D2C brands: Still worth it or already saturated?

June 27, 2026 by Harshit Gupta

The global retail landscape in 2026 presents a fundamental contradiction: while the direct-to-consumer (D2C) model is experiencing record-breaking total transaction volumes, the early-stage "disruptor" playbook has reached a state of terminal saturation. The inquiry into whether D2C brands remain a viable investment or a saturated relic requires a departure from binary conclusions. Instead, the analysis reveals a structural transformation from the venture-subsidized growth of the 2010s toward a mature, hyper-efficient era defined by "Profitable Resilience". As the global D2C market approaches a staggering valuation of $900 billion, the distinction between high-performing entities and those facing obsolescence is no longer determined by the ability to build a digital storefront, but by the mastery of complex unit economics, agentic commerce protocols, and omnichannel agility.

Global Market Architecture and the 2026 Growth Trajectory

The quantitative health of the D2C sector remains robust when viewed through the lens of total addressable market expansion. The global D2C market size has reached $28.06 billion in 2025 and is projected to scale to $55.72 billion by 2030, representing a consistent compound annual growth rate (CAGR) of 14.7% to 14.9%. However, broader definitions that include the integration of direct sales within established ecommerce ecosystems suggest the market is nearing $900 billion globally, with over 64% of consumers worldwide now expressing a preference for buying directly from brands to ensure a superior experience.

In the United States, D2C ecommerce sales are forecast at $239.75 billion for 2026, accounting for 19.2% of total retail ecommerce. This signifies a stabilization of market share; while the "gold rush" era of triple-digit growth has concluded, D2C has successfully embedded itself as a permanent pillar of the retail infrastructure. The plateauing of market share at approximately 19% through 2028 indicates that the model is no longer in a phase of cannibalizing traditional retail, but is instead optimizing for sustainable capture within its established territory.

Regional D2C Market Metrics (2025-2026) | Market Share / Value | Forecast Growth Rate (CAGR) | Dominant Drivers |

North America | >38.5% Global Share | 12.4% | Advanced logistics; high tech-literacy |

Asia-Pacific | Fastest Growing Region | 18.2% | Social commerce; mobile-first adoption |

Europe | Second Highest Performance | 13.1% | Sustainability; UK/Germany digital adoption |

India | $29.27 Billion (Social) | 37.5% | Quick commerce; WhatsApp ecosystems |

The geographic divergence in 2026 is critical for strategic planning. While North America remains the revenue powerhouse, holding the largest regional share, the Asia-Pacific region has emerged as the primary laboratory for D2C innovation. China, in particular, has pioneered "super app" integrations and livestream shopping models that have become the global standard for high-conversion engagement. Meanwhile, India’s D2C market is on a trajectory toward $200 billion, fueled by a social commerce explosion that is projected to grow from $29 billion in 2025 to over $143 billion by 2030. This regional shift underscores that the D2C model is not saturating globally at a uniform rate; rather, the "saturation" is a localized phenomenon in Western markets where traditional paid media channels have become prohibitively expensive.

