Building a Startup in Belgium vs Neighboring Countries

March 14, 2026 by Harshit Gupta

The European entrepreneurial landscape in 2025 and 2026 is characterized by a mature but highly fragmented competitive environment. For founders evaluating the optimal geography for a new venture, the choice between Belgium and its immediate neighbors—France, Germany, the Netherlands, and Luxembourg—is no longer merely a question of corporate tax rates. Instead, it involves a complex analysis of administrative velocity, labor market flexibility, venture capital density, and the long-term sustainability of innovation-based fiscal incentives. As of late 2025, the broader European Union has demonstrated a marginal decline in innovation performance of 0.4 percentage points, yet the core Western European nations continue to lead as Innovation Leaders and Strong Innovators. Within this context, Belgium stands as a resilient but complex hub, growing at 1.5% in 2023 and exceeding the euro area's stagnant average, while simultaneously facing critical labor shortages that threaten to constrain future expansion.

Administrative Foundations and Incorporation Velocity

The initial hurdle for any founder is the speed and cost of incorporation. The European Union has made significant strides in harmonizing company law, but national variances in notary requirements and capital mandates create distinct entry profiles. France and the Netherlands have prioritized speed, whereas Germany and Belgium maintain more rigorous, albeit modernized, oversight frameworks.

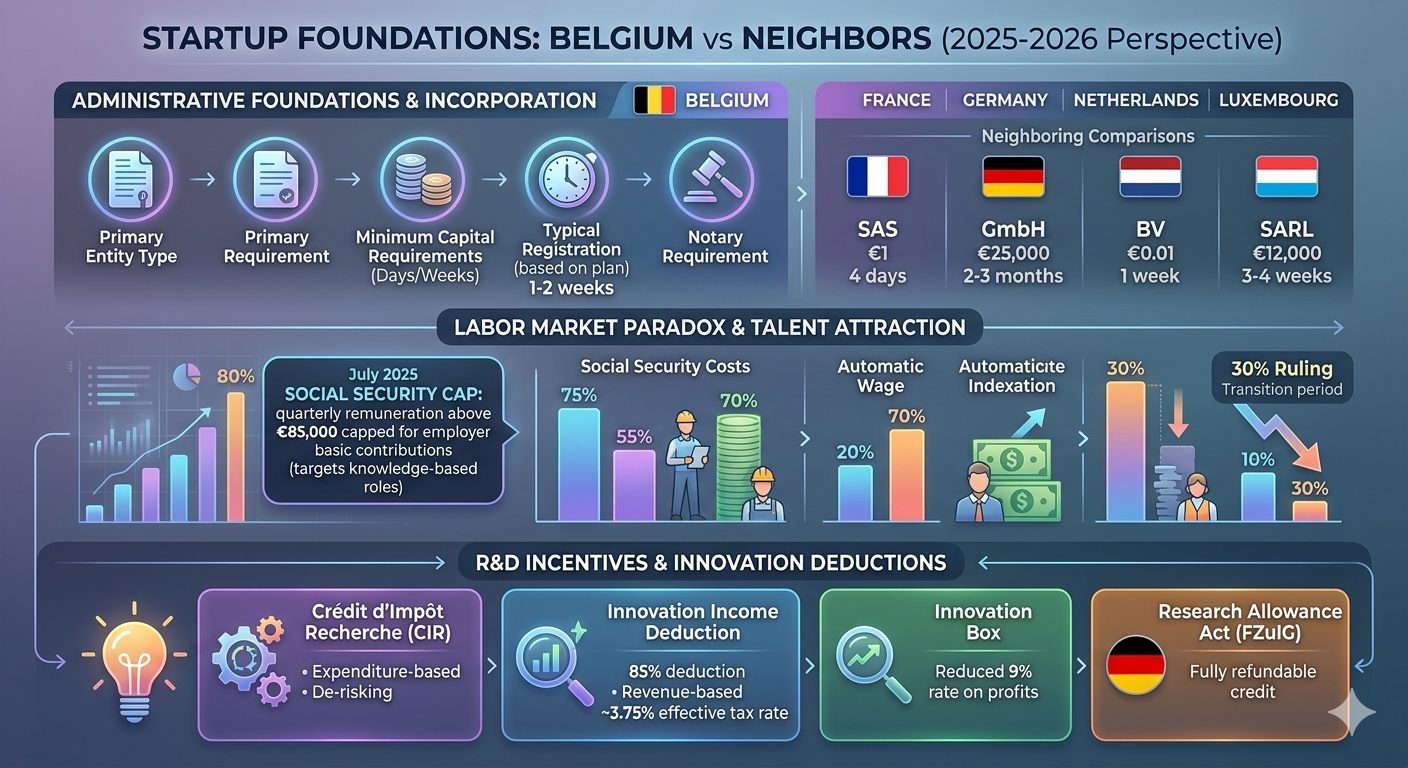

The Belgian Paradigm: From Capital to Viability

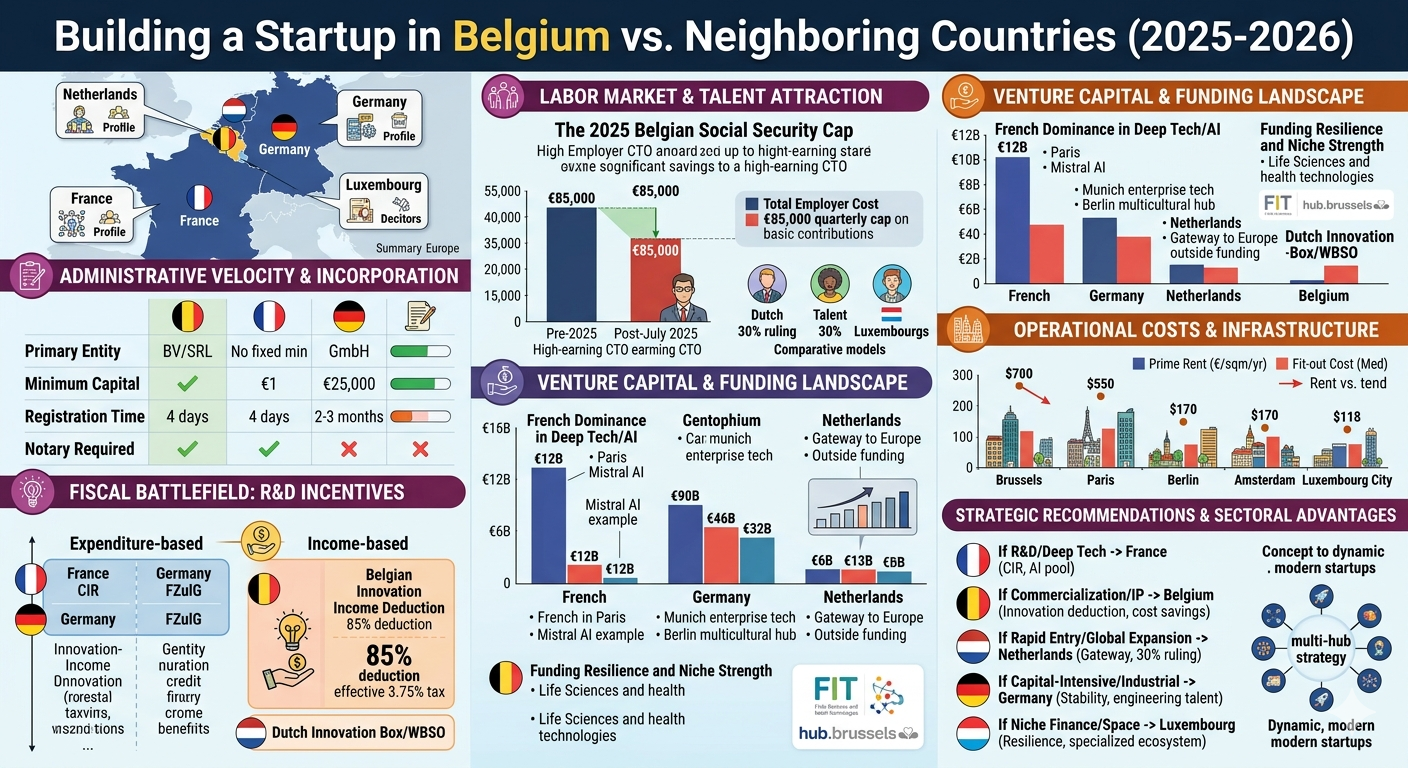

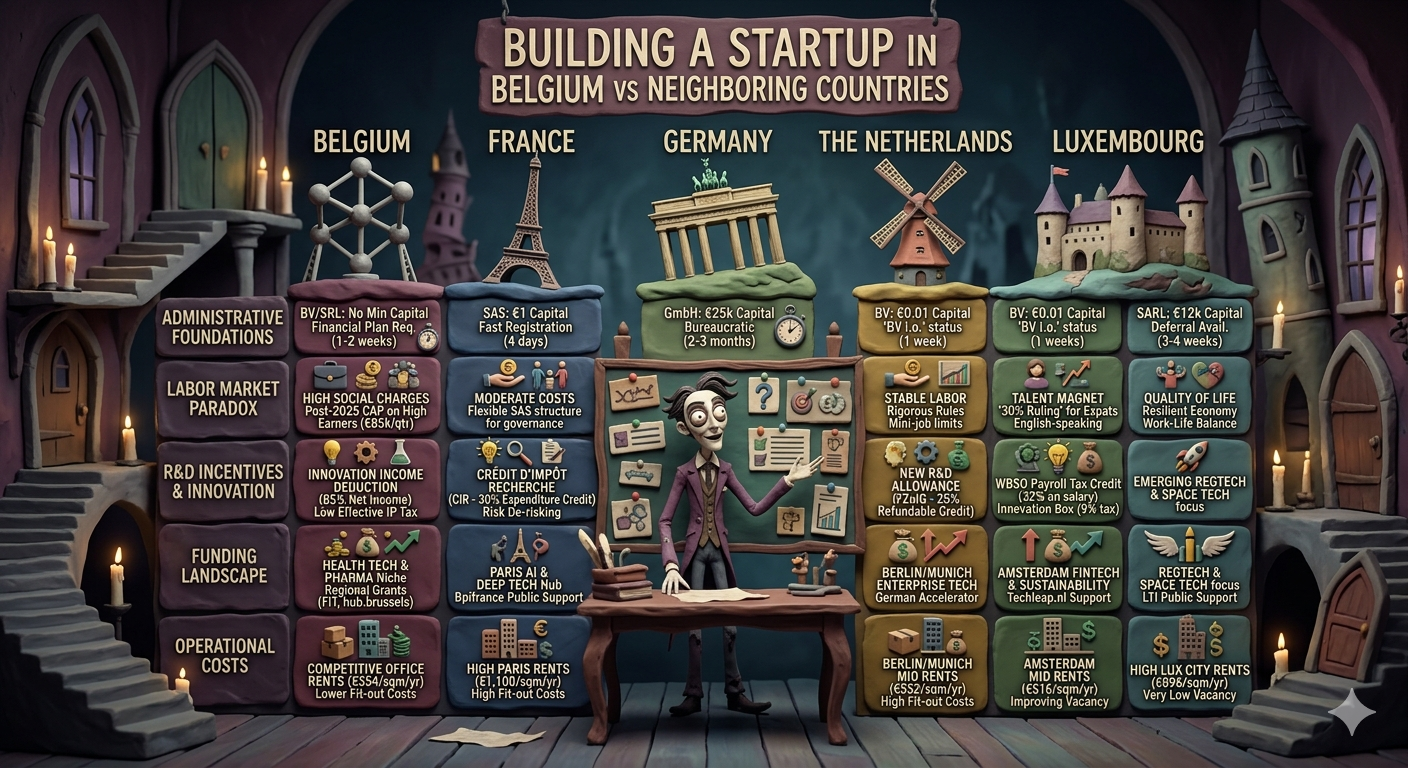

Belgium’s 2019 reform of the Code of Companies and Associations remains the definitive structure for current formations. The Private Limited Company (BV/SRL) has emerged as the standard vehicle for startups due to its lack of a fixed statutory minimum capital requirement. However, this flexibility is counterbalanced by the requirement for a "sufficient" financial plan. Founders must demonstrate that the venture possesses enough equity to sustain operations for at least two years, a document that must be filed with a notary during the mandatory deed of incorporation process. This shift necessitates early-stage fiscal discipline but adds a layer of professional cost and time that more streamlined jurisdictions avoid. For larger ventures or those seeking public listing, the Public Limited Company (NV/SA) remains the primary option, requiring a minimum capital of €61,500, which must be fully subscribed at the time of incorporation.

Neighboring Comparisons in Legal Velocity

France offers a stark contrast in administrative speed. A French startup can often be registered in as little as four working days, provided the founders are legal residents. The Simplified Joint-Stock Company (SAS) has become the go-to structure for investor-backed companies because of its governance flexibility, allowing shareholders to define management