout," where a founder continues to lead while suffering from cognitive impairments, such as "brain fog," impaired executive function, and strategic myopia. Research from Octopus Ventures indicates that 65% of startup failures are rooted in internal conflict or founder burnout, making mental health a primary structural risk for the business.

Mental Health Indicator | Statistic | Impact on Business |

Poor Mental Health | 45% of founders | Increased error rates and financial mistakes. |

Chronic Stress | 85% of founders | Deterioration of team morale and culture. |

Insomnia | 55% of founders | Impaired working memory and decision-making. |

Concealed Burnout | 73% of founders | "Shadow burnout" leading to sudden CEO collapse. |

Contemplating Exit | 61% of founders | Loss of core leadership and institutional knowledge. |

The Demographic Moat: Homophily and Exclusion

The venture capital industry remains one of the most homogenous sectors in finance. This demographic uniformity is not merely a social issue but an economic one, as it leads to "homophily"—the tendency of investors to back founders who share their gender, race, and educational background.

The Myth of the Pipeline Problem

While VCs often cite a lack of qualified women and minority candidates, the data contradicts this. Women represent 40% of top MBA students and a similar percentage of entry-level investment bankers and consultants. However, they represent only 11% of investing partners in VC firms. The exclusionary nature of VC networks means that women and minority founders receive only a tiny fraction (less than 15%) of total venture funding.

This homogeneity creates a "sea of others" for diverse founders, putting them at a psychological and informational disadvantage. The lack of role models and the prevalence of "all-male" boards create a status quo bias that reinforces the "trap" for those outside the traditional Silicon Valley archetype.

Case Studies in Capital Destruction

The failure of venture-backed firms often follows a predictable pattern: over-capitalization, aggressive scaling before product-market fit, and a loss of governance oversight.

The Industrial Failures: Northvolt and Lilium

Sweden's Northvolt, once the beacon of European battery technology, filed for bankruptcy in 2025 despite raising over $15 billion. The failure was attributed to "scaling too quickly" before operations were ready and a complex financing structure that required the approval of 15 different banks for every strategic shift. Similarly, the German electric aircraft startup Lilium filed for bankruptcy after raising over $1 billion, citing a loss of founder control and investor-driven decision-making as key factors in their inability to secure further funding.

The Governance Catastrophes: WeWork and FTX

WeWork’s collapse from a $47 billion valuation to bankruptcy highlights the "dark side" of founder-controlled entities that lack board oversight. SoftBank’s willingness to provide Neumann with multi-class voting rights effectively immunized him from the board, allowing for billions in value destruction through self-dealing and eccentric management. In the case of FTX, a total lack of corporate governance and regulatory compliance led to a $1.8 billion loss of investor capital, demonstrating that even sophisticated VCs can be blinded by the "unicorn" hype.

Unit Economic Failures: Getir and Byju’s

Getir’s retreat from 9 countries after burning $1.8 billion proved that "ultrafast delivery" was technically possible but economically impossible at scale. Similarly, the Indian edtech giant Byju’s fell from a $22 billion valuation to near-zero due to unsustainable growth mandates and governance failures, underscoring the "trap" of raising too much capital at over-inflated valuations.

Company | Capital Raised | Peak Valuation | Primary Cause of Failure |

Northvolt | $15B+ | $12B+ | Over-scaling; operational complexity. |

WeWork | $11.5B | $47B | Governance failure; unit economics. |

Getir | $1.8B | $11.8B | Unsustainable GAAC model. |

Lilium | $1B+ | $3.3B | Fundraising deadlock; loss of control. |

Byju's | $5.5B | $22B | Unsustainable growth; governance. |

Alternative Pathways: Reclaiming Sovereignty

The realization that venture capital is often a "trap" has led many founders to explore alternative funding models that prioritize long-term independence and sustainable profitability.

Bootstrapping and Self-Financing

Bootstrapping allows founders to retain 100% control and ownership, growing the business at the pace of its revenue. While growth may be slower, bootstrapped firms are far more resilient, with a 35-40% survival rate compared to the 10-15% of VC-backed firms. Successful examples like GitHub and Spanx demonstrate that massive scale can be achieved without early venture dilution.

Revenue-Based Financing (RBF)

RBF is a non-dilutive alternative where investors provide capital in exchange for a percentage of future monthly revenue until a "cap" (e.g., 1.5x the investment) is reached. This model is particularly attractive for SaaS and e-commerce businesses because it does not require giving up board seats or equity. If revenue drops, the monthly payment drops, providing the company with operational flexibility that traditional debt does not offer.

Venture Debt

Venture debt is typically used by venture-backed startups to extend their "runway" between equity rounds. It is less dilutive than equity but more dangerous, as it requires regular interest and principal repayments. If a company misses its revenue targets, the debt-holder can take control of the company's assets or force a bankruptcy.

The Zebra Movement: Profit and Purpose

The "Zebra" startup movement is a direct response to the "Unicorn" culture. Zebra companies are "real" (not mythical), focus on "both black and white" (profit and purpose), and prioritize "stamina" over "blitzscaling". Zebras often use community funding or RBF to maintain their independence and solve real-world problems without the pressure of a ten-year fund exit cycle.

Funding Alternative | Primary Advantage | Primary Disadvantage |

Bootstrapping | 100% Ownership & Control | Growth speed limited by revenue. |

Revenue-Based Financing | Non-dilutive; flexible payments | Requires consistent revenue (> $10k/mo). |

Venture Debt | Extends runway without dilution | Repayment obligation; risk of default. |

Equity Crowdfunding | Diverse supporter base; early validation | Complex legal/compliance overhead. |

Synthesis and Strategic Outlook

The structural "trap" of venture capital exists because of a fundamental misalignment between the needs of a ten-year venture fund and the needs of a sustainable, long-term business. The venture model is designed to maximize "outlier" returns at the expense of the "average" portfolio company. For the founder, this means that the moment they sign a term sheet, they are no longer building a company for its own sake, but rather a financial asset for a fund's specific timeline.

To navigate this landscape, founders must develop "growth intuition"—the ability to recognize when to accelerate and when to consolidate, regardless of board pressure. This requires building "guardrails" around unit economics, team quality, and personal well-being. Furthermore, the industry requires a shift toward "intelligent growth," where capital is viewed as a tool for scale rather than a substitute for a viable business model.

The dark side of venture capital—the dilution, the loss of control, the psychological erosion, and the systemic exclusion—is not an accidental byproduct but a core feature of the current model. Founders who enter this system without a deep understanding of its legal and psychological mechanics are not merely raising capital; they are entering a high-stakes gamble where the odds are systematically stacked against them. Reclaiming entrepreneurship from the "trap" of venture capital requires a return to economic physics: where revenue exceeds costs, growth compounds rather than consumes, and the founder's vision remains the primary engine of value.

Protect Your Future: The Precision Vesting Calculator

Don't let a "handshake deal" complicate your exit. Map out your ownership journey with our Vesting Calculator

Calculate Your Vesting Schedule →