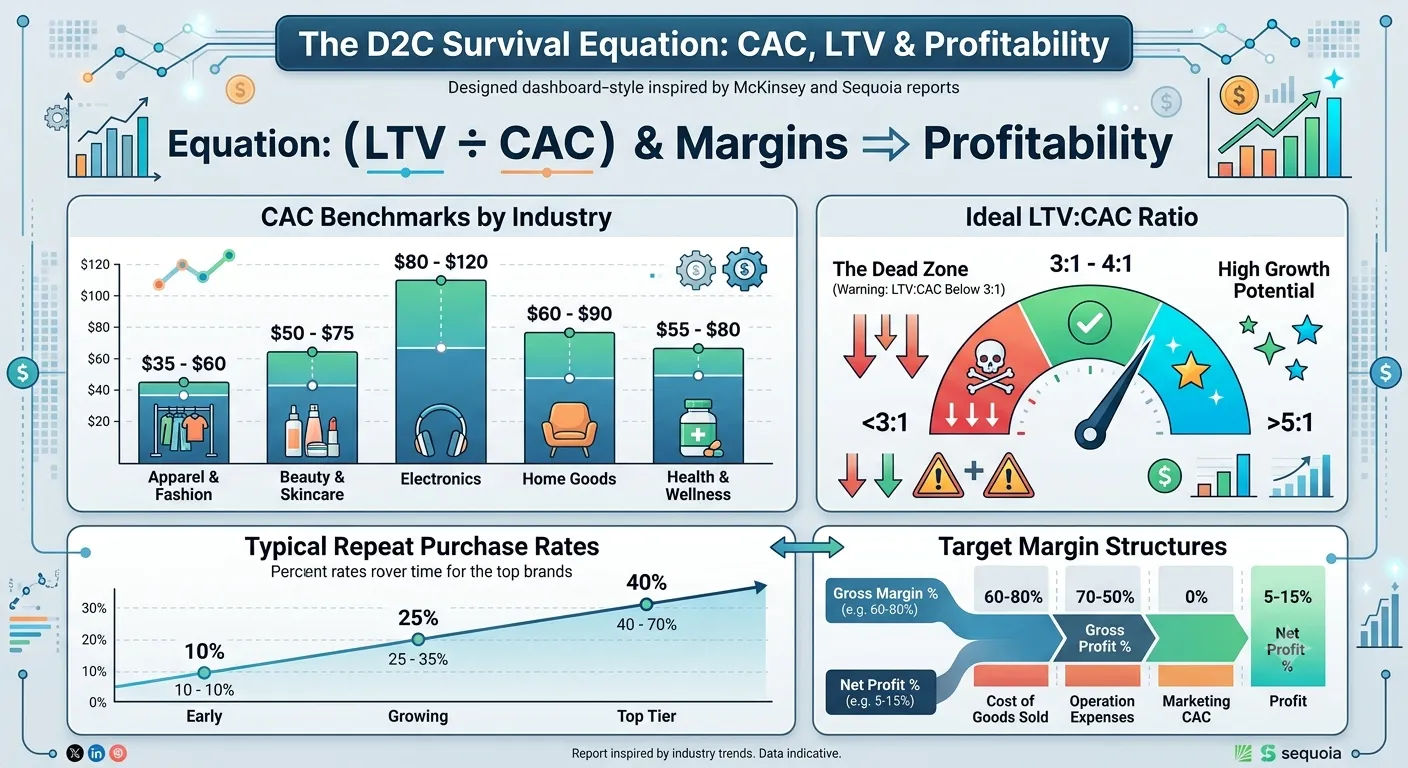

The Unit Economic Arbiter: CAC, LTV, and the Profitability Mandate

The most aggressive headwind facing the D2C model in 2026 is the erosion of contribution margins. The historical advantage of bypassing intermediaries—which traditionally offered a 30% to 50% higher profit margin—is being systematically dismantled by escalating customer acquisition costs (CAC) and operational overheads. Paid media CAC for D2C brands has risen by roughly 40% to 60% between 2023 and 2025, driven by platform saturation on Meta and Google, the permanent loss of third-party tracking signals, and a "creative fatigue" cycle that requires a constant, expensive stream of new content.

Category-Specific Acquisition Benchmarks

The viability of a D2C brand in 2026 is often determined by its vertical, as the cost to acquire a customer varies significantly based on purchase frequency and average order value (AOV). For example, luxury goods face the steepest acquisition costs, averaging $175 per customer, while food and beverage brands maintain the most efficient acquisition profiles at $45 to $53.

D2C Industry Segment | Average CAC (2026) | Viable LTV:CAC Ratio | Target Repeat Purchase Rate |

Food & Beverage | $15−$53 | 4:1 | 40%−60% |

Beauty & Personal Care | $$25 - $130 | 3:1 | 45%−60% |

Apparel & Fashion | $$40 - $120 | 3:1 | 25%−40% |

Consumer Electronics | $$76 - $150 | 3:1 | 15%−25% |

Jewelry & Luxury | $$120 - $400 | 5:1 | 10%−20% |

High-performing brands have adapted by prioritizing the "Golden Ratio" of 3:1 for lifetime value (LTV) to CAC. Organizations with an LTV:CAC ratio below 3:1 are increasingly finding themselves in a "dead zone," where the cost of replacing churned customers exceeds the profit generated from their initial purchase. This is particularly evident in the mid-market segment ( $10 million to $50 million revenue), where fixed costs often rise faster than revenue, compressing EBITDA margins to a narrow 7% to 8%.