and voting rights in the bylaws rather than following rigid statutory defaults. In the Netherlands, the Private Limited Company (BV) can be started with a capital deposit of just €0.01, and the "BV in oprichting" (BV i.o.) status allows entrepreneurs to trade while the incorporation is still being finalized.

Germany, while globally respected for its industrial stability, remains the most bureaucratically demanding jurisdiction. The standard GmbH requires a €25,000 capital commitment, with at least 50% paid upfront. The Unternehmergesellschaft (UG), or "mini-GmbH," provides a lower-capital alternative starting at €1, but it mandates the retention of 25% of annual profits until the €25,000 threshold for a full GmbH is reached. The registration timeline in Germany frequently extends to two or three months, significantly longer than its peers.

Country | Primary Entity | Minimum Capital | Registration Time | Notary Required |

Belgium | BV / SRL | No fixed min; based on plan | 1-2 weeks | Yes |

France | SAS | €1 | 4 working days | No (usually) |

Germany | GmbH | €25,000 | 2-3 months | Yes |

Netherlands | BV | €0.01 | 1 week | Yes |

Luxembourg | SARL | €12,000 (deferral avail.) | 3-4 weeks | Yes |

Luxembourg has recently modernized its SARL framework to remain competitive. As of December 2025, a new draft bill allows for a 12-month deferral of the €12,000 minimum capital requirement for cash contributions, aiming to synchronize the jurisdiction with the faster timelines seen in France and Belgium. The SARL-S (Simplified SARL) remains an option for individual entrepreneurs with a capital requirement of only €1, though it is restricted to natural persons.

The Labor Market Paradox: Talent and Social Charges

The most significant operational differentiator for startups in 2025 and 2026 is the management of human capital and the associated social security burden. Belgium has historically been perceived as a high-cost labor market, but recent 2025 reforms have introduced a strategic advantage for high-growth tech firms.

The 2025 Belgian Social Security Cap

Effective July 1, 2025, the Belgian government introduced a quarterly remuneration cap of €85,000 for calculating employer social security contributions. Previously, employer contributions—which average approximately 25-28%—were uncapped, making high-earning experts in AI, biotechnology, and fintech prohibitively expensive. Under the new regime, basic employer contributions are not due on the portion of an employee's salary that exceeds this €85,000 quarterly threshold.

This reform specifically targets "knowledge-based roles" and is intended to attract global talent by reducing the cost of high-earning individuals. For a startup employing a Chief Technology Officer with an annual salary of €400,000 (€100,000 per quarter), the saving is substantial. While other smaller contributions totaling approximately 3% remain payable on the full salary, the basic 25% charge is capped, providing a significant reduction in the total cost of employment compared to the pre-2025 era.