The Margin Compression Crisis

Beyond marketing spend, margin compression is being driven by a "vicious cycle" of pricing complexity and operational leakage. Tariffs introduced in 2025 have already pushed retail prices of imported goods up by 5.4%, with only one-fifth of the total cost burden reached consumers so far, meaning brands are largely absorbing these costs upstream. Simultaneously, the pressure to offer free shipping and deep discounts to compete with Amazon's logistics machine has turned shipping and returns into significant revenue eroders. Successful operators in 2026 have abandoned "lazy discounting" as an acquisition lever, instead using it exclusively to convert "fence-sitters" who have already expressed high intent.

Technological Transformation: Agentic Commerce and the AI Discovery Layer

The most disruptive force in the 2026 D2C ecosystem is the transition from traditional search to "agentic commerce". AI agents are no longer passive tools; they are autonomous entities capable of executing complex shopping assignments, synthesizing reviews, and making purchase decisions on behalf of consumers. It is estimated that agentic commerce will reach $1 trillion in the U.S. retail market by 2030, with 40% of enterprise applications in 2026 already powered by AI agents.

The Rise of Answer Engine Optimization (AEO)

As discovery moves from Google Search to LLM platforms like ChatGPT and Perplexity, D2C brands are facing a "Zero-Click Shopping" reality. Over 60% of Gen Z and Millennials now report that AI tools influence their final purchase decisions. This shift necessitates a move from traditional Search Engine Optimization (SEO) to Generative Engine Optimization (GEO).

AI Discovery Metric (2026) | Performance Value | Context / Implication |

LLM-Referred Traffic Conversion | 2.47% | 4th highest acquisition channel; beats Meta/Google |

AI-Assisted Conversion Lift | 76x (TikTok/Reels) | Visitors engaging with AI assistants show massive ROI |

Branded AI Sales Growth | 32% Faster | Brands with native agents outperform platform-only brands |

AI-Mediated US Retail (2030) | $$190B - $$385B | Projected value of autonomous AI transactions |

The data indicates that visitors who arrive from high-velocity channels like TikTok and then interact with an on-site AI shopping assistant convert at 76 times the rate of those who do not engage. This suggests that "worth it" in 2026 is defined by a brand’s ability to integrate into the AI stack. Brands are increasingly standardizing their product data and taxonomies to ensure that AI agents can accurately ingest and recommend their catalog. Stripe and Google have even introduced agentic commerce protocols—the Agentic Commerce Protocol (ACP) and Universal Commerce Protocol (UCP)—to provide the infrastructure for these autonomous transactions.

The Attribution Gap and Agentic Resistance

However, this technological leap creates a widening "attribution blind spot". When an AI agent shortlists a product hours before a consumer completes a branded search, traditional analytics fail to capture the upstream influence of the AI. Only 16% of brands currently have any form of AI search tracking in place, leaving a significant portion of their "organic" revenue misunderstood. Furthermore, a counter-movement known as the "Human Premium" is emerging; 82% of consumers still prefer human interaction for customer service, and brands that overtly signal human judgment and authenticity—such as Hermès’ hand-drawn digital interface—are gaining a competitive edge against "AI slop".

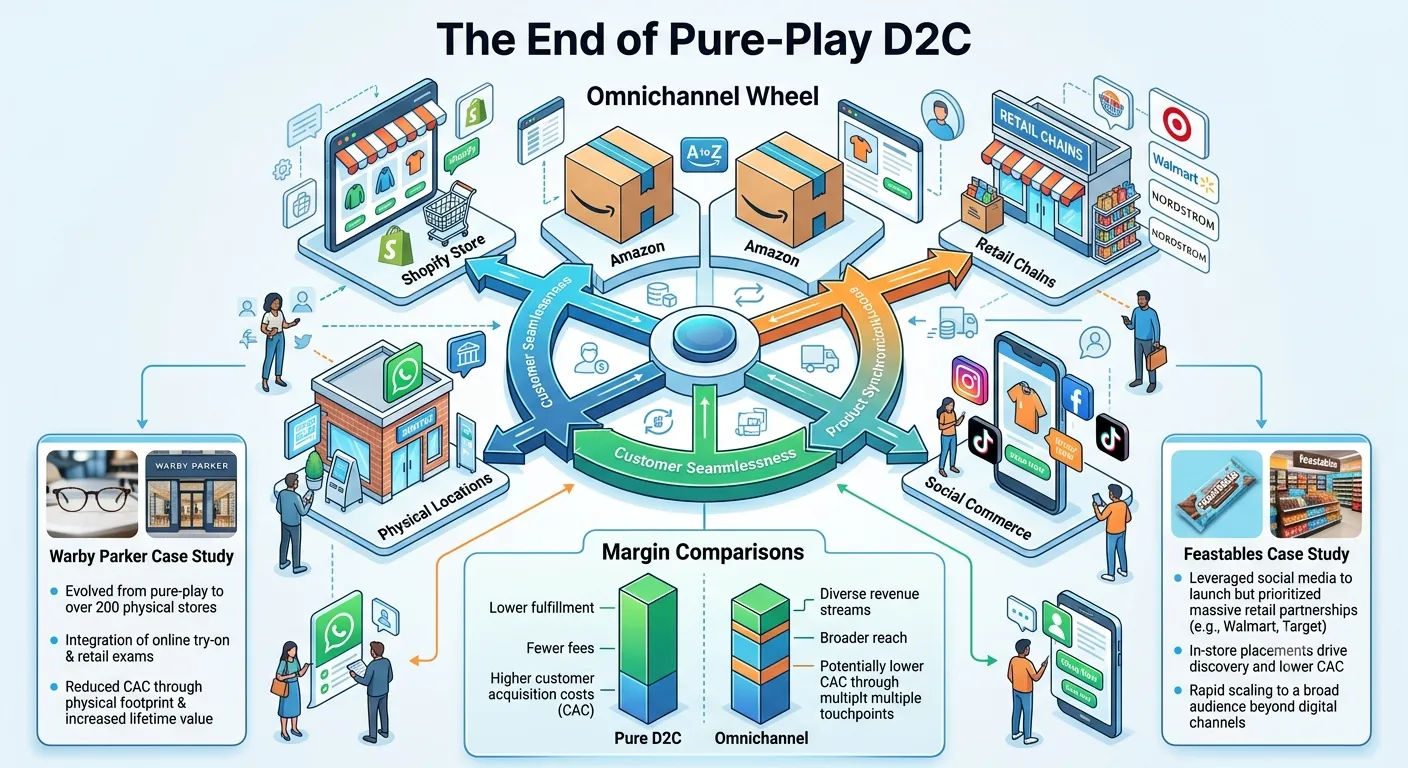

Omnichannel Evolution: The Death of the Pure-Play Model

The most definitive evidence of D2C saturation lies in the collapse of the "pure-play" digital model. In 2026, the industry has shifted toward "Channel Agnosticism," where D2C is viewed as a single, high-margin channel within a broader ecosystem that must include physical retail, marketplaces, and wholesale partnerships to achieve scale.

The Hybrid Growth Framework

The "Warby Parker effect" describes the mandatory transition for digital-native brands into physical spaces. Warby Parker's expansion to over 300 retail stores and its shop-in-shops within Target have created "accretive" revenue streams that digital channels alone could not match. Similarly, brands like Glossier and Feastables have pivoted to hybrid models, with Feastables scaling from a digital experiment into a powerhouse through partnerships with Walmart and Target.

Channel Profitability Matrix (2026) | Gross Margin Range | Operational Complexity | Customer Data Ownership |

Owned D2C Site (Shopify) | 55%−70% | High (Traffic & Ops) | Full |

Amazon / Marketplaces | 20%−30% | Medium (Platform Fees) | Limited |

Wholesale / Retail | 30%−45% | Low (B2B Logistics) | Minimal |

Social Commerce | 45%−60% | High (Creative Velocity) | Partial |

Marketplaces like Amazon, despite their high commissions (10% to 20%), remain attractive because their CAC is often 30% to 50% lower than that of independent traffic generation. The consensus among 2026 strategists is that a healthy D2C brand should aim for 60% to 80% of volume on owned channels to protect margins, while using marketplaces for demand generation and discovery.

Unified Inventory and Logistics Excellence

Operational efficiency has replaced marketing flair as the primary differentiator for D2C brands. The rise of quick commerce has shifted consumer expectations toward same-day delivery, with 77% of shoppers now expecting fulfillment within two hours in urban centers. To meet this, brands are adopting "Unified Inventory" systems that synchronize stock across marketplaces, websites, and physical dark stores. Warehouse automation has moved from experimental to mainstream, with AI-led slotting and barcode-driven picking reducing operational costs by 30% and boosting picking speed by up to 60%.