Salary Component (Quarterly) | Belgian System (Pre-2025) | Belgian System (Post-July 2025) |

Gross Salary | €100,000 | €100,000 |

Employer SS (Basic ~25%) | €25,000 | €21,250 (25% on first €85k) |

Other Employer SS (~3%) | €3,000 | €3,000 |

Total Employer Cost | €128,000 | €124,250 |

This fiscal strategy acknowledges the tightening of the Belgian labor market. With unemployment at 5.6% and a demographic trend showing a stagnant working-age population after 2024, the ability to compete for the world’s top engineers is paramount. However, founders must also account for Belgium’s automatic wage indexation, which protects employee purchasing power but can lead to sudden, inflation-driven increases in a startup's burn rate.

Comparative Talent Attraction: The Dutch and Luxembourg Models

The Netherlands continues to use the "30% ruling" as its primary talent magnet. This allows employers to pay 30% of an employee’s salary as a tax-free allowance for five years. However, 2025-2026 marks a transition period for this incentive. The tax-free percentage is scheduled to decrease to 27% by 2027, and a salary cap based on the public sector maximum (approximately €262,000) will apply to all holders by 2026. Despite these restrictions, the Netherlands remains highly attractive due to near-universal English proficiency and a startup visa that is among the easiest to obtain in the European Union.

Luxembourg, meanwhile, has been ranked 2nd globally for talent competitiveness and 2nd for work-life balance. Its strategy relies on a high-quality lifestyle and a powerful passport to attract international professionals. In Germany, the labor market remains resilient with a statutory minimum wage of €12.82 as of January 2025, and employer social security contributions of roughly 22.5%. Germany’s challenge remains the "mini-job" limit and the relative rigidity of hiring and firing rules compared to the more flexible Dutch or French environments.

Venture Capital and the Funding Landscape

The funding environment for 2025 and 2026 shows a stabilization of venture capital activity, though it remains far below the 2021 peak. Total European startup funding reached approximately $51 billion in 2024, with a notable shift toward larger, late-stage rounds and AI-focused investments.

The French Dominance in Deep Tech and AI

France has emerged as the most dynamic hub for venture capital in continental Europe. Paris alone attracted over €12 billion in 2024, with AI startups like Mistral AI raising massive rounds (e.g., €1.7 billion Series C in 2025). The French ecosystem is supported by Bpifrance, which acts as a powerful public champion for tech entrepreneurship. France's ability to recycle capital from successful first-generation exits, such as Datadog and Mistral AI, has created a virtuous cycle of reinvestment.

The German and Dutch Funding Vectors

Germany remains a close second to France in terms of total funding value, particularly in deep tech and biotech. In 2025, Germany is expected to regain its position as the second-largest VC hub by deal value, surpassing France due to consistent momentum in earlier-stage rounds. Cities like Munich have become the undisputed centers for enterprise technology and automotive software, while Berlin continues to attract a multicultural founder base.

The Netherlands punches above its weight, with Amsterdam ranking as a top-five European hub. Its funding is concentrated in fintech, logistics, and sustainability, benefiting from its role as a "Gateway to Europe". Dutch startups are also increasingly drawing capital from Asia and North America, with 32% of total European fundraising coming from outside the continent.

Belgium’s Funding Resilience and Niche Strength

Belgium, while having a smaller total funding volume, is on track for a drop in deal value in late 2025, yet it maintains strong sector-specific performance in health technologies and pharmaceuticals. The Belgian investment climate is characterized by significant FDI flows (USD 23 billion in 2023) and a highly developed financial sector that supports life sciences and ICT. Regional agencies like Flanders Investment & Trade (FIT) and hub.brussels provide essential grants and R&D subsidies that complement private venture capital.

Ecosystem Dimension | Belgium | France | Germany | Netherlands | Luxembourg |

VC Hub Status | Strong Niche | Continent Leader | Established Tier 1 | Logistics/Fintech | Emerging Specialist |

Primary VC City | Brussels | Paris | Berlin / Munich | Amsterdam | Luxembourg City |

AI / Deep Tech | Life Sciences | AI / LLMs | Enterprise / Auto | Sustainability | Space / Regtech |

Public Support | Regional Grants | Bpifrance | HTGF / EXIST | LTI |

The Fiscal Battlefield: R&D Incentives and Innovation Deductions

For many founders, the net cost of R&D is the deciding factor in location choice. Europe offers some of the world's most generous R&D tax incentives, but they vary significantly in their mechanism (expenditure-based vs. income-based).

France and the CIR Advantage

The Crédit d'Impôt Recherche (CIR) in France is a cornerstone of the European innovation economy. It allows companies to recover 30% of their R&D expenditures up to €100 million. This expenditure-based credit effectively de-risks the early years of a startup's life when profits are non-existent. However, the French tax authorities are known for rigorous and frequent audits, and the actual refund process can be slow.

Belgium and the Netherlands: The Income-Based Approach

Belgium and the Netherlands offer powerful incentives for companies that have reached the commercialization stage. The Belgian Innovation Income Deduction allows for an 85% deduction of net innovation income from the taxable base, leading to an effective corporate tax rate of approximately 3.75% for qualifying Intellectual Property (IP). This makes Belgium one of the most attractive locations in the world for an IP-rich company once it begins generating revenue.

The Dutch Innovation Box provides a similar benefit, taxing qualifying R&D profits at a reduced rate of 9% instead of the regular 25.8%. The Netherlands also uses the WBSO program to provide a payroll tax credit on R&D wages (32% on the first €350,000), making it more of an operational subsidy than a back-end tax break.

Germany’s New Competitive Edge

Until recently, Germany lacked a significant R&D tax credit. The Research Allowance Act (FZulG) now provides a 35% credit for SMEs and 25% for large firms on R&D wages and contract research. A critical advantage of the German system is that it is fully refundable; companies without tax liability receive the credit as a cash payment, providing essential liquidity to early-stage startups.

R&D Incentive | France (CIR) | Germany (FZulG) | Netherlands (WBSO) | Belgium (Innovation) |

Subsidy Type | Tax Credit | Refundable Credit | Payroll Offset | Income Deduction |

Rate (approx.) | 30% | 25-35% | 32% (on salary) | 85% (of income) |

Effective Benefit | Expenditure-based | Expenditure-based | Expenditure-based | Revenue-based |

Max Benefit | €100M threshold | €3.5M cap (SMEs) | Tiered system | Uncapped |

Operational Costs and Infrastructure

While digital infrastructure is high across all five countries, physical office space and fit-out costs remain a major component of a startup's burn rate. In 2025, prime office rents have continued to rise across most European cities due to a shortage of "Grade A" ESG-compliant buildings.

Real Estate Concentration and Decentralization

Paris remains the most expensive hub in the region, with prime office rents in the Central Business District (CBD) reaching €1,100 per square meter per year in late 2025. This reflects the extreme concentration of the French ecosystem. In contrast, Brussels offers the most competitive rents among the neighboring hubs at €354 per square meter, making it a highly cost-effective base for startups that require a central European presence but wish to minimize occupancy costs.

Luxembourg City, despite its small size, is the second most expensive market at €696 per square meter, driven by its status as a global financial center. Germany and the Netherlands occupy the middle ground, with Berlin at €552 and Amsterdam at €516.

Fit-Out and Operating Expenditures

Fit-out costs have also seen significant year-on-year increases. For a medium-standard office fit-out in 2025, a startup can expect to pay approximately €2,333 per square meter in Berlin and €1,661 in Brussels. These costs, combined with utilities and mandatory insurance, mean that a typical German GmbH needs to reserve at least 20% of its revenue for operational expenses.

City | Prime Rent (€/sqm/yr) | Rent Trend (2025) | Fit-out Cost (Med) | Vacancy Rate |

Brussels | €354 | Stable | €1,661 | 7.8% (4% CBD) |

Paris | €1,100 | +4% | €1,161 | Low (Supply gap) |

Berlin | €552 | Stable | €2,333 | Stable |

Amsterdam | €516 | +4% | €1,250 | Improving |

Luxembourg | €696 | +4% | No data | Very Low |

Brussels stands out for its low CBD vacancy rate of 4%, which is primarily driven by the "replacement" of obsolete buildings with new, green buildings favored by European institutions and the private sector. Startups looking for space in Brussels must compete with the public sector, which accounts for approximately 31% of total office take-up.