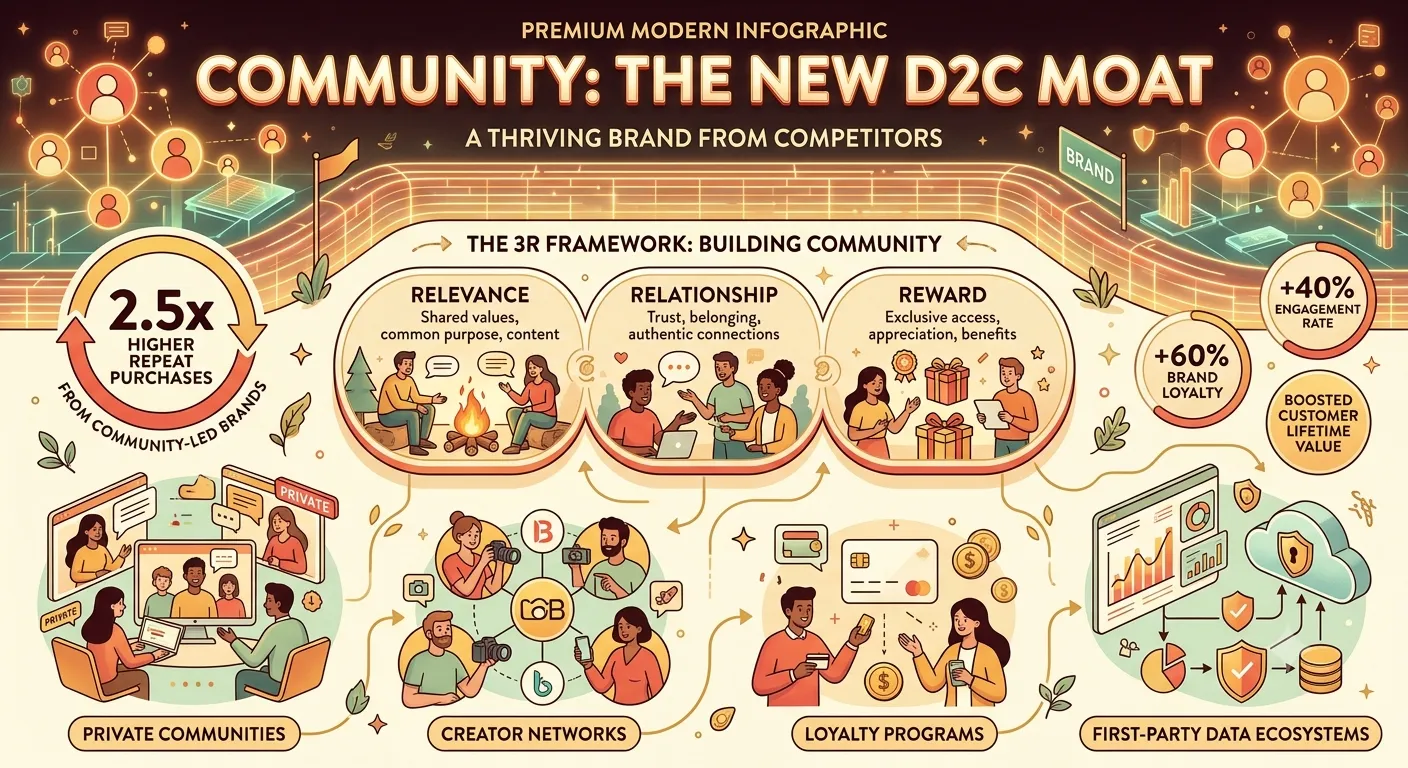

Community-Led Growth and the First-Party Data Fortress

As the "algorithmic tax" on paid social platforms continues to rise, successful D2C brands are shifting their focus from "demand capture" to "community-led growth". In 2026, a brand’s community is considered a competitive moat because, unlike a product or a pricing strategy, a community cannot be easily copied.

The 3R Retention Framework

The "3R" model—Relevance, Relationship, and Reward—has become the standard for preventing the 12-to-18-month growth plateau that kills most D2C startups.

Relevance: Leveraging AI for hyper-personalization, where content and offers adjust instantly based on real-time behavioral signals.

Relationship: Building micro-communities through owned media, such as private WhatsApp groups or exclusive member forums, which have been shown to drive 2.5 times higher repeat purchase rates.

Reward: Implementing emotional loyalty programs that focus on exclusive access and brand advocacy rather than just transactional discounts.

First-Party Data as Infrastructure

With the disappearance of third-party cookies, first-party data has evolved from a reporting tool into a core growth asset. Brands that treat this data as infrastructure—activating behavioral signals in real-time to adapt individual customer journeys—are building more durable growth. For instance, fitness brands are successfully exchanging "Zero-party data" (such as diet quizzes) for email and SMS opt-ins, allowing them to generate over 30% of total revenue through owned channels within months.

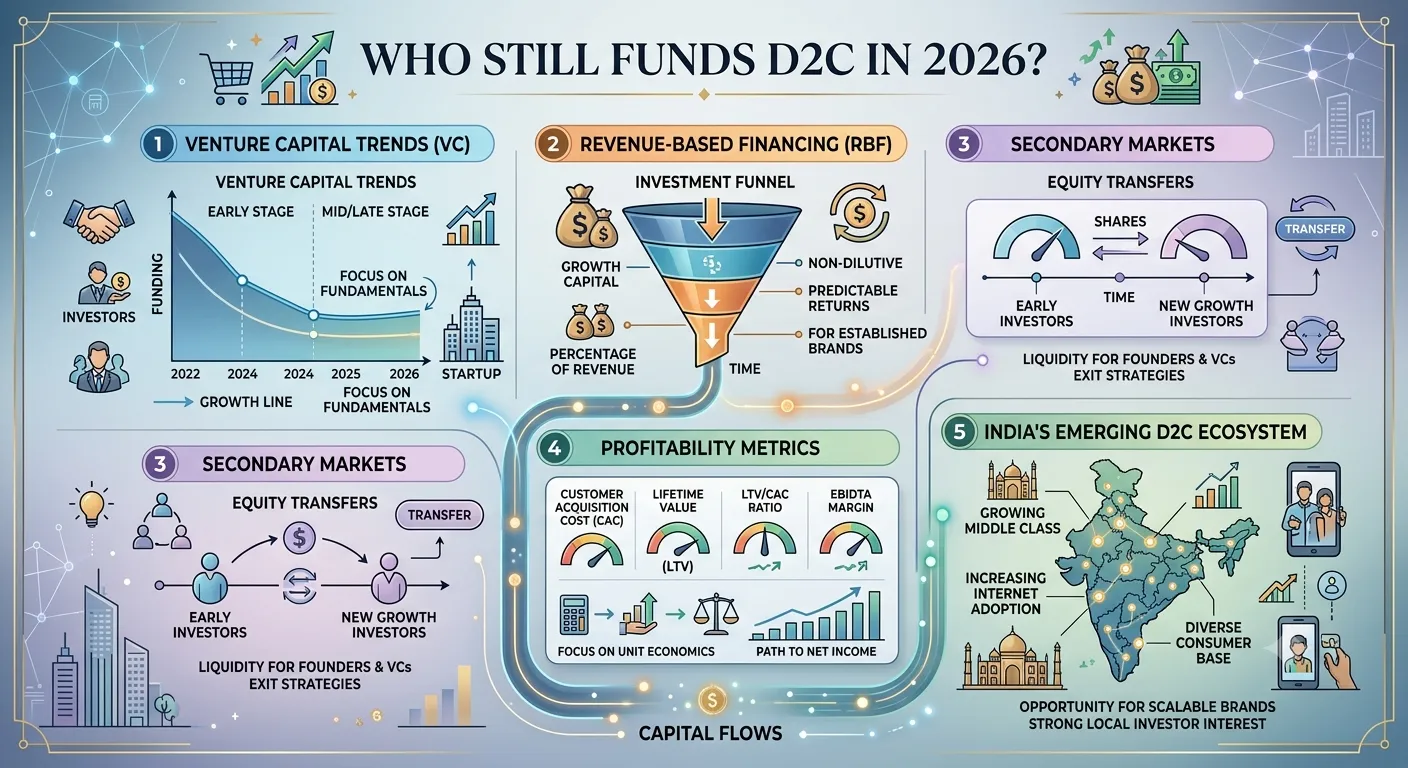

The Investment Landscape: Selective Capital and the Indian D2C Boom

The venture capital (VC) market for D2C brands in 2026 is characterized by extreme selectivity. While total VC funding accelerated to approximately $141 billion in late 2025, investors have largely moved away from the "growth at any cost" model. Capital is now concentrated in brands with clear category leadership, high repeat consumption, and a proven path to profitability.