Quality of Life and Ecosystem Resilience

The long-term success of a startup hub depends on its ability to withstand economic shocks—a metric where Luxembourg and the Netherlands lead. Luxembourg retains its place as the 2nd most resilient economy in the world in 2025, according to the FM Global Resilience Index.

Work-Life Balance and Founder Satisfaction

The Netherlands and Luxembourg are frequently named among the world's best countries for work-life balance, with the Dutch valuing personal flexibility and the Luxembourgers ranking 2nd globally in 2025. This culture of flexibility is not just a lifestyle benefit; it leads to a more productive and satisfied workforce, which is critical for the intense early years of a startup.

Germany also ranks high for quality of life, offering a world-class healthcare system and public transport that acts as a major draw for international talent. France’s "old-world charm" in Paris is balanced by high costs and complex labor rules, though the "French innovation centers" provide a supportive community that is both competitive and collaborative.

Sectoral Advantages: Where to Build What

A founder’s decision should ultimately be guided by their specific sector, as each jurisdiction has developed distinct "superclusters" supported by targeted regulations and academic infrastructure.

Biotechnology and Life Sciences: Belgium and Germany

Belgium is a global leader in life sciences, particularly in pharmaceuticals and health technology. The proximity to world-renowned research centers and a highly educated workforce makes it the primary hub for companies in this space. Germany is also a strong contender, with Munich serving as the hub for deep tech and Tubulis raising one of the largest biotech rounds of 2025.

Artificial Intelligence and Software: France and Germany

France is the undisputed leader in European AI as of 2025. The success of Mistral AI and the championing of tech entrepreneurship by the national government have made Paris the top destination for software founders. Germany remains the preferred choice for enterprise software and automotive technology, benefiting from proximity to corporate giants like SAP and Volkswagen.

Fintech and Logistics: The Netherlands and Luxembourg

The Netherlands is the ideal base for fintech and logistics, leveraging Amsterdam’s financial history and the port of Rotterdam’s logistical dominance. Luxembourg is a specialized alternative, offering a "European passport" for financial services and a burgeoning space technology sector (SpaceResources.lu).

Space Technology and Regtech: Luxembourg

Luxembourg has successfully carved out a niche in space technology and regulatory technology (Regtech). Its status as a Tier 1 global financial hub makes it an ideal testing ground for startups that need to navigate complex EU financial regulations.

Synthesis: Strategic Recommendations for the 2026 Founder

For the entrepreneur building a startup in Western Europe in 2026, the choice of jurisdiction depends on the phase of the company and its core value driver.

If the primary goal is Research and Development (R&D) with heavy upfront technical costs and no immediate profit, France is the logical choice. The 30% CIR credit and the density of the Paris AI community provide a safety net and a talent pool that is unmatched in the region.

If the focus is on commercialization and IP protection, Belgium offers the most significant fiscal advantage. The 85% innovation deduction, combined with the 2025 social security cap for high earners, allows a company to scale its workforce and protect its margins far more effectively than in France or Germany.

If the strategy is rapid market entry and global expansion, the Netherlands provides the most frictionless environment. The speed of incorporation, the 30% ruling for talent, and the universal use of English make it the easiest "Gateway to Europe."

If the venture is a capital-intensive industrial project, Germany remains the anchor. While the bureaucracy is slow, the industrial depth and the quality of the engineering talent pool in Munich and Berlin provide a stability that is highly valued by late-stage investors and corporate partners.

Finally, for niche, high-value financial or space ventures, Luxembourg offers a specialized, highly resilient ecosystem with a work-life balance that helps in retaining top-tier international executives.

The 2026 founder is increasingly likely to follow a "multi-hub" strategy: incorporating in the Netherlands or Luxembourg for legal and fiscal efficiency, while maintaining an R&D lab in Belgium or France to capture subsidies, and sales teams in Germany to access the continent’s largest domestic market. This geographic arbitrage is the hallmark of the sophisticated European startup in the post-2025 era.