Alternative Financing and the Exit Paradox

Revenue-Based Financing (RBF) has become a primary catalyst for D2C expansion, particularly for brands generating over $100,000 in monthly revenue. This model allows founders to scale without equity dilution, aligning investor returns directly with business performance.

Funding Type (2025-2026) | Typical Check Size | Investor Sentiment | Key Requirement |

Seed Stage | $3M (Avg) | Cautiously Robust | Clear PMF; unit economic proof |

Late Stage / Pre-IPO | $$19.5M - $$450M | Highly Selective | 30%+ growth; positive Rule of 40 |

Revenue-Based | $$500K - $$5M | Expanding | Monthly revenue >$100K |

Secondary Markets | $210B (Global) | Surging | Liquidity needs for early investors |

Sources:

India has emerged as the global leader for D2C capital deployment outside the U.S. In 2025, several Indian brands, such as the quick-commerce giant Zepto and the fashion brand Snitch, raised large institutional rounds despite the broader "funding winter". These brands are successful because they control their entire vertical stack—from supply chain and logistics to customer data—commanding premium valuations that pure-play marketplaces no longer receive.

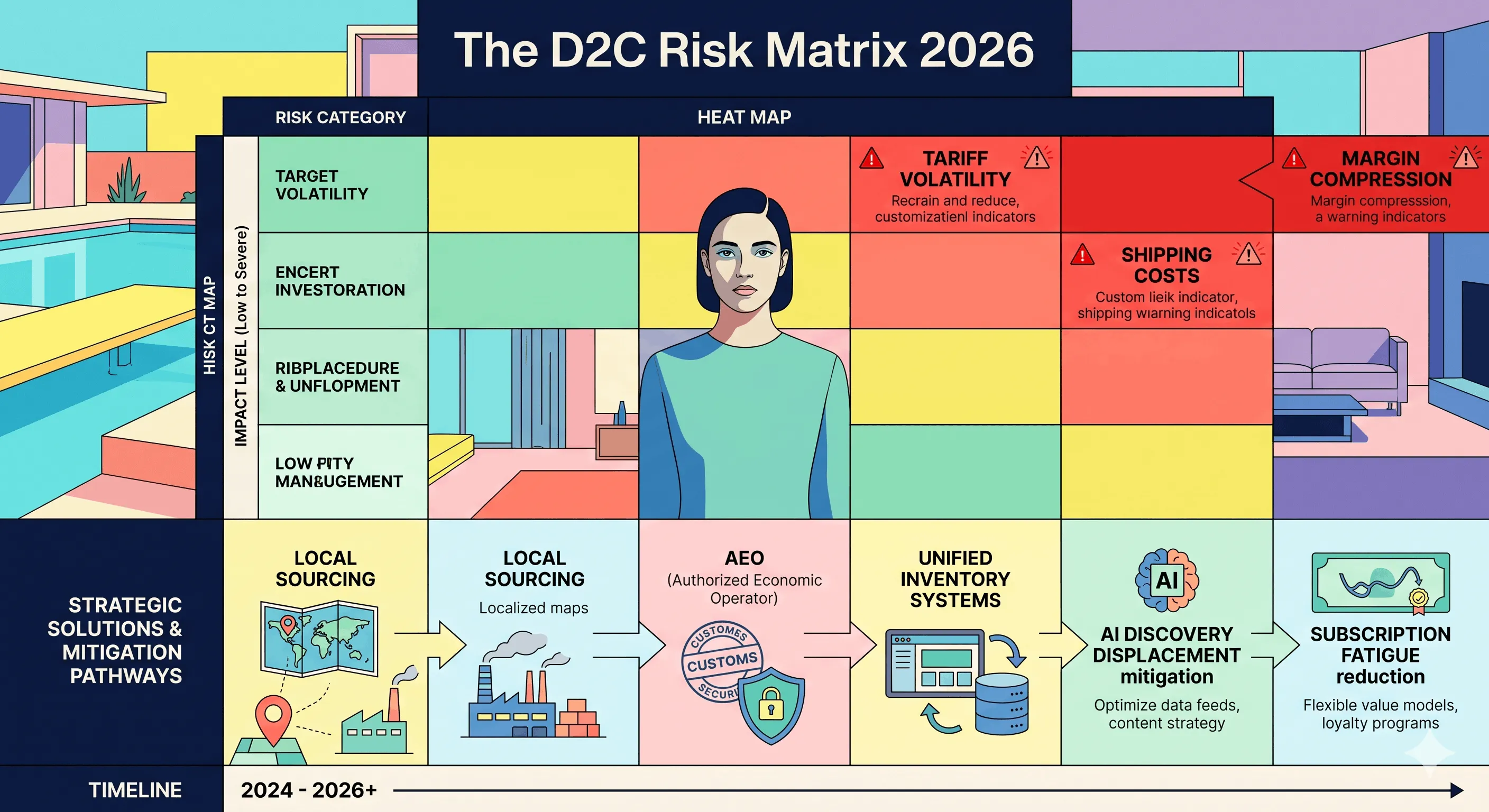

Barriers to Entry, Risks, and the "Dead Zone" of 2026

The threshold for a new D2C brand to become "worth it" in 2026 has never been higher. The industry faces an "affordability crisis," with lean tech startups facing baseline operational expenses of approximately $45,000 per month. The "talent problem" is equally severe; the skillset required to run a profitable D2C operation now spans paid media, unit economics, supply chain, and data analysis—a combination of skills that is both rare and expensive.

Regulatory and Macroeconomic Pressures

The 2025 tariff increases remain a dominant design constraint for 2026 operating models. Brands must now map tariff exposure across all products and monitor cost drift with high frequency, as price increases in exposed categories like household furnishings and electronics can rise by 20% within six months. Additionally, the rise of "Digital Product Passports" in Europe is forcing brands to invest heavily in supply chain transparency, which is becoming a mandatory requirement for market access.

Critical Risks for D2C in 2026 | Probability | Economic Impact | Strategic Mitigation |

Margin Compression (Shipping/Fees) | High | 5%−15% Net | Unified inventory; local sourcing |

AI Discovery Displacement | Medium | 10%−20% Traffic | Answer Engine Optimization (AEO) |

Tariff Volatility | High | 5%−20% Price | Sourcing diversification |

Subscription Fatigue / Churn | Medium | 20%−30% LTV | Relationship-based retention (3R) |

Sources:

Case Studies in Brand Failure and Lessons Learned

The 2025-2026 cycle has seen several high-profile marketing blunders that highlight the risks of modern D2C. Coca-Cola's over-reliance on AI-produced holiday campaigns and American Eagle’s "Sydney Sweeney" tagline debacle demonstrate that modern consumers have a "finely tuned BS detector". Tesla’s market share decline to 38% in the U.S. serves as a warning that narrative momentum cannot compensate for operational and market realities indefinitely. The lesson for 2026 is clear: brilliant marketing can drive the first purchase, but if the product, price, or cultural alignment fails, the model collapses.

Synthesis: The "10x Founder" and the Future of D2C

The final analysis suggests that D2C brands are not "saturated," but they have entered their smartest and most demanding era. Success in 2026 is reserved for the "10x founder"—leaders who use AI tools to accelerate learning and execution while maintaining a "human premium" in their brand storytelling.

To remain "worth it," a D2C brand must transcend the transaction. It must operate with:

Real-time data intelligence to manage fragmented shopper journeys.

Omnichannel architecture that treats the digital storefront as just one of many experiential touchpoints.

Defensive distribution strategies that prioritize owned email and SMS lists to protect against algorithm volatility.

The brands that will lead the next decade are those that recognize D2C is not a business model in itself, but a capability for building deep, data-rich relationships in a world increasingly dominated by autonomous agents and anonymous marketplaces. The future belongs to those who combine technology with humanity, trust with transparency, and commerce with community.

Want to calculate the equity for your cofounder?

Nail your cap table before you sign. Whether you're splitting equity with a co-founder or planning your next funding round, our Equity Calculator gives you precision in seconds

Equity calculator →